Business

Generation PMCA Q4 2025 Quarterly

Donny DBM/iStock via Getty Images

Top-Down and Bottom-Up

Investors typically fall into two camps. They are either top-down, guided by macro views and often taking thematic slants, or bottom-up, ignoring the big picture to focus on individual securities. We have always conducted analysis across the spectrum. Our goal is to select undervalued securities by thoroughly analyzing each individual company. But we also evaluate the overall economic environment, to alter our portfolio approach, especially when our macro alerts trigger.

We developed proprietary tools and formalized a four-pillar approach several years ago. Two pillars are top down: TRIM™ (our Indicator of Momentum to alert us to material market declines) and TEC™ (our Economic Composite to spot recessions). The other two pillars are bottom up: value (to determine price to Fair Market Value) and TRAC™ (to optimize entry and exit points).

During most periods, bottom-up analysis suffices because the economy is humming along; however, we specifically built our macro tools to provide us with alerts when the likelihood of macroeconomic issues overwhelming markets is high. Though, in our view, one should not vacillate between being fully invested or entirely in cash. Certain companies ought to be owned through thick or thin, otherwise the upside might be missed. Conversely, a top-down view can assist in avoiding positions that may suffer as the economy softens and markets are pressured.

Best of Both Worlds

Since TEC™ is still alerting us to a potential recession, we have maintained our hedging strategies, continuing to hold short positions (where authorized) or inverse long ETFs. We aren’t just concerned with the potential for a near-term peak in the economic cycle, but the markets are overvalued and inflecting from TRAC™ ceilings. Certain segments, such as technology, are experiencing significant overspending, housing is already in a downturn from prior excesses, and economic and geopolitical policies are creating instability.

Although, when uncertainties rise some securities decline unduly. This allows us to build portfolios of quality companies that trade down to levels that are attractive discounts to our FMV estimates. Even without a recession, undervaluations often occur when specific sectors come under scrutiny or because of company-specific news items or rumours. Investors often sell when issues arise, without taking the time to evaluate situations. Furthermore, selling begets selling as fear overpowers rational behaviour. As bottom-up analysts, we welcome these opportunities to take advantage of short-term price declines from what we believe are temporary issues until misperceptions dissipate.

Using both approaches, we can hedge based on a negative macro-outlook, avoid cyclical companies when a recession is expected, and embrace undervalued quality companies that ought to do well, even in a downturn.

Top Heavy

We’re expecting a recession because the yield curve previously inverted, monetary growth is anemic, economic statistics have waned, and unemployment should rise. Even in the absence of a recession, overall economic growth could soften for a prolonged period.

Population growth—the driver of economic growth—is in reverse. The U.S. is now experiencing net emigration—more people are leaving than coming—which hasn’t occurred since 1935. Not just as a result of record deportations but also because Americans are departing in record numbers. It may get worse. A recent Gallup survey showed 20% of Americans want to live elsewhere, up from 10%, even in the 2008 recession. Canada’s population suffered the largest quarterly drop since the 1940s. This is exacerbating the already poor demographics—an ageing population because baby boomers are a disproportionate cohort and fertility rates are too low to keep pace with deaths. Other regions, such as Asia (China, Japan, and South Korea) and Europe (Italy, Greece, and Portugal) are suffering declining populations too.

Basic economics suggests that population growth leads to growth in unit volumes which in turn leads to expanding sales, profits, and share prices. If populations don’t grow, the rest doesn’t easily follow. Immigration, albeit done properly, is a necessity for economic growth.

For the last several years, until recently, job openings in the U.S. have consistently been well above the number of unemployed. Certain sectors (agriculture, dining, hospitality, nursing, construction, and manufacturing) could see significant labour shortages if immigration policies aren’t remedied.

Unusually, recent economic growth has been occurring without job growth. For the third consecutive quarter, more CEOs intend to cut rather than add jobs. The percentage of part-time to full-time jobs is up materially. A further sign of uncertainty amongst employers. The number of job openings also continues to fall. Now, the number of unemployed is above total job openings, which has only occurred twice in the last 30 years, both during recessions. AI has major implications for employment too. Block (SQ) just terminated 40% of its workforce citing AI and the fundamental changes it’s having on how the company operates, allowing for a much smaller team.

Excluding AI spending, the U.S. economy likely contracted in 2025. Growth in capital spending by the major tech companies is expected to be nearly 3 times 2024’s and double last year’s record high spending level. It’s so high that it is expected to be essentially on par with all incremental U.S. bank lending, or 1.6% of GDP. Meanwhile, AI companies have yet to show meaningful returns from this spending, forecasts appear overly optimistic, free cash flows are being depleted, cash hoards spent, debt is increasing, and accounting has become aggressive with depreciation terms counter-intuitively lengthened.

Real estate prices clearly topped out. Pending home sales set a record low in 2025. There’s still a record 50% more sellers than buyers. House prices should decline and rents soften. Though, ultimately, a lack of building will offset the dwindling demand.

The one likely positive impact of all this is low inflation. Disinflation should be driven by increasing unemployment, lower growth in incomes, tight monetary policy (including waning velocity of money from tighter credit conditions), stagnation in foreign economies, and the impact from AI.

The massive spending on AI could result in excess capacity—overbuilding—which would result in an additional source of disinflation. The major spenders appear to be morphing from capital light to capital intensive businesses.

