Crypto World

U.S. Inflation Holds at 2.4% in February 2026 Amid Stable Core CPI Trends

TLDR:

- U.S. inflation steady at 2.4% in February 2026, unchanged from January’s rate.

- Core CPI held at 2.5%, marking the lowest reading since 2021, showing easing pressures.

- Energy prices rebounded, with natural gas rising 10.9% and fuel oil up 6.2%.

- Shelter and food costs contributed steadily to monthly CPI changes, supporting stability.

U.S. inflation in February 2026 remained stable at 2.4%, reflecting moderate price growth and balanced sector performance.

Energy and core inflation trends offset other declines, indicating a steady and predictable price environment for the early 2026 economy.

Energy Prices Influence Headline Inflation

Energy costs were a primary factor in February 2026 inflation trends. Overall energy inflation rose to 0.5%, reversing the -0.1% decline from January.

This shift contributed to maintaining headline inflation at 2.4% year-over-year. Gasoline prices declined at -5.6%, a smaller decrease than January’s -7.5%, while fuel oil surged 6.2%, counteracting disinflation in other categories.

Natural gas prices continued strong growth, rising 10.9%, slightly higher than January’s 9.8% increase. These energy price movements reflect ongoing volatility within the sector.

Despite the rebound in energy, overall inflation remained moderate, suggesting that price increases are currently controlled. This stability aligns with market expectations and indicates a predictable inflation environment.

Monthly changes show how energy prices affected headline CPI. Gasoline contributed 0.8%, fuel oil added incremental pressure, and natural gas continued to elevate costs for households and businesses.

Without these energy rebounds, the 2.4% inflation rate might have fallen further. Food and shelter trends further shaped inflation dynamics.

Food prices held at 3.1%, while shelter increased by 0.2% monthly, reflecting consistent demand. Together, these sectors moderated the net impact of volatile energy prices.

Used vehicle prices declined by -3.2%, accelerating from January’s -2% drop, further balancing inflation. The vehicle market continues to normalize after supply disruptions, helping prevent excessive overall price growth.

Producer and consumer indicators support this stabilization. PPI fell slightly to 2.9%, while consumer inflation expectations dropped to 3.0%, reflecting confidence in moderate inflation.

The combination of energy, food, and shelter trends demonstrates how sector-specific movements influence headline inflation. February 2026’s 2.4% rate shows that price growth remains contained despite volatility in select areas.

Core Inflation and Economic Stability

Core inflation, excluding food and energy, remained at 2.5% year-over-year in February 2026. Monthly core CPI increased 0.2%, lower than January’s 0.3%, indicating a modest slowdown in underlying price pressures.

This moderation highlights that services and housing costs are growing steadily, without extreme fluctuations. The lowest core inflation reading since 2021 reflects a stable environment for policy and economic planning.

Shelter, contributing the largest weight in the consumer price index, remained at 3.0% annual growth. Food stayed at 3.1%, while energy’s rebound offset declines elsewhere.

Combined, these movements created a balanced CPI outcome for the month. Used car and truck prices, declining 3.2% monthly, point to a normalization in markets previously disrupted by supply shortages.

These declines also provide relief to consumers, helping maintain overall inflation stability. Historical trends illustrate that 2025 saw inflation peaks around 3.0% in September before gradually falling to 2.4% by early 2026.

This cyclical pattern confirms that inflationary pressures are easing steadily across sectors. Producer Price Index movements also support this view, with PPI easing to 2.9%.

Consumer expectations fell to 3.0%, indicating moderated perceptions of future inflation. The stable headline and core inflation, combined with predictable sector trends, signal that price growth is under control.

Energy rebounds and shelter costs balanced disinflation elsewhere, producing steady and manageable U.S. inflation.

New Zealand’s financial regulator has designated a local currency-pegged stablecoin, NZDD, as not a financial product—a distinction that a leading law firm says could sharpen regulatory clarity for stablecoins and fintech pilots. The Financial Markets Authority (FMA) published the designation in a designations notice tied to its fintech sandbox initiative. The authority stressed that NZDD’s economic substance is that it is not a debt security, not an investment, and that holders do not receive income, interest, or other gains. While the move is product-specific, it signals a pragmatic approach to financial innovation that seeks to balance market access with investor protections.

Key takeaways

- The designation confirms NZDD is not treated as a debt security or an investment under current rules, setting a clearer expectation for issuers and users of currency-pegged stablecoins in New Zealand.

- The ruling stems from the FMA’s fintech sandbox, illustrating how live testing of digital assets can inform regulatory design without broad-brush sweeping conclusions.

- Officials caution that the designation applies to the specific product and version of NZDD described in the notice and does not constitute a blanket policy for all stablecoins.

- The FMA intends to broaden the sandbox with an on‑ramp or restricted license for FinTech firms, a step that could ease market access while preserving protective guardrails that can be adjusted as firms mature.

- Market context signals notable interest in New Zealand’s crypto space: Protocol Theory estimated that about half of the country’s population is either crypto investors or considering investing, while DataCube Research projects the local crypto market could reach roughly $254 billion in value.

Tickers mentioned:

Market context: The designation arrives amid a wider regulatory push to balance innovation with safeguards as the crypto sector matures. Regulators in multiple jurisdictions are carving clearer pathways for digital assets through sandbox tests and phased licensing regimes, with IMF guidelines on stablecoin risks serving as references for policy discussions and industry practices.

Sentiment: Neutral

Price impact: Neutral. The article describes regulatory actions and sandbox plans rather than market moves or price data.

Trading idea (Not Financial Advice): Hold. The development represents regulatory clarity and potential for future licensing, but no immediate market positioning is warranted from these announcements alone.

