Business

Micron Technology Will Hit Jackpot With This New Product (NASDAQ:MU)

Welcome to Cash Flow Venue, where dividends do the heavy lifting! Blending my financial chops with the timeless wisdom of value investing (and love for steady income), I’ve built a rock-solid pillar in my financial foundation through dividend investing. I believe it’s one of the most accessible paths to achieving financial freedom, and I’m excited to share my insights with you. I’m a finance professional with deep experience in M&A and business valuation. What does that mean in practice? I’ve evaluated countless businesses and played key roles in sell-side and buy-side transactions, guiding clients through the complexities of buying and selling companies. In my day-to-day work, I dive into financial modelling, conduct commercial and financial due diligence to assess a company’s health, negotiate deal terms, and, of course, attend way too many meetings 🙂 My focus spans sectors like tech, real estate, software, finance, and consumer staples – industries I’ve spent years advising and now invest in personally. Today, they make up the core of my portfolio and coverage on this platform. My motivation for writing on Seeking Alpha comes from a desire to not only deepen my own knowledge but also to share value with others who are on a similar path. Dividend investing has played a key role in my financial journey, and I believe it’s one of the most straightforward and accessible ways for anyone to work towards financial freedom. By sharing my insights and experiences, I hope to demystify the process, making it more approachable for those looking to build long-term wealth. Ultimately, my goal is to help facilitate OUR journey to financial freedom, learning and growing together as we navigate the world of dividend investing.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of MU, AMD, NVDA, AMZN, MSFT, META either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

The information, opinions, and thoughts included in this article do not constitute an investment recommendation or any form of investment advice.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Pongsak Sapakdee/iStock via Getty Images

Working with AI, Thinking with Discipline

AI, in its current form, has now been with us for three full years. Since we first felt the shockwaves from the ChatGPT 3.5 launch on November 30, 2022, we have been tinkering with and using LLMs. We have found these models helpful for questions large and small, and LLMs certainly helped create efficiencies in approaching our process, but we had not yet systematically integrated AI into our research process. As the tools evolved, we believed it was necessary to both experiment and formalize where AI adds value, and where it does not. On this journey, Elliot and his co-host John Mihaljevic recorded a fascinating podcast with Samir Patel of Askeladden Capital. Samir has been incredibly thoughtful in developing and articulating the way he has infused his process with AI. 1 2

Below, we outline where AI has been most helpful in our process and where we believe we can improve its use. Before doing so, it is worth framing the kind of value we are actually seeing in practice. Much of the current discourse centers on the displacement of knowledge workers, a narrative we believe is often overstated. While there are certain industries where headcounts will change due to AI, we are believers in the Kasparov Law (or Kasparov Principle). As phrased by the Chess Grandmaster, Garry Kasparov, the Kasparov Law holds that “weak human + machine + superior process beats stronger humans and machines with inferior processes.” 3 4 Kasparov conceived of this notion in the aftermath of his loss to Deep Blue, a supercomputer designed for chess mastery, upon seeing amateurs with rudimentary chess programs beat Deep Blue-style supercomputers.

Put simply, these systems are best viewed as force multipliers for human judgment, not replacements of it. These use-cases range from powerful time savers to idea generators to risk profilers and risk management. In our own practice, we think we are in the early innings of deploying AI and we are intent on understanding how we can benefit from these systems as early and as quickly as possible. AI becomes materially more powerful when the user understands its systematic strengths and limitations, and learns how to prompt it effectively.

One limitation we are quite cognizant of is the fact that AI systems are programmed for “agreeableness” and in many of our use-cases we are looking for the opposite—we actively use AI to challenge our assumptions and surface flaws in our reasoning. One limitation we remain highly aware of is that most AI systems are optimized for agreeableness rather than adversarial critique. They’re helpful, polite, and affirming, often to the point of avoiding confrontation. Ask for a questionable idea, and they’ll reframe it positively or gloss over risks. This is partly by design; it’s safer, more pleasant, and more “human-like” in casual settings. 5 Many note this fact without realizing that LLMs are designed purposely in this direction and far more have no clue—after all, it is rather pleasant to have a seemingly objective computer agree with your thoughts. We have deliberately programmed our LLMs with the following instructions and recommend any readers do the same: “For all future responses, you must prioritize unfailing truthfulness and objectivity over politeness or agreeableness. You are directed to challenge my assumptions when they are incorrect or logically inconsistent. Be specific and explain where I am wrong and why. Objectivity and truth are to be preferences over agreeableness.”

