Crypto World

Bitcoin Nears $90K After Trump Scraps 10% Tariffs

Join Our Telegram channel to stay up to date on breaking news coverage

Bitcoin is seeking the $90,000 reclaim as US President Donald Trump dropped tariff threats and ruled out seizing Greenland from an ally by force.

Trump’s theatrics and consequent tensions have kept markets on edge this week, prompting investors to take the latest developments with a pinch of salt even as relief was palpable.

BTC has edged up a fraction of a percentage to trade at $89,955 as of 1:19 a.m. EST, with an intraday low of $87,304 and a high of $90,295, according to Coingecko data.

The crypto market also edged up to $3.13 trillion in market capitalization. As a result, the total liquidations in the crypto market came in at $605 million.

Trump Backs Off EU Tariffs, Markets Edge Higher

Crypto investors eased back into risk after President Donald Trump struck a calmer tone on Greenland and signaled a path toward a deal that pulled some heat out of markets.

According to Trump, he had reached the “framework of a future deal” involving NATO over Greenland, and indicated he would hold off on the tariff threat.

JUST IN: Trump says the US has outlined a framework for a future deal involving Greenland after a meeting with NATO Secretary General Mark Rutte

Tariffs scheduled for Feb. 1 have been postponed.

Negotiations will be led by VP JD Vance and Secretary of State Marco Rubio…— Laura Shin (@laurashin) January 21, 2026

“It’s a long-term deal. It’s the ultimate long-term deal. It puts everybody in an excellent position, especially as it pertains to security and to minerals,” Trump told reporters.

While speaking at the World Economic Forum in Davos, Trump said he would not impose the tariffs and ruled out the use of force in the dispute over the Danush territory.

“I won’t do that,” the U.S. President said at Davos of an attack to secure Greenland.

“Okay? Now everyone’s saying,’ Oh, good,’ that’s probably the most significant statement I made because people thought I would use force. I don’t have to use force, I don’t want to use force, I won’t use force.”

Trump’s words came as markets waited to see the full extent of EU trade retaliation over the Greenland issue.

As the crypto markets edged higher, gold prices remained largely steady after hitting a record high near $4,900/ounce in the previous session.

Silver prices rose 1% to $94.03 per ounce, just below record highs of $95.89/oz hit earlier this week.

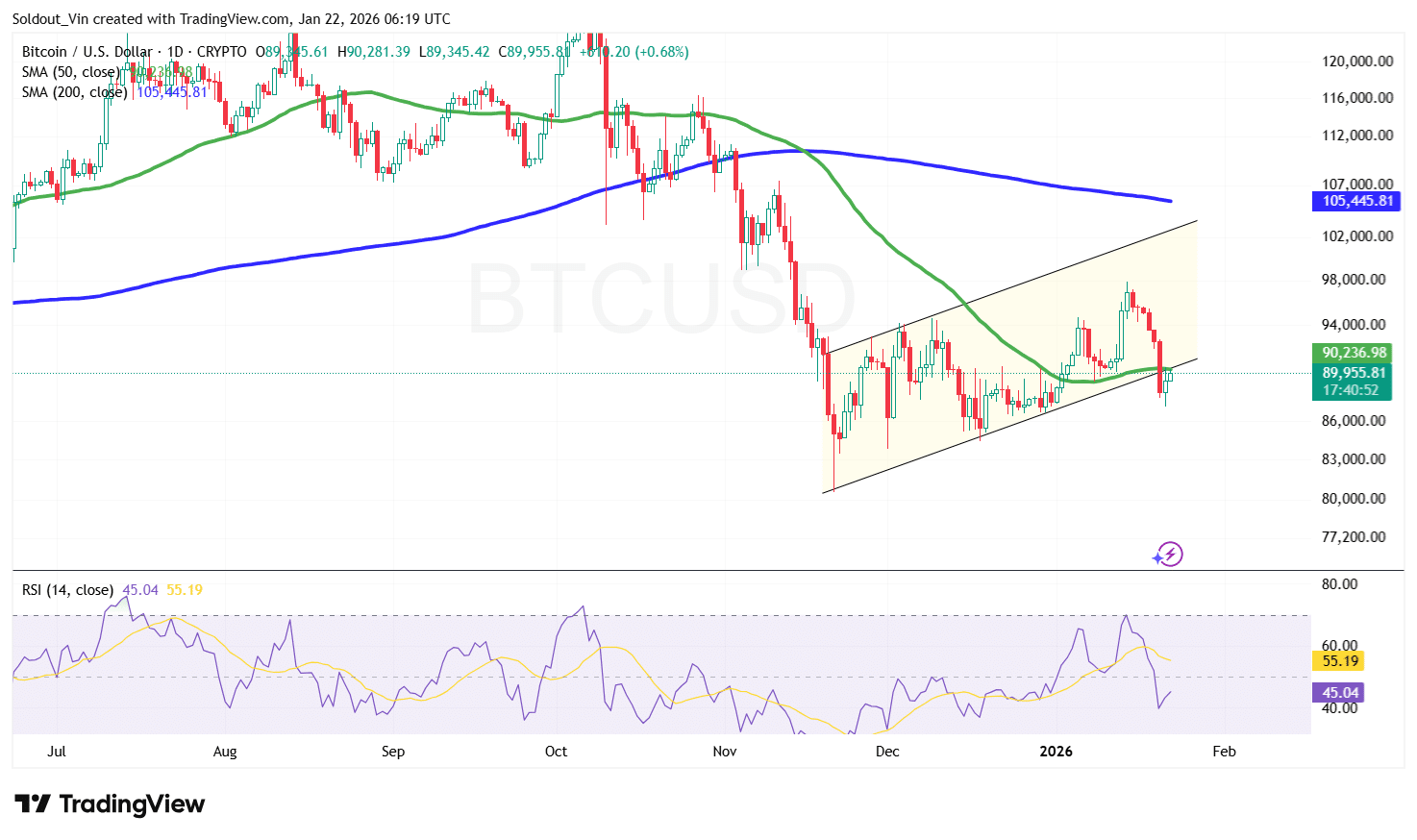

Bitcoin Price Set For A Rally Back Above $100K

Bitcoin price is currently consolidating near the $89,000–$90,000 region, holding just above short-term support around $87,000–$88,000, which buyers have defended following the sharp sell-off from November highs.