Market context: The NZDD designation comes as New Zealand trial sites a broader push to align financial innovation with consumer protections. Regulators in various jurisdictions are testing frameworks that support fintech and tokenized assets while delineating when traditional securities rules apply. IMF guidelines on stablecoin risks are among the reference points cited by policymakers and industry observers as they weigh designations, licensing paths, and cross-border standards. For readers following this space, the New Zealand case adds to a growing mosaic of how regulators distinguish stablecoins from conventional debt or equity instruments without stifling innovation.

Why it matters

The FMA’s designation of NZDD as not a financial product marks a deliberate regulatory stance that could influence how issuers approach digital assets within New Zealand’s borders. By clarifying that NZDD is not a debt security and does not promise income, the regulator provides a concrete example of how a currency-pegged stablecoin might be classified in a way that does not automatically trigger securities laws. This distinction matters for issuers seeking to pilot new digital instruments within a governed framework, as it can reduce uncertainty around product design, disclosures, and investor protections required in the sandbox environment.

Law firm MinterEllisonRuddWatts, which advised the NZDD issuer in relation to its sandbox participation, described the move as an important step toward broader regulatory certainty for stablecoins in the country. The firm stressed that the designation is not a general ruling on all stablecoins but a product-specific decision that may serve as a reference point for future iterations and other token designs. The acknowledgment that policy can evolve in parallel with technological innovation underscores a regulated but adaptive approach—one that seeks to embrace fintech growth while maintaining guardrails to guard consumer interests.

Beyond the legal classification, the FMA’s sandbox expansion signals a practical pathway for market participants. Officials have indicated plans to introduce an on‑ramp or restricted license for FinTech firms as part of the sandbox, with the aim of providing regulated access to the market under targeted restrictions that could be gradually relaxed as a company demonstrates capability and compliance. This incremental licensing approach could lower the barrier to entry for crypto-enabled services and related fintech ventures, enabling more experimentation under supervision rather than in a purely speculative, unregulated milieu. The move also aligns with international norms seen in other jurisdictions that favor controlled innovation over outright prohibition, a stance that could attract startups seeking a compliant foothold in the Asia-Pacific region.

Public interest in New Zealand’s crypto ecosystem remains high. A 2024 Protocol Theory report noted that nearly half of the country’s roughly 5.2 million residents are already crypto investors or actively considering investment, underscoring the market’s potential. DataCube Research projects the domestic crypto market could reach about $254 billion in value, a horizon that reinforces why regulatory clarity matters for participants ranging from exchanges and wallet providers to developers building compliant tokenized financial products. All of these threads—the clarity on NZDD, the sandbox expansion, and the broader market milieu—illustrate a regulatory environment that seeks to foster responsible innovation while acknowledging the need for ongoing policy refinement.

As New Zealand continues to refine its approach, observers will be watching for how NZDD’s designation influences subsequent product classifications and licensing decisions within the sandbox. Will other stablecoins or tokenized instruments gain similar determinations, and how quickly will the on‑ramp licenses be rolled out to accommodate growing interest? The answers will shape the next phase of crypto and fintech activity in the country, potentially setting a model for other small economies navigating the balance between innovation and oversight.

What to watch next

- Details of the on-ramp or restricted FinTech license as part of the FMA sandbox expansion, including eligibility criteria and any phased rollout timeline.

- Whether additional stablecoins or digital assets will receive product-specific designations under the sandbox framework.

- Any further guidance from the FMA or related agencies on the regulatory treatment of crypto assets and fintech innovations beyond NZDD.

- Updates to IMF-stated guidelines or international standards that could influence New Zealand’s ongoing regulatory evolution.

Sources & verification

- FMA stablecoin designation notice detailing NZDD’s classification and the sandbox link: https://www.fma.govt.nz/business/legislation/secondary-legislation/designations/financial-markets-conduct-ecdd-holdings-limited-stablecoin-designation-notice-2026/

- MinterEllisonRuddWatts article on the first-of-its-kind designation: https://www.minterellison.co.nz/insights/first-of-its-kind-designation-nzdd-stablecoin-declared-not-a-financial-product

- FMA expands sandbox page announcing broader licensing options: https://www.fma.govt.nz/news/all-releases/media-releases/fma-expands-sandbox/

- IMF guidelines referenced in industry discussion: https://cointelegraph.com/news/imf-guidelines-stablecoin-risks-regulations

- Protocol Theory 2024 report on NZ crypto investor prevalence: https://hub.easycrypto.com/news/the-next-wave-of-crypto-users-in-new-zealand#:~:text=New%20research%20by%20Protocol%20Theory,ownership%20for%20building%20financial%20freedom.

- DataCube Research projection for New Zealand’s crypto market: https://www.datacuberesearch.com/new-zealand-fintech-cryptocurrency-market

Regulatory clarity and market momentum in New Zealand

The case of NZDD demonstrates how regulators can pursue a nuanced recognition of new financial instruments without stifling experimentation. By drawing a clear line between what constitutes a financial product and what does not, the FMA provides a navigable path for issuers, developers, and investors who are eager to participate in a digitized financial landscape. The sandbox framework, with its potential on‑ramp licenses, offers a controlled environment in which firms can test products, governance structures, and consumer protections before expanding into broader markets. In a world where stablecoins and tokenized assets attract increasing policy attention, New Zealand’s approach adds to a growing set of case studies that illustrate how a thoughtful, phased regulatory model can support innovation while maintaining systemic safeguards.

What it means for the wider crypto ecosystem

For developers, exchanges, and fintechs operating in or eyeing New Zealand, the designation and the sandbox expansion could lower friction for compliant product launches and pilot programs. For investors, it signals a regulatory environment that distinguishes between stablecoins with real-world utility and instruments that fall under traditional securities rules. And for policymakers, it offers a live example of how to balance innovation with investor protection, a balance that many jurisdictions continue to strive for as the crypto economy matures and scales. As international dialogue around stablecoins evolves, New Zealand’s measured, evidence-based approach may serve as a practical blueprint for other regulators seeking to modernize financial legislation without compromising safety and resilience.

