Crypto World

Europe’s role in the next wave of tokenisation

Welcome to our institutional newsletter, Crypto Long & Short. This week:

- Lukas Enzersdorfer-Konrad on how the EU’s regulatory clarity could allow tokenised markets to scale

- Andy Baehr tells BNB to “suit up”

- Top headlines institutions should pay attention to by Francisco Rodrigues

- “Bitcoin’s drawdowns compress as markets mature” in Chart of the Week

Expert Insights

Europe’s role in the next wave of tokenisation

– By Lukas Enzersdorfer-Konrad, chief executive officer, Bitpanda

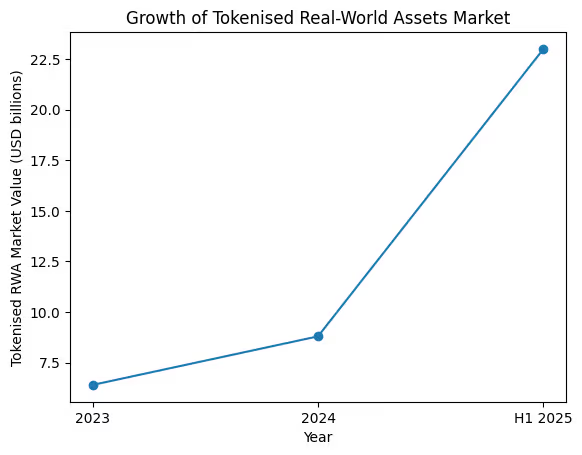

The tokenisation of real-world assets (RWAs) has moved from buzzword to business case. It has become the bedrock of institutional blockchain adoption. In the first half of 2025 alone, the value of tokenised RWAs surged by 260%, reaching $23 billion in on-chain value. Over the past several years, the sector has experienced rapid and sustained growth, enough to shift tokenisation from an experimental concept to a core pillar of digital-asset infrastructure. This signals a structural shift in how financial markets are built and ultimately expanded.

Tokenisation is emerging as the foundation of institutional blockchain adoption with BlackRock, JPMorgan and Goldman Sachs having publicly explored or deployed related initiatives and major institutions validating its potential. Despite this momentum, growth remains constrained. Most assets are still embedded in permissioned systems, segmented by regulatory uncertainty and limited interoperability. Scalable public-network infrastructure remains underdeveloped, slowing the path from institutional pilots to mass-market participation. In short, tokenisation works, but the market rails to support global adoption are still being built.

What’s missing? Regulation, as an enabler. Institutions need clarity before committing to balance sheets and building long-term strategies. Retail investors need transparent rules that protect them without shutting them out. Markets need standards they can trust. Without these elements, liquidity stays shallow, systems stay siloed and innovation struggles to move beyond early adopters.

Europe has undoubtedly emerged as an early leader in this area. With MiCA now in force and the DLT Pilot Regime enabling structured digital-securities experimentation, the region has moved beyond fragmented sandboxes. The European market is the first to implement a unified, continent-wide regulatory framework for tokenised assets. Instead of treating compliance as an obstacle, the region has elevated regulatory clarity into a competitive advantage. It provides the legal, operational and technical certainty that institutions require to innovate with confidence and at scale.

The continent’s regulatory-first approach is already generating tangible momentum. Under MiCA and the EU’s DLT Pilot Regime, banks have begun issuing tokenised bonds on regulated infrastructure, with European issuance exceeding €1.5 billion in 2024 alone. Asset managers are testing on-chain fund structures designed for retail distribution, while fintechs are integrating digital-asset rails directly into licensed platforms. Together, these developments mark a shift from pilot programmes to live deployment, reducing one of the industry’s longest-standing bottlenecks: the ability to build compliant infrastructure from day one.

A new phase: interoperability and market structure

The next frontier of tokenisation will hinge on interoperability and shared standards, areas where Europe’s regulatory clarity could again set the pace. As more institutions bring tokenised products to market, fragmented liquidity pools and proprietary frameworks risk recreating the silos of traditional finance in digital form.

While traditional finance has spent years optimising for speed, the next wave of tokenisation will be shaped by trust in who builds and governs the infrastructure, as well as whether both institutions and retail participants can rely on it. Europe’s clarity around rules and market structure gives it a credible opportunity to define global standards rather than simply follow them.

The EU can reinforce this position by encouraging cross-chain interoperability and common disclosure standards. Establishing shared rules early would allow tokenised markets to scale without repeating the fragmentation that slowed earlier financial innovations.

Headlines of the Week

– By Francisco Rodrigues

President Donald Trump’s surprise nomination of Kevin Warsh to lead the Fed introduced new variables that shook the markets. The precious metals rally saw a violent selloff, while cryptocurrency prices endured a major correction, with major players nevertheless moving to capture value.

Vibe Check

Suit up, BNB

– By Andy Baehr, head of product and research, CoinDesk Indices

Last week’s CoinDesk 20 (CD20) reconstitution brought BNB into the index for the first time. This wasn’t a question of size — BNB has long been one of the largest digital assets by market cap. It was a matter of meeting the liquidity and other requirements that govern CD20 inclusion. For the first time, BNB cleared those hurdles.

The result? One of the largest composition changes since the index launched in January 2024. BNB enters the CD20 with a weight exceeding 15%, making it an immediate heavyweight in the lineup.

From a portfolio construction perspective, this is a meaningful shift. BNB has historically exhibited lower volatility than the broader CD20, which could reduce the index’s overall risk profile. Its correlation with other index constituents has been moderate rather than lockstep (until recently, at least), adding a diversification benefit. The potential outcome: a lower-risk, more diversified index.

Of course, adding a big name means pushing other constituents down the weight ladder, even with the capping mechanisms CD20 employs. The pie charts tell that story clearly — existing holdings get compressed to make room for the new arrival.

As crypto enters what we’ve been calling its “sophomore year” of institutional maturity, the CoinDesk 20 is beginning its own third year of existence. The index evolves alongside the market it’s meant to capture.

Sunday scaries (real or imagined?)

This past weekend felt rough. Bitcoin traded below $75K, billions in liquidations got clocked, and if you’re in crypto, you were probably watching it happen in real time. Whether you count 24/7 market access as a blessing or a curse, it’s simply a fact of life now.

After a few weekends like this one, it starts to feel like a pattern — like crypto absorbs the world’s anxieties while traditional markets sleep. So, we decided to test that feeling against the data.

The scatter plot shows daily returns for the CoinDesk 20, with weekend moves highlighted separately. Yes, there are a few instances of outsized downside moves on Saturdays and Sundays. But there are plenty of quiet weekends too — and plenty of weekday chaos that doesn’t fit the narrative.

It may be memory inflation. Painful weekends stick in our minds more than calm ones. The drama of watching markets move when others aren’t paying attention amplifies the psychological weight. The data suggests that Sunday scaries might be more perception than pattern.

