Crypto World

CoolWallet Integrates TRON Energy Rental to Reduce TRX Transaction Costs

CoolWallet, a self-custody hardware wallet provider, has announced the integration of TRON energy rental services, allowing users to reduce transaction costs while securely managing TRX and other TRC-20 assets.

In a press release shared with CryptoNews, the firm said the new feature allows CoolWallet users to access TRON’s blockchain infrastructure while maintaining full control over their private keys and funds through CoolWallet’s hardware wallet paired with its mobile application.

TRON remains one of the most actively used networks among CoolWallet customers, particularly due to its role in stablecoin transfers and low-fee payments.

The update is designed to expand TRON’s accessibility for retail users looking for cost-efficient transactions without sacrificing self-custody protections.

Lower Fees Through Energy Rental

The firm explains that under TRON’s resource model, transactions consume Energy, often requiring users to burn TRX for network fees. CoolWallet’s update introduces an energy rental mechanism that reduces the amount of TRX burned per transaction, helping users retain more of their holdings while maintaining full transaction functionality.

The integration also introduces flexible payment options, allowing users to pay for Energy using either USDT on TRON or TRX, providing greater cost control for frequent transfers and DeFi activity.

By lowering transaction costs, the feature is expected to make token movements and decentralized finance participation more economical for users operating within the TRON ecosystem.

Expanding Secure Self-Custody Access

CoolWallet emphasized that the integration maintains the company’s core focus on security and user sovereignty. Transactions are executed with full self-custody, meaning users retain ownership of their assets at all times without relying on third-party intermediaries.

“TRON plays a critical role in the global stablecoin ecosystem, particularly for users who prioritize cost efficiency and transaction speed,” said Michael Ou, CEO of CoolBitX. “This integration reflects our commitment to supporting the blockchain networks our users depend on most, while ensuring they retain full security and control over their assets.”

Sam Elfarra, Community Spokesperson for the TRON DAO, said the collaboration strengthens access to TRON’s infrastructure through one of the most portable hardware wallet solutions available.

“CoolWallet’s integration represents an important step in making TRON’s infrastructure more accessible to users who prioritize security and self-custody,” Elfarra said. “By bringing TRON support to one of the most portable and user-friendly hardware wallets available, we are expanding access to TRON’s blockchain infrastructure and DeFi applications.”

Strengthening TRON’s Retail and DeFi Ecosystem

The companies said the partnership reflects a shared commitment to reducing barriers to blockchain adoption while maintaining the highest standards of security and user control.

By combining TRON’s scalable infrastructure with CoolWallet’s hardware wallet design, the integration delivers secure, cost-efficient access to blockchain services for everyday users.

The post CoolWallet Integrates TRON Energy Rental to Reduce TRX Transaction Costs appeared first on Cryptonews.

