Crypto World

Fidelity Launches Digital Dollar Stablecoin FIDD

Fidelity Investments has entered the stablecoin market with the launch of Fidelity Digital Dollar (FIDD), marking a significant step by one of the world’s largest asset managers into on-chain dollar instruments. Announced on February 4, 2026, the new stablecoin is issued by Fidelity Digital Assets, National Association, and is available to both retail and institutional clients. Each token is redeemable at a 1:1 ratio with the U.S. dollar, positioning FIDD as a regulated, institutionally managed alternative in a stablecoin market that now exceeds $316 billion in total capitalization.

Key takeaways

- Fidelity has launched its first U.S. dollar-backed stablecoin, Fidelity Digital Dollar (FIDD), available to retail and institutional clients.

- FIDD can be purchased or redeemed directly through Fidelity platforms at a fixed rate of $1 per token.

- Reserve assets are managed internally, leveraging Fidelity’s long-standing asset management infrastructure.

- The stablecoin operates on the Ethereum mainnet and can be transferred to any compatible address.

- Daily disclosures provide transparency on circulating supply and reserve net asset value.

- The launch follows new U.S. regulatory clarity for payment stablecoins.

Sentiment: Neutral

Market context: The launch comes as regulatory clarity in the United States improves and traditional financial institutions increase their participation in tokenized cash, custody, and blockchain-based settlement infrastructure.

Why it matters

Fidelity’s move into stablecoin issuance signals a broader shift in how traditional asset managers approach blockchain-based financial infrastructure. Rather than relying solely on third-party stablecoins, Fidelity is now offering a proprietary digital dollar backed by its own balance sheet processes and operational standards.

For institutional investors, the availability of a stablecoin issued and managed by a globally recognized financial institution may reduce counterparty concerns that have historically limited stablecoin adoption in regulated environments. Retail users, meanwhile, gain access to an on-chain dollar that integrates directly with existing Fidelity platforms.

More broadly, the launch highlights how stablecoins are increasingly viewed as foundational financial plumbing rather than speculative crypto assets. As asset managers, banks, and payment firms adopt similar models, competition may shift toward transparency, reserve management, and regulatory alignment.

What to watch next

- Whether FIDD expands beyond Ethereum to additional blockchain networks.

- Potential exchange listings and liquidity growth outside Fidelity platforms.

- Regulatory reporting standards applied to Fidelity-issued stablecoins.

- Adoption by wealth managers and institutional treasury operations.

Sources & verification

- Fidelity’s official announcement dated February 4, 2026.

- Daily reserve and supply disclosures published on Fidelity’s website.

- Statements from Fidelity Digital Assets leadership regarding regulatory alignment.

Fidelity Digital Dollar enters the regulated stablecoin landscape

Fidelity Investments’ decision to issue a proprietary stablecoin represents a notable evolution in the firm’s digital asset strategy. The new token, Fidelity Digital Dollar (FIDD), is designed to function as a blockchain-based representation of the U.S. dollar while remaining closely integrated with Fidelity’s existing financial infrastructure.

Issued by Fidelity Digital Assets, National Association, FIDD is available to eligible retail and institutional investors through Fidelity Digital Assets, Fidelity Crypto, and Fidelity Crypto for Wealth Managers. Clients can purchase or redeem the stablecoin directly with Fidelity at a fixed price of one U.S. dollar per token, a structure intended to mirror the operational simplicity of traditional cash balances.

Unlike many stablecoins that rely on external reserve managers or opaque custodial arrangements, FIDD’s reserve assets are managed by Fidelity Management & Research Company LLC. This internal structure allows Fidelity to apply the same portfolio oversight, risk controls, and compliance standards used across its traditional asset management business.

Transparency is a central component of the product’s design. Fidelity publishes daily disclosures detailing FIDD’s circulating supply and the net asset value of its reserves as of each business day’s close. This approach aligns with growing regulatory expectations for stablecoin issuers and aims to address long-standing concerns around reserve sufficiency and disclosure practices in the sector.

From a technical perspective, FIDD is issued on the Ethereum mainnet, enabling holders to transfer tokens to any compatible Ethereum address. This design choice allows the stablecoin to integrate with existing decentralized finance infrastructure while remaining accessible through centralized platforms.

Fidelity Digital Assets President Mike O’Reilly described the launch as the result of years of internal research into stablecoins and blockchain-based financial systems. According to the firm, the goal is to provide investors with on-chain utility without sacrificing the stability and operational rigor associated with traditional financial products.

The timing of the launch is closely tied to regulatory developments in the United States. Recent legislation establishing clearer rules for payment stablecoins has reduced legal uncertainty for large financial institutions considering issuance. Fidelity has positioned FIDD as a response to this evolving framework, emphasizing compliance and investor protection alongside technological innovation.

Stablecoins have become a critical component of digital asset markets, facilitating trading, settlement, and cross-border transfers. With total market capitalization now exceeding $316 billion, the sector has attracted increasing scrutiny from regulators and policymakers. Fidelity’s entry reflects a broader trend of established financial firms seeking to bring stablecoin activity within regulated, institutionally managed environments.

Fidelity’s broader digital asset strategy provides important context for the move. The firm has been building blockchain-related infrastructure since 2014, long before digital assets became mainstream. Its offerings now include custody, trading, research, and investment products tailored to institutional clients, intermediaries, and retail investors.

By adding a proprietary stablecoin to this lineup, Fidelity is effectively extending its ecosystem into on-chain cash management. For wealth managers and institutional clients already using Fidelity’s digital asset services, FIDD may serve as a settlement layer that reduces reliance on external stablecoin issuers.

The launch also raises questions about how competition in the stablecoin market may evolve. As more traditional financial institutions issue their own tokens, differentiation may increasingly depend on regulatory status, transparency, and integration with existing financial services rather than yield incentives or aggressive growth strategies.

While Fidelity has not disclosed immediate plans for expanding FIDD beyond Ethereum or adding advanced programmable features, the infrastructure chosen leaves room for future development. Potential use cases could include on-chain settlement for tokenized securities, collateral management, or integration with institutional payment systems.

For now, Fidelity Digital Dollar stands as a signal that stablecoins are moving deeper into the core of traditional finance. Rather than operating at the margins of the financial system, regulated digital dollars issued by major asset managers may become standard tools for both crypto-native and traditional investors navigating an increasingly hybrid financial landscape.