New Zealand’s financial regulator has ruled that a local currency-tied stablecoin, NZDD, isn’t a financial product, a move a local law firm says is an important step toward regulatory clarity.

The Financial Markets Authority (FMA) said on Wednesday that the new designation for the stablecoin pegged to the New Zealand dollar resulted directly from a financial technology sandbox pilot the regulator is running.

“The economic substance of the NZDD stablecoin is that it is not a debt security, as the NZDD stablecoin is not an investment, and no income, interest or other gain is paid to the NZDD stablecoin holder,” the FMA said.

Law firm pegs designation as a step in the right direction

New Zealand law firm MinterEllisonRuddWatts, which said it acted for NZDD issuer ECDD Holdings in relation to its participation in the FMA sandbox, called the new designation an important step toward regulatory certainty for stablecoins in the country.

“However, it is important to note that the designation relates to a specific product and version of a stablecoin, being the NZDD in the form described in the designation notice and does not constitute a general determination as to the regulatory treatment of all stablecoins,” the firm said.

“The designation signals a pragmatic approach by the FMA to financial innovation that is consistent with developments in comparable jurisdictions and provides a foundation from which further pathways can be developed,” it added.

Sandbox pilot to expand with new license

The FMA also announced it’s planning to introduce an on-ramp or restricted license for FinTech firms as part of its sandbox pilot.

Related: New Zealand bans crypto ATMs in crackdown on criminal cash conversions

“Our financial system is changing faster than ever before. This new type of licence will support firms to get access to the market with some restrictions in place that can be removed as the firm grows,” FMA chief executive Samantha Barrass said.

A 2024 report by Web3 consumer research firm Protocol Theory estimated that nearly 50% of New Zealand’s 5.2 million population are either current crypto investors or are considering investing.

Separately, data analytics firm DataCube Research projects New Zealand’s crypto market will be worth around $254 billion.

Magazine: All 21 million Bitcoin is at risk from quantum computers

TLDR

- Hackers took control of Bonk.fun’s domain and deployed wallet-draining malware on the platform

- Users affected were those who approved a fraudulent terms-of-service prompt following the compromise

- Previously established connections and transactions through external terminals remained unaffected

- Originally branded as LetsBONK, the service went live in April 2025

- By late 2025, Bonk.fun’s market dominance plummeted from 84% to a mere 7%

On March 12, Bonk.fun—a Solana-powered meme coin launchpad supported by Raydium and the BONK token—issued an urgent alert advising users to steer clear of its website after cybercriminals hijacked a team member’s account and embedded wallet-draining malware into the domain.

Tom, the platform’s operator posting from the handle @SolportTom, disclosed the security incident on X and instructed users to avoid accessing the site pending resolution. The official Bonk X account echoed this warning.

According to Tom, the attack exclusively impacted users who approved a deceptive terms-of-service authorization on the compromised platform following the breach. Historical site connections and transactions executed via third-party trading interfaces remained secure.

An investigation into the incident is currently ongoing. While the team hasn’t revealed the total financial damage, Tom indicated that swift detection and rapid community notification helped contain the losses.

“We’re employing every available resource to resolve this matter,” Tom stated, emphasizing that users who’ve placed their trust in the platform over the past eight months remain the team’s top concern.

Launched in April 2025 through a collaboration between the BONK community and Raydium, Bonk.fun enables users to create tokens on Solana without any programming knowledge, utilizing dynamic logarithmic bonding curves. The platform previously operated under the name LetsBONK.

Bonk.fun’s Dramatic Market Share Collapse

In the months following its debut, the platform surpassed Pump.fun to capture 84% of Solana’s launchpad sector by mid-2025. This commanding position proved temporary.

By year-end 2025, Bonk.fun’s market control had crashed to merely 7%, based on analytics from Dune. Monthly revenue tumbled to approximately $84,000, while Pump.fun generated over $720,000 during the equivalent timeframe.

The downturn resulted from unsustainable reward systems and a deceleration in successful token deployments. Pump.fun countered by initiating substantial buyback programs, acquiring Kolscan, and enhancing its infrastructure capacity.

In early 2026, Bonk.fun eliminated creator fees entirely in an attempt to recapture users. This strategy produced a brief revenue surge toward the end of January 2026.

Platform Lost Traction Prior to Security Breach

The rebound was short-lived. Pump.fun introduced fresh incentive programs and recaptured more than 70% of the market by February 2026.

This breach fits within a wider trend affecting the cryptocurrency sector. Phishing operations that manipulate users into authorizing malicious transactions on compromised domains have been escalating. Throughout 2025, fraudulent proceeds from such schemes approached $17 billion.

The Bonk.fun team continues to advise all users against accessing the website until they can verify the platform’s security has been fully restored.

At the time of publication, no specific loss amount from the hack has been publicly disclosed.