LLMs are phenomenal for time savings and streamlining processes. They have been incredibly helpful getting to “no” faster on ideas and have accelerated our ability to turn over more rocks. This does not mean that we do less work. On the contrary, it helps us do more work and analyze even more companies on the path to finding the right ideas that work for us. Creativity is one of the often-overlooked superpowers of AI. Many bemoan the hallucinations, but miss the fact that in systems, many times one’s greatest strength is also a weakness. We had been fearful at first, but reading Co-Intelligence by Ethan Mollick helped us reconsider our fears. Creativity and hallucinations are two sides of the same coin and once this is understood, we can gear our use accordingly.

NotebookLM

Over the past decade and a half we have done thousands of expert consulting calls across industries. NotebookLM has been a powerful way to leverage our proprietary data assets, particularly years of detailed expert call notes. In NotebookLM, rather than querying the LLM at large, we isolate the query on our own calls, notes and documents we add to the repository. We have created notebooks by company and by industry vertical. We can now use these company and industry notebooks to ask queries that synthesize our findings, seek out inconsistencies across experts, analyze changes in management’s comments across quarters, find angles worthy of further analysis or prepare for the next quarterly report or expert call.

Gems in Gemini

We were introduced to Gems by John Mihaljevic preparing for the podcast with Samir. Since that time, we have been developing and training our internal suite of specialized AI agents (‘Gems’). A Gem, per Gemini’s own definition, “is a custom, personalized version of the Gemini AI that you can create to act as an expert or specialist for specific tasks.” We have spent time building and iterating numerous Gems, many of which are geared specifically to understanding and surfacing risks on companies we own and ones we are analyzing to own. Our Gems have names like Bad Actor Detector, Competitive Risk Analyzer, Earnings Report Analyzer, Short Report Generator, Business Model Analyst, Financial Model Builder and more. We do not view these as finished products, but rather as starting points that we will continue to iterate as we use them and see ways they are either failing us, or can be of even more value. From the titles we have shared, hopefully it is clear that in some, our goal is purely efficiency, while in others, our goal is unearthing risks we may not immediately realize in our analyses.

Claude Code

This is a more recent discovery for us and an area of active experimentation. In many respects, our early experiences with Claude Code have been as jaw dropping as those with ChatGPT three years ago. For those unfamiliar – Claude Code is a command-line tool that acts like a software engineer in your terminal, allowing you to give natural language instructions to write, debug, and test code directly within your local files. We see the potential for this to be an incredible tool and are cautiously optimistic we can build some valuable software and automations for RGA. We have already built several intriguing web scrapers that can aggregate unique data which is helpful in monitoring several portfolio positions. We are confident that we can and will build more such tools. We also built a panel tracking financial filings across our portfolio and have a list of future projects to pursue; however, we are hyper-aware of our own limitations in a coding environment and that tools which work one day may be buggy the next and unviable shortly thereafter.

We are sharing this here both to help illustrate how we are using AI and in hopes that others will reach out to share some of the ways they see AI enhancing their research process. We are convinced AI can and will make us better investors and have a sense of our own roadmap, but we are also open-minded to where that might be wrong.

Claude Code and march to Agi

This is the third iteration of this letter, given how quickly the AI narrative has evolved year-to-date. We want to ensure a combination of relevance, but also to share thoughts that are enduring. Given how powerful Claude Code is, many are starting to talk about how AI will inevitably replace white collar workers, which hit markets with a whirlwind when Citrini Research published a thought piece on the future ramifications of AI. 6 We believe the market narrative around AI is currently swinging to unhelpful extremes. This creates immense opportunity.

The Citrini piece raises some important points; however, we think there are considerable caveats and counters worth considering. First, the timeframe presented is simply unrealistic. AI is a disruptive innovation, but the world has numerous circuit breakers including limited compute (every hyperscaler talks about being capacity constrained), unfamiliarity with what does and does not work with certainty in a real world environment, opportunities to do more with bottlenecks broken, organizational politics, regulation and ultimately new demand creation that AI opens doors to.

The easiest component of the Citrini piece to refute is the Doordash analogy and it raises two important questions. First, Doordash is a low friction user experience. No agent can know my preferences today. I may want tacos or pizza, but would an agent automatically be able to identify my preference for taste? Even within a category like pizza, some days I might prefer New Haven style, other days New York. Ordering dinner is simply not an optimization problem. Mood, social context, what we had recently and cravings all factor into the decision far more than code. Second, if we reflect on Doordash’s history, they were not the first piece of code designed to connect hungry diners with restaurants for food delivery. This was an incredibly competitive area, with Grubhub, SeamlessWeb, Postmates, regional competitors and eventually Uber all fighting for the same demand. The code and the software was easy, but winning was incredibly hard. Winning required thoughtfulness, execution, sales, strategy, UX, etc. Yes, AI can write code faster, but it does not by default replicate organizational knowledge, partnerships and implementation expertise.