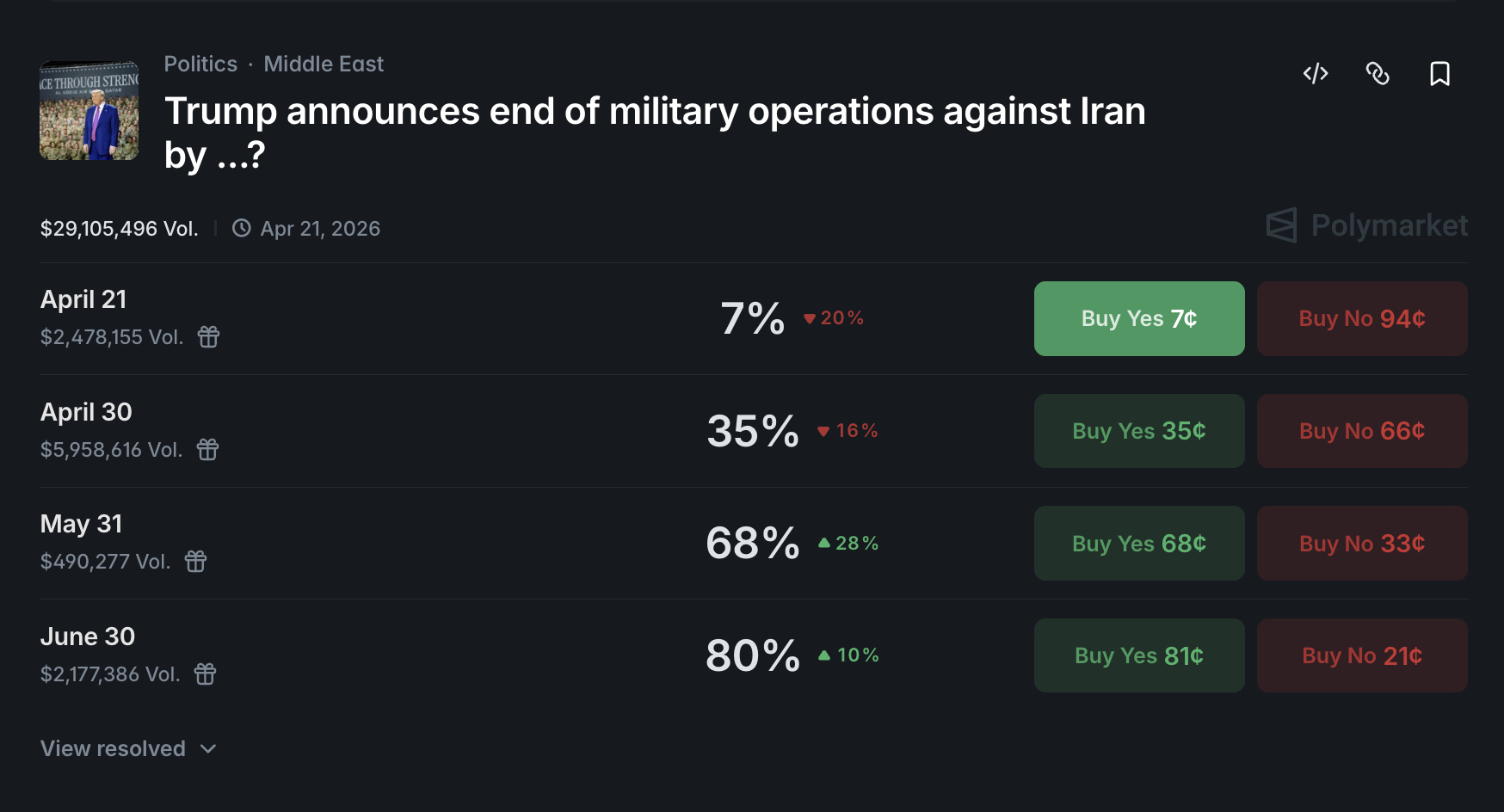

The Strait of Hormuz is back under Iranian control, Trump is threatening to level Iran’s power grid, and somehow BTC is still standing where altcoins would already be bleeding out. Something in the structure of this market has changed, but the Bitcoin price prediction is still bullish.

The weekend’s flare-up hit hard across traditional assets. Brent crude surged to $88, European natural gas futures spiked as much as 11%, and S&P 500 futures dropped 0.6% after Friday’s record close. Bitcoin’s 0.5% pullback looked almost serene by comparison.

— Jesse Cohen (@JesseCohenInv) April 19, 2026

Futures are down big after this weekend’s Iran developments.

Futures are down big after this weekend’s Iran developments.

Dow Futures are down 500 points. pic.twitter.com/ZNDPeEb2Wv

This is now the fourth major Iran-related escalation since the conflict began on February 28, and the pattern is consistent. Each successive crypto sell-off is shallower than the last. Bank of England Deputy Governor Sarah Breeden warned April 18 that the war “heightens combined market stress risks,” yet BTC held above $70,000 throughout.

Discover: The best crypto to diversify your portfolio with

Bitcoin Price Prediction: $80K Still The Target

Bitcoin hit its 2026 low of $63,000 on February before bouncing to $78,000 on the ceasefire talk last week, liquidating $200 million in shorts in the process. The current $74K level sits in the middle of a well-defined five-week range between $73,000 and $78,000.

RSI showed a slightly oversold rebound after the April 1 wick; Chaikin Money Flow data points to active dip-buying despite elevated volatility, the same pattern as Bitcoin’s post-Ukraine invasion consolidation in 2022, with EMA 100 and 200 closing in for a golden cross.

Key support sits higher, after the jump last week, at $73,000. Resistance is clustered at $76,000–$78,000. Polymarket currently prices an 80%+ probability of a deal by the end of June, which sets up a good scenario. Ceasefire confirmed, Strait reopens, then BTC breaks $78,000, targets $80,000–$94,000 range within weeks.

Bernstein maintains a $150,000 year-end 2026 target in a call backed, in part, by MicroStrategy’s purchase of 4,871 BTC ($329.9 million) between April 1–5, right into the conflict’s worst week.

Long-term holders are buying the fear. That doesn’t guarantee a near-term breakout, but it sets a credible demand floor.

Discover: The best pre-launch token sales

Bitcoin Hyper Bullish as BTC Grinds Through War-Risk Consolidation

Bitcoin above $74,000 sounds bullish until you map the resistance. $76,000 is a ceiling that’s been rejected twice already, and a full move to Bernstein’s $150,000 target implies months of sustained catalyst flows like a ceasefire, ETF inflows, and macro easing, all arriving in sequence.

There are a lot of dominoes to be pushed. Those looking for asymmetric upside without waiting for BTC to clear four layers of resistance are increasingly looking at the infrastructure layer being built on top of Bitcoin itself.

Bitcoin Hyper ($HYPER) is positioned at that intersection. It’s built as the first-ever Bitcoin Layer 2 with full Solana Virtual Machine (SVM) integration, bringing sub-second smart contract execution to the Bitcoin ecosystem without sacrificing Bitcoin’s base-layer security.

The pitch is direct: fix Bitcoin’s core limitations of slow transactions, high fees, and zero programmability, while preserving the trust that makes BTC worth building on. The presale has raised $32 million at a current price of $0.0136, with 36% APY staking available.

