News Videos

DARKEST Moment in Crypto HAPPENING NOW!!

BIGGEST CRYPTO DUMP EVER HAPPENING NOW! (What Comes Next?)

✅ Bitunix (no kyc, $10,000 bonus): https://www.bitunix.com/register?vipCode=AltcoinDaily

⭐ Follow Altcoin Daily on 𝕏: https://twitter.com/AltcoinDaily

🟠 Become a channel member & get access to perks:

https://www.youtube.com/channel/UCbLhGKVY-bJPcawebgtNfbw/join

🎁 Altcoin Daily Merch: https://m046hz-bk.myshopify.com

🟡 50% deposit bonus on first $100 on WEEX: https://www.weex.com/events/welcome-event?vipCode=oz5p&qrType=activity

🟣 Best Crypto Exchange To Trade ($12,000 Bonus): https://www.coinw.com/en_US/register?r=ALTCOINDAILY

🔴 $30k USDT bonus with Phemex with our link: https://phemex.com/a/k/ALTCOINDAILY30

🔵 $30k bonuses with our link – Buy & Trade Crypto on Bybit: https://partner.bybit.com/b/altcoindaily

🟢 $8k bonus on Bitget Exchange with our link: https://bonus.bitget.com/AltcoinDaily

Altcoin Daily in Spanish: www.youtube.com/@AltcoinDailyenEspanol

Follow Altcoin Daily:

www.twitter.com/AltcoinDaily

www.instagram.com/thealtcoindaily/

Join Altcoin Daily on Telegram: https://t.me/AltcoinDailyANN

Hit Like, Share, and Subscribe for more daily cryptocurrency news

Altcoin Daily, the best cryptocurrency news media online!

Video by Aaron:

www.instagram.com/aarontarnold/

www.twitter.com/aarontarnold

For business inquires email: info.altcoindailyio@gmail.com

Timestamps:

0:00 – Darkest Day In Crypto Happening Now?

1:32 – Cardano Founder goes ALL IN

2:31 – Why is this happening?

3:55 – BIG NEWS

4:35 – Donald Trump steps in

5:48 – Coinbase CLO says Trump is helping

6:50 – Cathie Wood says “I would shift from gold to BTC”

8:43 – price predictions

9:55 – conclusion

**Note: My overall opinion is that the name of the game is to accumulate as much Bitcoin as possible. Alts are interesting but a lot more speculative. I use them to accumulate more Bitcoin & Ethereum.

***********************************************************************

🏺Support The Channel!!🏺(We Get A Kickback From Affiliate Links)

Protect and store your crypto with a Ledger Nano:

https://shop.ledger.com/?r=4b0f6c5711dc

Robinhood exchange has crypto & stocks:

https://join.robinhood.com/aarona-78df3a8

***********************************************************************

Altcoin Daily, the best cryptocurrency news media online!

#bitcoin #cryptocurrency #news #btc #ethereum #eth #cryptocurrency #litecoin #altcoin #altcoins #forex #money #best #trading #bitcoinmining #invest #trader #cryptocurrencies #top #investing #business #success #investment #finance #coinbase #binance #stocks #wallstreet #investor #wealth #bullish #crash #collapse #economy #cnbc #cryptolive #altcoindaily

***NOT FINANCIAL, LEGAL, OR TAX ADVICE! JUST OPINION! I AM NOT AN EXPERT! I DO NOT GUARANTEE A PARTICULAR OUTCOME I HAVE NO INSIDE KNOWLEDGE! YOU NEED TO DO YOUR OWN RESEARCH AND MAKE YOUR OWN DECISIONS! THIS IS JUST EDUCATION & ENTERTAINMENT! USE ALTCOIN DAILY AS A STARTING OFF POINT!

This is NOT an offer to buy or sell securities.

Investing and trading in cryptocurrencies is very risky, as anything can happen at any time.

This information is what was found publicly on the internet. This information could’ve been doctored or misrepresented by the internet. All information is meant for public awareness and is public domain. This information is not intended to slander, harm or defame any of the actors involved but to show what was said through their social media accounts. Please take this information and do your own research.

*The channel is not responsible for the performance of sponsors and affiliates.

Most of my crypto portfolio is Bitcoin, then Ethereum, but I hold many cryptocurrencies, possibly ones discussed in this video.

cryptocurrency, crypto, altcoin, altcoin daily, news, best investment, top altcoins, best crypto investment, ethereum, xrp, crash, crash, price, prediction, podcast, interview, finance, stock, investment, too late, bitcoin, cryptocurrency news, bitcoin news, cryptocurrency news media online, best crypto investments, 2026 prediction, should I buy ethereum?, blackrock, donald trump, coin bureau, binance, coinbase, trading crypto, trade, make money, cryptosrus, bitcoin today, bitcoin cnbc, altcoin news,