Crypto World

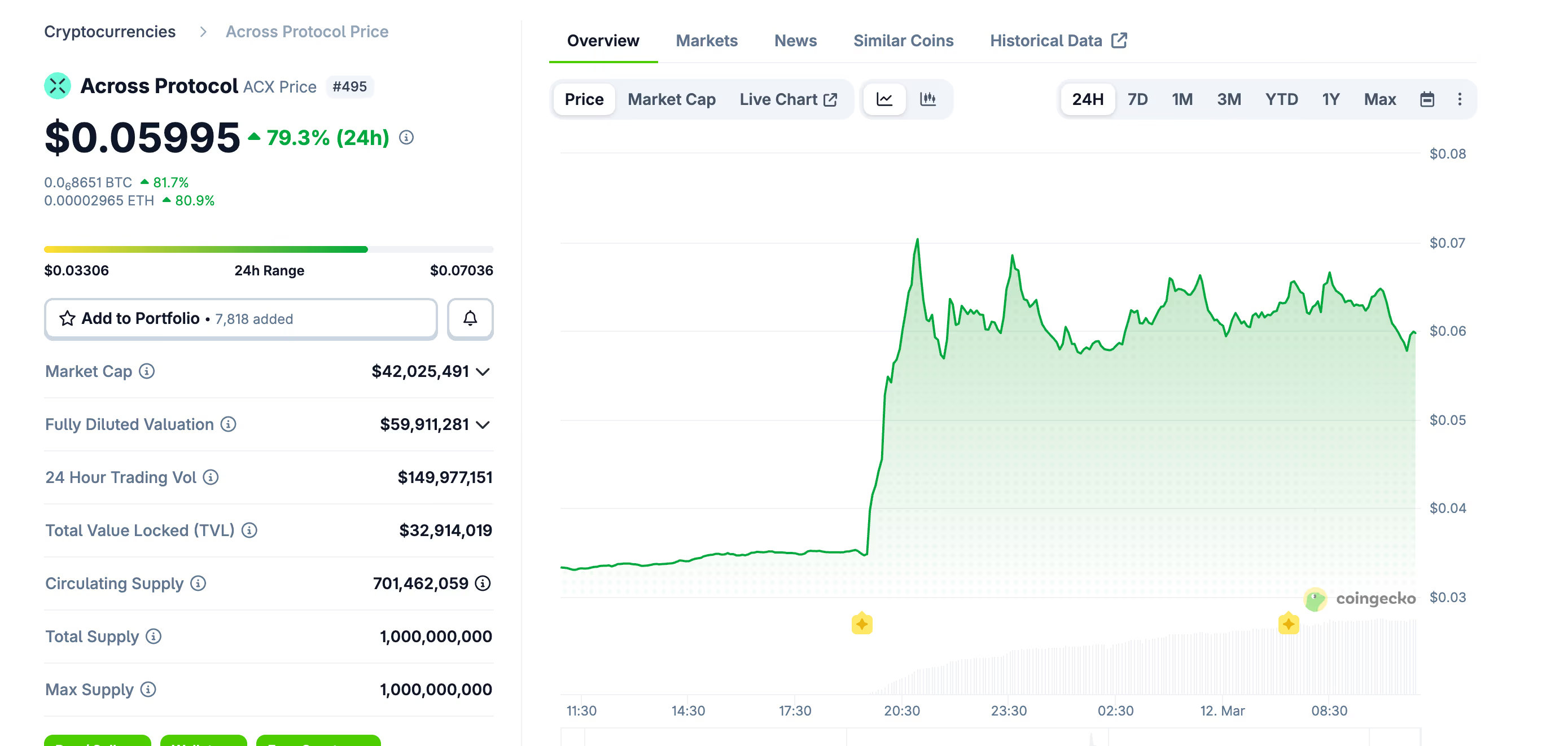

Across’s acx rockets 80%, massively beating bitcoin, on plans to dump its DAO structure

A DeFi protocol just proposed going private as its stewards believe the current DAO structure is creating a hurdle to close institutional deals.

Across Protocol’s ACX token jumped 80% to $0.06 on Thursday after the team behind the cross-chain bridging platform published a ‘temp-check’ proposal to dissolve its token structure and convert into a traditional U.S. C-corporation.

“As Across deepens our work with institutional and enterprise partners, the token and DAO structure has materially impacted our ability to close partnerships and integrations,” the proposal reads. “Transitioning to a traditional legal entity would meaningfully improve our ability to enter enforceable contracts, structure revenue agreements, and deliver more value to Across stakeholders.”

“At current ACX valuations, we believe the Across Protocol is significantly undervalued. The proposed structure gives us an opportunity to explore new ways to foster growth while acting in the best interests of the broader Across community.”

A temp check in DeFi governance is essentially a non-binding poll that gauges community sentiment before a formal vote. It lets the team see whether there’s enough support to proceed as an official governance proposal, which is then voted on by token holders.

The move would give token holders two choices: exchange their ACX for equity in the new company, or sell their tokens for USDC at $0.04375, a 25% premium to the previous 30-day average trading price.

The token was trading at roughly $0.033 before the proposal went live. The immediate surge to $0.07 before settling around $0.06 reflects the market pricing in the buyout floor, though the current price already sits well above the proposed $0.04375 buyout, suggesting traders are betting on either a higher offer or that the equity option is worth more.

In comparison, BTC is currently trading flat, according to CoinDesk market data. The CoinDesk 20, which measures the performance of the largest digital assets, is also trading flat.

The mechanics are straightforward. A new entity called “AcrossCo” would hold all protocol IP and manage development. Token holders above 5 million ACX could convert to equity directly.

Smaller holders could access equity through a no-fee SPV structure with a minimum of 250,000 ACX, roughly $10,000 at current prices. Everyone gets treated equally at a 1:1 token-to-share ratio regardless of size.

Those who don’t want equity get the USDC buyout at the 25% premium. The buyout window would open within three months of the proposal passing and stay open for six months, funded by the protocol’s liquid assets.

A community call is scheduled for March 18, formal discussion runs through March 25, and a Snapshot vote would follow on March 26. If it passes, the conversion would begin in early April.

Is the DAO vision dead?

DeFi proponents spent years arguing that tokens and DAOs were superior to traditional corporate structures for building decentralized infrastructure.

Across is one of the first protocols to publicly argue the opposite, that the token structure is actively holding back growth and that a C-corp would deliver more value to the same stakeholders.

Risk Labs acknowledged the token has been “significantly undervalued” and described the proposal as a chance to “double down on Across” through a structure that institutional partners actually understand.

The 24-hour trading volume of $149 million is roughly 3.5 times the token’s market cap, reflecting the intensity of speculative interest around the proposal.

Whether that interest translates into support for the conversion or simply a trade on the buyout premium is what the next two weeks of governance discussion will determine.

