Crypto World

Can Hyperliquid price rally above $40 as oil perps trading surge?

Hyperliquid price rallied over 8% on Thursday as demand for oil futures on the platform continued to hold steady on the platform.

Summary

- Hyperliquid price rallied to a four-week high of $37.3 on Thursday, led by a surge in oil perps trading activity on the derivatives platform.

- HYPE has also confirmed a bullish reversal pattern on the 4-hour chart.

According to data from crypto.news, Hyperliquid (HYPE) price shot up 8% to a four-week high of $37.3 on Thursday, March 12. At this price, the token is up 45% from its February low and 81% higher than its lowest point this year.

HYPE price jump came along with a jump in trading volume, which rose 42% over the past 24 hours to around $437 million. Its market cap was settled at $8.86 billion.

CoinGlass data shows that its open interest has risen by 10%, suggesting that the major catalyst for its recent gains has come from the derivatives market, with traders opening more positions on the futures market.

A large share of this surge has been driven by activity in energy markets, especially the WTI perpetual, which tracks West Texas Intermediate crude oil. Oil prices have recently surged to four-year highs amid geopolitical tensions in the Middle East involving the U.S., Israel, and Iran.

Reports indicate that Iran has threatened to block the Strait of Hormuz, a key maritime chokepoint. Iranian officials have noted that they would shift from reciprocal responses to continuous pressure as they attempt to push oil prices to as high as $200.

Investors are concerned about rising inflation as a result of surging oil prices. However, derivative traders were quick to capitalize on the volatility. Notably, WTI oil futures have become the most active HIP 3 contract on the platform, surpassing even precious metals like gold and silver, which had earlier dominated activity.

Open interest in the oil-linked contract has also grown significantly in the period. At the same time, the HIP 3 permissionless perpetuals market on Hyperliquid has recorded more than $1.2 billion in total open interest.

Besides the energy sector, Hyperliquid price also seems to have received a boost from traders turning to the platform as a 24/7 venue to speculate on geopolitical developments, particularly when traditional exchanges such as the CME and ICE are closed for the weekend or after hours.

On the 4-hour chart, Hyperliquid price has confirmed a breakout from an inverse head and shoulders pattern that had been forming since mid-February this year. When such a pattern is confirmed, it typically tends to signal a bullish reversal. In the case of Hyperliquid, it seems to have further strengthened the uptrend.

As such, HYPE is likely to continue its uptrend past the $40 psychological resistance level to $41.7, a target calculated by adding the height of the inverse head and shoulders formed to the price point at which the pattern was confirmed.

The MACD indicator suggested that bulls were still in control of the market with the MACD lines trending upwards and above the zero line. At the same time, the Chaikin Money Flow index showed a positive 0.16 reading, a sign that capital was flowing into the market, helping sustain the ongoing bullish momentum.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

TLDR

- Nomura initiated a Buy rating on NIO with a $6.60 price objective, suggesting approximately 34% potential gains from current trading levels

- Macquarie increased its price objective to $6.50 while maintaining an Outperform stance following fourth-quarter 2025 earnings

- Fourth-quarter revenue climbed 76% annually and 59% sequentially to reach RMB34.7 billion

- Vehicle gross margin expanded to 18.1% during Q4, compared to 13.1% in the prior-year period

- NIO projected Q1 2026 vehicle deliveries between 80,000 and 83,000 units, with revenue expectations exceeding analyst estimates

The Chinese electric vehicle manufacturer Nio has experienced an eventful week. Following the release of impressive fourth-quarter 2025 financial results, the company secured multiple analyst upgrades and elevated price objectives from prominent Wall Street firms.

The standout metric proved difficult to overlook. Fourth-quarter total revenue reached RMB34.7 billion, representing a 76% increase compared to the same quarter last year and a 59% jump from the previous quarter. Such robust expansion typically captures market attention.

Nomura made the boldest move, elevating NIO from a Neutral stance to Buy. The investment bank established a $6.60 price objective, reduced from its earlier $8.40 forecast, yet still suggesting roughly 34% upside potential from the stock’s recent trading level around $4.94.

The brokerage highlighted two consecutive quarters of operational improvements, emphasizing increased vehicle deliveries and enhanced expense management as catalysts for stronger profitability. Nomura now anticipates NIO will achieve non-GAAP operating profit breakeven during 2026.

Despite reducing delivery projections for 2026 and 2027 — acknowledging intensified competition within the EV sector — Nomura still forecasts vehicle deliveries will expand at approximately 25% compounded annual growth between 2025 and 2028. Revenue expansion is anticipated at roughly 21% during the identical timeframe.

