Crypto World

Aster Testnet Launches; Mainnet Rollout and New Features Coming in Q1

TLDR

- Aster’s layer-1 blockchain testnet is now live for all users, marking a key milestone for the platform.

- The Aster team plans to launch the mainnet in the first quarter of 2026.

- New features, including fiat currency on-ramps, will be introduced in Q1 2026.

- Aster will release its code for developers, fostering ecosystem growth and innovation.

- The platform’s shift to a perpetual futures DEX positions it as a competitor to Hyperliquid.

Aster, a decentralized crypto exchange (DEX) and perpetual futures platform, has announced the launch of its layer-1 blockchain testnet. The testnet is now available to all users, with the mainnet rollout scheduled for the first quarter of 2026. This major milestone is part of the company’s ambitious plans to enhance its platform and expand its offerings.

Aster’s Upcoming Features and Q1 2026 Launch Plans

Aster’s roadmap for 2026 includes several key developments that will significantly enhance its services. The introduction of fiat currency on-ramps will allow users to seamlessly convert their traditional currency into digital assets. Along with this, Aster will release its code for developers, enabling third-party builders to contribute to the platform’s growth.

The upcoming Aster layer-1 mainnet is designed to improve the platform’s efficiency and scalability. It will also serve as the backbone for future features and expansions. These developments are expected to increase Aster’s appeal to both traders and developers, fostering a more vibrant ecosystem.

In March 2025, Aster rebranded as a perpetual futures DEX. This move positioned the platform as a competitor to Hyperliquid, another prominent perpetual futures DEX. Hyperliquid operates on its own application-specific blockchain network, highlighting the trend of Web3 projects developing custom layer-1 blockchains for high-throughput transactions.

Aster’s decision to launch its own layer-1 blockchain aligns with this growing trend. It reflects the increasing demand for specialized blockchains that can handle high transaction volumes. By moving away from general-purpose chains like Ethereum and Solana, Aster aims to provide a more tailored and efficient solution for its users.

Surge in Perpetual Futures Trading Volume and Market Growth

The perpetual futures market saw a sharp rise in trading volume during 2025. According to DefiLlama, the cumulative trading volume nearly tripled, growing from approximately $4 trillion to over $12 trillion by the year’s end. About $7.9 trillion of this volume was generated in 2025, signaling increasing interest in crypto derivatives.

Monthly trading volumes hit the $1 trillion mark in October, November, and December. This surge highlights the growing demand for perpetual futures contracts, which allow traders to keep positions open without expiration dates.

Monero (XMR) has reached its 12-year milestone since its launch in 2014.

Summary

- Monero celebrates 12 years since launch in 2014 as leading privacy-focused cryptocurrency network.

- Network hides sender, receiver, and amount using cryptographic tools like Ring Confidential Transactions.

- Despite over 70 exchange delistings, Monero maintains active users and steady market participation.

The project has positioned itself as a privacy-focused cryptocurrency designed to hide transaction details on a public blockchain.

On April 18he project marked the occasion with a public message shared on X. The team stated “we’re celebrating our 12th birthday today” while thanking users for continued support of privacy-focused transactions.

Monero has maintained its position as one of the leading privacy coins in the digital asset sector over the years, focusing on confidentiality in transfers.

Monero was built to address transparency found in other blockchain networks. Unlike Bitcoin, where transactions are publicly visible, Monero hides sender, receiver, and transaction amounts.

The network uses technologies such as Ring Confidential Transactions and stealth addresses. These tools are designed to prevent linking transactions to specific users or wallet balances.

The system also ensures that coins cannot be traced through transaction history. This design aims to prevent tracking of individual units across the network.

Moreover, Monero has faced ongoing regulatory scrutiny due to its privacy features. Over the years, several exchanges have removed the token from their platforms.

Reports suggest the token has experienced more than 70 delistings across different jurisdictions. Despite this, trading activity and user participation have continued across alternative platforms and peer-to-peer markets.

The project has remained active through a global developer and user community that continues to maintain and update the protocol.

Development Activity and Market Performance

Monero developers are currently working on upgrades, including a planned FCMP++ update aimed at improving network performance and privacy features.

Interest in privacy coins has shown periodic changes in market cycles. Monero experienced renewed attention earlier this year alongside movements in other privacy-focused assets such as Zcash.

At the time of reporting, Monero trades near $351 with a market capitalization of about $6.47 billion (per CoinGecko’s data). The asset has recorded short-term gains over recent trading sessions, with modest increases in both daily and weekly performance.

TLDR:

- A $292M rsETH exploit enabled massive borrowing on Aave, leaving the protocol with unbacked collateral exposure.

- Aave’s ETH pool reached full utilization, restricting withdrawals as panic-driven outflows exceeded $5.4 billion.

- Technical indicators show AAVE weakening after rejection near $120, with momentum still favoring downside pressure.

- Critical support near $90 remains under watch as markets assess stability following one of 2026’s largest DeFi events.

Aave’s lending markets faced acute stress after a large exploit tied to Kelp DAO triggered a liquidity crunch. The incident drained hundreds of millions in assets and pushed Aave’s ETH pool to full utilization, limiting withdrawals across the protocol.

Liquidity Crunch Follows Kelp DAO Exploit

A sudden exploit involving Kelp DAO’s rsETH token triggered widespread concern across decentralized finance markets.

The attacker reportedly drained 116,500 rsETH, valued at about $292 million, from a LayerZero bridge. The stolen assets were then deployed in a strategy that strained Aave’s liquidity.