source

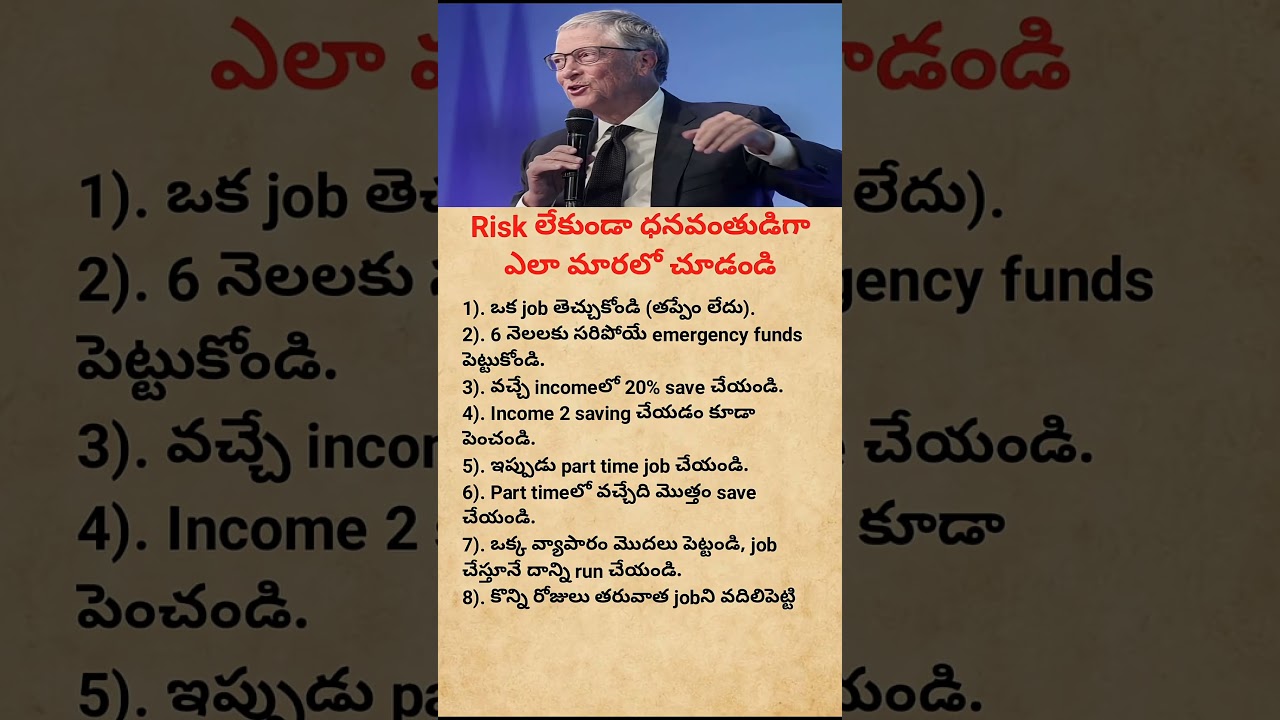

Financial Rules by Bill Gates That Can Change Your Life

In this video, we share powerful financial lessons inspired by Bill Gates.

These simple money rules teach you how to reduce risk, save smartly, build emergency funds, and create multiple income sources.

If you want financial stability and long-term success, this video is for you.

👉 Watch till the end for practical money advice that anyone can follow.

#BillGates

#FinancialFreedom

#MoneyManagement

#PersonalFinance

#WealthBuilding

#FinancialTips

#SuccessRules

#SmartSaving

#EmergencyFund

#MultipleIncome

#Motivation

#LifeLessons

#RichMindset

#FinancialEducation

#MoneyTips

source

🧠 My FREE Daily 5-Min Crypto Newsletter: https://www.cryptonutshell.com/subscribe

⮕ 🔒 Cold Storage Wallet: https://ledger.pxf.io/aOZEeQ

⮕ 💰 Get Up To $200 With Coinbase: https://coinbase-consumer.sjv.io/R59WLg

Markets are panicking. But underneath the fear, a very different story is playing out.

The VIX just surged past 26, oil is spiking, and Bitcoin whipsawed through the mid-$60,000s over the weekend. On the surface, it looks like chaos. But when you dig into the price action, the ETF flows, and the historical playbook for what happens when geopolitical conflict meets monetary policy, the picture snaps into focus. This isn’t a breakdown. It’s a position reset — and the setup forming right now could catch almost everyone offside.

In this video, we break down why markets are absorbing bad news instead of accelerating lower, what the Fed has done every single time the US has entered sustained Middle East conflict, and why BlackRock’s head of digital assets says the real source of Bitcoin’s volatility isn’t institutions — it’s leveraged perp platforms masking the strongest institutional base the asset has ever had.

Featuring insights from Tom Lee (Fundstrat), Arthur Hayes (Maelstrom / BitMEX), and Robbie Mitchnik (BlackRock Digital Assets).

Key insights from this episode:

– Why this correction has all the hallmarks of a position reset, not a market top

– The Fed’s historical response to every major US military conflict since 1990

– How $458 million flowed into Bitcoin ETFs on a single day with zero outflows across all 12 funds

– Why Bitcoin’s “leveraged NASDAQ” reputation is being driven by perp platforms, not fundamentals

– The 0.2% IBIT redemption figure that separates signal from noise

– What the asymmetry between short-term risk-off and medium-term liquidity expansion means for crypto

TIMESTAMPS

0:00 – Why this panic looks different

2:40 – Tom Lee on position resets and market bottoms

5:21 – The Fed’s Middle East war playbook

7:15 – Arthur Hayes on conflict, liquidity, and the Fed

9:56 – What the March FOMC meeting means for crypto

11:21 – Robbie Mitchnik on volatility, leverage, and institutional conviction

15:00 – The 0.2% redemption stat that changes everything

#Bitcoin #Crypto #ethereum

Crypto Investors are in SERIOUS Trouble (Tom Lee & BlackRock)

source

🚨 RIPPLE BOMBSHELL: Brad Garlinghouse Says XRP Investors Will Be “VERY HAPPY” By 2031 | Daily Crypto Briefing

In today’s Jungle Inc Crypto Daily Briefing (March 10, 2026), we break down 7 major stories shaking the crypto and institutional finance world — including Ripple’s bold 5-year utility roadmap, XRP leading Bitcoin in institutional inflows, Ripple securing an Australian financial license, Circle stock surging 49% YTD, CFTC Chair calling blockchain prediction markets “Truth Machines,” Bitcoin rebounding above $71K on geopolitical news, and Strategy Inc. dropping $1.3 BILLION on Bitcoin.

