Crypto World

Crypto Retail Investors Try Meta-Analysis of the Market

Retail investors are scanning the crypto landscape for signs a bottom may be forming, hoping to time new purchases as market conditions potentially improve. A weekly briefing from Santiment on Saturday noted that retail traders are meta-analyzing price action, seeking indications that others are capitulating—a behavior that often marks troughs in bear markets. The term has surged as a top topic on social media, with Santiment tying the chatter to rising selling pressure. Google Trends data show a clear uptick in searches for “crypto capitulation” over recent days, underscoring how participants interpret price swings as signals rather than mere volatility. In this environment, Bitcoin has traded under pressure, dipping toward the $60,000 level on Thursday as part of a broader downtrend that has persisted for months.

The term capitulation describes a scenario where investors rush to exit positions out of fear that the market will not recover, a dynamic analysts monitor when assessing a market bottom. If the chorus of sellers grows loud enough that many participants capitulate at once, some interpret that as a sign that the worst may be behind them, even if others argue that bottoms in bear markets often arrive after multiple rounds of selling pressure. The debate remains a central theme as markets test psychological support levels and risk appetite remains fragile.

Capitulation signals and the coming bottom

“If everyone is waiting for ‘capitulation,’ the bottom might have already happened while they were waiting for a clearer sign,” Santiment cautioned in its assessment. The idea is that waiting for a definitive capitulation before buying can cause investors to miss a move that follows the initial flush of fear, a phenomenon that has played out in past cycles. Yet, several voices in the analyst community urge caution. Caleb Franzen, a market observer active on X, pointed out that capitulation is often a recurring theme in bear markets and that a single event rarely marks the ultimate bottom. “Bear markets typically experience multiple capitulation events,” Franzen wrote, highlighting the risk that the downturn may extend even after a strong capitulation signal appears.

As the debate unfolds, Bitcoin’s price action continues to weigh on sentiment. The flagship asset has seen volatility and regional price pressures, with a notable moment when it briefly struck a $60,000 level—an area not visited since October 2024 during this cycle’s slide. While some traders see this as an opportunity to accumulate, others caution that the move could be a continuation of the downtrend unless stronger catalysts emerge. The market’s complexity is underscored by a mix of on-chain data, macro considerations, and shifting liquidity conditions that collectively shape the near-term trajectory.

Further context comes from the broader sentiment gauges that traders monitor. The Crypto Fear & Greed Index, a composite measure of risk appetite across the market, slid deeper into an Extreme Fear zone in recent days, signaling a cautious stance among participants. This mood aligns with the period of heightened scrutiny around capitulation narratives and the ongoing debate over whether a bottom is in place or still distant. The blend of sentiment metrics and price dynamics creates a nuanced backdrop where several outcomes remain plausible in the weeks ahead.

In parallel, a separate thread of analysis emphasizes that capitulation—while relevant—may not be a single event but a process that unfolds over multiple episodes. CryptoGoos noted that true capitulation in Bitcoin had not yet materialized, a stance echoed by other analysts who stress that bottoms often require a confluence of confirmation signals, including on-chain activity, macro surprises, and investor positioning. The conversation reflects a market that is trying to quantify risk, distinguish genuine signaling events from noise, and position for a potential reversal when the confluence of factors tilts toward relief selling abating and demand reasserting itself.

Bitcoin’s recent movement sits at the center of these debates. Data from CoinMarketCap show the asset had fallen about 24% over the last 30 days, trading around $68,970 at the time of publication, with a low near $60,000 earlier in the week. The slide has kept risk managers vigilant, as fluctuations can influence leverage, funding rates, and liquidity across exchanges. In this environment, investors are weighing the potential for a sustainable bottom against the risk that the market could slip further before any durable recovery takes hold.

The market’s current state is a reminder that retail participation often shapes near-term moves, yet the longer-term trend remains dependent on a complex mix of factors, including macro policy expectations, liquidity dynamics, and how quickly market participants can absorb new information. While capitulation remains a focal point for many observers, the ultimate measure of a bottom will likely come from a broader pattern of price stabilization, sustained demand, and a shift in sentiment that signals a durable change in risk appetite.

Why it matters

For retail investors, the ongoing capitulation narrative frames risk tolerance and entry points. The possibility that a bottom could be forming—even if still contested—offers a potential upside scenario if buyers re-enter on perceived oversold conditions. For builders and traders, the discussion underscores the importance of risk controls, liquidity access, and the ability to distinguish meaningful capitulation signals from temporary price shocks. The broader market context—where macro indicators and regulatory developments can abruptly reframe risk sentiment—remains a critical backdrop for decision-making.