According to Coin Bureau, the attacker deposited the compromised rsETH as collateral on Aave V3. This move allowed the borrowing of nearly $236 million in wrapped ETH.

However, the rsETH backing those positions is now considered invalid, leaving the loans without proper collateral support.

As a result, Aave is facing an estimated $280 million in unrecoverable debt. The protocol’s ETH pool reached 100% utilization, meaning nearly all available liquidity has been borrowed. Users attempting to withdraw ETH encountered delays or were unable to exit positions.

Market reaction was swift, with large-scale withdrawals reported across the platform. Data suggests over $5.4 billion in ETH outflows occurred خلال the panic phase. High-profile withdrawals added to the pressure, including a reported 65,584 ETH withdrawal by Justin Sun.

This situation marks a major stress event for Aave’s risk management systems. It also serves as a real-time test for its Umbrella safety module, which is designed to handle extreme conditions. The unfolding events continue to draw attention across the crypto sector.

AAVE Price Faces Pressure After Failed Rally

Market data shows that AAVE experienced a sharp rejection after attempting a breakout toward the $115–$120 range. The price has since retreated to around $93.90 on the 4-hour chart. Despite a modest recovery within the session, broader momentum remains weak.

Earlier price action reflected a steady decline from the $120 region toward $90 levels. This phase was followed by a period of sideways consolidation between $92 and $102. The recent rally attempt failed to hold, leading to renewed selling pressure.

Technical indicators show a bearish short-term structure. The Relative Strength Index is currently at 34.55, approaching oversold territory but not fully there. Its position below the moving average suggests continued downward momentum.

At the same time, the MACD indicator remains in negative territory. The widening histogram signals sustained selling activity, with no clear crossover indicating a reversal yet. This aligns with the broader price rejection seen on the chart.

Key support is now concentrated around the $90 level, with $89.50 acting as a critical breakdown point. If this zone fails, the next downside targets could fall between $85 and $80. On the upside, resistance remains firm near $100 and higher around $110.

Traders are closely monitoring whether the price can stabilize above the current support levels. A rebound would require improving momentum signals and renewed buying activity. Until then, the market structure continues to reflect caution following the recent exploit.

TLDR:

- PEPE remains within a strong weekly demand zone, signaling possible accumulation despite an 88% correction from highs.

- A breakout above $0.000006 resistance could confirm trend reversal and open room for major upside targets.

- Historical fractal patterns suggest potential for explosive rallies if the current support structure holds steady.

- Failure to hold above $0.0000017 may invalidate the bullish setup and extend consolidation further.

PEPE traded near a major support zone after a steep correction, with price stabilizing around $0.00000376. The weekly structure showed a potential re-accumulation phase forming, as traders monitored whether the current demand area could sustain a recovery.

Weekly Accumulation Zone Draws Market Attention

The latest chart showed PEPE sitting within a high-confluence support region formed by a fair value gap, order block, and horizontal demand. This area ranged between $0.0000030 and $0.0000018, where price activity remained steady.

A tweet from Crypto Patel described this setup as a rare fractal structure, noting similarities with a previous accumulation phase. The post referenced a past 4,515% move that followed a similar pattern during the earlier cycle.

Price data confirmed that the current level aligned with historical consolidation zones before large upward expansions. The chart also showed price maintaining position above the lower boundary, which remained critical for structural stability.

At the same time, the analysis noted that invalidation would occur below $0.0000017. Holding above this level kept the accumulation structure intact, while a breakdown could shift the market into a deeper consolidation phase.

Resistance Levels and Price Structure Define Next Move

The chart marked a key resistance zone near $0.000006 to $0.000007123, where previous support turned into resistance. Price attempts to reclaim this level, which had failed during earlier retests following the breakdown.

Trendline analysis showed that two ascending supports were broken before the decline accelerated. Each breakdown was followed by rejection, forming a consistent pattern of lower highs across the weekly timeframe.

The chart also presented projected upside targets if the price breaks and holds above resistance. These targets ranged between $0.000028 and $0.0001, based on earlier expansion patterns.

At the same time, historical data showed projected moves of 3,079% and 5,592% during bullish cycles. These projections aligned with prior market behavior observed during strong upward phases.

Current price action remained below resistance, keeping the structure within a defined range. Short-term movement showed minor upward attempts, although no confirmed breakout had formed.

The chart also showed an 88.99% correction into the current zone, reflecting deep pullbacks seen in previous cycles. This retracement brought the price back into a demand area where accumulation had occurred before.

Traders continued to watch whether the price could reclaim the resistance level and confirm a shift in structure. Until then, the market remained within a consolidation phase defined by support holding and resistance capping upward movement.

Three wallets, one denial, and $5.7 billion in market cap gone in 48 hours.

RaveDAO’s RAVE crashed 90% over 24 hours as crypto exchanges Binance and Bitget opened investigations into the trading activity that catapulted the token to a $6 billion market cap last week.

Bitget CEO Gracy Chen confirmed the probe on X, and Binance co-CEO Richard Teng subsequently said the exchange was reviewing the matter and would “always” do its part to examine signs of market misconduct. Gate.io was also named in the original allegations from onchain investigator ZachXBT, who has offered a $25,000 bounty for whistleblowers with evidence of the parties involved.

The collapse accelerated after the project’s Saturday denial rather than stabilizing on it.

