Crypto World

CoinPoker Debuts New App with Rake Free Poker, Signs Abby Merk and Papo MC

[PRESS RELEASE – Panama City, Republic of Panama, March 10th, 2026]

Online poker site CoinPoker launched a new software client and mobile app in March 2026 alongside rake-free poker games and the signing of new sponsored players.

Joining the site’s ambassador team – already including some of the top names in poker, such as three-time Triton Series champion Mario Mosböck and WSOP Online main event champion Benjamin ‘Bencb’ Rolle – are Abby Merk and Alejandro ‘Papo MC’ Lococo.

https://x.com/CoinPoker_OFF/status/2030009912424849452

United States pro Abigail ‘Abby Poker’ Merk is an award-winning poker content creator from Chicago, ranked among the top female players in Illinois. With a background in volunteering, tutoring, and mentorship, Abby has also trained women in leadership skills and strategic thinking through the game of poker.

Freestyle rapper Papo MC has over $15 million in live tournament earnings – the #2 ranked player in Argentina behind Nacho Barbero – and a World Series of Poker bracelet.

Other household names of poker, such as Jean-Robert Bellande, Faraz Jaka, Mariano, YoH ViraL, Nik Airball, and Brantzen Wong, have also recently announced partnerships with CoinPoker.

https://x.com/mariomosboeck/status/2030247270378020932

Rake-Free Poker Games

Throughout March, CoinPoker is hosting rake-free poker games – players receive all cash game rake and tournament fees back daily, in the form of various promotions. In the first half of the month, players can potentially earn 100% flat rakeback credited to their accounts at 08:00 UTC each day.

In the second half of March, CoinPoker is returning all rake to players in the form of Splash Pot cash drops, CoinRaces leaderboards, and a Level Up Series of tournaments with boosted prizepools and refunded buy-ins – making for free poker tournaments until March 31.

Level Up Series

The Level Up tournament series debuts the site’s new multi-day tournaments and features such as bubble protection, blind rollback, final table deals and more. These events run alongside the site’s regular freerolls and MTTs, with added value in the prizepool and a full rebate on the rake.

That free poker event made headlines on PokerStrategy, and the 100% rakeback promotion was featured on Esports Insider.

Following its new software rollout, CoinPoker has also been rated among the best poker apps by the likes of Card Player Magazine and Gambling Insider and seen record traffic, rivalling the likes of GGPoker with over 7,000 players online for launch day.

The new poker app and desktop client include in-built player stats powered by PokerIntel, new games like PLO6, All-in or Fold, and Bomb Pot formats, and new features like EV cashouts, Interactive Emojis, and Throwables at the tables. No Limit Hold’em, Pot Limit Omaha, and PLO5 are also available, now with an improved lobby and table interface.

Throughout March, all of its poker games are essentially free to play to debut the new software, and its welcome bonus offer of 150% up to $2000 also returns in April onwards.

About CoinPoker

CoinPoker is an online poker site available for download on Windows, Mac, iOS, or Android, alongside an in-browser web client for free poker on mobile.

The platform’s tournaments and cash games are played in stablecoin Tether (USDT). Other major cryptocurrencies are also accepted, such as Bitcoin, Ethereum, and USDC, and 25+ countries can also deposit by bank transfer.

Alongside free poker action against real opponents around the world, the site also has an attached crypto casino and sportsbook.

Website: https://coinpoker.com/

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

Opinion by: Jesus Rodriguez, co-founder of Sentora

If you look at decentralized finance (DeFi) as a stack of computational primitives, it’s remarkably complete — yet fundamentally broken.

We have automated market makers for liquidity, like Uniswap. We have lending markets for capital efficiency, and bridges for cross-chain “packet switching.” Step back and look at the architecture from a systems engineering perspective.

There is a gaping hole where the risk backstop should be.

Insurance is the “missing primitive” of the decentralized web. It is the translation layer that turns scary, opaque technical risk into a legible line item — a number you can compare, hedge and budget for. Without it, we aren’t building a financial system; we’re building a very sophisticated, high-stakes casino.

Insurance hasn’t worked, so far

A lot of chatter has been spent on why onchain insurance hasn’t “mooned” despite billions in total value locked (TVL). Personally, I suspect the failure is structural, not just a “lack of interest.” We’ve been fighting against the physics of risk management.

Most first-generation protocols tried to use DeFi-native assets, like Ether (ETH) or protocol tokens, to insure the very same DeFi stack those assets live in. This is a classic “reflexivity” trap. When a major exploit happens, the entire ecosystem usually suffers a setback. The collateral loses value at the exact moment the payout is triggered. In systems terms, this is a positive feedback loop of failure. It’s like trying to insure a house against fire using a bucket of gasoline. To work, insurance requires uncorrelated capital: assets that don’t care if a specific smart contract gets drained.

Historically, we relied on retail yield farmers to provide “cover.” These users don’t wake up caring about actuarial tables or underwriting. They care about APY and points. This is not the stable, long-term underwriting base that is required to build a multibillion-dollar risk engine. Real insurance requires a “low cost of capital” base — institutional-grade assets that are happy to sit and collect a steady 2%-4% spread without needing to “degenerate” into 100% APY schemes.

The scaling imperative

We’ve spent years obsessing over TVL as the North Star of DeFi. TVL is a vanity metric; it tells you how much capital is sitting in the “danger zone.” The metric we actually need to optimize for — the one that actually measures the maturity of the industry — is total value covered (TVC).

If we have $100 billion in TVL but only $500 million in TVC, the system is effectively 99.5% “naked.” In any traditional engineering discipline, this would be considered a catastrophic failure in safety margins. You wouldn’t fly in a plane that was 0.5% “safety tested.”

The scaling imperative for the next era of DeFi is to bridge this gap. We need a path where TVC scales linearly with TVL. Currently, they are decoupled. TVL grows exponentially based on speculation, while TVC crawls linearly because the “risk markets” are illiquid and manually managed. Scaling DeFi isn’t just about Layer 2 throughput; it’s about “risk throughput.”

Pricing the ghost in the machine

We often talk about risk as an ethereal, spooky thing that happens to other people. In a mature financial system, risk is a commodity. It needs to be assetized.

Think of DeFi insurance as the pricing engine of risk. Currently, when you deposit into a vault, you are consuming a bundle of risks: smart contract risk, oracle risk and economic design risk. These risks are currently unpriced — they are just hidden baggage you carry.