Still, after a weekend like this past one, the feeling is real even if the statistical significance isn’t. We keep on indexin’ through it all — tracking what’s happening, measuring what matters and trying to separate signal from sentiment.

Chart of the Week

Bitcoin’s drawdowns compress as markets mature

Bitcoin’s peak-to-trough drawdowns have steadily compressed over time, moving from -84% in the first epoch (post-1st halving) to a current cycle maximum of -38% as of early 2026. This persistent reduction in “peak pain” suggests a structural shift toward market maturity, as institutional capital and spot ETFs establish a more stable price floor compared to the retail-driven 80%+ crashes of previous eras. Historically, bitcoin has taken approximately 2 to 3 years (roughly 700 to 1,000 days) to fully recover from major cycle bottoms to new highs, though recovery speed has recently increased, with Epoch 3 reclaiming its peak in only 469 days.

Listen. Read. Watch. Engage.

Looking for more? Receive the latest crypto news from coindesk.com and explore our robust Data & Indices offerings by visiting coindesk.com/institutions.

The U.S. Securities and Exchange Commission is advancing its framework to reinterpret how federal securities laws apply to crypto assets, moving two proposed rules to the White House for review. The centerpiece is an interpretive notice that could narrow the jurisdiction of federal securities laws over many digital assets, signaling a potential regulatory shift while the White House weighs the plan.

Regulatory records show the SEC submitted the two proposals to the Office of Management and Budget for review on a recent Friday, with one item explicitly detailing which digital assets the agency might deem securities under federal law. As of Monday, the record listed the package as “pending review” by the White House, a status that could influence both enforcement and regulatory posture depending on the administration’s assessment.

Key takeaways

- The SEC forwarded two proposed rules to the White House Office of Management and Budget, including an interpretive notice on what digital assets could be securities.

- Chair Jay (Paul) Atkins signaled last week that the agency would not treat four asset classes as securities: digital commodities, digital tools, digital collectibles (NFTs), and stablecoins, while offering a cohesive token taxonomy for these types.

- The interpretive framework aims to clarify when a “non-security crypto asset” might qualify as an investment contract, providing regulatory guidance ahead of any potential congressional action.

- The move follows a memorandum of understanding with the CFTC, underscoring growing cross-agency coordination as lawmakers consider a broader market-structure bill for digital assets.

SEC interpretive move and what it could mean for crypto regulation

The SEC’s latest step appears to aim at providing a more coherent framework for determining when a crypto asset falls under securities laws. In a notice released last week, Chair Atkins indicated that digital commodities, digital tools, digital collectibles—including non-fungible tokens—and stablecoins would not be treated as securities under the agency’s purview. The interpretive notice is described as establishing a “coherent token taxonomy” for these asset classes and addressing how a non-security crypto asset may or may not be considered an investment contract under the Howey test.

If finalized, the interpretive rule could serve as a bridge to crypto regulation while Congress debates a more comprehensive market-structure bill to bring clear, unified rules to the sector. The AML-style approach would aim to reduce regulatory ambiguity and potentially recalibrate how exchanges, custodians, and developers operate in the interim. The policy aligns with the agency’s recent collaboration with the CFTC, highlighted by a Memorandum of Understanding signed earlier this month to clarify jurisdictional boundaries and regulatory expectations in the crypto markets.

Regulators and market participants have long sought a stable, forward-looking framework that reduces uncertainty around whether a given token is a security. The SEC’s proposed taxonomy is meant to outline how different digital asset types should be treated, and crucially, when assets may still be subject to investment contract analysis even if they fall outside the securities umbrella. The White House review stage is a critical gate: a positive outcome could accelerate regulatory alignment, while a protracted or revised review could push the timetable for broader legislative action.

Broader policy momentum: White House talks, stablecoins, and the CLARITY Act

Beyond the White House review, the crypto policy landscape continues to evolve at the congressional level. Politico reported on Friday that White House officials and lawmakers had reached an agreement in principle on some aspects of the crypto regime, including stablecoin yield considerations that could shape the market-structure bill’s trajectory in the Senate Banking Committee. However, the committee indefinitely postponed its markup of the bill in January after Coinbase CEO Brian Armstrong expressed public concerns about the legislation as written, underscoring the political sensitivity surrounding crypto regulation.

As of Monday, there had been no public announcement of a new date for the markup. Senate leadership outlined a workflow prioritizing other legislation, such as the SAVE America Act, before returning to bipartisan crypto debate. Senate Republicans and allies have signaled continued interest in a structured approach to digital assets, but the path remains contingent on both legislative negotiation and regulatory clarity from agencies like the SEC and the CFTC.

The ongoing discussions touch on the CLARITY Act, a proposed framework intended to clarify crypto markets and stablecoins under a market-structure agenda. The interagency dynamics—between the SEC’s jurisdictional interpretations, the CFTC’s role in cash and derivative markets, and congressional arbitration—will shape how quickly a final, enforceable regime can take effect, and what form it will take for issuers, exchanges, and users alike.

Investors and builders should watch two interlinked developments: the White House’s decision on the SEC’s interpretive rules and the progress (or stall) of the market-structure bill in Congress. While a regulatory pathway for many digital assets could reduce policy risk, it could also introduce new compliance obligations, particularly for entities operating in the cross-border or custody-heavy segments of the market. The tension between advancing a broad framework and accommodating industry concerns is likely to persist as lawmakers seek to balance investor protection with innovation.

As the regulatory clock ticks, participants should monitor the White House’s review timeline, the final content of the interpretive notice, and any updates to the market-structure bill’s language—especially provisions around stablecoins and collateral use. The next few weeks could reveal whether the administration’s review will accelerate clarity or reveal remaining ambiguities that require legislative refinement.

What remains uncertain is how quickly the White House completes its review and whether Congress will greenlight a comprehensive framework on digital assets in the near term. For market participants, the key question is whether the unfolding process will reduce regulatory surprise or introduce new interpretive wrinkles that alter how tokens are categorized and traded.

Readers should keep an eye on updates from RegInfo.gov and official agency notices, as well as any new statements from Senators and regulatory staff about the CLARITY Act and related crypto amendments. The evolving stance from the White House and Congress will continue to shape the baseline for crypto regulatory risk, guiding how exchanges structure listings, how issuers approach token design, and how traders price risk in a landscape that remains in flux.

Investors and industry watchers should stay tuned to forthcoming White House feedback on the SEC’s proposals, the pace of the Senate Banking Committee’s work, and further clarity on how the CFTC and SEC will coordinate enforcement and policy in the months ahead.

US Senators Adam Schiff and John Curtis are expected to introduce a bipartisan bill on Monday that would bar sports betting and “casino-style” contracts from prediction markets regulated by the Commodity Futures Trading Commission (CFTC), according to a Monday Wall Street Journal report.

“Too many young people in Utah are getting exposed to addictive sports betting and casino-style gaming contracts that belong under state control, not under federal regulators,” Senator Curtis, one of the bill’s co-sponsors, told the WSJ.

