Crypto World

Bitcoin (BTC) climbs as Iran conflict tests crypto’s safe-haven case, says Bernstein

Bitcoin’s recent strength during geopolitical uncertainty reflects a fundamental shift in the asset’s ownership structure, according to Wall Street broker Bernstein.

The cryptocurrency climbed roughly 7% last week, with ether (ETH) gaining about 9%, outperforming gold and global equity indices as markets reacted to escalating global conflict. The broker said the performance highlights how institutional ownership is reshaping the market.

“We believe the combination of Strategy’s treasury model and ETFs have transformed bitcoin’s ownership structure,” analysts led by Gautam Chhugani said in the Monday report.

Strategy, which the analysts described as acting like a “bitcoin central bank of last resort,” has continued buying through the downturn. The firm extended its streak of weekly purchases, acquiring about $1.57 billion worth of BTC, according to a Monday filing.

The company, led by Executive Chairman Michael Saylor, bought 22,337 bitcoin at an average price of $70,194 each, bringing its total holdings to 761,068 BTC acquired at an average cost of $75,696 per coin.

Strategy has also expanded its preferred equity financing strategy through the STRC product, which offers investors high-yield income linked to the Secured Overnight Financing Rate (SOFR) and has generated rising trading volumes. The additional liquidity helps fund more bitcoin purchases through at-the-market offerings.

Meanwhile, spot bitcoin exchange-traded funds (ETFs) have attracted about $2.1 billion in inflows over the past three weeks, bringing ETF ownership to roughly 6.1% of total bitcoin supply. The analysts said these vehicles are increasingly drawing allocations from wealth managers, pension funds and sovereign investors.

Retail investors have been net sellers in recent months, but long-term holders remain dominant. About 60% of bitcoin supply has not moved for more than a year, a signal that many investors continue to treat the asset as a long-term store of value, the report said.

Bitcoin’s recent outperformance during geopolitical stress has also revived debate about its role as “digital gold.” While the token lagged the precious metal for much of the past year, its gains during the latest bout of global uncertainty have prompted some analysts to argue the asset is beginning to behave more like a geopolitical hedge, though the comparison remains contested.

For equity investors, Bernstein added that Strategy (MSTR) remains a high-beta way to gain exposure to bitcoin’s upside, currently trading at about a 14% discount to its bitcoin net asset value on a basic share basis.

The largest cryptocurrency was trading 4.4% higher around $73,900 at publication time. Ether, the second-largest crypto by market capitalization was up 8.4% at $2,273.

Read more: CEO of crypto investment firm Keyrock says bitcoin is undervalued, entering ‘transition year’

The U.S. Securities and Exchange Commission (SEC) ended its civil enforcement action against BitClout founder Nader Al-Naji and several related defendants, saying the decision was “based on the particular facts and circumstances of this case.”

In a joint stipulation filed March 12, the U.S. District Court for the Southern District of New York, the SEC and Al-Naji agreed to close the case, ending the litigation permanently and preventing the agency from refiling the same claims.

The SEC filed the lawsuit in July 2024, accusing Al-Naji of violating securities laws through the crypto-based social network project BitClout, later associated with the decentralized social blockchain DeSo. The SEC and Department of Justice charged Al-Naji with wire fraud and the sale of unregistered securities.

The charges claimed Al-Naji raised approximately $257 million from the sale of BitClout’s native token, BTCLT. They alleged he led investors to believe the money would be used to pay him and other BitClout employees, but instead spent “more than $7 million of investor funds on personal expenditures,” renting a mansion in Beverly Hills and “extravagant cash gifts.”

The case also named several “relief defendants,” including Buse Desticioğlu Al-Naji, Joumana Bahouth Al-Naji, Intangible Holdings LLC, Firestorm Media LLC, Viridian City LLC and the DeSo Foundation.

BitClout, which debuted in early 2021, was promoted as a proof-of-work blockchain designed to run and monetize social media, but quickly drew controversy. The platform automatically created profiles for prominent figures by scraping their accounts on X, then still known as Twitter, without consent, prompting a cease-and-desist letter from law firm Anderson Kill alleging violations of California’s right-of-publicity law, CoinDesk reported at the time.

Critics also argued the project’s “creator coin” model could incentivize reputational attacks, because users could profit from shorting someone’s token while damaging their reputation. Others raised concerns that users had to convert bitcoin into BitClout’s BTCLT token to use the platform without an easy way to convert it back, effectively locking funds on the site.

Despite the backlash, Al-Naji said the project attracted backing from major venture firms including Andreessen Horowitz, Sequoia, Coinbase Ventures and Digital Currency Group.

Al-Naji and the relief defendants waived any claims for attorney’s fees or damages related to the investigation or litigation.

TLDR

- Olema Pharmaceuticals (OLMA) shares surged 8.5% Monday following a Q4 earnings beat, posting a loss of $0.50 per share versus the anticipated $0.51.

- The biotech firm recorded a GAAP net loss of $46.1 million in Q4 2025 and $162.5 million across the full fiscal year.

- Stifel maintained its Buy rating with a $48 price target post-earnings, highlighting the company’s cash reserves lasting through mid-2028.

- Roche’s recent persevERA trial failure has sparked concerns regarding Olema’s OPERA-02 trial prospects.

- Wall Street consensus leans “Moderate Buy” with a mean price target of $41, while shares are down 41% YTD despite a 234% surge over the trailing year.

Olema Pharmaceuticals (OLMA) shares rallied 8.5% during Monday’s trading session following the release of fourth-quarter results that narrowly topped analyst projections. The stock peaked at $16.07 intraday before closing near $15.96, marking a solid gain from the previous close of $14.71.

Olema Pharmaceuticals, Inc., OLMA

The biopharmaceutical company disclosed a quarterly loss of $0.50 per share for Q4 2025, surpassing the Street’s expectation of a ($0.51) loss by one cent. While modest, the earnings surprise proved sufficient to drive investor enthusiasm.

For fiscal year 2025, Olema recorded a GAAP net loss totaling $162.5 million. The fourth quarter alone contributed $46.1 million to that deficit. Management opted not to host an earnings conference call following the release.