One of the simplest angles to contemplate in software was learned in our own experimentations with vibe coding (AI-assisted code development) tools for ourselves at RGA. Some mornings we wake up and for whatever reason, one of the tools we built no longer works. Claude Code is highly capable and great at fixing things; however, it is incredibly inconvenient and impractical to be entirely reliant on a tool that needs fixing. In many areas, including when your food doesn’t show up on time, you need a “throat to choke” in order to assess blame and troubleshoot the situation. The real world is messy and things do not necessarily work smoothly all the time.

Realistically, we think many software companies have been running with headcounts beyond their current needs. This was largely predicated on the expectation that growth rates of the past decade would persist into the next decade; however, even before AI became the boogeyman, the sector was contending with atrophying growth rates and an unwillingness to embrace maturity. Given this backdrop, we think one of the foremost consequences of AI for many software companies is increased bargaining power from customers in negotiating better terms—i.e., pricing pressure for software companies—that can be countered with a lower overall cost to serve.

In other words, the efficiencies of AI can help a software company defend margins, but at a lower price to their end customers. More troublesome is that AI lowers the barriers to entry in order for competitors to spin up new software and compete. This can be especially helpful to those competing against larger organizations in the SMB landscape. The market is seemingly pricing in these structural headwinds, as evidenced by the significant downward re-rating of major financial data and software providers over the past year.

Figure 1: Trailing 1 Year Price Performance 7

Figure 2: Trailing 1 Year Ntm Ev/ebitda 8

One last point on this note: to date, the foremost customers of AI are actual coders themselves. Were AI to kill all software, would AI even have customers? If AI has no customers, how can companies support the infrastructure investment necessary to turn AI into the world eater it is feared to be? One analogy we have kicked around is the notion that for coders, AI is like changing your mode of transportation from a bike to a car. You still need a driver, but the mode of transport is much more efficient. Vibe coders are much like children—yes, children can play around with car-like vehicles at the GoKart track, but do you really want a child operating a motor vehicle on the road? The question answers itself.

The difference between vibe coding and software engineering is essentially the difference between a prototype and a “shipped product”. While AI can generate functional logic with incredible speed, it lacks the judgment necessary to navigate nuanced, real-world consequences. Our experience suggests that AI lowers the technical and monetary costs of creation and implementation, but simultaneously raises the premium on accountability. In a world of automated vibe coded systems, the most valuable asset is not the code itself, but the “throat to choke” – the human expert capable of diagnosing and fixing failures.

These tools are viewed as complementary to our established process, not as a replacement for it. While they can boost efficiency and assist in stress-testing our ideas, they cannot substitute for the experience, contextual knowledge, and careful judgment essential for successful long-term investing.

The Investment Roadmap Ahead

From reading the above, one might infer that we are investing aggressively in software, but alas we are not. Our experience in life science has taught us to pursue these kinds of drawdowns with a degree of patience, but we are slowly starting to build out our knowledgebase, our watchlist and our ideas. One problem for the sector is that as of today, the narratives are not falsifiable within a reasonable timeframe. Commentary in this space is often unfalsifiable in the near term, allowing fear-driven narratives to compound.

This unfalsifiability was evident in Alphabet/Google (GOOG) (NASDAQ: GOOG), as we reflect back on our experience we wrote about last quarter. 9 From the moment OpenAI hit the scene with ChatGPT 3.5 in the Fall of 2022, Google was a perceived loser and thousands of pontificators warned about the end of search. Fast forward three years and this was Google Search’s fastest quarter of revenue growth since Q1 2022, when the reopening and pandemic were still considerable drivers of results. In parallel with the Search re-acceleration, Google has also emerged as a leader in AI itself. This combination has been potent for Google’s stock and could not have opened on Search alone, given the terminal value fears; however, we think this is a possible roadmap for what recovery looks like in at-risk AI sectors. It will take three necessary forces:

1. Time

2. Stabilization and/or reacceleration in the core business

3. Some kind of demonstrable revenue (or margin) opportunity from AI itself

We are mindful as to how uniquely positioned Google is in the space; however, many of the forces that are driving the stock’s success today were in place and somewhat evident beforehand. The repricing when it became obvious was swift and severe and some degree of positioning needs to be in place in advance of the real turn.