By building a robust insurance primitive, we turn those hidden risks into tradable assets. We move from “I hope this doesn’t break” to “The market says the probability of this breaking is exactly 0.8% per annum, and here is the tokenized instrument that pays out if it does.”

Related: AI will forever change smart contract audits

This assetization is powerful because it creates a market signal. If the cost of cover for Protocol A is 5% while Protocol B is 1%, the market has effectively “priced” the security of the code. Insurance isn’t just a safety net; it’s the global oracle for protocol health. It turns “security” from a vague marketing claim into a hard, liquid price.

The dream of programmable insurance

The “end state” of this technology isn’t just a decentralized version of Geico — it’s a transition from legal insurance to computational insurance.

Think about the difference between a traditional legal contract and a smart contract. Traditional insurance involves 40-page PDFs, adjusters and a six-month claims process. It is a “human-in-the-loop” bottleneck.

Programmable insurance is a primitive that can be integrated directly into the transaction stack. It includes granular cover and atomic payouts. You don’t just “insure a protocol” in the abstract. You insure a specific LP position, a specific oracle feed, or even a single high-value transaction. If the state of the blockchain detects an exploit, the payout happens in the same block. There is no “claims department”; there is only “state verification.”

This makes insurance a “first-class citizen” in the code. You can imagine an “Insurance” button on every swap or deposit, much like how you choose “priority gas” today. It becomes a toggle in the UI.

The next wave of DeFi adoption

The real challenge for DeFi adoption isn’t convincing another 1,000 degens to use a bridge; it’s onboarding the fintechs and neobanks.

These entities are already knocking on the door. They are considering the 5% onchain risk-free rates and comparing them to their legacy rails, which are clogged with overheads and rent-seekers. However, for a neobank (think of firms such as Revolut, Chime or Nubank), “The code is the law” is not a valid risk management strategy. Their regulators — and their own risk committees — simply won’t allow it.

For these players, insurance isn’t a “nice to have”; it’s a hard requirement for deployment. They represent the next “trillion-dollar” wave of liquidity, but they are currently standing on the sidelines. They need a “wrapper” that makes DeFi look like a bank account.

If we can provide a robust, programmatically backed insurance layer, we aren’t just protecting degens; we are providing the “regulatory-compliant shield” that allows a neobank to put $1 billion of customer deposits into a lending vault. Insurance is the bridge between “crypto-native” and “global finance.”

We’ve spent the last few years building the “engine” of the new financial system. We have the pistons (liquidity), the transmission (bridges) and the fuel (capital). But we forgot the brakes and the air bags.

Until we solve the insurance primitive, DeFi will remain a niche experiment for the risk tolerant. By shifting our focus from TVL to TVC, moving toward uncorrelated collateral and embracing the “pricing engine” of assetized risk, we can finally turn this experiment into a resilient, global utility.

Strap in. There is a lot of code to write and even more risk to underwrite.

Opinion by: Jesus Rodriguez, co-founder of Sentora.

This opinion article presents the author’s expert view, and it may not reflect the views of Cointelegraph.com. This content has undergone editorial review to ensure clarity and relevance. Cointelegraph remains committed to transparent reporting and upholding the highest standards of journalism. Readers are encouraged to conduct their own research before taking any actions related to the company.

U.S. prosecutors asked a federal judge to set an October date for the retrial of Tornado Cash developer Roman Storm on two unresolved criminal counts after a jury failed to reach unanimous verdicts during the original hearing, according to a letter filed Monday in the Southern District of New York.

In a letter to U.S. District Judge Katherine Polk Failla, U.S. attorney Jay Clayton, a former chair of the Securities and Exchange Commission (SEC, asked for a date now to “to avoid further unnecessary delays,” even though Storm, who is currently free on bail, has a pending motion for a judgment of acquittal. Oral arguments on that motion are scheduled for April 9.

Storm is a co-founder of Tornado Cash, a crypto mixer designed to obscure the origin and destination of blockchain transactions. In August, a jury convicted Storm on one count tied to operating an unlicensed money-transmitting business, and failed to agree on verdicts for two other charges, leaving alleged violations of money laundering sanctions law unresolved. He is currently free on bail while awaiting further proceedings.

Storm criticized the planned retrial in an X post on Tuesday, saying the jury’s split decision reflected uncertainty about the government’s case.

“A jury of 12 Americans heard four weeks of evidence and deadlocked: no verdict on money laundering, and no verdict on sanctions violations,” Storm wrote. “The government’s response? Try again to make writing code a crime.”

Storm also referred to a U.S. Treasury report acknowledging that mixing services like Tornado Cash can serve lawful purposes on public blockchains. The report came after years of opposition to crypto mixers.

Defense lawyers told prosecutors that setting a trial date before the April motion is resolved would be premature.

Arkham’s data shows that their PnL on bitcoin has risen to $1.8 billion.

The Winklevoss twins, who have been predominantly vocal about Zcash and Cypherpunk lately, have made a large BTC transfer to the cryptocurrency exchange they co-founded a decade ago.

According to data from the analytics company Arkham, the $130 million transfer to Gemini’s hot wallets was done “presumably to sell.”

THE WINKLEVOSS TWINS SOLD $130M BTC

The Winklevoss Twins transferred $130M of BTC to Gemini Hot Wallets since last week, presumably to sell.

The Winklevosses once owned 1% of the circulating BTC supply – and now continue to hold $764M of BTC. Their total PnL on BTC is currently… pic.twitter.com/Pjzp45V3K7

— Arkham (@arkham) March 10, 2026

Their data further indicates that the brothers once owned roughly 1% of bitcoin’s supply. Previous reports suggested that they began buying BTC in 2011, purchasing $11 million in the cryptocurrency at $120 per unit from the $65 million they were awarded in cash and Facebook stock following a legal dispute with Mark Zuckerberg.

Although they reportedly sold a portion of their holdings to launch Gemini, their estimated PnL on bitcoin remains around $1.8 billion, Arkham added.

They have made several newsworthy donations over the years, including multi-million-dollar transfers of BTC to Donald Trump’s 2024 presidential campaign on the promise that he was pro-bitcoin, pro-crypto, and pro-business.

While championing for more privacy in the cryptocurrency industry, their focus has most recently switched toward Cypherpunk – a company dedicated to self-sovereignty.

You may also like:

In the initial statement, the brothers said they will “execute on our mission by accumulating, building, and supporting privacy-protecting assets and technologies at a time when the world needs them more than ever.”

