Business

PepsiCo pivoting to snack affordability

.webp?t=1770298497)

Microsoft Stock Tracking Worst 6-Month Stretch Since 2009

Form 6K Skillful Craftsman Education Technology Ltd For: 27 March

The company is selling new shares worth up to 1.5 billion rupees ($15.85 million), while existing shareholders, including venture capital firm Accel, is selling up to 28.4 million shares, the filing showed.

Sotherly Hotels to delist preferred stock from Nasdaq

BiomX receives NYSE American non-compliance notice

Iran Has Distracted From the Mag 7 Woes. Why the Slump Is a Good Thing for Stock Markets.

Shares in Next PLC NXT -1.71%decrease; red down pointing triangle jumped after the U.K. clothing retailer maintained its fiscal-year sales-growth expectations, despite warning that the Iran war could affect costs, prices and consumer demand.

The group said Thursday it had accounted for 15 million pounds ($20 million) in additional costs—including fuel and air freight—tied to the Middle East conflict. The costs didn’t affect Next’s guidance since they have been offset by savings, it said.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

The Big Money Show panel discusses the alarming new analysis showing Social Security and Medicare racing toward insolvency and warns that retirees face steep benefit cuts unless Washington acts fast.

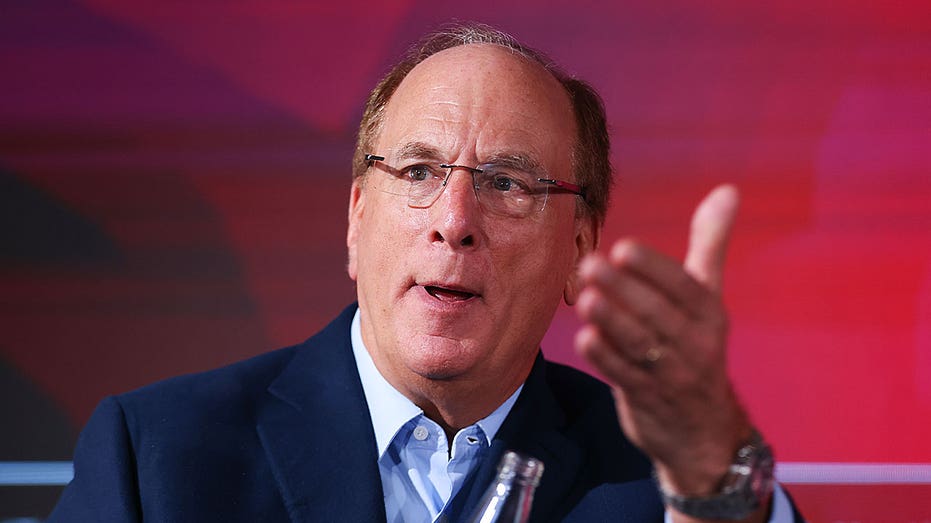

BlackRock CEO Larry Fink discussed possible Social Security reforms that would allow more Americans to benefit from the growth in the stock market while also ensuring the program is strengthened so it can survive to serve future generations.

Fink’s recently released annual chairman’s letter touched on how Social Security is “one of the most effective poverty-prevention programs in history” and that while it provides stability, it “doesn’t allow most Americans to build wealth in a way that grows their country.”

“Today, the system operates largely on a pay-as-you-go basis. Payroll taxes are used to pay current retirees, and the Social Security trust fund is invested primarily in U.S. Treasury bonds. In effect, workers lend money to the government and receive defined benefits in return.”

“The structure, designed as a social insurance program, emphasizes stability and predictability. What it doesn’t do is let people grow their benefits along with the broader economy. The question is whether the Social Security system could allow both,” Fink said.

NEW PROPOSAL WOULD CAP SOCIAL SECURITY BENEFITS AT $100K FOR WEALTHY COUPLES

BlackRock CEO Larry Fink said that Americans need to discuss ways to reform Social Security ahead of its insolvency. (Hollie Adams/Bloomberg via Getty Images)

He said that this could be accomplished by asking whether a portion of the system could be invested “carefully, broadly, and over decades” like other long-term pension systems.

“This would not mean privatizing Social Security or putting it all into the stock market,” Fink wrote. “It would mean introducing a measure of diversification, similar in principle to the federal Thrift Savings Plan, which manages retirement savings for millions of federal employees.”

“The goal would be to strengthen the system over time while preserving its core guarantees,” he added.

SOCIAL SECURITY’S MAIN TRUST FUND FACES DEPLETION IN 2032, TRIGGERING BENEFIT CUTS

Social Security’s main trust fund is on a path to insolvency in less than a decade, when benefits would be automatically cut to match payroll tax revenue. (Getty Images/iStock)

Fink noted a bipartisan proposal from Sens. Bill Cassidy, R-La., and Tim Kaine, D-Va., that would create a new investment fund that operates parallel to the existing trust fund rather than replacing it while investing in a diversified mix of stocks and bonds to generate higher returns.

