News Videos

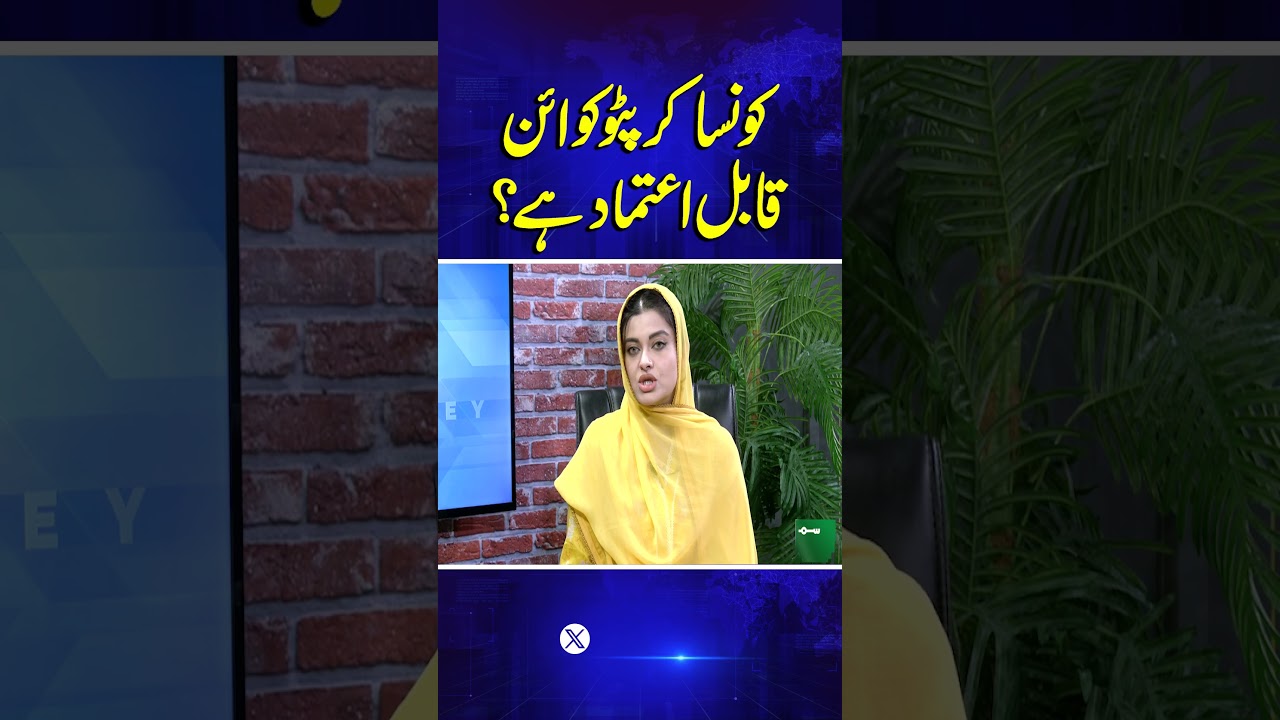

Which cryptocurrency is trustworthy?

Which cryptocurrency is trustworthy?

#samaatv #SamaaMoney #Business #cryptocurrency #DigitalCurrency #Money

SAMAA TV is the top Pakistani news channel covering national news from a diverse array of fields — from politics and current affairs, business and sports to international, entertainment and culture.

The channel aims at providing factual, in-depth and latest news as and when it happens.

Tune in to SAMAA TV to stay updated, whether at home or on the go, on all things current and relevant.

➽ Subscribe to Samaa News ➽ https://bit.ly/2Wh8Sp8

➽ Watch Samaa News Live ➽ https://bit.ly/3oUSwAP

Stay up-to-date on the major news making headlines across Pakistan on SAMAA TV’s top-of-the-hour segment. For in-depth coverage watch the bulletins.