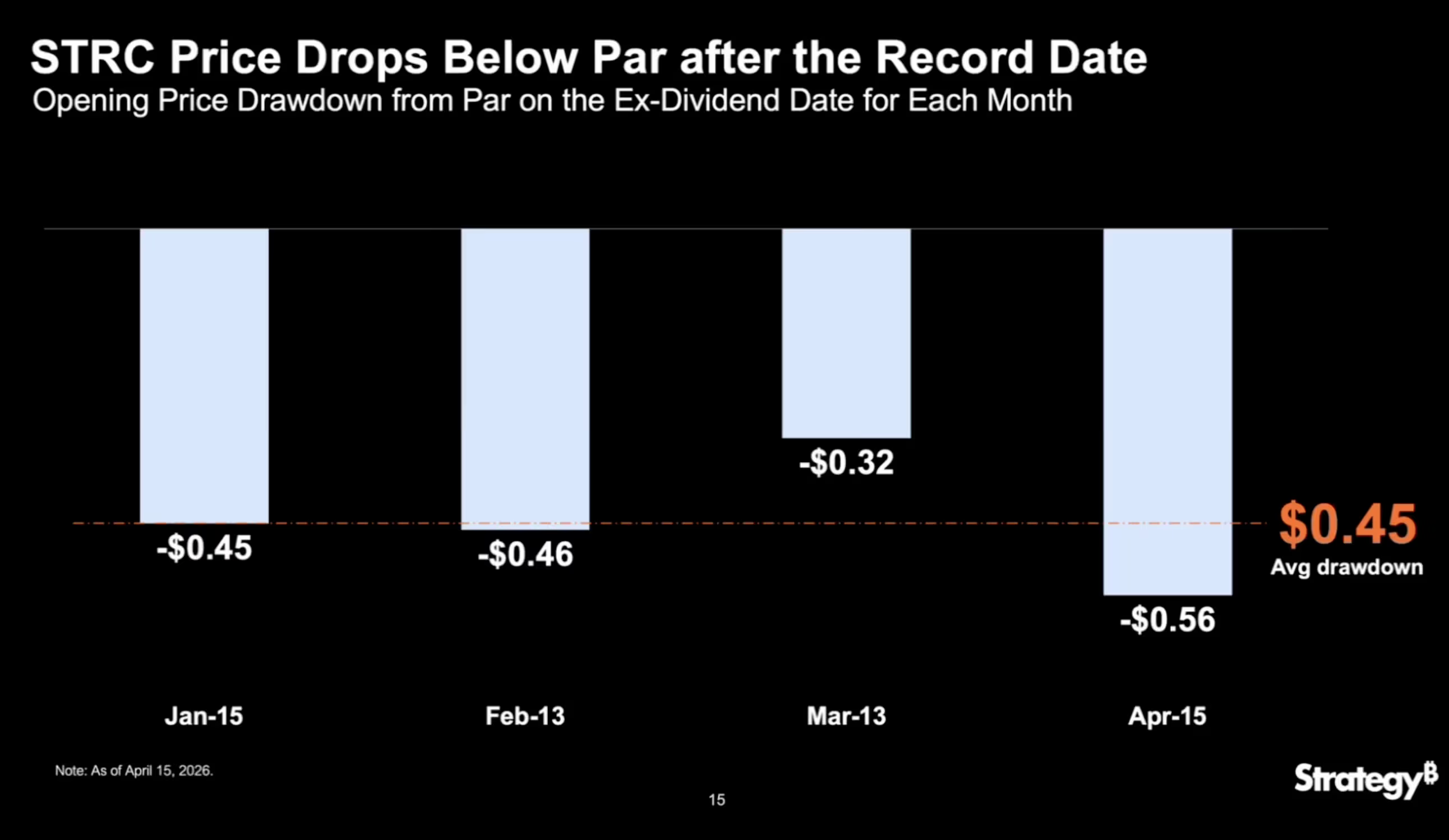

Leading bitcoin treasury company Strategy (MSTR) has proposed shifting the dividend payment schedule on its perpetual preferred equity, Stretch (STRC), from monthly to semi-monthly.

The amendment, outlined in Strategy’s investor presentation, would keep the 11.5% annualized dividend rate and total annual obligations unchanged (currently $1.2 billion). Holders would receive payouts roughly every two weeks instead of once a month, with the first semi-monthly payment expected on July 15, following the June 8 shareholder vote.

According to Strategy’s presentation, STRC currently sees an average $0.45 price drawdown after the ex-dividend date (the deadline to own a stock to receive a dividend), with recovery to its $100 par value taking around two weeks. Typically, on the ex-dividend date, the stock price drops by approximately the amount of the dividend payment.

When STRC trades below its $100 par value, Strategy cannot issue shares through its at-the-market (ATM) program to raise funds for bitcoin purchases. By smoothing the price action, the company aims to keep STRC closer to par, enabling more consistent capital raising.

Semi-monthly payments are expected to reduce this volatility and time lag.

Steadier bitcoin buying

More frequent payouts would also reduce reinvestment lag and spread out the buying pressure more evenly across the month, allowing Strategy to purchase bitcoin at a steadier pace and keep purchases consistent.

According to the presentation, the shift aligns with the typical twice-monthly U.S. payroll cycle and creates more entry and exit opportunities for shareholders, all aimed at lowering volatility.

STRC’s historical volatility averaged 13% from August 2025 to March 2026, but dropped to just 2% between March and April 2026, according to Strategy’s data.

If approved, STRC would become the only semi-monthly dividend-paying preferred in the market, compared with 921 that pay quarterly and 32 that pay monthly, the company said. Nasdaq rules require at least 10 calendar days between dividend declaration and the record date.

STRC recently fell below $99 following the April 15 ex-dividend date, a drop of more than $1, which is the volatility the company is aiming to reduce.

Disclosure: The author of this story owns shares in Strategy (MSTR).

Read more: The one metric investors are overlooking in Michael Saylor’s Strategy

Coinbase Institutional published an analysis on April 17, arguing that MicroStrategy’s persistent Bitcoin (BTC) buying reduces liquid float far more than the market appreciates.

Michael Saylor amplified the sentiment the following day, posting “Impossible to blockade Bitcoin” on X (Twitter).

Digital Asset Treasuries Squeeze BTC Float

The Coinbase analysis highlights that digital asset treasuries’ share of the BTC supply has quadrupled to above 4% over the past two years.

MicroStrategy alone now holds 780,897 BTC, making it the largest corporate Bitcoin holder globally.

That supply-tightening effect grows stronger as long-term holder accumulation rises and coins continue leaving exchanges. Strategy’s buying likely matters most when it facilitates a breakout at a key technical level.

Breakout traders, systematic funds, and momentum-driven bots can then reinforce the move.

However, Coinbase noted the price impact may be limited. Anticipated buying, ETF flows, miner supply, and derivatives hedging can all dilute MicroStrategy’s influence on any given trading session.

Saylor Reinforces Bitcoin’s Uncensorable Design

Saylor’s post aligns with his long-standing argument that Bitcoin’s decentralized architecture makes suppression futile.

The timing reinforced the narrative that corporate treasuries are accelerating Bitcoin’s entrenchment beyond the reach of any single government.

Strategy has signaled it will continue buying BTC every quarter indefinitely. The company reported a 5.6% BTC yield year-to-date for 2026.

Whether corporate treasury buying matters more through supply constriction or breakout facilitation may depend on where Bitcoin sits in its current market cycle.

The post Coinbase Says MicroStrategy’s Bitcoin Buying Tightens Supply More Than Market Expects appeared first on BeInCrypto.

Aave V3’s Wrapped Ether (WETH) reserve is carrying bad debt after attackers exploited KelpDAO’s rsETH liquid restaking token and used it as collateral to borrow against the lending protocol.