If introduced as reported, the measure would add to a widening Washington push against certain prediction market contracts. The report adds to the growing regulatory scrutiny over prediction markets, following renewed insider trading concerns sparked by the US-Israeli war with Iran.

On March 10, Schiff introduced the DEATH BETS Act, a bill seeking to prohibit CFTC-regulated prediction markets from listing contracts tied to war, terrorism, assassination and individual death.

Related: Prediction markets boom on Iran bets as Congress eyes ban

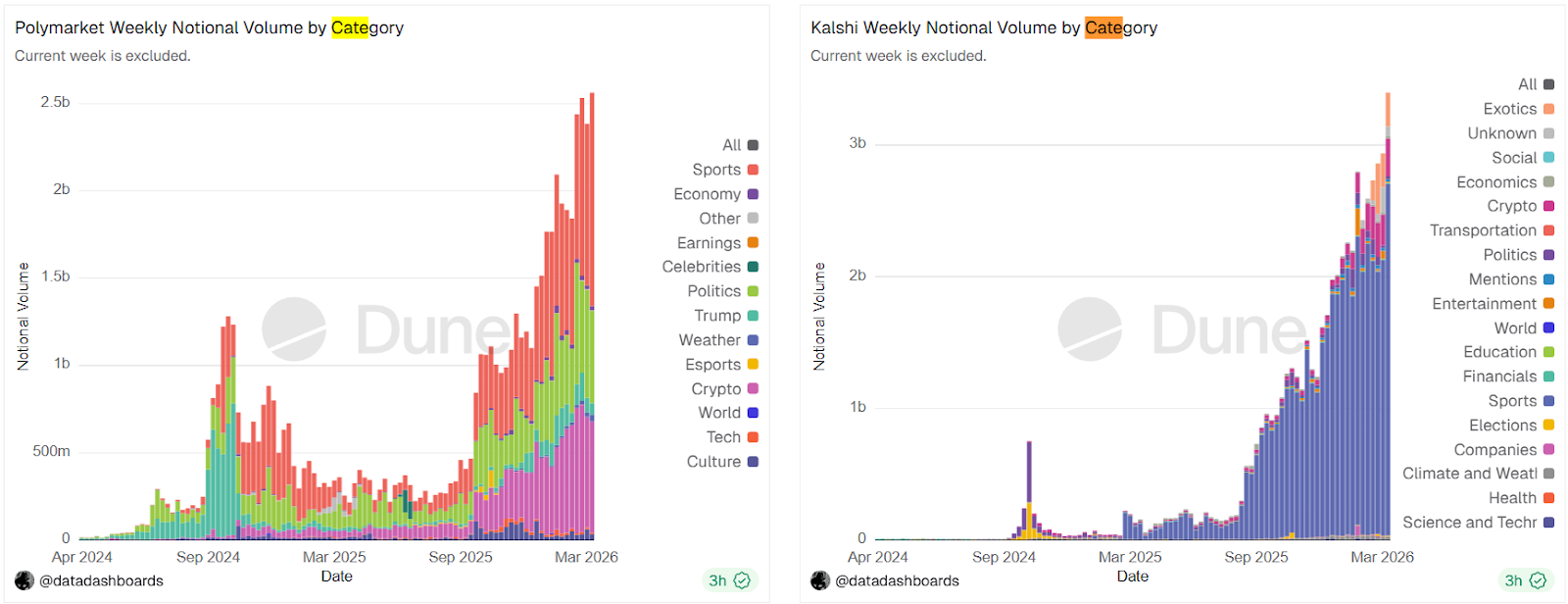

Sports markets drive trading volume

Sports betting is a leading source of trading activity on prediction market platforms. Sports-related contracts accounted for 47.7% of Polymarket’s weekly notional volume and 78.8% for Kalshi last week, according to Dune data.

Sports betting generated $1.2 billion in weekly notional trading volume for Polymarket and $2.6 billion for Kalshi.

State and federal lines blur

The regulatory pressure has also intensified outside Congress. On March 12, the CFTC issued a staff advisory classifying event contracts on prediction markets as a “financial asset class.”

The commodities regulator also submitted an Advanced Notice of Proposed Rulemaking, asking for public feedback on how the Commodity Exchange Act (CEA) would apply to prediction markets. Polymarket and Kalshi are regulated by the CFTC as Designated Contract Markets (DCM).

Related: Kalshi, Polymarket face trading halt in Nevada after court rulings

While CFTC Chair Michael Selig claimed the CFTC had “exclusive jurisdiction” over prediction markets, an Ohio judge tested that claim in a March 9 ruling, saying that Kalshi had failed to show the CEA “would necessarily preempt Ohio’s sports gambling laws,” or that these sports betting contracts would fall under the “exclusive jurisdiction” of the CFTC.

On Friday, a Nevada judge temporarily blocked Kalshi from offering sports, election and entertainment event contracts in the state for 14 days, finding regulators were reasonably likely to succeed in arguing the markets violated Nevada gambling law.

Cointelegraph approached the senators for comment and a copy of the draft bill.

Magazine: Inside a 30,000 phone bot farm stealing crypto airdrops from real users

Sunday’s $23 million hack of Resolv’s stablecoin USR has led to contagion across the DeFi sector.

Opportunistic traders used depegged USR to borrow against, draining liquidity in over a dozen yield vaults.

To make things worse, so-called “risk curators” then automatically allocated more funds to broken markets as lending rates spiked.

In November, a similar contagion hit DeFi’s “curated” vault ecosystem after Stream Finance announced a $93 million loss, leading to a 75% of xUSD.

Despite discussions of risk ratings and curators putting up first-loss capital in the aftermath, it appears not much was learned, after all.

Read more: Four months on, MEV Capital falls victim to $4B DeFi daisy chain implosion

The hack

Resolv Labs’ statement confirmed that a private key compromise led to the unauthorized (and unrestricted) “minting of approximately $80 million of uncollateralized USR.”

USR’s pre-hack token supply remains fully backed, with losses coming from liquidity providers (LPs) on decentralized exchanges as the hacker sold the minted tokens. For example, LPs on Curve Finance alone are estimated to have lost $17 million.

The hacker’s sell-off caused a depeg of USR, which is currently trading at $0.23, according to CoinMarketCap data. Blockchain security firm Beosin puts the attacker’s profits at 11,409 ether (ETH), worth over $23 million at the time of writing.

The Resolv team faced criticism for a slow response time while collecting the necessary multisig signatures to pause the protocol.

It has contacted the exploiter on-chain, requesting return of 90% of the converted ETH, as well as the remaining USR.

Read more: Venus Protocol hacker lost $4.7M after nine months of planning

The fallout

The hack may have been simple, but the knock-on effects have been anything but.

Depegged USR was pounced upon by opportunistic traders who used it to drain yield vaults with hardcoded price oracles. In buying cheap USR to use as collateral, users could borrow other assets, such as USDC, as if USR were still worth $1.