SAMAA TV is Pakistan’s first private satellite news channel that provides live transmission simultaneously from five cities of Pakistan: Karachi, Lahore, Islamabad, Quetta and Peshawar.

SAMAA’s live news bulletins, incisive political talk shows and a wide range of programs including sports, social issues and infotainment has enabled it to position itself among the top tier news and current affairs channels of Pakistan.

SAMAA Network :

SUBSCRIBE to get the latest SAMAA News content: https://bit.ly/2Wh8Sp8

► SAMAA News YouTube Channel: https://bit.ly/2Wh8Sp8

► SAMAA Originals YouTube Channel: https://bit.ly/32c1qO3

► SAMAA MONEY YouTube channel: https://bit.ly/2EkiglJ

► SAMAA SPORTS YouTube channel: https://bit.ly/34jyINP

► SAMAA ISLAMIC YouTube channel: https://bit.ly/2LT1WMF

Keep watching SAMAA!

For latest Urdu News updates visit:

http://www.samaa.tv

http://www.facebook.com/samaatvnews

http://www.twitter.com/samaatv

http://www.instagram.com/samaatv

https://whatsapp.com/channel/0029Va8EglPLCoX1JQRteR1x

Punjab Govt | CM Punjab | Punjab Assembly | Bilawal Bhutto | Imran Khan | News | Breaking News | Latest News | News Headlines | Prime Time Headlines | Samaa News | News Channel | Live News | Breaking News | Latest News | Pakistan Breaking News | Breaking News Today | News Headlines | Headlines News | Pakistan News | Headlines | Live News | News Updates | Samaa news live | Samaa | Samaa Live | Samaa News Live Streaming | Samaa Youtube Channel | Samaa Channel | Samaa Tv Live | Samaa Tv | Samaa Live Tv | Samaa Live News

source

#stealabrainrot #roblox #usa

source

The market looks calm on the surface but the cracks are getting worse. From global conflict to gold selloffs and debt stress, the system is under pressure and Bitcoin is feeding off it. This breakdown explains why the bottom may not be in yet and why more volatility is likely. The chaos is not a bug, it is the setup.

SPONSORS

✅ Ledn

👉 https://www.nmj1gs2i.com/9W598/9B9DM/?source_id=Youtube&sub1=Description

💡 Simply Bitcoin clients get 0.25% off their first loan

💸 Need liquidity without selling your Bitcoin? Ledn has been the trusted Bitcoin-backed lending platform for 6+ years. Access your BTC’s value while HODLing.

🛠️ The Bitcoin Way

👉 https://www.nmj1gs2i.com/9W598/D42TT/?source_id=Youtube&sub1=Description

✅ Your IT Team In The Bitcoin World: The Bitcoin Way is a specialized IT team providing individuals and businesses with exceptional guidance and technical support. With over 20 years of expertise in cybersecurity and privacy, they excel at simplifying the intricacies of Bitcoin. The Bitcoin Way’s mission is to empower individuals to utilize Bitcoin effortlessly while maintaining complete control over their funds.

⛓️ Sazmining

https://www.sazmining.com/?ef_transaction_id=&oid=10&affid=7&source_id=Youtube&sub1=Description

🎯 Use code SIMPLYBITCOIN for a discount

Because real Bitcoin starts at the source.

🛠️ Zero-maintenance, non-custodial Bitcoin mining.

🏗️ You own the miner. You keep the sats. They handle the rest.

📡Sat123

https://www.nmj1gs2i.com/9W598/KMKS9/?source_id=Youtube&sub1=Description

🎯 Use code SIMPLY for 15% off

Because self-custody doesn’t end at your wallet.

