Crypto World

Micron (MU) Stock: Analysts Hold Strong Despite Post-Earnings Dip

Key Takeaways

- Micron’s fiscal Q2 2026 delivered $23.86 billion in revenue with adjusted EPS of $12.20, surpassing analyst expectations

- The company projected fiscal Q3 2026 revenue of approximately $33.5 billion, significantly exceeding Street estimates

- Capital expenditure guidance for fiscal 2026 increased to more than $25 billion, roughly $5 billion higher than previous projections

- Shares declined following the earnings announcement despite impressive financial performance, primarily due to elevated spending concerns

- Analyst sentiment remains overwhelmingly positive with 29 Buy ratings, 5 Strong Buys, and no Sell recommendations according to MarketBeat data

Micron Technology unveiled exceptional quarterly results on March 19, yet the market’s response told a more complex story. Despite impressive revenue figures and unprecedented free cash flow generation, shares retreated as Wall Street digested the company’s ambitious capital investment strategy.

The memory chip giant reported fiscal second-quarter 2026 revenue reaching $23.86 billion alongside adjusted earnings of $12.20 per share. Micron also highlighted that it closed the period with $16.7 billion in cash and investments, marking a company record for free cash flow generation.

While these figures impressed, it was the forward-looking commentary that captured the most attention—both positive and negative.

For fiscal Q3 2026, Micron projected revenue of approximately $33.5 billion, substantially exceeding Wall Street’s expectations. The company attributed this robust outlook to explosive demand for high-bandwidth memory (HBM) products, which are essential components in AI data centers and acceleration hardware.

HBM represents today’s most sought-after memory technology. Micron operates within an oligopoly of just three major global producers, joined by Samsung and SK hynix. This concentrated supply structure has bolstered pricing power and supported healthy profit margins.

Understanding the Post-Earnings Decline

Notwithstanding the impressive financial performance, Micron’s stock price declined following the announcement. The catalyst? A significantly revised capital spending forecast.

The company disclosed that fiscal 2026 capital expenditures would surpass $25 billion, representing an approximate $5 billion increase from earlier guidance. Management explained the investment is necessary to expand clean-room infrastructure and accelerate DRAM manufacturing capacity to satisfy AI-driven demand.

This scenario represents a classic semiconductor industry dilemma—deploying massive capital to capture growth opportunities while risking oversupply if market conditions deteriorate. Memory manufacturers have historically encountered this challenge, and investors maintain vivid memories of past overcapacity cycles.

Additionally, the stock’s valuation had already reflected substantial optimism. Prior to Thursday’s retreat, Micron had surged more than 61% during 2026, building on strong momentum from 2025. At such elevated levels, any hint of risk can trigger profit-taking behavior.

Wall Street Maintains Conviction

The analyst community showed no signs of wavering. According to MarketBeat data released on March 19, Micron holds five Strong Buy ratings, 29 Buy ratings, and four Hold ratings. Notably, zero analysts recommend selling the stock.

This represents nearly unanimous bullish positioning. The four Hold ratings suggest some analysts advocate patience at current valuations, but bearish recommendations remain completely absent.

Price targets underwent revisions as analysts updated their financial models following the report. MarketBeat’s consensus tracking indicated a range settling between approximately $425.62 and $446.66.

Several firms subsequently raised their targets. Needham elevated its price objective to $500. UBS similarly increased its target while reaffirming its Buy rating. Both institutions cited the sustained strength of AI-related memory demand as their primary rationale.

These $500 price targets represent more than optimistic projections—they embody a conviction that Micron’s AI-driven growth trajectory extends further than current market pricing acknowledges.

The investment debate surrounding Micron has evolved. Questions no longer center on whether the company is emerging from a downturn. Instead, the focus has shifted to whether Micron can sustain expansion without excessive capital deployment.

Presently, analysts are answering affirmatively. With 34 Buy or Strong Buy ratings and zero Sell recommendations in current MarketBeat data, Micron stands as one of the most broadly supported equities in the AI semiconductor sector.

The stock declined on March 19. The analyst community’s conviction remained intact.

Shares in crypto exchange Gemini surged after hours as stronger-than-expected fourth-quarter results showed revenue growth driven by credit card adoption and a reworked fee structure.

Gemini reported on Thursday that its Q4 revenues rose 39% from the year-ago quarter to $60.3 million, reportedly beating analyst expectations of $51.7 million.

It reported a net loss of $140.8 million for Q4, deepening from its $27 million loss from a year ago. Gemini posted a total 2025 loss of $585 million, ahead of its total 2024 losses of $156.6 million.

Gemini co-founders Cameron and Tyler Winklevoss said in a shareholder letter that Q4 was the company’s highest quarterly revenue in three years, even with trading volumes declining, the revenue gain was reflective of “deliberate fee structure work through the back half of the year.”

Shares in Gemini (GEMI) initially jumped 14% after hours on Thursday to a high of $6.83, but settled at $6.36 for a gain of 5.8% after ending the trading day flat at around $6.

The results are Gemini’s second after going public in September and came amid a broad crypto market decline in late 2025, which saw Bitcoin (BTC) rapidly decline from its all-time peak above $126,000 in October.

Gemini lays off 30% of staff so far this year

In February, Gemini said it was withdrawing from the UK, the EU and Australia, citing challenging market conditions. The company also planned to lay off 25% of its workforce, in part due to artificial intelligence.

In their letter, Cameron and Tyler Winklevoss said Gemini had reduced its workforce by “roughly 30% since the start of 2026,” citing an increased use of AI.

