Crypto World

Wall Street heavyweight Cantor among investment banks pitching crypto trading firm FalconX for its potential IPO

Wall Street financial services firm Cantor is among investment banks that are pitching cryptocurrency trading platform FalconX for its potential IPO, according to two people with knowledge of the matter.

The company has held preliminary talks with possible advisors, but FalconX has not yet formally appointed bankers for its initial public offering, the people said, who spoke on condition of anonymity as the matter is private.

FalconX declined to comment. Cantor did not respond to a request for comment by publication time.

Investment banks often pitch companies for an IPO by presenting themselves as the best partner to take the business public, combining valuation analysis, market timing advice, and distribution strength.

The goal is to win the mandate by convincing the company that they can maximize valuation, ensure a smooth listing process, and generate strong aftermarket performance. While some firms might lead the IPO process, most deals are done through a syndicate of multiple banks.

Last year, Decrypt reported in June that FalconX had held informal talks with bankers and consultants about going public. Later in the year, the company’s CEO, Raghu Yarlagadda, told the Wall Street Journal that the firm was considering an IPO.

However, the crypto market has been under pressure since then, with the bitcoin price falling from an all-time high of $126,000 in October to near $70,000. Recently, CoinDesk reported that crypto exchange Kraken has put its IPO plans on hold after confidentially filing with the SEC in November, with sources saying the process will likely restart once the environment improves. To date, digital asset custodian BitGo (BTGO) is the only crypto native firm to list this year. The shares have fallen around 40% since their IPO.

Despite this tough market backdrop, crypto firms such as FalconX and Copper are continuing talks about potential public listings. Last year, several crypto exchanges, including CoinDesk parent Bullish (BLSH) and Gemini (GEMI), went public, and industry observers say that in 2026, financial infrastructure firms could be next in line for IPOs.

Cantor connection

Cantor and FalconX already have an existing relationship centered on institutional crypto lending, with the investment bank providing one of the first major credit facilities to the crypto prime broker.

In 2025, Cantor launched a $2 billion bitcoin-backed financing program and extended an initial credit line of over $100 million to FalconX, allowing it to borrow against bitcoin collateral and access liquidity without selling assets. The deal is part of a broader partnership aimed at building institutional-grade credit infrastructure in digital assets, reflecting growing convergence between traditional finance and crypto markets.

If Cantor wins the IPO mandate, it would likely be due to the existing relationship with the trading firm.

FalconX is a U.S.-based cryptocurrency trading and brokerage firm that primarily serves large institutional clients, including hedge funds, asset managers, and market makers.

Founded in 2018, the company operates as a digital asset prime broker, offering services including trade execution, liquidity access, credit and clearing. The company raised $150 million in a Series D financing round in June 2022, valuing the platform at $8 billion.

While no formal announcement has been made, FalconX has been scaling up ahead of a potential listing and has pursued an aggressive acquisition strategy over the past year as it builds out a full-service institutional crypto platform.

In 2025, the firm acquired derivatives specialist Arbelos Markets and took a majority stake in Monarq Asset Management, before striking a deal for crypto exchange-traded product (ETP) issuer 21Shares, its third major transaction of the year. Together, the deals expand FalconX’s reach across trading, derivatives, and asset management, reflecting a broader push to consolidate infrastructure and offer more regulated, institutional-grade investment products.

Cantor has steadily expanded its footprint in digital assets, positioning itself as one of the more active traditional finance firms in crypto markets. The Wall Street firm manages Tether’s U.S. Treasury reserves and has backed several crypto ventures, while publicly signaling support for blockchain infrastructure and trading businesses.

Its growing involvement reflects a broader push to bridge institutional capital with the digital asset ecosystem, particularly as more crypto companies explore public listings.

Cantor is a global financial services firm headquartered in New York. Founded in 1945, it’s best known as a major player in fixed-income trading, particularly U.S. Treasuries, as well as investment banking, brokerage, and asset management.

Regulators are signaling a shift in digital-asset oversight as the SEC outlines an interpretive framework for applying securities laws to crypto. SEC Chair Paul Atkins, in prepared remarks at the Practising Law Institute, said the agency intends to move away from a broad enforcement-first stance toward a more principled, interpretive approach. The remarks follow the agency’s interpretive notice on crypto regulation and a memorandum of understanding with the CFTC signed last week.

“While the interpretation provides long-needed clarity, I should like to assure this audience that it amounts to a beginning, not an end,” Atkins told attendees, underscoring the framework is intended to evolve alongside market developments.

The interpretive notice, released earlier in the week, frames how federal securities laws may apply to crypto assets. It suggests that most cryptocurrencies are unlikely to be securities under federal law, with a narrow exception: traditional securities that are tokenized. Atkins later clarified that digital commodities, digital tools, digital collectibles including non-fungible tokens (NFTs), and stablecoins are typically not within the SEC’s purview.

Key takeaways

- The SEC signals a shift from enforcement-by-press release toward a interpretive, rules-based approach to crypto regulation after a new interpretive notice and a memorandum with the CFTC.

- Under the framework, most crypto assets are unlikely securities; only tokenized traditional securities would fall under federal securities laws.

- Assets like digital commodities, digital tools, NFTs, and stablecoins are generally not considered securities by the agency’s current interpretation.

- Regulatory progress intersects with Congress and the White House, as lawmakers push a market-structure bill (the CLARITY Act) and seek consensus on stablecoin regulation and crypto-asset provisions.

- Watch for how the evolving framework interacts with legislative efforts, potential CFTC authority expansion, and ongoing industry pilots and experiments.

Regulatory posture shifts amid a mixed legislative backdrop

The SEC’s interpretive stance arrives as part of a broader recalibration of how crypto regulation will be enforced and applied. The agency had long faced criticism for a perceived “enforcement-by-crisis” approach, especially for startups and projects navigating an evolving market. By contrast, the latest framework emphasizes clarity and consistency, aiming to reduce guesswork for issuers, exchanges, and investors while preserving robust investor protections.

The interpretive notice explicitly clarifies that, for many digital assets, existing securities laws may not apply in the same way as for traditional stocks or bonds. The acknowledgment that most crypto assets are not securities could lower some regulatory friction for many projects—though it also places a clear boundary around assets that would still be subject to securities regulation.

Atkins connected the interpretation to ongoing SEC coordination with the CFTC, noting the memorandum signed last week. The agreement signals an intent to harmonize approaches where possible, a relevant development given the overlapping jurisdictions in crypto markets, market infrastructure, and derivatives. The result could be a more predictable regulatory environment for token issuers and market participants, even as questions about enforcement and future rulemaking linger.