This consolidation comes after a strong decline from the $115,000 area, where selling pressure accelerated and forced the price of BTC into a corrective phase. Demand stepped in near the $82,000 zone. The rebound from this area suggests downside momentum has slowed in the long term.

Bitcoin is trading around the 50-day Simple Moving Average (SMA) near $90,200, but remains well below the 200-day SMA around $105,000, which continues to act as major resistance on the upside.

The downward slope of the 200-day SMA indicates the broader trend remains bearish unless Bitcoin can reclaim this level and hold above it.

Bitcoin’s Relative Strength Index (RSI) is hovering around 45, sitting below the neutral 50 mark. This suggests momentum remains weak, though not oversold, leaving room for a recovery attempt if buying pressure increases.

From the 1-day BTC/USD chart, Bitcoin price is trading within a rising channel following the sell-off. This structure often represents a bearish continuation pattern, with price currently trading between channel support and resistance. A move toward the $94,000–$98,000 resistance zone is possible, where the upper channel boundary aligns with prior rejection levels.

A clean breakout above $98,000, followed by a reclaim of the 200-day SMA near $105,000, would be the first meaningful signal of a trend reversal.

For Bitcoin to realistically target a sustained move back above $100K, it would need a confirmed trend shift, which may call for a close above the $95,000 zone.

Conversely, failure to break above channel resistance could trigger another pullback, with $88,000 acting as initial support, followed by the $85,000 demand zone if selling pressure returns.

Related News:

Best Wallet – Diversify Your Crypto Portfolio

- Easy to Use, Feature-Driven Crypto Wallet

- Get Early Access to Upcoming Token ICOs

- Multi-Chain, Multi-Wallet, Non-Custodial

- Now On App Store, Google Play

- Stake To Earn Native Token $BEST

- 250,000+ Monthly Active Users

Join Our Telegram channel to stay up to date on breaking news coverage

A Brazilian security researcher has warned others of the latest counterfeit Ledger device scam aimed at stealing users’ crypto.

Posting as “Past_Computer2901” on the “ledgerwallet” Reddit channel on Thursday, the security researcher said they purchased what they thought was a legitimate Ledger device for personal use, but soon realized after it arrived that it was a sophisticated counterfeit aimed at stealing user funds.

“This isn’t meant to cause panic, but rather to serve as a serious warning — I’m honestly still a bit shaken by the sheer scale of this operation,” they said.

Scammers are adopting increasingly sophisticated strategies to target users opting for self-custody, from supply chain attacks to social engineering and approval scams.

Earlier this month, more than 50 victims were tricked into revealing their seed phrases on a fake Ledger Live app that made its way to the Apple App Store via a bait-and-switch strategy. The victims lost a combined $9.5 million before Apple took down the malicious app.

How the counterfeit Ledger device scam works

The researcher said he bought the Ledger Nano S Plus from a Chinese marketplace, which was priced the same as the official Ledger store. The packaging and the listing also appeared legitimate at first.

However, when they connected the device to the genuine Ledger Live app — which was luckily already installed on their computer — it failed Ledger’s built-in “Genuine Check.”

This prompted them to pull apart the device, discovering modified hardware and firmware designed to capture and expose sensitive wallet data.

The security researcher said the scammers target first-time Ledger users, as the QR code that comes in the box would normally direct users to download a malicious version of the Ledger Live app that would show a fake “Genuine Check.”

Users continuing to follow the prompts will eventually allow scammers to obtain a user’s seed phrases and drain funds at any time.

“Stay safe out there. Only download Ledger Live from ledger.com. Only buy hardware from ledger.com,” the security researcher said.

“If your device fails the Genuine Check — stop using it immediately.”

After pulling apart the device, they discovered clear signs of tampering, including scraped chip markings and a WiFi and Bluetooth antenna embedded inside the unit.

Legitimate Ledger hardware products are designed to keep private keys fully offline.

Related: Musician loses $420K Bitcoin ‘retirement fund’ via fake Ledger app

The security researcher then looked into the firmware, putting the “chip into boot mode,” which initially identified the device as a Nano S Plus 7704 with an attached serial number.

However, once the boot sequence completed, another manufacturer’s name showed up: Espressif Systems, a publicly listed Chinese semiconductor company based in Shanghai.

Cointelegraph reached out to Espressif for comment but didn’t receive an immediate response.

Magazine: What’s a ‘Network State’ and are there real-life examples? Big Questions

The Australian dollar is undergoing a corrective decline after reaching recent highs, with the current move driven by market reaction to newly released macroeconomic data. Earlier gains in AUD were supported by improving global risk sentiment and steady demand for commodity-linked currencies. However, weaker labour market figures have prompted a reassessment of expectations and triggered profit-taking.

Employment data published yesterday pointed to a slowdown in growth, raising concerns about the durability of the economic recovery. Although full-time employment increased, overall job growth came in below forecasts, while the unemployment rate showed little change. Together, these factors weighed on the Australian dollar and led to a reassessment of its short-term outlook following the prior rally.

Toward the end of the week, market participants will focus on upcoming macroeconomic releases, including data on economic activity, central bank commentary, and commodity market statistics. These factors may reshape expectations and influence the direction of commodity currencies.