The latest press release shared by the company reads that Cypherpunk Technologies has invested $5 million into Zcash Open Development Lab (ZODL), which is its first tech investment outside of ZEC.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

US lawmakers have launched an investigation into several Wall Street underwriters, including Dominari Securities, whose parent company is linked to the Trump family, over their role in bringing Chinese companies to US stock markets that were later tied to stock manipulation schemes.

On Monday, the House of Representatives Select Committee on China, chaired by Representative John Moolenaar with Rep. Ro Khanna as ranking member, sent letters to three US companies — D. Boral Capital, Dominari Securities and Revere Securities — seeking information about Chinese initial public offerings (IPOs) they helped underwrite.

“These scam centers defraud American households through coordinated “ramp-and-dump” stock manipulation schemes involving Chinese shell companies listed on American exchanges, which your firm appears to facilitate,” the lawmakers wrote.

The Chinese companies allegedly used US IPOs to inflate their share prices through coordinated trading and promotion, then dumped shares on retail investors before the stocks crashed. In some cases, dozens of accounts allegedly placed nearly identical buy orders above the IPO price, temporarily pushing valuations higher before insiders sold their stakes.

Related: Trump Sends Pro-Bitcoin Fed Chair Nomination to the Senate

Chinese stock schemes drain billions from investors

The lawmakers cited estimates that around $16 billion in US investor wealth has been drained since 2023 through such schemes. They also pointed to FBI data showing a 300% increase in complaints tied to Chinese stock manipulation cases.

The inquiry seeks documentation from the underwriters, including communications, trading records, funding sources and due diligence policies related to Chinese IPOs.

The committee said it is examining whether US financial intermediaries may have inadvertently helped facilitate manipulation schemes tied to Chinese issuers. The firms have been asked to submit the requested documents by Friday.

Related: Trump’s Media Company Closes $105M Crypto.com Deal

Dominari draws scrutiny in Chinese stock probe

One of the brokerage firms named in the probe is Dominari, which has ties to the Trump family. Located in New York’s Trump Tower, it is owned by Dominari Holdings, where Eric Trump, son of US President Donald Trump, is the fourth-largest shareholder. Eric Trump and Donald Trump Jr. joined the company’s advisory board in February 2025.

Last year, Dominari helped facilitate fundraising for Thumzup, a public company that adopted a Bitcoin (BTC) treasury strategy and also attracted millions of dollars in investment from Donald Trump Jr.

Magazine: Bitcoin may take 7 years to upgrade to post-quantum — BIP-360 co-author

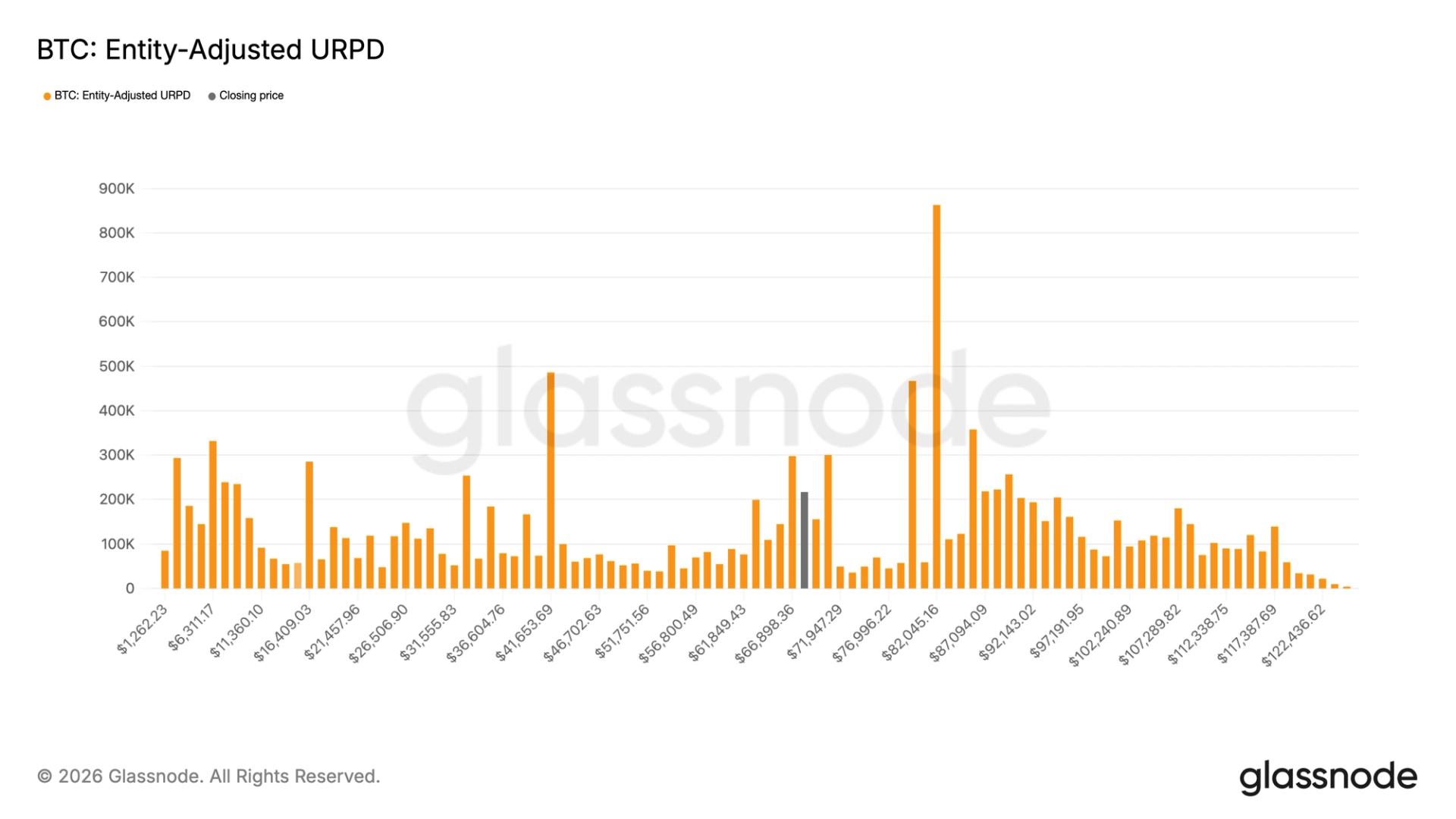

Bitcoin’s recent dip triggered heavy trading activity, with nearly 600,000 BTC changing hands in the $60,000–$70,000 range, according to blockchain data tracked by Glassnode.