Gross margin projections for 2026 and 2027 received upward revisions, while operating margin estimates were boosted by over 3 percentage points for both fiscal years. This represents a substantial reassessment of the company’s cost efficiency.

Enhanced Profitability Fuels Positive Analyst Sentiment

Macquarie similarly elevated its price objective, advancing to $6.50 from $6.10, while preserving its Outperform recommendation. The firm identified vehicle margin expansion as the primary narrative.

Vehicle margin reached 18.1% during Q4 2025, climbing significantly from 13.1% during the comparable quarter one year prior. The recently launched ES8 model received credit for contributing substantially to that improvement. Additional sales margin widened to 11.9% from merely 1.1% in Q4 2024.

NIO also reduced R&D expenditures through workforce optimization and intends to maintain quarterly R&D costs within the RMB2.0 billion to RMB2.5 billion range. The manufacturer generated positive operating cash flow during the quarter, which Macquarie noted reduces future capital-raising requirements.

Macquarie did reduce its fiscal 2026 volume projection by 8%, acknowledging subdued near-term demand and escalating competition within the EV SUV category from rivals including Li Auto, XPeng, Xiaomi, and Seres. However, it narrowed its 2026 net loss forecast to RMB1.8 billion from RMB4.5 billion, reflecting decreased operating costs and an improved product portfolio.

Additional Financial Institutions Provide Analysis

BofA Securities increased its price objective to $6.70 while maintaining a Neutral recommendation, observing that Q4 performance largely aligned with projections. Morgan Stanley reaffirmed its Overweight rating with a $7.00 price target following optimistic delivery growth commentary from NIO’s founder.

For Q1 2026, NIO provided delivery guidance of 80,000 to 83,000 vehicles. The midpoint sits approximately 8% below Bloomberg consensus figures but 2% above Macquarie’s projection. Revenue guidance ranging from RMB24.5 billion to RMB25.2 billion exceeded both Macquarie’s estimate and broader consensus expectations.

NIO has three additional mid- to large-size SUV models under development, with two variants scheduled to debut during Q2 2026.

The stock had appreciated 17.77% during the preceding week through Wednesday’s trading session, with a market capitalization standing at $14.41 billion.

Crypto World

Marathon Petroleum (MPC) Stock Surges After Blowout Q4 Earnings and Strong Cash Returns

Key Highlights

- Marathon Petroleum reported Q4 2025 adjusted EPS of $4.07, surpassing analyst consensus of $3.01 by more than 35%

- Annual 2025 adjusted EBITDA reached approximately $12 billion

- Shareholders received $1.3 billion in Q4 distributions, contributing to $4.5 billion total for the year

- Marathon closed 2025 with $3.7 billion cash position and zero utilization of its $5 billion revolving credit line

- Wall Street analysts set price targets between $210 and $225, maintaining predominantly bullish ratings

Marathon Petroleum (MPC) delivered an exceptional fourth quarter in 2025, capturing Wall Street’s attention with results that significantly exceeded expectations. The refining giant reported adjusted earnings reaching $4.07 per diluted share, obliterating the consensus forecast of $3.01 by over 35%. Quarterly revenue totaled $33.4 billion, marginally topping analyst projections.

Marathon Petroleum Corporation, MPC

Quarterly net income reached $1.5 billion, translating to $5.12 per diluted share. This represented a dramatic improvement from the $371 million recorded in the year-ago quarter. Adjusted EBITDA for the period climbed to $3.5 billion versus $2.1 billion in Q4 2024.

The Refining & Marketing business unit emerged as the primary catalyst behind the earnings outperformance. This segment generated EBITDA of $1.997 billion while maintaining crude capacity utilization at 95%. The R&M margin expanded to $18.65 per barrel.

Operational refining costs increased to $5.70 per barrel, yet the margin growth easily absorbed this headwind. Capture rates exceeding 100% played a critical role in the quarter’s success.

The midstream operations added meaningful value, producing EBITDA of $1.7 billion. Enhanced throughput volumes and contributions from newly acquired assets drove this performance, though some asset sales provided a partial offset.

The Renewable Diesel business unit contributed $7 million in EBITDA. While not the primary growth driver, it remains a developing component of the portfolio.

Marathon concluded the year holding $3.7 billion in cash. The company maintained a pristine balance sheet with zero outstanding borrowings against its $5 billion revolving credit facility entering 2026.

Shareholder Returns Remain a Strategic Priority

The refiner distributed $1.3 billion to investors during Q4. Throughout 2025, total distributions reached $4.5 billion. Since 2017, Marathon has allocated over $45 billion toward share repurchases, meaningfully reducing outstanding shares and enhancing per-share financial metrics.