“Today, AI is used in more than 40% of our production code changes and we expect that number to climb to close to 100% in the not-too-distant future,” they said. “Not using AI at Gemini will soon be the equivalent of showing up to work with a typewriter instead of a laptop.”

The Winklevoss brothers said the company’s plan this year was to “focus and double down on America,” adding they were encouraged by the pro-crypto stance of US market regulators.

Prediction markets and credit card key 2026 priorities

Gemini launched its in-house prediction market, Gemini Predictions, across all 50 US states in December, shortly after it obtained a license from the Commodity Futures Trading Commission.

Related: Gemini bets on ‘super app’ as stock sinks to record low on Q3 results

The company said it would refine and expand its prediction market offering and also scale its credit card and exchange.

The Winklevoss brothers said Gemini would “shift into becoming a markets company with Gemini Predictions” and use that infrastructure for its perpetual futures contracts once they’re approved in the US.

Magazine: Are DeFi devs liable for the illegal activity of others on their platforms?

Scammers impersonating the FBI via a token are telling Tron users they are under investigation and must complete a check to avoid having their assets frozen.

The US Federal Bureau of Investigation says a scam using a token on the Tron blockchain is impersonating the agency with the aim of grabbing personal information.

FBI New York’s X account shared on Thursday a message some Tron users received via a token bearing the agency’s name and seal that said their wallet was “under investigation.”

The message then prompts the recipient to complete a sham anti-money laundering verification online “to avoid a total block on your assets.”

The message uses the same urgent call to action as many phishing scams in crypto that steal billions each year. In April, the FBI said it received over 140,000 complaints referencing crypto scams in 2024, resulting in $9.3 billion worth of losses, a 66% increase from the year before.

The FBI told Tron users to “exercise caution” if they encounter the fake token and urged them not to provide “any identifying information to any website associated with such token.”

The FBI said those who may have already sent information to the scammers should file a report with the Internet Crime Complaint Center.

FBI once created token to catch fraudsters

In 2024, the FBI created a fake artificial intelligence-related token to catch fraudsters engaged in market manipulation.

Related: Ex-LA cop gets 5 years in prison for helping crypto ‘Godfather’ extort victims

The so-called “trap token,” called NexFundAI, was designed to act as bait, targeting those engaged in fraudulent crypto activities, particularly pump-and-dump schemes.

At least 18 people who helped manipulate the token’s trading volume were charged in the FBI’s sting operation.

Magazine: China’s ‘50x’ blockchain boost, Alibaba-linked AI mines Bitcoin: Asia Express

Ether (ETH) traded lower on Thursday after a fresh knee-jerk reaction to yesterday’s US interest rate decision and a higher inflation outlook.

Key takeaways:

-

ETH dropped 7% to $2,100 on Thursday, liquidating $144 million in longs.

-

A break below $2,000 could trigger over $2.5 billion in additional long liquidations across exchanges.

-

The 50-day moving average around $2,100 is a key level to watch.

Ether risks $2.5 billion long liquidations

Data from TradingView showed 7% daily ETH price losses, with ETH/USD dropping as low as $2,140 on Thursday.

Ether’s correction is accompanied by significant long liquidations across the crypto market totaling $492.8 million over the last 24 hours. More than $144 million in long ETH positions were liquidated with Ether’s move to $2,100.

The correction occurred despite another 60,999-ETH purchase by Tom Lee’s Bitmine Immersion Technologies, which now holds roughly 4.6 million ETH, or 3.81% of the total supply.

Related: Ether accumulation data points to a rally toward $2.8K, but there’s a catch

Ether’s decline came amid fresh selling in US-based spot ETH exchange-traded funds (ETFs), which recorded more than $55.5 million in net outflows on Wednesday, snapping a six-day inflow streak, according to data from Farside Investors.

Ether’s downward momentum may increase if spot and institutional buyers don’t step back in soon.

Ether’s downside may hinge on the key $2,000 support, as a correction below would trigger over $2.5 billion worth of leveraged long liquidations across all exchanges, CoinGlass data shows.

This means a significant amount of bullish bets would get wiped out on a move lower, leaving ETH vulnerable to a sharper downside cascade if bearish momentum takes hold.

ETH price stays sensitive to FOMC risks

Ether’s bearishness today follows the decision by the US Federal Open Market Committee (FOMC) to leave interest rates unchanged after the March 18 meeting.

