Business

Trader’s guide to navigating supply disruption by war

Qatar’s closure of a major liquefied natural gas plant after an Iranian drone attack has taken about a third of global helium production offline, Bloomberg Economics estimates. That’s a hit to chipmakers since it’s an essential component of production and there’s no substitute.

Surging energy prices also threaten to dampen demand for semiconductors by driving up the operational costs of AI data centers.

Food and Stoves

Supply disruptions in West Asia, where India sources most of its gas, have created acute shortages in its cooking gas market. That has pummeled shares of Eternal Ltd and Swiggy Ltd as well as restaurant operator Jubilant Foodworks Ltd.

Fears of an extended cooking-gas shortage have boosted shares of manufacturers of electric cook-tops, such as TTK Prestige Ltd and Stove Kraft Ltd, as consumers look for alternatives to gas.

Automakers

Car makers may also suffer as higher oil prices threaten to stifle consumer demand. Ford Motor Co is the most vulnerable because of the disproportionate amount of its revenue that comes from oil-guzzling cars.

Toyota Motor Corp and Hyundai Motor Co may face the most impact from the decrease in East Asia sales, as the region accounts for 17% and 10% of their total sales, respectively, according to Bernstein analysts including Eunice Lee. Hyundai shares have plummeted 23% this month, with Toyota down 12%.

Retailers

Rising oil prices drive up distribution costs while also draining the discretionary spending power of consumers at the pump.

Shares of US-listed apparel brands and retailers have slid, with Lululemon Athletica Inc, Nike Inc, Macy’s Inc and RH all seeing double-digit drops this month.

Clothing suppliers in China are also bracing for higher input costs, with chemical fibers (oil-derived) such as polyester and acrylic widely used in garment manufacturing.

Fertilizers

As much as 35% of global fertilizer raw materials pass through the Strait of Hormuz, according to Morningstar DBRS analyst Andrea Petroczi-Urban. This bottleneck is expected to drive North American fertilizer prices higher as global demand intensifies. In anticipation of tightened supply, producers like Nutrien Ltd and The Mosaic Co have seen their stock prices climb.

The outlook is more somber across the Asia-Pacific region, which relies heavily on West Asian imports. Morgan Stanley economists note that Australia is particularly exposed. Stock of Dyno Nobel Ltd has fallen 9% this month, while Nufarm Ltd’s shares have declined 4%.

In India, officials have asked China to allow the sale of some urea cargoes as the war curtails the nation’s gas supplies, threatening fertilizer production in the country. Stocks including Rashtriya Chemicals & Fertilizers have dropped.

Business

Stove Kraft, TTK Prestige shares plunge up to 5% despite LPG supply squeeze fears from Israel-Iran war. Here’s why

The drop in stock prices comes as investors rushed to book profits following a massive rally last week. Further, hopes of possible talks between US and Iran also eased LPG gas fears slightly. US President Donald Trump said Sunday that the United States was in discussions with Iran as the war enters its third week but that Tehran was not ready for a deal to end it.

“Yes, we’re talking to them,” Trump told reporters aboard Air Force One, without detailing the nature of such talks, when asked if there was any diplomacy under way to end a conflict that has spread across the Middle East and roiled global markets. Iran, on the other hand, has denied the claims.

LPG supply constraint is significant for India as as it is the world’s second-largest LPG importer. Several restaurants across the country have run out of gas supplies or switched to simpler menu items that require little to no cooking gas.

For induction cooktop players, this means more sales. Tata Group’s Croma said it has observed a threefold jump in demand for induction cooktops over the past few days, The Economic Times reported earlier. Further, Stove Kraft said its average weekly online sales have jumped four times.

“At Croma, we have observed a sharp and immediate uptick in demand for induction cooktops over the past few days. Our average daily run rate has surged significantly,” Infiniti Retail Ltd (Croma) CEO & MD Shibashish Roy said.