Read more: Oracle error adds to turmoil at DeFi giant Aave

As if things weren’t bad enough, “risk curators” automated strategies then allocated further funds to the affected markets, whose high utilization had spiked supply yields.

Chaos Labs’ Omer Goldberg explained how Morpho’s Public Allocator feature allowed curators “including Gauntlet, re7, kpk, and 9summits” to autoallocate millions of dollars worth of assets into markets “based on pre-configured and approved caps and credit lines.”

In some cases, Goldberg says, allocation into broken vaults continued for hours.

The chaos also brought innovation, however, as the auto-allocations were even specifically targeted to free up additional liquidity. Enterprising competitors Obsidian also capitalized on the incident, offering a migration service to users whose deposits are stuck in illiquid Morpho vaults

Assessing the damage

Morpho’s Paul Frambot tallied 15 affected vaults with over $10,000 of exposure to USR.

According to security researcher Weilin Li, curators of the affected vaults, on Morpho and elsewhere, include Gauntlet, Re7, MEV Capital, Extrafi, Seamless, August, Clearstar, kpk, Leyrock and 9Summits.

For those who followed November’s collapse, many of these names may be familiar.

Yearn, whose contributors were amongst the harshest critics of the yield vaults which led to November’s crash, suffered a minimal loss of $377.

Ironically (or tellingly), Resolv’s own risk manager, Steakhouse, wasn’t exposed to USR, despite stating that “operationally, Resolv demonstrates institutional rigor” just five days before the hack.

The backing of Inverse Finance’s DOLA stablecoin was indirectly exposed to the depeg of USR, with the team pledging to patch the $340,000 hole.

A number of lending markets paused USR markets, including Venus Protocol, which was itself hacked last weekend, and Lista.

Fluid was the worst hit, and may have accrued up to $17.5 million of bad debt. However, the team reassured users that it had “secured short-term loans to cover 100% of the bad debt.”

It also considers selling FLUID tokens “should any additional funds be required.”

Following a dicey few months for top dog lending protocol Aave, with governance drama and an oracle mishap, Aave Labs’ Stani Kulechov was keen to highlight Aave’s lack of exposure.

DeFi daisy chain

The web of platforms affected by the compromise of a single private key is a stark reminder of how one of DeFi’s key innovations, interoperability, is a double-edged sword.

Automated allocation may optimize returns under normal conditions, but when things break, which they often do in DeFi, unintended behavior follows.

Without their own funds in play, the current setup incentivises “malicious game theory pushing [curators] to seek more risk.”

This latest episode has renewed calls for curators to have skin in the game. One approach is tranching of deposits, with curators set to lose out first should their risk be improperly “curated.”

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Glider and Ondo Finance have introduced a platform to let retail investors build and automate custom portfolios of tokenized US stocks, offering direct exposure to equities without a brokerage account.

According to the announcement, the platform allows users to create personalized baskets of onchain stocks that track real-world assets, removing the need for wallets, gas fees or manual transaction management.

Glider co-founder and CEO Brian Huang told Cointelegraph that unlike traditional exchange-traded funds, which bundle assets into fixed products, the platform lets users construct index-like portfolios with custom weightings that are automatically maintained, avoiding reliance on pooled products.

The platform automatically executes and rebalances these portfolios, allowing users to gain exposure to tokenized equities without managing individual trades. The assets track underlying shares and can be traded beyond standard market hours.

Huang added that the model avoids the liquidity constraints that have limited earlier tokenized ETF offerings. He said:

“This is the first time direct indexing has been offered for onchain stocks… The problem that all ETFs have had on chain is liquidity. There’s no liquidity constraint on Glider because these are directly indexed. You hold the underlying assets and tap into their underlying liquidity.”

Tokenized stocks on Ondo’s platform are designed to mirror the price of their underlying shares and can be transferred and traded onchain, while Glider automates portfolio construction and rebalancing without requiring users to execute transactions manually.

The initial rollout will focus on tokenized US equities, with plans to expand into additional asset classes such as commodities, while also introducing features that allow users to lend positions and generate yield on their holdings.

A spokesperson for Ondo said the platform is not currently available to US users but said the company holds several SEC registrations, positioning it for a potential future launch in the United States.

Related: Binance adds Ondo’s tokenized stocks in latest RWA push

Tokenized stocks grow alongside evolution of crypto ETPs

Tokenized equities and crypto exchange-traded products (ETPs) have both expanded rapidly over the past year.

