Crypto World

BLSH leaps past Coinbase after 62% spot trading jump in February

Crypto platform Bullish (BLSH), which operates an institutional-only crypto exchange business, climbed into the top three centralized crypto exchanges by spot trading volume for the first time in February, overtaking Coinbase (COIN) as trading activity across the industry slowed, according to CoinDesk Data’s February Exchange Review.

Spot trading volumes on Bullish, which is the parent company of CoinDesk, rose 62.6% month over month to $76 billion, the exchange’s highest monthly total since October 2025. The surge lifted Bullish’s market share to 5.06%, up 2.04 percentage points, making it the third-largest centralized exchange by spot trading volume.

The increase pushed Bullish, which went public on the New York Stock Exchange last year, ahead of Coinbase (COIN), which held a 4.59% share of the spot market during the month.

The milestone comes even as overall activity on centralized exchanges declined. Combined spot and derivatives trading volumes fell 2.41% in February to $5.61 trillion, the lowest level recorded since October 2024, the report said.

The slowdown coincided with subdued volatility in major cryptocurrencies. Despite heavy volatility in the first and last weeks of February, bitcoin spent much of the month trading in a narrow range between $60,000 and $70,000, limiting speculative activity that often drives higher trading volumes.

Spot trading accounted for $1.50 trillion of that total, down 3.01% from January. Derivatives trading fell 2.41% to $4.11 trillion but remained the dominant force, accounting for 73.2% of all trading on centralized exchanges, the report said.

While Binance remained the dominant exchange by a wide margin, recording $331 billion in spot trading volume during February, which represents about 22% market share, its dominance declined to its lowest monthly level since October 2020, suggesting trading activity is becoming more distributed across competing platforms.

Bullish’s rise in the rankings highlights shifting dynamics among centralized exchanges amid intensifying competition. Exchanges are increasingly competing on liquidity, trading incentives, and new product offerings to attract traders during periods of slower market activity. Some have partnered with major U.S. stock exchanges to offer tokenized securities or have launched prediction market trading.

Ripple Labs is pursuing a strategic move to buy back private shares, aiming to provide liquidity for investors and employees while signaling confidence in the company’s long-term value. A Bloomberg report on March 11, 2026, indicated Ripple plans to tender up to $750 million of its private stock, a program that would value the company at about $50 billion. The tender is expected to run through April, aligning a significant repurchase with a financial picture that has not always reflected the company’s ambitions. The plan sits against a backdrop of a volatile crypto market and a company that has been expanding beyond its core payments rails into broader financial services and technology initiatives. Despite a higher valuation from the buyback, Ripple’s publicly traded token price has faced pressure, illustrating the gap between private market activity and public market sentiment.

Key takeaways

- Ripple plans a private share buyback of up to $750 million, pegged to a $50 billion valuation, according to Bloomberg.

- The tender offer is expected to run through April, providing liquidity options for existing shareholders and employees.

- The $50 billion valuation represents a roughly 25% uplift from the valuation implied by its November 2025 fundraising round.

- Ripple has moved to expand beyond crypto with a $1.2 billion acquisition push that includes non-bank prime broker Hidden Road and treasury management system provider GTreasury, signaling a strategic pivot toward broader fintech services.

- Regulatory development remains on Ripple’s radar, including ongoing discussions around a U.S. national trust bank charter, while the company pursues an Australian financial license through a local payments acquisition.

- Market indicators show XRP has declined sharply in recent months, while RLUSD has surpassed $1 billion in market capitalization since its December 2024 launch, and private-market prices for Ripple’s stock have slipped.

Tickers mentioned: $XRP, $RLUSD

Sentiment: Neutral

Price impact: Positive. The buyback, by signaling confidence and offering liquidity at a higher implied valuation, could bolster sentiment among private holders despite the near-term price softness in XRP.

Market context: The move comes in a climate where crypto markets are juggling liquidity constraints, regulatory scrutiny, and ongoing debates about tokenized finance offerings. Regulatory progress, such as national-charter discussions, intersects with corporate strategies aimed at expanding cash flows and diversification beyond a single business line. At the same time, public market dynamics for XRP differ from private market activity for Ripple, underscoring a nuanced landscape for investors and employees holding private shares.

Why it matters

The proposed $750 million share repurchase frames Ripple as a company intent on unlocking liquidity for a dispersed base of investors and employees, a common path for privately held tech and fintech firms seeking to optimize capital structure ahead of broader strategic moves. The buyback values Ripple at about $50 billion, a level that implies strong confidence among insiders and external backers about the firm’s growth potential, even as XRP experiences a sustained price drawdown in public markets. The contrast between private valuation signals and public-market price action highlights how market participants weigh corporate strategy differently from token-based trading dynamics.

Beyond the buyback, Ripple’s foray into broader financial services reflects a deliberate pivot from a crypto payments network toward a more diversified financial technology platform. The company disclosed an $1.2 billion acquisition that encompassed Hidden Road, a non-bank prime broker, and GTreasury, a treasury management system provider. Taken together, the deal signals a push into institutional infrastructure—areas that could broaden Ripple’s revenue streams and reduce reliance on pure crypto volatility. The expansion aligns with the company’s stated intent, in earlier public communications, to explore regulated fintech avenues, including a potential Australian financial license through the acquisition of a local payments firm. These steps suggest a strategy aimed at building a multi-faceted fintech portfolio that can weather fluctuations in crypto market cycles.

On the regulatory front, the U.S. move toward formal national trust bank charters—where Ripple and other crypto firms appear to be advancing—adds a layer of legitimacy that could unlock uses for its stablecoin operations and related services. Ripple’s application to not be a stablecoin issuer for RLUSD, as outlined in OCC communications, indicates a careful negotiation of regulated capabilities. The regulatory environment remains a critical variable for investors assessing Ripple’s long-term viability and for institutions evaluating the risk and reward of engaging with a company pursuing both fintech licenses and crypto-enabled products.