In other words, traders went bargain hunting, snapping up nearly 600,000 BTC ($42.48 billion) in this price band during the correction. Of these, more than 200,000 BTC were accumulated in the past two weeks alone.

Note that at the start of the year, roughly 997,000 BTC had last moved within the $60,000–$70,000 range. Since bitcoin’s recent drop below $70,000, that number has jumped to 1.558 million BTC.

Taken together, it means that nearly 8% of the circulating supply is owned by people who bought their bitcoin in this range, creating a dense cluster of ownership. As such, the $60,000–$70,000 range could act as an important support level going forward.

At press time, bitcoin changed hands above $70,000, trading at levels, which have previously seen thin trading activity. CoinDesk Research has previously highlighted the “air gap” between $70,000 and $80,000, a range where relatively little supply changed hands.

Still, the market is at a point where things could spice up, because analysis by Checkonchain shows that around 40% of bitcoin holders have paid more than $70,000 for their coins.

- Legal injunction halts South Korean delistings of FLOW cryptocurrency.

- Altcoin rotation supports FLOW’s surge, outperforming broader crypto markets.

- Momentum indicators show FLOW in the overbought region, hinting at a possible pullback.

FLOW, the native token of the Flow blockchain, has seen a dramatic surge today, climbing over 53% in just 24 hours.

The jump comes despite recent announcements that major South Korean exchanges, including Upbit and Bithumb, planned to delist the token.

At first glance, delisting news might seem like a bearish trigger, but in FLOW’s case, the market response has been the opposite.

Here’s why the FLOW price is rising

The primary reason behind the surge is a legal move to suspend the delistings.

The Flow Foundation filed an injunction with the Seoul Central District Court to halt the planned March 16 delistings.

This move has reassured investors that the token will remain accessible on major South Korean platforms, removing a significant risk that had weighed on FLOW’s price for months.

In addition, Binance recently removed its monitoring tag for FLOW, signalling that previous technical issues have been resolved.

Together, these developments have alleviated fears about liquidity and safety, prompting a rush of capital back into the token.

Trading volumes have also spiked dramatically, indicating that both domestic and international traders are jumping in on the momentum.

Altcoin rotation strengthens the bullish momentum

Beyond the legal developments, FLOW’s rally has also benefited from a broader market trend.

Capital is currently rotating into altcoins, with investors seeking opportunities outside Bitcoin (BTC) and Ethereum (ETH).

This environment has amplified FLOW’s gains, as traders are looking for tokens with high growth potential and positive news catalysts.

FLOW’s performance today illustrates how market psychology and sector-wide trends can interact.

Even though BTC and the broader market have seen modest gains, FLOW’s price movement is clearly outpacing them due to its specific news-driven momentum.

This demonstrates how individual altcoins can decouple from broader market trends when there is a strong, token-specific catalyst.

FLOW price forecast

The pending court decision will remain the primary catalyst, as a favourable ruling could sustain momentum, while a rejection could trigger a swift correction.

Looking ahead, the immediate support is around $0.0481, which has acted as a pivot during the surge.

Holding above this level suggests that buyers remain in control and that the rally could continue toward the $0.07 area.

However, FLOW is currently in overbought territory, with momentum indicators like the RSI suggesting that a short-term pullback is possible.

If the price falls below the pivot, the token could retrace toward the 50-day moving average near $0.04743.

Crypto World

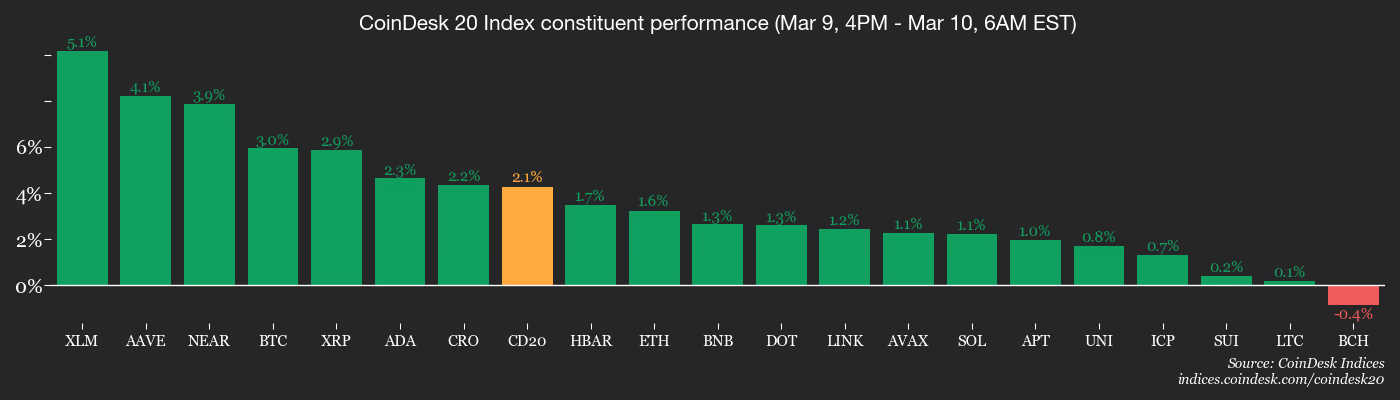

Stablecoin market expands, BTC price rallies as Iran war panic cools: Crypto Daybook Americas

By Omkar Godbole (All times ET unless indicated otherwise)

The stablecoin market is expanding again, led by USDC, and bitcoin’s rally is gathering steam.

The panic over the Iran war has cooled in the past 24 hours after President Donald Trump said the conflict could be over soon. The result: Bitcoin, which held resilient through the turmoil, has rallied past $70,000, up over 4%. The CoinDesk 20 Index, ether (ETH), solana (SOL), and XRP (XRP) are up 3% to 5%, and smaller coins like HYPE, ZEC, and RENDER rallying 7% to 11%.

The market capitalization of USDC, the second-largest dollar-pegged cryptocurrency, is fast closing on the record high of $78.6 billion, extending a recovery from the late-January low of $70.9 billion. Stablecoin leader USDT’s supply has risen to $184 billion from the late-February low of $183.5 billion.

This upswing in supply of top coins pegged to the U.S. dollar indicates the dry powder sitting on the sidelines is increasing and could be deployed to fund new crypto purchases as the rally extends. ETF inflows are supportive of a continued bullish trend as well.