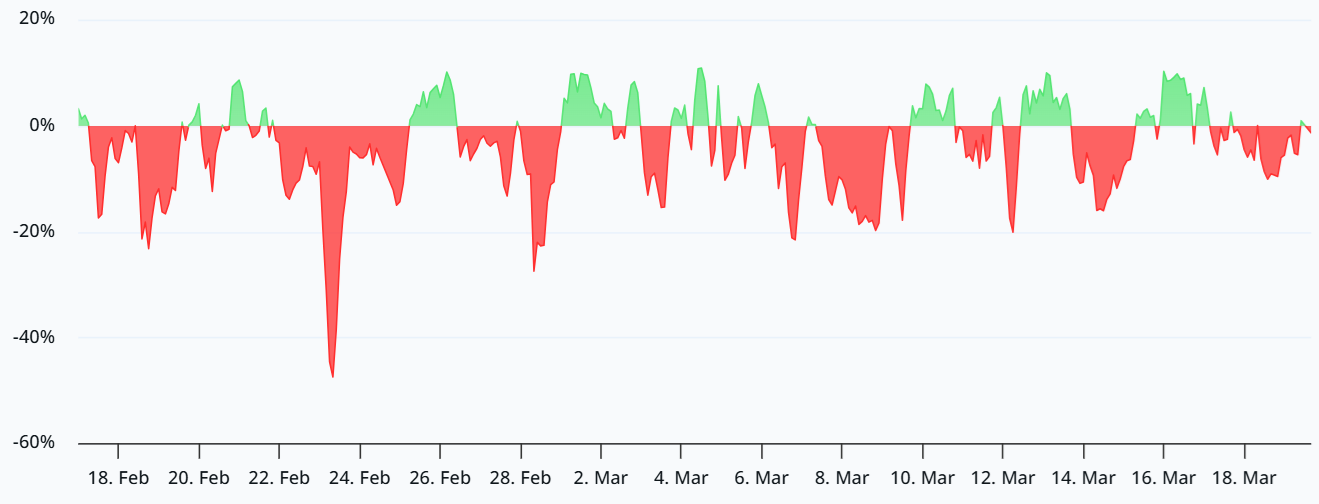

The chart below shows that the ETH/USD pair has declined after seven of the last eight FOMC meetings, establishing one of the clearest macro-driven fractals in its history.

ETH has set a consistent pattern as it stabilizes or rallies ahead of the meeting, then corrects sharply once the decision and the accompanying commentary hit news wires.

Typical post-FOMC drawdowns ranged between 16% and 23%, while deeper deleveraging phases pushed ETH price losses to 33%-43%.

From a technical perspective, Ether remains cautiously bullish despite macro risks. The price is retesting a key support zone near $2,100, which aligns with the upper trendline of an ascending triangle and the 50-day simple moving average (SMA).

Bulls are required to hold ETH above this level to regain their footing. It will then open the path toward the next major resistance at $2,575, where the 100-day SMA is.

Higher than that, the price could rise toward the measured target of the triangle at $2,700, 24% above the current price.

Conversely, failure to hold above $2,100 would weaken the setup, pushing ETH/USD back toward the triangle’s support line near $2,000, while putting the broader recovery at risk.

As Cointelegraph reported, a close below the 20-day exponential moving average near $2,000 would suggest that the bears are back in control, risking a deeper correction toward the next major support area around $1,800.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

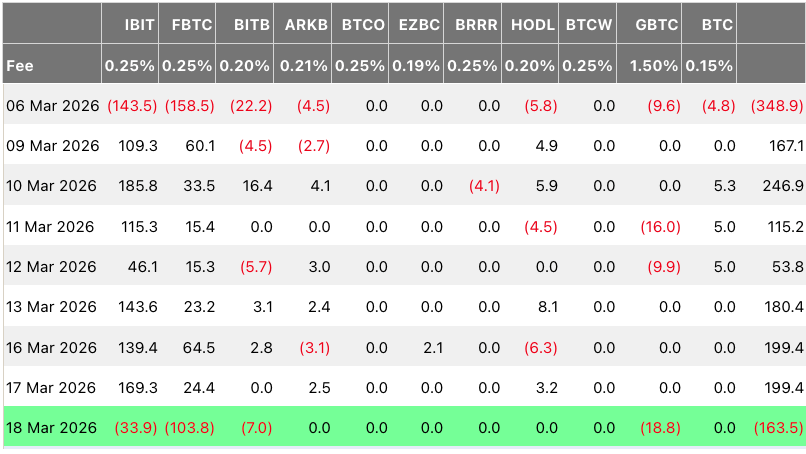

US spot Bitcoin exchange-traded funds (ETFs) ended their inflow streak amid a BTC price dip after recording $1.2 billion of inflows over seven consecutive days.

Spot Bitcoin (BTC) ETFs saw $163.5 million in outflows on Wednesday, according to Farside data.

The Fidelity Wise Origin Bitcoin Fund (FBTC) led the outflows at about $104 million, followed by BlackRock’s iShares Bitcoin Trust ETF (IBIT) with $34 million.

Before Wednesday’s $163.5 million outflows, the ETFs were roughly $100 million shy of positive year-to-date flows, ending their longest inflow streak since October 2025.

The reversal came as Bitcoin fell below $71,000 on Wednesday, after surging above $75,000 earlier in the week, reigniting extreme fear among investors.

Altcoin ETFs share the negative sentiment with minor losses

The negative trend spilled across altcoin ETFs, with Ether (ETH) leading the losses at around $56 million, according to Farside.

Similar to Bitcoin funds, Fidelity Investments led the outflows as the Fidelity Ethereum Fund (FETH) saw redemptions of $37 million, followed by the Grayscale Ethereum Trust (ETHE) with $9 million in outflows.

Solana (SOL) saw minor losses at around $300,000, while XRP (XRP) ETFs reported zero inflows.

Investor sentiment worsened during the day, with the Crypto Fear & Greed Index briefly recovering to 26, or “Fear,” on Wednesday before dipping back to “Extreme Fear” on Thursday.

Kyle Rodda, senior financial market analyst at Capital.com, highlighted the fragile market sentiment driving recent price swings.

“The price-action screams of a market that’s run out of puff and maybe poised for protracted downside,” Rodda said. He referred to rising inflation risks, surging energy prices from the Israel-Iran conflict, and a broader repricing of rate expectations after the Fed lifted its inflation forecast, leaving investors cautious.