Solidity developer and auditor 0xQuit flagged the situation on X, warning depositors that the WETH pool is effectively impaired and that partial withdrawals may only become possible after Aave’s Umbrella backstop settles the deficit.

How Drained rsETH Created Bad Debt on Aave

The exploit started with an attacker funding wallets through Tornado Cash. Approximately 116,500 rsETH was drained from KelpDAO, totaling over $290 million.

The attacker then supplied the stolen rsETH as collateral on Aave V3 and borrowed a large volume of WETH against it.

Because the rsETH became unbacked after the drain, the resulting positions are effectively unliquidatable. This left Aave holding WETH obligations it cannot recover through normal liquidation.

“Wish I had better news but looks like WETH on aave is fucked. Withdraw if you can but likely too late,” warned 0xQuit, Solidity developer and auditor.

What Umbrella Means for WETH Depositors

Aave’s Umbrella system, which replaced the legacy Safety Module in late 2025, is designed for exactly this scenario.

Users who staked aWETH in the Umbrella vault face automatic slashing to cover the deficit.

Once the slashing cycle completes, remaining WETH suppliers should regain partial withdrawal access.

However, a full recovery is not guaranteed, and depositors may face a haircut on their positions.

The incident marks the first major real-world test of Umbrella’s automated bad debt coverage. It also raises fresh questions about the risks of whitelisting liquid restaking tokens as collateral on lending protocols.

Meanwhile, the Upshift team, offering non-custodial vaults for managing tokenized assets, have assured users that they do not have any exposure to rsETH.

“We are in touch with KelpDAO about a potential exploit of rsETH. As a precaution, the Kelp team have decided to temporarily pause deposits and withdrawals to the High Growth ETH and Kelp Gain vaults while their investigations take place. Upshift USDC, Core USDC and EarnAUSD vaults have zero exposure to rsETH. We will provide updates as we receive them from the Kelp team,” wrote Upshift.

The post Aave WETH Suppliers Urged to Withdraw After KelpDAO rsETH Exploit appeared first on BeInCrypto.

KelpDAO has reportedly lost more than $280 million after attackers drained positions across multiple Decentralized Finance (DeFi) protocols on Ethereum and Arbitrum.

On-chain investigator ZachXBT flagged the incident on April 18, identifying six attacker-controlled wallets actively moving the stolen funds.

How the KelpDAO Attack Happened

Blockchain data shows the attacker wallets received initial funding through Tornado Cash, the privacy mixer, hours before the theft began.

The wallets then interacted with DeFi protocols, executing token approvals and swaps through KyberSwap and KelpDAO before converting all positions into ether (ETH).

“KelpDAO appears to have had $280M+ stolen one hour ago on Ethereum and Arbitrum. The attack addresses were funded via Tornado Cash,” ZachXBT wrote on Telegram.

Within roughly one hour, the attackers consolidated approximately 75,700 ETH, worth around $178 million at current prices, into a single wallet.

The remaining stolen value includes additional tokens and positions on Arbitrum. As of publication, no outflows from the consolidation wallet had been detected.

The pattern suggests a private-key compromise rather than a smart-contract exploit in any specific protocol.

The victim appears to have held significant DeFi exposure across both chains, and the attacker systematically withdrew and swapped those positions into raw ETH.

A Growing Pattern of Whale-Targeted Attacks

The incident follows a sharp rise in phishing and social engineering attacks targeting high-value holders.

In January 2026 alone, a single phishing victim lost $284 million, accounting for over 70% of the month’s total crypto theft losses.

If confirmed at $280 million, this would rank among the largest individual wallet compromises on record.

Security analysts are expected to publish deeper on-chain analysis in the coming hours.

Elsewhere, reports also indicate that the Instagram account of Solana meme coin launchpad Pump.fun has been compromised.

“Any posts made from the official pump fun Instagram account should not be trusted. Ignore any and all posts made by the account until we have secured the account,” the team wrote.

Nevertheless, Pump.fun platforms remain operational and user funds are safe.

The post KelpDAO Loses $280 Million in DeFi Wallet Drain Across Ethereum, Arbitrum appeared first on BeInCrypto.

Crypto World

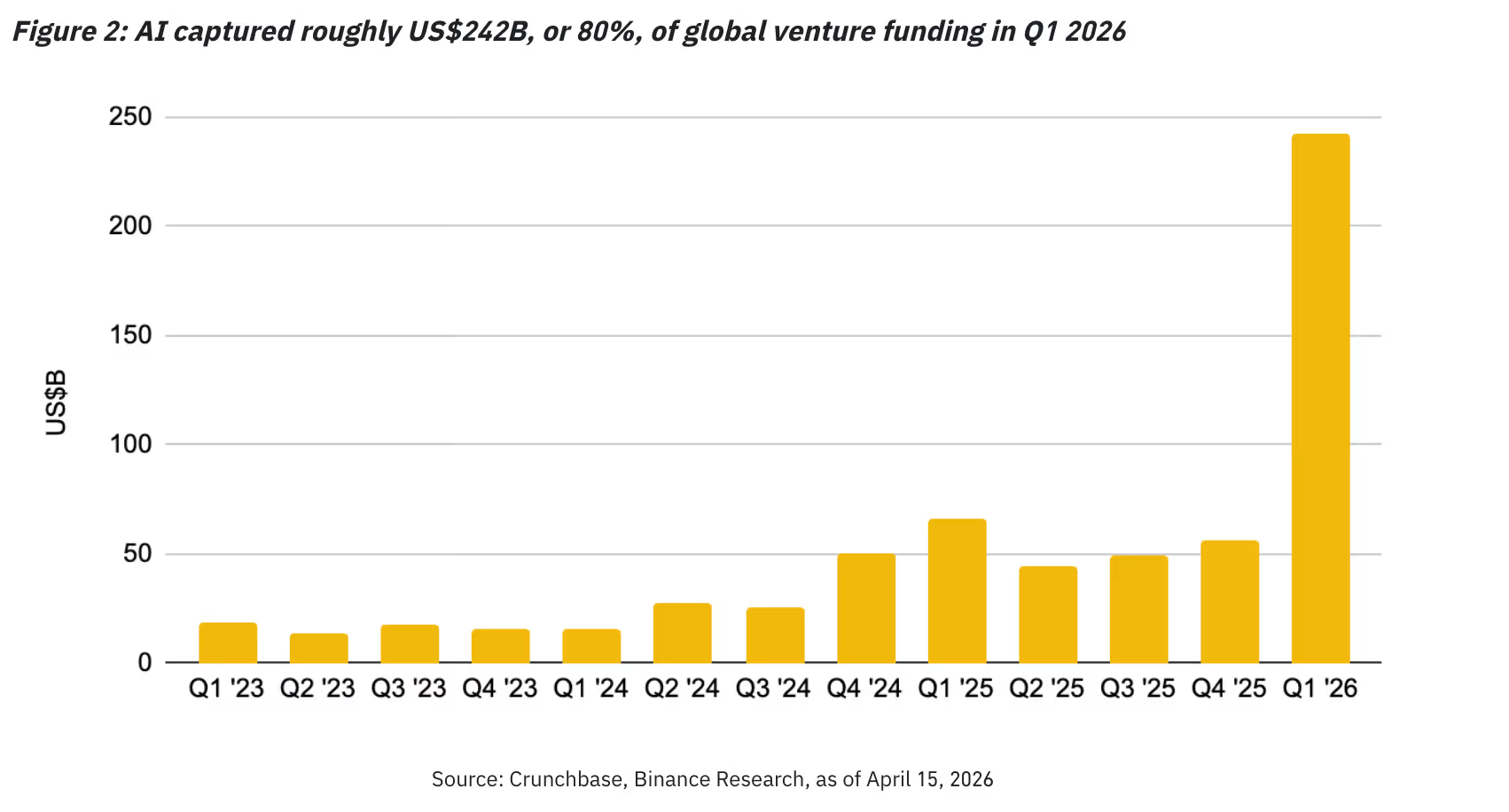

Here is how crypto firms are adapting as AI is increasingly eating into venture capital fundings