Consumers’ income growth has already slowed dramatically and consumers’ balance sheets are stressed. Delinquencies for student loans along with credit card balances and auto loans have all moved much higher over the last few quarters.

Bank credit was already tightening when the recent pall over the private lending sector began. Private credit delinquencies have remained low; however, a few lender issues and media attention have caused investors to pull out funds and managers to take steps to gate (prohibit) withdrawals, insofar as these are illiquid investments, until loans mature.

All this has helped lower inflation with the U.S. core CPI rate falling to 2.5% and the Truflation rate, which tracks prices of a wide range of goods and services in real time, now below 1%, which augers well for lower interest rates and could help buoy stock and bond valuations.

From the Top

We’re now stuck with some poor economic policies.

Debt levels are too high and governments show little interest in cutting expenditures. Debt levels this high relative to GDP have been shown to suppress economic growth.

Tariffs don’t simply act as an additional tax; they also lower economic activity because they add inefficiencies, complexities, uncertainties, and suppress demand. Worse, the longer these policies persist the more it causes business to seek alternatives, including new trading partners. Trading channels are being altered. The EU inked a massive free trade agreement with India and is pursuing the same with South America. Mark Carney, while visiting Beijing, even referred to Canada’s trade relationship with China being more predictable than that with the U.S.

Looking Toppy

Returns are generally the opposite of valuations. Meaning the lower the valuations the higher the returns and vice versa.

While the average U.S. stock was somewhat reasonably valued over the last few years, the median price-to-earnings ratio for stocks broadly has now lifted to its worst decile. This lowers the return outlook for U.S. stocks to paltry figures. Whenever the S&P 500 valuation has exceeded 23x next-12-months earnings expectations, as it was over the last few months, the subsequent 10-year real return (after inflation) was essentially nil, with a range of -2% to +2% annually.

On top of this, the average S&P 500 decline from intra-year highs in midterm election years is 18%, worse than typical annual drawdowns, and this ignores the larger declines which accompany recessions.

Even steady businesses, like Costco (COST) and Walmart (WMT), trade at such lofty valuations that a decline back to an average normal trading level (12% below FMV) would imply drops exceeding 30%.

It’s not just stocks; bonds aren’t cheap either. Investment Grade U.S. corporate bonds trade at the narrowest spread (approximately 1%) to 10-year government bonds since 2007. High-yield corporate bonds are historically narrow too, just under half the historical average of 5.5%. They should yield closer to 9.5%, not around the current 6.9%. And that’s just assuming the average, in times of stress spreads expand well beyond the historical average.

Some commodities, which have risen way too far above their costs of production, could suffer too. Gold and silver trade well above where they ought to. If gold reverted to its typical premium to the average all-in cost of production it would fall by more than 50%. Once commodity prices rise this far above production costs they generally fall back to normal premiums within 24 months. Silver recently retraced 47% from its high before lifting again, and it still sits at more than 3x where it would be expected to trade based on its cost of production. Excessive trading is prevalent too. The value traded of the silver bullion ETF during the week it peaked, in late January, exceeded the grand total for every year but 5 since 2006.

Since 2011, Bitcoin has fallen by more than 50% from its highs 4 times (about every 3.5 years), and it recently declined 48% from its high. This is not a safe-haven vehicle in our view.

Once the last momentum trader gives way, true economic value reasserts itself.

Corporate insiders realize things are frothy. There were more officers and directors selling shares than buying in January than in any month in the last 5 years.

AI related stocks are trading at huge multiples of revenue.

Overpaying for a company, even a great growing company, can have a poor result, when the share price re-attaches to fair value or declines to a normal discount if it falls out of favour.

From a bottom-up standpoint, we’ve had to review far more companies than usual before finding an opportunity for purchase. A top-down created problem.

Top of the Heap

Competition has intensified in most fields. AI should heighten competitive threats.

AI lowers barriers to entry—by lowering costs and increasing rates of change—which should increase the flow of goods and services. This should erode pricing power and pressure profit margins. The advent of online stores, and their impact on brick-and-mortal retailer margins, provided an example of what might follow for many businesses.

Anthropic’s own Claude AI programs are so effective that it’s writing much of its own code and its capabilities are increasing astonishingly month by month.

A land grab is also taking place amongst AI providers. The largest competitors are spending a disproportionate amount of their cash flow on capital expenditures. In an egregious example, which could have a very poor ending, OpenAI has made over $1.4 trillion in spending commitments; however, it’s losing enormous amounts of money and requires substantial funding to meet its obligations. Meanwhile, its main product, ChatGPT, is also losing market share to Gemini, Grok, Claude, Copilot and others.

Nvidia (NVDA)’s profit margins are so attractive that many customers (Alphabet (GOOGL), Amazon (AMZN), Meta, Microsoft (MSFT), OpenAI) have chosen to design and build their own chips for AI purposes. It’s believed that this is being done at a fraction of the cost, and with more productive outcomes.

High capital spending in overly competitive areas is not a good combination. Net profit margins for the S&P 500, which are cyclical, are now at all-time highs of 13.6% yet have fallen to 8% or below on 5 separate occasions in the last 25 years.