Operating cash flow for 2025 approached $8.3 billion. Management continues executing a balanced capital allocation strategy combining regular dividends with aggressive share buybacks, which forms a cornerstone of the investment thesis.

Analyst price objectives have moved upward recently. Wall Street firms have published targets of $210, $217, and $225 during February. The consensus 12-month price target across coverage sits slightly above $204, with most analysts maintaining Buy-equivalent ratings.

Shares have been changing hands near the high-$190s range, marking substantial year-to-date appreciation. The stock advanced approximately 3% on March 11 and continued extending gains throughout the week.

Favorable Market Conditions Supporting Performance

Escalating geopolitical instability across the Middle East has driven oil prices upward and improved investor sentiment toward domestic refiners. Market participants are anticipating tighter product supply-demand dynamics and more robust refining crack spreads.

Elevated crude prices present both challenges and opportunities for Marathon. While input costs increase, refining margins can expand when finished product pricing outpaces crude appreciation. Current market conditions suggest investors are betting on this favorable scenario.

Institutional ownership patterns show continued strong interest from large asset managers. Some major shareholders reduced holdings during late 2025, while others increased positions — representing normal portfolio rebalancing activity for a large-cap energy name.

For full-year 2025, Marathon recorded adjusted EBITDA approaching $12 billion, with the refining and marketing segment achieving $7.15 per barrel in Q4 compared to a $5.63 full-year average.

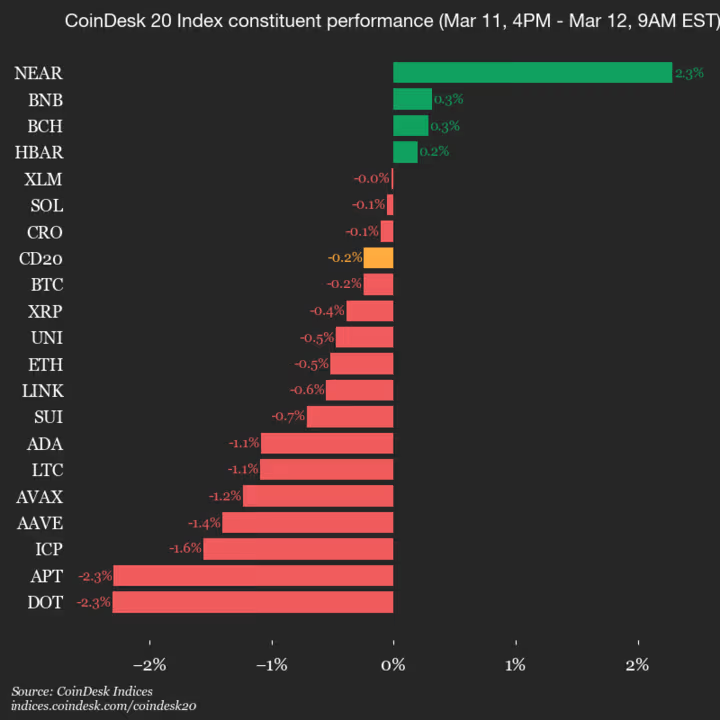

CoinDesk Indices presents its daily market update, highlighting the performance of leaders and laggards in the CoinDesk 20 Index.

The CoinDesk 20 is currently trading at 2012.94, down 0.2% (-4.89) since 4 p.m. ET on Wednesday.

Four of 20 assets are trading higher.

Leaders: NEAR (+2.3%) and BNB (+0.3%).

Laggards: DOT (-2.3%) and APT (-2.3%).

The CoinDesk 20 is a broad-based index traded on multiple platforms in several regions globally.

Bitcoin (BTC) circled $70,000 into Thursday’s Wall Street open after US jobs data matched expectations.

Key points:

-

Bitcoin shrugs off more US macro data as jobless claims copy flat CPI numbers.

-

Oil stays volatile, while markets ignore almost any chance of a March interest-rate cut.

-

BTC price action stays indecisive around the $70,000 mark.

Bitcoin surfs new US jobless claims release

Data from TradingView showed ongoing BTC price compression on the day, with BTC/USD acting in an increasingly narrow range.

US initial jobless claims were 213,000 for the week through March 7, just 1,000 below the previous week’s print and 2,000 below market consensus.

The numbers furthered relief over the US economy after Wednesday’s Consumer Price Index (CPI) release also avoided major deviations from its expected values.