Market data from Ripple’s public footprint show a diversified picture. On the private market side, Forge Global has recorded a more than 9% decline in Ripple’s private share price as of midweek, illustrating that private investors remain wary of near-term price catalysts even as the company pursues strategic expansion. In the public-facing metrics, Ripple reported that it processed more than $100 billion in transactions, with RLUSD surpassing a $1 billion market capitalization since its December 2024 launch, underscoring the platform’s growing footprint in on-chain settlement and stablecoin-enabled programs. XRP, the native token, has fallen more than 53% over the past six months, reflecting the broader risk-off sentiment in crypto markets and the particular volatility of project and token narratives within the space.

The evolving narrative around Ripple—combining liquidity events, strategic acquisitions, and regulated expansion—is shaping how market participants assess the company’s near- and medium-term trajectory. The buyback could serve as a signal to investors that the board views current private valuations as representational of potential upside, while the expansion into institutional infrastructure markets may offer a buffer against crypto-cycle volatility. Yet the path remains contingent on regulatory developments, execution of the acquisitions, and the broader macro backdrop for risk assets within the crypto and fintech spaces.

What to watch next

- Completion of the $750 million tender and any updates on the final valuation implied by the buyback.

- Progress on the Australian financial-license pursuit through the local payments firm acquisition and any regulatory milestones.

- Updates on Hidden Road and GTreasury integration, and how the new assets contribute to Ripple’s revenue mix and risk profile.

- Crypto-market conditions and XRP price movement, particularly as Ripple’s private-market activities unfold alongside public trading activity.

Sources & verification

- Bloomberg report detailing Ripple’s planned $750 million share buyback at a $50 billion valuation and the tender timeline through April.

- Ripple’s statements and public disclosures related to not pursuing an IPO and to regulatory charters, including OCC communications from December.

- Acquisitions of Hidden Road and GTreasury and related financial details reported for the company’s expansion beyond crypto.

- Ripple’s public posts noting transaction volumes, RLUSD market capitalization, and XRP price movements, including X (formerly Twitter) activity.

- Forge Global data reflecting changes in Ripple’s private share price as of midweek.

Ripple’s buyback and growth push reshape its valuation narrative

Ripple’s decision to advance a private share repurchase underscores a broader strategic arc that combines liquidity options for private holders with a deliberate expansion into regulated, non-crypto financial services. The tender, set to unfold through April, arrives alongside a valuation implication of $50 billion, a level that would mark a meaningful uplift from the private-market assessments that followed the November 2025 funding round. The juxtaposition of a rising private valuation against a softer public token price highlights a nuanced dynamic: the market is pricing Ripple’s future cash flows and regulatory prospects differently than its current crypto-market performance would suggest.

The acquisition strategy central to this narrative—covering Hidden Road and GTreasury in a single $1.2 billion move—signals a pivot toward infrastructure and treasury management capabilities that could broaden Ripple’s appeal to institutions and developers seeking integrated fintech services. By embedding itself in areas such as prime brokerage and cash management, Ripple could diversify revenue streams and reduce exposure to episodic swings in the crypto market. This shift mirrors a broader industry trend where crypto firms leverage regulated, utility-focused offerings to stabilize growth trajectories and unlock new monetization channels beyond pure token value appreciation.

Regulatory progress remains a key variable in how this story unfolds. The December determination by the Office of the Comptroller of the Currency to conditionally approve national trust bank charters for several crypto companies marks a meaningful, if conservative, step toward formalizing a path for regulated digital finance. Ripple has specifically stated that its RLUSD-related charter would not position it as a stablecoin issuer, suggesting a hedged approach to tokenized settlement that prioritizes compliance and governance. In parallel, the company’s plan to pursue an Australian financial-license pathway via a local payments acquisition indicates Europe- and Asia-anchored expansion ambitions, potentially creating a bridge between U.S. regulatory developments and international growth opportunities.

Market observers will monitor how the private buyback interacts with ongoing public-market dynamics. The 9% dip in private Ripple shares on Forge Global, alongside XRP’s 53% six-month decline, highlights the split between private investor sentiment and public token performance. Yet the RLUSD program, already surpassing a $1 billion market cap, demonstrates tangible traction in the stablecoin space, hinting at a real-use case that could complement Ripple’s broader platform ambitions. As the tender progresses and regulatory steps materialize, the company’s trajectory could hinge on how effectively it can translate an expanded product slate into sustainable, compliant revenue streams that resonate with institutional and retail participants alike.

Anchorage Digital has taken a strategic stake in Immunefi and its IMU token, tying a U.S.-chartered crypto bank directly into on-chain bug bounty infrastructure for DeFi security.

Summary

- Anchorage Digital invested in Immunefi and purchased IMU, tightening links between a U.S.-chartered crypto bank and one of crypto’s largest bug bounty platforms.

- The deal signals institutions now treat on-chain security as core infrastructure, with Immunefi’s bug bounties positioned as a way to cut exploit tail risk across DeFi and L1s.

- Anchorage can route banks and asset managers toward standardized bounty programs and security SLAs, while Immunefi gains a regulated partner to legitimize IMU’s role in its Security OS.

Anchorage Digital, the first federally chartered crypto bank in the United States, has made a strategic investment in security infrastructure provider Immunefi and purchased its native IMU token, tightening the link between regulated financial institutions and on-chain bug bounty markets. The move underscores how institutional players are increasingly treating protocol security as critical infrastructure rather than an afterthought, especially as capital flows back into higher-risk DeFi and L1 ecosystems.

Immunefi operates one of crypto’s largest bug bounty platforms, linking white-hat hackers with protocols that pay out rewards for disclosed vulnerabilities instead of suffering live exploits. By taking both an equity-style strategic position and exposure to IMU, Anchorage is effectively underwriting the thesis that better-aligned incentives between security researchers and protocols can reduce tail-risk events that destabilize markets and damage institutional confidence. For clients that custody assets with Anchorage, the signal is clear: security infrastructure is becoming part of the investable stack, not just a cost center.

The timing matters. After multiple cycles of bridge hacks, governance takeovers, and oracle failures, institutional allocators have become acutely sensitive to smart contract risk, often demanding audit trails, bug bounty coverage, and clear incident response procedures before deploying size into a protocol. Anchorage’s backing gives Immunefi a regulated, U.S.-chartered partner that can open doors with banks, asset managers, and corporates who require robust counterparties before touching on-chain security workflows. In practice, this could translate into larger, more structured bounty programs and standardized security SLAs around major DeFi and infrastructure projects.