The stock’s performance has been nothing short of volatile. While OLMA has delivered a remarkable 234% return over the past twelve months, shares had tumbled 41% year-to-date prior to Monday’s rally.

Trading activity registered at 518,220 shares — significantly below the stock’s typical daily volume of approximately 1.6 million. The subdued volume suggests investors may be proceeding cautiously rather than piling in aggressively.

Analyst Reaction

Stifel responded swiftly to the earnings release, reaffirming its Buy rating and $48 price objective. The firm emphasized Olema’s financial runway stretching into mid-2028 as a significant advantage, providing adequate resources to reach several critical milestones ahead of palazestrant’s anticipated commercial debut.

Palazestrant is currently in development for second- and third-line metastatic breast cancer treatment, with market entry projected for 2027.

The broader analyst community maintains an optimistic outlook. Ten analysts have assigned Buy ratings to the stock, with one Hold and one Sell rating. The consensus price target stands at $41.00 — representing substantial upside from current trading levels.

Oppenheimer reaffirmed its Outperform rating on March 9th. JPMorgan lifted its price target from $29 to $32 last November, maintaining an Overweight stance. TD Cowen also holds a Buy rating, highlighting palazestrant’s superior exposure compared to rival therapies.

H.C. Wainwright reduced its target to $38 but retained its Buy rating in response to recent clinical trial developments.

The Roche Factor

Earlier this month, Roche announced that its persevERA clinical trial — assessing giredestrant combined with palbociclib in first-line metastatic breast cancer patients — failed to achieve statistical significance on its primary progression-free survival endpoint. While a favorable numerical trend was observed, the miss carries significant implications.

The persevERA outcome is considered a potential indicator for Olema’s own Phase 3 OPERA-02 trial, which is evaluating palazestrant. Topline results from OPERA-02 aren’t anticipated until 2028 at the earliest.

Stifel noted that Roche’s complete persevERA dataset will likely be unveiled at ASCO 2026, which could represent the next significant catalyst — or obstacle — for OLMA shares.

Regarding financial health, Olema maintains a stronger cash position than debt, boasting a current ratio of 8.03. The stock’s 50-day moving average currently sits at $24.18, considerably above Monday’s trading range.

Institutional ownership accounts for 91.78% of outstanding shares. Meanwhile, company insiders have been net sellers — divesting approximately 805,501 shares valued at roughly $23 million during the past three months.

The company currently commands a market capitalization of approximately $1.09 billion.

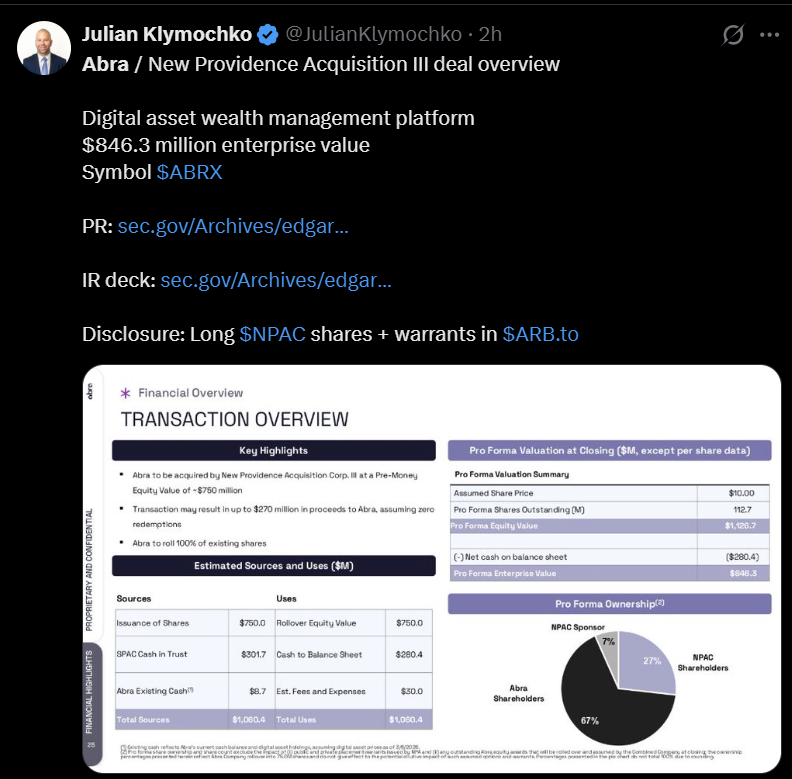

Digital asset wealth management platform Abra is going public through a reverse merger with special purpose acquisition company New Providence Acquisition Corp. III, marking the latest attempt by a crypto company to access public markets as investor interest in the sector rebounds.

On Monday, Abra announced that it had signed a definitive agreement with the blank-check company, or SPAC, valuing the crypto wealth manager at a pre-money equity valuation of $750 million.

Existing investors, including Pantera Capital, Blockchain Capital, RRE Ventures, Adams Street and SBI, will roll over their shares into the combined entity rather than cashing out.

Following the transaction, the new entity is expected to trade on the Nasdaq under the ticker symbol ABRX.

The public company will focus on crypto wealth management, offering custody and segregated accounts, yield strategies, crypto-backed loans, treasury management and trading services.

Founded in 2014 by CEO Bill Barhydt, Abra operates a digital asset platform serving high-net-worth investors, institutions and family offices. Its investment management arm, Abra Capital Management LP, is registered as an investment adviser with the US Securities and Exchange Commission, allowing it to provide portfolio management services to clients.

Abra has been restructuring its US operations following regulatory scrutiny. In 2024, the company reached a settlement with regulators in 25 US states over its Abra Earn crypto lending product, agreeing to return assets to investors and wind down the program for US clients. The settlement came as the company shifted its focus toward institutional and wealth management services.

Related: VC Roundup: Big money, few deals as crypto venture funding dries up

Crypto companies increasingly eye public markets

Abra is one of several digital asset companies seeking public listings as the industry looks to attract traditional capital.

In the past year, SPACs have drawn renewed interest as a route for crypto-related companies to enter the public markets, Jessica Groza, partner with Kohrman Jackson & Krantz, said. “While this model offers rapid liquidity, valuation flexibility, and access to institutional capital, it also carries substantial risks: volatility, structural dilution, opaque disclosures, technical complexity and regulatory uncertainty.”