🛰️ Satellite phones, Starlink kits, Faraday bags

⛺️ For sovereignty, off-grid living & emergencies

Chapters:

00:00 – Is the Bitcoin bottom really in

00:50 – Why markets still look fragile

01:40 – War, oil routes, and rising risk

02:45 – Why stressed nations turn to Bitcoin

03:20 – Gold failing as a safe haven

03:55 – Japan and the global debt risk

04:45 – Why the system cannot collapse

07:55 – Cash is losing in this system

09:15 – Debasement is the real driver

10:40 – Why volatility is a Bitcoin opportunity

✓ SUBSCRIBE – https://bit.ly/3QbgqTQ

✓ LEAVE A LIKE

✓ COMMENT

Connect with Dante:

► https://x.com/Dante_Cook1

DISCLAIMER: All views in this episode are our own and DO NOT reflect the opinions/views of any of our guests or sponsors.

Copyright Disclaimer Under section 107 of the Copyright Act 1976, allowance is made for “fair use” for purposes such as criticism, comment, news reporting, teaching, scholarship, education, and research. If you are or represent the copyright owner of materials used in this video and have a problem using said material, please contact Simply Bitcoin.

source

#bankcharges #banktruth #atmfees #money #finance #indianbanks #banking #hiddencharges #moneyloss #savingtips #financialawareness #india #viral #trending #youtubeshorts #shorts #telugushorts #telugu #factvideo #truth #reality #moneytips #alert #awareness #viralshorts #explore #trendingshorts #indiatrending #digitalindia #financefacts

fair use :-Some contents are used for educational purpose under fair use. Copyright disclaimer Under Section 107 of the Copyright Act 1976, allowance is made for “fair use” for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use is a use permitted by copyright statute that might otherwise be infringing. Non-profit, educational or personal use tips the balance in favor of fair use.

source

📚 Learn 50+ years of Real Economics in only 7 weeks. Apply here: https://www.stevekeen.com/?video=EJicZxhhzgc

(Apply this week and get my 3-Book Rebel Economist Bundle as a Free Bonus. Plus if you’re fully approved by my team, get Ravel© – my proprietary economic visualization software I use in my YouTube videos; to predict the economy, like I did years before the 2008 Financial Crash happened).

The Iran-US War Won’t Just Destroy Oil Markets It Will Collapse Bitcoin.

Most economists are focused on oil. But there’s a deeper crisis hiding in plain sight and it starts with the energy Bitcoin needs to survive.

In this video, I break down the exact chain reaction no one is talking about: how an Iran-US war disrupts global energy supply, why that kills crypto mining dead, and why Bitcoin’s energy dependency makes it the most vulnerable asset of the 21st century.

📌 WHAT WE COVER IN THIS VIDEO:

✅ Why the US Iran war is the single biggest threat to Bitcoin right now

✅ The hidden link between the Strait of Hormuz, global energy, and Bitcoin mining

✅ Why crypto’s energy consumption becomes catastrophically exposed post-conflict

✅ How a Bitcoin collapse forces a global return to fiat currency

✅ The bitcoin prediction no crypto investor wants to hear — but needs to

✅ What the bitcoin analysis data tells us about fragility under geopolitical shock

This isn’t speculation it’s economics. War reshapes energy. Energy shapes money. And Bitcoin, for all its digital promises, runs on electricity.

If you think crypto is a safe haven in a wartime world, watch this first.

Our latest analysis begins with a critical look at rising oil prices and the ongoing inflation impacting households globally. We discuss the potential for an economic collapse as geopolitical tensions escalate, particularly within the middle east conflict. This video explains how a potential iran usa conflict could reshape the globaleconomy, impacting bitcoin today and broader crypto news. 🚀📉

This isn’t speculation it’s analysis backed by geopolitical facts most channels are afraid to cover.

Our latest analysis focuses on the future of cryptocurrency, particularly in light of ongoing global events. We explore the impact of the iran us conflict on bitcoin today, questioning its role as a stable payment gateway. This video examines recent bitcoin news and provides a comprehensive bitcoin analysis amidst the volatile landscape of the middle east. 🚀📉

HOW TRUMP’S RECKLESS DECISIONS ARE ACCELERATING THE U.S. COLLAPSE

While the world watches the Iran crisis unfold, one uncomfortable truth is being ignored Trump’s own behaviour is pushing the US economy collapse into overdrive.The Trump dollar collapse isn’t just a theory anymore it’s the logical consequence of a leader who governed by impulse, not strategy. When the most powerful nation on Earth is steered by ego rather than intelligence, the cracks don’t just appear they widen into crises. The Iran escalation? Partly a Trump legacy. The inflation spiral? Partly a Trump legacy. And now, ordinary Americans are left to foot the bill for decisions made by a man more concerned with headlines than consequences.