From a market-structure perspective, the unfolding dialogue around capitulation highlights how sentiment analytics, on-chain data, and price action interact to create a narrative about participation. While the data points discussed—ranging from Santiment’s retail-trader observations to Google Trends spikes and the Crypto Fear & Greed Index—offer a composite picture, they do not guarantee a bottom. Instead, they contribute to a framework that investors can use to calibrate expectations, manage risk, and prepare for a potential shift in momentum as the market weighs new information and potential catalysts.

What to watch next

- Watch for any sustained price stabilization around key support zones near $60,000 and above, which could indicate a base forming.

- Monitor capitulation signals and on-chain activity for confirmation that selling pressure is abating, not simply cooling temporarily.

- Track Google Trends and social sentiment to assess whether interest in capitulation remains elevated or begins to fade as prices stabilize.

- Follow macro developments and regulatory updates that could shift risk appetite and liquidity conditions across markets.

- Observe price action around major technical levels and liquidity at major exchanges, which can influence short-term volatility and trader positioning.

Sources & verification

- Santiment weekly summary on retail capitulation and bottom signals, including links to the full written report.

- Google Trends data showing rising searches for “crypto capitulation” during Feb 1–Feb 8, 2026.

- Bitcoin price data and 30-day performance from CoinMarketCap.

- On-chain and market commentary from analysts referencing capitulation dynamics and multiple capitulation events in bear markets.

- CryptoFear & Greed Index readings indicating current sentiment levels (Extreme Fear).

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Bitcoin, USDC, and XRP remain key pillars as investors balance store of value, stability, and payments.

Summary

- Bitcoin, USDC, and XRP lead the crypto ecosystem, driving innovation, stability, and cross-border payments.

- ConfluxCapital enables users to earn daily returns through AI-driven quantitative crypto strategies without complex setups.

- The platform offers a $20 signup bonus, automated trading, and flexible withdrawals to simplify crypto investing.

In the booming wave of digital assets, Bitcoin, USDC, and XRP are arguably the three most influential cryptocurrencies. Bitcoin, as decentralized digital gold, continues to lead industry trends; USDC, as a stablecoin, ensures value stability and facilitates asset management and trading; and XRP, with its high-speed, low-cost cross-border payment network, is highly favored by financial institutions.

These three cryptocurrencies together form the core foundation of the modern blockchain ecosystem, continuously driving innovation and development in the global digital economy.

Now, with Confluxcapital, a leading intelligent quantitative strategy mining platform, anyone can easily participate in Bitcoin, USDC, and XRP quantitative strategies, earning stable daily returns without complex equipment or technical barriers.

Whether they are an experienced investor or a beginner, Confluxcapital provides an efficient and compliant strategy environment, allowing anyone to truly create value with digital assets.

What is a quantitative strategy?

ConfluxCapital’s Cryptocurrency AI Quantitative Strategy refers to an investment strategy that uses artificial intelligence and quantitative trading algorithms to automate cryptocurrency trading. In short, it allows programs and AI to replace humans in identifying buying and selling opportunities, automatically trading in the cryptocurrency market to generate stable returns.

ConfluxCapital advantages:

- Receive an instant $20 bonus upon registration. Automated operation: After purchasing a strategy package, earnings are automatically credited to an account the next day, with no need to monitor the market.

- Flexible withdrawals: Withdrawals to a crypto wallet are available once the account balance reaches $100, or reinvest for even more returns.

- Top-tier security: Dual security protection with McAfee® and Cloudflare® ensures assets are safe.

- Globally trusted: Recognized by over 3 million users in 195+ countries and regions.

- Multi-currency support: Supports settlement in major digital assets such as XRP, DOGE, SOL, BTC, ETH, LTC, USDC, USDT, BNB, and BCH.

- Zero extra fees: No hidden fees, transparent and worry-free.

How to start earning daily with Confluxcapital

Step 1: Register an Account

Step 2: Choose a Plan

Confluxcapital offers a variety of earning strategies to meet specific financial goals. Whether someone is looking for short-term gains or long-term returns, there’s one for them.

Step 3: Start Earning

Enjoy earnings without any management. Daily earnings will be automatically deposited into an account, which can then be withdrawn to a cryptocurrency wallet address.

Strategy Name

unit price

Days

Total Revenue

Starter Strategy

$100

2 days

$100+$6

Basic Strategy

$600

5 days

$600+$45

Advanced Strategies

$5,000

15 days

$5,000+$1,215

Elite Strategy

$25,000

25 days

$25,000+$11,250

Quantum Strategy

$90,000

20 days

$90,000+$36,000

Infinite Strategy

$200,000

25 days

$200,000+$110,000

Once the strategy is executed, the resulting profits will be automatically credited to the user’s account the following day. Accumulated funds in the account can be flexibly used to add to existing strategy configurations or withdrawn to a personal encrypted wallet according to platform rules.