Hyper offers a real capital stack at a seed-stage price. Dig into the mechanics, because the raised size suggests this isn’t flying under the radar.

The post Bitcoin Price Prediction: Iran War Goes On, Crypto Can’t Catch A Break appeared first on Cryptonews.

Gold, silver, and platinum prices declined on Monday as escalating tensions between the United States and Iran weighed on precious metals markets.

The US Navy fired on and seized an Iranian cargo ship in the Gulf of Oman, reviving concerns before the US-Iran ceasefire expires this week.

Gold, Silver, and Platinum Record Losses as Geopolitical Tensions Escalate

Precious metals have started to unwind last week’s rally. Silver had climbed more than 6% Friday to over $83 on hopes of de-escalation. Iran also temporarily reopened the Strait of Hormuz for commercial vessels.

However, that move reversed once shipping stalled again. Today, the silver price fell 1.07% to $79.89, per Trading Economics data. Platinum led the sell-off with a 2.22% drop to $2,094.20. Gold slid 0.85% to $4,792.48.

Copper retreated 0.80% to $6.0544, coming off its highest close since early February. Zinc and lead also declined.

Follow us on X to get the latest news as it happens

On the other hand, industrial and battery metals held up better than precious metals. Lithium gained 1.77%, while iron ore and steel nudged higher.

Brent jumped as much as 7.9%, and WTI climbed over 7% toward $90, reviving inflation concerns that trim Fed rate-cut expectations and weigh on non-yielding metals.

The crypto market was also part of the broader sell-off. BeInCrypto Markets data showed that the total market capitalization declined 1.15% over the past 24 hours. Bitcoin (BTC) dropped below $74,000 in early Asian trading hours today before settling at $74,190 by press time.

All attention now shifts to Wednesday’s ceasefire deadline and a possible new round of negotiations. Trump said US negotiators would fly to Islamabad on Monday.

Iranian state broadcaster IRIB said Tehran had no plans to join the next round, citing unnamed Iranian sources.

“There are currently no plans to participate in the next round of Iran-US talks.”

However, Al Jazeera reported that Iranian officials would “most probably” attend, citing preparations already underway in Islamabad. Further losses in precious metals hinge on whether either side returns to the table and on the outcome.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Precious Metals Fall as US-Iran Conflict Escalates Ahead of Ceasefire Deadline appeared first on BeInCrypto.

- RaveDAO token plunged 95% from $26 to under $1.

- RAVE launched in December 2025 on Binance Alpha.

- ZachXBT’s on-chain analysis also highlights MemeCore, River and MYX among questionable projects.

RaveDAO (RAVE) has plunged below $1, erasing more than 95% of its earlier rally to an all-time high of $26.

The sharp decline follows an investigation by blockchain analyst ZachXBT, which alleged clear signs of price manipulation.

The findings have raised broader concerns about potential insider-driven schemes affecting multiple tokens listed on centralised exchanges, contributing to selling pressure across the segment.

RaveDAO token dumps amid ZachXBT’s explosive allegations

ZachXBT, a pseudonymous investigator celebrated for dismantling multimillion-dollar crypto frauds, took to X on April 18, 2026, to dissect RAVE’s suspicious trajectory.

He pinpointed concentrated wallet activity controlling the token’s liquidity, engineering artificial pumps to trap retail buyers before orchestrated dumps.

“RAVE launched in Dec 2025 on Binance Alpha with a 1B total supply. The addresses below, linked to the initial distribution, control ~95% of the RAVE supply,” the on-chain sleuth posted.

Labelling it a textbook “pump-and-dump,” ZachXBT offered a $25,000 bounty for transaction proofs, urging platforms like Binance, Bitget, and Gate.io to launch probes.

He notes that the exchanges acknowledged his call, a move that could mirror past successes in securing refunds and bans.

Yet ZachXBT questioned why CEXs have waited for his call to acknowledge potential manipulation.

“While it’s good the exchanges responded, I find it unlikely this activity wasn’t spotted internally before I raised it publicly.”

RAVE’s price carnage unfolded mercilessly, plummeting from $26 to under $1 within 24 hours, with trading volume surging amid mass liquidations.

Billions of dollars in market cap vaporised, leaving holders stunned. The declines saw the token’s value drop to lows of $0.50, where it hovered as of writing on April 20, 2026.

Update: Three hours ago multisig 0x53d7 linked to the RAVE initial distribution which I flagged above sent ~23M RAVE ($23M) to two Bitget deposit addresses and the price dropped 40% from $1 to $0.6.

Deposit addresses

0x26aC542f5a04D574580881723224DAcD1EDB9B45… pic.twitter.com/Qi1asiFWsB— ZachXBT (@zachxbt) April 19, 2026

ZachXBT also hits other tokens

The potential price manipulation extends to similar tokens.

“RAVE is not the only token with manipulation we have seen on major centralized exchanges,” he posted.

“It’s just the most blatant, reaching a top 15 market cap within 10 days before dropping 95% in hours. Other projects with highly questionable price action recently include: SIREN, MYX, COAI, M, PIPPIN, RIVER.”