RaveDAO posted a six-part X thread stating the team “is not engaged in, nor responsible for, recent price action.”

The thread did not address any of the specific onchain allegations that prompted the scrutiny, including the concentration of roughly 90% of the 1 billion RAVE supply across three Gnosis Safe multi-signature wallets attributed to the team, or the millions of tokens transferred to exchanges shortly before the rally began.

The original rally took RAVE from about $0.25 to $27.33 in nine days, a 10,800% move that triggered $44 million in liquidations on Friday, just behind bitcoin and ether, with the bulk of them from short sellers positioned against the token.

Investigators flagged a “bait and liquidate” pattern in which visible token transfers to exchanges suggested incoming sell pressure, drawing traders into short positions before those tokens were withdrawn and prices ripped higher, forcing shorts to cover at progressively worse levels.

RaveDAO presents itself as a Web3 entertainment platform offering onchain ticketing for electronic music events, tracing its origins to a 2023 Istanbul afterparty. The project reported about $3 million in 2025 revenue and lists partnerships with Binance, OKX, Bitget, and Polygon.

RaveDAO’s thread did confirm the team plans to “liquidate portions of unlocked tokens” when appropriate to fund operations and marketing, and said it was “exploring appropriate models, including price-triggered or performance-triggered locks, that tie team incentives to ecosystem growth.”

It did not commit to any specific lockup mechanism or timeline, however.

Crypto World

Grayscale Files Spot TAO ETF as Bittensor Network Rebounds from Covenant AI Exit and 38% Drawdown

TLDR:

- Grayscale raised TAO weighting to 43.06% in its AI fund, its largest single-asset reallocation ever made.

- Community miners restored SN3, SN39, and SN81 from open-source code with no central operator involvement needed.

- Bitwise and Grayscale both filed TAO ETF applications on April 2, with an SEC decision tracked for August 2026.

- Teutonic targets a 1-trillion-parameter training run in May, timed with the ETF’s peak SEC review window.

Bittensor proved antifragile after a 38% drawdown triggered by Covenant AI’s sudden exit from three major subnets. Community miners restored SN3, SN39, and SN81 entirely from open-source code, with no central operator involved.

Around 70% of supply remained staked throughout the disruption. Spot outflows exceeded $70 million on multiple consecutive days after the crash.

Grayscale’s spot TAO ETF filing and a series of protocol upgrades are now drawing renewed attention to $TAO’s recovery case.

Grayscale’s ETF Filing and Institutional Moves Signal Confidence in Bittensor

Grayscale raised its TAO weighting to 43.06% inside its AI fund on April 7. That move marked the largest single-asset reallocation the fund has ever executed.

It came three days before the Covenant crash became public. The timing led observers to conclude that Grayscale had been running independent structural analysis on the network.

On April 2, Grayscale filed an S-1 Amendment for a spot TAO ETF on NYSE Arca. Bitwise filed a parallel TAO strategy ETF on the same day.

The SEC decision window is currently tracked for August 2026. However, market analysts note the repricing may not wait for formal approval.

Crypto analyst @Karamata2_2 pointed to Bitcoin and Ethereum as precedents for pre-approval price movement. Both assets moved significantly during their respective SEC review windows.

That pattern places the current filing period as a meaningful near-term catalyst. The $218–$240 demand zone remains the key structural level for $TAO to hold.

Supporting the institutional picture, GeneralTensor closed a $5 million funding round in March. The round was anchored by a Goldman-backed fund, with DCG also participating.

The TAO Institute launched on April 15 with a dedicated subnet risk index. Together, these moves reflect sustained institutional engagement despite the recent network turbulence.

Protocol Upgrades and Active Subnets Reinforce Bittensor’s Antifragile Case

BIT-0011, the Conviction Mechanism, is a core protocol upgrade shaping Bittensor’s next phase. Subnet founders and stakers lock alpha tokens to earn conviction scores across 30-day intervals.

The staker holding the highest score gains ownership of the subnet. Tokens locked during the active period cannot exit until the interval concludes.

The community restart of SN3, SN39, and SN81 without founder intervention served as a real stress test. Chain emissions and ownership routing continued without interruption throughout that period.

Karamata2_2 described the outcome as the best live demonstration of antifragility the network could have produced. BIT-0011 formalizes that model at the protocol level going forward.

Teutonic, formerly Templar, is targeting a 1-trillion-parameter decentralized training run for mid-to-late May. Should that milestone land during the ETF application’s most visible SEC review window, attention may return sharply.

The narrative shifts from a network that survived its biggest blowup to one that is still actively scaling. That framing matters most precisely because Covenant’s exit raised doubts about the technology’s depth.

Active subnets continue producing measurable output across the ecosystem. Chutes AI accounts for 14.39% of daily emissions and processes over 50 billion tokens per day, with a revenue-funded buyback already live.

TargonCompute co-authored an Intel TDX whitepaper and projects $10.4 million in ARR. With 128 active subnets expanding toward 256 and a subnet alpha market cap near $1.03 billion, Bittensor’s operational picture remains intact.

Crypto World

President Trump accuses Iran of ceasefire breach as Bitcoin reacts to market uncertainty

U.S. President Donald Trump has accused Iran of breaching a ceasefire agreement.

Summary

- Trump accused Iran of ceasefire violation following reports of activity in Strait of Hormuz.

- Iran denied allegations and claimed United States actions breached agreement under international law frameworks.

- Bitcoin price showed volatility, dropping from recent highs amid rising geopolitical uncertainty and market caution.