📌 KEY TOPICS COVERED

✅ Brad Garlinghouse says XRP investors will be “very happy” by 2031

✅ XRP leads ALL assets in 2026 institutional inflows — $123M vs Bitcoin’s $117M

✅ Ripple secures Australian Financial Services License (AFSL) via BC Payments acquisition — finalizing April 1, 2026

✅ RippleX SVP Markus Infanger outlines 3 priorities: Institutional DeFi, RWA tokenization ($2B), and full-stack financial integration

✅ Circle stock (CRCL) up 49% YTD — Bernstein sets $190 price target, 60% upside

✅ USDC circulation hits $78 billion — 25% of entire stablecoin market

✅ GENIUS Act fueling stablecoin institutional adoption

✅ CFTC Chair Michael Selig endorses blockchain prediction markets as superior to political polls

✅ Bitcoin rebounds to $71,785 — outperforming gold by 9% this month

✅ Strategy Inc. (formerly MicroStrategy) buys 17,994 BTC at ~$76K average

📊 TODAY’S MARKET SNAPSHOT (March 10, 2026)

XRP: $1.40 | +2.62% | $123M YTD institutional inflows

Bitcoin: $71,785 | +2.91% | +7% this month

Ethereum: $2,051 | +2.88% | $340M YTD outflows

Circle CRCL: $118.17 | +5.7% | +49% YTD

Crude Oil: $83.81 | Declining on peace signals

Gold: Down ~2% MTD — lagging Bitcoin as safe haven

🔍 TAGS & SEARCH TERMS

XRP news today, Ripple news today, Brad Garlinghouse interview 2026, XRP price prediction 2031, XRP institutional adoption, XRPL real world assets, RippleX 2026, Ripple Australia license, AFSL crypto, XRP vs Bitcoin inflows, Circle USDC stablecoin, CRCL stock 2026, GENIUS Act stablecoin regulation, CFTC prediction markets, Polymarket Kalshi regulation, Bitcoin price today, Bitcoin ETF inflows, Strategy MicroStrategy Bitcoin purchase, Michael Saylor Bitcoin 2026, crypto news today, XRP 2026, institutional crypto, Ripple ODL, Nostro Vostro XRP, crypto daily briefing, Jungle Inc Crypto

🌿 JUNGLE INC CRYPTO

Investigative crypto journalism at the intersection of institutional finance, regulatory intelligence, and digital assets.

🚀 JOIN THE JUNGLE INC COMMUNITY

The digital asset landscape is moving fast. Subscribe to stay updated on the institutional adoption of the XRP Ledger and the evolution of global liquidity.

🎯 PROFESSIONAL CRYPTO ANALYSIS

As an Enrolled Agent (EA) and dedicated content creator since 2018, I provide high-level analysis on the intersection of traditional finance and Web3. My coverage focuses on:

XRP & Ripple: Utility, legal developments, and global payment rails.

Layer 1 Infrastructure: Real-world asset (RWA) tokenization, DeFi, and scaling on Ethereum, Cardano, and Polkadot.

Macro Trends: Regulation, market cycles, and institutional capital flows.

⚠️ DISCLAIMER

This video contains news commentary and analysis intended for informational and educational purposes only. I am not a financial advisor. I am an Enrolled Agent, but the views expressed here are my personal opinions and do not constitute professional tax or investment advice. Cryptocurrency markets are highly volatile; always conduct your own research. Past performance is not indicative of future results.

📬 CONTACT & INQUIRIES

jungle@jungleincxrp.com

source

Hey Darlings 💛, if you’re enjoying Aspire, be sure to SUBSCRIBE HERE: https://www.youtube.com/@EmmaGrede?sub_confirmation=1

The truth is, most of us weren’t taught how to manage our money, we were taught not to talk about it.

From salary transparency and investing to honest discussions about debt and risk, women are left out of the conversation. Today’s guest, Tori Dunlap, is trying to change that. She’s built HerFirst $100K into a multi-million dollar education platform by helping women reshape their relationship with money and start building wealth.

In this conversation Emma and Tori get into the real reasons why so many women avoid looking at their bank accounts, how money narratives impact our decisions before we are even old enough to understand them and why waiting until you’re ready to invest is ultimately costing you your future.

Tori also speaks candidly about why she believes women in relationships should keep separate accounts, how the trad wife trend can be misleading and why getting rich isn’t something women should ever feel guilty about.

You’ll learn:

• Why “I’m bad at math” is keeping women broke

• What most of us get wrong about investing and how to do it right

• What today’s economic uncertainty actually means for your money

• Why financial education is the highest-return investment you can make

What’s your biggest money block right now? Drop it in the comments, we’d love to hear from you. And don’t forget to subscribe so you never miss an episode of Aspire with Emma Grede.

#aspirewithemmagrede #podcast #podcastinterview #finance #habits #interview #wealth #business #entrepreneur #entrepreneurship #businessadvice #financialfreedom #financialliteracy #skims #sharktank #psychology #motivation #attitude #money #success #successmindset #successmotivation #successtips #jobsearch #unemployed #financialfreedom #money #moneymindset #negotiation #interview #careergirlsguide #career #advice #interview #job #moneymanagement #moneytips #women #startup #womeninbusiness #womenempowerment #communicationskills #selfimprovement #communicationmastery

00:00:00 – Introduction

00:01:38 – Meet Tori Dunlap

00:02:43 – Why money is the most taboo topic

00:04:04 – Society views women in a specific box

00:05:50 – Shifting the conversation about money

00:09:15 – Money equals options and freedom

00:12:38 – Understanding your money story

00:17:20 – Women and financial shame

00:20:19 – The psychology of spending

00:25:25 – Ad Break

00:28:12 – How she saved $100K at 25

00:33:03 – From 100K to multi-millionaire

00:42:18 – Why women need to get rich

00:46:30 – Starting to invest: The basics

00:48:41 – Ad Break

00:51:07 – First steps to investing

00:56:20 – The emotion around money decisions

01:09:15 – Running a bootstrapped business

01:15:24 – Ad Break

01:19:18 – How running the company changed her

01:25:26 – The future of financial feminism

01:31:22 – Women unapologetically pursuing wealth

01:34:44 – Rapid Fire Questions

01:37:18 – What is something you aspire to?

_____

SUBSCRIBE

https://www.youtube.com/@EmmaGrede?sub_confirmation=1

_____

Buy Emma’s Book: START WITH YOURSELF is yours April 2026! Preorder today wherever you buy books or at https://www.emmagrede.com/

_____

ABOUT ASPIRE WITH EMMA GREDE

Build the life of your dreams and learn from the world’s most successful people.