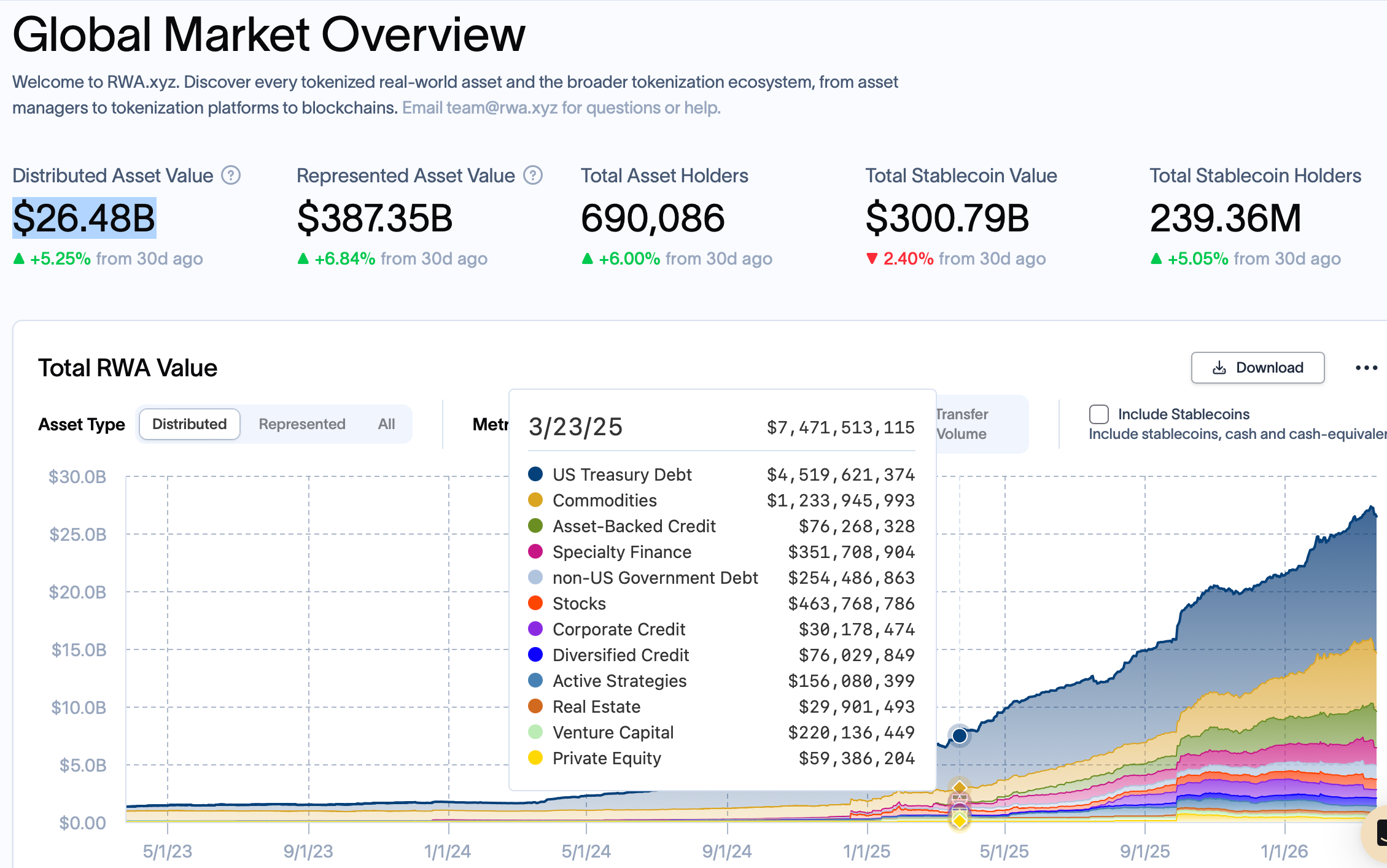

Data from RWA.xyz shows the total value of tokenized real-world assets (RWA) has grown sharply to around $26.5 billion, up from around $7.5 billion the same time last year. Among the RWAs onchain, around $908.5 million are tokenized stocks.

At the same time, crypto ETPs have moved beyond spot Bitcoin (BTC) and Ether (ETH) funds, with issuers increasingly exploring more complex and actively managed products.

In February, crypto ETP issuer 21Shares launched a new product offering European investors exposure to a preferred stock issued by Michael Saylor’s Strategy, the largest public holder of Bitcoin. The 21Shares Strategy Yield ETP is available to institutional and retail investors and offers a dividend linked to Strategy’s Bitcoin holdings.

21Shares president Duncan Moir told Cointelegraph the product improves access to Strategy’s STRC preferred stock, which is not widely available or easily cross-listed, while expanding distribution and liquidity through its ETP structure.

He added that the structure also simplifies tax treatment for European investors by handling reporting and withholding at the product level. Moir said:

It’s probably the product we’re seeing the most interest in across multiple regions. From the day we launched it, we’ve had more inbound inquiries to the sales team than for any crypto product, to be honest.

Earlier this month, BlackRock expanded its crypto lineup with a Nasdaq-listed product tied to Ethereum staking. The iShares Staked Ethereum Trust ETF (ETHB) provides spot Ether exposure while generating potential monthly income by staking a portion of its holdings.

However, BlackRock’s head of digital assets, Robert Mitchnick, said the asset management behemoth plans to remain cautious in expanding its crypto ETF offerings, despite growing interest in more complex structures.

Magazine: Big Questions: Can Bitcoin save you from the dreaded Cantillon Effect?

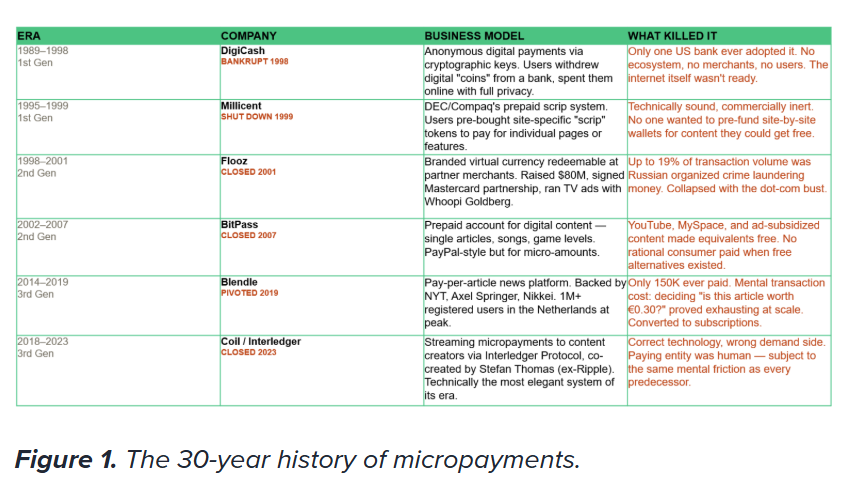

Stripe’s newly launched Machine Payments Protocol (MPP) could mark a turning point for micropayments — a long-promised but underutilized use case in crypto and beyond — as AI agents reshape how transactions are made.

That’s the key takeaway from newly published analysis by Forrester senior analyst Meng Liu, who argues that MPP may succeed where decades of earlier efforts failed.

Introduced earlier this month, MPP enables AI agents to execute transactions automatically, removing the need for human approval at each step. It is described as an open protocol for coordinating payments between AI agents and services. Liu frames this as a structural shift from human-initiated payments to machine-to-machine transactions.

Micropayments, which are typically small transactions worth a few cents or dollars, have long been seen as a way to monetize digital content, services and data, but have struggled to gain traction at scale.

A major barrier to adoption has been human behavior, including cumbersome digital checkout processes and reluctance to approve small charges, Liu said.

By contrast, AI agents executing payments as part of task completion, such as paying to access data or use online services, eliminate those constraints.

“Payment becomes a programmatic step, not a discrete decision,” Liu wrote. “There’s no checkout moment, no cart abandonment risk, and no mental transaction cost.”

Importantly, MPP is not a new settlement network. Instead, it acts as a coordination layer for automated payments, designed to work across existing infrastructure, including traditional rails, digital wallets and, where supported, crypto rails.

Related: AI agent payment volumes lower than reported, but adoption is growing: a16z

AI payments push extends beyond Stripe

Stripe is a payments company that has expanded into digital assets, including support for stablecoins, crypto on-ramps and blockchain-based payment tools. While MPP itself is not inherently blockchain-based, other companies are also developing infrastructure for AI-driven payments, particularly in areas such as micropayments and autonomous transactions.

One recent example is MoonPay, which released an open-source wallet standard designed for AI agents. The framework allows agents to hold, send and receive digital assets, enabling them to transact independently without human intervention.

Meanwhile, analysts at Bernstein believe AI agents could boost demand for stablecoins, as they are well-suited for handling frequent, low-value payments. Like Forrester’s Liu, Bernstein also pointed to Coinbase’s x402 protocol, which enables automatic internet payments between machines.