Contextual backdrop: market structure, stablecoins, and the legislative path

Beyond the SEC’s interpretive framework, lawmakers are actively shaping the arc of crypto regulation through legislation and hearings. A market-structure bill, known in industry circles as the CLARITY Act, advanced in the House in mid-2025 but has faced a slower path in the Senate. As of the latest briefing, it had not yet been scheduled for a markup in the Senate Banking Committee, leaving a critical regulatory hinge unresolved.

In parallel, the White House has engaged with lawmakers behind closed doors to advance the same package. A spokesperson for Wyoming Senator Cynthia Lummis confirmed that Republican senators met with White House crypto adviser Patrick Witt to discuss advancing the market-structure bill. Lummis’ team described the session as very productive and positive, with negotiators “99% of the way there on stablecoin yield” and ongoing, productive talks on the digital-asset provisions of the bill.

Stablecoins remain a focal point of regulatory and policy debate, particularly around yield, banking implications, and consumer protections. The sense among some policymakers is that achieving a workable framework for stablecoin issuance and redemption is a prerequisite for broader bipartisan consensus on crypto regulation.

The regulatory dialogue is further colored by ongoing market experiments and pilot programs. For example, the market has seen pilots exploring tokenized trading and other asset-ization concepts under the watchful eye of multiple agencies. While these pilots illustrate a regulatory appetite for innovation, they also underscore that practical, real-world testing will continue to inform how rules evolve in practice.

As the SEC’s interpretive framework takes root, traders, issuers, and developers should prepare for a regulatory environment that favors clarity and predictability but remains nuanced. The boundary between what constitutes a security in crypto, and what does not, will likely continue to shift as new asset classes and products emerge. The interplay between the SEC, the CFTC, and Congress will shape the pace and direction of this evolution in the months ahead.

Readers should watch for updates on the CLARITY Act’s progression in the Senate, any further formal guidance from the SEC, and on-the-ground outcomes from ongoing tokenization trials and stablecoin regulatory debates. The convergence of executive and legislative activity suggests that substantial clarity—across asset classes and market infrastructure—may still be months away, even as the groundwork for a more predictable regulatory framework takes shape.

Kentucky House Bill 380, a state-level crypto regulatory bill, includes provisions that would force crypto hardware wallet manufacturers to build a “backdoor” into devices, Bitcoin (BTC) advocacy organization Bitcoin Policy Institute (BPI) has warned.

The provisions require crypto hardware wallet manufacturers to provide recovery options for users’ seed phrases, and were added to the bill in a “last-minute” floor amendment, BPI said. The amended Section 33 of the bill reads:

“A hardware wallet provider shall provide a mechanism for, and assist any person who owns a hardware wallet that was provided by the provider with, resetting any password, PIN, seed phrase, or other similar information that is necessary to access the contents of the hardware wallet.”

The sponsors of the legislation are state Representatives Aaron Thompson and Tom Smith.

The bill also proposes identity verification checks for users requesting a password, seed phrase, or PIN reset from a hardware wallet manufacturer.

“The mandate is technologically impossible for non-custodial wallets. Hardware wallets are specifically designed so that no one, including the manufacturer, can access or recover a user’s seed phrase,” BPI said in response.

The provisions threaten the self-custody of private keys, which is a foundational feature of cryptocurrencies, according to BPI, which added that requirements like this push users toward centralized custodians that are susceptible to hacks and business failures.

Related: BPI targets August for BTC tax relief, but warns time is running out

SEC officials defend the right to self-custody

US Securities and Exchange Commission (SEC) Chair Paul Atkins said he is “in favor” of market participants having self-custody options, especially in cases where intermediaries would impose a financial or operational burden on the user.

In November 2025, Hester Peirce, an SEC commissioner and head of the regulator’s Crypto Task Force, reaffirmed the right to self-custody and financial privacy, saying that both were foundational to freedom.

Peirce asked the hosts of the Rollup podcast in November 2025: “Why should I have to be forced to go through someone else to hold my assets?

“It baffles me that in this country, which is so premised on freedom, that would even be an issue — of course, people can hold their own assets,” she said.

Magazine: Bitcoin’s long-term security budget problem: Impending crisis or FUD?

Crypto World

Binance New Listing Announcement Talk Heats Up as Pepeto Presale Accelerates and the Window Before Listing Gets Smaller Every Day

The stablecoin standoff in the Senate could break this week. Tim Scott, chair of the Banking Committee, said he expects the first compromise proposal on yield provisions before Friday. When that framework passes, every audited presale with working products enters a different pricing environment overnight.

The binance new listing announcement debate is picking up across every trading community, but the biggest opportunity right now is not the debate itself. It is the presale that already crossed $8 million during extreme fear and has a confirmed Binance listing approaching while most traders are still afraid to move.

Tim Scott told a DC crypto lobby event on March 18 that a breakthrough on the stalled market structure bill is within reach according to CoinDesk.

The FOMC held rates steady at 3.50% to 3.75% on March 19 and BTC slid from $76,000 to $69,000 on the decision according to CoinGecko. Binance new listing announcement speculation picked up as traders shifted focus toward audited presales with live products, expecting the regulatory clarity to reprice them first.

Binance New Listing Announcement Candidates and the Presale That Already Has the Products, the Audit, and the Capital

Pepeto Is Leading the Binance New Listing Announcement Conversation Because the Exchange Tools Are Live and the Capital Proves the Conviction

Capital is flowing again. Pepeto keeps pulling investment ahead of its Binance listing, and the wallets entering during a correction are not speculators chasing hype. The presale crossed $8 million at $0.000000186, and the three exchange tools are already live and verified before a single token trades publicly.

PepetoSwap stops your capital from bleeding through the fees that every other exchange takes on each position, so what you put in is exactly what works for you. The risk scorer reads every contract for hidden traps and flags the dangerous ones before your wallet ever signs anything, which means you stop losing money to scams that a quick scan would have caught.

Holders already inside are earning 196% APY compounding daily while they wait for the event that changes everything. All of that makes Pepeto the kind of entry that a binance new listing announcement rewards the hardest, because the products are built, the audit is done, and the community already committed real capital during fear.

The original Pepe coin reached $11 billion on 420 trillion tokens with nothing behind it. The person who created that project is now building Pepeto with three working tools and the same supply. Matching even a small part of that run from $0.000000186 is the kind of math that makes this correction feel like a gift. A former Binance expert on the dev team built the exchange from the ground up, and SolidProof cleared every contract before public capital entered.