About Conflux Capital

Founded in London, UK in 2023, Conflux Capital holds a valid operating license issued by the local government. The platform focuses on quantitative trading, combining intelligent algorithms and arbitrage strategies to provide standardized value-added solutions for crypto asset holders. The team is dedicated to improving strategy execution efficiency and fund transparency, offering multi-currency strategy options to users with different risk appetites.

Conclusion

While XRP still has room for short-term growth, its potential risks are increasingly apparent. Faced with signs of whales exiting the market, more and more savvy investors are choosing to enter the market in a timely manner to diversify their assets and obtain more stable passive cash flow. Confluxcapital’s convenient multi-currency quantitative strategy service perfectly meets this need, enabling investors to fully utilize their existing crypto assets (including XRP, BTC, USDC, etc.) and create a long-term, stable source of income in volatile markets.

No hardware or technical expertise is required to enjoy a one-stop quantitative strategy service, allowing anyone seeking a second or higher income to enjoy a stable and efficient asset appreciation experience.

For more information, visit the official website and download the application.

Email:[email protected]

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Crypto World

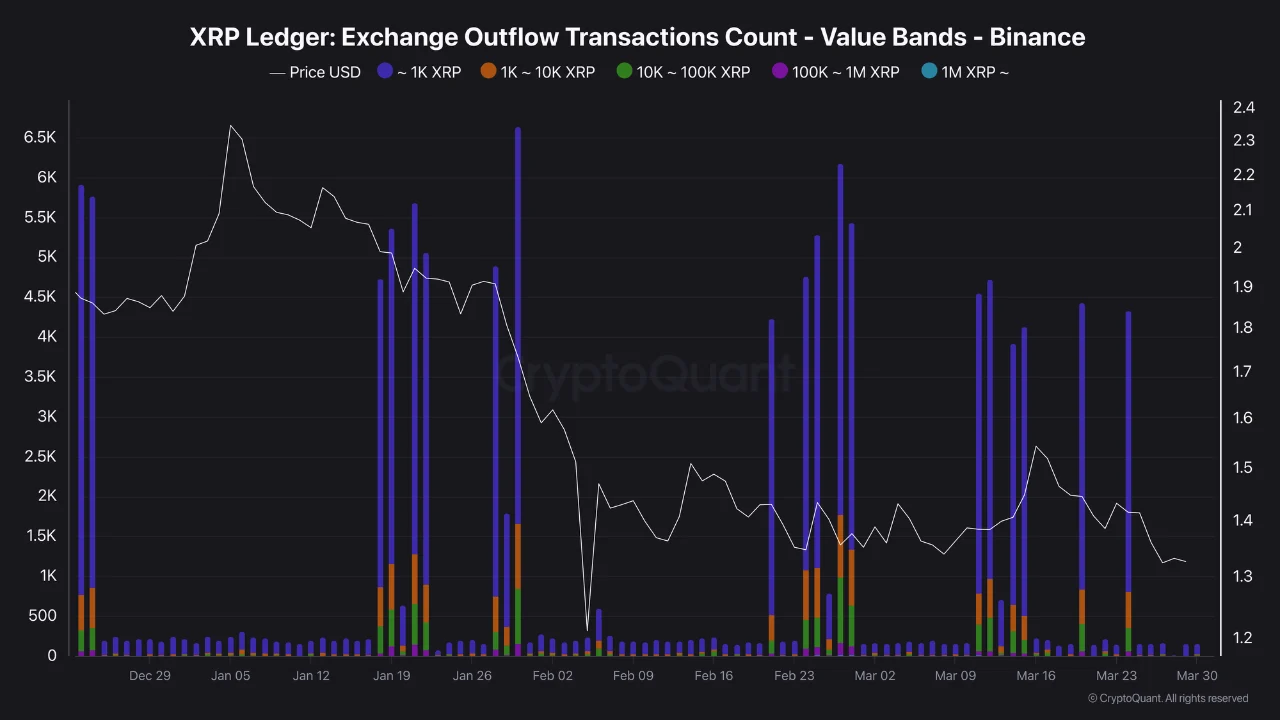

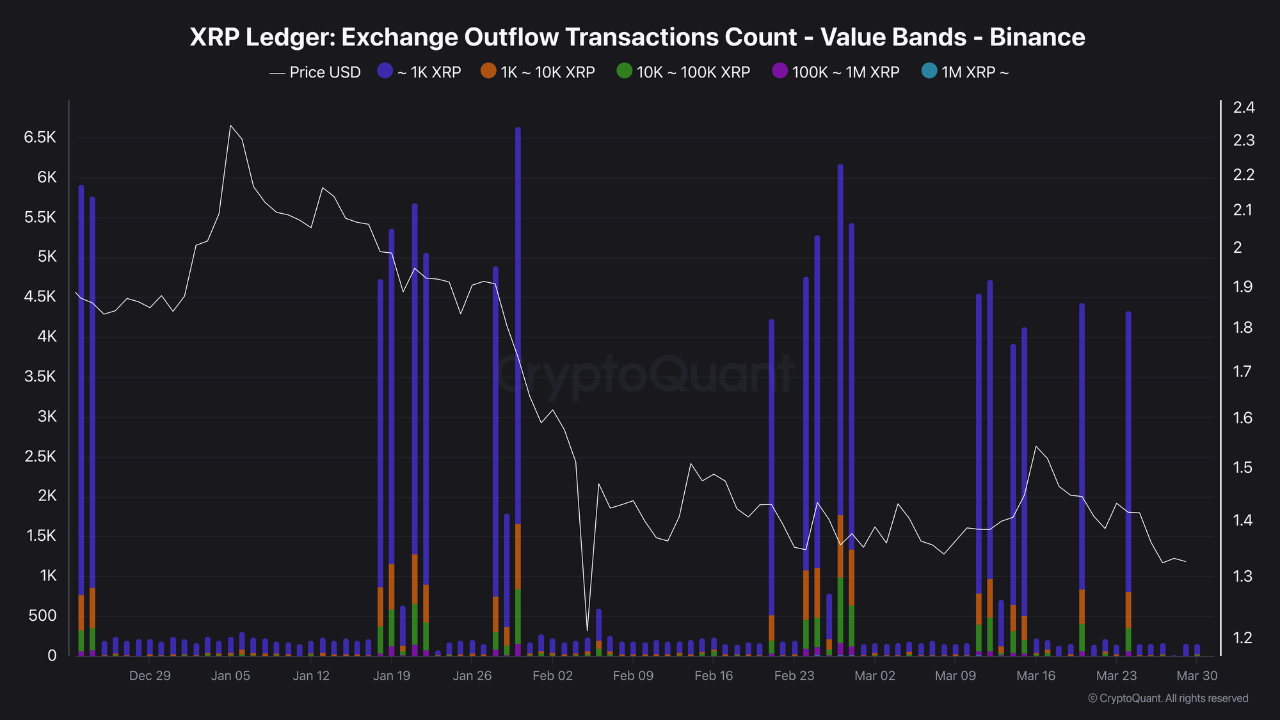

XRP Holds Steady Between $1.30 and $1.50 as Whales and Mid-Sized Investors Keep Accumulating

TLDR:

- XRP has been trading between $1.30 and $1.50 for months, showing resilience amid altcoin weakness.

- Binance outflow transactions surged since late February, with some days recording nearly 6,000 withdrawals.

- Most outflow activity is driven by transactions of 1,000 to 100,000 XRP, pointing to mid-sized investors.