Emma Grede, one of America’s richest self-made women, wants you to make the most of your life. On Aspire with Emma Grede, learn through thought-provoking conversations with some of the most successful and smartest minds on the planet, including goop founder Gwyneth Paltrow, investor, philanthropist, and former chair of Starbucks Mellody Hobson, podcast host Jay Shetty, billionaire entrepreneur and Shark Tank star Mark Cuban, global entrepreneur Charlotte Tilbury, Shopify President Harley Finkelstein, bestselling author of ‘Let Them Theory’ Mel Robbins, and public luminaries like Meghan, Duchess of Sussex, Charlamagne Tha God, Jessica Alba, former First Lady Michelle Obama, and Netflix Co-CEO Ted Sarandos. Each episode unpacks their habits, philosophy, and strategies, covering career advice, well-being, psychology, and, of course, how to win in business. The show offers personal stories, data-driven advice, real-world strategies, and the experience you need to turn your dreams into reality.

LISTEN TO ASPIRE WITH EMMA GREDE

link.pscrb.fm/f0281/Aspire_YT

ABOUT EMMA GREDE

Emma Grede is a founding partner and chief product officer of SKIMS and CEO of Good American. She also made history as the first Black woman to serve as an investor on Shark Tank. Learn more at: https://www.emmagrede.com/

source

GET IN EARLY! Crypto Is About To Wake Up!

⭐ Follow Altcoin Daily on 𝕏: https://twitter.com/AltcoinDaily

🟠 BTC Conference 2026 – ‘ALTCOINDAILY’ for 10% off Ticket: https://2026.b.tc

🟠 Become a channel member & get access to perks:

https://www.youtube.com/channel/UCbLhGKVY-bJPcawebgtNfbw/join

🎁 Altcoin Daily Merch: https://m046hz-bk.myshopify.com

🟡 50% deposit bonus on first $100 on WEEX: https://www.weex.com/events/welcome-event?vipCode=oz5p&qrType=activity

🟣 Best Crypto Exchange To Trade ($12,000 Bonus): https://www.coinw.com/en_US/register?r=ALTCOINDAILY

✅ Bitunix (no kyc, $10,000 bonus): https://www.bitunix.com/register?vipCode=AltcoinDaily

🔴 $30k USDT bonus with Phemex with our link: https://phemex.com/a/k/ALTCOINDAILY30

🔵 $30k bonuses with our link – Buy & Trade Crypto on Bybit: https://partner.bybit.com/b/altcoindaily

🟢 $8k bonus on Bitget Exchange with our link: https://bonus.bitget.com/AltcoinDaily

Altcoin Daily in Spanish: www.youtube.com/@AltcoinDailyenEspanol

Follow Altcoin Daily:

www.twitter.com/AltcoinDaily

www.instagram.com/thealtcoindaily/

Join Altcoin Daily on Telegram: https://t.me/AltcoinDailyANN

Hit Like, Share, and Subscribe for more daily cryptocurrency news

Altcoin Daily, the best cryptocurrency news media online!

Video by Aaron:

www.instagram.com/aarontarnold/

www.twitter.com/aarontarnold

For business inquires email: info.altcoindailyio@gmail.com

Timestamps:

0:00 – WHY you should buy Bitcoin now! (explained in 5 minutes)

5:00 – Ethereum to $80k? Why you should buy ETH

9:26 – Final thoughts

**Note: My overall opinion is that the name of the game is to accumulate as much Bitcoin as possible. Alts are interesting but a lot more speculative. I use them to accumulate more Bitcoin & Ethereum.

***********************************************************************

🏺Support The Channel!!🏺(We Get A Kickback From Affiliate Links)

Protect and store your crypto with a Ledger Nano:

https://shop.ledger.com/?r=4b0f6c5711dc

Robinhood exchange has crypto & stocks:

https://join.robinhood.com/aarona-78df3a8

***********************************************************************

Altcoin Daily, the best cryptocurrency news media online!

#bitcoin #cryptocurrency #news #btc #ethereum #eth #cryptocurrency #litecoin #altcoin #altcoins #forex #money #best #trading #bitcoinmining #invest #trader #cryptocurrencies #top #investing #business #success #investment #finance #coinbase #binance #stocks #wallstreet #investor #wealth #bullish #crash #collapse #economy #cnbc #cryptolive #altcoindaily

***NOT FINANCIAL, LEGAL, OR TAX ADVICE! JUST OPINION! I AM NOT AN EXPERT! I DO NOT GUARANTEE A PARTICULAR OUTCOME I HAVE NO INSIDE KNOWLEDGE! YOU NEED TO DO YOUR OWN RESEARCH AND MAKE YOUR OWN DECISIONS! THIS IS JUST EDUCATION & ENTERTAINMENT! USE ALTCOIN DAILY AS A STARTING OFF POINT!

This is NOT an offer to buy or sell securities.

Investing and trading in cryptocurrencies is very risky, as anything can happen at any time.

This information is what was found publicly on the internet. This information could’ve been doctored or misrepresented by the internet. All information is meant for public awareness and is public domain. This information is not intended to slander, harm or defame any of the actors involved but to show what was said through their social media accounts. Please take this information and do your own research.

*The channel is not responsible for the performance of sponsors and affiliates.

Most of my crypto portfolio is Bitcoin, then Ethereum, but I hold many cryptocurrencies, possibly ones discussed in this video.

cryptocurrency, crypto, altcoin, altcoin daily, news, best investment, top altcoins, best crypto investment, ethereum, xrp, crash, crash, price, prediction, podcast, interview, finance, stock, investment, too late, bitcoin, cryptocurrency news, bitcoin news, cryptocurrency news media online, best crypto investments, 2026 prediction, should I buy ethereum?, blackrock, donald trump, coin bureau, binance, coinbase, trading crypto, trade, make money, cryptosrus, bitcoin today, bitcoin cnbc, altcoin news,

source

![Bitcoin Has One Hurdle To Beat Before Going Higher! [Data]](https://wordupnews.com/wp-content/uploads/2026/03/1773233177_maxresdefault.jpg)

Despite rising geopolitical tensions and massive volatility in oil markets, Bitcoin continues to rally. In this episode, Ran breaks down the key data and market signals to answer the big question: can Bitcoin’s rally continue even as global uncertainty grows? We look at how Bitcoin is reacting to macro headlines and whether the momentum can push prices even higher or if a slowdown is ahead. Here’s what the data suggests for Bitcoin’s next move.