According to ZachXBT, all projects have exhibited “highly questionable price action” and supply dominance by the team.

MemeCore, RIVER and PIPPIN prices echoed the Rave token bleed, dumping double digits to erase recent gains.

Some retail traders commented on ZachXBT’s post, noting this could be an opportunity to short. His response:

I do not recommend shorting manipulated tokens with a high insider concentration.

— ZachXBT (@zachxbt) April 20, 2026

Data on CoinMarketCap showed M, River and Siren were down 7-9% in the past 24 hours as of writing.

Bitcoin price briefly fell below $74,000 on Monday as fading prospects of U.S. Iran peace talks and escalating tensions in the Strait of Hormuz weighed on sentiment.

Summary

- Bitcoin briefly dropped below $74,000 as Iran ruled out U.S. peace talks and tensions escalated in the Strait of Hormuz.

- Iran retaliated to a U.S. ship seizure with drone and missile strikes, while conflicting signals over negotiations kept markets on edge.

- Oil prices surged, with WTI nearing $90 and Brent above $95, as renewed conflict raised fears of supply disruptions and broader market volatility.

According to reports, Iranian sources recently said that Iran will not show up for the peace negotiations with the U.S. that were set to be held in Islamabad today. This comes after the nation promised to retaliate against the U.S. for intercepting and seizing one of its cargo ships in the Strait of Hormuz.

The heightened volatility in the surrounding Gulf region after the war began had left markets on edge, with economists expressing concerns of a global recession if supply lines remained blocked.

Shortly following the U.S. intervention on the ship, Iran responded with its own offensive strategy, attacking U.S. military ships with drones and ballistic missiles.

The tensions between the two nations flared up earlier in the weekend. On Friday, Iran reopened the Strait of Hormuz amid its stated commitment to de-escalate. However, Tehran decided to close it again just hours later as the U.S. continued to maintain the naval blockade.

While the U.S. later announced that both parties would attend peace negotiations on Monday, Iran has refuted these claims entirely. Earlier, Iran had also dismissed Trump’s suggestion that it would give up on its uranium enrichment plan as part of any future deal.

Crude oil price, which fell earlier due to expectations of peace discussions between the nations and reopening of the strait, surged significantly following the recent breakdown in communication. Notably, West Texas Intermediate crude oil rose 6.7% to nearly $90 while Brent crude rose 6% to above $95 again.

Since crypto markets operate around the clock, they reacted immediately to the latest geopolitical developments over the weekend, with prices largely trending lower.

Bitcoin (BTC) had rallied to $78,400 on Friday, but the move was swiftly rejected, with the price slipping below $74,000 as hostilities resumed. At press time, the bellwether asset was trading just under the $75,000 level.

Further price swings may lie ahead as the ceasefire deadline passes without any clear extension. Overnight attacks have added to the uncertainty, while the absence of any concrete peace negotiations continues to weigh on market sentiment. Traders are now bracing for continued volatility as geopolitical risks remain elevated.

As such, if Bitcoin sharply falls below $74,000 again, it could slide further to $72,000, which acts as a major support level. Failure below the $72,000 mark might invite a broader selloff toward the $68,000 zone. On the other hand, if Bitcoin stabilizes over $76,000, it could embolden bulls to target a return to the $80,000 psychological threshold.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Key Points

- The Chinese technology firm Huawei has entered a strategic partnership with Vietnam’s SHB bank this past weekend

- The collaboration encompasses technology infrastructure design and comprehensive data platform construction

- Security and operational stability for banking systems form core components of the agreement

- This partnership joins existing Huawei collaborations with SCB, SeABank, and Home Credit across Vietnam

- Huawei secured major contracts in 2024 for Vietnam’s 5G infrastructure development

The Chinese technology conglomerate Huawei Technologies Group has formalized a strategic partnership with SHB, a prominent Vietnamese banking institution, signaling the company’s accelerating expansion throughout Vietnam’s financial landscape.

SHB publicly disclosed the partnership on Sunday. According to the arrangement, Huawei will provide expertise in crafting the bank’s technological framework and establishing robust data infrastructure. The agreement additionally ensures that SHB’s operational systems maintain consistent reliability and comprehensive security.

“The cooperation with SHB is an important milestone in the group’s market expansion in Vietnam,” said Spawn Fan, a senior Huawei executive, in the bank’s statement.

This isn’t Huawei’s inaugural venture into Vietnam’s banking industry. The technology powerhouse maintains established partnerships with multiple financial institutions including SCB, SeABank, and Home Credit, spanning initiatives in digital transformation, security protocols, data intelligence, cloud infrastructure, and banking platform optimization.

Strategic Expansion in Southeast Asia

The newly announced SHB collaboration strengthens Huawei’s increasingly substantial position within one of Southeast Asia’s most dynamic and rapidly expanding markets. Vietnamese financial institutions have aggressively prioritized digital infrastructure modernization, creating opportunities that Huawei has strategically pursued.