Related: Crypto traders eye ‘bullish relief rally’ after Fed holds rates steady

The Federal Open Market Committee (FOMC) announced on Wednesday that it would hold the Federal Funds rate steady at 3.5-3.75%, as it monitors macroeconomic impacts from the ongoing war in the Middle East.

Federal Reserve Chairman Jerome Powell said inflation remained “somewhat elevated” above the Fed’s 2% target, highlighting economic uncertainty stemming from events in the Middle East.

Magazine: Bitcoin’s ‘narrative vacuum,’ Ethereum now inevitable: Trade Secrets

Coinbase Asset Management has moved to tokenize its Bitcoin Yield Fund on the Base blockchain, unveiling a tokenized share class for the fund in partnership with Apex Group. The move is framed as a way to enable institutional access to a yield-bearing Bitcoin exposure while preserving regulatory compliance.

Apex Group said in a statement on Thursday that the tokenized share class of Coinbase Asset Management’s fund “is set up to interact with compatible platforms, wallets, and infrastructure without compromising compliance.”

Coinbase Asset Management president Anthony Bassili said the share class integrates “identity and eligibility at the token level” to support regulatory requirements. The approach reflects a broader push among traditional asset managers to bring tokenized investments—ranging from stocks and bonds to funds and real assets—onto public blockchains in pursuit of lower costs, faster settlement, and around-the-clock trading.

Industry players have been exploring tokenization across a spectrum of assets, with BlackRock, Fidelity Investments, and Franklin Templeton already launching tokenized funds on-chain. The Coinbase initiative adds another high-profile entry to a growing ecosystem of regulated, on-chain fund access.

The tokenized share class of Coinbase’s Bitcoin Yield Fund, which provides exposure to Bitcoin and a yield component, will be available on the Base network only to institutional and accredited investors outside the United States. The arrangement leverages the ERC‑3643 permissioned token standard to ensure that only eligible investors can access the yield product.

Apex acts as the on-chain transfer agent for this tokenized structure, responsible for managing token ownership, enforcing transfer and compliance rules, and maintaining a transparent record of transactions on Base.

Coinbase has signaled plans to broaden access by launching a tokenized share class of the Coinbase Bitcoin Yield Fund for U.S. investors in the future, expanding the program beyond the current non-U.S. eligibility window.

Historically, Coinbase’s non-U.S. version of the Bitcoin Yield Fund targeted an annual return in Bitcoin in the 4% to 8% range. Coinbase explained that the product was designed to provide native yield options for Bitcoin, addressing a gap created by the lack of yield-generating mechanisms for non-staking digital assets compared with proof-of-stake tokens like ETH or SOL.

The broader context for these developments is a formalization of on-chain access to traditional financial products. As institutions seek cost efficiencies and more flexible settlement, tokenized funds and other on-chain assets are becoming increasingly mainstream, albeit with careful attention to regulatory alignment and investor eligibility.

Key takeaways

- The Bitcoin Yield Fund now has a tokenized share class on Coinbase’s Base network, developed with Apex Group for compliant, on-chain handling.

- Access is limited to institutional and accredited investors outside the U.S. for the current tokenized offering, with plans to reach U.S. investors later.

- The token uses ERC‑3643, a permissioned standard designed to restrict ownership to eligible participants and support regulatory controls on-chain.

- Apex serves as the on-chain transfer agent, overseeing ownership, transfers, and compliance data on Base.

- Even as Coinbase rolls out this non-U.S. version, other asset managers including BlackRock, Fidelity, and Franklin Templeton have already launched tokenized funds on-chain, signaling a broader industry trend.

On-chain compliance and the promise of institutional tokenization

At the core of this initiative is a specialized focus on regulatory alignment. By insulating the tokenized share class behind a permissioned standard, Coinbase and Apex are aiming to prevent unauthorized access while enabling seamless interaction with compatible platforms, wallets, and infrastructure. The official framing from Apex emphasizes that the tokenized structure can operate across ecosystems without compromising compliance, a critical consideration for institutions weighing on-chain custody and transfer mechanisms.

Anthony Bassili’s emphasis on identity and eligibility at the token level underscores the shift from purely decentralized narratives toward regulated, auditable on-chain products. In practice, this approach means that investor verification and compliance checks can be encoded directly into the token’s lifecycle, potentially reducing friction in future cross-border and cross-platform dealings for regulated participants.

What’s next for investors and the market

The move arrives at a moment when large fund managers are increasingly experimenting with tokenized vehicles as a way to improve efficiency and broaden access. The non-U.S. version of Coinbase’s Bitcoin Yield Fund sets a precedent for cross-border issuance that prioritizes regulatory controls, while still tapping into the liquidity and programmability offered by Base’s blockchain infrastructure.

Coinbase’s stated intention to roll out a U.S.-based tokenized share class for the Bitcoin Yield Fund will be closely watched. If executed, it would position Coinbase alongside a growing cohort of traditional asset managers pursuing tokenized, yield-bearing offerings for a domestic audience—an area that has drawn attention from regulators and institutional participants alike.

Looking ahead, observers will want to see how broader adoption unfolds: Will more funds adopt ERC‑3643 or similar permissioned standards? How quickly will institutional custodians and exchanges integrate tokenized share classes with existing settlement rails? And what regulatory clarifications emerge as on-chain products expand from foreign-only access to domestic markets?

For now, the Coinbase-Apex collaboration marks a notable step in the ongoing evolution of regulated, on-chain asset issuance. The degree to which this model scales—across asset classes, jurisdictions, and investor bases—will help define the next phase of institutional tokenization in crypto finance.