Our Model Portfolios

Our managed accounts are invested based on one or more of our Models (particular investment strategies with notional allocations of securities). A managed account’s holdings will generally be similar to its applicable Model’s, but may not hold all of them based on client-specific factors (income requirements, tax-related considerations, requests/restrictions, and cash available for purchases) and/or market forces which impact specific investment decisions from time to time.

The following descriptions of the holdings in our managed accounts are intended only to explain the reasons that we have made, and continue to hold, these investments in the accounts we manage for you and are not intended as advice or recommendations with respect to purchasing, selling or holding the securities described. Below, we discuss each of our new holdings and updates on key holdings if there have been material developments.

All Cap Model

The All Cap Model combines selections from our large cap strategy (Global Insight) with our small and medium cap ideas. We generally prefer large cap companies for their superior liquidity and lower volatility. The smaller cap positions tend to be less liquid and more volatile; however, we may hold these positions where they are cheaper, trading at relatively greater discounts to our FMV estimates, making their risk/reward profiles favourable.

In the last few months, we bought CONMED (CNMD) and Superior Plus (SUUIF). We sold Headwater (HWXCF) because it lifted to a TRAC™ ceiling, in line with our FMV estimate. Our large cap positions are summarized in the Global Insight section.

CONMED is a medical device and equipment manufacturer. The share price has been declining over the last several years while the company grapples with supply-chain issues and competitive pressures. Its new CEO has made repairing supply-chain constraints the number one priority. Signs are emerging that the situation is improving with backorders at a 3-year low. The aim is to now build a world-class, data-driven supply chain. We see strong growth ahead for the company’s BioBrace and surgical smoke management products. BioBrace is a cutting-edge reinforced bioinductive implant used for orthopedic procedures. Because research has found that surgical-related smoke contains a mixture of harmful byproducts including dead cellular material, carcinogens, viruses, bacteria, and toxic gases, over 20 States have enacted legislation to address surgical smoke evacuation. The company offers a range of products to offset these issues. Should the stock price continue to languish, it could be an ideal takeover target for a larger medical device maker. Our FMV estimate is $60.

Superior Plus is a leading North American distributor of propane and compressed natural gas (CNG). The two markets are polar opposites. While CNG is dominated by large scale players (Superior’s 44% market share makes it the largest), because significant capital investment is required and there are regulatory complexities, propane is fragmented with large-scale distributors, including Superior, comprising just 29% of the market. In propane, cost advantages are vital. The company’s Superior Delivers initiative aims to reduce propane delivery costs through data-driven route optimization. Lower costs enhance customer value, which translates to additional customers and greater scale, further driving down unit costs. Unfortunately, Superior’s plan has encountered issues forcing management to push out expected savings to 2027. Their credibility has severely eroded, which could explain why the stock trades near a 20-year low. Ultimately, the company’s plan should result in rising cash flow, otherwise it’s likely to attract activist investors to spur on the process. Our FMV estimate is $14.

Global Insight (Large Cap) Model

Global Insight portfolios hold large cap stocks (typically with market caps over $5 billion at the time of purchase but may include those in the $2-5 billion range) where portfolios are managed Long/Short or Long only. At an average of less than 70 cents-on-the-dollar versus our FMV estimates, our Global Insight holdings appear much cheaper, in aggregate, than the overall market.

In the last few months, we have made several changes in our large-cap positions. We bought Uber Technologies (UBER) (after selling it in the previous quarter), Netflix (NFLX), Sanofi (SNY), Diamondback Energy (FANG),and Meta Platforms (META). We sold Chevron (CVX), Deutsche Post (DPSGY), Kesko (KKOYY) and GSK (GSK) after each ran up TRAC™ceilings near our FMV estimates.

Uber Technologies has been under pressure because the advent of autonomous vehicles (AVs) is viewed by the market as an existential threat. First, it will likely take many years for AVs to reach mass adoption—the World Economic Forum forecasts that less than 1% of new car sales in 2030 will have level 4 highway and urban capabilities and only 30 global cities will have significant robotaxi fleets. Second, though AVs are clearly the future, Uber has several initiatives underway to remain the platform leader as the world transitions. It recently announced Uber Autonomous Solutions, a suite of services to help partners commercialize AV technology and reduce costs for what is likely to be a highly fragmented industry as dozens of national, regional, and global companies supply AV hardware and software. Recent announcements include: Wayve (a UK-based fleet Uber will own and operate); WeRide (WRD) (a partnership with over 300 AVs on Uber’s platform by this year-end); and Apollo Go (a partnership that aims to put thousands of AVs on the Uber network in Asia and the Middle East). Meanwhile, we expect Uber’s dominant ride-share business and Uber Eats to generate substantial free cash flow, increasing toward $20 billion annually over the next 5 years. Our FMV estimate is $110.

Netflix’s battle with Paramount for Warner Bros. Discovery has all the ingredients of a great movie. Spoiler alert—Netflix bowed out of the process after Paramount raised its offer to $31 per share. While we believed that Netflix was in a win-win situation, the decision to step away demonstrated discipline and prudent capital stewardship. Netflix earns a $2.8 billion break fee and should have renewed focus on its core global streaming business which we believe has untapped potential. We expect to see more gaming, sports, live comedy, musical performances, and events such as Skyscraper Live, which drew 6.2 million views. While competition in streaming is heated, from the many competitors including You Tube, Netflix has an unparalleled content library and the ability to create differentiated original content with a genuine feel sourced in various local markets, which then caters to its diverse global userbase. Our FMV estimate is $140.