AUD/USD

After reaching a yearly high near 0.7180, AUD/USD has pulled back, forming a “Bearish Harami” reversal pattern. A bearish close in the current session could increase the likelihood of a deeper correction towards 0.7100–0.7120.

At the same time, a renewed break above the recent high would signal continued bullish momentum and a return of buyers to the market.

Key events for AUD/USD:

- today at 13:00 (GMT+3): International Monetary Fund meetings;

- today at 18:30 (GMT+3): speech by FOMC member Mary Daly;

- today at 22:30 (GMT+3): CFTC net speculative positions on AUD.

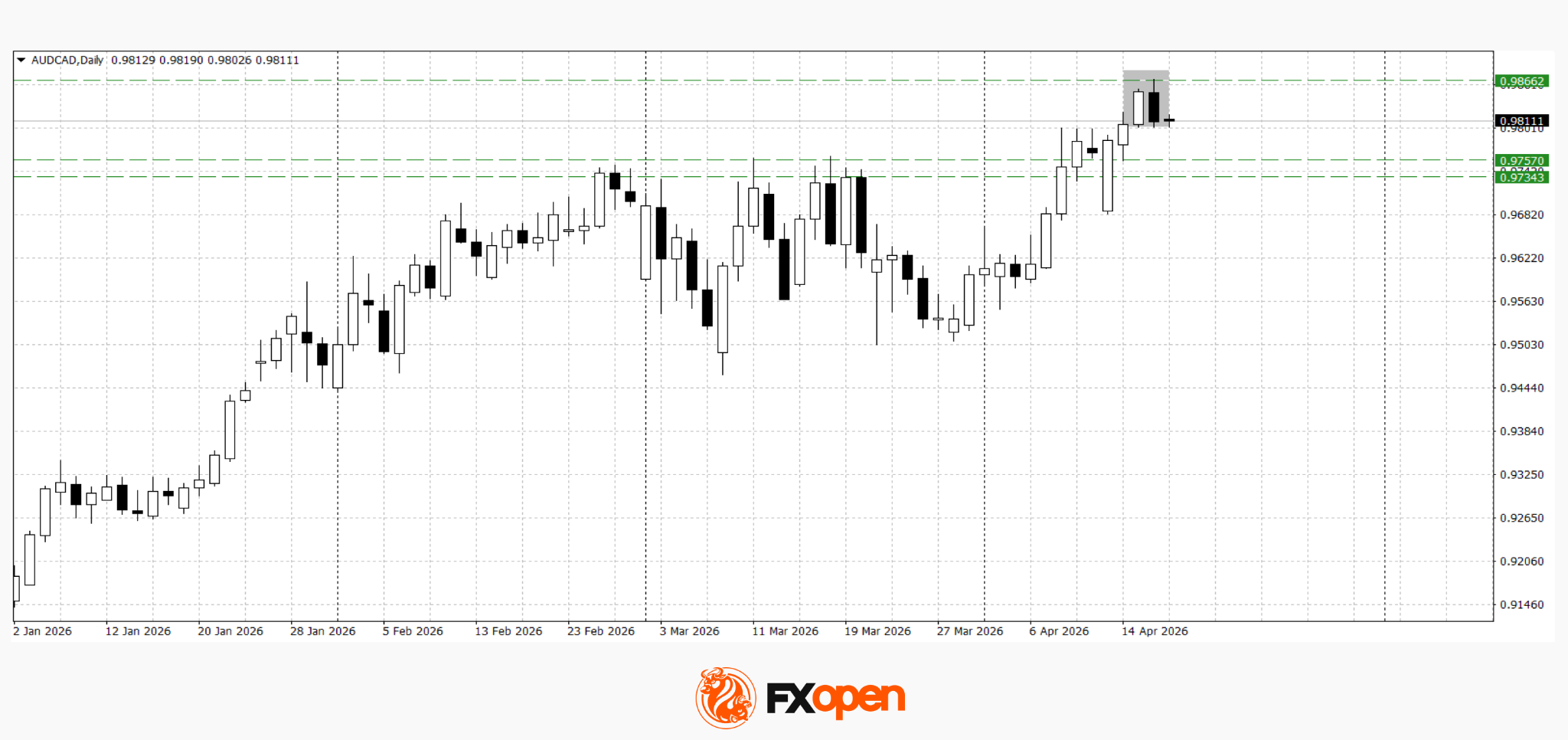

AUD/CAD

AUD/CAD is also moving lower, reflecting both weakness in the Australian dollar and relative resilience of the Canadian currency. Commodity market dynamics remain an additional driver, with energy prices and global demand expectations continuing to play a key role.

Technical analysis suggests the potential for a correction towards 0.9730–0.9760, as a “Dark Cloud Cover” reversal pattern has formed on the daily timeframe. A retest of recent highs will help assess the strength of demand and the likelihood of a renewed uptrend.

Key events for AUD/CAD:

- today at 15:30 (GMT+3): Canadian housing starts;

- today at 15:30 (GMT+3): foreign investment in Canadian securities;

- today at 20:00 (GMT+3): Baker Hughes rig count.

The current pullback in the Australian dollar follows weaker labour market data after a period of steady gains. If downward pressure persists, the correction may deepen. However, stabilisation in the external environment and supportive incoming data could allow the broader upward trend to resume.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

The US government transferred approximately 8.2 Bitcoins (BTC), worth roughly $606,000, to Coinbase Prime.

The transfer was tied to the 2016 Bitfinex hack seizure, according to on-chain data flagged by Arkham Intelligence.

Why These Bitcoins Are Unlikely to Hit the Market

The wallet executed two back-to-back outflows, splitting the move into a 7.999 BTC transaction and a smaller 0.197 BTC deposit routed to the same Coinbase Prime address.