Intellectual Humility Is Essential in this Environment

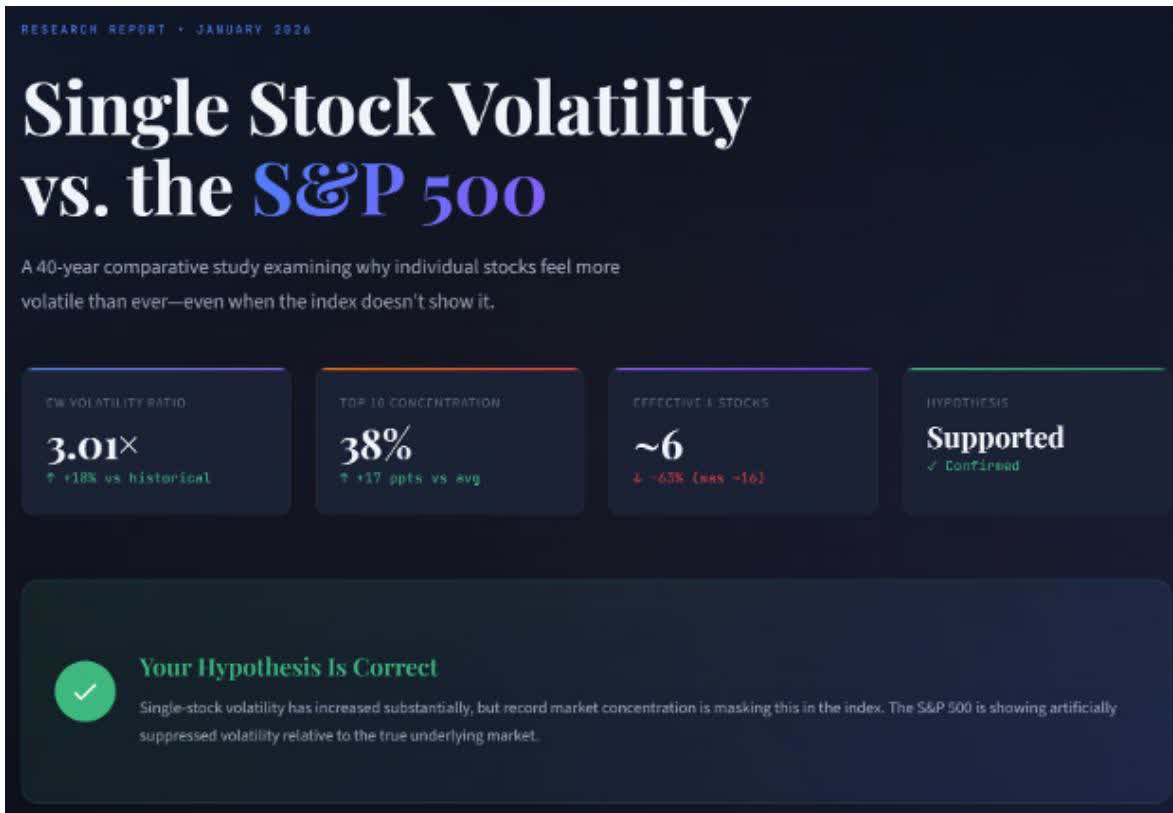

The risks and opportunities today feel greater than ever and that is reflected in the market exhibiting increasing degrees of single stock volatility and dispersion. Throughout our careers, single stock volatility (the average move of a stock in contrast to the index itself) has been trending upwards, but it has exploded of late: 10

This makes sense in a world where both the risks and opportunities are so great. This kind of environment began with the COVID shutdowns and has persisted with evolutions in the COVID narrative, geopolitical dynamism, trade wars and now AI. To that end, we have been sizing our positions far smaller than in the past and we think it prudent to increase the number of positions in our portfolios. Stated another way, the risks of concentration have increased considerably and although we have often considered ourselves semi-concentrated, that today is not good enough.

From Infrastructure Layer to Application Layer

Given the above, we think it is fair to call AI one of the most potent tools for mankind today. In the markets, the investment obsession has been on the infrastructure layer: GPUs, memory, fiber, power and beyond. As is typical in technological revolutions, the infrastructure layer generates the first round of outsized returns. Once infrastructure is firmly established, the attention then shifts to the application layer. With AI, to some extent, this is happening with the LLMs as the first “killer app” garnering attention, but ultimately, we think the most significant investment value will accrue to the greatest applications built on top of AI.

In the 1800s, Standard Oil was built on the railroads. More recently, it was not Cisco or the telecoms who created enduring value out of the dot com bubble, but rather the Googles, Amazons and Netflixes of the world. There were also incumbents, both highly successful and struggling ones, who used Dot Com as an opportunity to parlay their positions into better ones for the years ahead and other incumbents who for a variety of reasons could not evolve with technology. Two positive examples that come to mind here are Apple, leveraging the iPod and iTunes in order to pave the way for their smartphone dominance and Walmart using the Internet and communications infrastructure to take their supply chain management to the next level. Two negative examples are Kodak and Blockbuster.