India is also grappling with a sharp LPG shortage as the ongoing war between Iran and the US-Israel alliance has led to the prolonged closure of the Strait of Hormuz, one of the world’s most critical energy supply chokepoints. Tanker movement through the route has been severely disrupted as Iran continues to target vessels attempting to pass through the corridor. The situation has forced several global suppliers to declare force majeure on gas shipments.Despite assurances from US President Donald Trump, the strait effectively remains closed to traffic. Iran’s Islamic Revolutionary Guard Corps has warned that oil shipments from the Gulf will be blocked unless US and Israeli attacks stop.

Also Read | Mutual fund portfolio down Rs 1.5 lakh in 12 days. Is the decline due to regular plans or market volatility?

Gas crisis in India

The supply disruption linked to the closure of the Strait of Hormuz has pushed up gas prices in India. Domestic cooking gas prices have increased by Rs 60 per cylinder, while commercial LPG prices have risen by Rs 114.5.

Shortages have been reported in multiple cities including Mumbai and Bengaluru. In some areas, restaurants have warned they may have to shut operations because of inadequate fuel supplies.

Meanwhile, the Indian Railway Catering and Tourism Corporation (IRCTC) has asked all its licensees to shift to alternate cooking methods such as microwave ovens and electric induction systems at railway food centres.

Sensex, Nifty today: Catch all the LIVE stock market action here

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

Business

ETMarkets Smart Talk | Power, infra, auto sectors look attractive after correction: Devang Mehta

While the uncertain macro environment has kept investors on edge, corrections across sectors have also opened up selective opportunities. In an interaction with ETMarkets Smart Talk, Devang Mehta, Deputy Managing Director & CIO – Equity NDPMS at Spark Capital Private Wealth, said that domestic-focused sectors such as power, infrastructure, and auto are beginning to look attractive after the recent market correction.

He also advised investors to stay disciplined, continue their SIPs, and focus on long-term investing rather than reacting to short-term volatility. Edited Excerpts –

Q) Thanks for taking the time out. March has been an absolute roller coaster for equity markets not just for India but across the globe. How are you reading into markets – more pain ahead?

A) The equity markets in March 2026 have indeed experienced extreme volatility, primarily driven by the escalation of a U.S.-Israel war with Iran and the subsequent closure of the Strait of Hormuz.

This conflict has triggered a “risk-off” environment, characterized by sharp declines in global indices and a surge in crude oil prices past $100–$110 per barrel and foreign outflows as well

The conflict has disrupted roughly 20% of global oil supplies transiting the Strait of Hormuz, raising fears that oil could be on the boil. If the war continues, the collateral and economic damage could lead to more pain.

Though its next to impossible to gauge the intensity and duration of the war, long term investors have to adjust to the volatility and uncertainty.

Indian market has now been going through price correction, valuation correction and time correction since last 19 months and data typically shows that after underperformance and with earnings cycle positively coming back, one needs to stay focused and not panic.

Q) IT sector seems to be the worst hit thanks to the AI commentary but with geopolitical tensions rising other sectors have also started to see some rub-off effect. Any sector(s) that are now available at attractive lev

A) IT has particularly been a hugely underperforming sector and it has its own reasons. But as markets were settling down in February, post a decent budget, good earnings season and a bit of clarity about US tariffs, unfortunately, the Iran & US – Israel war related news took prominence and had its impact on global and our own markets.

With all the newsflow around and India’s sensitivity for the oil and gas dependence, most of our sectors and companies in the indices and even broader markets went through a severe correction.

Sectors which are domestic centric and have not much of a global exposure should ideally be sought after in the first phase.

Capex oriented sectors like power, HVDC, engineering, capital goods, infrastructure and even discretionary consumption related sectors like auto and auto components have seen meaningful corrections.

Some accumulation here would be a good start to construction of new portfolios. Niche pharmaceuticals and wellness including hospital businesses and few BFSI related companies also qualify for long term investment.

Q) What could be the good, bad and ugly for Indian markets in the near term?

A) Good – Following a sluggish 2025, India Inc. is expected to see around15% YoY earnings rebound over FY26–FY27.

With India’s valuation premium over other emerging markets compressing, expectations are high for a return of foreign capital in 2026.