___________________________________________

𝗙𝗘𝗔𝗧𝗨𝗥𝗘𝗗 𝗢𝗡 𝗧𝗛𝗜𝗦 𝗦𝗛𝗢𝗪!

⬇⬇⬇⬇⬇⬇

🟥 𝗕𝗧𝗖𝗖 – 𝗚𝗲𝘁 𝗮 𝗛𝗨𝗚𝗘 𝟭𝟬% 𝗗𝗲𝗽𝗼𝘀𝗶𝘁 𝗕𝗼𝗻𝘂𝘀 & 𝗧𝗿𝗮𝗱𝗲 𝗢𝗶𝗹 𝗮𝗻𝗱 𝗠𝗼𝗿𝗲 𝘄𝗶𝘁𝗵 𝗬𝗼𝘂𝗿 𝗕𝗼𝗻𝘂𝘀!!!

👉 Exclusive to Banter! Sign up: https://bit.ly/btcc-ran

☑️ Get a 10% Bonus on any deposit over $500 USDT (up to $100K)!

☑️ Receive up to $10,000 in BONUSES!

☑️ No KYC or VPN required!

📺 𝗛𝗼𝘄 𝗧𝗼 𝗖𝗹𝗮𝗶𝗺 𝗬𝗼𝘂𝗿 𝗡𝗲𝘄 𝗨𝘀𝗲𝗿 𝗕𝗼𝗻𝘂𝘀: https://youtu.be/60fF4hojV44

_________

💰 𝗞𝗔𝗦𝗧 – 𝗣𝗮𝘆 𝘄𝗶𝘁𝗵 𝗬𝗼𝘂𝗿 𝗖𝗿𝘆𝗽𝘁𝗼 & 𝗘𝗮𝗿𝗻 𝘂𝗽 𝘁𝗼 𝟭𝟮% 𝗖𝗮𝘀𝗵𝗯𝗮𝗰𝗸!!

🎁 Sign up TODAY for a chance to WIN a Gold Card!

👉 Download App: https://go.kast.xyz/VqVO/132852K8

🐧 Bonus: Use code ICBB1NJFEE to Redeem a FREE Pengu Standard Card!

___________________________________________

𝗛𝗢𝗦𝗧 𝗖𝗛𝗔𝗡𝗡𝗘𝗟𝗦

⬇⬇⬇⬇⬇⬇

👉 𝗥𝗮𝗻 𝗼𝗻 𝗫: https://x.com/cryptomanran

👉 𝗥𝗮𝗻 𝗼𝗻 𝗜𝗻𝘀𝘁𝗮𝗴𝗿𝗮𝗺: https://bit.ly/ran-insta

___________________________________________

👁️🗨️ 𝗖𝗿𝘆𝗽𝘁𝗼 𝗕𝗮𝗻𝘁𝗲𝗿 𝗮𝗯𝗶𝗱𝗲 𝗯𝘆 𝘁𝗵𝗲 𝗳𝗼𝗹𝗹𝗼𝘄𝗶𝗻𝗴 𝗰𝗼𝗱𝗲 𝗼𝗳 𝗰𝗼𝗻𝗱𝘂𝗰𝘁:

https://www.cryptobanter.com/our-ethics/

We take our code of ethics very seriously and have engaged @zachxbt ( / zachxbt ) to monitor our progress. If you feel we’re not living up to it and have hard evidence please mail ZachXBT directly at reportcb@protonmail.com

⚠️ 𝗕𝗘𝗪𝗔𝗥𝗘 𝗢𝗙 𝗦𝗖𝗔𝗠𝗠𝗘𝗥𝗦 𝗜𝗡 𝗢𝗨𝗥 𝗖𝗢𝗠𝗠𝗘𝗡𝗧𝗦 𝗔𝗡𝗗 𝗖𝗢𝗠𝗠𝗨𝗡𝗜𝗧𝗬 𝗖𝗛𝗔𝗡𝗡𝗘𝗟𝗦

___________________________________________

📝 𝗗𝗶𝘀𝗰𝗹𝗮𝗶𝗺𝗲𝗿:

Crypto Banter is a social podcast for entertainment purposes only!

All opinions expressed by the hosts, guests and callers should not be construed as financial advice! Views expressed by guests and hosts do not reflect the views of the station. Listeners are encouraged to do their own research.

#Bitcoin #CryptoNews #OilPrice #ClarityAct #Ran

⏱ 𝗧𝗶𝗺𝗲𝘀𝘁𝗮𝗺𝗽𝘀:

00:00 Truth Behind War Headlines and Market Data

03:21 Trump’s Secret Strategy to Control Oil Prices

10:29 Iran Reveals The Only Way To End This War

13:00 Bitcoin Performance vs S&P 500 During War

14:15 Historical Data: Bitcoin Gains After Conflict Ends

16:21 Bitcoin Breaks 12-Year Dollar Correlation Pattern

17:23 Clarity Act Deadline: Crypto Regulation Update

19:58 The 2022 Simulation: Is a Crash Coming?

22:20 Crypto Card Giveaway and Trading Bonus

🎬 𝗪𝗮𝘁𝗰𝗵 𝗠𝗼𝗿𝗲 𝗖𝗿𝘆𝗽𝘁𝗼 𝗩𝗶𝗱𝗲𝗼𝘀: https://www.youtube.com/live/xZk1K2_vDjw?list=PLmOv2_vzOoGd_je37xsSrQD4WVpum0UDa&index=2

source

Bitmine is the largest Ethereum Treasury company, having stacked up more than 4.4 million ETH (so far). Driving this accumulation is company CEO Tom Lee, who’s basically Ethereum’s very own Michael Saylor. Lee has been hyper-bullish on Ethereum’s potential… but not everyone’s convinced.