For Immunefi, Anchorage’s involvement also helps legitimize IMU as part of a broader security ecosystem rather than a speculative side token. If the relationship deepens, one plausible path is tighter integration between Anchorage’s custody stack and Immunefi’s bounty coordination layer, allowing institutional clients to pre-commit budgets to security programs or ring-fence funds for rapid response payouts when vulnerabilities surface. Such tooling would mirror traditional cyber insurance and incident-response retainers, but enforced and settled on-chain.

At the ecosystem level, the deal signals a slow but decisive shift: instead of merely insuring against crypto risk from the outside, regulated entities are now buying into the core primitives that reduce that risk at the protocol level. Whether that bet pays off will show up directly in exploit frequency, recovery rates, and the willingness of large, regulated pools of capital to treat DeFi rails as investable infrastructure rather than a speculative side-show.

Travis Hill, chair of the US Federal Deposit Insurance Corporation (FDIC), confirmed that, in his opinion, a law passed in July would not give the agency the authority to guarantee stablecoin deposits.

In remarks prepared for the American Bankers Association (ABA) Washington Summit on Wednesday, Hill said that under rules for the stablecoin payments bill, the GENIUS Act, the FDIC would not allow the government to guarantee deposits once the law was fully implemented. Similarly, stablecoin issuers would be prohibited from representing that the digital assets were FDIC insured, and a proposed plan would stop “pass-through insurance” by third parties.

“If a payment stablecoin arrangement qualified for pass-through insurance, this would mean that if a bank holding the issuer’s reserves in a deposit account failed, the FDIC would insure the deposit account based on the interests of the stablecoin holders, rather than insuring the account as a corporate deposit account eligible for only $250,000 of insurance,” said Hill.

The GENIUS Act, passed by Congress and signed into law by US President Donald Trump in July, established a US regulatory framework for payment stablecoins. The law will be fully implemented 18 months after it was signed or 120 days after related regulations are finalized in agencies like the FDIC and Treasury Department.

Related: Crypto turnaround at Fed as Kraken scores account and Trump nominee goes to Senate

While the FDIC may not be insuring stablecoin holders’ deposits, issuers will be expected to fully back the dollar-pegged coins.

Stablecoin yield debate continues in market structure bill

Hill’s remarks did not include a discussion of the digital asset market structure bill under consideration in the US Senate, where lawmakers and crypto and banking industry representatives have been clashing over how to handle stablecoin yield, tokenized equities, and ethics.

The ABA said in late January that one of several priorities it has this year is to “stop payment stablecoins from becoming deposit substitutes that slash community bank lending by prohibiting paying interest, yield or rewards regardless of the platform.”

The White House has hosted three meetings with industry leaders so far this year to discuss how to move forward on the bill, but it was unclear as of Wednesday if or when it would advance.

Magazine: All 21 million Bitcoin is at risk from quantum computers

Key takeaways:

-

Professional traders remain cautious, pricing low odds for a Bitcoin breakout to $78,000 despite recent ETF inflows.

-

US and Israel-Iran war and soft US labor data offset momentum in Bitcoin ETFs.

Bitcoin options: 17% chance of breaking $78,000

Bitcoin (BTC) reclaimed the $70,000 mark again on Wednesday. However, repeated failed attempts to break above $74,000 over the last five weeks have fueled skepticism. The ongoing US and Israel-Iran war, coupled with disappointing US labor numbers, has only added to the cautious outlook.

Traders are now evaluating whether recent inflows into Bitcoin exchange-traded funds (ETFs) signal an imminent bullish breakout.

While US-listed Bitcoin ETFs saw $414 million in net inflows between Monday and Tuesday, this was insufficient to offset the $576 million in net outflows recorded the previous Thursday and Friday.

Data from the derivatives market suggests that professional traders are skeptical of a significant rally before the end of the month.

Bitcoin call options on Deribit for March 27, which target a $78,000 strike price, traded at $704 on Wednesday. This pricing indicates that whales and market makers see less than a 17% chance of Bitcoin gaining roughly 12% from its current levels.

This cautious outlook is also visible in the futures market, where demand for leveraged long positions remains stagnant.

The annualized premium (basis rate) for monthly Bitcoin futures has stayed below the 4% neutral threshold. Notably, this metric failed to shift even after a 16% four-day rally that peaked with a retest of $74,000 on March 4.

Current onchain and derivatives data point toward indifference rather than an expectation of a sharp crash.

Economic outlook offsets institutional BTC inflows

Professional traders appear wary of sustained BTC price momentum, largely due to a worsening global economy.

Seema Shah, chief global strategist at Principal Asset Management, said that investors are far more focused on how the conflict feeds into inflation, according to Yahoo Finance.

Raymond James strategist Tavis McCourt wrote on Monday that the $25 oil price gain essentially offsets the fiscal benefit from the One Big Beautiful Bill Act, according to CNBC.

McCourt added that after the Gulf War in 1990 and the Russian invasion of Ukraine in 2022, it took about six months for oil prices to get back to where they were before.

The 92,000 job positions cut in the US during February, announced on Friday, vastly disappointed analysts, as consensus anticipated a 55,000 increase. Sentiment further deteriorated on Monday after JPMorgan reportedly reduced the value of private credit loans made to software firms, according to Financial Times.

Regardless of the economic outlook, yield products revolving around Strategy (MSTR US) shares are becoming increasingly supportive for Bitcoin’s price. The company announced a record high daily average price and trading volume, offering opportunities to issue at-the-market share offerings and use the proceeds to buy additional spot Bitcoin positions.

Related: Price predictions 3/11: BTC, ETH, BNB, XRP, SOL, DOGE, ADA, BCH, HYPE, XMR

X user “gumsays” said that Strategy Variable Rate Perpetual (STRC US) adoption would lead to Strategy buying billions worth of Bitcoin per week.

The analysis added that a potential series of ETF inflows could result in sustained institutional demand. Therefore, traders will likely have to wait until after March for Bitcoin to break $78,000.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

The U.S. markets regulators are melding their operations in the places where the duties of the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) overlap, and building a crypto oversight framework is listed among the core aims of a written agreement released on Wednesday.