✅ How the US-Israel-Iran war escalation could crash global energy markets overnight

✅ Why the dollar collapse is no longer a conspiracy it’s a real risk

✅ Trump’s hidden agenda why Trump backed Israel and what it means for YOU

✅ Iran’s nuclear program: what happens when a rogue state gets the bomb

✅ The new arms race: how Iran nuclear capability reshapes Middle East alliances

✅ The role of the US, China & Russia and who really controls the outcome

✅ End times prophecy decoded: does the Middle East conflict align with Biblical predictions?

✅ The significance of Jerusalem in Biblical prophecy and the Second Coming of Jesus

✅ How the JCPOA (Iran nuclear deal) has been rendered obsolete

✅ What this means for global stability and what you should do NOW

🔥 The geopolitical landscape is shifting faster than ever. The US-Israel-Iran war isn’t just a military story — it’s an economic earthquake, a prophetic convergence, and a turning point for humanity.

Whether you’re tracking global markets, studying end times prophecy, or trying to understand why the world feels like it’s on the edge — this video connects the dots.

📩 Subscribe for weekly geopolitical breakdowns nobody else is covering.

👇 Drop your thoughts below do you think war with Iran is inevitable?

#iranwar #middleeastconflict #bitcoinfall #economiccollapse #dollarcollapse #usisraeliranwar #Endtimesprophecy #Biblicalprophecy #IranNuclear #TrumpAgenda #jerusalem #SecondComingOfJesus #geopolitics #worldwar3 #eschatology #globaleconomy #bitcoin #bitcoinminningenergy #bitcoinmining

#bitcoin #bitcoincollapse #bitcoinpredictions #usiranwar #cryptonews #bitcoinmining #cryptocurrency #iranwar #bitcointoday #financialeducation

source

How to Become a Chartered Financial Consultant (ChFC) in India

Finance

Career jobs

Finance Career Opportunities

Chartered Financial consultant

CHFC

#chfc #career #job #exam #highpayingcareer #facts #shorts

source

0,5 Bitcoin erreicht? Herzlichen Glückwunsch! Jetzt wird es Zeit für den nächsten Schritt. Kaufe diese 5 Dinge, um dein Leben massiv aufzuwerten.

____________________________________

WERBUNG:

🔒 Hardware Wallet BitBox02: Bitcoin langfristig aufbewahren

Spare 5% mit dem Rabattcode BITCOINREISE

https://bitbox.shop/?ref=KVcp0JucZr

💜 Pocket Bitcoin: Bitcoin kaufen und verkaufen

Willkommensbonus von 5 CHF/EUR mit dem Empfehlungscode BITCOINREISE

https://pocketbitcoin.com/de/invite/bitcoinreise

💙 Relai App: Bitcoin kaufen und verkaufen

Spare 0,1% auf die Gebühren mit dem Rabattcode BITCOINREISE

🤍 21bitcoin: Bitcoin kaufen und verkaufen

Spare 0,2% auf die Gebühren mit dem Referral Code BITCOINREISE

https://21bitcoin.app.link/invite/?code=BITCOINREISE

🖤 Coinfinity: Bitcoin kaufen und verkaufen

Spare 0,32% auf die Gebühren mit dem Empfehlungscode BITCOINREISE

https://coinfinity.co/

Damit unterstützt du meine Arbeit enorm!