Huawei’s expanding influence in Vietnam represents a significant shift from previous policy positions. Until quite recently, Vietnamese authorities maintained strict restrictions preventing Chinese corporations from participating in the nation’s 5G telecommunications infrastructure.

This policy underwent a dramatic reversal in 2024 when Huawei successfully secured multiple contracts to develop significant portions of Vietnam’s 5G network. The current SHB partnership reflects a continuation of this evolving relationship — demonstrating strengthening connections between Vietnamese organizations and Huawei spanning both telecommunications and financial technology sectors.

Partnership Scope and Implementation

SHB ranks among Vietnam’s most significant privately-owned commercial banking institutions. The comprehensive partnership with Huawei encompasses multiple critical domains: architectural design for technology infrastructure, comprehensive data platform construction, and continuous operational assistance ensuring system stability and security.

These initiatives represent substantial commitments. Constructing data platforms and architectural frameworks for commercial banking operations requires extensive integration with fundamental banking technology systems.

According to statements from the Vietnam Banks Association, Huawei’s activities throughout Vietnam’s financial industry concentrate on digital transformation initiatives, cybersecurity enhancement, advanced data analytics, cloud computing solutions, and banking operational efficiency — capabilities that align directly with the SHB partnership framework.

The 5G infrastructure contracts Huawei won in 2024 marked a fundamental policy transformation from Vietnamese government authorities. This strategic pivot created pathways for expanded collaboration, with the SHB agreement representing one of the most substantial manifestations of this revised approach.

Spawn Fan, the Huawei representative referenced in SHB’s official announcement, characterized the partnership as a significant achievement — not solely for SHB’s technological advancement, but for Huawei’s comprehensive Vietnam market strategy.

The Vietnam Banks Association has verified that Huawei’s current financial sector engagements include SCB, SeABank, and Home Credit, with the SHB partnership now expanding that portfolio.

Strategy co-founder Michael Saylor has stoked expectations of another large Bitcoin purchase just days after Strategy disclosed a roughly $1 billion buy in mid-April. The company revealed that between April 6 and 12 it acquired 13,927 BTC for about $1 billion, at an average price of $71,902 per coin. In a sign that Saylor may be signaling more activity, he posted on X with the message Think Even ₿igger, accompanied by a chart of Strategy’s purchase history—a pattern he has used in the past to hint at forthcoming buys, according to coverage of the episode.

In the same period, Strategy’s leadership publicly discussed a broader capital management move: paying its dividend more frequently, with a plan to double the cadence to semi-monthly payments. The intention, said Strategy CEO Phong Le, is to stabilize the STRC price, dampen cyclicality, improve liquidity, and expand demand for the stock. The stance comes as Strategy has prepared a preliminary proxy filing with the U.S. Securities and Exchange Commission; the definitive proxy is expected on April 28, with shareholder voting running through June 8 and potential implementation slated for mid-July if approved.

Key takeaways

- Strategy hints at another Bitcoin purchase after disclosing a $1 billion acquisition of 13,927 BTC in early April, with Saylor signaling via a post comparing Strategy’s past buys.

- The company is proposing to shift STRC dividend payments to a semi-monthly schedule (twice a month, on the 15th and month-end), aiming for 24 payments a year at an 11.5% yield.

- The move to semi-monthly dividends is framed as a way to stabilize price and liquidity, with Strategy describing it as a unique approach among preferred equities.

- Strategy holds the largest Bitcoin treasury among publicly traded companies, with 780,897 BTC worth about $58.2 billion, according to Bitbo data, and it has a habit of recurring weekly purchases.

- Despite the Bitcoin buys, the company reports significant unrealized losses on digital assets, totaling about $14.46 billion in its first-quarter results.

Strategy’s latest Bitcoin move and the social signal

The disclosed purchase of 13,927 BTC for roughly $1 billion occurred over a one-week window in April, at an average price near $71,902 per coin. The social signal accompanying the filing—Saylor’s “Think Even ₿igger” post with a chart of Strategy’s purchase history—has historically coincided with additional buying or hints of future transactions, a pattern analysts monitor as a potential short-term predictor of capital deployment. The development sits within a broader narrative of corporate Bitcoin treasury management where large hodlers weigh ongoing accretion against volatility and capital allocation priorities.

Dividend plan to stabilize price and liquidity

Le framed the dividend proposal as a mechanism to reduce price volatility and encourage steady demand for STRC. If approved, Strategy would pay semi-monthly dividends on the 15th and the last day of each month, totaling 24 payments per year at the current rate of 11.5%. Le noted that this cadence would position STRC as a highly distinctive instrument in the market, and the company has worked through multiple iterations to reach a viable schedule that accommodates NASDAQ’s rules on record and payment dates. Nasdaq-listed STRC would still need to comply with minimum gaps between record and payment dates—an issue the company acknowledged as an operational constraint.

The plan was detailed in an investor presentation linked to the proxy materials, with the preliminary filing submitted to the SEC and a definitive filing expected by April 28. If shareholders approve the proposal, the new semi-monthly schedule would take effect mid-July, subject to the usual regulatory and procedural approvals.