Sanofi’s Dupixent is a blockbuster medication used to treat moderate-to-severe inflammatory conditions including atopic dermatitis (eczema) and asthma. New indications should help drive high single-digit annual earnings growth through 2030. Post-2031, the company will likely see growth temporarily stall, or even decline, when it loses patent protection. Uncertainty about the post-expiry growth profile may explain why the stock trades at a relatively low multiple of this year’s expected earnings. However, the company has plans for meaningful growth beyond Dupixent with new drug revenues hitting €5.7 billion in 2025, up 34% year-over-year. Strategic acquisitions and steady performance from its vaccines business should also contribute to growth. Even if earnings decline somewhat post patent expiry, the total return could still be above 8% annualized from expected earnings growth alone, with potential upside from new drugs, acquisitions, and a revaluation once its profile is appreciated. Our FMV estimate is €100.

Diamondback Energy is a Texas-based oil and gas company focused on the Permian Basin. We view the company as a disciplined capital allocator with best-in-class execution. Diamondback exited 2025 with its best drilling efficiency and completion efficiency stats in several years and an industry-leading reinvestment rate. Its efficient operations mean that its healthy dividend ought to be protected down to $37 WTI oil; therefore, management views its dividend as a fixed obligation. We expect full-year 2026 oil production to be 500,000 daily barrels of production which should translate to $4.4 billion of free cash flow, at lower than prevailing oil prices. Since oil prices have been volatile, the share price is likely to be so as well. Our FMV estimate is $210.

Meta Platforms’ capital expenditures are expected to balloon to $120 billion this year, which equates to nearly half of the company’s revenues. Investors are right to be skeptical of this spending on AI since the company appears to have sunk tens of billions on the metaverse with little, if anything, to show for it. Unlike with the metaverse spending, we see a boost to revenues and profitability from Meta’s AI investments. AI-driven improvements and engagement increased the Q4 year-over-year growth in ad impressions by 18% and Instagram Reels watch times by 30%. We also expect cost savings from a material reduction in Meta’s workforce over the next 2 years due to AI productivity enhancements. Our FMV is $770.

Multifaceted Diversification

We also aim to limit volatility and drawdowns by combining investment strategies, especially where returns are less correlated. The goal is to outperform through economic cycles with low correlation, therefore less susceptibility, to market index declines. We can construct portfolios with multiple unique return drivers—strategies that differ in style and approach—based on bottom-up fundamentals, macro tools, or pure quantitative analysis. This can provide exposure to different styles and asset classes beyond just stock and bond indexes.

The benefits of multifaceted diversification are not only from different ways to perform but also from a portfolio comprised of strategies that are less correlated. So that when a strategy underperforms, it’s less likely to occur at the same time as another strategy, which softens the volatility and drawdowns of the overall investment portfolio.

Global Tactical Allocation Model

Our Global Tactical Allocation Model (GTAM) investment process combines macroeconomic analysis with valuation and momentum. ETFs (exchange traded funds) are used to gain exposure to 4 broad asset classes: Equities—major markets, emerging markets, sectors, styles, private equity; Fixed Income—bonds issued by governments, investment grade corporations, high-yield issuers, as well as mortgages, and bond indexes; Real Assets—real estate, infrastructure, renewable energy; and Commodities—Precious Metals or Oil. GTAM emphasizes ETFs that should outperform based on the macro environment, are selling at attractive absolute and relative valuations, possess good relative price momentum, and are at TRAC™ floors.

Current exposures are: Equities (66%); Fixed Income (15%); Real Assets (16%); and Commodities (none). Its current broad themes are U.S. technology, consumer staples, and emerging markets. Positions in U.S. software and cybersecurity were established after AI fears sent these sectors down nearly 30% from their late 2025 peaks.

Quantitative Investment Models

Quantitative equity strategies commonly select securities based on systematic, rules-based decisions, using technology to uncover and exploit historical statistically significant anomalies. Our quantitative equity strategies employ proprietary and systematic processes that rank large cap stocks based on factors such as relative valuation, operating metrics (quality), financial strength, and price momentum. The two models noted below select approximately 30-40 holdings from the top-ranked stocks in the model’s respective universe. TRAC™ is utilized to optimize entry and exit points.

The Quantitative Global Value Model (QGVM) invests in large-cap equities from around the world. The U.S., Canada, and Japan currently represent the top 3 countries. The top 3 sectors are Financials (27%), Consumer Staples (18%) and Industrials (16%). The companies held in QGVM currently have the following characteristics: median forward P/E of 13.3x, ROE and ROIC of 22% and 12% respectively, and dividend yield of 2.1%.

The Quantitative Canadian Value Model (QCVM) restricts its universe to Canada’s S&P/TSX Composite. The top 3 sectors are currently Energy (18%), Industrials (17%), and Information Technology (16%). We have materially reduced our materials weighting after our precious metals holdings reached TRAC™ ceilings and our FMV estimates. Proceeds were used to buy technology stocks which have experienced severe corrections due to concerns about AI. The companies held in QCVM currently have the following characteristics: median forward P/E of 15.9x, ROE 11%, and dividend yield of 2.1%.

Income Model

Our high-yield investment strategy has an average current annual yield (income we receive as a percent of current market value of income securities held) of about 5.0%, and most of our holdings—corporate bonds/debentures, preferred shares, REITs, and high-yielding common shares—trade below our FMV estimates.