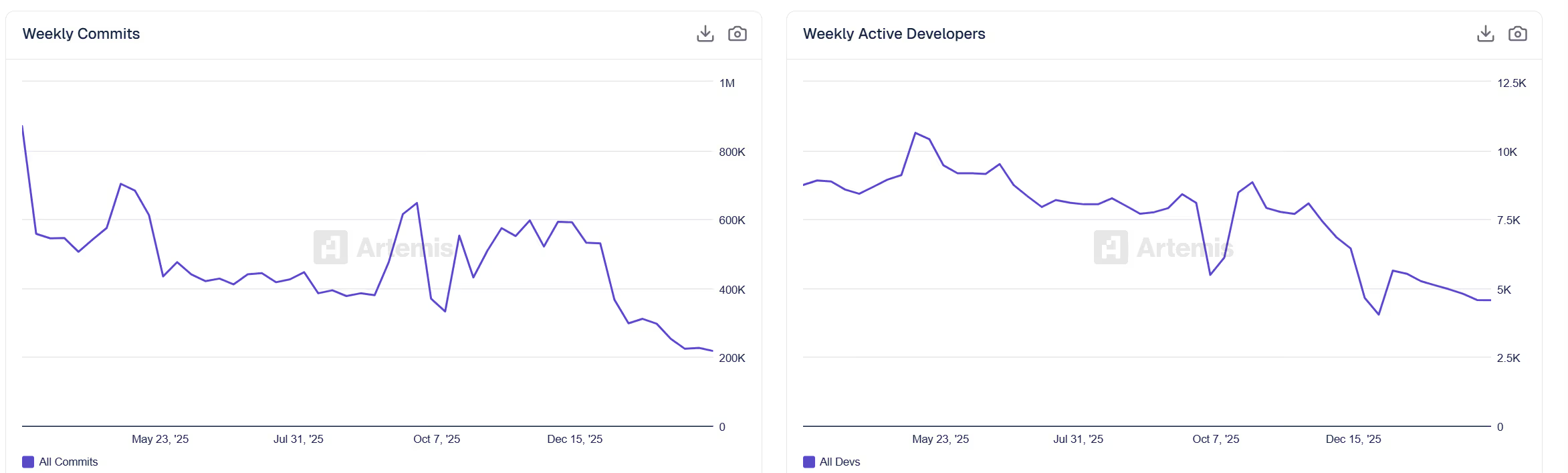

Blockchain ecosystems are losing developers across the board while artificial intelligence projects dominate growth on GitHub, the world’s largest platform for hosting and collaborating on software code.

Weekly crypto commits (publishing new code) to repositories have fallen roughly 75% since early 2025, dropping from about 850,000 to 210,000, while active developers declined 56% to around 4,600, according to data from analytics platform Artemis.

Repositories track where developers are writing code, building tools and launching new projects, they offer one of the clearest signals of where software innovation is happening.

The contraction stands in stark contrast to the broader software ecosystem. GitHub added about 36 million developers in 2025 alone, bringing its global base to more than 180 million, with platform-wide commits rising roughly 25% year over year, according to GitHub’s Octoverse report.

Much of that growth is flowing into artificial intelligence. GitHub now hosts more than 4.3 million AI-related repositories.

The number of repos importing large language model software development kits surged about 178% to more than 1.1 million over the past year, while generative AI projects now attract more than 1 million monthly contributors.

The numbers suggest developers are reallocating time toward AI infrastructure rather than blockchain.

Repositories using Jupyter Notebooks, commonly used for machine learning experimentation, grew about 75%. Dockerfile repositories used to deploy AI applications jumped roughly 120%. TypeScript, the programming language underpinning much of the modern web and many AI tools, overtook Python and JavaScript to become GitHub’s most-used language after gaining more than 1 million contributors in a single year.

Within crypto, the decline is broad but uneven.

Ethereum’s weekly active developer count fell 34% over three months to 2,811, according to Artemis. Solana shed 40% to 942 developers. Base, the Coinbase-incubated Layer 2 that was among 2024’s fastest-growing ecosystems, dropped 52% to 378 developers.

Newer chains that attracted speculative interest during last year’s bull market are faring worst. Aptos lost about 60% of its developers, BNB Chain commits plunged 85%, and Celo fell 52%.

The only category of meaningful size still growing is wallet infrastructure, which rose about 6% to 308 weekly active developers.

Still, the data suggests crypto may be consolidating rather than collapsing.

Electric Capital’s annual developer report shows the sector peaked at roughly 31,000 monthly active developers in 2022 before falling to about 23,600 in 2024, with estimates suggesting further declines to around 18,000 by mid-2025.

The composition of the remaining workforce is also changing. Developers with more than two years of tenure grew about 27% year over year and now produce roughly 70% of commits. The exodus is concentrated among part-time contributors and newcomers with less than 12 months of experience, a group that declined 58% in one tracking period.

Crypto development has historically followed market cycles, and activity could rebound if another bull market draws builders back.

But previous downturns offered fewer alternatives for displaced developers. In 2025, generative AI represents a rapidly expanding frontier with deep venture funding and immediate commercial demand, raising the question of whether this cycle’s talent drain proves harder to reverse.

Stablecoin yield providers will inject more capital into the US banking system, argues White House Council of Advisors for Digital Assets executive director Patrick Witt, amid debate over whether stablecoin yields will draw deposits away.

“Foreigners exchange local currency for stablecoins from a US-based issuer,” Witt said in an X post on Wednesday, adding that “global demand for USD is massive.”

“That is net new capital entering the American banking system,” Witt said. Most US stablecoin issuers hold US dollars or US Treasuries to back each token issued.