Most of the objectives of the memorandum of understanding in combining supervision, product approvals and policy interpretations, plus coordinating enforcement actions and providing dual registration, will effect the regulated majority of the crypto sector. But the agreement also specifically listed “Providing a fit-for-purpose regulatory framework for crypto assets and other emerging technologies,” as a top goal.

SEC Chairman Paul Atkins had previewed the MOU in Tuesday remarks, detailing how the agencies are offering contact information for regulated firms to call combined meetings to discuss policy matters and product applications.

“For decades, regulatory turf wars, duplicative agency registrations, and different sets of regulations between the SEC and CFTC have stifled innovation and pushed market participants to other jurisdictions,” Atkins said in a statement on Wednesday. “By aligning regulatory definitions, coordinating oversight, and facilitating seamless, secure data sharing between agencies, we will ensure our rules and regulations deliver the clarity market participants deserve.”

The new agreement says the staff of the CFTC and SEC will meet regularly and share data on mutual interests. That includes enforcement actions, which have historically been pursued independently, sometimes leaving a crypto firm confronted with similar accusations by both agencies. If the two regulators overlap in an enforcement case, they’re agreeing to “confer on potential charges and relief, sequencing of filings, litigation strategy and public communications.”

During the previous administration, other crypto positions of the two agencies sometimes directly contradicted each other, including in how certain assets were being placed in which bucket: securities or commodities.

Now, their enthusiasm for friendly crypto rules is mutual and essentially unopposed, with the CFTC run by a sole Republican chairman on an otherwise empty five-member commission and the SEC led by Atkins and two other Republicans, with the Democrat seats kept vacant.

The chairmen of the agencies were both appointed by President Donald Trump, who arrived in office last year with a new-found enthusiasm for crypto, stemming in part from his own growing business interests. Both Atkins and CFTC Chairman Mike Selig had worked for crypto clients prior to taking their jobs.

MetaMask has integrated the Uniswap API as a core swap provider, routing in-wallet trades through Uniswap v2, v3, v4, and UniswapX across 16+ networks for deeper, CEX-like liquidity.

Summary

- MetaMask now routes swaps through the Uniswap API, tapping v2, v3, v4, and UniswapX liquidity across more than 16 networks directly from the wallet UI.

- The API already underpins routing for Uniswap’s own products plus OKX, Talos, Fireblocks, Anchorage Digital, and Ledger, giving MetaMask users institutional-grade pricing and depth.

- With Uniswap’s protocol volume surpassing 40 trillion dollars, the link positions MetaMask as default EVM wallet and Uniswap as default DEX backend, squeezing centralized venues and rival aggregators.

MetaMask has integrated the Uniswap API as one of its core swap providers, allowing users to route trades directly through Uniswap v2, v3, v4, and UniswapX from within the wallet across more than 16 networks. The move tightens the link between the most widely used self-custodial wallet and the largest on-chain DEX liquidity venue, effectively turning MetaMask into a front-end for Uniswap’s full routing stack rather than just a generic swap aggregator.

According to the announcement, MetaMask selected the Uniswap API based on liquidity depth, pricing efficiency, and infrastructure reliability across supported chains. The same API already powers swap flows for Uniswap Labs’ own products, as well as institutional and retail platforms including OKX, Talos, Fireblocks, Anchorage Digital, and Ledger, giving it a track record with both exchanges and custody providers. For end users, this means tighter spreads and deeper routing for volatile or long-tail assets without leaving the wallet.

The scale is non-trivial: cumulative historical trading volume through the Uniswap protocol has now exceeded 40 trillion dollars, underscoring how much order flow and price discovery sits on its pools. By plugging that liquidity into MetaMask’s native swap UX, the integration effectively reduces friction between retail order flow and DeFi’s largest AMM infrastructure. In practical terms, MetaMask users get a more “CEX-like” experience on-chain: one click to quote and execute across fragmented pools and versions.

For developers, the Uniswap API remains free to integrate, with no subscription or per-call fees; teams can generate API keys via the Uniswap developer platform and tap into the same routing engine now wired into MetaMask. That pricing model keeps barriers low for wallets, fintechs, and trading tools that want industrial-grade routing without building their own infrastructure or paying SaaS-style tolls. Over time, this could consolidate more of the retail swap stack around Uniswap’s infra, even as liquidity at the protocol level remains open and permissionless.

Strategically, the MetaMask–Uniswap link pushes the ecosystem a step closer to a de facto standard: MetaMask as the default EVM wallet, Uniswap as the default DEX backend. For centralized venues and competing aggregators, the risk is that a growing share of high-intent order flow never touches their rails, instead going straight from self-custody into Uniswap liquidity via wallet-native swaps. For users, the incentive is simple: fewer hops, deeper liquidity, and reduced reliance on centralized intermediaries for everyday trading.

Bonuses and features are often the first things players look at when choosing an online casino. They shape the initial experience, influence how far a bankroll stretches, and determine whether a platform feels rewarding over time or just during the first deposit. 888casino and ZunaBet both compete for player attention in 2026, but they do so with very different toolkits. One is a long-established brand operating within traditional frameworks. The other is a crypto-native newcomer that arrived this year with a bonus structure, game library, and reward system designed to outperform what legacy platforms typically offer. Here is how they actually compare when you break down what each one puts in front of players.

888casino: A Familiar Name With a Traditional Approach

888casino has been part of the online gambling landscape since 1997, making it one of the oldest platforms still in operation. It operates under 888 Holdings, a company listed on the London Stock Exchange with licenses from the UK Gambling Commission, Gibraltar Regulatory Authority, and other jurisdictions. The brand carries nearly three decades of recognition and has maintained a steady presence across European and international markets.

The casino library at 888casino covers standard ground. Slots make up the largest portion, joined by table games, video poker, and live dealer experiences. The platform operates its own proprietary software alongside games from external providers, which gives it some exclusive titles not found elsewhere. Total game counts vary by market but generally land in the range of a couple of thousand titles. It is a mature library that covers mainstream categories without pushing into exceptional territory on volume.

888casino also connects to 888sport, the company’s sportsbook product. Football, tennis, basketball, horse racing, and other popular sports are covered with competitive odds. The sportsbook is functional and well-integrated but operates as a companion product rather than a standout feature in its own right.