Forty cents of every venture capital dollar invested in crypto companies in 2025 went to firms building products that combine artificial intelligence and crypto, more than double the 18 cents a year earlier.

“AI is increasingly entering crypto not as a parallel narrative, but as part of crypto’s own product and infrastructure stack,” Binance Research said, citing data from Silicon Valley Bank, noting that this shows “how quickly AI is becoming embedded within crypto roadmaps.”

That pressure is visible in crypto’s shift from AI “co-pilots” to “agents.” Co-pilots help users analyze information, while agents can monitor conditions and execute actions. In trading environments, where timing affects outcomes, reducing the gap between insight and execution can change behavior.

The trend is part of a wider surge in AI spending. Crunchbase data shows AI companies raised about $242 billion in the first quarter of 2026, or roughly 80% of global venture funding. Gartner estimates total AI spending will reach $2.52 trillion this year.

Crypto leading the AI push

This trend, however, isn’t surprising.

As capital concentrates in one area, it often pulls adjacent sectors along with it, pushing firms to adapt their strategies and shorten product cycles, Binance Research wrote.

While almost all sectors are trying to incorporate AI into their business models, the report says that crypto platforms have moved faster than traditional finance in deploying such systems. This is due to support from always-on markets in the digital assets sector and programmable infrastructure, whereas TradFi faces market-hour constraints and intermediary systems that agents must pass through.

For example, the research noted that on Binance’s AI Pro beta, nearly half of the activity on a recent day, 45.7%, was triggered by the system rather than users.

These interactions came from scheduled tasks and monitoring systems, pointing to growing use of AI tools that run in the background without prompts.

Adoption of AI solutions is uneven across the 17 exchanges and brokers Binance Research surveyed. Risk management, market signals, and fraud detection are standard, while user-facing tools such as copy trading, chatbots, and portfolio advisors are present in only 47% to 71% of them.

Several major platforms have shipped agentic products this year, moving AI closer to monitoring and execution within set guardrails. That compresses the value chain between identifying an opportunity and acting on it, Binance Research added.

That means the competitive landscape will shift from who’s integrating AI features to who’s owning users’ decision-making loops, the report noted.

Iran’s government has named Bitcoin (BTC) as one of the payment options for tolls on oil shipments passing through the Strait of Hormuz, a move highlighted by observers as a clear signal of Bitcoin’s role as a neutral and strategic asset in a sanctions-driven economy. Sam Lyman, head of research at the Bitcoin Policy Institute (BPI), described the development as a notable instance where Bitcoin’s censorship-resistant properties are front and center in state-level financial decisions.

According to Lyman, the Iranian authorities chose BTC for its resilience to external interference—“No one can freeze Bitcoin. No one can shut down the Bitcoin network.” Yet he cautions that, at present, there is no on-chain evidence of BTC toll payments being executed, and Iran’s payments ecosystem remains diversified across multiple instruments, including Chinese yuan and US dollar-pegged stablecoins.

Iran’s payment mix for tolls now includes yuan, USD-pegged stablecoins, and BTC, a combination that reflects a broader push to sidestep traditional financial channels amid international sanctions. However, Lyman notes that the bulk of Iran’s crypto activity to date has been denominated in USD-backed stablecoins, underscoring how dollar-mapped liquidity remains a core part of the regime’s on-chain strategy.

In framing this development, Lyman emphasizes a broader point about how policymakers should view Bitcoin. The move illustrates why some lawmakers advocate considering Bitcoin as a strategic asset, rather than pursuing a blanket hostility toward digital assets or a dismissive stance on their utility in national finance. As the discussion around crypto and national security evolves, this incident provides a real-world data point on how a state actor contemplates the potential of censorship-resistant settlement rails.

Key takeaways

- Iran publicly designates Bitcoin as a payment option for oil tolls crossing the Strait of Hormuz, signaling a strategic use of BTC beyond speculative trading.

- Bitcoin’s censorship-resistant properties are cited as the primary rationale for its use in sovereign-level payments, according to Sam Lyman of the Bitcoin Policy Institute.

- As of now, there is no on-chain evidence confirming BTC toll payments; Iran’s crypto activity remains dominated by USD-backed stablecoins, notably USDt.

- Iran has shifted roughly $3 billion in cryptocurrencies since 2022, with the majority in stablecoins; U.S. authorities report a smaller portion of frozen assets relative to total movement, suggesting ongoing liquidity despite sanctions.

- The episode feeds into a broader policy debate about whether Bitcoin should be treated as a strategic asset by Western lawmakers and regulators, rather than being treated solely as a fringe or risk-prone technology.

Bitcoin as a strategic asset in Iran’s trade payments

Iran’s government has long pursued a formal digital asset strategy, a stance that has evolved since at least 2018. In the Hormuz toll context, Bitcoin has been positioned as a possible backbone for cross-border settlement where conventional financial channels are constrained by sanctions and geopolitical pressures. Lyman pointed out that the government’s willingness to accept BTC alongside yuan and USD-pegged stablecoins reflects a deliberate hedging of liquidity channels in a restrictive environment.

In the eye of observers, the assertion that BTC serves as a strategic asset hinges on two factors: censorship resistance and reliability under pressure. Bitcoin’s network-persistence means it cannot be unilaterally shut down by a single authority, a feature that can be appealing when traditional rails are subject to sanctions or asset freezes. Lyman underscored this logic in his discussion with Cointelegraph, framing BTC as part of a broader toolkit rather than a quick fix for all payment frictions.

Still, the practical reality remains nuanced. The Iranian government has not publicly disclosed confirmed on-chain BTC toll payments for Hormuz tolls to date. Lyman notes that while BTC is listed among accepted instruments, on-chain activity in this specific payment channel has not been evidenced publicly. This gap between the stated policy and observable transaction data highlights a common challenge in assessing the real-world use of crypto in state finance: official statements can outpace, or partially obscure, on-chain signals.

As part of the same ecosystem, the government’s stance toward stablecoins continues to be influential. USDt, a dollar-pegged stablecoin issued by Tether, has long been a dominant instrument in Iran’s on-chain activity. Lyman pointed out that the majority of crypto interactions in Iran are denominated in USDT, underscoring how dollar-denominated liquidity remains a central pillar of the regime’s digital asset operations.