- Whales have maintained an accumulation zone between $1.20 and $3.00 for over a year without selling to retail.

XRP has been trading within a defined range for several months, oscillating between $1.30 and $1.50. On-chain data from Binance shows a growing accumulation trend, with outflow transactions rising notably since late February.

Binance Outflow Data Points to an Active Accumulation Phase

Despite challenging conditions across the broader crypto market, XRP has shown a degree of resilience. The asset continues to hold within its established trading range while other altcoins have faced heavier losses.

This steady price action has drawn attention from market analysts tracking on-chain behavior. The pattern suggests that some investors are using the consolidation period to build positions.

Data from Binance shows a clear resurgence in outflow transactions starting from late February. Several days during this period recorded more than 4,000 outflow transactions on the exchange.

Source: Cryptoquant

Some peaks reached close to 6,000 transactions within a single day. This level of activity is notable for an asset still trading over 60% below its all-time high.

Most of the activity is driven by transactions ranging between 1,000 and 100,000 tokens. This range typically corresponds to mid-sized investors rather than large institutional whales.

The pattern differs from the usual whale-dominated movements seen in early bull market cycles. As a result, the accumulation appears to be spread across a broader segment of the market.

An increase in outflow transactions generally means investors are moving tokens off exchanges. This behavior is often interpreted as a preference to hold assets in private wallets.

It suggests reduced selling intent and a longer-term holding mindset. Analysts often view this trend as a positive on-chain signal during a consolidation phase.