Some indicators, however, still call for caution. The Coinbase Premium Index, which measures the gap between bitcoin prices on the Nasdaq-listed Coinbase (COIN) exchange and offshore giant Binance, remains negative, a sign that demand from U.S. investors is still lagging. Historically, bull runs have seen sustained Coinbase premiums.

In traditional markets, oil has fallen back below $100, which supports continued stability in all risk assets, including cryptocurrencies. The dollar index and Treasury yields have also pulled back from recent highs. Stay alert!

Read more: For analysis of today’s activity in altcoins and derivatives, see Crypto Markets Today

What to Watch

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

- Crypto

- Macro

- March 10, 9:00 a.m.: U.S. existing home sales for February est. 3.9M (Prev. 3.91M)

- Earnings (Estimates based on FactSet data)

Token Events

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

- Governance votes & calls

- Aavegotchi DAO is conducting ballot 1and 2 of a multi-sig signer election, asking token holders to choose one signer from various nominees. Voting ends March 10.

- Ssv.network DAO is voting to cancel DIP-46 and reallocate the originally approved $15 million development budget, splitting it into $14.9 million for DVT and $100,000 as a retroactive research grant. Voting ends March 10.

- Realtoken Ecosystem Governance DAO is voting to temporarily pause interest rates on the RMM (Real Estate Monetary Fund) to zero for 15 days. Voting ends March 10.

- Unlocks

- Token Launches

Conferences

For a more comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead“.

Market Movements

- BTC is up 2.56% from 4 p.m. ET Monday at $70,734.01 (24hrs: +4.60%)

- ETH is up 1.68% at $2,061.24 (24hrs: +3.38%)

- CoinDesk 20 is up 2.02% at 2,015.27 (24hrs: +4.08%)

- Ether CESR Composite Staking Rate is up 17 bps at 2.81%

- BTC funding rate is at 0.0024% (2.6105% annualized) on Binance

- DXY is unchanged at 98.84

- Gold futures are up 2.02% at $5,194.10

- Silver futures are up 6.50% at $89.50

- Nikkei 225 closed up 2.88% at 54,248.39

- Hang Seng closed up 2.17% at 25,959.90

- FTSE 100 is up 1.84% at 10,437.86

- Euro Stoxx 50 is up 2.94% at 5,852.45

- DJIA closed on Monday up 0.50% at 47,740.80

- S&P 500 closed up 0.83% at 6,795.99

- Nasdaq Composite closed up 1.38% at 22,695.95

- S&P/TSX Composite closed up 0.32% at 33,189.30

- S&P 40 Latin America closed up 1.61% at 3.532,70

- U.S. 10-Year Treasury rate is unchanged at 4.14%

- E-mini S&P 500 futures are unchanged at 6,823.00

- E-mini Nasdaq-100 futures are unchanged at 25,100.25

- E-mini Dow Jones Industrial Average futures are unchanged at 47,948.00

Bitcoin Stats

- BTC Dominance: 59.53% (0.77%)

- Ether-bitcoin ratio: 0.02905 (-0.27%)

- Hashrate (seven-day moving average): 1,008 EH/s

- Hashprice (spot): $31.06

- Total fees: 2.52 BTC / $171,578

- CME Futures Open Interest: 103,205 BTC

- BTC priced in gold: 13.7 oz.

- BTC vs gold market cap: 4.76%

Technical Analysis

- The chart shows SOL’s daily price action in candlestick format since August last year.

- The token is again trapped in a back-and-forth trading range, this time between $75 and $90, mimicking the October and December-January pattern.

- The next move depends on the direction in which the range is ultimately resolved. A bullish resolution could bring a quick-fire rally above $100, while a breakdown would suggest continuation of the broader bearish trend.

Crypto Equities

- Coinbase Global (COIN): closed on Monday at $199.79 (+1.30%), +3.46% at $206.70 in pre-market

- Circle Internet Group (CRCL): closed at $111.84 (+9.74%), +2.18% at $114.28

- Galaxy Digital (GLXY): closed at $21.50 (+4.57%), +3.09% at $22.16

- MARA Holdings (MARA): closed at $8.66 (+8.11%), +2.31% at $8.86

- Riot Platforms (RIOT): closed at $14.70 (+3.78%), +2.52% at $15.07

- Core Scientific (CORZ): closed at $15.16 (+2.02%), +1.45% at $15.38

- CleanSpark (CLSK): closed at $9.61 (+4.34%), +2.29% at $9.83

- Exodus Movement (EXOD): closed at $10.83 (-0.64%)

- CoinShares Bitcoin Miners ETF (WGMI): closed at $37.33 (+3.49%)

- Bullish (BLSH): closed at $36.06 (+3.15%), +1.14% at $36.47

Crypto Treasury Companies

- Strategy (MSTR): closed at $138.95 (+4.06%), +3.25% at $143.46

- Strive Asset Management (ASST): closed at $8.51 (-2.18%), +4.58% at $8.90

- Sharplink (SBET): closed at $7.60 (+3.26%), +1.71% at $7.73

- Upexi (UPXI): closed at $0.97 (+7.78%), +6.19% at $1.03

- Lite Strategy (LITS): closed at $1.20 (+5.26%)

ETF Flows

Spot BTC ETFs

- Daily net flows: $167.1 million

- Cumulative net flows: $55.52 billion

- Total BTC holdings ~ 1.28 million

Spot ETH ETFs

- Daily net flows: -$51.3 million

- Cumulative net flows: $11.61 billion

- Total ETH holdings ~ 5.73 million

Source: Farside Investors

While You Were Sleeping

Crypto World

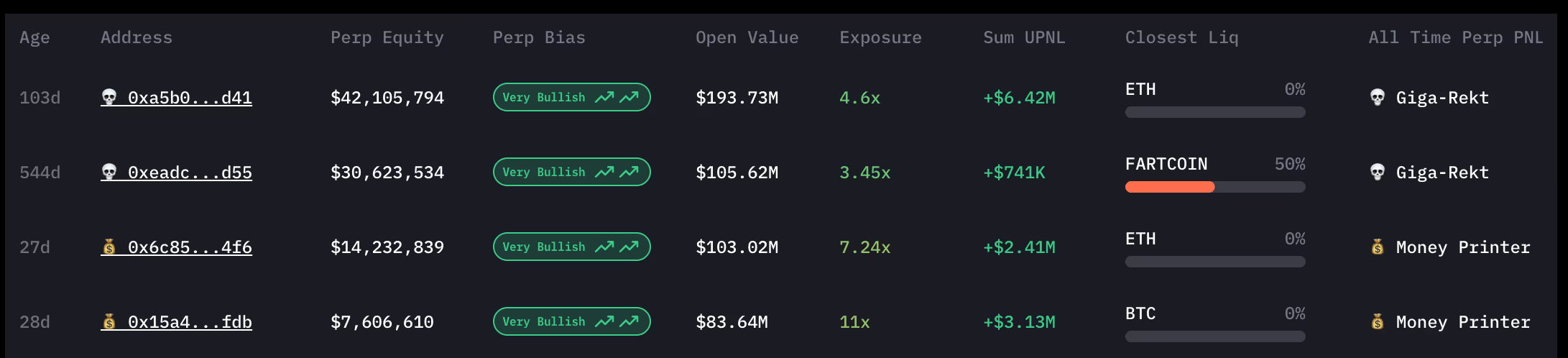

Massive leveraged bets show crypto traders are convinced this week’s rally is the real deal