U.S. high-yield corporate bonds (ICE BofA Index) yield 6.9%, and because high-yield corporate bond spreads are narrow relative to history, we expect a widening, especially if the economy weakens and corporate delinquencies increase.

We recently purchased Big Yellow Group (BYLOF), Blue Owl Technology Finance (OTFC), and Shurgard Self Storage (SSHGF), and sold Whitestone REIT (WSR) when it ran up to a TRAC ceiling in line with our FMV estimate.

We bought two dominant self-storage REITs—Big Yellow Group—the largest in the UK and Shurgard Self Storage—one of the largest in Europe. They pay dividend yields of 5.0% and 3.0% respectively, both have little leverage, should grow earnings by mid- to high-single digits, and trade well below our respective. €13 and €43 FMV estimates. While the major risk for each is higher interest rates, both should fare well in a recession when self-storage companies benefit from downsizing, and most importantly, the self-storage has offered the highest project returns and lowest volatility of all real estate segments.

Blue Owl Technology Finance is a business development corporation which lends its permanent capital base to other companies. Its share price declined because most of its loans are to software companies. The market is fearful of AI creating instant competition for software providers; however, Blue Owl Technology lends to established, highly profitable, mission-critical and cybersecurity-based, software companies, mostly with first lien secured loans, and it’s only suffered one loss historically. Our FMV is $16 and the shares yield 12.2%.

Investment Grade Income Model

Our investment grade strategy utilizes a systematic process to rank Canadian investment-grade rated corporate bonds based on their duration, yield, financial strength, and momentum.

Currently, positioning has emphasized longer-dated bonds—duration is 10.1 years, 4.5 years more than the S&P Canada Investment Grade Corporate Bond Index. The average yield-to-maturity is 4.8% versus 4.0% for the index.

From Top to Bottom

Few investment managers are expecting a recession. Almost all expect continued economic growth. Investors are assuming that record profits and profit margins will continue apace.

It doesn’t help that broad-based speculation is being fueled by easy access for individuals to online brokerage apps and prediction markets, egged on by hype, momentum, and FOMO. Investment newsletter writers—great contra-indicators—have been euphoric lately, more bullish than at any other time since 2000. This adds to our economic and market concerns, providing comfort in our hedges.

While it’s not easy to properly assess individual companies, it’s more difficult to make a correct and timely call on the overall economy or markets. Still, we are compelled to do both.

We seek the reward from bottom-up analysis of companies whose share prices have fluctuated too far below our assessed FMVs. And gain comfort from hedging when our alerts indicate a potential recession while sentiment runs high and major indexes hit ceilings in our work.

Sorry if this letter was a bit of a downer. Bottoms up!

Randall Abramson, CFA

GenerationPMCA Corp.

References

- In this letter, ROE, ROIC, dividend yield, yield, and yield to maturity, are calculated for the respective Model portfolio based on the holdings as at the date of this letter of an actual representative account managed in accordance with such Model. These figures are neither a measure of results achieved nor projected future performance. The Model’s holdings, and therefore ROE, ROIC, and yields, are subject to change at any time and may differ among accounts managed based on the same Model.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