Traditional initial public offerings (IPO) have been the preferred route for several big name crypto players over the past year, including stablecoin issuer Circle Internet Group, which listed on the New York Stock Exchange in June 2025, and crypto exchange Gemini, which debuted on Nasdaq later that year.

Blockchain-focused financial services company Figure Technologies and institutional trading platform Bullish also went public via IPO during the same period.

Other companies are reportedly exploring public offerings as well, including hardware wallet maker Ledger and institutional crypto custodian Copper.

Related: Crypto Biz: Circle stock defies Wall Street and digital asset selloff

Crypto World

Metaplanet Raises $531M Through Share Placement and Warrants to Accelerate Bitcoin Accumulation

TLDR:

- Metaplanet raised ~$255M instantly through a share placement priced at a 2% market premium.

- Fixed-strike warrants at a 10% premium could release an additional $276M if fully exercised.

- The warrant structure monetizes equity volatility instead of forcing large-scale shareholder dilution.

- All capital raised from the $531M structure is earmarked exclusively for Bitcoin accumulation.

Metaplanet, Japan’s publicly listed Bitcoin treasury company, has secured up to $531 million in new capital. The fundraise combines a direct share placement and a series of fixed-strike warrants.

New shares were sold to institutional investors at a 2% premium to market, raising approximately $255 million. The warrants, set at a 10% premium, add potential access to another $276 million upon exercise.

Together, the instruments position the company for a major push toward its 210,000 BTC target.

A Two-Part Capital Raise Designed Around Bitcoin

The share placement portion of the raise closed with global institutional investors at a 2% premium over market price.

Metaplanet brought in roughly $255 million through this transaction, representing the confirmed and immediate capital from the raise.

The involvement of international institutions in the placement reflects broader interest in Metaplanet’s Bitcoin strategy. This part of the deal stands on its own and delivers capital to the company’s treasury regardless of the warrants.

The second component consists of fixed-strike warrants issued to investors at a 10% premium above market. These warrants can generate an additional $276 million for Metaplanet if holders choose to exercise their rights.

Exercise is most likely when the company’s share price stays at or above the warrant’s strike price over time. Until then, Metaplanet holds the premium income collected from selling the warrants to investors.

CEO Simon Gerovich shared the details on social media, confirming the total potential capital at $531 million. He described the warrants as tools designed to monetize the company’s equity volatility. Every dollar from the full raise, if realized, is earmarked for Bitcoin accumulation.

Warrant Structure Captures Equity Volatility to Fund Bitcoin Purchases

The warrant mechanism is a key distinction between this raise and a plain secondary share offering. In a standard share sale, a company issues new equity and immediately dilutes existing shareholders in the process.

Metaplanet’s approach uses the market’s appetite for its stock as a funding source without forcing dilution at scale. This design gives the structure an edge in managing shareholder perception while raising capital.

Investors who buy the warrants are paying for the option to acquire shares at a locked-in price in the future. Metaplanet receives that payment upfront and channels it alongside the share placement proceeds.

Both pools of capital flow into Bitcoin purchases. Bitcoin was priced near $73,394 per coin at the time Gerovich made the announcement.

Metaplanet has become Japan’s most prominent corporate Bitcoin holder and is frequently compared to MicroStrategy.

The company has been building its Bitcoin reserve relentlessly, guided by a long-term target of 210,000 BTC. This raise brings it measurably closer to that goal.

The next thing to track is full warrant exercise, which would deliver the entire $531 million into Bitcoin. If the stock holds, all the capital flows directly into Bitcoin purchases.

