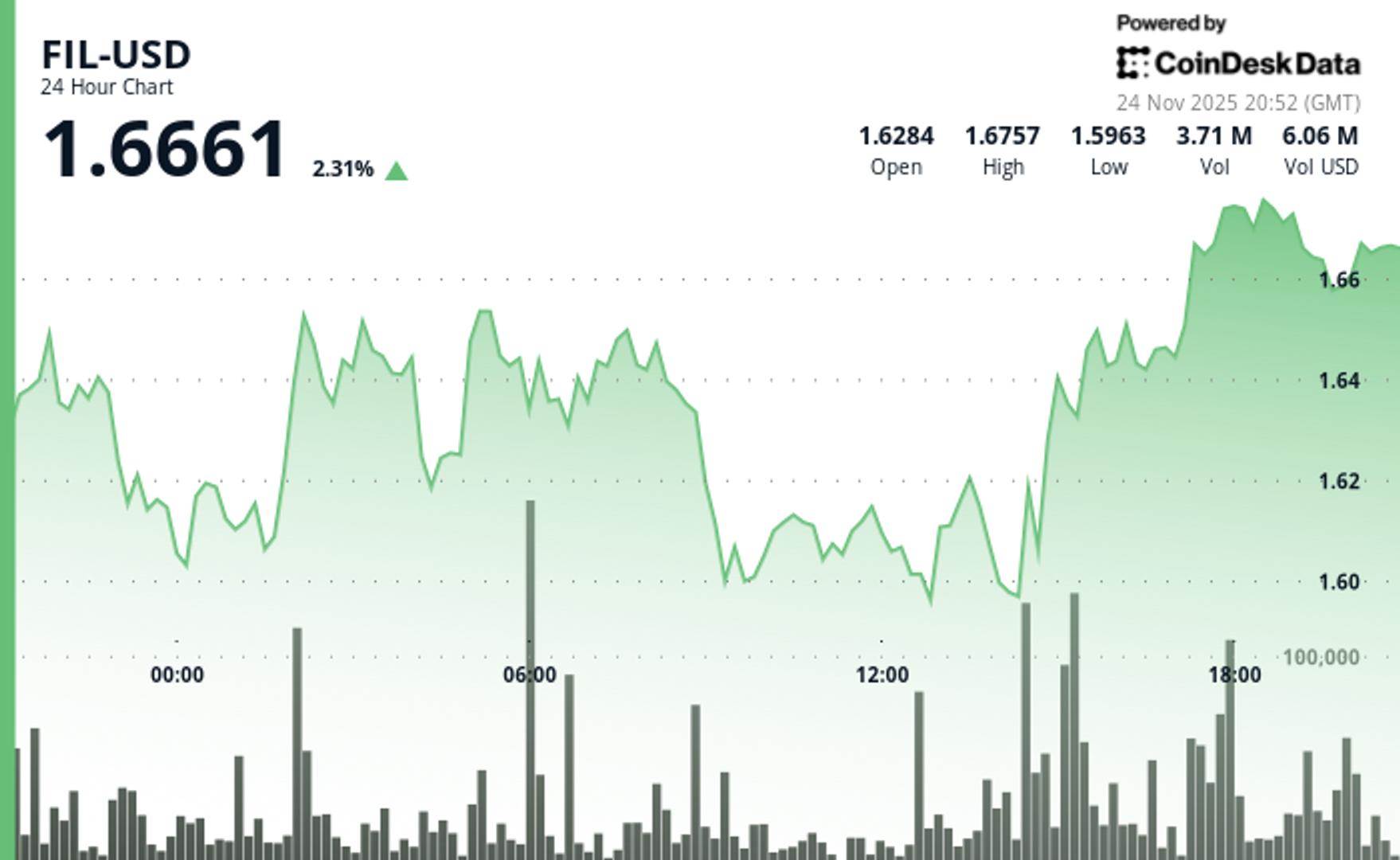

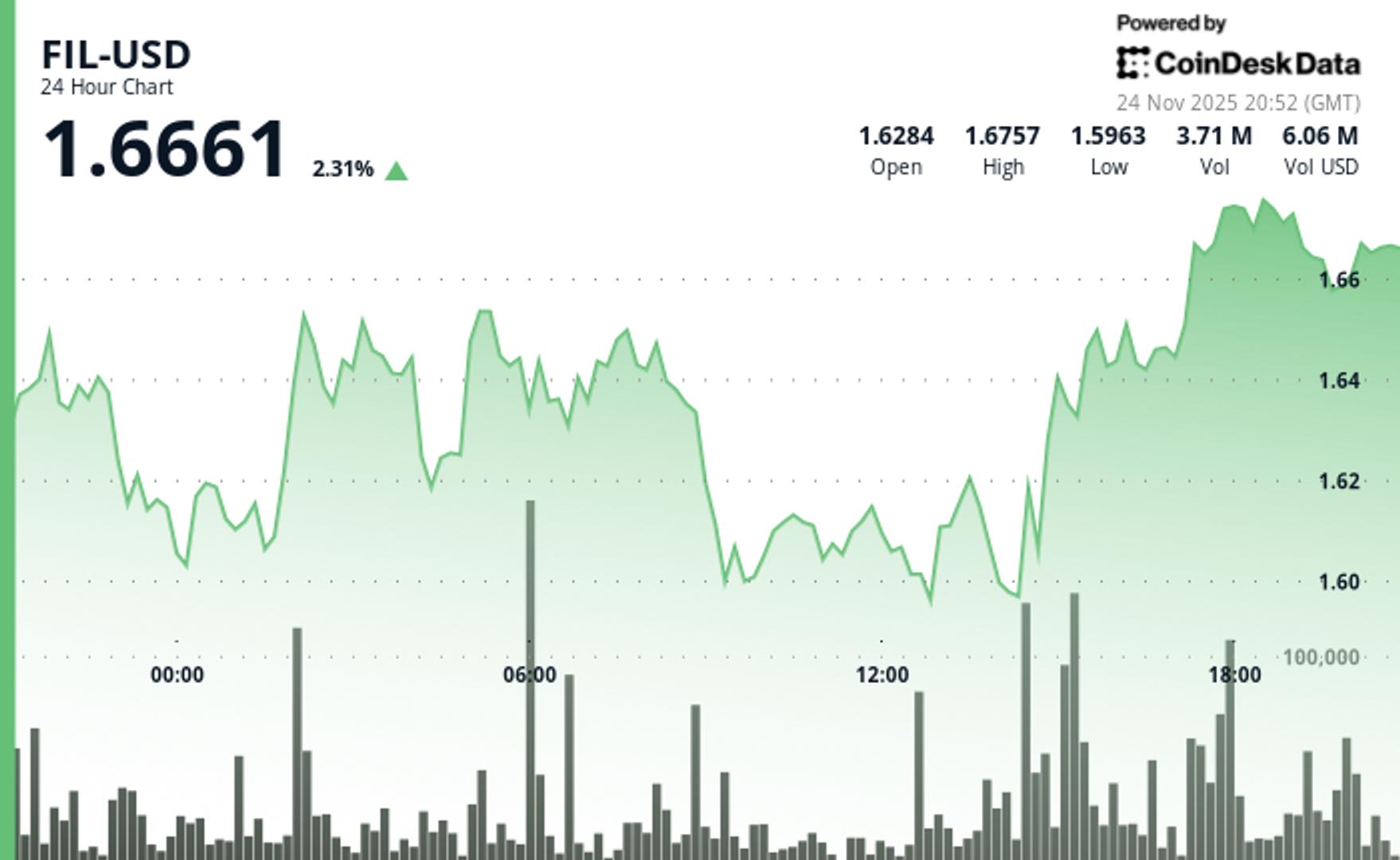

CryptoCurrency Filecoin Rises 2% After Breaking $1.63 Resistance Published 2 weeks ago on 24 November 2025 By NewsAdmin FIL broke out on heavy volume as technical momentum accelerated past critical threshold levels. Related Topics: Up Next Japan Eyes New Rules for Crypto Exchanges Don't Miss ECB Says Stablecoins Threaten Financial Stability Continue Reading Advertisement You may like Click to comment Leave a Reply Cancel replyYour email address will not be published. Required fields are marked *Comment * Name * Email * Website Save my name, email, and website in this browser for the next time I comment.