Strong SIP-led inflows and retail participation continue to cushion the market against foreign investor volatility.

Headline CPI inflation printed at a benign 2.75% in January 2026, though a new series makes historical comparison difficult.

Recent pro-growth measures, including income tax & GST rate cuts and interest rate reductions (125 bps cut to 5.25% as of early 2026), aim to stimulate consumption.

Bad – The Indian Rupee recently sank to all-time lows, breaching ₹92.35 against the US Dollar, which threatens to increase “imported inflation”. Pending trade deals with the US is also a overhang. Foreign Institutional Investors have been aggressive net sellers, offloading over ₹32,800 crore in the first week of March 2026 alone.

The Ugly – A major escalation in the Middle East, such as a shutdown of the Hormuz Strait, could push oil prices to unsustainable levels, causing a severe, sudden shock to the Indian economy. If global uncertainty prompts sustained record-breaking selling by foreign institutional investors, market multiples could face intense downward pressure.

Q) FPIs have been net sellers in 2025, and the story continues in 2026 may be for a different reason now. The story seems to be changing around the FDI route as India opens channels for Chinese investment to land into several industries. What are your views?

A) FPIs have been massive net sellers in India during 2025, driven by high valuation concerns, US tariff anxieties, and a “Sell India, Buy China” trend. The record outflows in 2025 were driven by a “risk-off” sentiment due to high Indian valuations compared to its peers, weak corporate earnings, and global macro headwinds like rising US bond yields.

As of early 2026, FPIs remain cautious. While they briefly turned net buyers in February 2026 following a US-India trade deal, this reversed in March due to escalating Middle East conflicts and a weakening rupee.

India has begun relaxing FDI norms for neighboring countries, including a 60-day fast-track approval for projects, to attract manufacturing investment. This represents a shift from the 2020 restrictions, allowing Chinese capital to enter critical industries.

This policy change aims to bridge the investment gap and boost local manufacturing, even as India manages a massive trade deficit with China. It highlights a strategic move to balance security concerns with economic growth necessities.

The most striking change is the relaxation of Press Note 3 (2020), which had virtually frozen Chinese investment since the Galwan clash. The story is changing from a broad “avoid China” stance to a calibrated, strategic engagement.

Stock markets have already started pricing this in, with Electronic Manufacturing Services (EMS) and renewable energy stocks surging on the news.

Q) Rupee seems to be hitting fresh lows every week – where do you see the currency headed and how will it impact Indian markets/economy?

A) The Indian Rupee (INR) has indeed been hitting fresh record lows against the US Dollar (USD), falling past the 92 level and touching around 92.35–92.37. This weakness is driven by a combination of high geopolitical tension, rising crude oil prices, and significant foreign capital outflows.

The rupee is expected to trade in a broad 90–93 range as long as geopolitical tensions in the Middle East persist and oil prices remain high.

As a major importer of crude oil, electronics, and machinery, a weaker rupee makes these inputs significantly costlier. This feeds directly into domestic inflation, raising costs for petrol, diesel, and electronics.

The cost of importing goods is outpacing export growth, widening the current account deficit (CAD). Indian companies with large unhedged foreign currency loans face higher repayment burdens, squeezing their margins.

Q) Will Crude@$100/bbl and above hurt Indian markets and macros? We have been making an investment pitch to the world about our macro stability which could be challenged in the near future. What are your views?

A) Crude oil prices sustained above $100/bbl pose significant risks to India’s macroeconomic stability by widening the current account deficit (CAD), increasing inflation (by 35–40 bps), and potentially reducing FY27 GDP growth to around 6%.

While this challenges the investment narrative of macro stability and threatens equity market pressure, strong foreign exchange reserves (around $720 billion) and potential for a shorter-duration shock may mitigate long-term damage.

With $720 billion in forex reserves and lower global demand, this shock may be acute rather than prolonged, preventing a structural break.

While a short-term spike causes volatility, a sustained, long-term trend above $100 requires a rebalancing of portfolios towards defensives. The “macro stability” pitch is challenged, but not entirely broken unless the conflict causing the price rise persists for over a long duration.