Banking and crypto industry clash over stablecoin yields

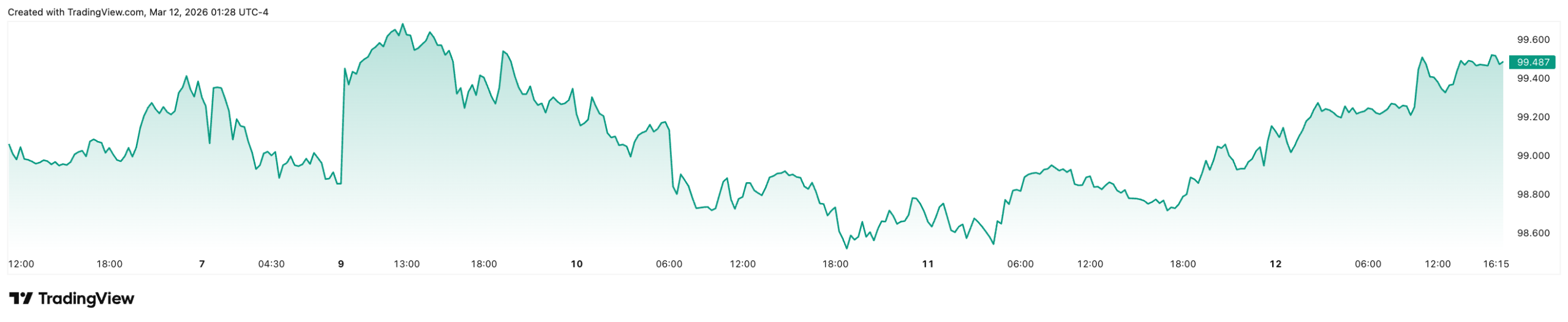

The US dollar index, which tracks the strength of the dollar against a basket of major currencies, fell to its lowest level in four years on Jan. 28, at 95.818, according to TradingView. It has since recovered 3.80% to 99.468.

It comes as the debate between crypto firms and US banks continues to heat up over the US CLARITY Act, aimed at providing the industry with clearer regulation, over whether allowing stablecoin yields will pull deposits out of traditional banks.

Major US bank Standard Chartered recently estimated in a research note that increasing stablecoin adoption could lead to US bank deposits decreasing “by one-third of stablecoin market cap.”

However, Witt argued that what’s often “lost” in the GENIUS and CLARITY Act discussions is how GENIUS-compliant stablecoins “will actually lead to deposit inflows.”

Community banking exec causes controversy in crypto industry

On Friday, the Independent Bankers Association of Texas president Christopher Williston said that making concessions in the CLARITY Act debate would risk harming local lending and economic production, prompting backlash from the crypto community.

“It’s simply impossible to roll over in the fight for liquidity that powers the economies of the places we call home,” he said.

Related: Republican opposition to CBDC could hold up housing affordability bill

Zero Knowledge Consulting founder Austin Campbell responded that “If community banks and crypto can’t find a way to work together, we already know who the winners are… It is the big banks.”

Witt also chimed in on this debate, saying it “feels like I’m watching an arsonist threaten to burn down their own home.”

Magazine: All 21 million Bitcoin is at risk from quantum computers

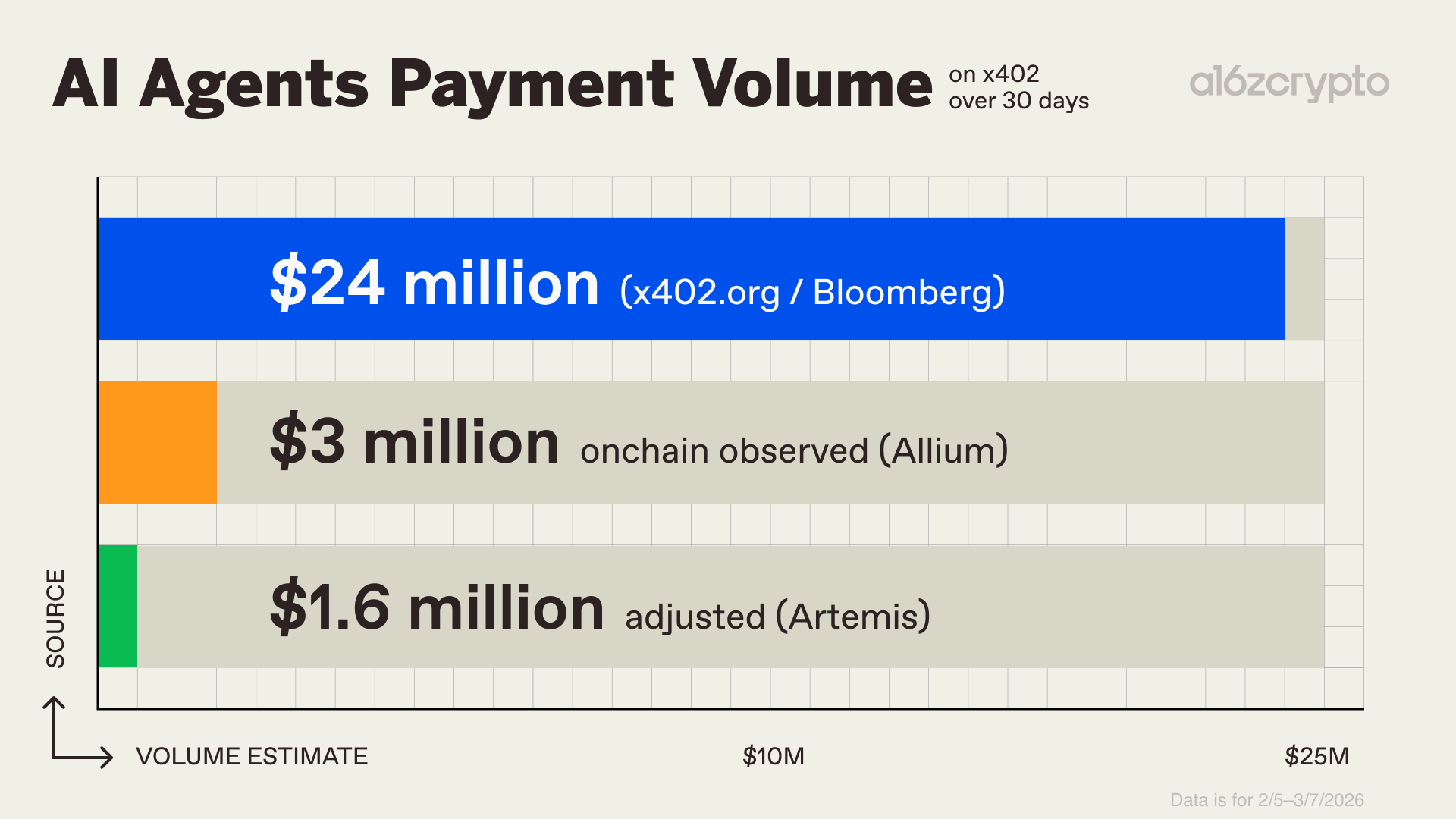

Payment transaction volumes among artificial intelligence agents are more than 90% lower than reports suggest, but crypto giants are pouring billions into building the infrastructure around it.