The claim follows reports that Iran opened fire in the Strait of Hormuz during the truce period.

Trump described the situation as a “serious violation” and warned that further action could follow if negotiations fail. He stated ”it will happen, one way or another” while referring to ongoing efforts to reach a resolution.

Despite the tension, Trump indicated that discussions are still active. He expressed confidence that a deal could be reached before the ceasefire deadline set for April 22.

Iranian officials responded by rejecting the accusations and placing blame on the United States. A spokesperson from Iran’s Ministry of Foreign Affairs stated that U.S. actions had breached the terms of the ceasefire.

The spokesperson said ”the blockade of ports is unlawful and violates international law” in a statement shared publicly. The response also referenced international legal frameworks, including provisions under the United Nations Charter.

Iran’s statement described the situation as escalating tensions rather than a one-sided breach. Both sides have continued to exchange claims, adding to uncertainty around the ceasefire status.

Bitcoin Price Reacts to Geopolitical Developments

Bitcoin has shown price movement in response to the developments. The asset declined from around $76,300 to near $75,500 as reports of renewed tension emerged.

Market data indicates that Bitcoin had earlier risen above $78,000 after initial reports suggested progress in negotiations. The reversal followed conflicting updates from both sides regarding the ceasefire.

Crypto markets often react to geopolitical events, with price swings linked to investor sentiment and risk perception during uncertain periods.

Moreover, the broader crypto market has also experienced volatility during the same period. Traders have adjusted positions as new information continues to emerge from diplomatic discussions.

Bitcoin remains sensitive to external developments, especially those linked to global stability and economic outlook. Market participants are monitoring updates related to the ceasefire and any potential policy response.

Price fluctuations have remained within a narrow range over the past sessions, reflecting cautious trading behavior. The situation continues to evolve as negotiations between the United States and Iran remain ongoing.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Crypto World

France faces the brunt of an increasing violent crime wave against the crypto community

France is facing a rise in crypto-related kidnappings as so-called “wrench attacks” become more frequent, brazen and violent.

That shift was visible this week amid the staging of an annual international blockchain and crypto conference. A police motorcade escorted VIP guests to a dinner at the Palace of Versailles. And security was also notably reinforced at the Carrousel du Louver, where the conference was taking place.

Wrench attacks in France have put the country so notably under the international spotlight that government officials took the stage at the conference in Paris to acknowledge their alarm at the scale of the problem. They said that this year alone, the country has suffered at least 41 crypto-related kidnappings and home invasions. That’s one every two to three days.

Jean-Didier Berger, Minister Delegate to the Interior Ministry, said a new set of measures is being prepared with Interior Minister Laurent Nuñez to tackle the growing issue. A prevention platform has already drawn thousands of registrations, but authorities say further steps are needed as incidents continue to rise.

Wrench attack epicenter

The country has become the epicenter of a global rise in wrench attacks. Across multiple jurisdictions, attacks on crypto holders are becoming more frequent and more violent, according to security researchers and law enforcement data.

Globally, the trend is also on the rise. In 2025, there were 72 verified physical coercion incidents globally, a 75% increase from the previous year, according to Certik and crypto researcher Jameson Lopp’s data, which tracks 188 attacks since 2014. Many more go unreported, he said. Cases involving physical assault rose even faster, up 250% year-over-year.

The term “wrench attack” refers to the use of physical force to extract access to digital assets. For some attackers, it is easier to coerce a person than to break encryption.

“Every time a wrench attack is successful, it tells the world that crypto owners are juicy targets,” Lopp told CoinDesk.

Unlike traditional bank transfers, crypto transactions cannot be reversed. Once a victim authorizes a transfer under duress, the funds can be moved quickly across wallets and chains.

Attackers seek points of weakness

Researchers say the way attackers identify victims has also changed.

“We’re seeing a shift from ‘find a wallet’ to ‘hunt a person,’” Phil Ariss of TRM Labs told CoinDesk. Rather than scanning for technical vulnerabilities, attackers build profiles, he added. They look at social media activity, public appearances and leaked datasets. They track routines and identify points of weakness.

“The biggest avoidable mistake is tying real-world identity, location and routine too tightly to visible crypto wealth,” Ariss said.

The problem is exacerbated when attackers get a helping hand from government officials. In one widely known case, in which a French tax official sold wrench attackers sensitive data. The case raised concerns among security experts that insider leaks and compromised state data were feeding directly into wrench attacks.

The pool of potential victims has widened, with mid-level holders increasingly being targeted, sometimes based on limited or indirect signals.

Anybody is a potential victim

Cases now include families, with children targeted alongside crypto-holding parents, making the attacks harder to categorize by severity.

In January 2025, Ledger co-founder David Balland was kidnapped in France along with his partner. During the attack, one of his fingers was severed and sent to associates as part of a ransom demand. He was rescued after a police operation.

Other cases have involved prolonged captivity and torture, such as one in New York, where a crypto investor was held for more than two weeks. In Canada, a home invasion escalated into waterboarding and sexual violence as attackers attempted to force access to funds.

Lopp said both opportunistic and organized groups are involved, but there are signs of increasing coordination. “We do seem to be seeing more organized groups now,” he said.

TRM Labs’s Ariss says his team has observed similar patterns, noting some groups operate with defined roles and pre-planning, including surveillance and follow-home tactics.

“These look less like one-off robberies and more like small kidnap or robbery crews specializing in crypto jobs,” Ariss said.