Volatility, however, remained in oil, which was up by more than 5% on the day at the time of writing after initially rising above $95. News of a coordinated release of 400 million barrels from reserves to counteract the Strait of Hormuz impasse thus failed to alter the price trend.

Analyzing the situation, trading resource The Kobeissi Letter suggested that a lack of clarity from US President Donald Trump over how long the Middle East conflict would last was fueling oil’s ongoing surge.

“The reason behind this rally was largely that President Trump was not signaling how long the Iran war would last,” it wrote on X.

“Since then, the ONLY factor that has changed is that President Trump has said the war will be over ‘pretty quickly.’ However, this also implies that military action will likely continue until at least the end of March.”

The latest inflation prints, meanwhile, did nothing to alter the market’s views of future Federal Reserve policy.

The latest data from CME Group’s FedWatch Tool showed the odds of an interest-rate cut at the Fed’s March 18 meeting — a key potential crypto tailwind — at less than 1%.

BTC price breakout can take “several more weeks”

Key Bitcoin price levels remained in place as traders waited for directional cues.

Related: Bitcoin braces for oil shock and death crosses: 5 things to know this week

Trader Daan Crypto Trades flagged $72,000 and $62,000 as lines in the sand around spot price, with the Point of Control (PoC) at around $68,000.

“Anything in between will just chop you up as we have been seeing already. Ranges like these can easily take several more weeks before resolving,” he told X followers on Wednesday.

As Cointelegraph reported, consensus stayed bearish on the mid-term outlook, favoring a drop to new macro lows to come.

Trader and analyst Rekt Capital noted that by historical standards, Bitcoin’s bear market should continue from here.

“Time-wise, Bitcoin will soon be halfway through its Bear Market,” he summarized in one of several recent X updates.

“Retracement-wise however, Bitcoin has already performed 75% of the downside in its Bear Market correction.”

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

Tether, the crypto firm behind the most popular stablecoin USDT, said Thursday it has invested in Ark Labs to bring programmable payments to the Bitcoin network.

The backing formed part of a $5.2 million funding round for the startup. Ark Labs develops Arkade, a system that aims to allow faster transactions and application building on top of Bitcoin. With the new funding, the start-up said it has raised about $7.7 million in total.

The project focuses on making Bitcoin usable for payments and financial tools that often require faster settlement and automation. Arkade acts as an execution layer that developers can use to build services such as payment networks, lending tools and digital asset platforms.

“Bitcoin is the most liquid digital asset in the world, but it has lacked the programmable infrastructure that financial applications require,” said Marco Argentieri, CEO of Ark Labs. “Arkade aims to change that,” he added.

Tether said the funding will help expand infrastructure that could support stablecoins on Bitcoin. Stablecoins are digital tokens pegged to fiat currencies such as the U.S. dollar and often move across other blockchains like Ethereum or Tron.

“Stablecoins were born on Bitcoin, and expanding access on the Bitcoin network remains a priority for us,” Tether CEO Paolo Ardoino said in a statement.

The investment is part of Tether’s effort to expand beyond its stablecoin issuance roots and enhance the use of its $185 billion digital dollar token USDT. Last month, the firm invested in online marketplace Whop and cross-chain protocol LayerZero.

Key Takeaways

- AAL declined approximately 3% to $11.11 during pre-market hours on March 11, continuing a steep slide from mid-February highs

- Crude oil-linked jet fuel has jumped from $85–90 per barrel to a range of $150–200 per barrel amid escalating Middle East conflict

- Unlike competitors, American maintains zero fuel hedging exposure, leaving it vulnerable to a $50M annual cost increase per penny of fuel price rise

- Wall Street consensus has shifted toward caution, with TD Cowen and Rothschild slashing forecasts and lowering ratings

- Internal pressure mounts as the flight attendants’ union delivered an unprecedented no-confidence declaration targeting CEO Robert Isom

American Airlines (AAL) delivered an adjusted pre-tax profit of merely $352 million for 2025. Meanwhile, Delta achieved $5 billion and United reached $4.6 billion during the same period. This performance disparity has become increasingly critical.

American Airlines Group Inc., AAL

Brent crude currently hovers near $91 per barrel, with industry analysts projecting sustained levels above $95 through the next eight weeks should Middle Eastern supply chain disruptions persist. Jet fuel costs have rocketed from their previous $85–90 baseline to peaks approaching $200 per barrel, based on Air New Zealand’s reporting.

While most global carriers employ fuel hedging strategies to mitigate risk, American has chosen a different path. Without hedging contracts, the carrier faces complete vulnerability to volatile spot market pricing — and current conditions are proving particularly harsh.