Welcome bonuses at 888casino have historically been modest compared to some competitors. Offers vary by market and change periodically, but they typically involve a deposit match with a cap that sits well below what many newer platforms now offer. The terms tend to come with standard wagering requirements that players need to work through before any bonus funds become withdrawable.

Payments run through conventional channels. Visa, Mastercard, PayPal, Skrill, Neteller, bank transfers, and other traditional methods handle deposits and withdrawals. Processing times follow the usual patterns — e-wallets are quickest while bank and card methods can take several business days. The system is comprehensive but operates within the standard limitations of traditional financial infrastructure.

888casino rewards loyal players through a VIP program with tiered levels. Players earn comp points through real-money wagering that can be exchanged for bonus funds. Higher tiers offer improved conversion rates, faster withdrawals, and access to exclusive promotions. It is a structured program, which puts it ahead of operators that rely solely on ad hoc promotions, though the actual return rates remain modest compared to what newer platforms are now introducing.

ZunaBet: Bigger Numbers at Every Level

ZunaBet launched in 2026 under Strathvale Group Ltd with an Anjouan gaming license. The team behind it brings over 20 years of combined gambling industry experience, and they used that experience to build a crypto-native platform that challenges established operators on bonuses, features, and player value simultaneously. Everything from the welcome offer to the loyalty program to the payment system was designed to outperform what traditional platforms deliver.

The game library sets the scale immediately. ZunaBet hosts 11,294 games from 63 providers. Pragmatic Play, Evolution, Hacksaw Gaming, BGaming, and Yggdrasil headline the list, while more than fifty additional studios push the variety well beyond what most single platforms offer. Slots dominate the count as expected, but live dealer rooms and RNG table games carry genuine depth. Comparing this to a traditional library of a couple of thousand titles illustrates just how wide the content gap has become between legacy and next-generation platforms.

The sportsbook was built as a full standalone product. Football, basketball, tennis, hockey, and other major global sports get comprehensive market coverage. Esports occupy a permanent position with dedicated markets on CS2, Dota 2, League of Legends, and Valorant. Virtual sports and combat sports extend the offering further. The sportsbook is not an afterthought attached to the casino — it stands on its own merits for players whose primary interest is sports betting.

The welcome bonus immediately distinguishes ZunaBet from more conservative operators. New players can claim up to $5,000 plus 75 free spins across three deposits. The first deposit matches at 100% up to $2,000 with 25 spins. The second matches at 50% up to $1,500 with 25 spins. The third matches at 100% up to $1,500 with 25 spins. The total package dwarfs what most traditional casinos offer and sustains bonus value across three separate deposits rather than concentrating everything into a single moment.

Payments are entirely crypto-based. Over 20 coins are accepted including BTC, ETH, USDT across multiple chains, SOL, DOGE, ADA, XRP, and more. ZunaBet charges no processing fees. Withdrawals move through the blockchain without bank involvement, business hour restrictions, or geographic speed variations. Fast, free, and consistent for every player on the platform.

Native apps cover iOS, Android, Windows, and MacOS. The dark-themed responsive interface loads quickly across all devices. Live chat support operates around the clock.

Bonus Structures: Conservative vs Aggressive

The welcome bonus comparison alone tells a significant story about how these platforms position themselves.

888casino has traditionally kept its welcome offers relatively contained. Deposit matches with moderate caps and standard wagering requirements are the norm. The offers are fine for casual players looking for a small boost, but they do not dramatically extend a new player’s runway or create a compelling incentive to make multiple deposits.

ZunaBet’s $5,000 plus 75 free spins welcome package operates on a completely different scale. The three-deposit structure is particularly notable because it rewards players who stick around rather than just showing up once. Each deposit triggers its own match and its own batch of free spins, creating three separate waves of bonus value rather than a single event. For players evaluating where their first deposits will go the furthest, the math favours ZunaBet by a considerable margin.

Loyalty: Comp Points vs Direct Rakeback

Beyond the welcome bonus, the ongoing loyalty experience determines how much value a platform returns to regular players over time.

888casino uses a comp points system tied to its VIP tiers. Real-money wagering earns points that convert to bonus funds at rates that improve as players climb through the levels. Higher tiers bring perks like faster withdrawals, dedicated account managers, and exclusive promotions. It is a structured system and more transparent than platforms that rely purely on rotating promotions. However, the conversion rates and overall return remain conservative, and the value can feel modest relative to the volume of play needed to reach the upper tiers.

ZunaBet approaches loyalty through its dragon evolution program with six tiers — Squire at 1% rakeback, Warden at 2%, Champion at 4%, Divine at 5%, Knight at 10%, and Ultimate at 20%. A dragon mascot named Zuno evolves alongside the player’s progression. Higher tiers add up to 1,000 free spins, VIP club access, and double wheel spins.

The core difference is the mechanism. Comp points require conversion and the resulting value depends on exchange rates set by the platform. Rakeback is direct — a percentage of your wagering comes back without conversion steps or variable rates. At 20%, the return is substantial and easy to calculate. A player does not need to track points, check conversion tables, or wonder what their loyalty is worth. The number is right there, applied automatically, every session. For regular players who care about maximizing the return on their activity, rakeback at these rates represents a meaningful upgrade over traditional comp point economics.

Payment Speed and Cost

888casino processes payments through conventional methods that work reliably but slowly by modern standards. E-wallet withdrawals are fastest, card and bank methods stretch across multiple business days, and international players may encounter conversion fees depending on their location and currency. It is the standard experience that traditional platforms have offered for years.

ZunaBet eliminates the wait entirely. Crypto withdrawals process on-chain without banks, without card networks, and without fees from the platform. There is no variation in speed based on geography or payment method because there is only one payment channel and it works the same way for everyone. For players who have experienced the difference between waiting days for a traditional withdrawal and receiving crypto within the same session, the choice becomes straightforward.

What the Comparison Reveals

888casino has earned its longevity. Nearly three decades in operation, publicly traded, and licensed across major jurisdictions all speak to a platform with genuine staying power. For players who value brand history, traditional VIP structures, and conventional banking, it remains a reasonable choice with a track record to back it up.