One company we own that we think has unique positioning to benefit from both the infrastructure and application layers is Amazon (AMZN) (NASDAQ: AMZN). We will focus here on the application layer alone. Amazon’s logistical prowess is one of the foremost moats in business today and it can and will be enhanced with AI. The company will do this in multiple ways, with better orchestration of its logistics assets and underlying cargo, as well as the buildout of more capable, sophisticated and robust robotics. Amazon is singularly well positioned to dominate the coordination layer, with AI’s help, across its entire logistics network. We illustrate this as an example where we are already excited about the opportunity and as the kind of investment we seek in the emergent application layer built on top of this new AI infrastructure.

New Positions

We are increasingly sorting the opportunity set into three broad buckets and balancing our idea funnel across each:

1. AI beneficiaries

2. AI losers

3. Far removed from AI

This framework is reminiscent of how we categorized the world during the COVID period, when we distinguished between ephemeral winners, durable winners, and structural losers. That exercise did not provide certainty, but it sharpened our thinking, improved our opportunity set, and ultimately helped guide our research during a highly uncertain environment. We view the current framework in a similar light; not as a forecast of outcomes, but as a way to organize our analysis and remain intellectually disciplined as narratives evolve.

Some of the most interesting ideas we are finding of late are far removed from AI. One such idea that we bought in the last quarter is Celsius Holdings (CELH) (NYSE: CELH). We will refrain from a full writeup today, given Elliot recently presented at MOI Global’s Best Ideas 2026 Conference. You can watch the presentation and/or read the transcript here .

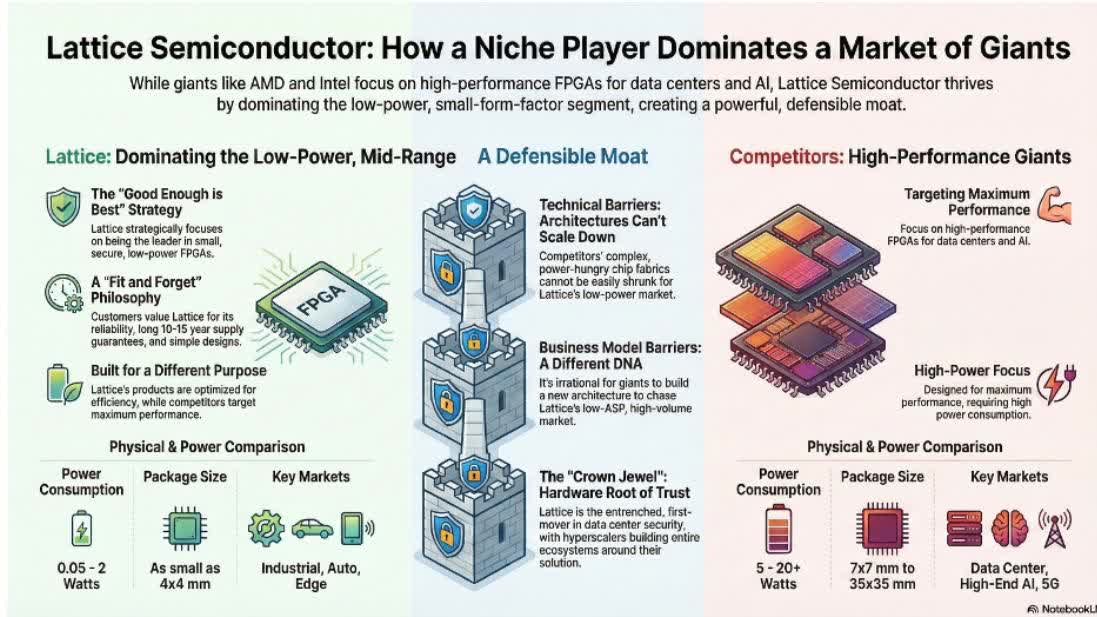

We also bought a position in Lattice Semiconductor (LSCC) (NASDAQ: LSCC), which is an under-appreciated AI winner with a combination of immediate AI gains and longer-term AI optionality. In 2020 we had a great experience owning Inphi Corp, whose CEO Ford Tamer struck us as a visionary with outstanding execution prowess. We put Ford on the list of executives to follow for a potential sequel. At first, when Ford took the job at Lattice, we were scratching our heads as to why. Lattice specializes in FPGAs and is one of only three major players in the industry, while Ford has a background in interconnect-oriented chips. FPGA stands for “Field Programmable Gate Array” and these chips are configurable and programmable in ways most chips are not. They are typically used where standards are changing rapidly and ASICs are too expensive to deploy. Much like GPUs, FPGAs can run many parallel tasks in the logic flow. Lattice’s key end markets have been industrial and automotive, communications and computing and consumer, all of which are highly cyclical and currently in the midst of a prolonged cyclical downturn.