BTC treasury size, market backdrop, and investor reaction

Strategy’s balance sheet remains anchored in Bitcoin, with the company holding 780,897 BTC, the largest stash among publicly traded firms. Bitbo’s data places Strategy’s BTC holdings at approximately $58.2 billion in value, underscoring the scale of its treasury position. The stock market reaction to the ongoing program has been nuanced: Strategy’s shares (MSTR) rose by about 11.8% on a recent session to around $166.50, though they remain down roughly 47% over the past year. The dynamic underscores a complex investor calculus: large-scale BTC exposure paired with sensitive equity pricing and the potential impact of dividend policy changes.

On the accounting side, Strategy reported substantial unrealized losses on its digital asset holdings for the first quarter, tallying about $14.46 billion. The disclosures reflect the market’s swing in BTC prices and the accounting treatment for crypto holdings at scale, contributing to a broader conversation about risk management and liquidity needs for corporate treasuries tied to digital assets.

What to watch next

Investors will be keeping a close eye on the proxy process and whether the semi-monthly dividend plan gains shareholder approval. The timing of the next BTC purchase remains uncertain, but the social signaling by Saylor adds an element of anticipation around Strategy’s treasury strategy. As regulators and markets continue to refine frameworks for corporate crypto holdings and investor protections, Strategy’s moves could serve as a barometer for how publicly traded companies balance growth, income, and risk in a volatile asset class.

Sources and context for these developments were reported in coverage detailing Strategy’s recent Bitcoin purchases, the proposed dividend schedule, and the company’s regulatory filings. For reference, strategic data on Strategy’s Bitcoin holdings is tracked by market trackers such as Bitbo, and the proxy filing timeline aligns with the SEC’s typical review and voting windows.

Traditional banks could see their market dominance challenged by the rise of stablecoins and tokenized real-world assets as these digital currencies move beyond their current niche uses.

Summary

- Moody’s Investors Service suggests that the disruption risk for the banking sector remains limited at this stage because current U.S. rules prevent stablecoins from paying yield.

- The growth of tokenized real-world assets and stablecoins could eventually place pressure on traditional banks by causing deposit outflows and reducing their overall lending capacity.

Moody’s Investors Service Digital Economy Group associate vice president Abhi Srivastava told crypto media that stablecoin use remains “limited” for now, even though the sector’s market capitalization climbed past $300 billion by the end of last year.

While the role of these assets in cross-border commerce and on-chain finance is expanding, the existing US payment landscape is currently fast and trusted enough to keep disruption at bay.

Srivastava observed that “for the banking sector, at this stage, disruption risk appears limited,” largely because US rules prevent stablecoins from paying yield to holders.

According to him, domestic deposits are unlikely to be replaced at scale while these yield restrictions remain in place. However, long-term growth in stablecoins and tokenized RWAs—physical or financial assets represented by blockchain tokens—could eventually trigger deposit outflows.

Such a trend would reduce the lending capacity of traditional banks by placing “pressure” on their core business models, he added.

Legislative gridlock over yield and oversight

Regulatory policy regarding stablecoins has turned into a major point of contention between the crypto industry and the banking sector. The primary concern centers on yield-bearing stablecoins, which banks fear will directly compete for their customers.

This specific issue has become a major stumbling block for the Digital Asset Market Clarity Act of 2025, or the CLARITY Act.

The Digital Asset Market Clarity Act of 2025, or the CLARITY Act, has hit a wall in Congress as lawmakers struggle to balance the interests of the crypto industry with those of the bank lobby. The framework was designed to set clear rules for asset classification and regulatory oversight, but it stalled after major players like Coinbase voiced opposition to specific provisions.

The ban on yield-bearing stablecoins and a lack of legal safeguards for open-source developers remain the primary points of contention.

Banks have lobbied heavily against allowing stablecoins to offer interest, fearing such a move would trigger massive deposit outflows and sap their ability to provide loans. Srivastava warned that over time, the growth of tokenized RWAs—physical assets represented on a blockchain—could place significant “pressure” on traditional financial institutions.

Senator Thom Tillis of North Carolina recently signaled plans to introduce a compromise draft to bridge the gap between crypto firms and traditional banks. However, this updated proposal has already faced resistance and remains unreleased to the public.

Spot Bitcoin (BTC) and Ethereum (ETH) exchange-traded funds (ETFs) drew $1.27 billion in combined net inflows during the week ending April 17. This marked their strongest week since mid-January.

Across the five major spot crypto ETF products, total weekly inflows reached roughly $1.37 billion, including XRP, Solana, and Chainlink funds, a near 40% jump from the prior week.

Crypto ETF Flows Rebound After Q1 Drawdown

Bitcoin ETFs pulled in $996.38 million, while Ethereum ETFs added $275.83 million, according to SoSoValue data. Both marked the largest weekly inflows since the week of January 16.

The rebound comes after a difficult first quarter. BTC ETF assets fell nearly 35% from their $128 billion mid-January high to $83.40 billion by February 27.

In addition, ETH ETF assets dropped 46% over the same period. Now, the inflow surge has pushed total Bitcoin ETF net assets back above $100 billion.