“This is one of the most significant situations where Bitcoin is very clearly a strategic asset. The reason why Iran wants to use Bitcoin for these transactions is that no one can freeze Bitcoin. No one can shut down the Bitcoin network.”

The comment, attributed to Lyman, captures the core tension: Bitcoin’s perceived resilience against external controls sits alongside the practical reality that stablecoins and other instruments still dominate domestic crypto flows. BPI’s analysis, including its coverage of the Hormuz episode, also notes that a substantial portion of Iran’s on-chain activity has historically moved through USDt rather than BTC, reflecting both liquidity preferences and the regulatory environments surrounding stablecoins.

In a broader sense, the Hormuz toll framework can be read as part of a longer arc in which Iran has experimented with digital assets to bypass restrictions and diversify its financial channels. The government’s approach aligns with a multi-asset strategy rather than a single-asset solution, suggesting that BTC’s strategic prominence may emerge more from its stability of long-term censorship resistance than from its immediate transactional footprint.

Stablecoins and on-chain realities

The USDt dynamic is central to Iran’s crypto activity narrative. Lyman notes that the regime has used stablecoins extensively in its digital asset operations since the early days of the country’s crypto exploration. This preference persists despite publicized episodes in which stablecoin issuers and custodians faced enforcement actions or wallet freezes elsewhere in the ecosystem. Lyman frames this as a calculated risk, describing it as “rolling the dice” in the sense that stablecoins provide a familiar dollar proxy while carrying counterparty risk from issuers and custodians.

On the macro scale, Lyman estimates that Iran has managed to move roughly $3 billion in cryptocurrencies since 2022, with the majority denominated in stablecoins. Meanwhile, U.S. authorities have reported that only a fraction of those assets has been frozen—about $600 million—leaving a substantial portion still accessible for movement. The discrepancy between total crypto activity and frozen assets underscores how the regime has relied on the speed and flexibility of on-chain funds, particularly stablecoins, to navigate sanctions and maintain some degree of financial continuity.

These dynamics matter for policymakers and market participants alike. The use of stablecoins in sanctioned environments raises questions about enforcement reach, liquidity, and the substitution effects between different digital assets. It also highlights the ongoing importance of stablecoins in offshore and state-affiliated crypto activity, even as Bitcoin is increasingly framed as a strategic tool in high-stakes financial calculations.

For readers tracking market implications, the Hormuz development adds another layer to the evolving relationship between geopolitics and crypto liquidity. While Bitcoin’s censorship-resistant property is appealing in theory, the actual balance of assets and the on-chain evidence of toll payments remain under close watch. The Iranian case also illustrates how state actors may leverage a portfolio of instruments—BTC, yuan, and stablecoins—to preserve monetary sovereignty in a constrained environment.

More broadly, the Hormuz case invites a closer look at how Western policymakers might treat Bitcoin in national-security terms. If Bitcoin is recognized as a strategic asset, it could influence future regulatory debates and sanctions policy, potentially encouraging or discouraging certain kinds of on-chain transactions depending on their perceived strategic value and accessibility to sanctioned networks.

What to watch next

The next phase will likely hinge on whether any verifiable on-chain BTC toll transactions materialize and how policymakers and regulators adjust their framing of Bitcoin within national-security and sanctions regimes. Observers will also monitor whether Iran expands or shifts its mix of currencies for tolls and cross-border trade, and how stablecoin governance and custodial practices evolve in constrained markets. The Hormuz episode remains a critical, real-world flashpoint for understanding Bitcoin’s evolving role in geopolitical finance.

For researchers and investors, the key takeaway is that Bitcoin’s strategic value is being evaluated in state contexts, even as practical adoption and verification lag behind rhetoric. The balance between censorship resistance and regulatory risk will continue to shape how institutions, custodians, and markets perceive Bitcoin’s place in sanctioned economies.

Source note: These observations and figures are based on recent remarks from Sam Lyman, head of research at the Bitcoin Policy Institute. The Institute’s related analysis on the state of play around Bitcoin, the Strait of Hormuz, and the situation in Iran is available here: Bitcoin Policy Institute — State of Play.

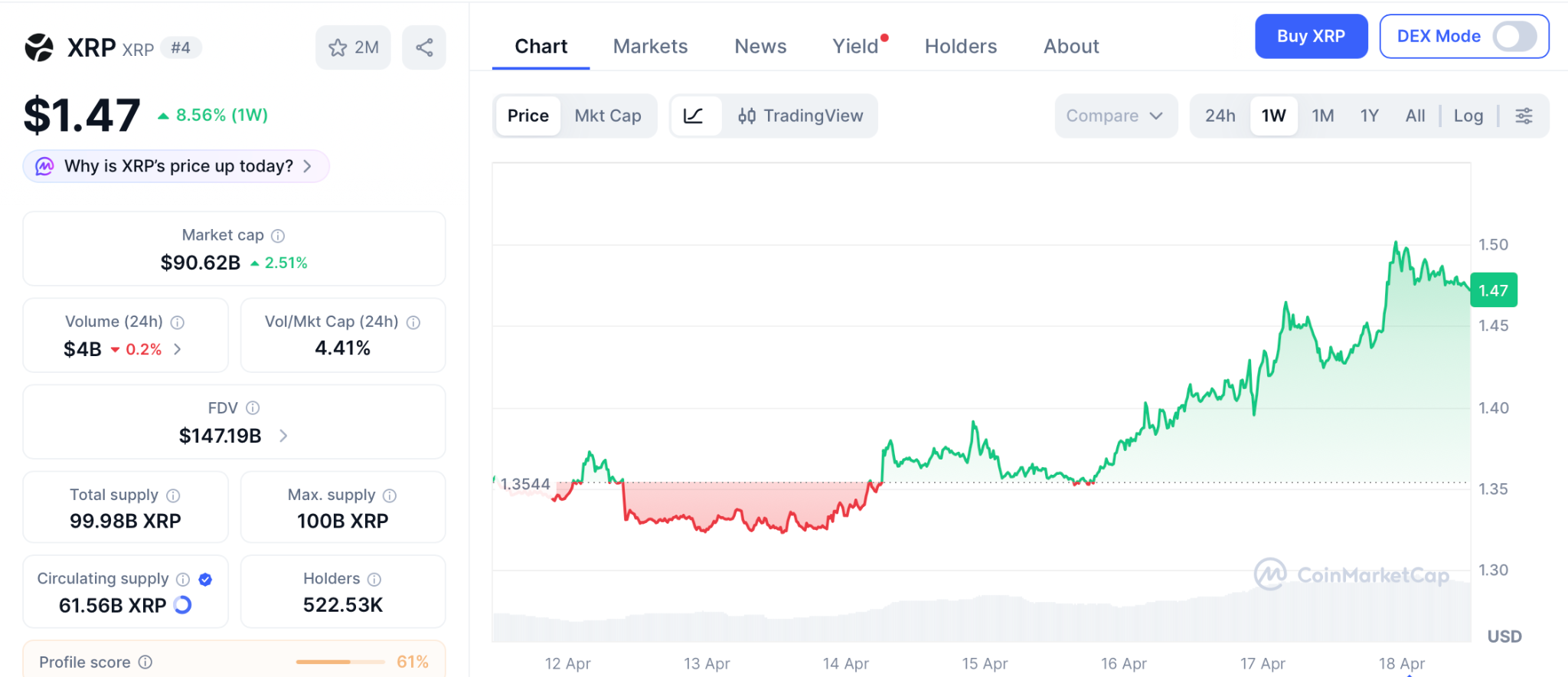

ChatGPT now targets $2.50 to $3.50 for XRP by late 2026, up to 155% upside from current levels, as Bitcoin moved past $78,000 on April 17 after the Strait of Hormuz reopened. XRP trades at $1.47 with fresh weekly inflows of $119.6 million reported by CoinShares.