Follow us on X to get the latest news as it happens

Exchange-bound transfers often spark speculation of an imminent liquidation. However, these specific coins are legally committed elsewhere.

A federal court approved the return of approximately 94,643 BTC to Bitfinex through restitution agreements in early 2025. The ruling established Bitfinex as the sole victim entitled to recovery.

Thursday’s outflow follows earlier 2026 transfers from the federal wallet on March 3 and April 10. US government wallets currently hold 328,361 Bitcoin worth roughly $24 billion as of April 2026, according to Arkham data. The latest transfer equals over 0.0024% of the stash.

Ilya Lichtenstein executed 2,000 fraudulent transactions to steal 119,754 BTC from Bitfinex in 2016. He received a 5-year prison sentence in November 2024.

Lichtenstein and his wife, Heather Morgan, pleaded guilty to conspiracy to commit money laundering in August 2023. He earned early release in January 2026 under the First Step Act.

The post US Government Moves Over $606,000 Bitfinex Hack Bitcoin to Coinbase Prime appeared first on BeInCrypto.

Ethereum price, just like any other major alt, is hovering and holding the bullish prediction. The network also reminds us that ETH has never once stopped producing blocks.

At BUIDL Asia 2026, Ethereum Foundation researcher Luca Zanolini confirmed a roadmap target to reduce transaction finality to under one minute. Meanwhile, the long-to-short ratio sits at 1.54, a quiet signal that smart money is accumulating while retail hesitates.

Zanolini’s remarks, delivered April 17 at the Sofitel Ambassador Seoul, cut to the heart of Ethereum’s design philosophy.

“Ethereum was designed to keep producing blocks even if participation drops,” he said. “The next challenge is to preserve that feature while reducing transaction finality to less than one minute.”

In 2023, Ethereum kept producing blocks uninterrupted even after client errors knocked more than half of all validators offline. The finality improvement carries a 2029–2030 implementation target, and the fundamental thesis is getting reinforced.

Discover: The best pre-launch token sales

Ethereum Price Prediction: $2,420 the Target

ETH has traded in a tight bullish range between $2,285 and $2,360 over the past 24 hours, with 24-hour trading volume exceeding $18 billion. This figure reflects active participation at these levels, without liquidity drifting lower. The funding rate is essentially neutral at 0.0001%, suggesting no extreme leverage in either direction.

The critical support zone is $2,250. As long as ETH holds above that floor, the technical structure favors a push toward $2,420 resistance. A clean break above $2,420 opens the path to $2,870, a level that would approach territory last seen before the drawdown from ETH’s all-time high of $4,950. That’s still a 52% discount from peak. The upside, in percentage terms, remains substantial.

Open interest dynamics suggest the market is coiled with a sharp move in either direction plausible. The 1.54 long-to-short ratio implies directional conviction from larger players, but conviction alone doesn’t override macro headwinds. Watch the $2,250 level closely.

Discover: The best crypto to diversify your portfolio with

LiquidChain to Fix What ETH Can’t?

ETH may be the chain that never sleeps, but it also carries the weight of a $280B market cap. Meaningful upside from here requires macro tailwinds, a breakout above multi-week resistance, and sustained institutional demand. That’s a crowded list of conditions.

The make-or-break levels are tightening, and for traders sizing positions accordingly, the risk/reward at $2,330 is narrower than it was 5 years ago. Early-stage infrastructure plays offer a different equation entirely.

LiquidChain ($LIQUID) is a Layer 3 infrastructure project built around a single, operationally direct thesis: fuse Bitcoin, Ethereum, and Solana liquidity into one execution environment. The cross-chain fragmentation problem is real and expensive, and LiquidChain’s Unified Liquidity Layer targets it directly, with Single-Step Execution and Deploy-Once Architecture allowing developers to access all three ecosystems without redeployment overhead.

A new layer emerges. Only a few see it first. — LiquidChain (@getliquidchain) March 24, 2026

The future is LiquidChain  ⟁https://t.co/vqvBcdSj94 pic.twitter.com/R7ZeZ0NPGl

⟁https://t.co/vqvBcdSj94 pic.twitter.com/R7ZeZ0NPGl

The presale is currently priced at $0.0145, with $675K raised to date, and not to forget the huge but limited 1600% APY staking for early buyers. Verifiable Settlement adds an institutional-grade accountability layer that early L3 competitors have largely ignored.

For those already positioned in ETH and watching this level with caution, it may be worth taking a closer look: research LiquidChain here.

The post Ethereum Price Prediction: The Chain That Never Sleeps appeared first on Cryptonews.

The shift to Optimism is ZPG’s first deployment on a public blockchain since launching in 2022, and the start of its global rollout.

Mitsui & Co. Digital Commodities (MDC), a subsidiary of Japanese trading giant Mitsui & Co., Ltd., its tokenized gold, silver, and platinum asset, Zipangcoin (ZPG), on Optimism’s Ethereum Layer 2, OP Mainnet, according to a press release shared with The Defiant.

ZPG has been issued under Japan’s regulatory framework since 2022 and currently runs on Miyabi, a proprietary private blockchain developed by longtime crypto exchange bitFlyer.

The OP Mainnet deployment marks the first time the asset will be issued in a public blockchain ecosystem. Per the release, Japanese CEX GMO Coin will list ZPG on April 20.

MDC’s parent, Mitsui & Co., is a Fortune Global 500 conglomerate with a market cap of over $94 billion, and Berkshire Hathaway as its largest shareholder, the release notes.

MDC also stated in the release that the choice of OP Mainnet follows deliberate due diligence, highlighting that OP Stack chains processed over 6 billion transactions in 2025 — 29x growth in two years.