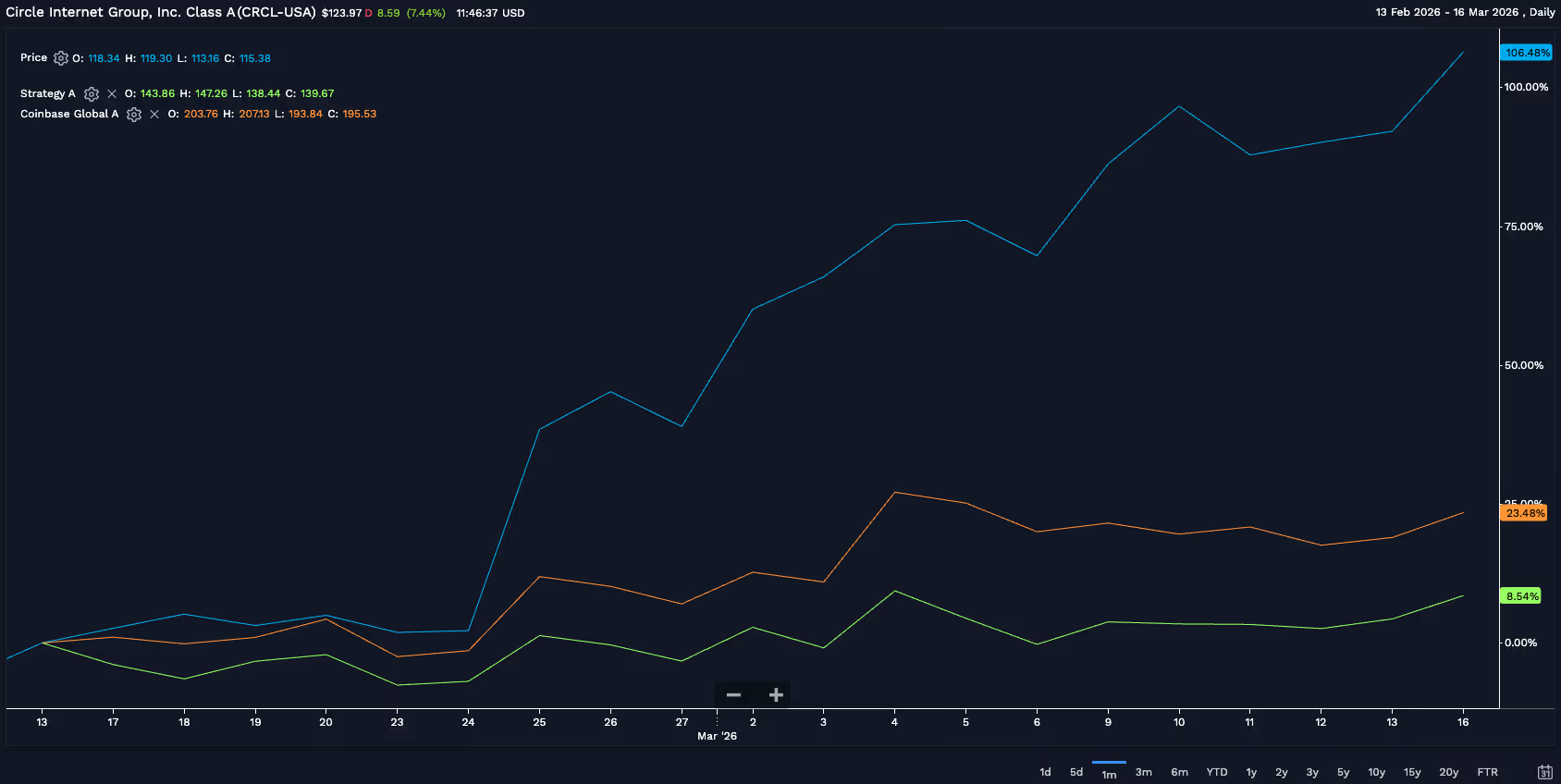

Shares of stablecoin issuer Circle (CRCL) have surged more than 100% over the past month, turning what many investors once viewed as one of the most conservative corners of crypto into one of the market’s hottest trades.

The rally gained momentum Monday, with the stock climbing another 8% to $124.37, outpacing other crypto-linked equities. Meanwhile, Michael Saylor’s Strategy (MSTR) and crypto exchange Coinbase (COIN) are up 23% and 8.5% in a month, respectively.

The move also coincided with recent bullish analyst calls. Clear Street upgraded Circle to Buy from Hold and raised its price target to $136 from $92, while Mizuho also raised its price to $120 from $100, pointing to improving fundamentals around the company’s USDC stablecoin.

Even Circle’s biggest bear, Compass Point’s Ed Engel, upgraded the company’s rating to Neutral from Sell in January. Currently, Seaport Global’s analyst is the most bullish on the stock, with a $280 price target, according to FactSet data.

Hottest crypto trade

The surge reflects a growing view among investors that Circle sits at the center of several powerful trends shaping the digital asset industry, from tokenized financial products to AI-driven payments.

Macro conditions may also be playing a role. Escalating tensions in Iran and rising oil prices have fueled concerns that inflation could remain sticky, potentially delaying Federal Reserve rate cuts. That scenario could benefit Circle because the company earns a large share of its revenue from interest on reserves backing USDC, its dollar-pegged stablecoin. Higher interest rates typically translate into stronger earnings for stablecoin issuers.

Circle’s core product is USDC, a digital token designed to maintain a value of $1. The stablecoin runs on public blockchains and allows users to move dollars globally, settle trades and post collateral without relying on traditional banking rails.

Unlike many crypto assets, demand for stablecoins often grows even when markets decline. Since October 2025, the total crypto market capitalization has fallen roughly 44%, while USDC’s market cap has remained relatively stable, according to Clear Street. The difference reflects USDC’s role as a payment infrastructure rather than a speculative asset.

Another driver is the rapid expansion of tokenized financial assets, which bring instruments like U.S. Treasuries and credit funds onto blockchain networks. Many of these products use USDC to process subscriptions, redemptions and payments. BlackRock’s tokenized Treasury fund BUIDL, for example, has grown to more than $2 billion in assets since launching in 2024.

Clear Street estimates the market for tokenized assets has expanded from about $1.5 billion in early 2023 to roughly $26.5 billion today, a trend closely tied to rising demand for stablecoins.

“The scale of this opportunity is significant,” Clear Street’s Lau said.

Other emerging use cases could add further momentum. Prediction markets such as Polymarket processed more than $22 billion in trading volume in 2025, largely using USDC as the settlement currency.

Analysts also point to AI-driven commerce as a longer-term catalyst. Autonomous software agents increasingly require programmable payment tools to purchase data, services or computing power. Early data suggests stablecoins already dominate these transactions, with roughly 98% of AI-agent payments settled in USDC.

Regulation could provide another boost. Analysts say the chances of U.S. crypto legislation advancing have improved after President Donald Trump voiced support for the proposed CLARITY Act, which would clarify oversight of digital assets and could encourage greater institutional participation.

For now, the result is a rare market moment: a company built around one of crypto’s most stable assets has become one of its fastest-rising stocks.

“We believe the Street has under-estimated the impact of tokenization, prediction markets, war and AI on USDC,” Lau noted.

Read more: Circle overtakes BlackRock in tokenized Treasuries as market hits record $11 billion

BlackRock’s ETHB staking ETF routes 70–95% of its Ethereum into validators run by Figment and others.

Summary

- ETHB is BlackRock’s first Ethereum ETF that adds staking rewards on top of spot exposure, with roughly 70–95% of ETH staked at any given time.

- Figment runs part of the validator infrastructure for ETHB alongside Galaxy Digital and Attestant, handling block proposals, attestations, and network security duties for the fund’s staked ETH.

- The ETF launched with about $100–107m in assets, did roughly $15.5m in first-day volume, and passes around 82% of gross staking rewards to shareholders, with a 0.25% fee cut to 0.12% on the first $2.5b for a year.

BlackRock’s new iShares Staked Ethereum Trust ETF (ETHB) is pulling institutional staking into the ETF wrapper — and delegating a crucial piece of that infrastructure to Figment. The fund, listed on Nasdaq under the ticker ETHB, is BlackRock’s first crypto product that offers staking rewards on top of spot exposure, staking between roughly 70% and 95% of its ether holdings through professional validator operators. Figment has been named one of the key node operators for ETHB, responsible for running Ethereum validation infrastructure, processing transactions, and helping secure the network on behalf of the trust.