The whales who loaded during fear at the same entry as retail understand what the listing does to this price, and once trading begins, every position bought today becomes the story the market tells for the rest of the cycle.

Solana Holds at $87 but the Recovery Math From $294 Takes Years Not Days

SOL trades at $87, down 69% from its $294.85 ATH according to CoinMarketCap. Spot Solana ETFs crossed $1 billion in assets. CoinCodex targets $137 by year end, roughly 52% from here.

Solid for a patient hold. But even tripling puts SOL at $270, still short of its own peak, and nowhere near the distance between a presale at $0.000000186 and a Binance listing.

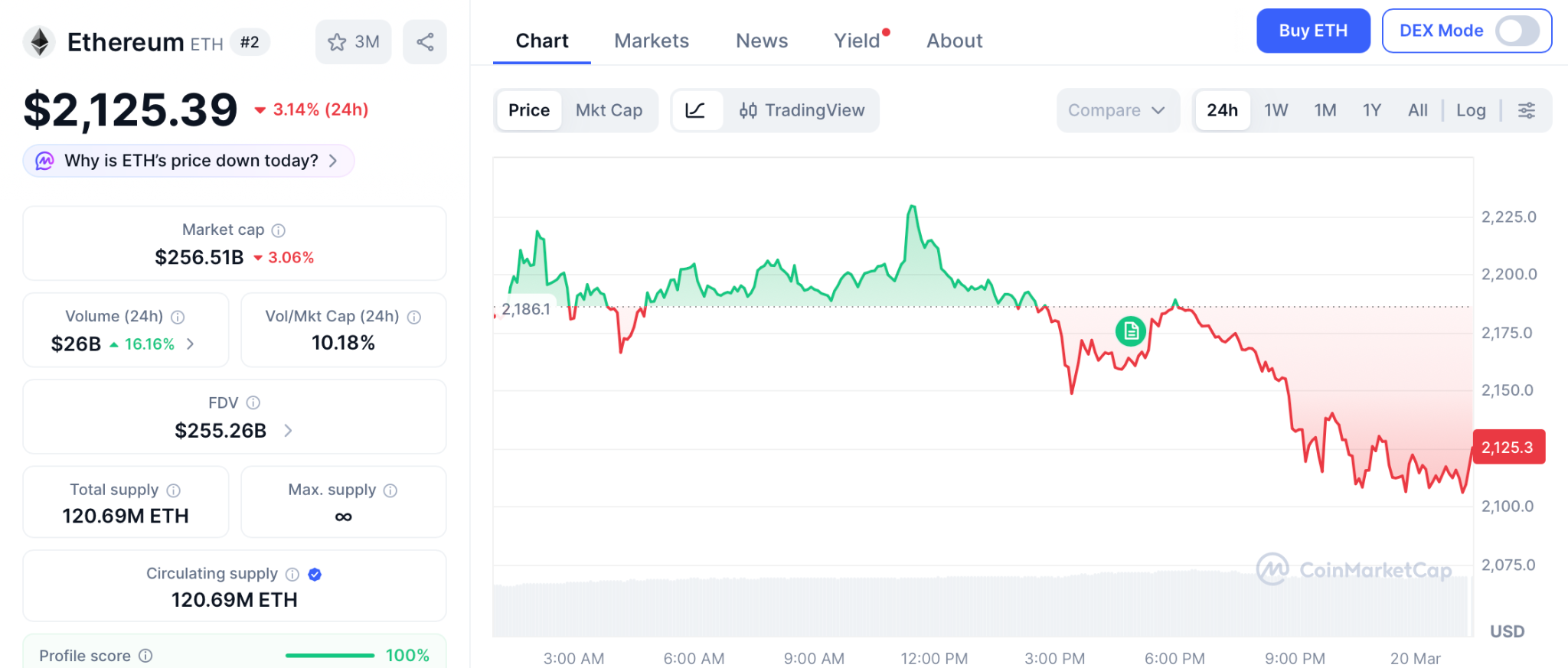

Ethereum Sits Below $2,200 and the DeFi Foundation Delivers Foundation Returns

ETH trades near $2,125, roughly 55% below its $4,878 ATH according to CoinMarketCap. Over $50 billion in DeFi TVL keeps Ethereum as the default smart contract chain.

Analysts target $3,000 to $4,000 for 2026. A move from $2,200 to $4,000 is less than 2x, and that kind of gain takes quarters to deliver what a presale to listing event delivers in a single candle.

The Binance New Listing Announcement Debate Keeps Growing but the Entry at $0.000000186 Will Not Wait for the Market to Feel Ready

The market structure bill is moving toward a vote and fresh capital is about to flood into crypto. The correction feels heavy and the fear is real. But that is exactly why the biggest entry is sitting in front of you right now. Every cycle ended the same way: the wallets that moved during fear built the wealth, and the ones who waited bought at prices set by the people who acted first.

The person who created the original Pepe coin is building an exchange at $0.000000186 with a clean audit and a Binance listing approaching. The Pepeto official website is where the wallets that refuse to carry regret into the next year are committing capital right now, and the correction will not keep this entry open forever.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What does the latest binance new listing announcement speculation mean for presale investors?

The market structure bill is moving and regulatory clarity reprices audited presales first. Pepeto at $0.000000186 with three live tools and a Binance listing is positioned for exactly that moment.

Why is Pepeto part of the binance new listing announcement conversation?

Pepeto crossed $8 million, passed a SolidProof audit, and has a confirmed Binance listing approaching. The exchange products are live before trading begins.

Is Pepeto a good investment before the Binance listing?

More than $8 million entered during extreme fear with 196% staking live. Visit the Pepeto official website before the listing closes the presale window.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

The SEC just handed tokenized stocks their biggest legitimacy moment ever, and it happened inside the world’s second-largest stock exchange.

Nasdaq’s SEC-approved pilot allows eligible participants to trade tokenized Russell 1000 stocks and major index ETFs on the same order book at the same price, with the same rights as traditional shares.

But tokenized stocks are still stocks: they simply can’t offer more than 10–15% returns. The crypto market is different because you can find early-stage projects like DeepSnitch AI and invest in them before the broader market notices they exist.

The SEC’s tokenized stock approval confirms that institutional capital is moving on-chain at scale, and when that happens, DeepSnitch AI will be at the forefront with its live AI tools. This is why many believe we should expect a DSNT Binance new listing announcement soon.