Whale Accumulation Adds to the Bullish Narrative for the Asset

Beyond retail and mid-sized investor activity, whale behavior has also drawn considerable attention. According to crypto analyst CW, whales have been accumulating consistently for over a year.

The analyst noted that whales typically build positions at the bottom before an uptrend begins. This observation adds another layer to the existing accumulation narrative.

CW further noted that the current whale accumulation zone sits between $1.20 and $3.00. Before this phase, strong accumulation was recorded in the $0.30 to $1.30 range as well.

These whales have not yet offloaded their holdings to retail investors. Based on available data, they appear to be continuing to buy.

The broader picture suggests that the asset is in an active accumulation phase across multiple investor segments. Both mid-sized holders and larger market participants appear aligned in their current behavior.

However, the key question remains whether this accumulation will be enough to trigger a breakout. A move above the $1.50 resistance level could confirm a shift in momentum.

At press time, XRP is trading at $1.35, still within its months-long range. Market participants continue to monitor on-chain data closely for further signals of a directional move.

Bitcoin is approaching the March monthly close with a potential sixth straight month in the red, hovering in the mid-$60,000s as macro headlines keep risk-off sentiment front and center. The latest price action saw BTC test the $65,000 area early in the week, with traders eyeing $67,500 to $68,000 as near-term resistance and noting a lack of sustained demand to spark a durable rebound. The backdrop combines geopolitical frictions around Iran with inflation and growth concerns, while equities tilt lower and expectations for aggressive Fed easing retreat.

-

BTC sits near critical levels: a move back above the $68,000–$69,000 zone is needed to shift the short-term bias away from a bearish channel.

-

Macro headlines remain a headwind, as tensions around Iran and energy markets feed inflation and risk-off sentiment in stocks and crypto alike.

-

March risks becoming a sixth red month for Bitcoin; April historically offers stronger average returns, though the path depends on macro liquidity and on-chain demand.

-

On-chain behavior shows whales reducing exposure while large exchange inflows rise, signalling potential near-term selling pressure in the absence of fresh buying demand.

-

New buyers are concentrated around a cost-basis between $60,000 and $70,000, a band that could indicate a fragile cushion for a meaningful rebound unless demand strengthens.

BTC price action tightens around critical levels

Bitcoin’s price action has resumed a cautious stance, with a late-week dip into the mid-$60,000s followed by a modest rebound. Data from Cointelegraph and price-tracking services show BTC hovering around $65,000, with traders highlighting resistance near the $68,000–$69,000 zone. A breach above that range would be a notable shift, while failure to reclaim higher ground keeps the market in a downbeat configuration.

Analysts underscored a pattern of lower highs and a break below prior support, signaling renewed short-term bearish momentum unless BTC can reclaim the $69,000–$70,000 area. In a Telegram update circulated to subscribers, a popular observer noted that the formation of a bear-flag structure on shorter timeframes points toward a continued path of least resistance to the downside unless price quickly reclaims the higher band around $69,000–$70,000.

Market chatter through the week framed this as a continuation of a broader bearish setup that has been developing since mid-March, with traders wary of a potential retest of the mid-$60,000s. Previous cycles have shown that the price must break above the immediate resistance to alter the near-term tilt; otherwise, the scenario remains skewed toward further downside toward a demand zone near $65,000.

Macro headwinds: geopolitics, energy, and monetary policy

Macro markets remain highly sensitive to geopolitical developments in the Middle East, where ongoing tensions are affecting energy prices and risk assets. Reports drawing attention to the potential for further escalation have kept oil markets elevated and injected volatility into equities and crypto alike. As the energy complex tightens and inflation dynamics stay in focus, traders are closely watching how policy signals will adapt to a higher-for-longer inflation regime.

Market commentary has connected these geopolitical and energy factors to broader risk sentiment, noting that tensions surrounding the Strait of Hormuz and related supply constraints can propagate into inflation expectations and the pricing of longer-dated rates. In parallel, a softening in equities has coincided with fading bets on rate cuts this year, a dynamic that has historically correlated with renewed caution in Bitcoin and other risk assets.

Observers point to the Fed’s policy outlook as a crucial hinge for crypto markets. With expectations for significant near-term rate relief waning, long-dated yields have moved higher on inflation concerns, complicating the prospect of any quick crypto rebound. Analysts at market-monitoring firms have highlighted that the combined effect of energy-price pressures and a cautious stance on monetary easing could keep upside momentum contained for Bitcoin in the near term.