AAL stock plummeted over 5% on March 5 following both a downgrade announcement and a crude price surge connected to intensifying geopolitical tensions surrounding the Strait of Hormuz. Shares recently traded near $11.04, representing a significant retreat from mid-February valuations.

During March 11 pre-market activity, AAL extended losses with another ~3% decline to $11.11. Delta experienced a 2.2% drop while United fell 3.6% in parallel trading, yet American’s unhedged position amplifies its vulnerability considerably.

Company disclosures reveal that each additional penny per gallon translates to approximately $50 million in added annual fuel expenses for American. By comparison, Delta faces $40 million per penny, while Southwest’s exposure stands at just $22 million.

Financial Outlook Faces Headwinds

Executive leadership has projected a Q1 2026 loss ranging from $0.10 to $0.50 per share, with full-year earnings estimated between $1.70 and $2.70 per share. These full-year projections rest on the assumption that fuel prices stabilize — an increasingly questionable premise.

The carrier’s most recent quarterly results disappointed expectations. Actual EPS registered approximately $0.16 against consensus estimates of $0.38. Operating margins compressed to roughly 0.2%.

On March 9, American took steps to strengthen its financial position, expanding revolving credit facilities from $3.0 billion to $3.11 billion while pushing maturity dates to March 2031.

The airline closed 2025 carrying $36.5 billion in total debt obligations, with management targeting a reduction below $35 billion before 2026 concludes. Sustained elevated fuel costs threaten this deleveraging objective.

Wall Street Sentiment Deteriorates

Investment firms have grown increasingly cautious. TD Cowen reduced its price objective from $17 to $13 while maintaining a Buy rating with diminished enthusiasm. Rothschild & Co downgraded AAL from Buy to Neutral while slashing its target from $17 to $12.50, pointing to “constrained financial maneuverability amid rising cost pressures.”

Among 17 analysts monitored by MarketBeat, current ratings show 9 Hold recommendations, 6 Buy ratings, and 2 Sell ratings. The consensus 12-month price target stands at $16.22 — suggesting potential upside exceeding 40% from present levels, though achieving this outcome faces mounting obstacles.

Compounding financial challenges, the flight attendants’ union delivered an unprecedented no-confidence resolution against CEO Robert Isom, highlighting operational shortcomings and competitive underperformance.

Industry observers are focused on American’s upcoming appearance at the J.P. Morgan Industrials Conference scheduled for March 17, where Isom is anticipated to detail the carrier’s strategy for managing escalating costs while pursuing debt reduction commitments.

Bitcoin remains pinned around $70,000, showing impressive price stability even as market sentiment remains deeply pessimistic amid the Iran war and oil price volatility.

Crypto’s fear and greed index, a widely tracked sentiment indicator, has persistently signaled extreme fear in recent weeks, suggesting traders remain cautious despite the lack of a major price breakdown.

Market positioning also paints a dour picture. Annualized funding rates for bitcoin perpetual futures have been negative since early March, reflecting a growing bias for bearish short bets. The current stretch marks the longest period of negative funding since April 2025, when bitcoin ultimately formed a market bottom, around $76,000.

This is consistent with fear on Wall Street, where the VIX index jumped to 25 this week, its highest in over a year.

Yet bitcoin’s price action has been notably resilient. Since the escalation of the Middle East conflict on Feb. 28, the largest cryptocurrency has gained roughly 7%. That compares favorably with other major assets over the same period. The Nasdaq 100 has been largely steady while the S&P 500 has dropped about 1%, gold has slipped roughly 3% and silver has fallen nearly 9%.

This is in addition, to brent crude briefly pushing back above $100 per barrel earlier today amid ongoing tensions in the region.

The contrast was also visible during Wednesday’s U.S. trading session. BlackRock’s iShares Bitcoin Trust (IBIT) traded 1% higher. While major equity benchmarks were in the red, including the S&P 500 (SPX), the Nasdaq 100 (QQQ), the Russell 2000 (IWM) and the Dow Jones Industrial Average (DJI), highlighting bitcoin’s relative resilience during U.S. market hours.

The outperformance likely stems from big traders and institutions snapping up coins in privately negotiated transactions, keeping demand steady.

For now, bitcoin appears to be performing better than the market mood surrounding it, holding steady despite persistent fear across the broader financial landscape.

The USD/JPY chart shows a bullish trend at the start of March, influenced by the escalation of military activity in the Middle East.

On one hand, the US dollar is strengthening due to increased demand for safe-haven assets. On the other, the Japanese economy is under pressure because of its heavy reliance on oil imports from the Middle East.