ETHB quietly marks a structural shift in how traditional finance can access Ethereum’s (ETH) proof‑of‑stake economy. At launch, the ETF came to market with around $100–107 million in initial assets and generated about $15.5 million in trading volume on its first day, according to multiple data providers. Under normal conditions, the fund stakes most of that ether, returning roughly 82% of gross staking rewards to shareholders, with the current implied annualized yield around 3.1%, while BlackRock and its partners retain the remainder as fees. Management fees are set at 0.25%, temporarily reduced to 0.12% on the first $2.5 billion in assets for the first year, a pricing structure designed to pull flows away from un‑staked spot products.

Figment’s role is central to that pitch. As one of Ethereum’s largest institutional staking providers, the company operates validators that handle block proposals and attestations for ETHB’s staked share of ether, alongside other providers such as Galaxy Digital and Attestant. By outsourcing validation to specialist firms instead of building its own infrastructure, BlackRock can offer regulated clients exposure to staking yields while keeping operational risk and technical complexity at arm’s length. That model also gives Ethereum another anchor tenant in its validator set, deepening the pool of professionally run nodes that secure the network.

For Ethereum itself, the timing is favorable. ETH is trading around $2,201, up roughly 6.8% in the last 24 hours, with a 24‑hour low near $2,041.70 and high just above $2,200, on nearly $27.76 billion in volume. Staked ether has already hit record highs on‑chain, and the arrival of a yield‑bearing BlackRock ETF that locks up a large portion of its holdings reinforces that supply sink while giving institutions a familiar wrapper for participating in Ethereum’s security budget. For live data, readers can follow crypto.news’ dedicated Ethereum price page, and for more on ETF‑driven flows and Ethereum’s evolving role, see our recent coverage of Bitcoin ETF inflows after Iran tensions, analysis of macro shocks and BTC price volatility, and Michael Saylor’s continued treasury‑driven Bitcoin accumulation.

The Ethereum Foundation’s new mandate — a sweeping document released Friday to clarify the organization’s role and principles — sparked a torrent of reactions, with supporters praising it as a long-overdue articulation of the blockchain’s ethos and critics saying it reinforces the foundation’s hands-off approach at a time when Ethereum needs stronger leadership to meet the growing needs of institutions.

The 38-page document lays out what the foundation described as a constitutional guide to its mission, emphasizing its role as a neutral steward rather than a centralized authority. The mandate frames the foundation’s job as maintaining Ethereum as a decentralized and resilient infrastructure while supporting the protocol layer and public goods across the ecosystem.

The document arrived at a pivotal moment for Ethereum. The network has matured into one of the world’s largest crypto ecosystems, and the foundation itself has gone through leadership changes and debates over how actively it should steer development.

Over the weekend, reactions on X quickly divided into two camps.

Critics: Not focused on products and institutions

Critics were quick to argue the mandate was overly philosophical and failed to address Ethereum’s need to compete for real-world adoption — particularly as institutional interest in blockchain grows.

Dankrad Feist, a former Ethereum Foundation researcher and key contributor to Ethereum’s scaling roadmap, said the document does little to address practical business development concerns about how the ecosystem serves real users.

“The fundamental problems remain: there are very few voices in ACD caring about real world Ethereum usage. There is nobody doing Ethereum BD (everyone else who is doing this also has their own separate interests),” he wrote in a post on X, referring to the two-weekly “all core developers” call.

Others suggested the mandate risks reinforcing a status quo in which the foundation holds significant soft influence without clearly defined responsibilities.

Yuga Cohler, an engineer at Coinbase, raised concerns the foundation may be focusing too heavily on ideological principles at a time when Ethereum faces increasing competition for institutional capital.

“Just as Netscape wasted time on a rewrite from version 4 to 6 at a time when Microsoft was absolutely killing them, the EF insists on focusing on cypherpunk values at a pivotal time when the institutions are finally coming onchain – often to other networks,” he wrote. “An EF determined to win would focus on how to make Ethereum the best chain for finance. That’s not what it’s doing today.”

Supporters: A clear statement of values

Others in the community welcomed the mandate as a reaffirmation of the network’s foundational principles.

Chris Perkins, president and managing partner at crypto investment firm CoinFund, said the document helps clarify the foundation’s purpose as a nonprofit steward of the ecosystem.

“The @ethereumfndn is a non-profit. Remember this. It makes sense for it to focus on vision, values and stewardship. I think its goals (censorship resistant, open source, private, and secure–CROPS) make sense,” he said in a post on X.

Taylor Monahan, a former Metamask employee and longtime Ethereum contributor, similarly described the mandate as a needed reminder of the foundation’s role, pushing back on critics who said the organization needs to operate like a product company.

“Users do not use blockchains. They use products. The EF is not building a product. They are building a blockchain. A platform. That allows anyone to permissionlessly build whatever the f** they want,” she wrote in her post. “I know it’s confusing bc there are a lot of shallow, single-purpose blockchains out there.”

Infrastructure firms in the Ethereum ecosystem also voiced support for the mandate.

Nethermind, a company that develops one of blockchain’s core client software implementations, said the document reflects many of the properties institutional buyers already look for when evaluating blockchain infrastructure.

“The EF Mandate codifies the properties institutional procurement already evaluates: operational resilience (security), data protection (privacy), no vendor lock-in (open source), and platform neutrality (censorship resistance),” the firm wrote in a post. “The @ethereumfndn protects the protocol. @Nethermind builds what institutions deploy on it.”

Supporters largely framed the mandate as a reaffirmation of Ethereum’s long-standing philosophy: maintaining a minimal base layer while enabling innovation at the application and infrastructure levels.

The broader debate

The debate surrounding the mandate reflects a deeper question about Ethereum’s identity as it grows.

The Ethereum Foundation has historically positioned itself as a coordinator of research, funding and ecosystem development, not a central governing authority. The new mandate appears designed to reinforce that philosophy, emphasizing principles such as censorship resistance, open-source development, privacy and security.

But as Ethereum becomes increasingly significant to global finance and digital infrastructure, questions about who — if anyone — speaks for the network, and how decisions are made, have become harder to avoid.

Read more: Ethereum Foundation publishes new mandate defining its role, core principles

And why DAPA is building the privacy layer the world actually needs

You might think privacy in crypto and other finacial transactions is a niche concern — the territory of paranoid technologists and whistleblowers. You would be wrong. In 2026, financial privacy is one of the most pressing issues facing ordinary people, businesses, and entire economies.