After funds are obtained, attackers tend to move quickly and frequently the crypto assets they attain are converted into stablecoins and routed across multiple chains, making recovery more difficult.

France’s role in this trend may reflect a mix of factors, Lopp said, including cases involving leaked personal data and cross-border criminal networks.

Rising prices, heftier loot

More broadly, rising asset prices have increased the potential payoff from a single attack, while improvements in digital security have reduced the effectiveness of purely technical exploits.

“It’s far easier than trying to rob a bank,” Lopp said.

Another issue is visibility: wrench attacks might be significantly underreported because many are reported as standard robberies or home invasions, with no mention of crypto.

“A large share of incidents are still recorded as simple robberies,” Ariss said, adding that the crypto element is often left out at the time of reporting, which can make it harder for authorities to connect cases or identify broader patterns.

The increase in attacks has raised questions about the risks of self-custody, a core principle of cryptocurrency.

Some security experts point to measures such as multi-signature setups, withdrawal delays and spending limits as ways to reduce risk by limiting how much can be accessed under duress.

“If coercion cannot produce immediate access to the majority of funds, the risk and return changes,” Ariss said. Such measures do not eliminate the threat but may reduce the incentive for attackers.

As crypto adoption grows, attacks are becoming more frequent and severe, turning what was once a niche concern into a broader security risk.

TLDR:

- Bitcoin trades near $75K as ETF inflows exceed $1B weekly, reversing a four-month outflow trend

- Stable US jobs data and easing geopolitics support risk assets across crypto and equity markets

- Solana and Ethereum upgrades improve efficiency, supporting network growth and user activity

- Institutional moves and rising stablecoin supply strengthen liquidity across crypto markets

Global markets are moving in a steady range as equities reach new highs while Bitcoin trades near $75,000. At the same time, ETF inflows, policy signals, and network upgrades are shaping current crypto market conditions.

Liquidity Conditions and Capital Flows Drive Market Stability

Market activity reflects a shift toward risk assets as liquidity conditions improve across global markets. Stocks are recording fresh highs, while Bitcoin continues consolidating within a narrow price range near $75,000.

A recent post by Nick Research outlined the current drivers influencing both crypto and traditional markets. The tweet noted strong ETF inflows exceeding $1 billion weekly, ending a four-month outflow streak. It also pointed to easing geopolitical tensions and steady earnings supporting a risk-on environment.

These ETF inflows indicate renewed institutional participation in digital assets. Capital movement into Bitcoin products shows improving sentiment among large investors after a prolonged period of reduced exposure.

At the same time, macroeconomic data in the United States remains stable. Job growth has shown recovery, while unemployment levels remain relatively low. This stability continues to support investor confidence across markets.

Geopolitical developments are also playing a role in shaping sentiment. Reports of easing tensions linked to a possible Iran ceasefire are contributing to a more favorable risk environment.

Monetary policy expectations are shifting gradually. The Federal Reserve is expected to ease at a slower pace, with rates projected near 3% by year-end. Quantitative tightening has paused, easing pressure on liquidity conditions.

Bitcoin is also showing increased correlation with traditional markets. The asset is now moving closely with the S&P 500 and gold, reflecting broader macro alignment.

Institutional Activity and Blockchain Upgrades Support Momentum

Beyond macro factors, institutional actions and blockchain upgrades are shaping current market conditions. Regulatory developments remain active, with the CLARITY Act expected to move into Senate markup in the coming weeks.

Institutional involvement continues to expand within the crypto sector. Deutsche Börse has committed $200 million to Kraken, signaling continued engagement from established financial firms.

In addition, Goldman Sachs has filed for a Bitcoin ETF, adding to the list of institutional products targeting digital asset exposure. These filings show continued integration between traditional finance and crypto markets.

Network upgrades are also contributing to improved efficiency across blockchain ecosystems. The Solana SIMD-266 upgrade is expected to reduce data costs by up to 98%, improving network performance.

Ethereum is preparing for upcoming upgrades, including Pectra and Glamsterdam. These updates are designed to enhance scalability and maintain network competitiveness.

Supply conditions remain another factor shaping the market. The post-halving environment continues to limit Bitcoin supply, while stablecoin supply is expanding toward the $1 trillion level.

This growth in stablecoin supply reflects increasing liquidity within the digital asset ecosystem. It also supports trading activity and broader market participation.

Together, macro stability, institutional flows, and network upgrades are shaping current market direction. These elements are driving activity across both crypto and traditional financial markets.