AI agents are starting to buy things, but “the numbers are inconsistent,” Andreessen Horowitz (a16z) partner Noah Levine wrote in an X post on Wednesday.

He said a Bloomberg article on Saturday reported that AI agents made $24 million in payments over a 30-day period, citing data from x402.org.

Levine said that data from Allium Labs shows there have been roughly $3 million in AI agent transactions over the same period. Filtering out wash trades shrinks the estimate to around $1.6 million, he added, adding that it is still very early days.

“The gap tells you how early-stage even the measurement infrastructure is.”

Levine said that most of the AI payment activity is around developer tools. Firecrawl, a platform that turns websites into AI-ready data, sells web scraping for 1 cent per query, Browserbase, an AI-centric web browser, sells browser sessions, while AI image platform Freepik sells image generation.

“These companies all accept cards, but x402 lets a developer or agent try the tool once without committing to a subscription,” Levine noted.

x402 is a simple payment standard developed by Coinbase that lets AI agents automatically make payments over the internet.

Agentic payments protocol adoption is growing

Levine noted that major payment and internet companies such as Stripe, Cloudflare, and Vercel have integrated x402, while Google has embedded the system into its agent payments protocol.

He added that the $1.6 million in volume “is not a big number, but the infrastructure being built around it is.”

“None of them are betting on $1.6 million a month. They are betting on what the number looks like when agents become the default buyer.”

Related: Alchemy introduces autonomous payment rails for AI agents on Base

Levine said that while humans remain involved, interactions occur through agentic platforms like Claude Code and the OpenClaw personal AI assistant, making transactions semi-autonomous.

Coinbase’s x402 Facilitator Launches on Polygon

Meanwhile, Coinbase announced on Thursday that its x402 Facilitator is adding support for the Ethereum layer-2 network Polygon, allowing developers to accept payments of the stablecoin USDC (USDC) on Polygon, Base, and Solana.

“Networks optimized for quick settlement and minimal fees are essential to make these machine-to-machine payments viable,” it stated.

“Very soon, there are going to be more AI agents than humans making transactions,” Coinbase CEO Brian Armstrong said on Monday.

Magazine: Crypto loves Clawdbot/Moltbot, Uber ratings for AI agents: AI Eye

India’s premier investigative agency, the Central Bureau of Investigation, has arrested Ayush Varshney, co-founder and chief technology officer of Darwin Labs Private Limited, in connection with the alleged GainBitcoin crypto fraud.

Summary

- The Central Bureau of Investigation arrested Ayush Varshney, co-founder of Darwin Labs, in the GainBitcoin fraud probe.

- Investigators say Darwin Labs helped build technical infrastructure linked to the alleged scheme, including the MCAP token and GBMiners platform.

- Varshney was intercepted at Mumbai airport while allegedly attempting to leave India after a Look Out Circular was issued.

CBI arrests GainBitcoin scam suspect at Mumbai airport

The case relates to the GainBitcoin scheme allegedly operated by Variabletech Pte. Ltd., which investigators say functioned as a Ponzi-style investment program that promised unusually high returns to participants who invested in cryptocurrency mining packages.

According to the CBI, funds collected from investors were later misappropriated.

Authorities are investigating the case under several provisions of the Indian Penal Code, including criminal conspiracy, criminal breach of trust and cheating, along with provisions under the Information Technology Act, 2000.

The probe stems from a December 2023 directive by the Supreme Court of India ordering that multiple complaints linked to the GainBitcoin scheme be consolidated and investigated by the CBI as the central agency.

Investigators say Darwin Labs and its co-founders — including Varshney, Sahil Baghla and Nikunj Jain — played a role in the technical development of components associated with the scheme.

These included the design and deployment of a crypto token known as MCAP and its associated ERC-20 smart contract.

Indian authorities allege the firm also built the underlying technological infrastructure used in the operation, including the Bitcoin mining platform GBMiners.com, a bitcoin payment gateway, a crypto wallet known as Coin Bank and the GainBitcoin investor portal.

Varshney had been absconding during the investigation, prompting authorities to issue a Look Out Circular against him. Immigration officials intercepted him at Mumbai airport on March 9 while he was allegedly attempting to leave the country.

He was subsequently taken into custody by the CBI and formally arrested on March 10.

The GainBitcoin case is considered one of India’s largest crypto-related fraud investigations, involving thousands of investors across multiple jurisdictions.

Wells Fargo has filed a trademark application for “WFUSD,” sparking speculation that the U.S. banking giant may be exploring a blockchain-based payment token or stablecoin.

Summary

- Wells Fargo filed a trademark for “WFUSD,” covering crypto-related payment and digital asset services.

- The move may signal exploration of a bank-issued stablecoin or blockchain-based settlement token.

- The filing comes as Wall Street banks prepare for clearer U.S. stablecoin regulation and expanding digital asset adoption.

According to the filing, the mark covers financial services tied to digital assets, including cryptocurrency-related payments and electronic financial transactions.

While Wells Fargo has not announced a product tied to the name, the application has raised the possibility that Wells Fargo could be preparing a dollar-pegged digital asset.