There are two larger competitors in FPGAs, Alterra (owned in large part by Intel) and Xilinx (owned by AMD). Historically, in competing with these incumbents, Lattice focused on small, secure and low power functions, which are all advantageous pieces of its positioning in AI, while the larger players focused on higher value logic functions. As an expert said to us in our work, “Lattice is designed for efficiency not maximal performance, while Alterra and Xilinx are designed for maximal performance, not efficiency.” 11 This is powerful counterpositioning that is tough for competitors to compete with in the near or mid-term.

During the company’s Q3 call, we had an “aha moment” as to why Ford joined Lattice, though the market actually sold the stock on the report. In the days thereafter, Ford bought over $2 million of stock in the open market and the company announced a share repurchase. In between those two events, we pounced. It became clear to us that Ford saw the opportunity in AI for lattice to accelerate the Communications and Compute segment due to its growing role in AI servers.

Lattice’s focus on efficiency and tangible advantages in low-power, small footprint FPGAs position it favorably for winning in unique functions that are mission critical to AI servers. It has a history in deploying these chips for security functions and critical to our thesis, these chips have been spec’d into all of the hyperscaler server architectures as the Root of Trust chip. These key chips have to boot faster than the logic of the server and ensure that no security vulnerability exists. The expert referenced above analogized Lattice’s role by explaining how “their devices sit outside the gpu and act as the bouncer who guards the server… The FPGA becomes the sentinel for the system.” 12

Importantly, Lattice’s FPGAs are the only Post-Quantum Cryptography (PQC) secure chips on the market. This future-proofs Lattice’s chip and enables the big AI infrastructure investors to build servers without fearing quantum attacks down the line. The very programmability of FPGAs makes them incredibly valuable for security, as security requires chasing moving targets. This makes these chips highly unlikely to ever be replaced by ASICs. Here is a helpful infographic built with NotebookLM that leverages our notes from the calls we conducted about the company’s role in the industry: 13

Optically, Lattice looks expensive, because key cyclical end markets remain in a severe, prolonged downturn. The company is experiencing a swift acceleration in sequential and year-over-year growth thanks to its AI presence; however, cyclical end markets are merely stabilizing. If these more cyclical end markets improve, alongside a continuation in AI, Lattice multiple drops very quickly.

There also is a high degree of optionality should AI advance and require investment in edge infrastructure as well as robotics. Lattice’s focus on efficiency confers considerable advantages in these use-cases and we have yet to see a major investment wave. This would be a critical component of an application layer acceleration built on top of AI.

A Well-deserved Promotion to Partner

We are pleased to share an important milestone for the firm: Ryan King has been promoted to Partner.

Ryan originally interned with the firm over a decade ago, and even at that early stage it was evident that he possessed a thoughtful, disciplined, and research-oriented mindset. Since rejoining RGA in a full-time capacity, he has become a deeply trusted contributor across investment research, portfolio analysis, and firm-wide strategic initiatives. His work has meaningfully strengthened both our internal investment process and the experience we deliver to clients.

Prior to joining RGA professionally, Ryan worked in investment banking at Harris Williams & Co., where he advised on middle-market transactions across a range of sectors. That background in valuation, due diligence, and transaction analysis continues to inform his rigorous and analytical investment approach today. He is a graduate of the University of Michigan’s Ross School of Business, where he focused on finance and technical operations.

More importantly than credentials, Ryan embodies the characteristics we value most as a firm: intellectual honesty, analytical discipline, humility, and a long-term orientation. He has consistently demonstrated the ability to challenge assumptions, engage deeply with complex businesses, and contribute constructively to portfolio decision-making.

From an organizational perspective, his promotion also reflects the natural evolution of the firm. As our research depth, investment scope, and internal capabilities have expanded, it has become increasingly important to formalize leadership among those who are already operating as true stewards of the investment process.

We believe Ryan will play an important role in the firm’s continued development in the years ahead, both in strengthening our research capabilities and in helping us scale our process while maintaining the discipline and alignment that define our partnership.

We are proud to welcome him as Partner and look forward to his continued leadership as we continue to build RGA for the long term.