A recent report by Culper Research reveals that Ethereum may be facing some serious issues, ironically caused by the Fusaka upgrade. That’s why they’re not only going short on Bitmine, but they’re bearish on Ethereum as a whole.

~~~~~

🛒 Get The Hottest Crypto Deals 👉 https://www.coinbureau.com/deals/

♣️ Join The Coin Bureau Club 👉 https://hub.coinbureau.com/

📱 Coin Bureau Telegram 👉 https://go.coinbureau.com/yt-telegram

💥 Coin Bureau Discord 👉 https://go.coinbureau.com/cb-discord

📲 Insider Info in our Socials 👉 https://www.coinbureau.com/socials/

🔥 TOP Crypto TIPS In our Newsletter 👉 https://www.coinbureau.com/newsletters/

💸 Coin Bureau Finance Channel 👉 https://www.youtube.com/@CoinBureauFinance

⭐ Coin Bureau Podcast Channel 👉 https://www.youtube.com/@coinbureaupodcast

📈 Coin Bureau Trading Channel 👉 https://www.youtube.com/@CoinBureauTrading

~~~~~

🔥OUR BRAND PARTNERS🔥

📈Bitget up to 50K USDT Deposit Bonus & GetAgent Plus Trial (Exclusive AI-powered Trading Assistant) 👉 https://go.coinbureau.com/bitget-getagent

📊Join Toobit for 100K USDT Bonus and 50% Lifetime Fee Discount 👉https://www.toobit.pro/t/coinbureau

~~~~~

📺Essential Videos📺

Ethereum Fusaka Explained 👉 https://youtu.be/biz2pd_DDIM

What If ETH Goes To Zero? 👉 https://youtu.be/8k5lK5Q96r0

Vitalik Selling 👉 https://youtu.be/PuX5B18EZvs

~~~~~

⛓️ 🔗 Useful Links 🔗 ⛓️

► Full Culper Research Report: https://culperresearch.com/wp-content/uploads/2026/03/Culper_ETH_3-5-2026.pdf

~~~~~

– TIMESTAMPS –

0:00 The Fusaka Upgrade & Fee Collapse

05:13 Ethereum’s New “Poison Transaction” Problem

08:32 Questionable Growth Metrics

12:44 Fusaka Broke ETH’s Tokenomics

17:50 What This Means For Ethereum

~~~~~

📜 Disclaimer 📜

The information contained herein is for informational purposes only. Nothing herein shall be construed to be financial, legal or tax advice. The content of this video is solely the opinions of the speaker who is not a licensed financial advisor or registered investment advisor. Trading cryptocurrencies poses considerable risk of loss. The speaker does not guarantee any particular outcome.

#ethereum #bitmine #eth #fusaka

source

When Narcissists Control Your Money | How to Recognize Financial Abuse

Are you living with a narcissist who controls every penny you spend? Learn how financial abuse works and why it’s so hard to break free.

In this video, we dive into the signs of narcissistic financial control, including how they monitor your spending, restrict access to money, and make even small purchases a struggle. If your partner or family member manipulates money to control you, you’re not alone — this is a common tactic in narcissistic abuse.

We’ll cover:

How narcissists use money to isolate and dominate

Examples of everyday financial manipulation

Steps you can take to regain control of your finances

Why financial independence is key to escaping abuse

If you’re struggling with a controlling narcissist, understanding these tactics can help you protect yourself and plan your escape. Don’t let someone else dictate your life through money.

💡 Watch our full financial series (link in description) to learn more strategies for breaking free from narcissistic control.

✅ Take action now: Subscribe for more tips on surviving narcissistic abuse, comment below if you’ve experienced financial manipulation, and share this video with someone who needs to see it.

#narcissists #financialabuse #narcissisticabuse #moneycontrol #EscapeNarcissist #victimtowarrior

source

![CAUTION: The Stage Is Set For Another Bitcoin Trap! [Probably Today]](https://wordupnews.com/wp-content/uploads/2026/03/1773230529_maxresdefault.jpg)

In today’s video Kyledoops outlines why the market looks like it’s setting things up for a major bull trap. Join live to find out why and what the catalyst would be for this to happen.

_____________________

𝗙𝗘𝗔𝗧𝗨𝗥𝗘𝗗 𝗢𝗡 𝗧𝗛𝗜𝗦 𝗦𝗛𝗢𝗪

⬇⬇⬇⬇⬇⬇

🟥 𝗕𝗧𝗖𝗖 – 𝗚𝗲𝘁 𝗮 𝗛𝗨𝗚𝗘 𝟭𝟬% 𝗗𝗲𝗽𝗼𝘀𝗶𝘁 𝗕𝗼𝗻𝘂𝘀 𝗨𝗽 𝘁𝗼 $𝟭𝟬,𝟬𝟬𝟬 & 𝗧𝗿𝗮𝗱𝗲 𝘄𝗶𝘁𝗵 𝗬𝗼𝘂𝗿 𝗕𝗼𝗻𝘂𝘀!!

👉 𝗡𝗼 𝗞𝗬𝗖! 𝗦𝗶𝗴𝗻 𝘂𝗽: https://bit.ly/btcc_welcome_deposit_bonus

📺 𝗛𝗼𝘄 𝗧𝗼 𝗖𝗹𝗮𝗶𝗺 𝗬𝗼𝘂𝗿 𝗡𝗲𝘄 𝗨𝘀𝗲𝗿 𝗕𝗼𝗻𝘂𝘀:https://youtu.be/tbvb7KCCbrU

🟩 𝗕𝗟𝗢𝗙𝗜𝗡 – 𝗚𝗲𝘁 𝗩𝗜𝗣𝟭 + 𝗨𝗽 𝘁𝗼 𝗮 $𝟭,𝟬𝟬𝟬 𝗕𝗼𝗻𝘂𝘀 + 𝗮 𝗖𝗵𝗮𝗻𝗰𝗲 𝘁𝗼 𝗪𝗜𝗡 𝟵,𝟰𝟬𝟬 𝗨𝗦𝗗𝗧!!