These factors have pushed the pair above 159.20 JPY per USD this week, surpassing the January high (point A). The 2026 peak lies nearby; however, technical analysis suggests that bullish momentum may be fading.

In our note of 26 February, we:

→ updated the wide ascending channel along with the intermediate growth trajectory (shown in purple);

→ highlighted signs of seller activity near 156.600.

As indicated by the arrow on the USD/JPY chart, after a small pullback to the lower purple line, buyers resumed their efforts, with the 156.600 level now acting as support.

Currently, we can observe that:

→ the RSI indicator is forming a bearish divergence;

→ it is becoming increasingly difficult for the price to reach the upper boundary of the purple channel;

→ the brief breach of point A resembles a bearish Liquidity Grab.

Additional bearish factors include:

→ the line dividing the upper half of the long-term channel into two parts;

→ proximity to the psychological 160 JPY per USD level.

It is worth recalling that in 2024, 1 USD briefly exceeded 160 JPY, but this level did not hold, as the Bank of Japan intervened. This context adds significance to the upcoming BOJ announcements, scheduled for next Thursday. Ahead of this event, USD/JPY may consolidate around current levels.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Geopolitical frictions and a shifting macro backdrop are sharpening focus on what could emerge as a tipping point for crypto and broader risk assets: the US midterm elections. In a March 11, 2026 market commentary, Binance Research surveys how election cycles historically fed rebounds in equities and Bitcoin, suggesting the upcoming vote might unlock a constructive window for risk-on assets. The report flags that the 12 months after past midterms have seen the S&P 500 rise by about 19% on average, while Bitcoin delivered roughly a 54% gain across the three post-midterm years on record. With the midterms slated for November 3, 2026, the study frames the coming year as a potentially pivotal phase for markets trading around political uncertainty.

Key takeaways

- Historical post-midterm performance shows a potential upside for risk assets, with the S&P 500 up ~19% on average and Bitcoin up ~54% over the three post-midterm years in prior cycles.

- Bitcoin has experienced negative returns during several midterm years (example declines: 2014, 2018, 2022), but the pattern in subsequent years has generally been a rebound.

- The near-term direction hinges on geopolitics, notably US-Israel-Iran tensions, with oil prices a potential pressure point if energy supply is disrupted.

- The energy market narrative was reinforced by an emergency energy stock release of 400 million barrels, the largest coordinated drawdown on record.

- Market participants appear to be in a wait-and-see phase, awaiting clearer directional signals once election outcomes are known.

Tickers mentioned: $BTC

Sentiment: Neutral

Price impact: Positive. The historical pattern of post-midterm rebounds in both equities and Bitcoin suggests a potential uplift in risk assets once political uncertainty subsides.

Trading idea (Not Financial Advice): Hold. Investors may want to wait for clearer post-election directional cues and macro signals before taking sizable new positions.

Market context: The narrative arcs around the midterms intersect with macro risk sentiment, regulatory discourse, and energy-market dynamics, all of which can shape liquidity and appetite for crypto assets in the near term.

Why it matters

The Binance Research framework emphasizes that the political risk hurdle commonly cleared after election outcomes has historically unlocked a more robust risk-on regime. In practical terms, if the 2026 midterms resolve with a clearer policy outlook, traders could see renewed bid activity across both traditional markets and crypto. The historical lens does not guarantee future moves, but it provides a reference for how sentiment has tended to shift when political ambiguity diminishes.

From a trader’s vantage point, the divergence between headline risk and market mechanics is notable. Even as Bitcoin (CRYPTO: BTC) has flirted with key levels and traded within ranges shaped by liquidity flows, the broader message of the Binance analysis is that the cycle often accelerates once electoral uncertainty recedes. In prior midterm years, Bitcoin’s trajectory has been punctuated by sharp corrections during the year itself, followed by significant recoveries in the ensuing periods. That pattern could inform risk budgeting and timing considerations for funds that aim to participate in the rebound without overexposure to interim volatility.

Oil and energy markets add another layer of complexity. As geopolitical tensions intensify, crude prices have shown sensitivity to supply expectations. Recent data suggest the market could spike further if disruptions endure, a scenario that tends to weigh on risk assets in the short run even as longer-term cycles remain dependent on policy clarity and liquidity dynamics. A one-day spike to the vicinity of $95 per barrel framed the current stress, underscoring how energy risk can spill over into equities and crypto markets.