Q) How should investors recalibrate their portfolio amid rise in volatility? Any theme/asset classes which they should go overweight or underweight on? (Assuming the person is between 30-40 years)

A) For investors aged 30-40, high volatility is an opportunity to accumulate units at lower costs rather than a reason to panic. With a long-term horizon, the goal is to maintain a high growth, yet resilient portfolio that can withstand short-term shocks.

Continue all Systematic Investment Plans (SIPs). Volatility allows SIPs to purchase a higher number of units at a lower cost, which leads to superior, long-term wealth creation.

Asset allocation according to one’s risk profile, liquidity requirements and life goals are the most critical factors. You don’t lose when markets panic, you lose when you panic.

Q) Your advise to investors of things which one must avoid doing in the current environment? We have already seen drop in SIP flows by over 3% on a MoM basis.

A) Monthly inflows hit ₹29,845 crore, down 4% from January’s ₹31,002 crore, ending a two-month streak above ₹30,000 crore. The moderation ties to the shorter month, with some end-of-month SIPs shifting to early March.

Market corrections often trigger fear, leading to panic selling, which turns paper losses into permanent losses. In all the market dips, investors who stayed invested recovered their losses, while those who panicked and sold missed the subsequent recovery, and saw a significant, realized drop in their portfolio.

Waiting for a “low point” to invest usually leads to missing out on the best days of the market. Missing the 10 best trading days in a decade can cut your long-term returns by HALF. Historically in Nifty you could have lost 82% of your wealth by sitting out just 2% of the trading days.

Trying to time the market is a losing strategy because nobody can consistently predict tops and bottoms. Think in terms of years, not months. Volatility is temporary; long-term growth is the target.

(Disclaimer: Recommendations, suggestions, views, and opinions given by experts are their own. These do not represent the views of the Economic Times)