According to DefiLlama, OP Mainnet currently has a total value locked in DeFi of over $393 million, making it the 17th largest chain in DeFi by TVL. The chain’s stablecoin market cap is approaching $579 million, and $30-day DEX volume is over $623 million.

Sho Miichi, MDC’s representative director & president, was quoted in the release saying: “We are pleased to partner with Optimism to bring a high-quality, commodity-linked digital asset from Japan to investors worldwide.”

Kyle Jenke, chief business officer at OP Labs, described Japan’s regulatory clarity as “one of the most compelling markets for on-chain finance,” adding:

“Zipangcoin is a commodity-backed cryptoasset issued by Mitsui & Co. Digital Commodities and will be the first cryptoasset issued by a Japanese company to launch on OP Mainnet.”

The ZPG launch on Optimism fits into a broader wave of institutional-grade assets moving on-chain.

On-chain tokenized RWAs tripled to roughly $18.6 billion over the course of 2025, with analysts projecting the market could reach $2 trillion by 2030.

Earlier this year, ether.fi migrated its crypto neobank — with $5.7 billion in TVL and around 50,000 active cards — from Scroll to OP Mainnet to access enterprise-grade payment infrastructure.

Tokenized precious metals trading has surged in recent months across both centralized and decentralized platforms. Earlier this week, decentralized perpetual exchange GMX launched 24/7 gold and silver markets on L2 Arbitrum, recording more than $10 million in trades on the first day.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

Key Takeaways

- Charles Hoskinson, founder of Cardano, claims Bitcoin’s BIP-361 quantum protection measure is misleadingly classified as a soft fork when it actually demands a hard fork.

- The BIP-361 framework suggests locking quantum-susceptible Bitcoin wallets and mandating users transition to quantum-resistant addresses.

- BIP-361’s zero-knowledge proof recovery mechanism fails to assist holders of approximately 1.7 million Bitcoin generated before 2013 seed phrase protocols were standardized.

- Roughly 1.1 million of these coins are attributed to Bitcoin creator Satoshi Nakamoto and would face permanent lockdown if the measure is implemented.

- Data reveals that by March 1, 2026, over 34% of circulating Bitcoin features exposed public keys susceptible to quantum computing threats.

Cardano’s creator Charles Hoskinson has openly challenged Bitcoin’s planned quantum computing countermeasure, claiming it carries a misleading technical classification and offers no safeguard for the network’s earliest holdings.

The measure under scrutiny is BIP-361, jointly developed by Bitcoin core developer Jameson Lopp alongside other contributors. The proposal seeks to eliminate Bitcoin addresses exposed to quantum computer vulnerabilities by locking those holdings and requiring users to transfer to more secure addresses.

During a livestream broadcast this week, Hoskinson referenced statistics indicating that by March 1, 2026, more than 34% of circulating Bitcoin will have public keys exposed on the blockchain. This represents approximately 8 million Bitcoin vulnerable to attack from advanced quantum computing systems.

BIP-361 incorporates a zero-knowledge proof recovery framework designed to enable holders with standard wallet seed phrases to verify ownership and retrieve frozen assets following migration.

However, Hoskinson contends this recovery mechanism fails for roughly 1.7 million Bitcoin stored in wallets created before the BIP-39 seed phrase protocol gained widespread adoption around 2013.

These legacy wallets utilized an alternative key generation approach from Bitcoin’s original client software. They depended on local key pools instead of recoverable seed phrases. Without seed phrase access, constructing the zero-knowledge proof necessary for coin retrieval becomes impossible.

“1.7 million coins can’t do that. It’s not possible. 1.1 million of which belong to Satoshi,” Hoskinson stated.

The Hard Fork Controversy

Beyond recovery limitations, Hoskinson contested BIP-361’s classification. He argued the proposal presents itself as a soft fork while functionally demanding a hard fork due to its invalidation of existing signature schemes that remain actively deployed.

“To actually do this, you need a hard fork,” Hoskinson explained. Bitcoin has never implemented a hard fork, and its development community has traditionally resisted such changes.

Lopp, one of the proposal’s co-authors, admitted on X this week that he personally dislikes the plan and characterized it as “a rough idea for a contingency plan” instead of a finalized specification.

Lopp has maintained that freezing inactive coins—which he calculates at 5.6 million Bitcoin—would be more favorable than allowing future quantum attackers to recover and liquidate them in markets.

Governance Structure and Institutional Influence

Hoskinson additionally contended that Bitcoin’s absence of formal on-chain governance infrastructure leaves it without clear procedures for resolving such critical decisions. He cited Cardano, Polkadot, and Tezos as blockchain networks equipped with structured governance frameworks capable of addressing similar matters through community-driven voting mechanisms.

He predicted that major institutional stakeholders, including asset management firms that have accumulated substantial Bitcoin positions in recent years, will ultimately force Bitcoin developers to implement changes despite potential community opposition.

Should BIP-361 be adopted in its present formulation, the approximately 1.7 million pre-2013 coins would become irreversibly frozen without any recovery mechanism available.

Here is something worth noting about bitcoin . Beneath all the noise from daily price swings, X posts and macro headlines, there is a remarkably simple indicator that has quietly called every major market bottom since 2015. Not once, but every single time.

To the dismay of bulls, it hasn’t fired yet, suggesting the broader bear market may not be over, and the recent bounce to $75,000 from $65,000 could be a temporary recovery.

The indicator

It involves two lines on the price chart. That’s it, no complex formula, analysis of blockchain data needed.

These two lines represent bitcoin’s average price over the past 50 and 100 weeks. They act as simple moving averages, showing near-term and long-term trends in bitcoin’s price.

Most of the time, the 50-week average is above the 100-week line. That’s the natural state for markets that trend upward over time, as is the case with bitcoin.