SEC approves Nasdaq’s tokenized stock trading pilot

The SEC has approved Nasdaq’s proposal to run a tokenized stock trading pilot, allowing eligible participants to trade tokenized versions of Russell 1000 stocks and major index ETFs.

The regulatory approval is the breakthrough that the tokenized equities sector has been waiting for. Until now, tokenized stock products have operated largely outside US markets, and this pilot puts tokenization directly inside the world’s second-largest stock exchange.

The approval dramatically accelerates tokenization’s legitimacy and adoption timeline. Combined with NYSE’s OKX partnership and DTCC’s Canton Network integration, the US financial infrastructure is now actively building blockchain-based settlement rails.

The tokenized equities market, currently at $1 billion on-chain, now has a regulated, exchange-backed pathway to scale orders of magnitude larger.

Top 3 Binance new listing announcements

DeepSnitch AI

The SEC just approved tokenized Russell 1000 stocks for on-chain trading. That’s a product designed for institutional allocators who want equity exposure without leaving the blockchain, and it will generate moderate annual returns. DeepSnitch AI was built for the traders who came to crypto looking for something very different from that.

In crypto, hesitation costs money. Markets rally and reverse in minutes, and if you’re reacting instead of anticipating, the move is gone by the time you see it. As Nasdaq’s tokenized stocks bring traditional finance participants on-chain, they will eventually start looking for the real asymmetric returns.

DeepSnitch AI is the intelligence platform that bridges that discovery: scanning whale movements, auditing contracts, decoding sentiment shifts, and surfacing opportunities before they reach mainstream attention. That’s the gap the SEC’s approval makes more valuable, not less: more participants, more capital, more noise, and more need for a tool that cuts through all of it.

Now in Stage 7 at $0.04487, with 200% gained from the original entry price and over $2.20 million raised, the Binance new listing announcement conversation looks like the natural next step for a project that already meets the criteria. Binance lists products with real utility and proven user demand. DSNT has both.

The presale closes March 31st. After that, a 7-day claim frame opens for tokens and bonuses, then Uniswap goes live. The tier-1 CEX listings follow from there, and none of those buyers get into DeepSnitch AI at $0.04487.

Fabric Protocol

Fabric Protocol builds financial infrastructure for autonomous robots: on-chain identities, wallets, and independent transaction settlement. The gap is real and largely ignored: today’s robots can’t open bank accounts or own assets.

The token model holds up. ROBO powers every network interaction, while demand ties directly to usage. The veROBO governance mechanism and 12-month cliff with multi-year vesting signal long-term alignment, not short-term extraction.

The development sequencing is pragmatic. Base first for rapid prototyping, purpose-built Layer 1 later for machine-native high-frequency operations.

Katana

Katana combines concentrated liquidity pools, auto-compounding yield optimization, ZK-privacy infrastructure, and a purpose-built Layer 2 on Polygon’s AggLayer into one integrated DeFi ecosystem. The bet is that the integration itself becomes the differentiator in a market where single-feature competition no longer wins.

The concentrated liquidity pools claim up to 4000x greater capital efficiency than traditional AMMs. Cross-protocol yield optimization automatically shifts capital to the highest-performing opportunities. Both target the manual complexity, keeping institutional capital off DeFi entirely.

The institutional angle sharpens the strategy. ZK-privacy tools, enterprise API integrations, and customisable regulatory reporting remove the infrastructure barriers that blocked traditional finance from engaging, not a lack of interest.

The bottom line

The SEC just blessed tokenized stocks, while DeepSnitch AI has launched the AI-native crypto intelligence: first, live, and ahead of the crowd.

Think Bloomberg Terminal crossed with ChatGPT, purpose-built for the only market that never sleeps.

That’s why $2.20M landed in the presale before a single exchange listing and why the Binance new listing announcement conversation is already happening. March 31st is the hard stop.

Visit the official website for more information, and join X and Telegram for community updates.

FAQs

What are the most anticipated upcoming Binance listings as tokenized stocks gain SEC approval?

Among upcoming Binance listings, DeepSnitch AI generates the strongest anticipation: a confirmed Uniswap debut on March 31st, a working AI platform with $2.20M raised, and a track record that meets Binance’s criteria for real utility and user traction.

What does the latest Binance listing news reveal about which projects qualify for tier-1 exchange exposure?

The latest Binance new listing announcement news consistently favors projects with live products and proven user demand. DeepSnitch AI checks both boxes.

How does DeepSnitch AI position itself for upcoming Binance listings compared to Fabric Protocol and Katana?

DeepSnitch AI was better positioned for upcoming Binance listings than Fabric Protocol or Katana. Both are still building toward product-market fit, while DSNT already delivers live intelligence tools and a confirmed March 31st Uniswap launch as its starting point.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