____________________________________

🎥 Werde Kanalmitglied auf YouTube

https://www.youtube.com/channel/UCDrgidocFz7Kb7ZET_tm7Bw/join

💙 Folge mir auf X / Twitter

Tweets by BitcoinReise

🧡 Besuche meine Webseite

https://www.bitcoinreise.com/

(Im entsprechenden Blog-Beitrag findest du alle Quellen zum Video)

⚡ Value 4 Value (Lightning)

bitcoinreise@walletofsatoshi.com

____________________________________

KAPITEL:

00:00 5 Dinge, die du kaufen solltest

00:54 Erlebnisse

01:50 Hochwertiges Essen

03:49 Bequemlichkeit

05:25 Eine sichere Aufbewahrungslösung

06:41 Eine Mitgliedschaft im Fitnessstudio

____________________________________

⚠️ Meine Inhalte dienen ausschliesslich Informations- und Bildungszwecken. Sie stellen keine Finanzberatung, Anlageempfehlung oder Aufforderung zum Kauf oder Verkauf von Wertpapieren oder Kryptowährungen dar. Ich bin kein Finanzberater und übernehme keine Haftung für finanzielle Verluste oder Handlungen, die auf Grundlage meiner Inhalte erfolgen. Jeder Zuschauer ist selbst dafür verantwortlich, sich vor Investitionsentscheidungen umfassend zu informieren und gegebenenfalls professionelle Beratung einzuholen. Trotz sorgfältiger Recherche übernehme ich keine Gewähr für Richtigkeit, Vollständigkeit oder Aktualität der Informationen.

____________________________________

Du möchtest mehr über die Grundlagen von Bitcoin erfahren und weitere Animationsvideos sehen? Begleite mich auf der BitcoinReise und abonniere meinen YouTube Kanal! 🎬

source

GRACIAS POR VER!

✅💎AGENDA TU SERVICIO POR WHATSAPP: https://api.whatsapp.com/send/?phone=573197910631

📷 INSTAGRAM: https://www.instagram.com/by.danfull

🤍TIKTOK: https://www.tiktok.com/@idanfull

🐦TWITTER: https://twitter.com/iDanFull

📱GRUPO DE TELEGRAM: https://t.me/iDanFull

🎬UNETE AL SERVIDOR DE DISCORD!: https://discord.gg/KQeJ9uWVcs

Crew GTA 5 ONLINE: https://socialclub.rockstargames.com/crew/idanfuil/wall

📧CORREO PARA COLABORACIONES:

www.danfull@gmail.com

–TAGS–

como duplicar carros en gta online,como duplicar coches solo sin ayuda,como duplicar coches sin ayuda ps4,como duplicar coches en gtaonline xbox,gta 5 money glitch,gta 5 solo money glitch,gta 5 solo car duplication glitch,gta 5 fast money,gta 5 solo afk,easy solo money glitch,solo money glitch in gta online,gta 5 ps4 pc xbox one,gta 5 pc xbox one ps4,gta 5 para pobres,dinero para pobres gta 5,como duplicar en gta,dinero infinito gta online,trucos gta v online, como modear coches no del cliente,car to car arena,como modear coches solo,como modear coches merge,nuevo glitch modear coches,modded cars gta 5,modear coches en xbox,modear coches en ps5 ps4 pc, coches ocultos gta5 online,coches secretos gta5 online,como desbloquear coches secretos gta5 online,mejores coches gta5 online,como tener el coche de policia en gta5 online,como tener el slamvan de lost gta5 online,slamvan de lost gta5 oline,autos ocultos gta5 online,grand theft auto 5 online,gta5 online trucos,coches gta5 online,cjp_mystic,guia para principiantes gta5 online,coches gratis gta5 online,cual es el mejor coche de gta5 online,gta5 ps4,gta5 ps5, dinero infinito ps4,gta 5 dinero ps4,gta 5 dinero rapido,gta 5 dinero online,gta 5 dinero modo historia,gta 5 dinero pc,gta 5 dinero gratis,gta 5 dinero solo,gta 5 dinero legal,gta 5 dinero afk,gta 5 dinero bolsa,gta 5 dinero bajo el agua,gta 5 dinero bajo el mar,bug dinero gta 5 online ps4,bug dinero gta 5 online,gta 5 bug de dinero truco gta v dinero, dinero gratis, truco masivo, sin starter pack, sin ayuda, gta v truco,modear coche gta v, modde gta v, modear coche, como modear coche gta v,modear, modear coche, modear bandito gta, gta v ps4 pc xbox,duplicar solo sin ayuda, duplicar sin criminal, duplicar coches gta v,gta v, duplicar solo sin ayuda, duplicar solo rápido, modear coches, modear autos, car to car,duplicar coches sin ayuda, duplicar coches con ayuda, duplicar coches con ayuda amigo, pasar coches a amigos, dinero gta v, modded cars gta v, gta v dinero, gta v rp, gta v rp infinito, trucos gta v online, ps4 XBOX pc trucos, pasar coches a amigos, duplicar coches solo, duplicar coches solo, solo sin ayuda, modear coches solo, modear coches,conjuntos mod, conjuntos mod gta v,pasar coches a amigos gta v, gta v regalar coches gta v, nuevo,tryhard, tryhard gta v,duplicar solo sin ayuda gta v, gta v truco dinero, duplicar carros solo sin ayuda gta v, duplicar autos sólo gta v online,duplicar coches,joggers blancos gta,como obtener jogger blancos,gta v online ps4 truco,xbox truco gta v,pc truco gta v,mod menu gta v ps4,gomo tener dinero facil gta v,nuevo truco,modear coches solo sin ayuda,ps4 pc xbox ps5,trucazo bestial,rp infinito,joggers,oufit mod,trucazo,frozen money sin savewizard,duplicar dinero en gta v,como hacer dinero en gta,como conseguir joggers en hombre,dinero infinito,truco gta,frozenmoney, gta 5 money glitch,gta 5 solo money glitch,gta online easy solo money glitch for poor people,gta 5 solo car duplication glitch,gta 5 fast money,gta 5 solo afk,easy solo money glitch,solo money glitch in gta online,gta v solo money glitch,gta 5 solo sin ayuda,gta 5 ps4 pc xbox one,gta 5 pc xbox one ps4,gta 5 para pobres,dinero para pobres gta 5,como duplicar en gta,dinero infinito gta online,trucos gta v online,trucos gta 5 dinero infinito,coches gratis gta v, gta 5,gta 6,gta san andreas,gta v,gta 5 online,gta 5 policia,gta roleplay,gta 6 trailer,gta auron,gta advance,gta auronplay,gta apocalipsis zombie,gta actualizacion,gta aliens,gta area 51,gta android mod pack,a gta 5,a gta 6,a gta v roleplay,a gta 5 online,a gta roleplay,a gta online,a gta v,a gta song,gta battle royale,gta bunker,gta bonificaciones,gta balacerasgta 5 los santos tuners,gta 5 nuevo dlc,gta 5 nueva actualizacion,gta5 nuevos coches,gta 5 nuevo dlc 2021,gta 5 dlc 2021,,duplicar en gta 5 online solo sin ayuda,tuners and outlaws dlc gta5 online, Grand Theft Auto 5, como ganar dinero en gta 5 online,como ganar dinero en gta 5 online 2021,como ganar dinero en gta 5 online 2022,como ganar dinero en gta 5 online 2023,gta 5 online,gta online,gta v,gta v online,gta 5,ganar dinero gta 5,ganar dinero gta 5 online,ganar dinero,ganar dinero gta online,ganar dinero gta v online,ganar dinero gta v,dinero facil,dinero rapido,dinero infinito.

source

The risk models that say when to accumulate or exit HERE.

Free trial 👉 https://app.cryptocapitalventure.ai

🌟 Follow Me On My Socials!

