Business

Buildroid AI secures $2mn to deploy AI-powered construction robots in UAE

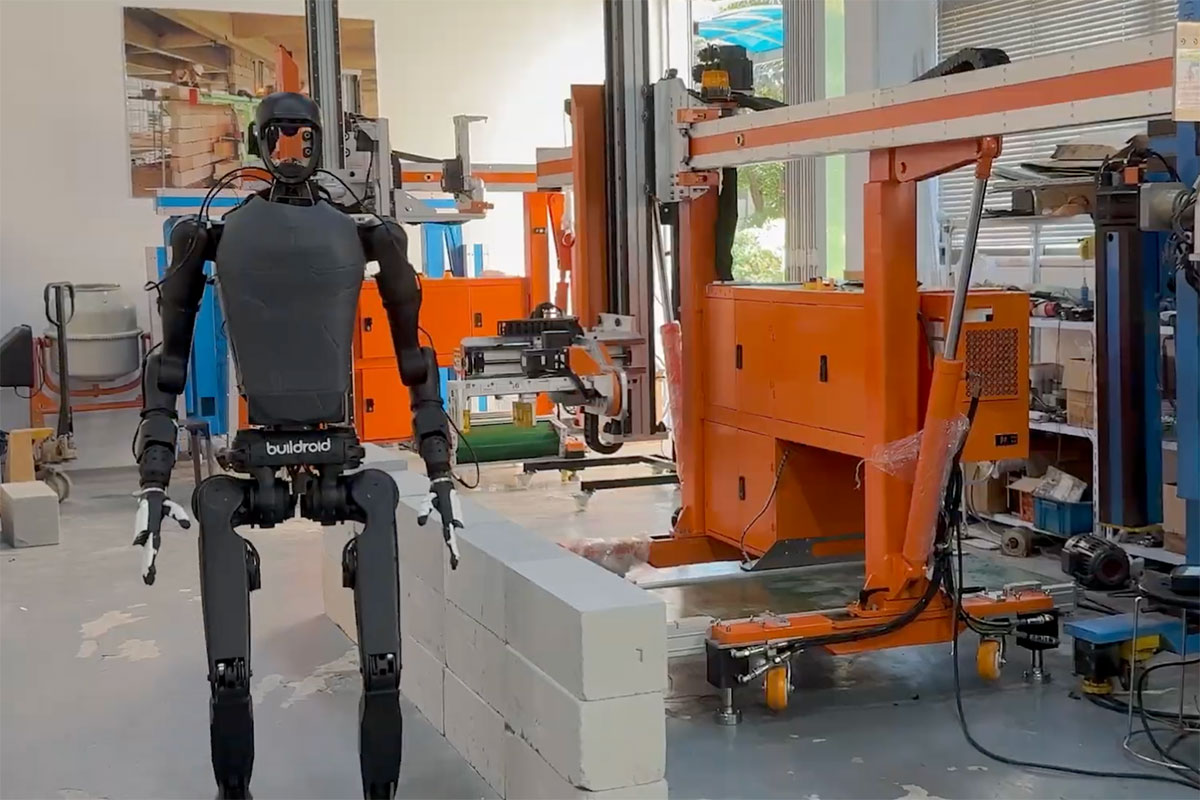

Buildroid AI, a robotics startup focused on automating construction, has emerged from stealth with US$2 million in pre-seed funding led by Tim Draper, the early investor behind Tesla, SpaceX, and Skype.

The company unveiled its first AI-driven block-laying robot at the Big Five Construction Conference in Dubai, targeting the UAE’s fast-growing US$42.75 billion construction sector.

Founded by Slava Solonitsyn, former CEO of Mighty Buildings, and Anton Glance, Buildroid aims to address chronic labour shortages and productivity challenges in the construction industry. The startup’s system integrates Building Information Models (BIM) with AI-powered digital twin simulations, built on Nvidia Omniverse, to plan, test, and optimise robotic workflows before deployment.

“UAE’s construction growth demands solutions to persistent labour shortages and productivity bottlenecks”, said Solonitsyn.

“Construction robots have been around for over a decade, but have had limited success, primarily because they automate narrow skills and require significant additional labour to support them. With the rapid development of AI, it has become possible to bring general-purpose and industrial robots to construction as well.”

The company’s first robot is being tested on active sites in the UAE, capable of building partition walls up to 10 times faster and at up to four times lower cost than manual labour.

Future models will include autonomous mobile robots that transport materials directly to block-laying units, reducing the need for human support.

Buildroid’s platform is designed as a multi-robot ecosystem, enabling contractors to integrate various robotic systems through simulation-first workflows, similar to an ERP platform for construction robotics.

The company plans to open its platform to vendors and operators, enabling scalability across the MENA region’s US$401 billion construction market by 2030.

Tim Draper said: “Buildroid’s platform combines the best robotic technologies validated through BIM-based simulations. Such an approach empowers builders with scalable, flexible vendor-agnostic automation that maintains the critical role of skilled human operators.”

With the new funding, Buildroid will expand pilot programmes with major contractors including ALEC, which is already trialling the company’s technology. Commercial deployments are planned for next year, starting with non-load-bearing walls and expanding into interior fit-out and broader construction workflows.