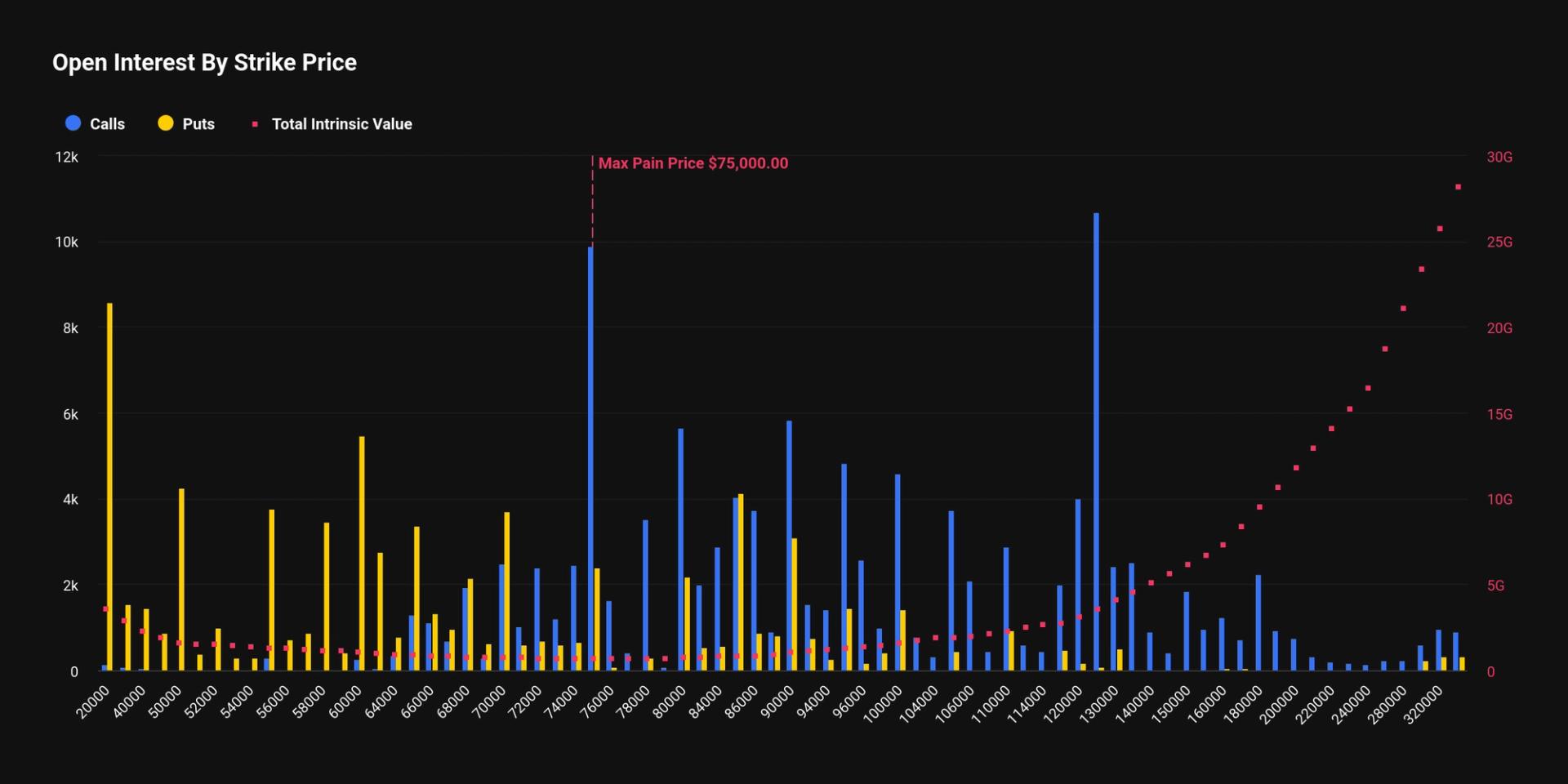

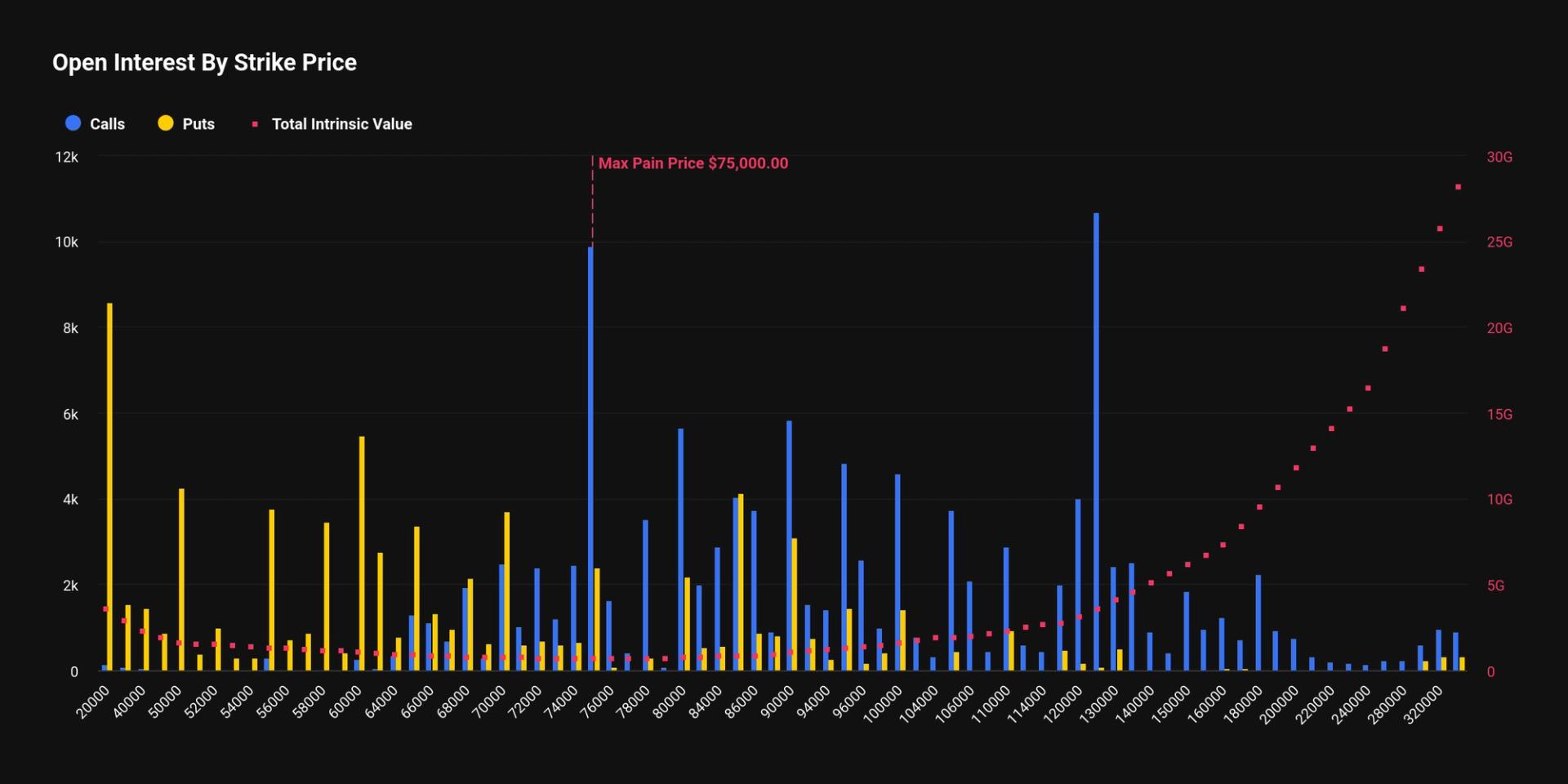

Nearly $600 million worth of $20,000 bitcoin put options has emerged as the third most popular strike ahead of Deribit’s quarterly expiry, showing how traders are positioning for extreme downside scenarios due to the Middle East conflict.