Blockchain technology promised freedom and transparency. But transparency cuts both ways. When every transaction you ever make is permanently recorded on a public ledger — visible to anyone with an internet connection — you have traded one kind of surveillance for another.

This is the problem that privacy coins exist to solve. And DAPA is solving it in a way that no other project has managed before.

The Transparency Trap

Bitcoin and Ethereum are often described as anonymous. They are not. They are pseudonymous — your real name is not attached to your wallet address, but everything else is.

Every transaction you make, every wallet you interact with, every balance you hold — it is all there, permanently, on a public blockchain. Sophisticated chain analysis tools used by exchanges, governments, and data brokers can often trace pseudonymous wallets back to real people with alarming accuracy.

Consider what this means in practice:

- A business rival can monitor your company’s payment flows in real time

- An employer can see exactly how much you were paid by previous clients

- A vendor you pay once can see your entire transaction history

- Governments can freeze assets based on wallet associations, not individual actions

- Data brokers can build detailed financial profiles and sell them

This is not hypothetical. It is happening right now, at scale. The open ledger that makes blockchain trustworthy is the same feature that makes it a surveillance tool.

What Privacy Coins Actually Do

Privacy coins are cryptocurrencies built from the ground up to shield transaction details from public view. The goal is simple: allow two parties to transact without broadcasting the details to the entire world.

But not all privacy coins are built equally. The approaches vary enormously in both technique and strength:

Mixing and tumbling

Early privacy approaches tried to obscure transactions by mixing coins from many users together, making it harder to trace the origin. This is relatively weak — determined analysis can often unpick the mix, and it provides no protection for balances.

Ring signatures and stealth addresses

Coins like Monero use ring signatures to blur which input actually signed a transaction, combined with stealth addresses to hide the receiver. This is significantly stronger, but the cryptographic approach has known theoretical weaknesses under certain conditions.

Zero-knowledge proofs

Zcash pioneered the use of zk-SNARKs — a form of zero-knowledge proof — to allow transactions to be verified as valid without revealing any of their contents. This is mathematically powerful but computationally expensive and complex to implement correctly.

Homomorphic encryption

This is where DAPA sits. Homomorphic encryption allows computation to be performed directly on encrypted data — without ever decrypting it. In the context of a blockchain, this means transaction amounts can be verified as mathematically correct while remaining completely hidden. It is arguably the most cryptographically sound approach available.

Why 2026 Is the Tipping Point

Privacy concerns in crypto are not new. But several converging forces have made 2026 a critical year for the sector:

Regulatory pressure is intensifying

Across Europe, North America, and Asia, regulators are pushing for greater blockchain surveillance capabilities. Know-Your-Customer requirements, travel rules for crypto transfers, and outright bans on privacy coins in certain jurisdictions are becoming more common. For ordinary users, this creates a genuine risk that financial privacy will simply be legislated away.

On-chain analytics has matured

The tools available to trace blockchain transactions have become extraordinarily sophisticated. Companies like Chainalysis and Elliptic can now attribute a high percentage of pseudonymous transactions to real identities. For most mainstream blockchains, meaningful anonymity no longer exists in practice.

Digital currencies are expanding

Central Bank Digital Currencies are being rolled out or piloted in dozens of countries. These government-issued digital currencies are, by design, fully traceable. As more transactions move onto these rails, the value of genuinely private alternatives increases dramatically.

Data breaches are normalised

Exchange hacks, data leaks, and insider threats mean that even data you intend to keep private can be exposed. Building privacy at the protocol level — rather than relying on a centralised party to keep your data safe — is the only robust approach.

What Makes DAPA Different

DAPA is not simply another privacy coin. It is a ground-up reconstruction of what a privacy-first blockchain should look like, built with modern cryptography and a modern consensus architecture.

ElGamal homomorphic encryption

DAPA uses the ElGamal encryption — a well-studied, battle-tested cryptographic scheme — to encrypt all transaction amounts on-chain. The blockchain can verify that inputs equal outputs (no coins are created) without ever learning the actual values involved. Your balance is encrypted. Your transfer amounts are encrypted. The network validates mathematically, not by reading your data.

BlockDAG architecture

Rather than a traditional linear blockchain, DAPA uses a Directed Acyclic Graph structure. This allows multiple blocks to be produced in parallel and referenced simultaneously, dramatically increasing throughput without sacrificing security. The result is a network that is faster, more resilient to forks, and better suited to high-volume payment usage.

Built in Rust

The entire DAPA daemon is written in Rust — a systems programming language chosen for its memory safety guarantees and performance characteristics. Rust eliminates entire classes of security vulnerabilities that plague C and C++ codebases, making DAPA’s core infrastructure significantly more robust.

Built for Total privacy

DAPA codebase provides a solid technical foundation, modified to implement full homomorphic encryption across the transaction model. This is not a rebrand — it is a genuine technical departure from the standard privacy blochain model.

The DAPA Ecosystem

DAPA is not just a coin — it is a growing ecosystem of tools designed to make private transactions genuinely accessible to everyone with a minimal cost:

- DAPA Coin — the core privacy currency, running on the live mainnet

- Web Wallet — a browser-based wallet at webwallet.dapahe.com for easy access from any device

- Zodiac Wallet — a desktop GUI wallet for Windows and Linux, available at dapahe.com

- DapaPay — a brand new payment platform at dapapay.com, bringing DAPA transactions to merchants and everyday use

- Block Explorer — full transaction and network visibility at dapaexplorer.cc

The combination of strong privacy cryptography with a practical, usable ecosystem is exactly what the sector has been missing.

The Genesis Sale: Getting In Early

DAPA is currently in its Genesis Sale — the earliest and most advantageous opportunity to acquire DAPA coins before wider exchange listings.

⚡ Genesis Sale — Tier 1 Details

- Price: $0.12 per DAPA

- Bonus: +50% coins on every purchase

- Supply: 2.5 million coins available in Tier 1

- Payment: PayPal, Stripe, Payoneer

- Buy now: dapacurrency.com

Early participants in projects with genuine technical differentiation have historically seen significant returns as the project matures and gains wider adoption. DAPA’s combination of homomorphic encryption, blockDAG architecture, and a live working ecosystem places it in a small category of projects with real substance behind the token.