The XRP price prediction from AI models keeps running ahead of price, and that gap is the exact signal that defines every cycle. While the market debates which way XRP breaks next, one presale has been pulling capital straight through the macro fog, and the numbers behind it are starting to earn their own coverage. Pepeto crossed $9.16 million at $0.0000001865 with a Binance listing closing in fast.

ChatGPT sees XRP’s first leg moving toward $1.60 to $1.85, then a push into $2.50 to $3.50 by late 2026 as ETF inflows pick up, per Yahoo Finance.

The XRP price prediction has every structural piece in place: Rakuten integrating XRP for 44 million Japanese users on April 15, the SEC CLARITY Act roundtable on April 16, and XRPL on-chain lending amendments now in validator voting per 24/7 Wall St.

But no wallet ever built generational wealth buying XRP after the forecast confirmed. The returns go to the buyers who picked the right project while $1.47 and extreme fear kept everyone else frozen.

XRP, Pepeto, and the ChatGPT Prediction Most Holders Are Missing

Pepeto Built What No Other Presale This Cycle Can Match

Crypto headlines rotate every hour, but the wallets that printed real gains keep those records on record forever. Shiba Inu turned sub-cent buys into account sizes most salaries cannot match, returning 49 million percent inside a matter of weeks. Traders who showed up two days late caught an entirely different number, while the first holders walked away with seven-digit results.

Pepeto is building the same pace regardless of where the XRP price prediction settles. Chatter on X, Telegram, and Reddit grows louder by the day, mirroring the buildup ahead of every major meme listing the market has seen.

The difference between the two projects is clear. Shiba Inu had no utility and lost 93% once the hype passed. Pepeto is built to do the opposite. Its scanner flags unsafe code before any wallet sends funds, PepetoSwap handles trades across three chains with no fees, and the bridge carries tokens between Ethereum, BNB Chain, and Solana with no gas cost.

SolidProof audited every contract before the presale accepted a single buyer. A former Binance team member manages the exchange while the builder who took Pepe to $11 billion from nothing leads development. Staking at 182% APY keeps positions growing while the Binance listing draws closer.

“Nothing in crypto pulls more attention than the meme coin space, but tokens without real products will not survive 2026. Pepe was the beginning, not the ending. Pepeto is the full vision I always carried, and with an experienced Binance engineer on the team, the exchange runs at an institutional quality,” said the cofounder behind the first Pepe coin.

XRP Price Prediction: XRP Holds $1.47 as ChatGPT Maps $3.50 Target on ETF Flows

XRP trades at $1.47 on April 17 after Bitcoin pushed past $78,000 per CoinMarketCap, with seven U.S. spot XRP ETFs now holding a combined $1 billion in AUM. Standard Chartered carries a $2.80 target while Grok sees $10 if adoption keeps accelerating.

This XRP cycle runs on a four-year rhythm. The buyers who picked the right project during fear become the names on every success list. Pepeto fills that role for 2026.

Conclusion

The XRP price prediction has ChatGPT and CoinShares inflows pointing past $2.50. News confirms big money is coming back. But returns from an $88 billion base cannot match what a presale priced in millionths of a cent can produce.

When XRP finally prints $3.50, every outlet will run the headline. Presale math produces far bigger multiples. Putting $1,000 into Pepeto today buys 5.36 billion tokens, which at a listing of $0.00005 works out to $268,000. Analysts base this target on Pepe’s all-time high, and they point out that Pepeto adds real utility Pepe never had, making a weaker result difficult to argue.

The wallets sitting on Pepeto at presale pricing carry the most one-sided return setup this cycle will produce, and the Pepeto presale is where that entry still sits open before the Binance listing sets a higher price.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What does ChatGPT predict for XRP in 2026 after the Hormuz reopening?

ChatGPT targets $2.50 to $3.50 for XRP by late 2026 per Yahoo Finance, up to 155% upside. Seven spot XRP ETFs now hold $1 billion in combined AUM.

Is XRP or Pepeto the better buy right now before the next rally?

Pepeto pairs a SolidProof audit, zero-fee exchange, cross-chain bridge, and contract scanner built by the Pepe cofounder and a senior Binance developer. The presale holds $9.16M at $0.0000001865 with 182% APY and a confirmed Binance listing.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Iran’s government naming Bitcoin (BTC) as a payment method for oil ships crossing the Strait of Hormuz highlights its role as a neutral, strategic asset, according to Sam Lyman, head of research at digital asset advocacy organization Bitcoin Policy Institute (BPI).

The government selected BTC as one of the payment methods for the tolls because of its censorship-resistant qualities, Lyman told Cointelegraph. He said:

“This is one of the most significant situations where Bitcoin is very clearly a strategic asset. The reason why Iran wants to use Bitcoin for these transactions is that no one can freeze Bitcoin. No one can shut down the Bitcoin network.”

Iran is accepting oil tolls in Chinese yuan, US dollar-pegged stablecoins and BTC. However, there is “no onchain evidence” of a BTC toll payment so far, Lyman said, adding that the “majority” of Iran’s crypto transactions are denominated in US dollar stablecoins.

The announcement from the Iranian government highlights why US lawmakers should recognize and treat Bitcoin as a strategic asset, rather than taking a hostile regulatory stance toward it or dismissing digital assets altogether, Lyman told Cointelegraph.

Related: Bitcoin community weighs in on reports of Iran’s crypto toll for oil ships

Stablecoin confiscation is just a cost of doing business

“Iran has had a digital asset strategy for several years, going back to about 2018, and the majority of transactions that take place there are with USDt,” (USDT), Lyman said. USDt is a dollar-pegged stablecoin issued by the company Tether.

The Iranian government is using stablecoins, despite the ability of stablecoin issuers to freeze wallets, he said. “I think they’re rolling the dice,” Lyman told Cointelegraph.

He said that the Iranian government has been able to shift about $3 billion in cryptocurrencies since 2022, with the “majority” of that value denominated in stablecoins.

However, the US Treasury Department was only able to freeze about $600 million in assets, according to Lyman.

“They were able to move $3 billion, and only have $600 million frozen. They were still able to move about $2.4 billion. So, I think that’s why stablecoins are still a go-to for the regime,” he said.