📸 Instagram: instagram.com/dangambardello

🐦 X: x.com/cryptorecruitr

⚡ Catch Me On X

⚡ http://x.com/cryptorecruitr

This channel focuses on macro analysis, liquidity cycles, and market behavior to help long-term investors understand where we are in the broader financial cycle.

I break down capital flows, risk conditions, and economic context across markets — and when relevant, how assets like crypto fit into the bigger picture.

This content is for patient capital, not short-term speculation.

*The above video references an opinion and is for news/information and entertainment purposes only. It is not intended to be investment advice, financial advice, or any solicitation, recommendation, endorsement, or offer that you buy or sell any cryptocurrency or securities. Trading in cryptocurrencies and securities is a high risk activity involving risk of loss so please seek a duly licensed professional for investment or financial advice. The information provided on this video should not be used to make any investment or financial decisions without consulting your financial or investment advisor. This video contains my opinion only and is not intended to cause harm or defame anyone or any entity.

source

If you hold Bitcoin or Ethereum… watch this! (alert!)

⭐ Follow Altcoin Daily on 𝕏: https://twitter.com/AltcoinDaily

🟠 BTC Conference 2026 – ‘ALTCOINDAILY’ for 10% off Ticket: https://2026.b.tc

🟠 Become a channel member & get access to perks:

https://www.youtube.com/channel/UCbLhGKVY-bJPcawebgtNfbw/join

🎁 Altcoin Daily Merch: https://m046hz-bk.myshopify.com

🟡 50% deposit bonus on first $100 on WEEX: https://www.weex.com/events/welcome-event?vipCode=oz5p&qrType=activity

🟣 Best Crypto Exchange To Trade ($12,000 Bonus): https://www.coinw.com/en_US/register?r=ALTCOINDAILY

✅ Bitunix (no kyc, $10,000 bonus): https://www.bitunix.com/register?vipCode=AltcoinDaily

🔴 $30k USDT bonus with Phemex with our link: https://phemex.com/a/k/ALTCOINDAILY30

🔵 $30k bonuses with our link – Buy & Trade Crypto on Bybit: https://partner.bybit.com/b/altcoindaily

🟢 $8k bonus on Bitget Exchange with our link: https://bonus.bitget.com/AltcoinDaily

Altcoin Daily in Spanish: www.youtube.com/@AltcoinDailyenEspanol

Follow Altcoin Daily:

www.twitter.com/AltcoinDaily

www.instagram.com/thealtcoindaily/

Join Altcoin Daily on Telegram: https://t.me/AltcoinDailyANN

Hit Like, Share, and Subscribe for more daily cryptocurrency news

Altcoin Daily, the best cryptocurrency news media online!

Video by Aaron:

www.instagram.com/aarontarnold/

www.twitter.com/aarontarnold

For business inquires email: info.altcoindailyio@gmail.com

Timestamps:

0:00 – intro (stay tuned)

0:05 – Fortunes are made in times like these

0:24 – 6th red month in a row

1:54 – Trump makes big announcement

2:23 – Do NOT Be fooled

2:58 – Why you should be bullish

5:05 – SC: 40k Eth & 500k BTC by 2030

8:24 – Tom Lee says April will be bullish

**Note: My overall opinion is that the name of the game is to accumulate as much Bitcoin as possible. Alts are interesting but a lot more speculative. I use them to accumulate more Bitcoin & Ethereum.

***********************************************************************

🏺Support The Channel!!🏺(We Get A Kickback From Affiliate Links)

Protect and store your crypto with a Ledger Nano:

https://shop.ledger.com/?r=4b0f6c5711dc

Robinhood exchange has crypto & stocks:

https://join.robinhood.com/aarona-78df3a8

***********************************************************************

Altcoin Daily, the best cryptocurrency news media online!