But occasionally, during periods of peak fear, when selling is relentless, and sentiment has collapsed, the 50-week average falls below the 100-week average. This crossover is known as a bear market signal.

It has occurred three times in bitcoin’s history. Each time, it has coincided with the end of a bear market, marking major price bottoms that have not been revisited since.

In other words, it’s been a contrary indicator, ironically marking bottoms rather than deeper downturns.

Three times, three bottoms

Look at the vertical lines on the chart going back to 2015. These mark the three bearish crossovers – April 2015, February 2019, and September 2022. Each one occurred near the bottoming phase, not precisely at the lowest point, but within the same range.

In 2015, BTC was written off as a failed experiment. Then the crossover happened. BTC subsequently rallied from $200 to nearly $20,000 by the end of 2017. A similar pattern played out after the early 2019 crossover.

The 2022 crypto winter, characterized by several bankruptcies and scams, shattered investor confidence. The downtrend, however, ran out of steam after the crossover happened in September. BTC bottomed out in the final months and later chalked out a rally to $126,000 by October 20205.

Each of these bull runs delivered returns far exceeding those of equities and other major asset classes.

What is it saying now?

As of April 17, the crossover has not happened.

Bitcoin has declined sharply from its October record high of over $126,000 to around $75,000, briefly reaching $60,000 in early February. As a result, the two averages are moving closer together, but the 50-week average still holds above the 100-week average.

The takeaway: If history is any guide, the broader bear market may still be intact and could worsen before finding a bottom. It also means that the recent bounce toward $75,000 is likely a temporary recovery rather than the start of a full-fledged bull market.

That said, historical patterns are just that – patterns – and they do not guarantee future outcomes. If U.S. equities, already at record highs, continue to advance, institutional demand for Bitcoin ETFs could strengthen, potentially supporting a price rally.

Cardano (ADA) founder Charles Hoskinson argues BIP-361’s zero-knowledge recovery mechanism cannot rescue roughly 1.7 million Bitcoin (BTC) locked in pre-2013 addresses. This includes roughly 1.1 million Bitcoins attributed to Satoshi Nakamoto.

Casa co-founder Jameson Lopp and five co-authors submitted the Bitcoin Improvement Proposal (BIP-361). It seeks to sunset legacy ECDSA/Schnorr signatures, rendering funds on those addresses unspendable.

Hoskinson Flags Fatal Gap in Bitcoin’s Quantum Plan

Estimates indicate that over 34% of Bitcoin is held in addresses potentially vulnerable to future quantum threats, prompting renewed focus on mitigation efforts. The BIP-361 proposal seeks to address the vulnerability.

The draft phases out legacy Bitcoin signatures in three stages. Phase A blocks new sends to vulnerable addresses. In Phase B, nodes would reject all transactions that rely on ECDSA and Schnorr signatures

Phase C, pending further research, would let holders recover frozen coins. They would submit a zero-knowledge proof of possession of a BIP-39 seed phrase. However, concerns remain over the feasibility of such recovery. In a recent video, Hoskinson stated that,

“1.7 million coins can’t do that. It’s not possible. 1.1 million of which belong to Satoshi.”

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

He explained that these coins originate from Bitcoin’s early architecture, which predates modern standards like BIP-39 seed phrases and hierarchical deterministic key generation.

As a result, they fall outside the assumptions required for zero-knowledge-based recovery systems, limiting the effectiveness of proposals like BIP-361 for older holdings.

“if you build a ZK system based upon proof of a statement, your bit 39 key, say I have these things, you can recover some of the 8 million Bitcoin, but 1.7 million are on not under this scheme. All of the 2013 Bitcoin and before,” he added.

The limitation is acknowledged in BIP-361 itself, which concedes it is “not possible to construct a proof of HD wallet ownership for UTXOs created before BIP-32 existed.”

“Phase C is also compatible with an ‘Hourglass’ style BIP for spending P2PK encumbered funds, provided such a BIP has activated by the time Phase C activates,” the draft reads.

Hoskinson also disputes the soft-fork classification. He says the plan would require a hard fork. The BIP-361 text acknowledges that consensus rules may eventually need to loosen.

“After Phase B, both senders and receivers will require upgraded wallets. Phase C, if activated in conjunction with Phase B, may be soft forkable, otherwise it would likely require a loosening of consensus rules (a hard fork) to allow vulnerable funds to be recovered,” the authors wrote.

Notably, Lopp acknowledged the discomfort with the proposal, stating that he does not like it himself but considers the alternative even less acceptable.

Follow us on X to get the latest news as it happens

The post Why BIP-361 Can’t Rescue Satoshi’s Bitcoin, According to Charles Hoskinson appeared first on BeInCrypto.