Readers should watch for updates on the US-tokenized version’s timeline and for further announcements from Apex Group and Coinbase Asset Management regarding platform integrations, eligible investor criteria, and potential expansion to additional fund families.

Nigel Farage has been unknowingly shilling crypto pump and dump schemes. And it only cost scammers £72 a video.

Fraudsters exploited his Cameo profile to purchase personalized clips where Farage read scripts packed with crypto slogans. “To the moon.” “HODL.” Token names dropped in casually. All repurposed as official endorsements for obscure cryptocurrencies that have since collapsed to zero.

Farage charges around £72 per video. He appeared to read the scripts without verifying what he was actually promoting. Retail investors got lured in. The tokens dumped. The Reform UK leader had no idea he was the marketing engine the whole time.

- Scammers paid Nigel Farage for Cameo clips to promote dubious tokens like “Stonks Finance” and “Faragecoin.”

- The endorsed tokens followed a classic pump and dump pattern, crashing shortly after the videos circulated.

- Regulatory loopholes on platforms like Cameo are creating new risks for retail investor protection.

The Tokens Farage Plugged Have One Thing in Common: They Crashed

The Guardian investigation named the tokens. Stonks Finance. NIG Finance. Trump Mania. Faragecoin.

The playbook was identical every time. Video gets posted on X and Telegram alongside claims that Farage “knows what’s up.” Retail buyers pile in. Token spikes. Insiders dump their holdings. Price collapses to near zero. Late buyers absorb all the losses.

One Stonks Finance video alone triggered a brief speculative frenzy before the inevitable crash.

The damage for retail investors has been severe. The tokens are unregulated. The promoters are anonymous. Recovering funds is basically impossible. And the Cameo clips gave these projects just enough legitimacy to bypass the usual red flags most investors would catch.

Farage Has Not Claimed the Videos Were Financial Advice — But That Was Exactly How They Were Used

Farage has publicly positioned himself as a crypto advocate, citing his debanking experience as a reason for supporting Bitcoin as an anti-authoritarian tool. But the tokens in these videos have nothing to do with Bitcoin.

Whether Farage knew his clips were being used for financial promotion is still unclear. The line between a personal shout-out and a commercial endorsement is deliberately blurry on platforms like Cameo. That grey area is exactly what scammers exploit. He has not publicly addressed the allegations. The videos are still out there.

Regulators are struggling to keep up. The FCA and SEC have strict rules for financial promotions but personalized video content sits in a legal grey zone that enforcement consistently lags behind. ]

The market outcome is already settled. The tokens collapsed. The liquidity is gone. Investors learned an expensive lesson. A paid Cameo clip is not due diligence.

Discover: The best new crypto in the world

The post Nigel Farage Cameo Videos Exploited to Promote Pump and Dump Crypto Scams appeared first on Cryptonews.

Key takeaways:

-

SOL derivatives signal bearish sentiment as funding rates hit 0% and put (sell) options trade at a premium.

-

While Solana leads in DEX volume, it faces stiff competition from Hyperliquid in the perpetual contracts sector.

Solana’s native token SOL (SOL) faced a 3-day 11% decline after peaking at $97.70 on Monday. Thursday’s move down to $87 triggered $25 million in leveraged long positions being liquidated, negatively impacting trader sentiment. SOL derivatives currently point to fear of further downside and a lack of conviction from bulls, increasing the odds of retesting the $80 level.

The SOL perpetual futures annualized funding rate stood near 0% on Thursday, signaling a lack of demand for longs. Bears have dominated leverage demand for the past month, which is highly unusual for crypto markets as traders are historically optimistic. Moreover, the mere cost of capital and exchange risks usually drive the funding rate near 9% under neutral conditions.

SOL options markets confirm that professional traders are not comfortable that the $87 level will hold for long.

The delta skew (put-call) jumped to 12% on Thursday, meaning put options traded at a premium relative to equivalent call instruments. Whales and market makers are not comfortable holding downside price exposure, even as SOL trades 70% below its all-time high. Part of this bearishness can be explained by weaker demand for the decentralized applications (DApps) industry.

Solana DApps revenue dropped to its lowest level in 18 months at $22 million, down from $36 million two months prior. The issue is not exclusive to Solana, as DApps revenue declined by 52% on BNB Chain over the same period, but increased competition in perpetual contracts trading is somewhat concerning as Hyperliquid dominates the industry.

While Solana remains the undisputed leader in decentralized exchange (DEX) volumes, driven by Pump, Raydium and Orca, the situation in synthetic derivatives is reversed. Blockchains specifically designed to handle perpetual contracts trading, such as Hyperliquid, Edgex, Zklighter and Aster, handle more than 80% of the total volume.

Related: Altseason is dead, expect shorter cycles and ‘violent’ rotations: Crypto exec

Weak onchain data and bearish derivatives delay SOL price recovery

The launch of an officially licensed S&P 500 Index perpetual futures contract on Hyperliquid has likely contributed to the weaker demand for SOL. The product offer, available for eligible users based outside of the United States, was developed by Trade[XYZ] and adds to the aggregate tokenized equities markets that nears $1.1 billion in assets.

SOL’s current $51 billion market capitalization represents a 42% discount relative to competitor BNB (BNB) at $88 billion. However, the Solana network’s total value locked (TVL) stood at $6.9 billion, while BNB Chain held $5.7 billion in TVL. More importantly, Solana’s 30-day network fees totaled $20.8 million, while BNB Chain had $9.1 million in fees, according to DefiLlama data.