Crypto traders on the perpetuals exchange Hyperliquid are placing increasingly aggressive leveraged bets that bitcoin will break above $75,000 after a sharp rally at the start of the week.

Bitcoin climbed to around $71,000 on Tuesday, up from roughly $65,000 when BTC futures opened on Sunday evening. The move has reignited calls for a retest of recent highs after being rejected near $74,000 last week.

Onchain data shows several large traders — often referred to as “whales” — opening highly leveraged long positions on Hyperliquid as prices rise.

One trader is holding ether (ETH) and bitcoin long positions worth $194 million with unrealized profit and loss standing at around $6.5 million. Another account has $103 million worth of long positions across a multitude of trading pairs, betting on a broader crypto breakout as opposed to a major-dominated rally.

Positions on Hyperliquid are typically opened with leverage, allowing traders to amplify exposure. One wallet, for example, opened a series of trades using 20x leverage, meaning a $1 million account could control a $20 million bitcoin position. This trader opened 20x leveraged longs on 600 BTC worth about $42.5 million while simultaneously taking a 20x long position on 20,000 ETH valued at roughly $41.2 million.

The whale also appears to be accumulating ether in spot markets. Data shows the address spent $21 million in USDC to purchase 10,158 ETH at an average price of $2,067 shortly before opening the derivatives positions.

Other nine-figure long positions demonstrate one thing: Crypto traders are confident this breakout will stick and won’t be a bull trap like last week.

A separate wallet, 0x985f, is taking a different macro stance. The address deposited $9.5 million in USDC into Hyperliquid within a five-hour window before opening 20x leveraged short positions on oil futures, including roughly $8.17 million in crude oil (CL) contracts and $6.15 million in Brent oil.

The same trader also opened short positions across several crypto tokens, including HYPE, PUMP, XPL, APT and ASTER, suggesting a broader bearish stance on select altcoins while large traders concentrate bullish bets on bitcoin and ether.

The positioning highlights how decentralized derivatives platforms such as Hyperliquid have become a hub for large leveraged bets during periods of strong bitcoin momentum.

A break above $75,000 could force short sellers to cover and accelerate the rally, while a move lower would quickly test the conviction of traders piling into nine-figure leveraged longs.

Gas prices at a Shell Station located on Foothill Blvd.

Robert Gauthier | Los Angeles Times | Getty Images

Rising oil prices may not just be a headwind to President Donald Trump’s fight to lower inflation. They could also undermine his signature legislative achievement.

Almost all of the economic effect of the individual tax cuts in the “big beautiful bill” — from both smaller withholdings and sweetened tax refunds — could be erased if oil prices remain elevated by more than $20 compared to before the U.S.-Iran war, according to Raymond James.

“With the $25 move last week, if the oil price stays here, it essentially offsets the fiscal benefit from the OBBA,” wrote strategist Tavis McCourt in a note.

McCourt’s analysis relies on applying any increase in oil market prices to the more than $420 billion that consumers spent on gasoline in the fourth quarter of 2025. He told CNBC in an interview he accounted for both potential reduced demand due to higher prices and companies’ needs to pad margins in his calculations.

That leads him to conclude a $20 move in oil prices could mean consumers spending $150 billion more at the pump. The Tax Foundation estimates that the big beautiful bill’s individual tax cuts total $129 billion for 2025, with the overwhelming majority of it set to appear through tax refunds this filing season.

U.S. oil before the war on Feb. 27 closed at $67.02. As of Tuesday morning, after a major whiplash in prices on Monday, oil is still trading more than $20 a barrel higher at $88.20.

@CL.1 since Feb. 27 chart.

Stephanie Roth, chief economist at Wolfe Research, said in a Monday interview her estimations for the hit consumers could take with elevated oil prices are also similar to the elevated spending she projected from the tax law. Though Wolfe in a Tuesday note said oil prices would need to remain above $100 for some time for that to happen.

“In all these scenarios, it has to last longer than it is now,” Roth said. “The impact on gas prices so far has been short-lived, and modest compared to how it may ultimately play out.”

But it will take time for oil prices to come down even if an end to the war in Iran arrives, which Trump said in an interview with a CBS News reporter on Monday is “very complete,” didn’t give a timeline for the war’s end in a press conference that followed.

McCourt noted it took about six months for oil prices to get back to levels where they were before surges higher after the Gulf War in 1990 and the Russian invasion of Ukraine in 2022.

Consequences of weaker stimulus

Fiscal stimulus from the tax law was expected to boost the economy in 2026, with some economists predicting a reacceleration of U.S. growth partially thanks to it.

Now, an oil price shock is hitting right as consumers are set to get those tax refunds. Citadel Securities last week estimated that only 30% of refunds had been distributed by March 1, with the figure expected to rise to around 75% by May 1.

“The bottom line is that if we were expecting those tax refunds to lift consumer spending, these higher oil prices are just redirecting all that cash toward energy costs,” wrote Gabriel Shahin, CEO of Falcon Wealth Planning, in an email to CNBC. “It’s essentially voiding out the economic boost we were set to see.”

But Dan Niles, portfolio manager at Niles Investment Management, framed the situation as the refunds helping the economy weather higher oil prices.

He already has faith consumers can do that, pointing back to when oil hit similar prices in 2022 and 2023, all while Wall Street broadly predicted a recession on the horizon thanks to rising interest rates.

“You already had that stress tested a bit,” Niles said. “So if that’s the case back then, and coming off of inflation surging in 2021, and you still didn’t get a recession, why would you think inflation down at 3% and oil at $100 would cause a recession now?”