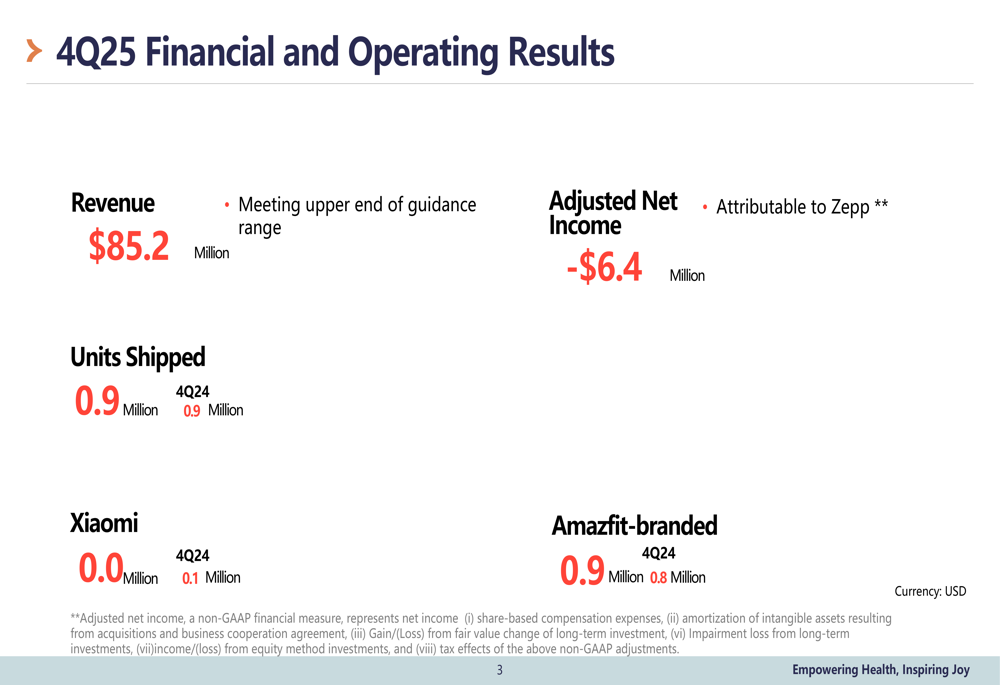

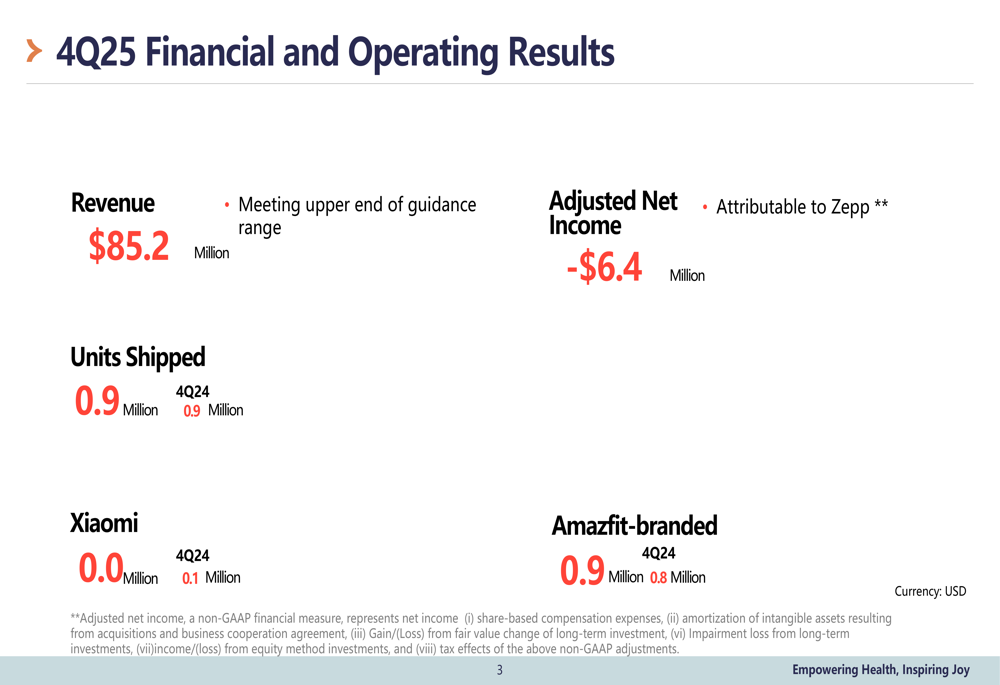

Zepp Health Q4 2025 slides: 43% revenue surge, record margins

The bank is scouting for senior executives to start operations as it wants to take a larger wallet share of corpo rate clients for whom it does debt and mergers and acquisitions (M&A) advisory currently, the people said, adding that the new vertical could be up and running in the next few months.

“It is now an open evaluation and a decision will be made in the next couple of months. The logic is to get a higher share of client wallets which continue to be serviced in India. The bank has an established business on the debt side and M&A with a lot of large clients. It makes sense to expand in this side of the business to deepen the franchise and gain market share,” said one of the persons, who did not wish to be identified.

A Barclays spokesperson declined to comment in response to ET’s queries. In January 2016, Barclays had discontinued the ECM business in India as part of a reduction in operations in nine markets, mostly in Asia, including India. The move was part of then CEO Jes Staley’s plans to reduce operations in markets where the bank was uncompetitive, in an attempt to conserve capital.

In India the bank had discontinued ECM, broking and research operations, cutting about 25 jobs, ET had reported then. Full bank operations were shut in Taiwan, South Korea, Malaysia, Thailand, Australia, the Philippines and Indonesia.

The renewed push to start ECM operations in India is aimed at ensuring that the bank offers a full bouquet of products to its clients in India. The bank services only corporate clients in the country. “When the ECM business was running in India the bank was doing well. ECM was still profitable. It suffered collateral damage because the bank decided to shut down the business in Asia, mainly because China was a difficult market to make it. This is now a fresh start,” said a second person.

Cresco Labs Will Remain Undervalued Without Any New Synergies (Rating Downgrade)

The war-torn country is battling to secure crucial funding from the IMF and EU, as well as putting up taxes.

Volatile fuel costs could add turbulence to your summer trip.

Gas prices have surged in recent weeks in tandem with war-driven volatility in crude oil markets. The national per-gallon average increased more than 10% over the past week, according to AAA, and it’s up even more in states including Utah, California, Florida and New Jersey.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

Buyside analyst covering global stocks on Seeking Alpha since 2018. I’ve been investing personally and professionally across major equity markets for about a decade. Subscribe for equity research and trading ideas.Opinions are not qualified investment or trading advice. Please do your own due diligence.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Disclaimer: All research, figures, and interpretation are provided on a best-effort basis only and may be subject to error. Any view, opinion, or analysis does not constitute as investment or trading advice; please do your own due diligence.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Darren Gordon-led Centaurus Metals has taken another important step towards a potential positive FID at its Jaguar nickel sulphide project in Brazil.

Business

Oil Price Today (March 16): Crude oil gains 1%, above $100 on Trump’s latest threat to Iran. Here’s why

Crude oil price on March 16

Brent crude also climbed by nearly a percent to trade above almost $105 per barrel in early trade. It traded marginally lower in early hours.