The proposal would require an initial investment of about $1.5 trillion and would be given 75 years to grow, and during that period the Treasury would continue covering Social Security benefits.

Once the fund matures, it would repay the Treasury and then supplement payroll taxes going forward to help close the gap between what the Social Security system takes in and what it pays out – while no one on Social Security or nearing retirement would see a change to their benefits.

Fink also noted that about six million Americans who are employed by state and local governments don’t currently contribute to Social Security and instead rely on public pension systems that invest in diversified portfolios.

BUDGET DEFICIT HITS $1 TRILLION FOR FIRST FIVE MONTHS OF FISCAL YEAR: CBO

| Ticker | Security | Last | Change | Change % |

|---|---|---|---|---|

| BLK | BLACKROCK INC. | 933.66 | -34.51 | -3.56% |

Other examples of alternative pension systems can be found overseas, with Australia’s superannuation system representing an approach that invests retirement contributions in the financial markets. Fink said that a “similar, carefully structured approach could be considered to strengthen Social Security.”

“I understand why any talk of changing Social Security makes people uneasy. Social Security is a core promise, and people rightly believe it should be honored. But under the current system, doing nothing could very well break that promise,” he said.

“Current projections show the trust fund won’t be able to pay full benefits by 2033. Many young Americans doubt they’ll ever fully see theirs,” he explained. “Addressing that gap will likely require multiple solutions. But thoughtful, long-term investing could be one of them.”

GET FOX BUSINESS ON THE GO BY CLICKING HERE

An analysis by the nonpartisan Committee for a Responsible Federal Budget (CRFB) noted that when Social Security’s main trust fund reaches insolvency – which is projected to occur in 2032 – federal law requires benefits be cut to match revenue from payroll taxes, which would amount to a roughly 24% cut for beneficiaries.

Fink noted that his chairman’s letter two years ago was focused on rethinking retirement and generated criticism for suggesting that Social Security was in need of reforms. He acknowledged that the latest letter may do the same, but said it’s a conversation that needs to be had.

“In my 50 years in finance, if there’s one thing I’ve learned, it’s that the problems we don’t talk about are the ones that should worry us most. And that’s exactly why we need the conversation now – because the cost of waiting is only getting higher,” he said.

Form 13D/A Venus Concept For: 27 March

JHVEPhoto/iStock Editorial via Getty Images

QuantumScape’s (QS) recent board appointment may prove more important than the headline suggests.

According to the company’s March 5 announcement, QuantumScape added Ross Niebergall to its board, an executive with deep ties across the defense industrial

Am schnellsten Weg finanziell frei!

Donald Trump breaks silence on Tiger Woods’ car crash and ‘difficulty’ he faces

Microsoft Stock Tracking Worst 6-Month Stretch Since 2009

-

Crypto World7 days ago

Crypto World7 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

NewsBeat2 days ago

NewsBeat2 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

Crypto World6 days ago

Crypto World6 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

News Videos2 days ago

News Videos2 days agoParliament publishes latest register of MPs’ financial interests

-

Sports4 days ago

Sports4 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

Sports4 days ago

Sports4 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Business5 days ago

Business5 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Tech5 days ago

Tech5 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Tech5 days ago

Tech5 days agoAI enters the chat: New Seattle dating app relies on tech to facilitate meaningful human connections

-

News Videos4 days ago

News Videos4 days agoCh 9 Financial Management Part 1 | Detailed One Shot | Class 12 Business Studies Boards 2026

-

Business7 days ago

Columbia Sportswear enters $500 million credit agreement with JPMorgan Chase

-

Tech6 days ago

Tech6 days agoToday’s NYT Connections Hints, Answers for March 22 #1015

-

Business1 day ago

Business1 day agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Business5 days ago

Business5 days agoWill Duke Basketball Win It All? Duke Basketball Enters Second Round as Third Favorite to Claim NCAA Title

-

Sports5 days ago

Sports5 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who hit 12 Derby-Oaks Doubles enters picks

-

NewsBeat5 days ago

NewsBeat5 days agoUpdate on Wisbech river crash as search for teenage boy enters fifth day

-

Entertainment4 days ago

Entertainment4 days agoCynthia Bailey Dishes on ‘RHOA’ Season 17, Discusses Kandi

-

NewsBeat2 days ago

NewsBeat2 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Tech4 days ago

Tech4 days agoSamsung will soon let you control smart home devices from your car’s dashboard

You must be logged in to post a comment Login