Moreover, the move extends a third straight week of positive BTC ETF flows and a second for Ethereum products.

Follow us on X to get the latest news as it happens

The recovery was not isolated to the two largest assets. XRP ETFs took in $55.39 million, nearly matching their 2026’s peak week in mid-January. Solana funds drew $35.17 million, reversing three consecutive weeks of outflows, while Chainlink ETFs added $5.30 million.

This marked the largest inflow outside its December launch week. Notably, LINK ETFs have not recorded a single week of net outflows.

Inflows picked up on the back of easing expectations around US–Iran tensions, but the backdrop remains fragile. Sentiment could come under renewed pressure after US naval forces fired on and seized an Iranian cargo ship in the Gulf of Oman, marking a clear escalation in the conflict.

At the same time, uncertainty surrounding Iran’s participation in the upcoming talks in Islamabad has added to market caution. Geopolitical developments, including the trajectory of negotiations and potential retaliation risks, are likely to remain a key driver of market sentiment in the near term.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Crypto ETFs Haul $1.37 Billion in Biggest Week Since January 2026, Altcoins Join Rally appeared first on BeInCrypto.

Three altcoins are entering next week with fresh bullish setups on their daily charts. DeXe (DEXE) leads with a 63.8% weekly gain, while Ethena (ENA) and MemeCore (M) show technical breakouts that suggest follow-through upside.

Each chart shows a distinct setup. DEXE has cleared a key Fibonacci retracement with strong momentum, ENA has broken a multi-month downtrend line, and M is riding an exponential support curve above a confirmed breakout zone.

Altcoin to Watch: DeXe Leads the Week With a 64% Rally

DeXe (DEXE) is the strongest performer on this watchlist, up 63.8% over the last seven days. Nearly 10% of that gain came in the last two sessions, with price trading at $15.85 and sitting directly on the 0.618 Fibonacci retracement at $15.61.

The coin has already cleared the $12.50 to $13 resistance zone, a level flagged in prior DeXe coverage. That area now acts as the first support if buyers step back.

The next major target on the upside is the 0.786 retracement at $19.39. Above that level, the chart shows a final target at the 1.0 retracement near $24.20, which would mark a full recovery to the February 2025 high.

Moving Average Convergence Divergence (MACD) remains elevated and positively sloped, which continues to support momentum. However, the Relative Strength Index (RSI) has reached the upper band and is showing the first hints of bearish divergence, a shift that could signal cooling ahead.

Volume has been declining across the advance, a typical sign that the move lacks fresh participation. The uptrend could stall if new buyers do not step in at higher prices.

If momentum reverses, the first downside target is $13. The second support sits at $10.31, which is the 0.382 Fibonacci retracement and the line that would define a deeper correction.

Ethena Breaks a Multi-Month Downtrend Line

Ethena (ENA) has gained 27.1% over the past week, the second-strongest performer on this list. Price trades near $0.1162 after a short-term pullback on the day, yet the weekly structure remains constructive.

Three days ago, the price pushed above a descending trend line. That line had guided the full move from the November 11 high at $0.3603 into the April 5 low at $0.0765.

The Fibonacci retracement anchored from those two points places the first resistance at $0.1435, which is the 0.236 level. Price is consolidating just below that zone, which is marked in red on the chart.

A confirmed close above $0.1435 would open the 0.382 retracement at $0.1849 and the 0.5 retracement at $0.2184. The 0.618 retracement at $0.2519 remains the primary target for a larger breakout. That level would represent a 116% gain from current prices (green).

Volume has been rising on bullish candles, signaling stronger buyer participation. RSI has climbed out of oversold without reaching overbought, which leaves room for further upside. Other altcoins have shown similar recovery setups heading into April.

The final bullish target sits at $0.3603, the breakdown zone from November. That path is ambitious, yet the chart no longer prints fresh lower lows, and the break of the trend line is the first structural shift in months.

MemeCore Holds Breakout Support After a 24% Weekly Gain

MemeCore (M) posted a 24.2% gain over the last seven days, rounding out this week’s three altcoins. The token broke out of a multi-month resistance zone on April 16 and has since converted that zone into support.

That resistance had capped gains since September 17, 2025. It now sits between $2.80 and $3.00 on the daily chart, and a retest on April 19 confirmed the area as support.

An exponential curve drawn on the chart (black) continues to track the price from below. A break of that curve would be the first clear sign that the trend structure has shifted.

The most recent pullback tagged the 0.5 Fibonacci retracement, which sits inside the same support band. A deeper correction would shift attention to the 0.618 retracement near $2.54, the last defense for the bullish thesis. Prior MemeCore coverage tracked a similar breakout attempt earlier this cycle.

RSI shows no bearish divergence, and MACD remains constructive. Volume has been trending lower even as price extends, a divergence that suggests the rally needs fresh buyers to sustain the current pace.

The post 3 Altcoins to Watch in the 4th Week of April 2026 appeared first on BeInCrypto.