In a post on Truth Social, Trump said he had ordered strikes on Iranian military assets on Kharg Island on Friday but avoided targeting oil infrastructure. However, he warned that if Iran continues attacking tankers in the Strait of Hormuz, the US could reconsider its decision.

The development gains significance as Kharg Island holds critical importance for Iran’s oil exports. Data shows that nearly 90% of the country’s oil shipments pass through the island.

A direct strike on the island’s export terminal would affect the majority of Iran’s crude exports. Such an attack could also trigger retaliation from Iran, either in the Strait of Hormuz or against energy infrastructure across the region, experts say.

Separately, Iranian drones struck a key oil terminal in Fujairah in the United Arab Emirates shortly after the attacks on Kharg. Four sources said oil loading operations at Fujairah have since resumed, although it remains unclear whether activity has returned fully to normal.

Fujairah, which lies outside the Strait of Hormuz, serves as the export outlet for about 1 million barrels per day of the UAE’s flagship Murban crude, a volume that accounts for roughly 1% of global demand.The US is also evaluating several high risk options on the ground. These include raiding Iranian nuclear sites to seize enriched uranium, taking control of the Kharg Island oil hub, and occupying parts of southern Iran to secure the Strait of Hormuz. He noted that each of these options would mark a significant escalation and carry substantially higher risk, SEB analyst Erik Meyersson told Reuters.

US-Iran talks soon?

US President Donald Trump said Sunday that the United States was in discussions with Iran as the war enters its third week but that Tehran was not ready for a deal to end it.

“Yes, we’re talking to them,” Trump told reporters aboard Air Force One, without detailing the nature of such talks, when asked if there was any diplomacy under way to end a conflict that has spread across the Middle East and roiled global markets.

“But I don’t think they’re ready. But they are getting pretty close,” Trump said. Iran’s foreign minister earlier denied any talks with the United States were taking place.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

More than six weeks after 84-year-old Nancy Guthrie vanished from her Tucson-area home in what authorities describe as a targeted abduction, the high-profile investigation led by the Pima County Sheriff’s Department and FBI has produced no arrests, no confirmed sightings of the missing woman and no public identification of a suspect.

Nancy Guthrie, mother of NBC “Today” show co-anchor Savannah Guthrie, was last seen the evening of January 31, 2026, after being dropped off at her Catalina Foothills residence following a family dinner. She missed a scheduled online church service the next morning, February 1, prompting relatives to check on her around 11 a.m. They discovered her phone and other belongings still inside, with signs of disturbance including blood on the porch. Investigators quickly classified the case as a possible kidnapping, securing the home as a crime scene.

Pima County Sheriff Chris Nanos has maintained that Nancy Guthrie was “taken in the dark of night from her bed,” citing her advanced age, limited mobility and reliance on medication as evidence against voluntary departure. Doorbell camera footage released early in the probe shows a masked individual carrying a backpack near the property, believed to be the primary suspect. Officials have indicated the same person may have scouted the home previously.

As the search reached Day 44 on March 16, 2026, key developments include ongoing forensic analysis of DNA evidence from gloves and other items recovered at the scene. Sheriff Nanos told NBC News in a recent interview that investigators believe the abduction was targeted, stating, “We believe we know why he did this, and we believe that it was targeted, but we’re not 100% sure.” He expressed continued hope that Nancy remains alive, though he acknowledged the passage of time complicates the outlook.

The family, including Savannah Guthrie and siblings Annie and Camron, offered a $1 million reward in late February for information leading to Nancy’s recovery. The FBI maintains a separate reward—doubled early in the case to $100,000 or more in some reports—for tips resulting in her location or the arrest and conviction of those responsible. Tips have exceeded thousands, with the public urged to contact 1-800-CALL-FBI, tips.fbi.gov or the Pima County Sheriff’s Department at 520-351-4900.

Recent updates highlight forensic progress: The FBI recovered additional images from Nancy’s security cameras, though details remain limited as analysis continues. Sheriff Nanos has noted potential use of an internet jammer by the perpetrator to disrupt connectivity that night, prompting door-to-door inquiries in the neighborhood about service interruptions.

Savannah Guthrie, who took time away from “Today” following the disappearance, returned to the NBC studio in early March for planning purposes and made an emotional on-set appearance around March 5-6, marking her first time back in Studio 1A since late January. She has used social media for pleas, expressing faith and urging the captor to release her mother. In one video, she addressed the public directly, emphasizing Nancy’s vulnerability and the family’s desperation.

Criticism has surfaced regarding the investigation’s pace. Some reports noted early tensions between local authorities and the FBI over evidence access, though officials insist collaboration remains strong. A separate $1.35 million lawsuit against Sheriff Nanos unrelated to the case has drawn attention but not impacted the probe directly.

Other elements include purported ransom demands involving Bitcoin that surfaced early but have not been verified as legitimate. No proof-of-life contact has been confirmed. The case has drawn parallels to other missing-persons matters in Tucson, with a separate elderly disappearance in March highlighting regional concerns, though no links exist.

Experts and former agents have offered theories: Some suggest the suspect may strike again, while others note the shift from active rescue to recovery focus given Nancy’s age and health needs. A 2013 “Today” segment featuring Nancy’s bedroom has been referenced in media as potentially providing unintended details to the perpetrator, though authorities have not commented.

Family members have been publicly cleared of involvement, countering online speculation. Savannah has donated to the National Center for Missing and Exploited Children, hoping the spotlight aids other families.