Multiple companies that opted for a digital asset treasury strategy focused on SOL, such as Forward Industries (FWDI US) and DeFi Development Corp. (DFDV US) are underwater in their holdings, adding to the negative sentiment. Ultimately, the weakness in Solana onchain activity and lack of enthusiasm in derivatives markets hint that a bull run above $110 will take longer than anticipated.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

Artificial intelligence is undergoing a structural transformation. What began as conversational interfaces powered by large language models is rapidly evolving into autonomous systems capable of executing real world digital tasks. In this emerging landscape of AI agents, one name has attracted significant attention, OpenClaw.

OpenClaw is not merely another chatbot. It represents a broader shift in how artificial intelligence systems operate, moving from reactive text generation to proactive digital execution. Its rapid rise in popularity has positioned it at the centre of discussions surrounding autonomous AI, intelligent automation and the future of digital work.

This article explores what OpenClaw is, why it gained viral traction, how it works conceptually and what it signals for the next phase of AI agent development.

What Is OpenClaw?

OpenClaw is an AI agent designed to perform tasks in digital environments autonomously. Unlike traditional AI chat interfaces that generate responses based on prompts, OpenClaw aims to interpret objectives, plan actions and execute them across systems.

At its core, OpenClaw transforms a large language model from a conversational engine into an operational agent.

Rather than simply answering questions, an AI agent such as OpenClaw can interpret user goals rather than isolated prompts, break complex objectives into structured steps, interact with software interfaces and APIs, execute commands within digital environments, and adapt its actions based on contextual feedback.

This distinction is fundamental. The shift from responding to acting marks a qualitative evolution in artificial intelligence.

Why Did OpenClaw Go Viral?

Several factors contributed to OpenClaw’s rapid visibility within the AI and developer communities.

Compelling Demonstrations of Autonomous Behaviour

Public demonstrations showed the agent carrying out multi-step digital tasks with minimal supervision. Observers witnessed an AI system planning, executing and iterating, not merely producing text. This display created a strong perception of progress towards genuinely autonomous AI systems.

Alignment with the AI Agent Trend

The rise of autonomous AI agents has been one of the most discussed developments in the post-LLM era. As businesses search for scalable automation and developers explore agent-based frameworks, OpenClaw appeared at precisely the right moment in the innovation cycle.

Accessibility and Developer Interest

Projects that emphasise openness, experimentation and adaptability often gain rapid traction. The idea of an AI agent that developers could explore, extend or integrate resonated strongly with the technical community.

A Clear Narrative, From AI Assistant to Digital Worker

OpenClaw’s positioning as an autonomous agent rather than a chatbot reframed expectations. It was presented not as a conversational novelty, but as a prototype of the future digital workforce.

How Does OpenClaw Work?

While implementations evolve, AI agents like OpenClaw typically rely on a layered architecture that combines reasoning, planning and execution capabilities.

Large Language Model Core

At the cognitive centre of the system lies a large language model. This model interprets instructions, analyses context, reasons through objectives and generates structured action plans.

In this context, the language model is not the final output layer. It functions as the decision-making engine that informs action.

Task Planning Mechanism

A planning module translates high-level goals into manageable subtasks. If instructed to compile a report, the agent may identify required data sources, access relevant tools, extract information, structure the findings and format the output.

This decomposition capability is central to autonomous behaviour.

Execution Layer

The execution layer enables interaction with external systems. This function may involve calling APIs, navigating software interfaces, running scripts, interacting with operating systems or managing workflows across platforms.

This layer converts cognitive reasoning into operational activity.

Memory and Context Management

Persistent memory allows the agent to maintain coherence across extended tasks. Rather than treating each interaction in isolation, the system retains relevant context, previous steps, and intermediate outcomes.

This continuity is critical for complex, multi-stage processes.

OpenClaw Compared with Traditional Chatbots

Traditional chatbots primarily generate textual responses based on user prompts. OpenClaw, by contrast, is designed to execute digital actions in line with user objectives.

A chatbot focuses on conversational interaction. OpenClaw focuses on operational interaction with systems and tools.

Traditional chat interfaces typically lack persistent, task oriented memory. OpenClaw integrates contextual memory to manage longer workflows.

Chatbots do not directly manipulate external systems. OpenClaw is designed to integrate with tools, APIs and digital infrastructures.

In practical terms, a chatbot communicates information. An AI agent such as OpenClaw carries out tasks.

Potential Use Cases of OpenClaw

The strategic relevance of OpenClaw lies in its practical applications. AI agents capable of autonomous execution could reshape multiple sectors.

Enterprise Automation

Businesses increasingly rely on fragmented SaaS ecosystems. An AI agent can bridge tools and automate cross-platform workflows, including reporting pipelines, CRM updates, marketing automation tasks, and structured data processing.

This automated workflow reduces manual intervention and improves operational efficiency.

Software Development and Testing

Developers could leverage AI agents for automated code testing, environment configuration, continuous integration tasks, debugging assistance and deployment management.

An AI agent that understands project context could streamline development cycles and reduce repetitive workload.

Advanced Personal Productivity

Beyond enterprise environments, autonomous agents may assist individuals in managing complex digital workflows, including intelligent calendar coordination, automated document handling, research aggregation and workflow orchestration across multiple tools.

OpenClaw extends productivity beyond reminders and into active task completion.

Strategic Implications for the Future of AI Agents

OpenClaw represents more than a single project. It signals structural shifts in the development of artificial intelligence.