April on the horizon? Historical context and potential mean reversion

March is shaping up to be a difficult month for Bitcoin, with data-tracking firms signaling a possible continuation of a six-month losing streak. CoinGlass data shows BTC on the cusp of closing March in the red, maintaining a structure that would echo the strongest downtrends Bitcoin has faced in recent cycles.

Some traders point to historical patterns where April has been more forgiving or even positive for Bitcoin. A number of market observers have highlighted that, in past cycles, April has yielded meaningful upside after a prolonged downturn, though much depends on macro conditions and liquidity flows. One analyst noted that early April strength could set up mean-reversion longs, particularly if broader macro conditions stabilize and Bitcoin retrieves risk-appetite from other assets.

The discussion around April’s potential gains is tempered by the reality that the long-term trend remains under the control of larger-timeframe structure. Another trader emphasized that while a fast bounce is possible, the overarching trend has not yet reversed without a clean break above the defined resistance level and a shift in on-chain demand dynamics.

Whales, liquidity, and the new-buyer base

On-chain dynamics reveal an evolving balance between accumulation and distribution. After an aggressive early-2026 phase of buying, Bitcoin whales have started to pare back some exposure, with analysts noting a divergence between on-chain accumulation and actual supply inflows to exchanges. In a quick-take assessment, CryptoQuant highlighted rising exchange inflows alongside a drop in on-chain buying, suggesting the market could face renewed selling pressure without fresh inflows of demand from buyers at scale.

That narrative is reinforced by stablecoin activity: the stablecoin ratio has remained subdued, indicating a relative dearth of sidelined capital waiting to re-enter the market. As a result, any renewed selling pressure from whales could find limited immediate liquidity, making price moves more sensitive to the available bid depth and to new buyers stepping in at meaningful volume.

Glassnode’s data adds nuance to the debate about demand and supply. The firm pointed out that a notable portion of new Bitcoin buying is concentrated in a cost-basis band between $60,000 and $70,000. While this indicates that new buyers are entering the market, the overall cluster is thinner than past cycles that followed strong recoveries. In other words, a sustained rebound would likely require a clearer uptick in demand rather than a mere reallocation of existing liquidity.

Beyond the headline numbers, the broader takeaway is that a meaningful recovery requires a shift in both macro conditions and on-chain demand. Short-term holders remain underwater for much of their holdings, reinforcing the sense that fresh buyers and renewed risk appetite will be essential to re-accelerate BTC higher.

This article is prepared with reference to market data and commentary from CoinGlass, CryptoQuant, Glassnode, and Mosaic Market, among others, to frame the ongoing crypto-price dynamics against a backdrop of macro and liquidity trends.

This article is produced in accordance with editorial policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions.

What to watch next: a clear shift above the $68,000–$69,000 zone could retarget the immediate resistance and potentially alter the near-term outlook, while continued macro fragility could keep Bitcoin tethered to the current range. market participants will also monitor on-chain signals for renewed demand and any changes in whale behavior as the market moves into April.

More than half of cryptocurrency investors don’t understand the fundamental concept of taxability when it comes to their digital asset holdings, according to a survey by the U.S.-listed crypto exchange Coinbase (COIN) and Cointracker, a crypto tax and portfolio tracking platform.

The 2026 Crypto Tax Readiness Report found that only 49% correctly understand that crypto is taxable anytime it is sold, while almost a quarter mistakenly believe simple transfers trigger tax events.

Despite the majority of users having good intentions when it comes to crypto tax compliance, the multi-platform reality of crypto ownership exacerbates the so-called cost basis problem, deducting the original purchase price of an asset to report capital gains.

The survey found users averaged 2.5 platforms/wallets with 83% using self-custodial wallets, and only 35% reporting that they’d adjusted their cost basis in the past. The survey, conducted in late 2025, surveyed 3,000 U.S. crypto users.

The confusion around cost basis in the new 1099-DA forms is made worse thanks to a degree of overreporting built into the new regime, Coinbase says. This is because everyday activities like stablecoin payments and Ethereum gas fees trigger taxable events, while generating little meaningful tax revenue.

Coinbase said it expects to issue over four million 1099-DAs Forms to customers with under $600 of proceeds – added to the fact that over 60 percent of its customers have incomplete cost basis data due to the way digital assets move across wallets and platforms.

“Today, that means every stablecoin payment, every small DeFi [decentralized finance] transaction, every gas fee is technically a taxable event,” Coinbase said. “The compliance burden this imposes on ordinary Americans isn’t just inconvenient – it’s a direct threat to the adoption and innovation the GENIUS Act was designed to unlock.”