A put option gives the holder the right, but not the obligation, to sell bitcoin at a predetermined price. With bitcoin trading below $70,000, the $20,000 strike is considered deep out of the money, meaning it would only gain value in the event of a sharp market collapse, or a 70% drawdown from current prices.

Roughly $596 million in notional value, the total dollar value of underlying contracts, is concentrated at the $20,000 strike, making it one of the three most dominant positions. The others sit at $75,000, with $687 million, and $125,000, with $740 million, highlighting a wide spread of expectations across both downside and upside scenarios.

Looking at it from face value, large positioning in a $20,000 put option could suggest fears of a meltdown. However, the structure of the market is more nuanced.

Much of this activity is likely driven by traders selling these far out of the money puts to collect premium, reflecting the low probability of bitcoin falling to $20,000 rather than a direct hedge against a crash. In other words, it is often a strategy tied to income generation or volatility positioning, rather than outright bearish conviction.

The total notional value of bitcoin options expiring on Deribit is $13.5 billion. While, even though the market is in extreme fear, the options market still leans slightly bullish, with a put call ratio of 0.63, indicating more call options than puts, typically used to express bullish views. Total open interest stands at 195,719 BTC, with 120,236 BTC in calls and 75,482 BTC in puts.

Meanwhile, the max pain level, the price at which the largest number of options expire worthless, is $75,000, which could potentially act as a magnet into expiry. As options market makers often hedge around this level, pulling price toward where the greatest number of contracts expire worthless.

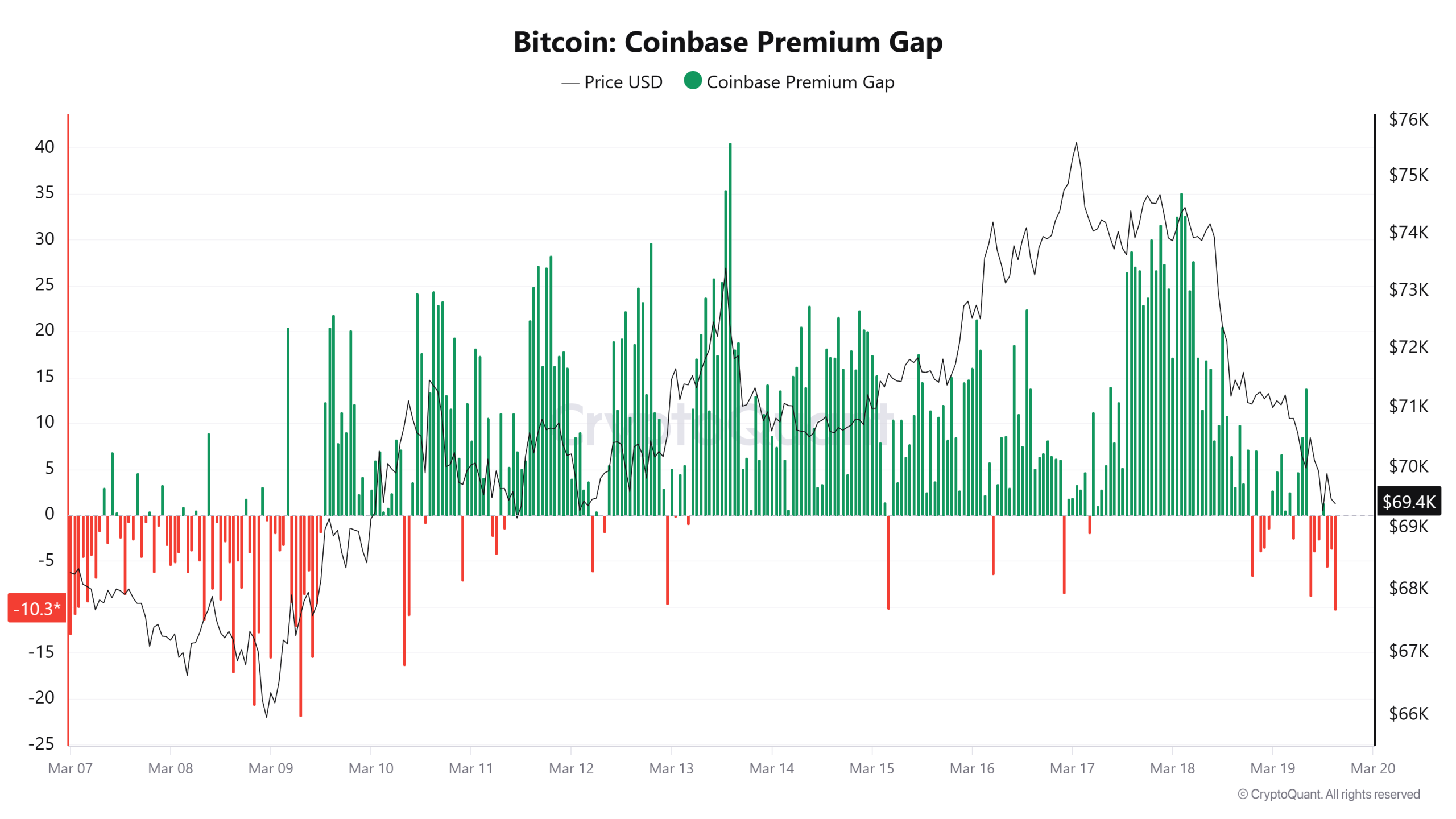

Bitcoin (BTC) dropped below $69,000 on Thursday, pulling the price back into its six-week range just days after tapping range highs above $76,000.

The pullback coincides with an increase in selling from Bitcoin futures markets and stalling demand from US-based investors, but the chance for a rebound rally remains. A recurring chart setup indicates that BTC can return to its bullish pathway if the necessary conditions are met.

Bitcoin futures set the trend as spot demand fades

The latest pullback aligns with a visible shift in derivatives’ dominance over spot activity. The Coinbase premium gap turned negative after a period of steady demand, pointing to weak follow-through from US-based investors.

Meanwhile, crypto analyst IT Tech noted a clear imbalance between the spot and perpetual futures. The cumulative volume delta (CVD), which tracks the net buying versus selling across markets, fell by $40.64 million for the spot CVD, while the perpetual CVD dropped by $506.75 million, highlighting stronger selling pressure from leveraged traders.

However, the funding rates have flipped positive to 0.05%, meaning long positions are now paying shorts, indicating a long bias across the derivatives markets.

The order book data shows bid-side support holding near the $70,000 region, with both spot and perpetual markets leaning toward buyers.