In parallel, market infrastructure signals have pointed to a broader risk-off posture in the near term. The energy-release maneuver by international authorities, described as the largest-ever coordinated drawdown, adds a layer of supply-side management that could temper volatility in the energy complex—but it does not eliminate the risk of further macro shocks. Analysts cautioned that continued geopolitical escalation could keep risk assets under pressure, at least until a clearer post-election framework emerges. For readers interested in the on-the-ground links to these developments, recent reporting from Reuters outlined the energy dynamics and the rhetoric around price stability amid the conflict.

Despite the near-term headwinds, the longer historical arc highlighted by Binance Research remains relevant: the period after the election and the associated resolution of political uncertainty has historically produced meaningful rallies. The message is not to extrapolate a foolproof blueprint, but to recognize that policy clarity can reframe risk appetite. Bitcoin’s own history of midterm-year drawdowns, followed by rebounds, adds a layer of complexity but also a potential pathway for investors who can weather the interim noise. To see a related compilation of market context including the energy shock and its ripple effects, readers can review the linked analyses and the energy market data sources cited in the coverage, including the market commentary that anchors these observations.

For a quick snapshot of the broader narrative in motion, a concise explainer video on market dynamics related to this cycle can be found here: Video discussion.

The analysis arrives as markets enter a period of heightened attention ahead of the November 3, 2026 vote, when the 120th Congress will take shape and set the tone for policy and regulatory signals in the year ahead. While the near term may ride a roller-coaster of headlines, the data from prior cycles provides a reference point for investors assessing whether a recovery window could be opening for equities and digital assets alike. The key takeaway: the post-election horizon could be the most constructive phase of the cycle, provided geopolitical tensions do not diverge into a sustained risk-off regime before the dust settles.

The crosscurrents at play—geopolitics, energy stability, and the timing of policy clarification—mean that market moves could be as much about risk sentiment and liquidity flows as about fundamentals. In the coming months, traders will be watching for progress in diplomatic channels, oil market signals, and any regulatory developments that could influence market structure or capital flows into crypto. The interplay of these factors will help determine whether the long-hoped-for recovery accelerates or remains restrained by ongoing uncertainty.

As with all such analyses, the caveat remains: past performance is not a guarantee of future results. However, the framework outlined by Binance Research provides a structured lens to interpret how the upcoming midterms might align with broader macro and crypto-market rhythms. The next few quarters will be telling as investors weigh the odds of a meaningful reset against continued geopolitical volatility and policy debates that will shape the market landscape for the remainder of the year.

What to watch next

- November 3, 2026 — US midterm elections determine the composition of the 120th Congress and influence policy signals for the year ahead.

- Post-election period — watch for any substantive shifts in regulatory discourse that could affect crypto market structure and liquidity.

- Geopolitical developments in the Middle East — escalation or de-escalation can impact energy prices and risk sentiment.

- Official energy-market actions — monitor further commentary on energy security and any additional emergency stock management outcomes.

- Market commentary updates — ongoing analyses that correlate election outcomes with volatility and liquidity in crypto markets.

Sources & verification

- Binance Research, Weekly Market Commentary (March 11, 2026) — historical post-midterm performance data and interpretation.

- Reuters reporting on energy disruptions and price implications related to Middle East tensions.

- Trading Economics data on crude oil price movements and daily price spikes.

- International Energy Agency announcements on emergency stock releases (largest coordinated drawdown).

- Election date and political timeline for the November 3, 2026 midterms.

Post-midterm dynamics could reshape crypto and risk assets

The central premise is that the political fog surrounding election outcomes has historically been a wind at the back of risk assets once it lifts. Binance Research’s synthesis shows a pattern of strength following periods of uncertainty, with the S&P 500 and Bitcoin delivering memorable advances in the year or years after midterm cycles. That pattern does not imply a guaranteed rally, but it offers a framework for considering how a calmer political horizon might influence price action across markets that have become increasingly interlinked in recent years.

In practice, the near-term trajectory will be colored by geopolitics and macro data arrivals. The immediate risk premiums tied to the US-Israel-Iran dynamic could push energy prices higher, which tends to compress risk appetite in the short run. Yet if the election outcomes resolve in a way that reduces political risk, liquidity could improve and traders may reallocate toward risk assets, including digital currencies. Bitcoin’s own history in midterm years—marked by episodic declines followed by longer-term recoveries—adds nuance to how investors should position themselves during this transition window. The historical signal is not a guarantee, but it is a lens for weighing potential outcomes as the cycle evolves.

Market participants will also be watching for any policy shifts or legislative milestones that could affect the crypto market structure, such as regulatory proposals or framework updates that impact market access and capital flows. The energy-market backdrop, with its flashpoints and emergency stock actions, will continue to feed volatility but also to shape the tempo of risk-taking. In a landscape where liquidity and risk sentiment are closely tethered to macro and geopolitical developments, the post-midterm period could offer a clearer directional signal for traders, investors, and builders navigating the crypto ecosystem.