The Bottom Line

Financial privacy is not a fringe concern. It is a fundamental right that the original promise of cryptocurrency implied but rarely delivered. The tools to build genuinely private money exist — ElGamal encryption, homomorphic computation, blockDAG consensus — and DAPA has assembled them into a working system.

Whether you are a privacy advocate, a developer interested in the cryptography, or simply someone who believes your financial data should belong to you, DAPA represents one of the most technically credible privacy projects currently in active development.

The Genesis Sale is live. The wallets are ready. The network is running.

It is time to take privacy seriously.

Crypto World

Bitcoin Price Soars to $74K, but Investors Are Already Eyeing New Altcoin GCoin This Week

Bitcoin’s price surged above $74,400 today, marking a multi-week high and reigniting optimism across the broader cryptocurrency market, as evidenced by the rise in altcoins.

The rally came amid renewed buying pressure, a wave of institutional demand, and yet another behemoth purchase by Michael Saylor’s Strategy.

Bitcoin Climbs to $74K as Market Momentum Builds

BTC rose to around $74,400 earlier today, then dipped slightly to its current price of about $73,700. The bulls regained control amid anticipation of macroeconomic developments, including inflation data releases, PPI, and more.

The move comes on the back of considerable institutional involvement last week. Data shows that investors in BlackRock’s IBIT BTC ETF bought a total of $600 million last week, marking five consecutive days of positive inflows.

Moreover, news just broke out that Strategy (formerly MicroStrategy) has bought another $1.57 billion worth of BTC during the same week, at an average price of around $70,194 per bitcoin. The largest corporate holder now owns a whopping 761,068 BTC worth $57.61 billion.

Today’s increase led to more than $300 million in liquidated short positions, which indicates the prevalent dominance of the bulls, at least for the time being. The good news is that this Bitcoin momentum is also transitioning through the rest of the market, and many altcoins are also charting considerable increases, painting the entire heatmap green.

With Bitcoin already testing major resistance near $74K, some analysts say the next phase of the market could be consolidation or a breakout. These are market conditions that generally favor altcoins.

GCoin Shines as Investor Focus Amid Favorable Market Conditions

As Bitcoin captures headlines with its latest rally, the attention is also shifting toward emerging altcoins that promise real-world utility in revenue-generating sectors. One of the projects gaining traction among early adopters is GCoin, the native utility token of the PlayNance ecosystem.

GCoin is designed to power a fully-fledged Web3 gaming and entertainment infrastructure, enabling real-time on-chain interactions through multiple platforms and digital experiences. Within its ecosystem, the token serves as a powerful economic engine, facilitating transactions, gameplay mechanics, and rewards.

According to the official website, the token is already actively used across the PlayNance ecosystem, powering:

- 10,000 on-chain games across many platforms

- 2.5M live sports events annually

- Millions of ongoing predictions and crash market interactions

The ecosystem itself processes an average of 1.5 million on-chain transactions every day, all executed using G Coin as the settlement and utility layer. PlayNance itself was founded in 2020 and specializes in non-custodial financial games and entertainment. Key products within the ecosystem include PlayW3’s social gaming aspect, PlayBlock, designed for high-frequency, real-time gasless transactions, and more.

G Coin is having its token generation event (TGE) in less than 36 hours, but interested parties can already buy the altcoin on its official sales page.

So far, almost 14 billion tokens have been sold, and the price is structurally increasing. This means that users have to participate quickly to lock in more favorable conditions. The project’s current market cap is around $40 million, and there are more than 200,000 holders, underscoring strong interest in what the project has to offer.

The smart contract has been audited by the market leader, CertiK.

Disclaimer: The above article is sponsored content. CryptoPotato doesn’t endorse or assume responsibility for the content, advertising, products, quality, accuracy, or other materials on this page. Nothing in it should be construed as financial advice. Readers are strongly advised to verify the information independently and carefully before engaging with any company or project mentioned and to do their own research. Investing in cryptocurrencies carries a risk of capital loss, and readers are also advised to consult a professional before making any decisions that may or may not be based on the above-sponsored content.

Readers are also advised to read CryptoPotato’s full disclaimer.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