But the specifics of what each platform offers tell a clear story in 2026. ZunaBet’s welcome bonus is several times larger. Its game library is several times bigger. Its rakeback system returns more to players more transparently than comp points can match. Its payment system moves money faster and cheaper than any traditional method available at 888casino.

ZunaBet was designed for a generation of players who evaluate platforms on measurable output rather than brand familiarity. More games, bigger bonuses, better loyalty returns, and faster payments — every metric that directly affects the player experience tilts in ZunaBet’s direction. For anyone making a fresh choice about where to play in 2026, the numbers make a compelling case.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Financial technology company Revolut announced on Wednesday that it has launched a bank in the United Kingdom after receiving regulatory approval from the Prudential Regulation Authority (PRA), a banking and financial services regulator.

Revolut Bank UK will begin offering deposit accounts for individuals and businesses, with eligible deposits up to 120,000 British pounds ($160,958) protected by the Financial Services Compensation Scheme (FSCS), according to the company’s announcement.

The FSCS offers a safety net for customer deposits at banks and other financial institutions, similar to the Federal Deposit Insurance Corporation (FDIC) insurance for US bank deposits up to $250,000.

Existing Revolut UK customers will be rolled over to the new account type gradually, with the process expected to take several months to fully complete, according to the company.

The new bank sets the stage for offering a “wider range” of services in the future, including lending, the company said.

Revolut also applied for a full banking license in Peru and a federal banking charter in the United States in January, as crypto and financial technology companies pivot to become banks, blurring the line between digital and traditional finance.

Related: Revolut makes second attempt at US bank charter, names new CEO for US business

Crypto industry has eyes on banks, but banking industry pushes back

Crypto industry companies are increasingly looking to acquire national bank charters in the US and other regulatory designations that would plug crypto directly into the traditional financial system.

These companies include blockchain developer company Ripple, institutional-grade blockchain infrastructure provider Paxos, and stablecoin issuer Circle.

In March, crypto exchange Kraken was granted a limited-purpose master account with the Federal Reserve Bank of Kansas City, giving the company direct, but limited, access to the Federal Reserve’s payments system.

The approval of Kraken’s limited-purpose master account was a historic first for the cryptocurrency industry.

However, a trade organization representing the banking sector in the US is reportedly considering filing a lawsuit against the Office of the Comptroller of the Currency (OCC) to block crypto companies from acquiring bank charters.

The banking lobby has repeatedly pushed back against yield-bearing stablecoins and crypto companies offering banking services over fears that blockchain-based financial services will erode the market share of traditional banks.

Magazine: Crypto wanted to overthrow banks, now it’s becoming them in the stablecoin fight

The February CPI data came in broadly as anticipated, reinforcing that higher inflation remains a factor but not a surprise driver for markets. Analysts at 21Shares argued that the macro picture had already priced in the March print, shifting attention to how the Federal Reserve would respond. The Bureau of Labor Statistics reported shelter costs rose 0.2% in February, while food climbed 0.4% and energy rose 0.6%; the core measure excluding food and energy rose 0.2%. Those numbers underscore a broad, uneven inflation trajectory. In crypto markets, the Total 3 market indicator — which tracks the broader crypto capitalization outside the two largest assets by market cap — dipped about 1% from an intraday high near $722 billion as traders absorbed the data. For readers tracking the macro narrative, the CPI release keeps the Fed in sharper focus while liquidity remains a driver for risk assets across crypto landscapes. CPI release.

Key takeaways

- The February CPI print aligned with estimates, reinforcing expectations that inflation momentum remains contained but persistent enough to influence policy signaling.

- Macro data priced in, shifting attention to the Fed’s reaction function and whether policymakers will “look through” temporary shocks or tighten preemptively.

- Crypto markets showed resilience, with the broader market excluding the leading two assets dipping about 1% from an intraday peak near $722 billion.

- Near-term Bitcoin price prospects point to a range around $68,000–$74,000, with a breakout above $75,000 potentially lifting the next leg toward $77,000–$80,000.

- Market expectations for near-term policy action remain modest, with roughly 0.6% of traders pricing in a rate cut at the March 18 meeting, per CME FedWatch.

Market context: The CPI outcome intersected with expectations about the Federal Reserve’s policy path, reinforcing a regime where macro data and liquidity conditions increasingly shape asset allocation across crypto markets. As investors parse the data, attention remains on potential ETF flows, liquidity conditions, and regulatory signals that could influence risk-on appetite in the sector.

Sentiment: Neutral

Market context: The broader crypto environment continues to respond to macro cues while traders weigh the durability of trend reversals and the potential for regime shifts in monetary policy. The latest price action sits within a framework of cautious optimism, where a measured CPI path and any dovish pivot from the Fed could catalyze incremental risk-taking among digital-asset traders.

Why it matters

The February CPI numbers anchor expectations for the Federal Reserve’s near-term trajectory, with market participants watching for clues about whether policy will remain restrictive or begin to ease as inflation cools. The quote from Stephen Coltman, head of macro at 21Shares, encapsulates the key debate: will the Fed “look through” a temporary inflation shock or tilt hawkish in anticipation of renewed price pressures? His question captures a central tension in macro markets: policymakers must balance the risk of stale data against the risk that over-tightening slows growth more than necessary. The CPI multipliers, the timing of potential rate cuts, and the path of the Fed’s balance sheet all feed directly into how risk assets, including crypto, are repriced in real time.

On the crypto side, Bitcoin and its peers have shown resilience even as macro indicators flash caution. The broader market—measured by Total 3, which excludes the two largest assets by market cap—has managed to hold a high-water mark even as the broader market cooled slightly after the CPI release. The dynamic is clear: when macro momentum remains supportive and liquidity is plentiful, infrastructure developers, traders, and hedgers position themselves for a range of outcomes. The interplay between inflation data, the Fed’s policy stance, and risk sentiment remains the dominant driver of near-term price action in digital assets, even as structural developments in the sector—such as staking, layer-2 scaling, and DeFi adoption—continue to underpin longer-term value propositions.