Cryptio, a developer of accounting software for digital assets, raised $45 million in a Series B funding round as financial institutions and corporations expand their use of blockchain-based assets.

The round closed about three weeks ago and was led by BlackFin Capital Partners and Sentinel Global. Existing investors 1kx, BlueYard Capital and Ledger Cathay Capital also participated, Fortune reported, citing a company announcement. The company’s valuation wasn’t disclosed.

Cryptio’s platform helps companies track the digital assets they hold and where those assets are stored across wallets, custodians and exchanges. In January last year, the firm raised $15 million in an extension to its Series A funding round from mid-2022.

The software also helps firms manage crypto loans and monitor other blockchain-based assets. The system organizes this data so companies can produce accounting records and financial reports.

Cryptio was founded eight years ago by Antoine Scalia, after he graduated from business school in Paris. Early customers were startups and smaller crypto companies.

The firm now employs about 110 people and serves more than 450 clients. Those clients include stablecoin issuer Circle Internet (CRCL) and the blockchain subsidiary of French bank Société Générale (GLE).

Cryptio operates in a growing market for crypto accounting tools. In January, crypto infrastructure firm Fireblocks acquired competing platform TRES Finance for $130 million.

Sentinel Global managing partner Jeremy Kranz said Cryptio has gained traction by working closely with large financial institutions and explaining how its system integrates with their existing accounting processes.

The fundraise comes as U.S. corporate adoption of the crypto space has accelerated, with the Trump administration pushing policies meant to strengthen the industry in the U.S. His cyber strategy has vowed to “support the security” of cryptocurrencies and blockchain.

Regulatory and accounting changes have also lowered barriers for institutions. Regulators replaced the SEC’s SAB 121 guidance with SAB 122, easing custody rules for banks, while new Financial Accounting Standards Board rules that took effect in 2025 require companies to report crypto assets at fair value.

Goddard’s Leadership: From Innovation to Isolation

Nio (NIO) Stock Climbs on Robust Q4 Earnings and Wave of Positive Analyst Revisions

10 Best Oscar-Winning Performances Ever, Ranked

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

The 6:23 AM Freeze: How Canada Shocked America’s Financial System

Berarti dari 2019 udah Financial Freedom.. wow (@r@radityadika#prazteguh #radityadika #podcast

Energy Policy | Lunch Money with Paul Krugman and Heather Cox Richardson

-

Business6 days ago

Form 8K Entergy Mississippi LLC For: 6 March

-

News Videos3 days ago

News Videos3 days ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Ann Taylor

-

Crypto World3 days ago

Crypto World3 days agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Tech1 day ago

Tech1 day agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

Sports7 days ago

Sports7 days ago499 runs and 34 sixes later, India beat England to enter T20 World Cup final | Cricket News

-

Politics6 days ago

Politics6 days agoTop Mamdani aide takes progressive project to the UK

-

Business2 days ago

Business2 days agoExxonMobil seeks to move corporate registration from New Jersey to Texas

-

Tech2 days ago

Tech2 days agoChatGPT will now generate interactive visuals to help you with math and science concepts

-

Sports5 days ago

Sports5 days agoThree share 2-shot lead entering final round in Hong Kong

-

Sports4 days ago

Sports4 days agoBraveheart Lakshya downs Lai in epic battle to enter All England Open final | Other Sports News

-

NewsBeat19 hours ago

NewsBeat19 hours agoResidents reaction as Shildon murder probe enters second day

-

NewsBeat7 days ago

NewsBeat7 days agoPiccadilly Circus just unveiled ‘London’s newest tourist attraction’ and it only costs 80p to enter

-

Entertainment5 days ago

Entertainment5 days agoHailey Bieber Poses For Sexy Selfies In New Luscious Lip Thirst Traps

-

Business4 days ago

Business4 days agoSearch for Nancy Guthrie Enters 37th Day as FBI Probes Wi-Fi Jammer Theory

-

Business1 day ago

Business1 day agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

NewsBeat3 days ago

NewsBeat3 days agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Tech3 days ago

Tech3 days agoDespite challenges, Ireland sixth in EU for board gender diversity

-

Business3 days ago

Business3 days agoSearch Enters 39th Day with FBI Tip Line Developments and No Major Breakthroughs

-

NewsBeat23 hours ago

NewsBeat23 hours agoI Entered The Manosphere. Nothing Could Prepare Me For What I Found.