Magazine: Big Questions: Can Bitcoin save you from the dreaded Cantillon Effect?

TLDR:

- Wallet 0x524, linked to Ondo Finance, transferred nearly 20M ONDO tokens across two separate destination wallets.

- Whale wallets 0x807 and 0x61d moved 2.84M ONDO from Coinbase Hot Wallet to Custody, signaling long-term holding intent.

- Wallet 0xFC9, flagged as a long-time associate wallet, received 4.9M ONDO tokens in a potential sell-off move.

- Ondo Finance crossed $800M in tokenized stock TVL, yet growing project success may increase VC and team profit-taking pressure.

ONDO token activity has attracted attention after a wallet linked to Ondo Finance moved nearly 20 million tokens.

On-chain data captures two outgoing transfers to separate destination addresses. At the same time, two whale investors moved a combined 2.84 million tokens off Coinbase Hot Wallet to Coinbase Custody.

These events come as Ondo Finance crossed $800 million in tokenized stock total value locked, marking a notable project milestone.

Large Transfers From Project-Linked Wallet Raise Sell-Off Concerns

Wallet 0x524, connected to Ondo Finance, transferred approximately 15 million ONDO tokens to multi-sig wallet 0x611.

That movement carried an estimated value of $3.95 million at the time of the transfer. The multi-sig structure of the destination wallet generally points to a more controlled custody setup.

Shortly after, 4.9 million ONDO tokens, worth around $1.29 million, moved to wallet 0xFC9. On-chain analyst Nazoku flagged this transfer on social media, describing 0xFC9 as a long-time associate wallet. The analyst noted the transfer to that wallet could be connected to a potential sell-off.

Together, both outflows account for nearly 20 million tokens leaving wallet 0x524 within a short period. Transfers of this size from project-affiliated wallets often draw quick attention from traders and market watchers.

Such movements are frequently interpreted as potential signs of incoming sell pressure. Such moves by core-affiliated wallets are hard to ignore when they happen close together.

This kind of activity can weigh on token sentiment, regardless of project fundamentals. Whether wallet 0xFC9 proceeds with a sell-off has not yet been confirmed. Market participants are closely watching both wallets for any further movement.

Whale Accumulation and $800M TVL Reflect Long-Term Market Confidence

On the other hand, two whale wallets moved 2.84 million ONDO tokens from Coinbase Hot Wallet to Coinbase Custody.

Moving assets to Custody is widely viewed as a long-term holding signal rather than short-term trading. Nazoku flagged this activity alongside the outflow report.

Whale 0x807 acquired 1.7 million tokens valued at around $458,000. Whale 0x61d withdrew 1.14 million tokens worth approximately $314,400 in the same period.

Both whales reportedly plan to hold their positions unless the token price gains at least 50%. This approach is common among investors who hold a high-conviction view on an asset.

Ondo Finance also reported that its tokenized stock TVL has crossed the $800 million mark. The project works within the real-world asset sector, an area that has drawn steady institutional interest. This figure reflects growing on-chain demand for tokenized financial instruments.

However, a growing TVL can also give venture capital backers and team members more reason to realize profits. As Nazoku pointed out, this creates a persistent selling force on ONDO that offsets positive project news.

The on-chain picture remains mixed, with profit-taking and accumulation happening side by side.

The online gambling market has shifted quickly over the past few years. What was once dominated by a handful of big-name operators is now a crowded space where players actively search for alternatives that better fit how they want to play. FanDuel remains one of the most recognized names in the industry, but search data and player forum activity suggest that a growing number of users are looking beyond established brands. Among the platforms drawing attention is ZunaBet, a crypto-first casino and sportsbook that launched in 2026 with a feature set designed to appeal to a different kind of player.

FanDuel: The Established Name

FanDuel built its reputation through daily fantasy sports before expanding into sports betting and online casino gaming. It operates legally in multiple US states and holds licenses from well-known regulatory bodies. The platform offers a solid sportsbook, a reasonable selection of casino games, and regular promotions tied to major sporting events.

For many players, FanDuel is a safe and familiar choice. It processes payments through traditional methods like bank transfers, credit cards, and PayPal. Its mobile app is polished, and its brand recognition is high thanks to years of advertising spend and partnerships with major sports leagues.

That said, FanDuel’s strengths also reflect its limitations. Its casino game library, while decent, is smaller than what some competitors now offer. Its loyalty and rewards structure is fairly standard. And its reliance on traditional payment rails means players deal with processing times and fees that have become a growing point of frustration, especially among younger users who are comfortable with cryptocurrency.

ZunaBet: The New Challenger

ZunaBet launched in 2026 and has quickly positioned itself as one of the more ambitious new entries in the crypto casino space. It is owned by Strathvale Group Ltd and operates under an Anjouan gaming license. The team behind the platform has over 20 years of combined experience in the gambling industry, which shows in the scale of its launch.

The numbers are hard to ignore. ZunaBet offers over 11,294 games from 63 providers, including well-known names like Pragmatic Play, Hacksaw Gaming, Evolution, Yggdrasil, and BGaming. That puts its library among the largest in the crypto-focused market. The game selection covers slots, RNG table games, and live dealer tables, giving players a full casino experience without needing to visit multiple platforms.

Beyond the casino, ZunaBet runs a full sportsbook covering football, basketball, tennis, NHL, esports titles like CS2, Dota 2, League of Legends, and Valorant, plus virtual sports and combat sports. This makes it a genuine hybrid platform rather than a casino with a sportsbook bolted on as an afterthought.