Key Takeaways

- A security breach affecting KelpDAO’s rsETH product on April 20 created cascading effects throughout Solana’s DeFi infrastructure

- Stablecoin lending platforms across the network have experienced dramatic spikes in utilization metrics

- Jupiter Lend currently shows 99% utilization with only $81 million remaining from its $421 million USDC reserves

- Both Kamino and Marginfi face severe liquidity constraints as borrowing rates exceed 8%

- The available capital for lending across Solana’s ecosystem has reached critically low levels

A security incident targeting KelpDAO’s rsETH infrastructure on April 20, 2026, has triggered widespread disruption across the Solana blockchain’s decentralized finance landscape.

The repercussions materialized quickly. Capital started evacuating from DeFi applications, creating a squeeze on stablecoin availability throughout Solana’s lending infrastructure. Multiple prominent platforms now operate with minimal reserves remaining.

Jupiter Lend faces particularly acute pressure. The protocol manages $421 million in total USDC deposits, of which $340 million has been distributed to borrowers. When factoring in mandatory reserve requirements, the platform operates at approximately 99% capacity. Current annual percentage yields for lenders stand at 4.36%.

Kamino Prime Market experiences similar stress conditions. Data indicates total USDC deposits of roughly $186.8 million against outstanding loans of $178.8 million. This configuration produces utilization approaching 96%, while lending yields have climbed to 8.92%.

Kamino’s Main Market exhibits comparable dynamics. The platform holds approximately $172 million in USDC deposits supporting $164 million in active loans. Utilization metrics hover around 95.75%, with lending returns reaching 10.2%.

Secondary Platforms Experience Significant Pressure

Marginfi data reveals USDC lending utilization at 88.32%, accompanied by lending yields of 7.65%. Save Finance, the rebranded iteration of Solend, has witnessed utilization climb beyond 70%, with corresponding lending rates at 3.9%.

These metrics demonstrate that liquidity stress extends well beyond flagship platforms. The pressure has permeated Solana’s entire lending infrastructure.

Elevated utilization percentages indicate extremely limited USDC availability for new borrowers. Users requiring access to capital face restricted options alongside escalating costs.

The constricted market conditions have additionally impacted derivative markets tracking Solana’s token valuation. Prediction markets estimating Solana above $150 during the April 13–19 window show only 0.4% probability on the affirmative side. These markets lack actual USDC trading volume, undermining their credibility as price signals.

Market Data Reveals Investor Sentiment

For April 16, certain prediction markets price Solana exceeding $100 at 100% certainty. However, with zero verifiable transaction volume supporting this figure, the indicator provides minimal analytical value.

Affirmative position shares betting on Solana reaching $150 by mid-April trade at merely 0.4 cents while offering $1 payouts upon correct resolution. This potential 250x multiplier underscores profound market doubt regarding imminent price appreciation.

The liquidity impact stemming from the KelpDAO security incident remains unresolved. Borrowing costs continue their upward trajectory as utilization persists at heightened levels throughout Solana’s primary lending protocols.

As of April 20, Kamino’s Main Market lending yield of 10.2% represents the peak rate documented among impacted platforms.

Bitcoin Price Prediction: Iran War Goes On, Crypto Can’t Catch A Break

90 Day Fiance’s Trisha Confirms She’s Pregnant at Tell-All

Huge celebs turn on David Haye – including ‘uncomfortable’ hosts Ant and Dec

-

Crypto World7 days ago

Crypto World7 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

NewsBeat6 days ago

NewsBeat6 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Theodora Dress

-

Crypto World6 days ago

Crypto World6 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos5 days ago

News Videos5 days agoSecure crypto trading starts with an FIU-registered

-

Sports3 days ago

Sports3 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World6 days ago

Crypto World6 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

Business18 hours ago

Business18 hours agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Crypto World2 days ago

Crypto World2 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Politics3 days ago

Politics3 days agoPalestine barred from entering Canada for FIFA Congress

-

Sports7 days ago

Sports7 days agoNWFL opens Pathway for new Clubs ahead of 2026 Season

-

Business3 days ago

Business3 days agoCreo Medical agree sale of its manufacturing operation

-

Entertainment6 days ago

Entertainment6 days agoBrand New Day’ Footage Reveals the Devastating Impact of ‘Now Way Home’

-

Politics23 hours ago

Politics23 hours agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Tech5 days ago

Tech5 days agoMicrosoft adds Windows protections for malicious Remote Desktop files

-

Entertainment6 days ago

Entertainment6 days agoKarol G’s ‘Ultra Raunchy’ Coachella Set Gave ‘Satanic Vibes’

-

Sports7 days ago

Sports7 days agoAaron Judge says Yankees need to ‘simplify’ approach amid offensive slump

-

Entertainment7 days ago

Entertainment7 days agoPete Davidson Reveals ‘Brutal’ Mom Moment That Got Him Sober

-

Entertainment6 days ago

Entertainment6 days agoHow Babylon 5 Turned Brief Side Story Into Emotional Masterpiece

-

Tech6 days ago

Tech6 days agoWhat was the first ransomware attack to demand payment in Bitcoin?

You must be logged in to post a comment Login