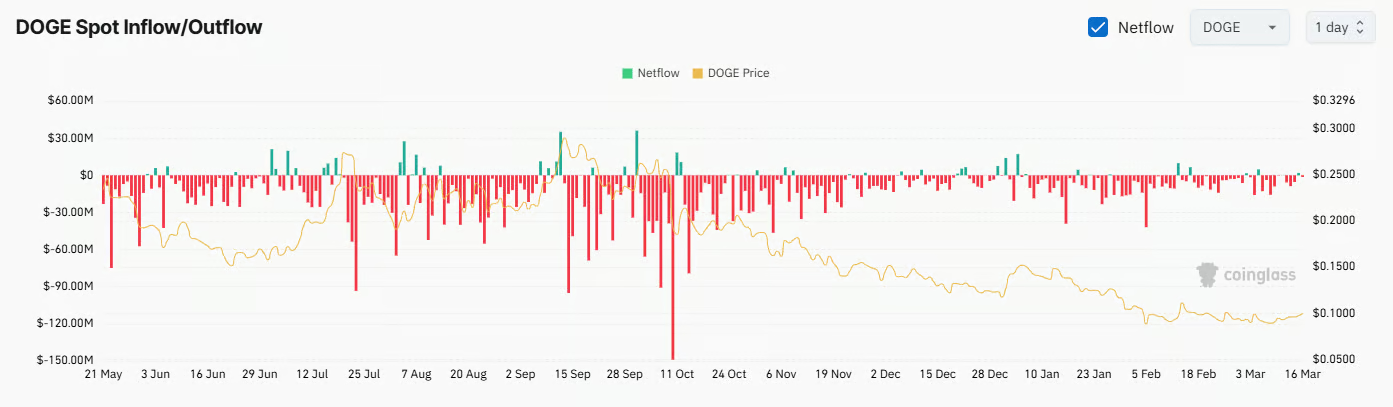

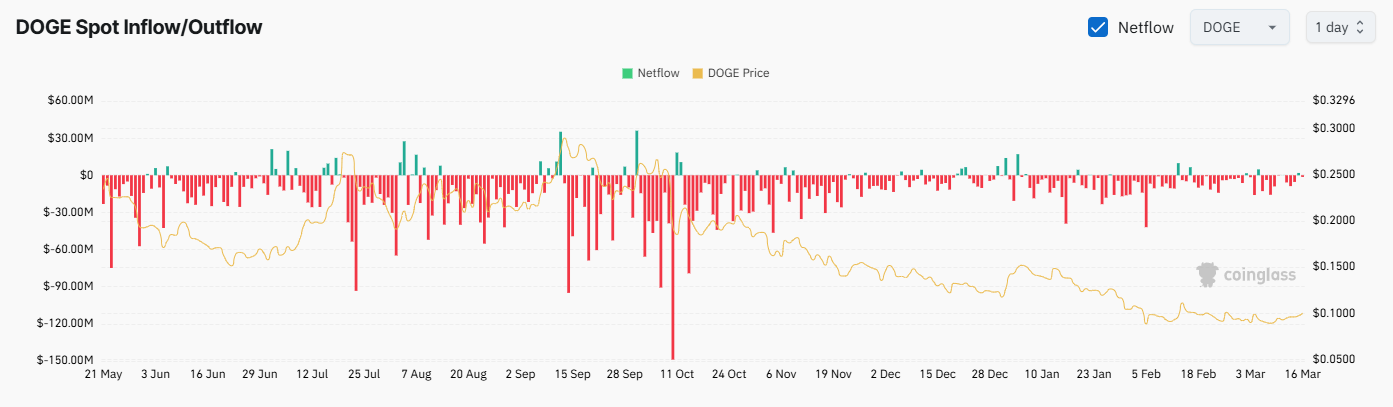

DOGE might explode to $0.50 if it breaks above a certain level, one analyst claimed.

The biggest meme coin has caught the recent green wave sweeping through the cryptocurrency market, with its price rising to a 10-day high.

Whales are waking up, too, hinting that the real rally might only be starting.

Further Gains Ahead?

The cryptocurrency sector, especially the meme coin niche, has registered a substantial uptick over the past 24 hours. The undisturbed leader, Dogecoin (DOGE), soared by 6% daily, while its market capitalization once again surpassed $15 billion.

Given the whales’ recent accumulation, the OG meme coin could be poised for an additional increase. The renowned analyst Ali Martinez revealed that this cohort of investors has acquired 470 million DOGE in the past 72 hours. The stash is worth roughly $47 million (calculated at current rates).

Following the latest buying spree, the whales boosted their total possessions to almost 36 billion coins, representing 23.5% of Dogecoin’s circulating supply.

Such accumulation is typically considered bullish for the price as it reduces the amount of tokens available on the open market and signals growing confidence among major holders. Whales are known as experienced investors who rarely jump on the bandwagon without proper knowledge or research, leaving unanswered questions about whether they know something we don’t. In the aftermath, smaller players might be encouraged to join the ecosystem as well, thereby injecting fresh capital.

Some industry participants support the bullish outlook. X user Trader Tardigrade claimed that DOGE “is breaking out” from a certain setup that has historically preceded “a massive pump.” For their part, CoinQTS described $0.125 as a “key level to watch,” predicting a rally to as high as $0.50 should the price break above $0.13.

You may also like:

The recent DOGE exchange netflow may also sit well with bulls. Data show that outflows have consistently outweighed inflows over the past weeks, indicating that investors have shifted from centralized platforms to self-custody methods, thereby reducing immediate selling pressure.

On the contrary, Dogecoin’s Relative Strength Index (RSI) should serve as a warning that a short-term correction may also be on the horizon. The technical analysis tool measures the speed and magnitude of price changes to assess potential reversal points. It runs from 0 to 100, with ratios above 70 considered bearish territory, while anything below 30 is considered a buying opportunity. Currently, the RSI stands at around 76.

The Potential Elon Musk Effect

It is no secret that the world’s wealthiest person is keen on Dogecoin and has, over the years, endorsed it publicly, which has led to substantial price gains. Not long ago, Musk confirmed that X Money, the platform’s upcoming payments feature, will go live next month. It is expected to allow users to send and receive funds directly through X, with a strong emphasis on integrating digital assets into the effort.

X user Fuel wondered what would happen if Musk made DOGE the default currency for the new feature, suggesting such a move could push the price to $0.50 or even $1.

Many commentators on the post believe that Dogecoin will not play such a central role in X Money, with some describing the token as a “joke just like all meme coins.”

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

France stocks higher at close of trade; CAC 40 up 0.31%

SEC drops lawsuit against BitClout founder Nader Al-Naji over DeSo crypto project

Virgin River’s Ben Hollingsworth Recalls Nina Dobrev Rumors

-

Tech5 days ago

Tech5 days agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

Crypto World3 days ago

HYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Business6 days ago

Business6 days agoExxonMobil seeks to move corporate registration from New Jersey to Texas

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Addict Lip Glow

-

Tech6 days ago

Tech6 days agoChatGPT will now generate interactive visuals to help you with math and science concepts

-

Sports2 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

NewsBeat5 days ago

NewsBeat5 days agoResidents reaction as Shildon murder probe enters second day

-

NewsBeat7 days ago

NewsBeat7 days agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Business5 days ago

Business5 days agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

Business22 hours ago

Business22 hours agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Business2 days ago

Business2 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World2 days ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

NewsBeat5 days ago

NewsBeat5 days agoI Entered The Manosphere. Nothing Could Prepare Me For What I Found.

-

Business7 days ago

Business7 days agoSearch Enters 39th Day with FBI Tip Line Developments and No Major Breakthroughs

-

Business2 days ago

Business2 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Business6 hours ago

Business6 hours agoAustralian shares drop as Iran war enters third week

-

Crypto World6 days ago

Crypto World6 days agoWill Chainlink price reclaim $10 amid volatility squeeze?

-

Sports5 days ago

Sports5 days agoPWHL, Senators discussing plan to keep Charge in Ottawa

-

Crypto World7 hours ago

Crypto World7 hours agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Sports3 days ago

Sports3 days agoCollege Basketball Best Bets: Conference Tournament Semifinal Picks

You must be logged in to post a comment Login