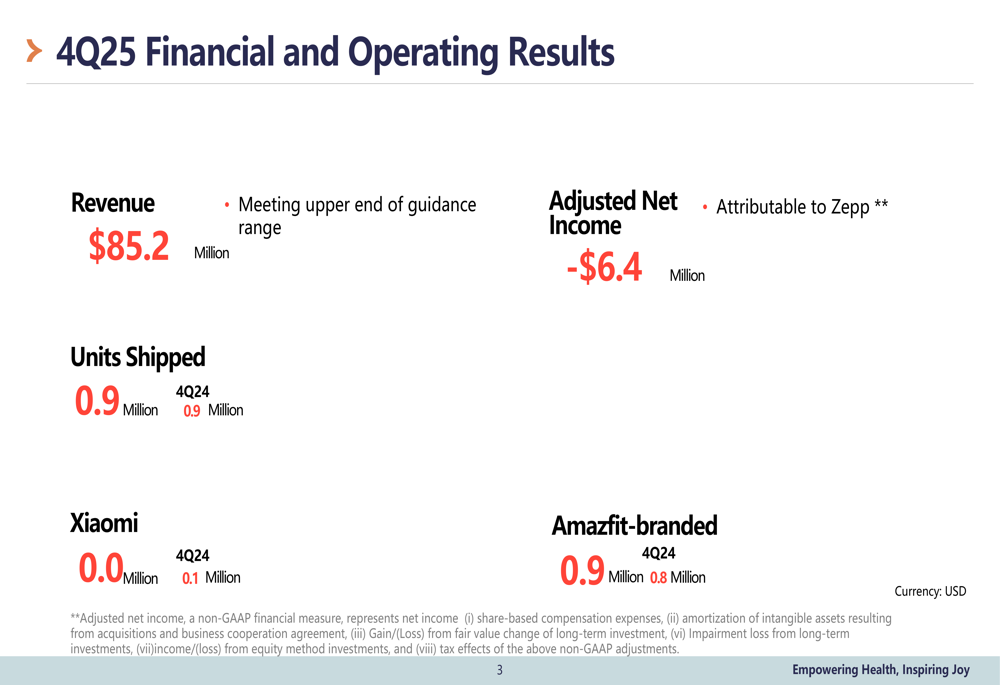

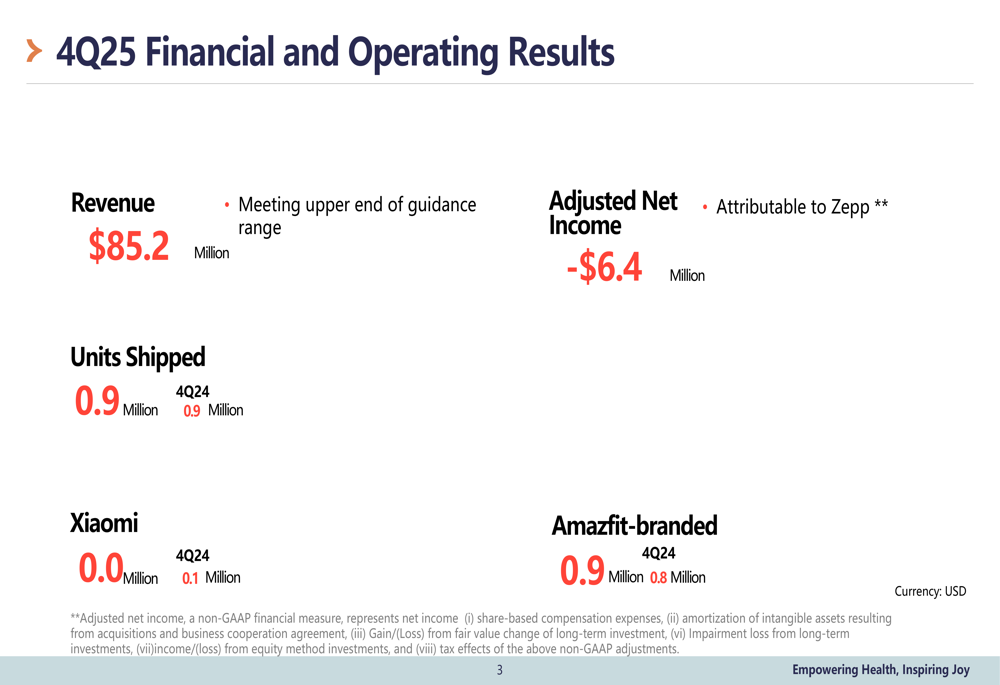

Earnings call transcript: Zepp Health’s Q4 2025 revenue surges 43%

Goldman Sachs Large Cap Growth Insights Fund Q4 2025 Commentary

Asia FX skittish as Iran fears, Fed caution boost dollar; Aussie rises before RBA

An update made to the government’s Smart Traveller includes an emphasis on what the “do not travel” advice applies to amidst the ongoing conflict in the Middle East.

Multiple countries in the Middle East, including Qatar, are currently under the government’s “do not travel” list, but it seems that it has not stopped some Aussie travellers from transiting through these countries.

Smart Traveller Clarifies ‘Do Not Travel’ Advice

A report by 9News notes that many Australian travellers rely on Middle East nations, particularly Qatar, as stopovers for Europe.

However, Smart Traveller has clarified in an update that, amidst the ongoing conflict, its “do not travel” advice given to certain Middle East applies to transit and layovers.

“We raised our level of advice for Qatar to do not travel on 28 February, due to the volatile security situation and military strikes,” Smart Traveller said on its website. “‘Do not travel’ advice applies to transit and layovers in Qatar. Even if you don’t plan to leave the airport.”

“If you travel to or transit through Qatar, you may be unable to leave,” it added. “Your safety will be at risk.”

Aside from Qatar, the United Arab Emirates and Lebanon received the same update as of press time.