#bitcoin #cryptocurrency #news #btc #ethereum #eth #cryptocurrency #litecoin #altcoin #altcoins #forex #money #best #trading #bitcoinmining #invest #trader #cryptocurrencies #top #investing #business #success #investment #finance #coinbase #binance #stocks #wallstreet #investor #wealth #bullish #crash #collapse #economy #cnbc #cryptolive #altcoindaily

***NOT FINANCIAL, LEGAL, OR TAX ADVICE! JUST OPINION! I AM NOT AN EXPERT! I DO NOT GUARANTEE A PARTICULAR OUTCOME I HAVE NO INSIDE KNOWLEDGE! YOU NEED TO DO YOUR OWN RESEARCH AND MAKE YOUR OWN DECISIONS! THIS IS JUST EDUCATION & ENTERTAINMENT! USE ALTCOIN DAILY AS A STARTING OFF POINT!

This is NOT an offer to buy or sell securities.

Investing and trading in cryptocurrencies is very risky, as anything can happen at any time.

This information is what was found publicly on the internet. This information could’ve been doctored or misrepresented by the internet. All information is meant for public awareness and is public domain. This information is not intended to slander, harm or defame any of the actors involved but to show what was said through their social media accounts. Please take this information and do your own research.

*The channel is not responsible for the performance of sponsors and affiliates.

Most of my crypto portfolio is Bitcoin, then Ethereum, but I hold many cryptocurrencies, possibly ones discussed in this video.

cryptocurrency, crypto, altcoin, altcoin daily, news, best investment, top altcoins, best crypto investment, ethereum, xrp, crash, crash, price, prediction, podcast, interview, finance, stock, investment, too late, bitcoin, cryptocurrency news, bitcoin news, cryptocurrency news media online, best crypto investments, 2026 prediction, should I buy ethereum?, blackrock, donald trump, coin bureau, binance, coinbase, trading crypto, trade, make money, cryptosrus, bitcoin today, bitcoin cnbc, altcoin news,

source

Steakhouse Financial front-end breach exposes users to phishing scam

Senegal Fans’ Trial in Morocco Postponed Again

Harry Potter star Paapa Essiedu’s life from famous wife to death threats

-

NewsBeat5 days ago

NewsBeat5 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

News Videos5 days ago

News Videos5 days agoParliament publishes latest register of MPs’ financial interests

-

NewsBeat3 days ago

NewsBeat3 days agoThe Story hosts event on Durham’s historic registers

-

Business4 days ago

Business4 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

NewsBeat5 days ago

NewsBeat5 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Tech7 days ago

Tech7 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

Entertainment2 days ago

Entertainment2 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Fashion6 days ago

Fashion6 days agoDoes It Matter What You Wear When You’re Laid Off and Looking?

-

Business6 days ago

Business6 days agoMore women enter wealth management, but few in advisory roles: study

-

NewsBeat7 days ago

NewsBeat7 days agoColombian military plane with 110 soldiers onboard crashes following takeoff

-

Politics7 days ago

Politics7 days agoHow Media Platforms Balance Performance and Accessibility in Image Delivery

-

NewsBeat6 days ago

NewsBeat6 days agoEntrepreneurs Forum survey reveals optimism in North East

-

NewsBeat6 days ago

NewsBeat6 days agoNASA Artemis II Astronauts enter 14-Day quarantine as moon rocket reaches launchpad

-

Business6 days ago

Business6 days agoLate-paying firms face multimillion-pound fines under new crackdown

-

Tech4 days ago

Tech4 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

Crypto World6 days ago

Crypto World6 days agoBTC gives up $70,000 level as markets mull higher interest rates

-

Sports5 days ago

Sports5 days agoFantasy Baseball Week 1 Preview: Top sleeper hitters for both five- and 12-day period led by Munetaka Murakami

-

Tech5 days ago

Tech5 days agoUS FCC Prohibits Approval Of New Foreign-Made Consumer Routers

-

Tech6 days ago

Tech6 days agoEmbedding compliance in AI adoption

-

Fashion6 days ago

Fashion6 days agoCoffee Break: Korean Skincare Set

You must be logged in to post a comment Login