As the investigation persists into its seventh week, officials stress the case is active with promising leads in DNA, video and timelines. No major public breakthrough has emerged, but Sheriff Nanos reiterated determination to pursue every angle until resolution.

The Guthries continue advocating for tips, describing Nancy as a beloved, faithful woman whose absence leaves a profound void. The community and national audience await developments in one of 2026’s most closely watched missing-persons cases.

At least eight central banks, including the U.S. Federal Reserve, the European Central Bank, the Bank of England and the Bank of Japan meet this week to set rates, in their first policy meetings since the Middle East conflict began.

Focus will be on policymakers’ assessment of the impact of higher oil prices on inflation and growth.

“The war … poses downside risk to economic growth and upside risks to inflation, so central bank responses will very much depend on the recent context, specifically whether inflation has been above, on, or below target,” said Carol Kong, a currency strategist at Commonwealth Bank of Australia.

Ahead of the meetings, the dollar retraced some of last week’s strong gains, leaving the euro bouncing slightly from a 7-1/2-month low hit earlier in the session to trade 0.14% higher at $1.1433.

Sterling was up 0.17% at $1.3245, though was not far from the 3-1/2-month low it hit on Friday as it clocked a 1.5% weekly decline.

The dollar index eased slightly to 100.20, but remained perched near last week’s 10-month high. U.S. President Donald Trump said on Sunday he is demanding that other countries help protect the Strait of Hormuz, adding that Washington is in talks with several nations about policing the critical shipping lane for oil and gas.

He warned in a separate interview with the Financial Times that NATO faces a “very bad” future if U.S. allies fail to assist in opening up the Strait.

The prospect of easing global energy disruptions sent oil prices down slightly, but markets remained in disarray with geopolitical tensions still running high and uncertainty over when the war, now in its third week, could end.

“As things stand now, the likelihood we will really see a change in current trajectory for central banks and their monetary policies around the world is, in our view, very, very limited,” said Jorry Noeddekaer, head of global emerging markets and Asia at Polar Capital, whose base case is for the war to be relatively short-lived.

RBA TO HIKE, BOJ IN DIFFICULT SPOT

The Australian dollar was up 0.55% at $0.7019, buoyed by hawkish rate expectations at home as the Reserve Bank of Australia is seen tightening policy on Tuesday.

Markets are now pricing in a 74% chance that the RBA could deliver a 25-basis-point hike.

“We are now pencilling two more hikes, one this week and another in May,” said CBA’s Kong.

“In Australia, inflation was already too high even before the Middle East conflict started, so with the new energy price shock, that will further increase risks to inflation.”

The yen meanwhile languished near the 160-per-dollar level and last stood at 159.44.

The Japanese currency has come under pressure due to the nation’s heavy reliance on the Middle East for energy supplies, with the war also throwing into question the BOJ’s rate outlook.

“For Japan, the key risk is not simply higher oil prices, but a deterioration in terms of trade driven by the costs of imported energy and logistics, compounded by yen weakness and constrained monetary policy flexibility,” said Amova Asset Management’s chief global strategist, Naomi Fink.

“Markets – especially foreign exchange – may be underestimating the probability of these pressures forcing a more difficult policy trade-off for the Bank of Japan.”

Elsewhere, the New Zealand dollar was up 0.47% at $0.5803, while the offshore yuan strengthened slightly to 6.9002 per dollar.

Top U.S. and Chinese economic officials held “remarkably stable” talks in Paris on Sunday that touched on potential areas of agreement in agriculture, critical minerals and managed trade for Trump and Chinese President Xi Jinping to consider in Beijing, sources said.

Kyle Richards ‘So Grateful’ To Attend Robert Cosby’s Funeral

money gayeb | photography sudipto | #ytshorts #viral #comedy

Oscars viewers claim Timothee Chalamet ‘lost himself’ Best Actor award after major snub

-

Tech5 days ago

Tech5 days agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

Crypto World2 days ago

Crypto World2 days agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

News Videos7 days ago

News Videos7 days ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Business5 days ago

Business5 days agoExxonMobil seeks to move corporate registration from New Jersey to Texas

-

Crypto World7 days ago

Crypto World7 days agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Addict Lip Glow

-

Tech5 days ago

Tech5 days agoChatGPT will now generate interactive visuals to help you with math and science concepts

-

Sports2 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

NewsBeat4 days ago

NewsBeat4 days agoResidents reaction as Shildon murder probe enters second day

-

Business5 days ago

Business5 days agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

NewsBeat6 days ago

NewsBeat6 days agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Business8 hours ago

Business8 hours agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Tech7 days ago

Tech7 days agoDespite challenges, Ireland sixth in EU for board gender diversity

-

Business2 days ago

Business2 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World1 day ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

NewsBeat5 days ago

NewsBeat5 days agoI Entered The Manosphere. Nothing Could Prepare Me For What I Found.

-

Business6 days ago

Business6 days agoSearch Enters 39th Day with FBI Tip Line Developments and No Major Breakthroughs

-

Business2 days ago

Business2 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Sports7 days ago

Sports7 days agoSkateboarding World Championships: Britain’s Sky Brown wins park gold

-

Crypto World6 days ago

Crypto World6 days agoWill Chainlink price reclaim $10 amid volatility squeeze?