Countries on the ‘Do Not Travel’ List

As of 16 March 2026, the following countries are on Smart Traveller’s “Do Not Travel” list:

- Afghanistan

- Bahrain

- Belarus

- Burkina Faso

- Central African Republic

- Chad

- Democratic Republic of the Congo

- Haiti

- Iran

- Iraq

- Israel

- Kuwait

- Lebanon

- Libya

- Mali

- Myanmar

- Niger

- North Korea

- Palestine

- Qatar

- Russia

- Somalia

- South Sudan

- Sudan

- Syria

- Ukraine

- United Arab Emirates

- Venezuela

- Yemen

Zepp Health Q4 2025 slides: 43% revenue surge, record margins

The bank is scouting for senior executives to start operations as it wants to take a larger wallet share of corpo rate clients for whom it does debt and mergers and acquisitions (M&A) advisory currently, the people said, adding that the new vertical could be up and running in the next few months.

“It is now an open evaluation and a decision will be made in the next couple of months. The logic is to get a higher share of client wallets which continue to be serviced in India. The bank has an established business on the debt side and M&A with a lot of large clients. It makes sense to expand in this side of the business to deepen the franchise and gain market share,” said one of the persons, who did not wish to be identified.

A Barclays spokesperson declined to comment in response to ET’s queries. In January 2016, Barclays had discontinued the ECM business in India as part of a reduction in operations in nine markets, mostly in Asia, including India. The move was part of then CEO Jes Staley’s plans to reduce operations in markets where the bank was uncompetitive, in an attempt to conserve capital.

In India the bank had discontinued ECM, broking and research operations, cutting about 25 jobs, ET had reported then. Full bank operations were shut in Taiwan, South Korea, Malaysia, Thailand, Australia, the Philippines and Indonesia.

The renewed push to start ECM operations in India is aimed at ensuring that the bank offers a full bouquet of products to its clients in India. The bank services only corporate clients in the country. “When the ECM business was running in India the bank was doing well. ECM was still profitable. It suffered collateral damage because the bank decided to shut down the business in Asia, mainly because China was a difficult market to make it. This is now a fresh start,” said a second person.

Cresco Labs Will Remain Undervalued Without Any New Synergies (Rating Downgrade)

The war-torn country is battling to secure crucial funding from the IMF and EU, as well as putting up taxes.

Crypto trading firm Blockfills has filed for bankruptcy

Academy disposes of Conan O'Brien “One Battle After Another”-style in bonus post-Oscars sketch

One Fan Just Proved Sims 5 Could Work in Unreal Engine 5, and He Did It in Two Weeks Flat

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

What if Bitcoin Creator Start Selling His 1 Million Bitcoin? Crypto Apocalypse?

FINANCIAL DERIVATIVES | COMMON POINTS | OPTIONS FUTURE FIRWARD SWAP | BCOM | CALICUT | SIXTH SEM

money gayeb | photography sudipto | #ytshorts #viral #comedy

-

Tech5 days ago

Tech5 days agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

Crypto World2 days ago

Crypto World2 days agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

News Videos7 days ago

News Videos7 days ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Business6 days ago

Business6 days agoExxonMobil seeks to move corporate registration from New Jersey to Texas

-

Crypto World7 days ago

Crypto World7 days agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Addict Lip Glow

-

Tech5 days ago

Tech5 days agoChatGPT will now generate interactive visuals to help you with math and science concepts

-

Sports2 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

NewsBeat4 days ago

NewsBeat4 days agoResidents reaction as Shildon murder probe enters second day

-

Business5 days ago

Business5 days agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

NewsBeat6 days ago

NewsBeat6 days agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Business9 hours ago

Business9 hours agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Tech7 days ago

Tech7 days agoDespite challenges, Ireland sixth in EU for board gender diversity

-

Business2 days ago

Business2 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World1 day ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

NewsBeat5 days ago

NewsBeat5 days agoI Entered The Manosphere. Nothing Could Prepare Me For What I Found.

-

Business6 days ago

Business6 days agoSearch Enters 39th Day with FBI Tip Line Developments and No Major Breakthroughs

-

Business2 days ago

Business2 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Sports7 days ago

Sports7 days agoSkateboarding World Championships: Britain’s Sky Brown wins park gold

-

Crypto World6 days ago

Crypto World6 days agoWill Chainlink price reclaim $10 amid volatility squeeze?