From a tactical perspective, the crypto narrative often hinges on price catalysts that align with macro cues. If the CPI prints continue to signal softening inflation and the Fed signals a more accommodative stance, the environment could become conducive to a slow but steady reallocation into risk assets, including crypto. Conversely, if the data surprises higher or the Fed remains steadfast in a hawkish posture, liquidity could tighten and risk appetite could wane, pressing prices lower in the near term. In this context, Bitcoin and Ethereum—each with distinct on-ramps to risk markets and different catalysts (security, scalability, staking yields, and institutional adoption)—will be watched closely as leading indicators of broader sentiment in the sector. Ethereum (CRYPTO: ETH) remains a focal point for investors watching network upgrades and the evolving dynamics of on-chain activity, while Bitcoin continues to serve as the benchmark for institutional sentiment toward digital assets as an entire category.

In the immediate horizon, price action for Bitcoin appears to be constrained within a corridor rather than forming a new uptrend. The market narrative suggests that a sustained break above the $75,000 mark could unlock a phase of consolidation between $75,000 and $80,000, with momentum dependent on macro signals, liquidity availability, and the pace at which policy expectations evolve. Historical patterns show that geopolitical shocks can trigger sharp but often brief rebounds in risk assets, including crypto, as investors reposition portfolios and seek hedges or uncorrelated stores of value. A potential easing cycle in 2026, if it materializes, could further accelerate any durable upside by reducing discount rates on future cash flows and encouraging risk-taking among diversified portfolios. For now, near-term traders appear to be watching for a decisive move beyond key resistance levels while staying mindful of the macro backdrop.

The market’s next phase will hinge on the March 18 FOMC decision and the accompanying dot plot. While the probability of a rate cut is currently modest, any shift in messaging toward a more permissive stance would likely be interpreted as a positive catalyst for both traditional and crypto markets. Investors should remain alert to any new inflation data and to updates in regulatory and ETF-related developments that could alter risk appetite and liquidity dynamics in this evolving space.

What to watch next

- March 18: Federal Reserve meeting outcomes and the accompanying policy statement; assess shifts in the policy stance and the dot plot.

- Bitcoin price signal: monitor whether the price sustains a break above $75,000 and whether it can push into the $77,000–$80,000 range.

- Evidence of sustained liquidity: track ETF inflows, macro liquidity conditions, and funding rates that could affect risk assets including crypto.

- Geopolitical or macro shocks: observe whether external events drive a rapid re-pricing across crypto markets and whether they catalyze follow-on rebounds.

- Regulatory and on-chain developments: continue to watch network upgrades, staking dynamics, and DeFi activity that influence long-term value propositions.

Sources & verification

- U.S. Bureau of Labor Statistics CPI February release and sector breakdowns (shelter, food, energy, core).

- Comments from Stephen Coltman, head of macro at 21Shares, regarding the Fed reaction function and policy signaling.

- CME FedWatch tool for probability of near-term rate cuts and market expectations at the March 18 meeting.

- Price charts and intraday levels referenced via TradingView and reputable price-tracking data for Bitcoin and Ethereum.

Markets digest CPI data as Fed policy looms and Bitcoin eyes a breakout

The February CPI print arrived in line with expectations, reinforcing the view that inflation momentum remains a factor but not a surprise driver for markets. In a briefing that highlighted the breadth of price pressures, shelter costs rose 0.2% in February, food increased 0.4%, and energy advanced 0.6%. The core CPI, which strips out volatile food and energy components, rose 0.2%. These figures, released by the U.S. Bureau of Labor Statistics, reflect a broad inflation path with pockets of resilience in housing and energy alongside more modest gains in some other sectors. Analysts at 21Shares noted that the print is now part of the pricing backdrop for the March data, complicating the path for policy but not delivering an outsized surprise that would upend markets. The crypto space, meanwhile, showed a measure of resilience as Total 3 — the broader market value outside the leading two assets — retraced roughly 1% from an intraday high near $722 billion, underscoring that liquidity and risk sentiment remain critical levers for digital assets in the near term. CPI release.

Market observers at 21Shares framed the data through the lens of the Fed’s reaction function. Stephen Coltman asked whether policymakers will “look through” temporary inflation shocks or tilt hawkish as a precaution, pointing to a central question as officials balance the persistence of price pressures against the evidence of cooling momentum. The answer, to many, will hinge on how the Fed interprets the trajectory of inflation and how aggressively it views the risk of a renewed uptick. The outcome will shape not just traditional asset classes but the risk appetite that propels crypto markets higher or lower in the weeks to come.

Looking at the near-term price action, Bitcoin’s path remains tethered to momentum around major psychological thresholds and resistance levels. In a scenario where the price breaks decisively above the $75,000 mark, bulls could push into a consolidation zone roughly between $75,000 and $80,000, with the potential to test the upper end of that band depending on macro cues and liquidity conditions. If, instead, the market fails to clear that resistance, the asset could consolidate in the lower to mid-$70,000s as traders await clearer signals from policymakers and the broader economy. The relevance of macro factors to crypto is a reminder that while the technology and use cases continue to evolve, the sector remains highly sensitive to the policy and liquidity backdrop that governs all risk assets.

Beyond Bitcoin, Ethereum’s ongoing developments around staking dynamics, network upgrades, and layer-2 scaling will continue to influence demand and on-chain activity. These structural factors can interact with macro signals to shape price trajectories over a longer horizon, even as the near term remains dominated by inflation data and monetary policy expectations. In sum, the CPI data reinforces a delicate balance: a still-elevated inflation backdrop paired with a potential shift in policy signaling could, if realized, unlock new phases of risk-on behavior that bolster crypto markets—provided liquidity holds and macro momentum remains supportive.