👉 𝗡𝗼 𝗞𝗬𝗖! 𝗦𝗶𝗴𝗻 𝘂𝗽: https://bit.ly/blofin_welcome

📺 𝗛𝗼𝘄 𝗧𝗼 𝗖𝗹𝗮𝗶𝗺 𝗬𝗼𝘂𝗿 𝗡𝗲𝘄 𝗨𝘀𝗲𝗿 𝗕𝗼𝗻𝘂𝘀: https://youtu.be/GK-8gEL8LVw

_____________________

𝗦𝗧𝗔𝗥𝗧 𝗧𝗥𝗔𝗗𝗜𝗡𝗚 𝗦𝗠𝗔𝗥𝗧𝗘𝗥!

⬇⬇⬇⬇⬇⬇

🐋 𝗪𝗛𝗔𝗟𝗘 𝗥𝗢𝗢𝗠 – 𝗠𝗮𝘀𝘁𝗲𝗿 𝘁𝗵𝗲 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗲𝘀 𝗼𝗳 𝗧𝗼𝗽 𝟭% 𝗧𝗿𝗮𝗱𝗲𝗿𝘀! 𝗟𝗲𝗮𝗿𝗻 𝘁𝗼 𝗧𝗿𝗮𝗱𝗲 𝗟𝗶𝗸𝗲 𝗮 𝗪𝗵𝗮𝗹𝗲!

👉 𝗕𝗲𝗮𝘁 𝘁𝗵𝗲 𝗛𝗲𝗿𝗱. 𝗝𝗼𝗶𝗻 𝘁𝗵𝗲 𝗪𝗵𝗮𝗹𝗲𝘀: https://bit.ly/Whale_Room_Kyle

💰 𝗪𝗛𝗔𝗟𝗘 𝗧𝗥𝗔𝗗𝗘𝗦 – 𝗧𝗵𝗲 𝗢𝗻𝗹𝘆 𝗗𝗮𝘁𝗮 𝗧𝗵𝗮𝘁 𝗠𝗮𝘁𝘁𝗲𝗿𝘀. 𝗔𝗹𝗹 𝗜𝗻 𝗢𝗻𝗲 𝗣𝗹𝗮𝗰𝗲! 𝟭𝟬𝟬% 𝗙𝗥𝗘𝗘!

👉 https://www.whaletrades.io/

_____________________

𝗧𝗥𝗔𝗗𝗘 𝗪𝗛𝗘𝗥𝗘 𝗞𝗬𝗟𝗘 𝗧𝗥𝗔𝗗𝗘𝗦!

⬇⬇⬇⬇⬇⬇

🟨 𝗕𝗬𝗕𝗜𝗧 – 𝗚𝗿𝗮𝗯 𝗮 $𝟱𝟬 𝗦𝗶𝗴𝗻-𝗨𝗽 𝗕𝗼𝗻𝘂𝘀 + 𝗘𝗮𝗿𝗻 𝘂𝗽 𝘁𝗼 $𝟯𝟬,𝟬𝟬𝟬 𝗶𝗻 𝗗𝗲𝗽𝗼𝘀𝗶𝘁 𝗕𝗼𝗻𝘂𝘀𝗲𝘀!!

👉 𝗦𝗶𝗴𝗻 𝘂𝗽: https://bit.ly/bybit-kyledoops

🟧 𝗣𝗜𝗢𝗡𝗘𝗫 – 𝗦𝗶𝗴𝗻 𝗨𝗽 𝗮𝗻𝗱 𝗧𝗿𝗮𝗱𝗲 𝘁𝗼 𝗨𝗻𝗹𝗼𝗰𝗸 𝗮 $𝟭𝟬𝟬 𝗕𝗼𝗻𝘂𝘀 𝗮𝗻𝗱 𝗘𝗮𝗿𝗻 𝘂𝗽 𝘁𝗼 𝟭,𝟬𝟬𝟬 𝗨𝗦𝗗𝗧!!

👉 𝗝𝗼𝗶𝗻 𝗡𝗼𝘄: https://bit.ly/Pionex_KyleDoops

🤖 𝗖𝗼𝗽𝘆 𝗞𝘆𝗹𝗲’𝘀 𝘀𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗲𝘀: https://bit.ly/Copy_Kyle

⬛️ 𝗚𝗥𝗩𝗧 – 𝗧𝗿𝗮𝗱𝗲 𝘄𝗶𝘁𝗵 𝗦𝗽𝗲𝗲𝗱 𝗮𝗻𝗱 𝗣𝗿𝗶𝘃𝗮𝗰𝘆!!

☑️ Earn 10% interest on your total trading account balance!

👉 𝗝𝗼𝗶𝗻 𝗻𝗼𝘄: https://bit.ly/grvt-kyle

🟪 𝗕𝗜𝗧𝗙𝗨𝗡𝗗𝗘𝗗 – 𝗣𝘂𝗿𝗰𝗵𝗮𝘀𝗲 𝗔𝗻𝘆 𝗖𝗵𝗮𝗹𝗹𝗲𝗻𝗴𝗲 𝘁𝗼 𝗨𝗻𝗹𝗼𝗰𝗸 𝗔𝗰𝗰𝗲𝘀𝘀 𝘁𝗼 𝗕𝗶𝗴𝗴𝗲𝗿 𝗧𝗿𝗮𝗱𝗶𝗻𝗴 𝗙𝘂𝗻𝗱𝘀!!

👉 𝗦𝗶𝗴𝗻 𝘂𝗽: https://bit.ly/join-bitfunded-kyle

_____________________

🛡️ 𝗡𝗢𝗥𝗗 𝗩𝗣𝗡 – 𝗕𝗲 𝗨𝗻𝗵𝗮𝗰𝗸𝗮𝗯𝗹𝗲! 𝗞𝗲𝗲𝗽 𝗬𝗼𝘂𝗿 𝗖𝗿𝘆𝗽𝘁𝗼 & 𝗜𝗱𝗲𝗻𝘁𝗶𝘁𝘆 𝗦𝗮𝗳𝗲!