Despite the wrinkles, the move to standardized reporting of crypto taxes will help adoption in the long run, said Matt Price, director of investigations at blockchain analytics firm Elliptic. Price, a former IRS special agent focused on criminal investigations, sees this as a shift toward targeted enforcement rather than the broad, manual investigations of the past.

Also a former head of investigations at Binance, Price understands the complexity of doing crypto taxes, having been paid partly in crypto by Binance and having to account for a volatile asset in the form of a payment.

“How do you even report it?” Price said in an interview. “I didn’t even have a 1099 to report that, so I had to essentially do all of my own accounting to file accurate taxes to account for that information.”

As such, the arrival of 1099-DA forms means welcome standardization that simply brings crypto in line with what other financial products have had for years and mirrors the approach of the 1099-B for brokerages.

“There’s certainly nuance and it’s a fair point that the basis is harder to calculate given the high frequency of trading,” Price said. “But there are some parallels to that in traditional investments as well; I don’t know how many retail traders are running algo trades on Schwab, for example, but that is also a very similar type of trade. If they can figure it out, I think the industry can probably figure it out.”

- XRP rises to $1.36 on institutional optimism and CEO remarks.

- Technical relief bounce supported by oversold conditions and volume surge.

- Key levels to watch are the support at $1.33 and the resistance at $1.40.

XRP has seen a notable lift in the past 24 hours, climbing to $1.36 and outperforming much of the broader market.

The rally appears to be driven by a combination of technical relief and renewed confidence from institutional investors.

Over the past 24 hours, trading volume surged nearly 50%, signalling that buyers are stepping in after the recent oversold conditions.

Ripple CEO commentary sparks optimism

A major factor behind this price movement is the recent commentary from Ripple’s CEO, Brad Garlinghouse.

In a March 27 Fox interview, Garlinghouse highlighted a growing demand for digital assets and stablecoins from traditional financial institutions.

He emphasised that the crypto landscape is maturing, with more banks and investment firms considering digital assets as part of their portfolios.

Garlinghouse also underscored progress on regulatory fronts, particularly regarding the anticipated CLARITY Act.

The CEO indicated that the act could provide clearer guidelines for crypto operations, fostering confidence among institutional participants.

The combination of regulatory clarity and increased interest from financial firms has sent a strong signal to traders.

Market participants appear to be reacting positively, interpreting the remarks as validation that XRP is positioned for broader adoption in the traditional finance sector.

Reports of large institutional XRP holdings, such as Goldman Sachs’ exposure through XRP ETFs, have further reinforced the bullish narrative.

Technical relief supports the bounce

Alongside these fundamental drivers, XRP’s technical indicators also support the recent surge.

The 14-day Relative Strength Index (RSI) had dipped to around 44, indicating that the asset is approaching oversold territory, which has created conditions for the bounce as selling pressure eases and buyers re-enter the market.

Moreover, XRP’s price gained modest tailwinds from a slight recovery across the broader crypto market.

While the overall market movement was subdued, it contributed to the momentum that carried XRP higher.

The short-term XRP price forecast

For traders watching the immediate market, $1.33 remains a critical support level.

Remaining above this support will be crucial for any attempt to test higher levels.

In case of a continued bullish trend and XRP breaks above $1.40, analysts believe the altcoin could see additional buying pressure and extend the current relief rally.

Other notable resistance levels that traders should watch include $1.45, which has acted as a ceiling over the past week.

Sustaining momentum beyond this level could open the door to a more meaningful uptrend.

However, failure to hold $1.33 could result in a pullback toward $1.30, where buyers may re-enter.

Notably, regulatory developments, particularly progress on the CLARITY Act, will be the key catalyst in the coming weeks.

Positive news could encourage further institutional participation, while delays might keep XRP trading within the $1.30–$1.40 range.

Key Takeaways

- ARTL shares skyrocketed 618% following the company’s announcement about developing ART27.13 as a complementary treatment for GLP-1 obesity medications.

- Shares plummeted over 23% Monday when Artelo disclosed a $31.4 million fundraising initiative involving share and warrant issuance.

- The company plans to issue roughly 3.18 million shares priced at $3.45 each, generating approximately $11 million in gross revenue.

- Warrant agreements for up to 6.37 million additional shares could yield another $20.4 million if fully exercised by investors.

- The financing arrangement was structured at-the-market under Nasdaq compliance guidelines and was scheduled to finalize on March 30.

Shares of Artelo Biosciences experienced a significant downturn exceeding 23% during early trading Monday following the biotechnology firm’s announcement of a financing plan targeting up to $31.4 million through combined share and warrant issuance.