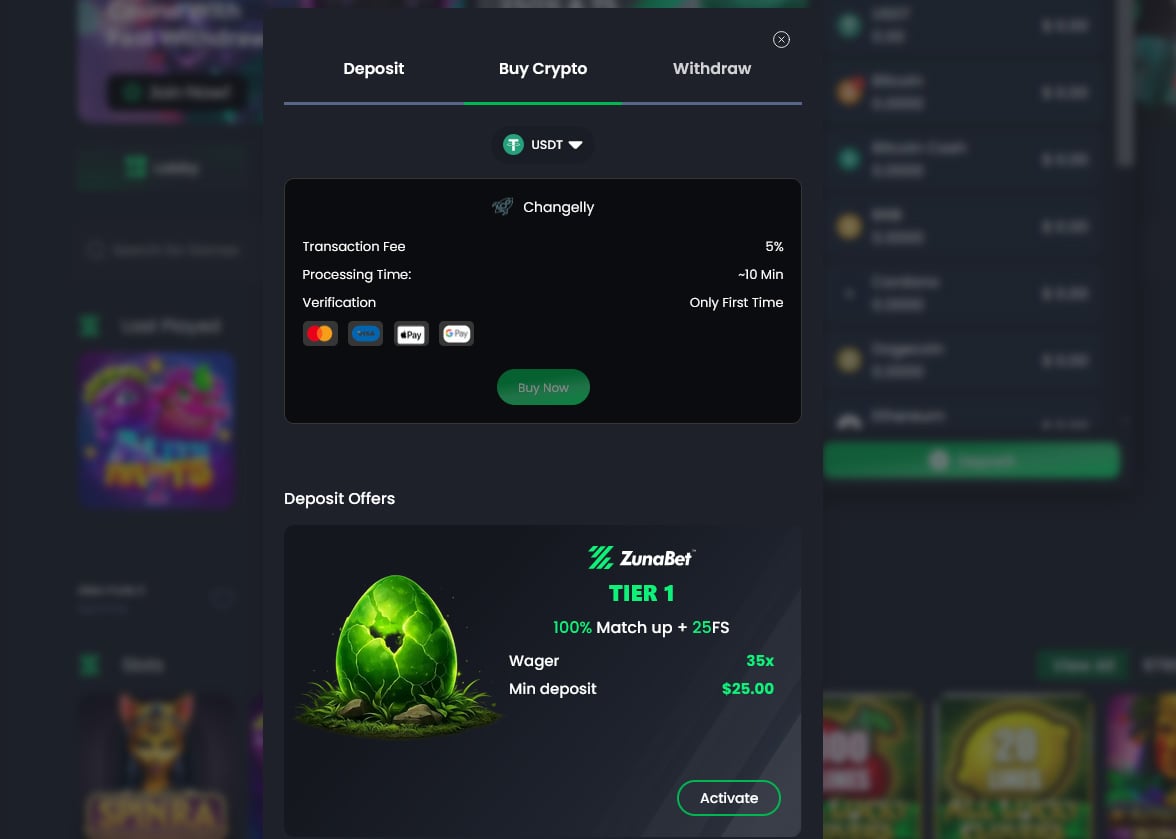

The platform supports over 20 cryptocurrencies including Bitcoin, Ethereum, USDT across multiple chains, Solana, Dogecoin, Cardano, and XRP. It charges no platform processing fees and emphasizes fast withdrawals, which directly addresses one of the most common complaints players have about traditional operators.

ZunaBet also offers dedicated apps for iOS, Android, Windows, and MacOS, along with 24/7 live chat support. Its interface uses a dark theme with fast loading speeds and responsive design, built on modern HTML5 technology.

Crypto vs Traditional Platforms

The divide between crypto and traditional gambling platforms is becoming one of the defining trends in the industry. Traditional platforms like FanDuel rely on bank transfers, cards, and e-wallets. These methods work, but they come with processing delays, fees, and identity verification steps that some players find cumbersome.

Crypto platforms like ZunaBet take a different approach. Transactions settle faster because they run on blockchain networks rather than through banks. There are no platform processing fees, and the range of supported currencies gives players flexibility that traditional operators simply do not match. For players who already hold cryptocurrency, this removes friction from the deposit and withdrawal process entirely.

This matters more than it might seem on the surface. A player who wins on a Friday night at a traditional casino might wait several business days for a withdrawal to clear. On a crypto platform, that same withdrawal can process in minutes. For a growing segment of the market, that speed and simplicity is not just a nice feature. It is the baseline expectation.

The broader trend is clear. As cryptocurrency adoption continues to grow globally, platforms built around crypto from the ground up have a structural advantage over those trying to add it as an afterthought. ZunaBet was designed as a crypto-first platform from day one, and that shows in how deeply cryptocurrency support is integrated into every part of the experience.

Loyalty Programs: Standard Points vs Gamified Progression

Loyalty programs are another area where the gap between old and new approaches is widening. Most traditional operators, including FanDuel, use point-based systems where players earn rewards through wagering volume. These programs work, but they tend to feel generic and do little to create genuine engagement beyond the transactions themselves.

ZunaBet has taken a different route with its dragon evolution loyalty system. The program has six tiers — Squire, Warden, Champion, Divine, Knight, and Ultimate — each tied to a mascot called Zuno that evolves as players progress. Rakeback starts at 1% and scales up to 20% at the highest tier. Benefits include tier-based free spins up to 1,000, VIP club access, and double wheel spins.

The gamified structure is a deliberate design choice. It borrows from the progression systems that players are already familiar with from video games, making the loyalty experience feel like part of the entertainment rather than a separate accounting exercise. For players who grew up with gaming, this approach feels natural in a way that traditional point systems do not.

A Platform Built for What Comes Next

The rising search interest in FanDuel alternatives reflects a broader shift in what players want. The established operators built their businesses around traditional payment methods, standard loyalty programs, and regulated US markets. They do those things well. But the market is not standing still.

ZunaBet represents a different model. It combines a massive game library, a full sportsbook with esports coverage, crypto-native payments, and a loyalty system that feels more like a game than a rewards card. It is built for players who expect speed, variety, and an experience that matches how they interact with technology everywhere else in their lives.

None of this means FanDuel is going away. It remains a strong platform with clear advantages in regulated US markets. But for the growing number of players who want something different, something faster, and something that feels like it was built for them rather than adapted from an older model, platforms like ZunaBet are where the energy is right now.

The online gambling industry has always moved toward whatever gives players more choice, more speed, and more reasons to stay engaged. Right now, that momentum is pointing toward crypto-first platforms with bigger libraries and smarter loyalty systems. ZunaBet is at the front of that wave, and the search data suggests players are paying attention.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

‘Wear my heart on my sleeve:’ Robert MacIntyre discusses his Masters meltdown

Nvidia’s Jensen Huang warns DeepSeek running on Huawei chips would be ‘horrible outcome’ for America

#reseller #business #antique #jewelry #fyp #money #gold #ytshorts

-

NewsBeat6 days ago

NewsBeat6 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Crypto World5 days ago

Crypto World5 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Politics6 days ago

Politics6 days agoWorld Cup exit makes Italy enter crisis mode

-

Fashion1 day ago

Fashion1 day agoWeekend Open Thread: Theodora Dress

-

Crypto World5 days ago

Crypto World5 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos4 days ago

News Videos4 days agoSecure crypto trading starts with an FIU-registered

-

Sports1 day ago

Sports1 day agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World5 days ago

Crypto World5 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

NewsBeat4 days ago

NewsBeat4 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Politics24 hours ago

Politics24 hours agoPalestine barred from entering Canada for FIFA Congress

-

NewsBeat7 days ago

NewsBeat7 days agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Crypto World22 hours ago

Crypto World22 hours agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Sports5 days ago

Sports5 days agoNWFL opens Pathway for new Clubs ahead of 2026 Season

-

Business2 days ago

Business2 days agoCreo Medical agree sale of its manufacturing operation

-

Sports7 days ago

Dexter Lawrence, Stefon Diggs, Trading for De’Von Achane

-

Crypto World6 days ago

Crypto World6 days agoTrump whales load up ahead of Mar-a-Lago luncheon.

-

Crypto World6 days ago

Sei Network Enters Quiet Reset Phase as On-Chain Metrics Signal a Slowdown in 2026

-

Business6 days ago

Kering slides after Morgan Stanley downgrade, Gucci woes loom

-

Tech6 days ago

Tech6 days agoGoogle adds E2E encryption to Gmail for iOS and Android enterprise users

-

Entertainment5 days ago

Entertainment5 days agoKarol G’s ‘Ultra Raunchy’ Coachella Set Gave ‘Satanic Vibes’

You must be logged in to post a comment Login