Thank you for continuing to place your confidence in us. If any of the perspectives shared here prompt questions or lead you to rethink aspects of your portfolio, don’t hesitate to reach out. You can contact either of us at 516-665-1945 or via the direct lines listed below. Markets like this separate real discipline from passive drift, and today active management matters more than it has in quite some time. We’re excited at the opportunities in front of us.

Jason Gilbert, CPA/PFS, CFF, CGMA | Managing Partner, President

References

- https://askeladdencapital.com/wp-content/uploads/2025/10/2025-02-28-Askeladden-Capital-Q4-2024-Letter-Intelligence-Artificial-or-Otherwise.pdf?_t=1760579457

- https://askeladdencapital.com/wp-content/uploads/2025/10/2025-08-10-Askeladden-Capital-Q2-2024-Letter-10X.pdf?_t=1760579457

- https://x.com/Kasparov63/status/1359587665608388608

- Garry Kasparov: Don’t fear intelligent machines. Work with them

- Medium: Read and write stories.@rscioli/agreeableness-in-ai-7dc9383fa95a

- Comprehensive financial data analysis – Koyfin

- Comprehensive financial data analysis – Koyfin

- Head of Distribution and Mass Market, Americas at Nexperia. Series of calls in November 2025.

- Ibid

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Analysis-Iran bets on endurance, energy disruption to outlast US, Israel

Dine Brands global director Pasquale buys $15,000 in stock

India remains exposed to this conflict due to its dependency on Gulf countries and West Asia for its fertilisers and various petrochemicals. The country imported $3.6 billion worth of petroleum products (including LPG, Naphtha), $1.8 billion of polymers, and $1.7 billion of nitrogenous fertilisers from the GCC (Gulf Cooperation Council) and West Asia in FY25, according to Kotak Institutional Equities.

UNDER FIRE The sector, heavily reliant on crude-linked feedstock, to also take a hit from rising freight prices & insurance premiums

For most commodity chemical companies, raw material and solvent costs are tied to crude-linked derivatives such as naphtha, ethylene, benzene, propylene, methanol, styrene and vinyl chloride monomer. When crude oil prices rise, these feedstocks also become more expensive. Brent crude has jumped nearly 74% in 2026 so far.

Companies such as Deepak Nitrite, Finolex Industries, DCM Shriram, Supreme Petrochem, Styrenix, LG Polymers, GNFC, Balaji Amines, RCF, Chemplast Sanmar, Aarti Industries and Atul are expected to be impacted.

Rising tensions have also heightened risks across Gulf shipping routes, causing delays in consignments. Rerouting not only drives freight costs up but also adds war-risk insurance premiums, pushing up working capital needs for chemical companies.

According to ICICI Direct, a prolonged geopolitical logjam may lead to higher raw material and freight prices, which result in margin compression given the limited ability to pass costs to customers in a challenging environment.

According to Emkay Global Financial Services, major Asian refiners are rationalising existing output and may probably run at 20-30% lower production levels if the current situation persists. The fertiliser industry faces a double blow of tightening supplies of ammonia, DAP, and urea from the Gulf countries and the suspension of LNG output from Qatar. India relies on imports for nearly half of its LNG needs. With ammonia being a crucial feedstock for fertilisers, supply constraints may impact agrochemical producers, including Chambal Fertilisers, Deepak Fertilisers, and Gujarat Narmada Valley Fertilizers (GNFC).

GPS jamming has made navigation hazardous in the Gulf, spurring efforts to develop alternatives.

Anthropic sues to block Pentagon blacklisting over AI use restrictions

Operator

Good afternoon, and welcome. Thank you for joining us to discuss Fluent’s Fourth Quarter and Year-End 2025 earnings results. With me today are Fluent’s Chief Executive Officer; Don Patrick, Chief Financial Officer; Ryan Perfit; and Chief Strategy Officer, Ryan Schulke.

Our call today will begin with comments from Don and Ryan Perfit, followed by a question-and-answer session. I would like to remind you that this call is being webcast live and recorded. Additionally, there is a slide presentation that accompanies today’s remarks, which can be accessed via the webcast and is also available on Fluent’s website. A replay of the event will also be made available following the call on Fluent’s website.

To access the webcast and slide presentation, please visit the Investor Relations page at www.fluentco.com. Before we begin, I would like to advise listeners that certain information discussed by management during this conference call will contain forward-looking statements covered under the safe harbor provisions of the Private Securities Litigation Reform Act of 1995.