Related: OP_NET launches Bitcoin DeFi push without bridges or wrapped BTC

Fractal setup mirrors early-March bounce

On the lower timeframes, Bitcoin is forming a similar fractal setup to the March 6 through March 8 correction when the price declined and swept internal liquidity levels before reversing higher on the charts.

The current move follows the same sequence, with successive lower lows developing into a potential exhaustion phase for the price.

In the prior breakout, the reversal aligned with a bullish divergence on the relative strength index (RSI) indicator, where RSI held equal lows as the price printed a lower low. The pattern signaled a fading momentum from sellers. A comparable divergence is now developing, reinforcing the bullish fractal structure.

The liquidation data also supports this setup. Significant long-side liquidations have been observed on both occasions, reducing the open interest and flushing out overleveraged positions.

A swift reclaim of $70,000 aligns with the previous fractal recovery path, opening a move toward $76,000. The $72,000 level acts as the key pivot, where a reclaim may trigger a short squeeze if short positions get trapped.

However, the setup remains time-sensitive. A breakdown below $68,300 shifts focus toward the $65,000 and $62,000 levels, where higher time frame liquidity sits for BTC.

Trading Stables founder Ryan Scott flagged $73,000 as a key base level, noting that failure to stabilize above this level signals a weak buyer response, raising the chance for a drop to range lows near $62,000.

Related: Bitcoin prediction markets see 70% chance BTC price crashes to $55K in 2026

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

Crypto World

Trillions in options set to expire Friday as quadruple witching tests crypto resilience

On Friday, global markets will face a trillions-of-dollars quarterly derivatives event known as quadruple witching.

The event occurs on the third Friday of March, June, September, and December, when four major types of derivatives expire simultaneously. These include stock index futures, stock index options, single-stock options, and single-stock futures.

Because traders must close, roll or settle these positions simultaneously, trading activity often surges, and price swings can intensify in the traditional markets.

Exact figures for the March 2026 expiry have not yet been published, though recent events illustrate the scale. In March 2025, roughly $4.7 trillion worth of equity and index derivatives expired during the quarterly event. According to TradeStation, that session saw the highest S&P 500 trading volume of the entire year, while other witching days also recorded above-average activity.

Large expiries like this often force institutions to rebalance portfolios, unwind hedges and adjust risk exposure within a short window. Much of the activity tends to concentrate in the final hour of trading, when liquidity spikes and volatility can increase rapidly.

This quarter’s expiration arrives during an already volatile trading environment. Conflict in the Middle East recently pushed oil prices to $120 per barrel, while gold slipped below $4,600 and bitcoin fell below $69,000. Meanwhile, the VIX volatility index jumped above 35 last week, the highest level in a year, signalling heightened stress in financial markets.

Although quadruple witching originates in traditional finance, it can spill into crypto markets. Bitcoin increasingly trades alongside broader risk assets, meaning sharp moves in equities often ripple into digital markets.

Cole Kennelly, CEO of Volmex Finance, said tomorrow’s event could drive volatility in crypto markets, noting that “quadruple witching could trigger a spike in cross-asset volatility as large derivatives positions expire. This may already be showing up in crypto, with the Bitcoin Volmex Implied Volatility (BVIV) Index trending higher into the event.”

How did bitcoin perform on quadruple witching days in 2025

On March 21, bitcoin was slightly down on the day, but the more significant move came later, with prices bottoming a few weeks afterward around $76,000 following the market reaction to President Trump’s “Liberation Day” tariffs.

On June 20, bitcoin declined 1.5% and continued drifting lower, reaching a local bottom near $98,000 just two days later. On September 19, Bitcoin fell over 1% on the day, but the real move unfolded in the following week, with a sharp drop from $177,000 to $108,000. Then, on December 19, bitcoin finished roughly 3% higher at around $85,000, though it remained in a broader drawdown from the October highs.

While price action on the day itself tends to be relatively muted, a consistent pattern of weakness emerges in the days to weeks that follow.

Even if the quad-witching doesn’t add to bitcoin’s volatility on Friday, crypto traders have another event, specifically for digital assets, to keep in mind.

Crypto derivatives face their own major quarterly expiry the week after, on March 27, with $13.5 billion set to expire on Deribit, where positioning points to elevated demand for volatility strategies rather than strong directional bets.

Exchange giant Coinbase’s (COIN) asset management arm is bringing its bitcoin yield fund onchain, creating a tokenized share class of the fund with $3.5 trillion fund administrator Apex Group.

The Coinbase Bitcoin Yield Fund, managed by Coinbase Asset Management (CBAM), will be available to investors on the Base network, Coinbase’s blockchain built on Ethereum. Apex remains the transfer agent, keeping records aligned with the fund’s net asset value.

The launch comes as global asset managers are looking at tokenization as the next frontier in how capital markets evolve, making bonds, equites and funds tradable on blockchain rails. Firms including BlackRock (BLK), Fidelity and Franklin Templeton have introduced tokenized funds in recent years, aiming to speed up settlement times, cut costs and open new distribution channels.

Brett Tejpaul, head of Coinbase Institutional, said the company’s asset management business already has a lot of institutional capital allocated, with many investors holding core positions in bitcoin and ether.

“Incrementally, we’re getting new capital coming to the space that wants the ability to get compounded returns, so their bet isn’t just on the appreciation of bitcoin, but while they’re waiting for it to rise in price, they’re earning yield along the way,” he told CoinDesk.

“The bitcoin yield fund allows them to do that by virtue of doing things like selling call options or participating in lending arrangements.”

Tokenized assets are potentially a multiple-trillion-dollar market, with estimates ranging from McKinsey’s projection of $2 trillion by 2030 to BCG and Ripple’s $18.9 trillion target by 2033.

Apex, a significant player in the fund service business supporting $3.5 trillion in assets, is increasingly leaning into tokenization as well. It acquired Tokeny last year, a specialist that facilitated the tokenization of over $32 billion in assets. Apex also said it plans to tokenize $100 billion in funds using the T-REX Ledger by June 2027 to manage ownership and compliance across multiple blockchains.

In the case of the Coinbase Bitcoin Yield Fund, the tokenized share class uses the ERC-3643 token standard, which encodes investor checks directly into the token. Only approved investors can hold or transfer the asset, with identity tied to each wallet through a dedicated onboarding process.

The setup replaces manual compliance checks with automated rules. If a wallet is not cleared, the transaction fails. That could reduce friction in how institutional investors access and move fund positions.

The fund is available to non-U.S. investors, but CBAM said it plans to create a tokenized share class of the fund’s U.S.-version as well.