Related: Crypto Biz: Institutions aren’t waiting for the bottom

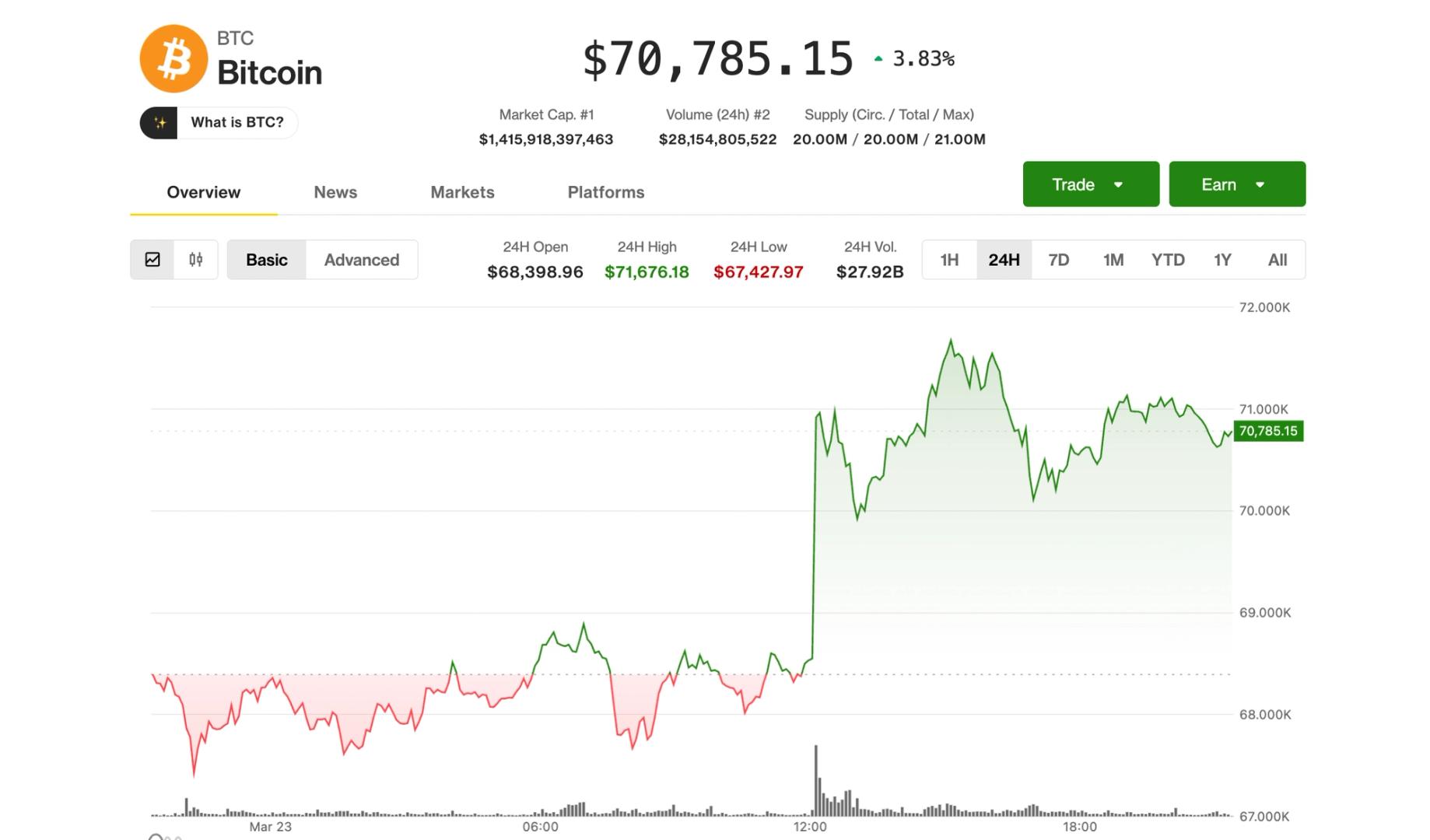

Bitcoin held onto gains Monday after an early surge above $70,000, but the rebound’s fate now hinges on what’s next between the U.S. and Iran.

The move followed U.S. President Donald Trump’s announcement of a five-day pause on strikes against Iranian energy infrastructure, citing “productive” diplomatic talks.

Iranian officials denied the existence of talks, but markets largely brushed it off, with risk assets holding firm through the session.

Bitcoin hovered just below $71,000 later in the session, up 3.8% over the past 24 hours. Altcoins outperformed, with ether (ETH), solana (SOL) and each gaining around 5%.

Crypto-linked equities also rallied, led by bitcoin miners, which have increasingly traded in line with AI infrastructure plays. Hut 8 (HUT) jumped more than 11%, while Bitfarms (BITF), Cipher Mining (CIFR), CleanSpark (CLSK), Riot Platforms (RIOT) and TeraWulf (WULF) advanced 6%-7%.

Traditional markets joined the move higher, with the S&P 500 and Nasdaq both closing about 1.2% up.

While the temporary pause has eased pressure in energy markets, traders should treat the rebound cautiously in risk assets.

“The macro ceiling has shifted,” said Jasper de Maere, OTC trader at Wintermute. “How much room opens up depends on the next five days.”

If oil stabilizes and shipping flows through the Strait of Hormuz normalize, he said, inflation concerns could ease, allowing rate-cut expectations to return and removing a key headwind for crypto.

In that scenario, bitcoin could make another run at the $74,000–$76,000 range, the level that has capped rallies in recent weeks, according to de Maere.

A breakdown in talks or renewed disruption to energy supply would have the opposite impact, he said. It would likely push oil higher again, reinforcing inflation risks and sending markets back into risk-off mode that could pull bitcoin back toward the mid-$60,000s.

The Russell 2000’s 2% rebound after a 10% correction signals a tentative risk‑on turn in U.S. stocks, giving Bitcoin and altcoins fresh “permission to breathe.

Summary

- The small-cap Russell 2000 index jumped about 2% after a bruising correction, signaling a tentative return of risk appetite in U.S. equities.

- Traders say the move is part of a broader “relief rally” that has also lifted high‑beta crypto and altcoins after weeks of macro and geopolitical stress.

- Rising stock–crypto correlation means small‑cap strength is increasingly viewed as a green light to rotate from cash into higher‑volatility tokens and perps.

The Russell 2000’s roughly 2% intraday surge comes just days after the index fell 10% from its recent peak and formally entered correction territory, capping a four‑week losing streak for U.S. stocks. U.S. small‑cap stocks staged a sharp rebound in New York on Monday as traders reassessed recession odds and war‑risk pricing, shifting from outright de‑risking toward a tentative risk‑on stance.

Analysts frame Monday’s bounce as a classic “risk‑on” rotation after weeks of selling tied to Middle East tensions and surging oil, with West Texas Intermediate futures having spiked toward $100 per barrel and Brent above $113 in recent sessions. “What you’re seeing is positioning, not euphoria,” one equity strategist said, arguing that investors who were underweight small caps are now “grudgingly adding beta back into the book” as worst‑case scenarios get priced out.