Crypto World

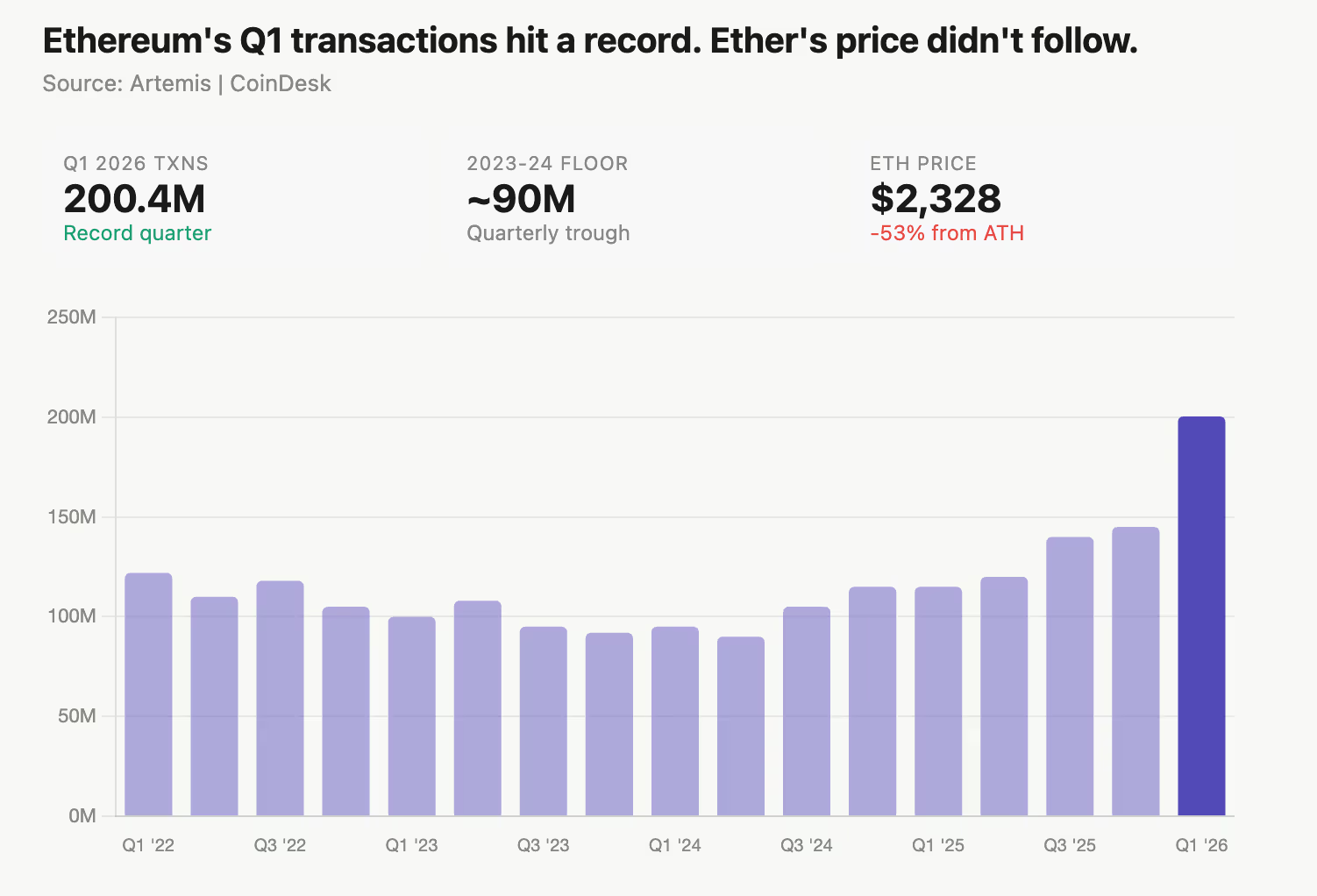

Ethereum had a record 200 million transaction in Q1. Here’s what it means for ether (ETH)

Ethereum, the world’s largest smart contract blockchain, just printed its busiest quarter ever, and the token’s price hasn’t budged.

The network processed 200.4 million transactions on its base layer in Q1 2026, marking the first time it has crossed that threshold in a single quarter, according to Artemis data. Quarterly transaction count bottomed near 90 million in 2023, then spent most of 2024 grinding sideways between 100 million and 120 million.

The Ethereum smart contract blockchain is a decentralized system that can automatically execute agreements without the need for a bank, lawyer, or middleman. Transactions on Ethereum are records of actions, such as sending native token ether (ETH), interacting with smart contracts, or transferring tokens, that are securely processed and imprinted on the blockchain.

Layer 2s and stablecoins lead the boom

The recovery in Ethereum’s on-chain activity began in mid-2025, with each successive quarter seeing higher activity than the last. This led to Q1 2026, when activity jumped 43% from Q4 2025’s 145 million, marking a clear U-shaped growth from the 2023 bottom.

Still, Ethereum’s native token ether is down over 50% from its August 2025 high of nearly $5,000. It traded around $2,328 as of Friday morning. This divergence may present an opportunity for traders looking to capitalize on fundamental growth and statistics.

Most of the traffic lives on Layer 2s, which are separate networks built on top of Ethereum that process transactions cheaply and then batch them down to the main chain for final settlement. Think of Layer 2s as extra packs attached to your bike, letting you carry more than you could on your own.

Base and Arbitrum are the two largest, where users interact with them for lower fees, and the activity shows up on Ethereum’s base layer as settlement and bridging.

Stablecoins, or tokenized versions of fiat currencies, are also being used heavily on Ethereum. According to Token Terminal, the total supply of stablecoins on Ethereum has reached a record $180 billion, according to Token Terminal, accounting for about 60% of the global stablecoin market.

Both trends push transaction counts higher on L1 through settlement and bridging activity, even when end users never directly touch the base layer.

The risk flagged by some analysts is that L2 activity masks base-layer fee pressure.

Ethereum earns less per transaction after the Dencun upgrade significantly reduced data costs for L2s, meaning more activity does not cleanly translate into more burn or more holder value.

The broader read is that Ethereum’s usage has completed the kind of multi-year recovery that typically precedes price movement rather than trails it.

Whether this quarter marks an inflection or the top of a local cycle depends on whether the 200 million figure holds in Q2, and whether the growth continues to be driven by genuine onboarding rather than bot activity, which has increasingly dominated stablecoin transaction volume on-chain.

Cardano founder Charles Hoskinson has gone on record calling Bitcoin’s proposed quantum defense both technically mislabeled and functionally inadequate. The detail most outlets are missing: roughly 1.7 million BTC may be beyond saving, no matter what developers vote through. This is all happening when Bitcoin price prediction is getting bullish.