Prediction market provider Kalshi may be hit with a temporary restraining order from the state of Nevada after a federal appeals court declined to block such a motion on Thursday.

The Nevada Gaming Control Board sent Kalshi a cease-and-desist order in March 2025, ordering it to stop offering sports-related prediction market contracts. However, Kalshi said a later temporary restraining order application by Nevada “sought to prohibit Kalshi from offering all its event contracts.” Kalshi tried to move the case to federal court, but the case was set to go back to a state court if the appeals court did not grant it an administrative stay.

On Thursday, a Ninth Circuit Court of Appeals panel denied Kalshi’s motion for an administrative stay in a federal case, clearing the way for the case to get thrown back to a state court.

In its appeal filed on March 13, Kalshi warned that it “faces imminent harm” if the appeals court did not grant its motion, as “the state court proceedings would undermine Kalshi’s appellate rights in this appeal” and a related action.

The platform said that it might find itself litigating the same issue — namely, the question of whether state regulators in Nevada have any jurisdiction — in four different venues, including a Nevada state court, Nevada federal court and two different appeals court cases.

“Allowing that to happen would create an untenable risk of subjecting Kalshi to conflicting federal and state court decisions,” the filing said. “For example, the state court could enter judgment against Kalshi, finding that the CEA does not preempt state gambling laws, while this Court in Assad [another case] arrives at exactly the opposite conclusion.”

Dan Wallach, a gaming lawyer, said in a post on X that a temporary restraining order would push Kalshi out of Nevada entirely for at least two weeks, pending a hearing on a preliminary injunction.

The temporary restraining order could come in the next day or so, he said.

Kalshi and other prediction market providers are facing pushback in over a dozen state actions, with state-level regulators arguing that they have jurisdiction over at least sports-related betting products. The Commodity Futures Trading Commission has argued that it has sole jurisdiction over prediction market providers, and filed an amicus brief in one of the federal cases to defend that position.

The CFTC even signed a memorandum of understanding with Major League Baseball, announced at the same time as MLB’s announcement it had partnered with Polymarket.

The negotiation to get a crypto market structure bill through its next stages in the Senate have hovered over an almost-there status for weeks, and Republican lawmakers met on Thursday to figure out how to bridge the final gaps.

The White House was expected to get some updated legislative language on Thursday, reflecting the ongoing work on the Digital Asset Market Clarity Act, according to people familiar with the situation. But the talks are still going, and even if the previously uncertain senators (such as Republican Thom Tillis) become satisfied with the bill’s stablecoin yield treatment, other distinct compromises (such as the approach to decentralized finance) also need to be secured before the Senate would be able to send the crypto industry’s top policy priority to President Donald Trump for a signature.

The longstanding debate that had focused on stablecoin yield — on which bankers and crypto businesses have been divided over the structure of stablecoin rewards programs — is close to a finish, the people said, though lawmakers have been discussing what else the community bankers might be offered to get their support while resolving some of their other priorities. That could include some unrelated provisions tied to Congress’ recent housing legislation, according to reporting from Politico.

Officials from Trump’s administration were said to be involved with the meeting of Republican members of the Senate Banking Committee, which is the second panel that needs to advance the bill before it would be repackaged into a final version that can get a vote of the overall Senate. Even if the effort advances from the committee by the end of April, as Senator Cynthia Lummis predicted this week, a couple of further hurdles may be out of lawmakers’ hands.

Democrats involved in the talks have said they still want senior government officials and lawmakers from profiting off of personal crypto interests — most pointedly aimed at Trump. And they want Democrats appointed to the party’s vacant seats at the Commodity Futures Trading Commission before the agency adopts new crypto rules. Those are both points that could require concessions from the White House, and crypto insiders are expecting those controversial points to be the last matters settled once the lawmakers are working on a final bill.

On the yield issue, Lummis has said that stablecoin rewards programs that steer clear of bank-line language on savings and interest may survive the compromise, insisting they’re more akin to credit-card rewards than interest from bank-account deposits.

Lummis said Coinbase CEO Brian Armstrong, whose opposition to a previous draft bill helped derail an earlier effort to get to a Senate hearing, has been more flexible in recent talks. The company didn’t immediately respond Thursday to a request for comment on its position.

As Congress works, the Securities and Exchange Commission spent much of the week issuing and discussing new crypto policy points, including a first-ever taxonomy that sets out regulatory definitions for U.S. crypto assets. In a CoinDesk op-ed on Thursday, Chairman Paul Atkins and the two Republican commissioners suggested they’re eager to have a new law back up the policy they’re working on.

“Only Congress can rewrite the law, and we stand ready to work with [Commodity Futures Trading Commission] Chairman Michael Selig to implement the CLARITY Act,” they wrote. “In the meantime, we are providing the responsible regulatory approach that markets demand.”

High Point’s win ends the hope of a perfect March Madness bracket for millions

SEC crypto-law interpretation marks a start, not an end

RMT calls off March tube strikes after further talks still ongoing

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

PAKE LOT KECIL KAPAN KAYANYA? #belajarforex #forex #bitcoingold #tradingcuan #cryptocurrency

Crypto Futures Trading Full Course | Crypto Futures Trading For Beginners | SAGAR SINHA

How to Start Investing with Rs. 500 in Pakistan | Financial Literacy for Beginners

-

Crypto World6 days ago

Crypto World6 days agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Tech4 days ago

Tech4 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Addict Lip Glow

-

Tech2 days ago

Tech2 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Sports5 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

Business4 days ago

Business4 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Business5 days ago

Business5 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World5 days ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

Business4 days ago

Business4 days agoAustralian shares drop as Iran war enters third week

-

Business5 days ago

Business5 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Crypto World4 days ago

Crypto World4 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Sports6 days ago

Sports6 days agoCollege Basketball Best Bets: Conference Tournament Semifinal Picks

-

Politics2 days ago

Politics2 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Fashion4 days ago

Fashion4 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

News Videos1 day ago

News Videos1 day agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World1 day ago

Crypto World1 day agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

Crypto World5 days ago

Crypto World5 days agoCrypto Losses Drop 87% in February, But Hackers Are Now Targeting People, Not Code

-

Politics2 days ago

Politics2 days agoReal-time pollution monitoring calls after boy nearly dies

-

NewsBeat1 day ago

NewsBeat1 day agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

Business3 days ago

Business3 days agoMeta planning major layoffs as AI spending and automation reshape workforce

You must be logged in to post a comment Login