🚨 Get Up to 74% Off + 4 Extra Months FREE!

👉 𝗘𝗫𝗖𝗟𝗨𝗦𝗜𝗩𝗘 𝗢𝗳𝗳𝗲𝗿: https://nordvpn.com/kyledoops

_____________________

𝗙𝗢𝗟𝗟𝗢𝗪 𝗞𝗬𝗟𝗘!

⬇⬇⬇⬇⬇⬇

👉 𝗫: https://x.com/kyledoops

👉 𝗜𝗻𝘀𝘁𝗮𝗴𝗿𝗮𝗺: https://bit.ly/kyle-insta

_____________________

👁️🗨️ 𝗖𝗿𝘆𝗽𝘁𝗼 𝗕𝗮𝗻𝘁𝗲𝗿 𝗮𝗯𝗶𝗱𝗲 𝗯𝘆 𝘁𝗵𝗲 𝗳𝗼𝗹𝗹𝗼𝘄𝗶𝗻𝗴 𝗰𝗼𝗱𝗲 𝗼𝗳 𝗰𝗼𝗻𝗱𝘂𝗰𝘁:

https://www.cryptobanter.com/our-ethics/

We take our code of ethics very seriously and have engaged @zachxbt ( / zachxbt ) to monitor our progress. If you feel we’re not living up to it and have hard evidence please mail ZachXBT directly at reportcb@protonmail.com (mailto:reportcb@protonmail.com)

⚠️ 𝗕𝗘𝗪𝗔𝗥𝗘 𝗢𝗙 𝗦𝗖𝗔𝗠𝗠𝗘𝗥𝗦 𝗜𝗡 𝗢𝗨𝗥 𝗖𝗢𝗠𝗠𝗘𝗡𝗧𝗦 𝗔𝗡𝗗 𝗖𝗢𝗠𝗠𝗨𝗡𝗜𝗧𝗬 𝗖𝗛𝗔𝗡𝗡𝗘𝗟𝗦

___________________________________________

Crypto Banter is a live-streaming channel that brings you the hottest crypto news, market updates, and fundamentals of digital assets. Join the fastest-growing crypto trading community to get notified on the most profitable trades and the latest crypto market updates & news!!

📝 𝗗𝗶𝘀𝗰𝗹𝗮𝗶𝗺𝗲𝗿:

Crypto Banter is a social podcast for entertainment purposes only.

All opinions expressed by the hosts, guests, and callers should not be construed as financial advice. Views expressed by guests and hosts do not reflect the views of the station. Listeners are encouraged to do their own research.

#CryptoMarket #BitcoinPrice #CryptoTrading #Kyle

___________________________________________

⏱ 𝗧𝗶𝗺𝗲𝘀𝘁𝗮𝗺𝗽𝘀:

00:00 Stage Set for a Bitcoin Bull Trap?

00:48 Stock Market Update – S&P 500, QQQ, DJI, BCO, OIL During Strait of Hormuz Closure

08:33 Gold Analysis Today – XAU

09:41 Dollar Index Analysis Today – DXY

11:57 Crypto Market Update – Bitcoin Sentiment, Funding Rates, ETF Inflows, Daily Exchange Volume

12:45 Total Crypto Market Cap Analysis

14:55 USDT Dominance Analysis – USDT.D

17:26 Bitcoin Analysis Today – BTC Resistance Ahead

🎬 𝗠𝗼𝗿𝗲 𝗩𝗶𝗱𝗲𝗼𝘀 𝘄𝗶𝘁𝗵 𝗞𝘆𝗹𝗲 𝗗𝗼𝗼𝗽𝘀:

source

Gold Price Analysis: How Iran Conflict and Surging Oil Keep Precious Metal Above $5,000

Smear campaigns using social media to criminalise Guatemala activists

Syracuse fires coach Adrian Autry after three unsuccessful seasons

-

Business5 days ago

Form 8K Entergy Mississippi LLC For: 6 March

-

Tech6 days ago

Tech6 days agoBitwarden adds support for passkey login on Windows 11

-

News Videos2 days ago

News Videos2 days ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Ann Taylor

-

Crypto World2 days ago

Crypto World2 days agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Tech8 hours ago

Tech8 hours agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

Sports6 days ago

Sports6 days ago499 runs and 34 sixes later, India beat England to enter T20 World Cup final | Cricket News

-

Politics5 days ago

Politics5 days agoTop Mamdani aide takes progressive project to the UK

-

Sports4 days ago

Sports4 days agoThree share 2-shot lead entering final round in Hong Kong

-

Sports3 days ago

Sports3 days agoBraveheart Lakshya downs Lai in epic battle to enter All England Open final | Other Sports News

-

Business23 hours ago

Business23 hours agoExxonMobil seeks to move corporate registration from New Jersey to Texas

-

Entertainment5 days ago

Entertainment5 days agoHailey Bieber Poses For Sexy Selfies In New Luscious Lip Thirst Traps

-

NewsBeat6 days ago

NewsBeat6 days agoPiccadilly Circus just unveiled ‘London’s newest tourist attraction’ and it only costs 80p to enter

-

Business3 days ago

Business3 days agoSearch for Nancy Guthrie Enters 37th Day as FBI Probes Wi-Fi Jammer Theory

-

Business7 hours ago

Business7 hours agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

NewsBeat2 days ago

NewsBeat2 days agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Tech2 days ago

Tech2 days agoDespite challenges, Ireland sixth in EU for board gender diversity

-

Entertainment7 days ago

Harry Styles Has ‘Struggled’ to Discuss Liam Payne’s Death

-

Crypto World7 days ago

Crypto World7 days agoNew Crypto Mutuum Finance (MUTM) Reports V1 Protocol Progress as Roadmap Enters Phase 3

-

Tech6 days ago

Tech6 days agoACIP To Discuss COVID ‘Vaccine Injuries’ Next Month, Despite That Not Being In Its Purview