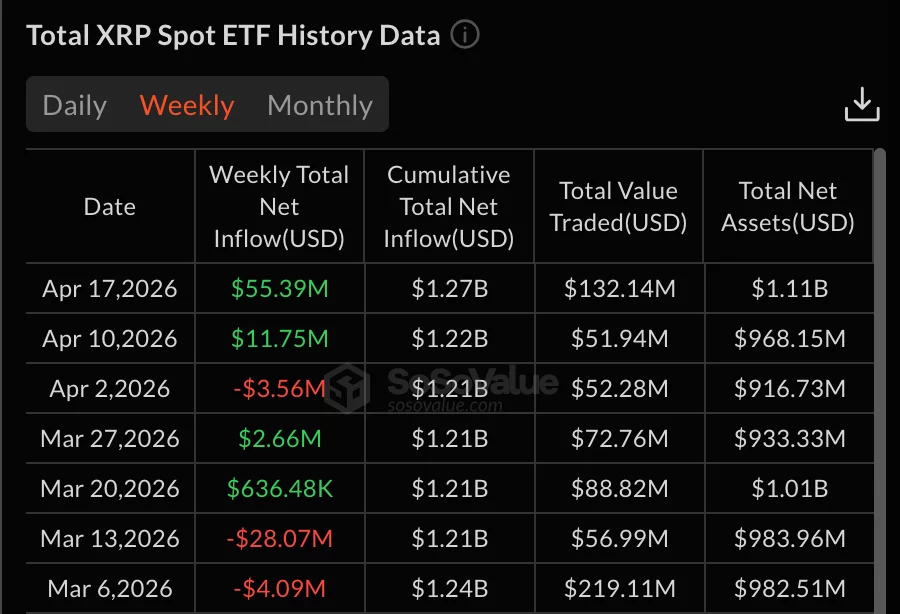

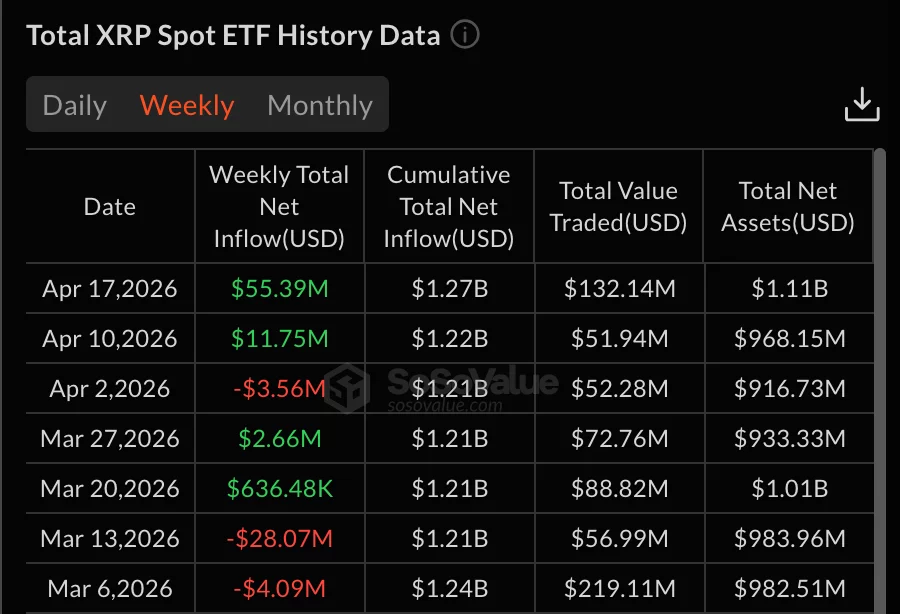

XRP exchange-traded products have recorded their strongest weekly inflows of the year.

Summary

- XRP ETFs recorded $55.39 million in weekly inflows, the highest level seen in 2026.

- Institutional investors increased exposure after XRP price rose more than 7 percent last week.

- Analysts note XRP remains within long-term bullish structure despite short-term market volatility signals.

The increase comes after renewed interest from both retail and institutional investors across the broader crypto market.

Data from SoSoValue showed that XRP ETFs attracted $55.39 million in net inflows over the past week. This marks the first time in 2026 that inflows have reached this level after several weeks of weaker performance.

The ETF products did not record any daily outflows during the week, indicating steady demand across all trading sessions.

Institutional investors increased exposure to XRP-linked investment products following a recent rise in price activity. XRP recorded a price gain of more than 7 percent over the same period.

Market data showed consistent inflows throughout the week, with the lowest daily intake at $1.46 million on April 13. Other trading days recorded higher levels of capital movement into XRP ETFs.

The broader crypto market also showed improved sentiment during the same period, which supported demand for digital asset investment products.

Market position and price performance

At press time, XRP traded near $1.43 with a market capitalization of approximately $88 billion. The asset recorded a slight daily decline but maintained a positive weekly performance.

Trading volume remained above $2 billion in the last 24 hours, reflecting continued market participation. XRP also appears positioned to end a multi-month period of negative returns, after six consecutive months of losses that began in late 2025.

The market movement follows volatility linked to earlier macroeconomic conditions, including a sharp correction in October 2025.

Meanwhile, market commentary from analyst EGRAG CRYPTO has focused on long-term chart patterns. The analyst stated “”the Bifrost Bridge is still our guide”” when describing XRP’s current structure.

The analysis suggests XRP remains inside a broader channel despite short-term pattern breakdowns. The commentary also noted that descending triangle formations may not fully reflect the wider trend.

The analyst added “”this is not a breakdown, this is a setup”” when referring to projected price levels between $9 and $13. The view is based on long-term accumulation phases and market structure interpretation.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