If launched, WFUSD would place the bank among a growing group of major financial institutions experimenting with blockchain-based settlement tools and tokenized payments. Banks have increasingly explored digital tokens as a way to move funds instantly and reduce costs in cross-border or institutional transfers.

The move would also reflect a broader trend of Wall Street firms expanding their crypto strategies. For example, JPMorgan Chase previously launched its blockchain-based payment token, JPM Coin, to facilitate institutional transactions across its internal network.

A potential stablecoin from Wells Fargo could emerge as regulatory clarity around digital dollar tokens improves in the United States. Policymakers have been working toward frameworks that would place stablecoin issuers under stricter oversight, a development that many analysts believe could favor large regulated banks entering the market.

If regulatory rules solidify, traditional financial institutions may become major issuers of dollar-backed digital assets, competing with established stablecoin providers such as Circle and Tether Limited.

For now, the WFUSD filing does not confirm a forthcoming launch, but it shows how major banks are positioning themselves for a financial system increasingly influenced by blockchain-based infrastructure.

Prediction market Kalshi has sued regulators in the US state of Iowa, claiming it did so as there was a risk of an impending enforcement action over its sports event contracts.

Kalshi sued Iowa Attorney General Brenna Bird, along with the Iowa Racing and Gaming Commission and its board, in an Iowa federal court on Wednesday, claiming there “is a substantial risk” Bird would bring enforcement action to block the company’s event contracts.

In its complaint, Kalshi said a company representative met with Bird for what was believed to be a discussion about a tax bill currently under consideration in the Iowa legislature.

“Instead, he [Kalshi’s representative] was greeted by a panel of attorneys, including Iowa’s Solicitor General, who proceeded to ask a series of pointed questions challenging whether Kalshi’s federally regulated offerings ran afoul of (preempted) Iowa state law,” Kalshi claimed.

After the meeting, Kalshi said it contacted a representative for the Attorney General on Tuesday “to seek assurances that the Iowa AG did not intend to bring an enforcement action against Kalshi.”

“The representative did not provide such assurances,” Kalshi said. “To the contrary, the official said in writing that ‘we will not give any assurances about potential future enforcement.’”

Cointelegraph contacted Bird’s office and the Iowa Racing and Gaming Commission for comment.

Prediction markets fight states over sports contracts

Kalshi’s lawsuit against Iowa is the company’s latest legal action targeted at a US state regulator over whether it can offer event contracts across the US.

In the latest lawsuit, Kalshi argued that “federal law preempts Iowa from subjecting Kalshi to state law,” and as a designated contract market, it is subject to the “exclusive jurisdiction” of the Commodity Futures Trading Commission.

The company has made a similar argument in multiple court cases with other state gambling regulators over the legality of sports event contracts.

Related: US Senate bill targets prediction markets on war and assassinations

Many state regulators have alleged that the contracts, which allow users to bet on the outcome of sporting events, are gambling, subject to separate state-level laws, and are offered without a license.

Federal courts have differed in their response to the lawsuits.

On Monday, an Ohio federal court denied Kalshi’s request to block Ohio regulators from taking action against its sports contracts, saying the company failed to show that they were subject to the CFTC’s jurisdiction.

A federal court in Massachusetts blocked Kalshi from offering event contracts in the state earlier this year, and Nevada sued the company last month after an appeals court knocked back Kalshi’s bid to stop the state from taking action.

Federal courts in New Jersey and Tennessee, in contrast, have sided with Kalshi to temporarily block state regulators from taking action over the company’s sports event contracts.

Magazine: How crypto laws changed in 2025 — and how they’ll change in 2026

Audi driver from Stokesley ploughed into car in Darlington

WhatsApp Launches Preteen Accounts That Adds Safeguards, Require Parent Management to Use

NZDD Stablecoin Is Not a Financial Product

-

Business6 days ago

Form 8K Entergy Mississippi LLC For: 6 March

-

News Videos3 days ago

News Videos3 days ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Ann Taylor

-

Crypto World3 days ago

Crypto World3 days agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Tech24 hours ago

Tech24 hours agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

Sports7 days ago

Sports7 days ago499 runs and 34 sixes later, India beat England to enter T20 World Cup final | Cricket News

-

Politics6 days ago

Politics6 days agoTop Mamdani aide takes progressive project to the UK

-

Business2 days ago

Business2 days agoExxonMobil seeks to move corporate registration from New Jersey to Texas

-

Sports4 days ago

Sports4 days agoBraveheart Lakshya downs Lai in epic battle to enter All England Open final | Other Sports News

-

Sports4 days ago

Sports4 days agoThree share 2-shot lead entering final round in Hong Kong

-

NewsBeat13 hours ago

NewsBeat13 hours agoResidents reaction as Shildon murder probe enters second day

-

NewsBeat7 days ago

NewsBeat7 days agoPiccadilly Circus just unveiled ‘London’s newest tourist attraction’ and it only costs 80p to enter

-

Entertainment5 days ago

Entertainment5 days agoHailey Bieber Poses For Sexy Selfies In New Luscious Lip Thirst Traps

-

Business4 days ago

Business4 days agoSearch for Nancy Guthrie Enters 37th Day as FBI Probes Wi-Fi Jammer Theory

-

Business23 hours ago

Business23 hours agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

NewsBeat2 days ago

NewsBeat2 days agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Tech3 days ago

Tech3 days agoDespite challenges, Ireland sixth in EU for board gender diversity

-

Tech7 days ago

Tech7 days agoACIP To Discuss COVID ‘Vaccine Injuries’ Next Month, Despite That Not Being In Its Purview

-

Tech2 days ago

Tech2 days agoChatGPT will now generate interactive visuals to help you with math and science concepts

-

Business2 days ago

Business2 days agoSearch Enters 39th Day with FBI Tip Line Developments and No Major Breakthroughs