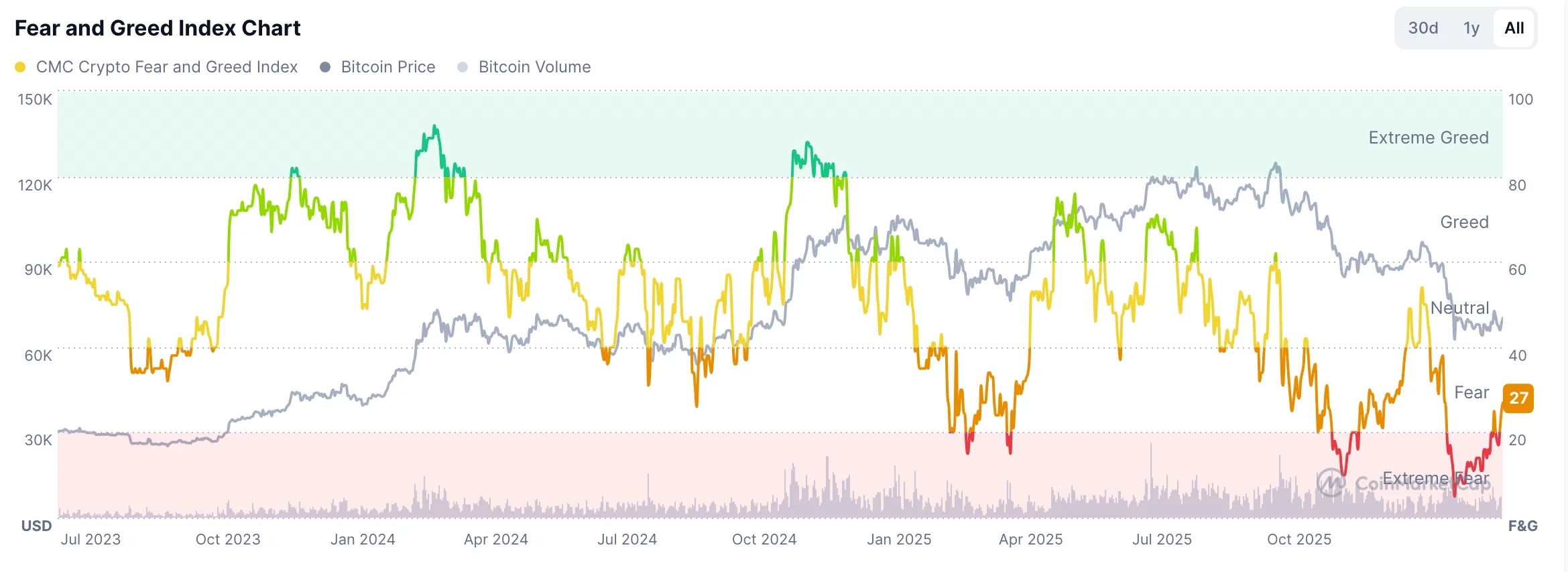

A crypto bull run could be on the horizon after President Donald Trump hinted that the ongoing Iran war will end soon, and as the Fear and Greed Index continues rising.

Summary

- Bitcoin and most altcoins jumped on Wednesday.

- Donald Trump hinted that the Iran war will end soon.

- The Crypto Fear and Greed Index is about to exit the fear zone.

Bitcoin (BTC) price rose to $71,000, while Ethereum was stuck above $2,000. The market capitalization of all coins jumped to $2.41 trillion.

The main reason for the potential crypto bull run is a statement from Trump, who noted that the Iran war will likely end soon, with officials predicting two more weeks of fighting. This means that it may end at the end of this month.

He noted that the war will end as there will be nothing more left to attack. As a result, ending of this war will be bullish for Bitcoin and other altcoins because it will remove one of the main risks in the market. It will also lower the ongoing inflation concerns, which explains why crude oil prices have dropped sharply from the weekly high.

Still, the main risk is whether Iran will stop the war. Analysts believe that it is in its interest to continue fighting for longer to prevent future attacks from the US and Iran. Indeed, Iranian officials noted that they would switch to continuous attacks with the goal of pushing oil prices to $200 a barrel.

The other potential catalyst for a crypto bull run is the Fear and Greed Index has risen gradually. It has jumped from the year-to-date low of 10 to 27. If the trend continues, it will likely move to the neutral zone followed by the green area.

Historically, crypto bull runs normally start whenever the index is rising. Prices then start their bear markets whenever they move to the extreme greed zone. This view mirrors the popular quote by Warren Buffett, where he recommends buying when others are fearful and selling when others are greedy.

My Bitcoin Strategy To Lock In Gains On This Pump

PM was warned of ‘reputational risk’ from Mandelson ties to Epstein, files show

Emphasizes authorities’ belief she was taken against her will from her Tucson-area home

-

Business5 days ago

Form 8K Entergy Mississippi LLC For: 6 March

-

Tech7 days ago

Tech7 days agoBitwarden adds support for passkey login on Windows 11

-

News Videos2 days ago

News Videos2 days ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Ann Taylor

-

Crypto World2 days ago

Crypto World2 days agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Tech16 hours ago

Tech16 hours agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

Sports6 days ago

Sports6 days ago499 runs and 34 sixes later, India beat England to enter T20 World Cup final | Cricket News

-

Politics6 days ago

Politics6 days agoTop Mamdani aide takes progressive project to the UK

-

Business1 day ago

Business1 day agoExxonMobil seeks to move corporate registration from New Jersey to Texas

-

Sports4 days ago

Sports4 days agoThree share 2-shot lead entering final round in Hong Kong

-

Sports4 days ago

Sports4 days agoBraveheart Lakshya downs Lai in epic battle to enter All England Open final | Other Sports News

-

NewsBeat5 hours ago

NewsBeat5 hours agoResidents reaction as Shildon murder probe enters second day

-

Entertainment5 days ago

Entertainment5 days agoHailey Bieber Poses For Sexy Selfies In New Luscious Lip Thirst Traps

-

NewsBeat6 days ago

NewsBeat6 days agoPiccadilly Circus just unveiled ‘London’s newest tourist attraction’ and it only costs 80p to enter

-

Business3 days ago

Business3 days agoSearch for Nancy Guthrie Enters 37th Day as FBI Probes Wi-Fi Jammer Theory

-

Business16 hours ago

Business16 hours agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

NewsBeat2 days ago

NewsBeat2 days agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Tech2 days ago

Tech2 days agoDespite challenges, Ireland sixth in EU for board gender diversity

-

Entertainment7 days ago

Harry Styles Has ‘Struggled’ to Discuss Liam Payne’s Death

-

Tech7 days ago

Tech7 days agoACIP To Discuss COVID ‘Vaccine Injuries’ Next Month, Despite That Not Being In Its Purview