For crypto traders, the Russell’s move matters less as a stock story and more as a liquidity signal. Research highlighted by CME Group shows that in 2025 and into 2026, on days when U.S. stocks rise, “crypto assets tend to rise, but not by as much, and on days when U.S. tech stocks are selling off, crypto assets tend to fall by even more.” A recent macro explainer on crypto bitcoin rotation makes the same point more bluntly: “Most big crypto moves don’t start with a whitepaper. They start with a change in the cost of money and the price of risk.”

Correlation data backs that up. The 30‑day correlation coefficient between Bitcoin and the S&P 500 has climbed to about 0.74, its highest level this year, meaning the two now trade in close step as “an extension of broader risk sentiment.” When breadth improves in equities — first in mega‑caps, then small caps like the Russell 2000 — crypto often responds with its own breadth shift: dominance falls, majors and then mid‑caps start to participate, and liquid altcoins outperform long‑tail names.

Recent coverage has already documented how macro swings drive spillovers into digital assets, from early‑2025 fragility that pushed traders into Bitcoin (BTC) as a macro hedge alternative, to later phases where easing conditions triggered broad rallies across altcoins and crypto‑linked stocks. As one macro‑focused fund manager told crypto.news in an earlier note on rotation, “When small caps catch a bid and the dollar stops ripping, crypto finally gets permission to breathe.”

Solana (SOL) is trading in a suffocating consolidation zone, hovering just above the $90 price area, but could blast above $100 if our prediction comes true.

The technical setup is precarious; the asset is down nearly 69% from its January 2025 peak of $295.91, and DEX volumes have collapsed from $118 billion to just under $50billion in a single week, a staggering contraction of on-chain activity. While bulls point to the upcoming Alpenglow upgrade for sub-second finality, the immediate price action suggests exhaustion.

The market is holding its breath and bags around the critical $80 support level. A breakdown here completes a bearish head-and-shoulders pattern on the 3-day chart. On-chain data signals heightened risk, with capital appearing to rotate out of large caps into speculative volatility. As the Federal Reserve’s policy meeting looms, traders are forced to ask: Is this the bottom for SOL, or a rest stop on the way to $59?

Solana Price Prediction: Can it Hold or Will It Crash to $59?

The fierce defense of the $80 level defines the current market structure. Bears have tested this floor repeatedly, weakening the buy wall. Technical indicators paint a conflicted picture; the 14-day RSI sits at a neutral 55.21, while the 50-day and 200-day moving averages have formed a death cross, typically a prelude to deeper correction.

If bulls can reclaim momentum, the first major hurdle is $93, followed by stiff resistance at $96 and $105. Clearing these levels invalidates the bearish thesis. Analysis suggests a decisive break below $80 unlocks a measured move toward $59–64. Conversely, Standard Chartered maintains a long-term target of $2,000 in 5 years, viewing this sub-$100 range as an accumulation zone for institutional infrastructure plays.

— Coin Bureau (@coinbureau) February 4, 2026

BULLISH: $800B Standard Chartered raises Solana price target to $2,000 by 2030 citing the growing dominance of SOL in micropayments and stablecoins. pic.twitter.com/T61K5Y04vK

BULLISH: $800B Standard Chartered raises Solana price target to $2,000 by 2030 citing the growing dominance of SOL in micropayments and stablecoins. pic.twitter.com/T61K5Y04vK

Short-term traders should watch the $86.14 pivot. Price action above this level keeps the recovery hope alive, while sustained trading below it favors the bears. Current volumes do not support a V-shaped recovery, suggesting a “chop and drop” scenario is more likely than an immediate moonshot.

Maxi Doge Offers High-Leverage Culture as SOL Consolidates

With Solana trapped in a low-volatility tightrope walk, active capital is fiercely rotating into presale environments where multipliers, not mere percentage points, are the target. While SOL struggles to gain 10%, early-stage memes are capitalizing on the “degen” appetite for leverage and community power. This shift is evident in the traction of Maxi Doge.

Maxi Doge ($MAXI) positions itself as the antidote to boring price action. Marketing itself as a 240-lb canine juggernaut, the project embodies the “1000x leverage” mentality with viral gym-bro humor.

The presale has already raised a total of more than $4.6 million, signaling robust demand despite broader market fears. Priced at $0.000281, $MAXI also offers 66% APY of staking rewards for early buyers.

The ecosystem includes a “Maxi Fund” treasury for liquidity and holder-only trading competitions, gamifying the grind of the bull market. Liquidity in meme sectors is thinning, yet projects with strong cultural narratives like “Never skip leg-day” continue to draw volume. However, presales carry inherent risks regarding launch volatility and vesting schedules.

The post Solana Price Prediction: Are We Ready For What’s Coming? appeared first on Cryptonews.

TLDR

- DJT stock rose 6% and traded at $9.15 during Monday’s session.

- President Donald Trump said the United States held productive talks with Iran over two days.

- The Dow Jones Industrial Average gained 1,117 points, or 2.4%, after the announcement.

- The Nasdaq Composite advanced 2.4% as markets reacted to the headlines.

- The S&P 500 recorded a $3 trillion market value swing within one hour.

Trump Media & Technology Group Corp. shares climbed on Monday after President Donald Trump announced progress in talks with Iran. The rally followed a broader U.S. stock market surge that lifted major indexes. DJT stock gained 6% and traded at $9.15 during morning activity.

The advance tracked gains across Wall Street as traders responded to headlines from Washington. President Trump said the United States held productive discussions with Iran over two days. His comments triggered swift moves across equity markets and lifted risk sentiment.

DJT Stock Jumps as Markets React to Iran Developments

DJT stock rose 6% on March 23 and reached $9.15 in early trading. The Florida-based media company moved in line with major U.S. indexes. However, the stock remains down 30% year-to-date.

Trump Media & Technology Group Corp., DJT

The Dow Jones Industrial Average jumped 1,117 points, or 2.4%, during the session. At the same time, the Nasdaq Composite also advanced 2.4%. The rebound followed a week when both indexes fell about 2%.

President Trump addressed the situation on Truth Social early Monday.

He wrote that the United States and Iran held “very good and productive conversations” over two days. He added that the talks aimed at “a complete and total resolution of our hostilities in the Middle East.”

His statement lifted equity markets within minutes of publication. However, Iran later denied that officials held any contact with Washington. That denial led to rapid market swings during the same hour.

Trump Comments Trigger $3 Trillion S&P 500 Swing

The S&P 500 Index recorded a market capitalization swing of about $3 trillion within one hour. The move followed Iran’s response that rejected claims of direct talks. Markets reacted quickly to both the president’s statement and Tehran’s denial.

Art Hogan, chief market strategist at B. Riley Wealth Management, spoke with CNBC about the rally.

He said, “The market has been desperate for any good news.” He added that the update appeared to be “the best news we can expect.”

Equities had declined sharply in the prior week before Monday’s rebound. The Dow and Nasdaq both posted losses of roughly 2% during that period. Monday’s gains reversed part of those declines across major benchmarks.