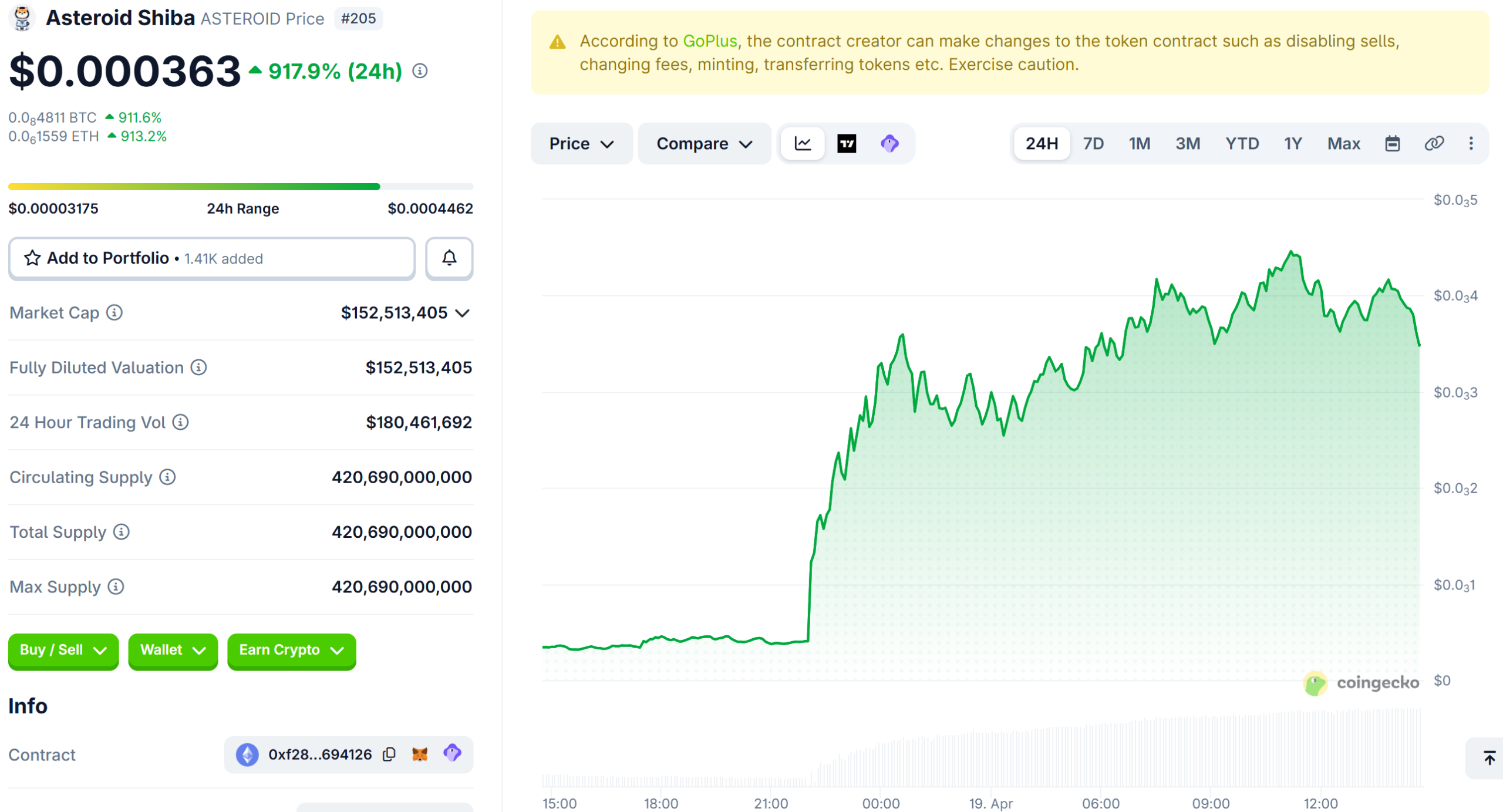

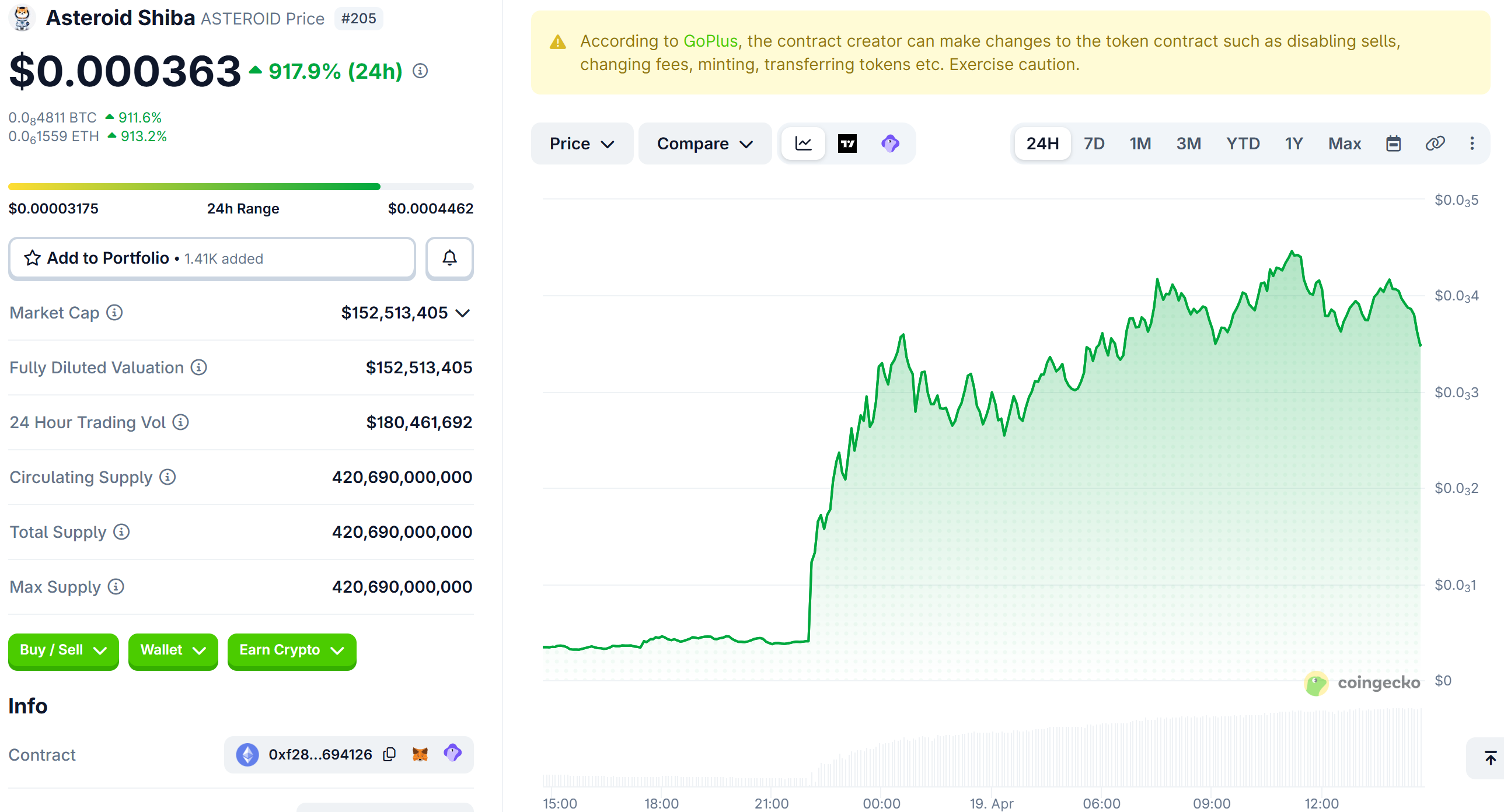

A trader sold 7.43 billion Asteroid Shiba (ASTEROID) tokens for $405 just one day before the meme coin rallied over 920%, turning that same position into a $2.6 million windfall.

On-chain data from Lookonchain revealed that wallet 0x5811 had bought the tokens 80 days earlier for $542. The sale locked in a $137 loss, erasing what would have been a life-changing gain.

What Triggered the Asteroid Shiba Rally

The rally began after Elon Musk replied to eight questions left behind by Liv Perrotto, a 15-year-old who died in January after a five-year battle with cancer.

Perrotto had designed a plush Shiba Inu named Asteroid as the zero-gravity indicator for SpaceX’s Polaris Dawn mission in September 2024.

For her final question, she asked Musk to make Asteroid the official SpaceX mascot. He agreed.

The Asteroid Shiba price is up by almost 920%, and nearly 68,000% in the last week.

Her mother, Rebecca Perrotto, responded on X, thanking him for keeping her daughter’s memory alive.

“You didn’t just honor a young girl’s dream, you are keeping her spirit alive. Liv’s love, her laughter, her unbreakable fight lives on through Asteroid,” she wrote.

Winners, Losers, and Risk

While wallet 0x5811 missed millions, another trader turned roughly $1,800 in ETH into nearly $500,000 within hours of Musk’s post.

However, Musk’s ability to move meme coins has shown signs of fading. Previous Musk-linked rallies in tokens like GORK and KEKIUS were short-lived.

Musk himself has previously compared meme coins to gambling. ASTEROID has no product, roadmap, or team behind it. The token carries significant risk for anyone buying after the initial move.

“If you expect to win at meme coins, you’re being foolish. You’re not going to win with meme coins. Don’t sink your life savings into a meme coin,” he said in an interview with The Joe Rogan Experience podcast.

The post Asteroid Shiba Gains 920% After Musk Names SpaceX Mascot, But One Trader Misses Big appeared first on BeInCrypto.