Many on Wall Street have drawn similarities between the surge in prices this time around to four years ago, when Russia invaded Ukraine.

Roth, though, cautioned investors against relying too much on that comparison.

“The economic backdrop is not a mirror image of where we are today,” she said. “Core inflation was running at 5.5% compared to 3% today. Job growth was running at around 500,000, now we’re at 37,000 over the past couple of months. So it’s just an entirely different backdrop.”

.GSPD vs. .SPX year-to-date chart.

McCourt added he thinks if the stimulus from the big beautiful bill isn’t as strong as originally thought, that likely won’t change too many outlooks for the year, particularly in stocks which he thinks never priced in a big surge in consumer spending. He noted that consumer discretionary stocks have underperformed the S&P 500 in 2026.

But he also had faith that the economy, not just the stock market, could weather oil prices and weaker-than-expected stimulus, so long as the labor market remains intact.

“We just have never had a sustained pullback in consumer spending without substantial job losses,” McCourt said. “We’ll have some shifts in spending… But it’s probably not going to impact the overall consumer spending levels.”

The ICT Silver Bullet strategy is a short-term trading approach derived from the Inner Circle Trader (ICT) methodology. It focuses on identifying high-probability price movements that tend to occur during specific intraday trading windows, particularly around the London and New York sessions.

Unlike many conventional forex trading strategies that rely primarily on indicators, the Silver Bullet strategy emphasises market structure, liquidity pools, and fair value gaps (FVGs) to identify potential entry points. By concentrating on defined time windows and liquidity-driven price movements, traders attempt to capture short-term market inefficiencies that may appear during periods of increased institutional activity.

In this article, we explain what the ICT Silver Bullet strategy is, how it works, and how traders analyse price action, liquidity, and fair value gaps when applying this method in forex markets.

Understanding the ICT Silver Bullet Strategy

What is a Silver Bullet in trading? The ICT Silver Bullet trading strategy is a sophisticated trading methodology developed by Michael J. Huddleston, known as the Inner Circle Trader, or ICT. This strategy is designed to take advantage of specific price movements that align with certain times throughout certain sessions, specifically the London and New York sessions.

Central to the ICT Silver Bullet strategy are two concepts: liquidity and fair value gaps. Liquidity in this context refers to places within the market where there is significant trading activity, often indicated by previous highs and lows of a trading session or historical price points that attract significant interest from traders.

Fair value gaps are price areas that were either skipped over quickly during rapid price moves or areas where the price has not returned for a significant period, reflecting a disparity between perceived value and market price.

The idea behind the strategy is based on executing trades during specific one-hour windows known as Silver Bullet times. By focusing on these concepts and timings, traders can more accurately analyse market movements and align their trades with the influxes of smart money, potentially improving their results by catching swift moves towards liquidity points.

Key Components of the Strategy

The Silver Bullet ICT strategy employs a detailed approach to trading that revolves around understanding market dynamics at critical times. Here are the main components that define this strategy:

Fair Value Gaps

A fair value gap (FVG) occurs when the price quickly moves away from a level without significant trading occurring at that price, leaving a “gap” that is likely to be tested again when the price returns to this point. In the context of the ICT Silver Bullet strategy, these gaps are targeted because they represent potential inefficiencies in the market where the price may return to balance or fill the gap. Traders using this strategy watch these gaps closely as they often present clear entry points when approached again.

Liquidity Targets

Liquidity targets are essentially areas where there is expected to be a significant volume of orders, which can lead to particular price movements when these levels are approached. These include:

- Previous session highs and lows: These are often areas where stop-loss orders accumulate, making them prime targets for liquidity-driven price moves.

- Swing points in the market: Reversal and continuation points that have historical significance.

- Psychological levels: These include round numbers or price levels ending in ’00’ or ’50’, which often act as focal points for trading activity.

Specific Silver Bullet Time

Unlike many strategies that align strictly with market opening times, the ICT Silver Bullet trading strategy utilises specific one-hour windows during the day when liquidity and volatility are expected to be high due to trader participation across the globe. These Silver Bullet hours are strategically chosen based on their potential to tap into significant market moves:

- London Open Silver Bullet: Occurs from 3:00 AM to 4:00 AM Eastern Standard Time (EST) in winter and from 2:00 AM to 3:00 AM in summer, which is 8:00 AM to 9:00 AM Greenwich Mean Time (GMT) in winter and 7:00 AM to 8:00 AM in summer.

- New York AM Session Silver Bullet: From 10:00 AM to 11:00 AM EST, translating to 3:00 PM to 4:00 PM GMT.

- New York PM Session Silver Bullet: From 2:00 PM to 3:00 PM EST or 7:00 PM to 8:00 PM GMT.

These time slots are selected based on historical data showing heightened trading activity and, therefore, increased probabilities to capture moves towards identified liquidity targets.

Implementing the ICT Silver Bullet Strategy

Traders utilising the ICT Silver Bullet strategy typically prepare by marking potential fair value gaps and liquidity targets before these key trading times. As these windows approach, they monitor price action closely for signs that the market is moving bullishly or bearishly toward these liquidity points, enabling them to search for an entry.

Is there a specific Silver Bullet time? This is an intraday strategy; therefore, ICT says it’s popular on a 15-minute timeframe or lower. Some traders use the 1-minute to 5-minute for the Silver Bullet setup, though those inexperienced with the strategy may prefer the 5-minute.

Traders can experiment with session timing and entry setups directly on FXOpen’s TickTrader platform, where real-time charts and over 1,200 tools support comprehensive analysis.

Here’s a breakdown of the Silver Bullet model:

Entry

- Market Direction and Liquidity Analysis: Before the designated Silver Bullet timeframes, traders perform a detailed assessment of the market direction on higher timeframes, such as the 15-minute to 4-hour charts. This initial analysis is crucial to align their strategies with the market’s overall momentum.

- Identifying Major Liquidity Points: Traders also mark significant liquidity targets during their analysis, such as previous session/day highs and lows. These points are expected to attract significant trading activity and thus are critical for planning entry points.

- Formation of Fair Value Gaps (FVG): During the Silver Bullet hours—specifically from 3:00 AM to 4:00 AM, 10:00 AM to 11:00 AM, and 2:00 PM to 3:00 PM EST—traders watch for the market to approach these liquidity points and leave behind a Fair Value Gap. This movement is essential as it indicates a potential inefficiency in price that the market may seek to correct.