From Conversational AI to Autonomous Systems

The first generation of large language models focused primarily on dialogue. The next phase centres on execution. Competitive advantage will increasingly depend on agents that can act reliably in digital environments.

Emergence of Digital Labour

As AI agents become more capable, they may assume roles previously requiring human digital interaction. AI agents do not necessarily eliminate human oversight, but they do change the distribution of digital labour.

Routine operational tasks could become progressively automated.

Integration as Competitive Advantage

Future AI value may depend less on model size alone and more on integration capacity, specifically on how effectively agents interact with real-world software ecosystems.

OpenClaw reflects this integration-focused paradigm.

Risks and Challenges

Despite its promise, autonomous AI agents introduce substantial considerations.

Granting an AI system access to digital tools requires strict governance structures. A human administrator should manage security and permissions carefully.

Reliability remains critical. If an agent makes incorrect decisions during early stages of a workflow, those errors may propagate throughout the process.

Governance and accountability frameworks are still developing. Questions remain regarding responsibility when autonomous systems perform unintended actions.

There is also the risk of over-automation. Excessive reliance on autonomous systems could reduce human situational awareness in critical operations.

Balancing autonomy with oversight will be essential for responsible adoption.

Is OpenClaw the Beginning of a New AI Era?

The key question is not whether OpenClaw is technically flawless today. The more important consideration is what it represents.

It symbolises the evolution of artificial intelligence from passive assistant to active operator.

If the conversational AI wave defined the early 2020s, the coming phase may be characterised by autonomous AI agents capable of interacting independently with digital systems.

OpenClaw illustrates how large language models can transition from generating insight to delivering execution.

Whether it becomes a dominant platform or remains an early milestone, it clearly reflects a broader trajectory. Artificial intelligence is moving from conversation towards action.

Opinion by: Jason Dominique, co-founder and CEO of ONCHAIN® Labs

For years, whenever we explain what we’re building, the reaction is familiar. There’s curiosity, some skepticism, and then the question that almost always follows:

“If this is such a big problem, why hasn’t it been fixed already?”

The answer is not that the industry failed to notice it, nor that the technology was too immature to address it. Access remained broken because fixing it correctly required rearchitecting how coordination, execution and settlement work together, while leaving it broken was both easier and profitable.

By “access” we mean the path between intent and ownership: the rules, intermediaries and detours that determine whether someone can reach an onchain asset directly or only through a platform that controls the route.

For most of the industry’s history, access has been treated as something users must earn or purchase before participating. Assets must be listed. Wallets must support them.

What began as a pragmatic workaround hardened into a durable economic structure.

If an asset is listed, access is monetized directly. If it isn’t, the native asset required to reach it is still monetized. Either way, the detour pays, regardless of user intent.

In practice, this has created a vast, largely invisible rerouting of value. Today, significant onchain volume is not executed directly against the assets users intend to reach, but is first detoured through intermediary-controlled native assets required to transact on each network.

Access scarcity became an economic artifact

As onchain asset creation accelerated, platforms encountered a real constraint. No exchange, wallet or custodial ramp could realistically surface everything. Scarcity did not appear in liquidity or settlement. It appeared in distribution.

Listings became gates. Routing decisions determined reachability. Once these detours proved profitable, they stopped being temporary.

This was not a moral failure. It was an incentive-driven outcome. Monetizing access required far less coordination, capital and risk than redesigning how users reach onchain assets directly. Once intermediaries realized the detour itself could be priced, there was little reason to remove it, especially when removal required deep architectural changes few teams could afford.

Over time, users were trained to accept the detour as normal. Acquiring intermediary-controlled native assets unrelated to intent. Bridging value across chains. Approving opaque transactions. These steps stopped feeling like friction and started feeling inevitable.

What emerged was an unspoken economic tax on participation, charged not in explicit fees, but in prerequisite assets, extra steps, delayed execution and abandoned intent.

Execution matured but access did not

While access remained economically gated, the execution layer matured rapidly. Automated market makers, permissionless liquidity and composable smart contracts turned execution into a largely solved problem.

These systems were never meant to be destinations. They were plumbing. Early on, interfaces were necessary, so decentralized exchanges became places users “went,” and on-ramps became gateways. Over time, the industry confused those interfaces with the infrastructure itself.

Related: An overview of intent-based architectures and applications in blockchain

That confusion is now unraveling. People are no longer consciously navigating execution venues. Trading increasingly happens inside wallets and applications, with execution abstracted away.

The data reflects this shift. In 2025, the DEX-to-CEX spot volume ratio crossed 21% and peaked above 37% earlier in the year. Centralized platforms still matter, but decentralized execution is becoming the default regardless of where users interact.

As execution fades into the background, the remaining bottleneck becomes impossible to ignore.

Builders are running into a ceiling

For builders, access has quietly become the limiting factor. Reaching users often requires relationships, listing approvals, or forcing users through native assets unrelated to the product’s core value.

This distorts incentives. Innovation slows not because ideas dry up, but because permission becomes the bottleneck. Teams optimize for gatekeepers rather than users. Distribution depends on capital and relationships instead of relevance.

Scale amplifies the problem. Even after issuance slowed in 2025, tens of thousands of tokens continued launching each day. Listing-based access cannot keep up with permissionless creation.

Permissionless issuance paired with permissioned access does not produce open markets. It produces fragmentation.

Access is moving to the transaction layer

The alternative is not another marketplace or aggregator. It is a redefinition of where access lives.