Trump Media & Technology Group Corp., listed under the ticker DJT on Nasdaq, moved alongside the broader market. The company operates Truth Social, the platform where the president shared his statement. Shares traded at $9.15 at the time of reporting and reflected the 6% daily gain.

This release reports a shift in Bitcoin trading as macro momentum and evolving U.S. regulation intersect with market infrastructure updates. The price moved below $70,000 after a brief rally to about $76,000 last week, reflecting broader expectations for higher-for-longer interest rates and addressable inflation risks. At the same time, the issuing authorities outlined a framework that places major crypto assets under the Commodity Futures Trading Commission’s jurisdiction, while signaling the potential for faster spot ETF approvals. The document also notes licensing developments in DeFi and ongoing policy discussions that could shape near-term market activity and long-term confidence.

Key points

- Bitcoin traded below $70,000 after a peak of about $76,000 last week, with macro data and a hawkish Fed stance contributing to the move.

- A US regulatory framework designates major crypto assets as digital commodities under CFTC jurisdiction, alongside existing listing standards that may quicken spot ETF approvals.

- Advances on the CLARITY Act address stablecoin yield structures, signaling potential limits on passive yields while allowing returns tied to transactional activity.

- S&P Dow Jones Indices has licensed Trade[XYZ] to launch the first officially licensed S&P 500 perpetual derivative on the Hyperliquid blockchain, expanding access for non-US investors.

Why it matters

Taken together, the release frames near-term volatility as tied to macro conditions while underscoring how regulatory clarity could attract institutional participation over time. The digital-commodity designation and broader listing standards may speed spot ETF approvals, widening the pathway for mainstream exposure. Moves on the CLARITY Act and DeFi licensing signal potential shifts in how crypto markets are structured and accessed, particularly for non-US investors leveraging cross-market products. Investors and builders should watch regulatory updates, ETF timelines, and licensing milestones to gauge how policy progress may translate into market dynamics.

What to watch

- Regulatory: track progress and potential enactment of the CLARITY Act and its stablecoin yield framework.

- ETF timelines: monitor whether spot crypto ETF approvals accelerate in light of the new framework.

- Licensing milestones: observe developments around the S&P 500 perpetual derivative on Hyperliquid and related licensing deals.

Disclosure: The content below is a press release provided by the company or its PR representative. It is published for informational purposes.

Bitcoin Falls Below $70,000 Amid Macroeconomic Pressure; Regulatory Developments Signal Long-Term Growth Potential

Abu Dhabi, UAE – March 23, 2026: Bitcoin has retreated below the $70,000 mark following a recent peak of $76,000 last week, as macroeconomic headwinds weighed on investor sentiment. The decline was primarily driven by higher-than-expected US Producer Price Index (PPI) data, alongside a more hawkish tone from Federal Reserve Chair Jerome Powell, who highlighted rising oil prices as a potential inflationary risk.

Markets are now increasingly pricing in a prolonged period of elevated interest rates, with expectations that the Federal Reserve could hold rates steady through 2027. Continued geopolitical tensions in the Middle East and sustained high oil prices could further fuel inflation, potentially prompting additional rate hikes—historically a negative backdrop for cryptoasset performance due to tightening financial conditions.

Despite short-term volatility, regulatory developments in the United States are providing a more constructive long-term outlook for the crypto sector.

The US Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC) have jointly introduced a comprehensive cryptoasset classification framework. Under this framework, major cryptoassets including Bitcoin, Ethereum, Solana, and XRP have been designated as digital commodities, placing them primarily under CFTC jurisdiction rather than the SEC.

This classification, alongside previously approved generic listing standards, is expected to accelerate the approval timeline for spot crypto ETFs. Such developments could unlock significant institutional inflows and support long-term price appreciation across the sector.

In parallel, progress is being made on the proposed CLARITY Act, with reports indicating that US lawmakers and the White House have reached a tentative agreement on stablecoin yield structures. The proposed framework would restrict passive yield generation while allowing returns tied to transactional activities such as payments and trading. If enacted, the legislation could represent a major milestone in establishing regulatory clarity and fostering growth within the crypto market.

In the decentralised finance (DeFi) space, S&P Dow Jones Indices has announced a landmark licensing agreement with Trade[XYZ], enabling the launch of the first officially licensed S&P 500 perpetual derivative contract on the Hyperliquid blockchain. This innovation allows non-US investors to gain 24/7 leveraged exposure to the S&P 500 via a decentralised platform, supported by real-time index data.

Following the announcement, Hyperliquid’s native token, $HYPE, rose 6% and is now up over 55% year-to-date, significantly outperforming major cryptoassets such as Bitcoin and Ethereum, which remain down over the same period. The performance reflects growing demand for decentralised infrastructure offering continuous access to both crypto and traditional financial markets.

Meanwhile, higher-risk assets such as memecoins—including $TRUMP, $PEPE, and $PENGU—were among the hardest hit during the recent market downturn, with declines of up to 20%, highlighting their elevated sensitivity to broader market movements.

Simon Peters, Crypto Analyst at eToro, commented: “While macroeconomic pressures have driven short-term volatility in crypto markets, the evolving regulatory landscape in the US represents a significant step forward. Greater clarity around asset classification and market structure could pave the way for increased institutional participation and long-term growth in the sector.”

Dmitry Volkov on the Structure of Modern Venture Investing

Solange’s Son Julez Smith & Tommie Lee Stun Fans W/ Flirty Clips

How Media Platforms Balance Performance and Accessibility in Image Delivery

-

Crypto World3 days ago

Crypto World3 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics3 days ago

Politics3 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Tech6 days ago

Tech6 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Crypto World2 days ago

Crypto World2 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

News Videos5 days ago

News Videos5 days agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World2 days ago

Crypto World2 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Politics6 days ago

Politics6 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Tech4 days ago

Tech4 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Politics6 days ago

Politics6 days agoReal-time pollution monitoring calls after boy nearly dies

-

Crypto World5 days ago

Crypto World5 days agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

Sports10 hours ago

Sports10 hours agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

News Videos5 days ago

News Videos5 days agoPARLIAMENT OF MALAWI – PAC MEETING WITH REGISTRAR OF FINANCIAL ON AMARYLLIS HOTEL – INQUIRY LIVE

-

NewsBeat5 days ago

NewsBeat5 days agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

Politics4 days ago

Politics4 days agoGender equality discussions at UN face pushbacks and US resistance

-

Business1 day ago

Business1 day agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Business5 days ago

Business5 days agoWho Was Alex Pretti? 5 Key Facts About the ICU Nurse Killed by Federal Agents in Minneapolis

-

Sports9 hours ago

Sports9 hours agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Tech1 day ago

Tech1 day agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Sports3 days ago

Sports3 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who nailed 12 Derby-Oaks Doubles enters picks

You must be logged in to post a comment Login