- Setting Limit Orders at FVGs: Once an FVG is identified, traders set their limit orders at the boundary of the FVG closest to their intended trade direction. If aiming for a long position, the order is placed at the top of the FVG; for a short position, at the bottom. This method allows traders to potentially enter the market as it moves to ‘fill’ the gap, aligning with the initial momentum assessment and the subsequent market reaction to liquidity levels.

Stop Loss

- Initial Placement: Traders typically place stop-loss orders to potentially manage risk tightly with respect to the FVG’s structure. If trading long, the stop loss might be set just below the low of the candle that forms the FVG; if trading short, just above the high.

- Swing Points: Alternatively, stop losses might also be placed beyond recent swing highs or lows, providing a buffer against market volatility and minor fluctuations that do not affect the overall market trend.

Take Profit

- Targeting Liquidity Points: The common practice for setting take-profit points involves aiming for the next significant liquidity target identified during the preparatory phase.

- Risk-to-Reward Considerations: Many traders set their take-profit goals based on a calculated risk-to-reward ratio, often aiming for at least a 1:2 ratio. This means that for every unit of risk taken, two units of reward are targeted. In terms of pips, traders generally look for at least 15 pips when trading forex and 10 points in indices.

EUR/USD Example

Let’s consider the Silver Bullet in forex. In the provided EUR/USD chart example, a detailed analysis of higher timeframes has established a bearish outlook. Consequently, the focus is on identifying sell trading setups while disregarding potential long setups.

During the 8:00 AM to 9:00 AM GMT window, there’s a noticeable Fair Value Gap (FVG) that forms following a swift rejection from an upward move. This price action reflects a viable entry point for a short position. Traders could place a limit order at the bottom boundary of the candle that initiated the FVG, with a stop loss positioned just above the candle’s high or the nearby swing point high, depending on their risk tolerance. The target for this trade is set at the previous day’s low, which is reached and prompts a short-term reversal in price direction.

Later in the day, between 7:00 PM and 8:00 PM GMT, another FVG develops. Following the same principle, we can enter at the bottom of the FVG. Setting a stop loss above the swing high is considered more prudent than directly above the candle high, which in this case would likely lead to a stop-out due to the tightness of the entry. Since the previous day’s low has already been reached earlier, the next logical target is the low of the US session, aligning with the day’s bearish momentum.

The Bottom Line

The ICT Silver Bullet strategy offers traders a way to combine liquidity concepts, fair value gaps, and session timing into a clear trading framework. While no strategy guarantees results, applying this method with patience and proper risk control may help refine trade entries and improve market analysis.

Those looking to apply these principles in a robust trading environment, may consider opening an FXOpen account and access over 700 markets, low commissions, and tight spreads.

FAQs

What Is the Silver Bullet Strategy in Trading?

The ICT Silver Bullet strategy in trading is a specific, time-sensitive approach designed to capitalise on liquidity and fair value gaps that typically form during key periods of market volatility. Developed by Michael J. Huddleston, also known as ICT, it aims to take advantage of the movements that occur when the market reacts to these gaps during certain hours of the trading day.

What Time Is the Silver Bullet Strategy Valid?

The Silver Bullet strategy is executed during three distinct one-hour windows corresponding to heightened market activity periods. These are:

- London Open Silver Bullet: Occurs from 3:00 AM to 4:00 AM Eastern Standard Time (EST) in winter and from 2:00 AM to 3:00 AM in summer, which is 8:00 AM to 9:00 AM Greenwich Mean Time (GMT) in winter and 7:00 AM to 8:00 AM in summer.

- New York AM Session Silver Bullet: 10:00 AM to 11:00 AM EST (3:00 PM to 4:00 PM GMT).

- New York PM Session Silver Bullet: 2:00 PM to 3:00 PM EST (7:00 PM to 8:00 PM GMT).

How Long Does the Silver Bullet Strategy Last?

As an intraday trading strategy, the Silver Bullet targets quick, short-term trades within specific one-hour windows. The trades are typically intended to be closed by the end of the trading day, capitalising on rapid movements towards and away from liquidity points.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Legend Biotech Corporation 2025 Q4 – Results – Earnings Call Presentation (NASDAQ:LEGN) 2026-03-10

DeFi Insurance Is The Final Frontier Of Onchain Finance

Bob Dylan Is One of Only 2 People To Achieve This Incredible Oscar Feat

-

Business4 days ago

Form 8K Entergy Mississippi LLC For: 6 March

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Ann Taylor

-

News Videos1 day ago

News Videos1 day ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Crypto World21 hours ago

Crypto World21 hours agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Tech5 days ago

Tech5 days agoBitwarden adds support for passkey login on Windows 11

-

Sports5 days ago

Sports5 days ago499 runs and 34 sixes later, India beat England to enter T20 World Cup final | Cricket News

-

Sports3 days ago

Sports3 days agoThree share 2-shot lead entering final round in Hong Kong

-

Sports2 days ago

Sports2 days agoBraveheart Lakshya downs Lai in epic battle to enter All England Open final | Other Sports News

-

Business6 days ago

Business6 days agoGuthrie Disappearance Enters Fifth Week as Family Visits Memorial

-

Politics4 days ago

Politics4 days agoTop Mamdani aide takes progressive project to the UK

-

NewsBeat5 days ago

NewsBeat5 days agoPiccadilly Circus just unveiled ‘London’s newest tourist attraction’ and it only costs 80p to enter

-

Entertainment3 days ago

Entertainment3 days agoHailey Bieber Poses For Sexy Selfies In New Luscious Lip Thirst Traps

-

Business2 days ago

Business2 days agoSearch for Nancy Guthrie Enters 37th Day as FBI Probes Wi-Fi Jammer Theory

-

NewsBeat12 hours ago

NewsBeat12 hours agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Tech22 hours ago

Tech22 hours agoDespite challenges, Ireland sixth in EU for board gender diversity

-

Crypto World6 days ago

Crypto World6 days agoNew Crypto Mutuum Finance (MUTM) Reports V1 Protocol Progress as Roadmap Enters Phase 3

-

Tech5 days ago

Tech5 days agoACIP To Discuss COVID ‘Vaccine Injuries’ Next Month, Despite That Not Being In Its Purview

-

Entertainment5 days ago

Harry Styles Has ‘Struggled’ to Discuss Liam Payne’s Death

-

Business17 hours ago

Business17 hours agoSearch Enters 39th Day with FBI Tip Line Developments and No Major Breakthroughs

-

NewsBeat5 days ago

NewsBeat5 days agoGood Morning Britain fans delighted as Welsh presenter returns to host ITV show