In intent-based and abstracted systems, users express outcomes rather than routes. Transactions dynamically source liquidity, assets and execution at the protocol level. Access stops being something granted by platforms and becomes something enforced by the network itself.

This shift is structural. Solving access at the transaction layer requires deep changes to coordination, execution and settlement, changes that were expensive, risky and slow to implement. That is precisely why monetized detours persisted for so long.

Once access becomes native to the network, the economics of the stack change. Listings lose leverage. Discovery becomes emergent rather than negotiated. Liquidity competes on execution quality rather than placement.

Execution works. Settlement scales. Value moves instantly and globally. The remaining question is whether access continues to be routed through detours users did not choose.

A quiet but irreversible transition

This transition will not arrive with a single protocol launch or headline-grabbing announcement. Systems built on structural friction rarely unwind overnight.

Access is moving closer to execution. When it does, the center of gravity in crypto shifts away from intermediaries and back toward networks.

The change will not be loud. It will be structural. By the time access feels “solved,” the old gates will already be impossible to justify.

Opinion by: Jason Dominique, co-founder and CEO of ONCHAIN® Labs.

This opinion article presents the author’s expert view, and it may not reflect the views of Cointelegraph.com. This content has undergone editorial review to ensure clarity and relevance. Cointelegraph remains committed to transparent reporting and upholding the highest standards of journalism. Readers are encouraged to conduct their own research before taking any actions related to the company.

Bitcoin (BTC) rebounded from weekly lows into Thursday’s Wall Street open as inflation targeted BTC price strength.

Key points:

-

Bitcoin price action preserves its new local trading range between 2021 highs and 2025 lows.

-

Gold leads a macro asset sell-off after the Federal Reserve continued a hawkish stance on interest-rate policy.

-

Fed Chair Jerome Powell says that the next rate cut depended on inflation “progress.”

Bitcoin struggles after hawkish Fed meeting

Data from TradingView showed a drop to $69,500 on the day, with BTC/USD reaching the area of its old all-time high from 2021.

The pair then returned above the $70,000 mark before circling the 2021 level, helping preserve a narrative of comparative strength despite various macro pressures.

On Wednesday, the focus switched from the Middle East and oil to US inflation as the Federal Reserve chose to hold interest rates at previous levels.

“Uncertainty about the economic outlook remains elevated. The implications of developments in the Middle East for the U.S. economy are uncertain,” Chair Jerome Powell said in an official statement.

Powell’s subsequent press conference reiterated that “progress” was required on inflation for rates to come down — a key tailwind for crypto markets.

“The rate forecast is conditional on the performance of the economy, so if we don’t see that progress, you won’t see the rate cut,” he told reporters.

SUMMARY OF FED DECISION (3/18/2026):

1. Fed halts rate cuts for the second straight meeting

2. Fed projects one rate cut in 2026, one in 2027

3. Fed 2026 PCE inflation forecast revised higher to 2.7%

4. Fed says implications of Middle East developments are “uncertain”

5. Fed…

— The Kobeissi Letter (@KobeissiLetter) March 18, 2026

With just a single cut in 2026 now expected, risk assets felt pressure from the Fed, with US stocks ending the day down by around 1.5%.

Trader: BTC price needs weekly close near $75,000

On Thursday, however, it was gold leading the comedown, falling 2.3% below $4,700 per ounce for the first time since Feb. 6.

Related: $58K BTC price still in play? Five things to know in Bitcoin this week

“All assets, except Oil, continue to sell off,” crypto analyst Michaël van de Poppe responded in a post on X.

“Not a bad case here. The opposite: Bitcoin is also correcting, and it’s correcting less than I would assume.”

BTC price action thus returned to a range bordered by the 2021 all-time high and the lowest level of 2025 at around $74,500.

“$BTC is still rejecting 2025 Yearly Lows. Won’t be of significance during the week, need weekly close above there,” trader Castillo Trading told X followers on Wednesday.

Van de Poppe said that he would be a “big buyer” of Bitcoin if it were to drop back to the low $60,000 zone.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

Geopolitical volatility makes strong case for bonds; stick to short-term funds: Devang Shah

Netflix Exec Addresses Meghan Markle & Prince Harry Relationship

Meningitis outbreak: Students turned away for vaccines in Kent

-

Crypto World6 days ago

Crypto World6 days agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Tech4 days ago

Tech4 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Addict Lip Glow

-

Tech2 days ago

Tech2 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Sports6 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

Business4 days ago

Business4 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Business6 days ago

Business6 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World5 days ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

Business4 days ago

Business4 days agoAustralian shares drop as Iran war enters third week

-

Business6 days ago

Business6 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Crypto World4 days ago

Crypto World4 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Sports6 days ago

Sports6 days agoCollege Basketball Best Bets: Conference Tournament Semifinal Picks

-

Politics2 days ago

Politics2 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Fashion4 days ago

Fashion4 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

News Videos1 day ago

News Videos1 day agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World1 day ago

Crypto World1 day agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

Crypto World5 days ago

Crypto World5 days agoCrypto Losses Drop 87% in February, But Hackers Are Now Targeting People, Not Code

-

Politics3 days ago

Politics3 days agoReal-time pollution monitoring calls after boy nearly dies

-

NewsBeat1 day ago

NewsBeat1 day agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

Business4 days ago

Business4 days agoMeta planning major layoffs as AI spending and automation reshape workforce

You must be logged in to post a comment Login