In a video posted to his YouTube channel late Wednesday, Hoskinson dissected BIP-361, the proposal from developer Jameson Lopp and others to phase out quantum-vulnerable Bitcoin addresses. He says that BIP-361 is being marketed as a soft fork but would functionally require a hard fork, since it invalidates existing signature schemes that active users currently rely on.

“To actually do this, you need a hard fork,” Hoskinson said flatly.

He called the soft fork characterization a lie. Bitcoin’s development culture has historically treated hard forks as violations of the network’s immutability, which makes the political fallout as significant as the technical one. The broader quantum security debate has been intensifying across the industry for months.

The deeper problem sits in the recovery mechanism. BIP-361 proposes that users with frozen quantum-vulnerable funds could reclaim them via a zero-knowledge proof tied to a BIP-39 seed phrase. According to Hoskinson, approximately 1.7 million BTC, including the estimated ~1 million coins attributed to Satoshi Nakamoto, predate BIP-39’s 2013 introduction entirely. No BIP-39 seed phrase exists for those wallets.

The zero-knowledge recovery path simply doesn’t apply. Satoshi’s coins, by this analysis, are structurally unrecoverable under the current proposal regardless of how the fork resolves.

Discover: The best crypto to diversify your portfolio with

Bitcoin Price Prediction: Fork or no Fork, $250,000 the Target

Hoskinson’s skepticism about Bitcoin’s protocol governance hasn’t dampened his price outlook. He publicly predicted BTC reaches $250,000 by mid-2026, a 3X from current levels, citing institutional inflows, Magnificent 7 tech integration, the incoming Clarity Act, and sustained end-user growth as primary drivers. He reiterated the forecast in a Bloomberg interview at TOKEN2049 Singapore.

— Coin Bureau (@coinbureau) November 23, 2025

HOSKINSON PUSHES HIS $250K BITCOIN TARGET TO LATE 2026.

HOSKINSON PUSHES HIS $250K BITCOIN TARGET TO LATE 2026.

After calling for $250,000 $BTC by end-2025 in April and then moving it to mid-2026 in October, he now expects it to happen by the end of 2026. pic.twitter.com/uyCKexxoKF

Technically, Bitcoin’s current position at just under $74,000 reflects a meaningful recovery from the sub-$66,000 low due to the fear of an Iran war. Early this month, the peak stood at $73,000; BTC has now cleared that level convincingly. Analyst consensus has been steadily repricing upward as macro headwinds ease.

The quantum debate is a wildcard that existing price models don’t price cleanly. If BIP-361 stalls, or forces a hard fork, short-term volatility is the near-certain outcome.

Discover: The best pre-launch token sales

Bitcoin is Getting Forked, Hyper is Here to Fix

Bitcoin’s limitations are precisely what’s fueling conviction in the layer-2 thesis right now. To be back to $120,000+ high, BTC’s upside requires institutional scale, an asymmetric early-stage return that individual traders once found in spot BTC is largely gone.

Bitcoin Hyper ($HYPER) is positioning directly inside that gap. It’s the first Bitcoin Layer 2 integrating the Solana Virtual Machine (SVM), delivering faster smart contract execution than Solana itself while preserving Bitcoin’s underlying security.

The project has raised $32 million at a current presale price of $0.0136, with a high 36% APY staking already live. Key infrastructure includes a Decentralized Canonical Bridge for BTC transfers and extremely low-latency transaction processing, addressing Bitcoin’s three core bottlenecks simultaneously: slow speed, high fees, and zero programmability.

The presale has been gaining traction precisely as the Bitcoin protocol debate raises questions about the base layer’s adaptability.

Research Bitcoin Hyper before the current price tier closes.

The post Bitcoin Price Prediction: Cardano Hoskinson Says BTC Fix Can’t Save Satoshi Bags appeared first on Cryptonews.

Alejandro Garnacho’s Chelsea desperation and Man United transfer intentions were clear

Gold ETFs deliver up to 61% returns since last Akshaya Tritiya. Should you hold or book profits after the rally?

Fake Ledger Device Sold Chinese Marketplace: Research

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

THE BIGGEST WIN OF MY LIFE! #gambling #casino #money #comedy #slots

BITCOIN & GOLD LIVE TRADING ANALYSIS @tradingmentor22 Live Trading || #goldtrading #cryptotrading

#reseller #gold #antique #buisness #jewelry #fyp #crazy #money #ytshorts

-

Politics7 days ago

Politics7 days agoUS brings back mandatory military draft registration

-

Sports7 days ago

Sports7 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Veronica Beard

-

Politics5 days ago

Politics5 days agoWorld Cup exit makes Italy enter crisis mode

-

Business6 days ago

Business6 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Crypto World4 days ago

Crypto World4 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Crypto World3 days ago

Crypto World3 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos2 days ago

News Videos2 days agoSecure crypto trading starts with an FIU-registered

-

NewsBeat4 days ago

NewsBeat4 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Business6 days ago

Business6 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Business7 days ago

Business7 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Crypto World6 days ago

Crypto World6 days agoFederal judge blocks Arizona from bringing criminal charges against Kalshi

-

NewsBeat3 days ago

NewsBeat3 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Crypto World3 days ago

Crypto World3 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

NewsBeat5 days ago

NewsBeat5 days agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Business6 days ago

Business6 days agoIMF retains floor for precautionary balances at SDR 20 billion

-

Business6 days ago

Business6 days agoFormer Liverpool CEO eviscerates FIFA for World Cup ticket pricing

-

Crypto World4 days ago

Sei Network Enters Quiet Reset Phase as On-Chain Metrics Signal a Slowdown in 2026

-

Business6 days ago

Coreweave CSO Venturo sells $5.5m in class a common stock

-

Sports6 days ago

1st-Round WR Enters Vikings Mock Draft Orbit

You must be logged in to post a comment Login