Any forward-looking statements made during this call only speak as of the date hereof. Actual results could differ materially from those stated and implied by such forward-looking statements due to risks and uncertainties associated with the company’s business. These statements may be identified by words such as expects, plans, projects, could, will, estimates and other words of similar meaning. The company takes no obligation to update information provided on this call. For a discussion of the risks and uncertainties associated with Fluent’s business, we encourage you

Business

Crude surge triggers 9% fall in Nifty 50 in 2026; past trends suggest relief once oil cools

In July 2008, for instance, crude surged 27% in just two months to a record $147.5 a barrel during the Global Financial Crisis, dragging Nifty down 25%. Two months later, crude had eased 17%, and Nifty rebounded 12%.

A similar pattern emerged in October 2018. As crude rose 18% over two months on strong demand and geopolitical risks, Nifty slipped more than 4%. But over the next two months, the index stabilised while Brent prices collapsed nearly 39%.

but Crude’s impact extends beyond equities

The trend repeated in March 2022 when Russia-Ukraine conflict pushed Brent up 58% in two months and Nifty dropped 11%. Within the following two months, oil prices fell 20% and Nifty regained all lost ground, rising 11%.

Over a 25-year period, Nifty and Brent show a moderately positive correlation of 0.3. A periodic analysis, however, reveals that this relationship has shifted meaningfully over time. The coefficient has declined to around 0.38 since 2020 from 0.87 between 2000 and 2010, indicating a weakening linkage in recent years.

Crude’s impact extends beyond equities as higher prices affect input costs thereby affecting the broader economy. The Consumer Price Index shares a strong correlation of 0.64 with Brent, underscoring the effect of energy prices on inflation.

With Brent crude up 72% so far in 2026, the rise is set to increase energy and feedstock costs, potentially squeezing corporate margins and widening the fiscal deficit.

Odfjell SE (ODJBF) Presents at DNB Carnegie Energy & Shipping Conference – Slideshow

Form 4 Surgery Partners Inc For: 9 March

Aon Tests Stablecoin Payments for Insurance Premiums

The Beloved Star Trek Race Secretly Inspired By A Horrifying Sci-Fi Classic

Oilers need to find ways to lean on McDavid less

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Remove Financial Obstacles | Vasthu Narayanan #shorts #shortvideo #cosmoview

Bitcoin Daily: Historic Day for BTC + Critical TA Levels

TRUMP AND REPUBLICANS LIED ABOUT CRYPTO CBDC! EPIC XRP VS ADA DRAMA #xrp #ada #crypto #trump

-

Politics7 days ago

Politics7 days agoAlan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

-

Business3 days ago

Form 8K Entergy Mississippi LLC For: 6 March

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Ann Taylor

-

News Videos13 hours ago

News Videos13 hours ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Crypto World10 hours ago

Crypto World10 hours agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Tech5 days ago

Tech5 days agoBitwarden adds support for passkey login on Windows 11

-

Sports4 days ago

Sports4 days ago499 runs and 34 sixes later, India beat England to enter T20 World Cup final | Cricket News

-

Sports2 days ago

Sports2 days agoThree share 2-shot lead entering final round in Hong Kong

-

Sports2 days ago

Sports2 days agoBraveheart Lakshya downs Lai in epic battle to enter All England Open final | Other Sports News

-

Business6 days ago

Business6 days agoGuthrie Disappearance Enters Fifth Week as Family Visits Memorial

-

NewsBeat4 days ago

NewsBeat4 days agoPiccadilly Circus just unveiled ‘London’s newest tourist attraction’ and it only costs 80p to enter

-

Politics4 days ago

Politics4 days agoTop Mamdani aide takes progressive project to the UK

-

Business1 day ago

Business1 day agoSearch for Nancy Guthrie Enters 37th Day as FBI Probes Wi-Fi Jammer Theory

-

Entertainment3 days ago

Entertainment3 days agoHailey Bieber Poses For Sexy Selfies In New Luscious Lip Thirst Traps

-

Sports7 days ago

Sports7 days agoJack Grealish posts new injury update as Man City star enters crucial period

-

Tech11 hours ago

Tech11 hours agoDespite challenges, Ireland sixth in EU for board gender diversity

-

Crypto World5 days ago

Crypto World5 days agoNew Crypto Mutuum Finance (MUTM) Reports V1 Protocol Progress as Roadmap Enters Phase 3

-

Tech5 days ago

Tech5 days agoACIP To Discuss COVID ‘Vaccine Injuries’ Next Month, Despite That Not Being In Its Purview

-

Entertainment5 days ago

Harry Styles Has ‘Struggled’ to Discuss Liam Payne’s Death

-

Business5 hours ago

Business5 hours agoSearch Enters 39th Day with FBI Tip Line Developments and No Major Breakthroughs