Privacy crypto still standing strong

Reform investigating candidate who ‘hates’ the NHS

Beiwacht notches second G1 in 2026 All Aged Stakes at Randwick

-

NewsBeat7 days ago

NewsBeat7 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Crypto World6 days ago

Crypto World6 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Theodora Dress

-

Politics7 days ago

Politics7 days agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World6 days ago

Crypto World6 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos4 days ago

News Videos4 days agoSecure crypto trading starts with an FIU-registered

-

Sports2 days ago

Sports2 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World5 days ago

Crypto World5 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

NewsBeat5 days ago

NewsBeat5 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Politics2 days ago

Politics2 days agoPalestine barred from entering Canada for FIFA Congress

-

Crypto World2 days ago

Crypto World2 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Sports6 days ago

Sports6 days agoNWFL opens Pathway for new Clubs ahead of 2026 Season

-

Business3 days ago

Business3 days agoCreo Medical agree sale of its manufacturing operation

-

Crypto World6 days ago

Crypto World6 days agoTrump whales load up ahead of Mar-a-Lago luncheon.

-

Politics5 hours ago

Politics5 hours agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Business6 days ago

Kering slides after Morgan Stanley downgrade, Gucci woes loom

-

Tech6 days ago

Tech6 days agoGoogle adds E2E encryption to Gmail for iOS and Android enterprise users

-

Entertainment6 days ago

Entertainment6 days agoBrand New Day’ Footage Reveals the Devastating Impact of ‘Now Way Home’

-

Crypto World7 days ago

Sei Network Enters Quiet Reset Phase as On-Chain Metrics Signal a Slowdown in 2026

-

Tech6 days ago

Tech6 days agoApple glasses won’t go brand shopping like Meta did with Ray-Ban and Oakley

You must be logged in to post a comment Login