Artelo Biosciences, Inc., ARTL

This sharp decline occurred after an impressive 230.41% rally the preceding Friday, which followed by two days the company’s revelation that it was investigating ART27.13, its experimental compound, as a complementary therapeutic option for GLP-1-based obesity medications.

The strategic decision to pursue capital raising immediately following such substantial share price appreciation seems to have triggered investor apprehension regarding potential ownership dilution.

Artelo revealed it executed binding agreements for the sale of roughly 3.18 million common shares at a combined offering price of $3.45 per unit. This transaction is projected to yield gross revenues of approximately $11 million prior to deducting placement fees and related costs.

Additionally, the biotechnology company intends to issue warrants providing purchasers with rights to acquire up to 6.37 million supplementary shares. Should these warrants be fully exercised through cash payment, Artelo could secure an additional $20.4 million in funding.

The company explicitly cautioned investors that warrant exercise remains uncertain. “No assurance can be given that any of the warrants will be exercised, or that the Company will receive cash proceeds from the exercise of the warrants,” Artelo stated in its official announcement.

H.C. Wainwright & Co. serves as the sole placement agent facilitating this financing transaction.

The private offering is being executed pursuant to Section 4(a)(2) of the Securities Act alongside Regulation D requirements. The offered securities remain unregistered under federal and state securities regulations. Artelo has committed to submitting a resale registration statement encompassing the newly issued securities.

Capital generated from this financing will be allocated toward operational expenses, settlement of specific bridge financing obligations, and broader corporate initiatives.

ART27.13’s Role in the GLP-1 Treatment Landscape

The initial dramatic price increase stemmed from Artelo’s Wednesday disclosure regarding its exploration of ART27.13 — an investigational therapeutic targeting the endocannabinoid system — as a possible adjunct therapy to GLP-1 medications.

GLP-1 therapeutics, which regulate glucose metabolism and appetite control, represent the cornerstone of the rapidly expanding obesity pharmaceutical market. This sector is currently led by Eli Lilly (LLY) and Novo Nordisk (NVO).

According to Artelo, previous clinical observations in oncology patients indicated that ART27.13 might help maintain lean muscle tissue in individuals receiving GLP-1 treatments. The company has subsequently submitted a provisional patent application addressing this therapeutic indication.

“With new non-clinical research commencing and the recent filing of a patent application covering the use of CB2 agonists with GLP-1 drugs, we are aiming to build a scientific and strategic foundation with ART27.13 in an area of potentially significant commercial relevance,” stated Andrew Yates, Artelo’s chief scientific officer.

TLDR:

- February 2026 funding rates landed in the bottom 3–15% of all historical monthly readings across major tokens.

- Every bottom-15% funding rate streak on record has recovered, with a median timeline of two to five weeks.

- SOL on Hyperliquid posted -18.33% annualized in February, the lowest reading ever recorded across all tracked pairs.

- Boros allows traders to long ETH funding rate markets and lock in fixed rates ahead of an expected mean reversion.

Funding rates across major crypto perpetual markets are raising a critical question: has the market finally bottomed?

After Bitcoin shed over 50% from its October 2025 all-time highs, perpetual funding rates collapsed to historic lows in February 2026.

Most major tokens recorded readings in the bottom 5% of all-time monthly data. Now, with crypto prices rallying despite US-Iran war escalations, traders are watching funding rates closely for early reversal signals.

February 2026 Funding Rates Dropped to Levels Never Seen Before

Funding rates in February 2026 were not just low — they were structurally outside the normal range of market history.

BTC on Binance recorded an annualized rate of -0.68%, placing it in the bottom 4.5% of all 66 months on record. That reading alone sat 12 percentage points below BTC’s historical mean of 11.8%.

ETH told an even sharper story. Binance recorded ETH at -4.03% annualized, landing in the bottom 3% of all historical monthly readings.

Hyperliquid and Lighter posted similarly depressed figures, with ETH sitting in the bottom 15% and bottom 20% respectively across those platforms.

XRP and SOL absorbed the worst damage of the month. XRP on Hyperliquid posted -12.77%, the single worst month in that market’s entire recorded history.

SOL on Hyperliquid came in at -18.33%, the lowest absolute reading among all tracked pairs across every platform.

The deviation from historical medians reinforces just how extreme the period was. SOL on Hyperliquid deviated 29.2 percentage points from its median.

BTC on Binance, the least extreme major, still deviated 7.0 percentage points. For most tokens, February was not simply a bad month — it was an anomaly by every measurable standard.

Historical Patterns Suggest These Lows Have Always Preceded a Recovery

The most telling data point in this analysis is also the simplest: every bottom-15% funding rate streak in the historical record has recovered.

That pattern holds across multiple assets, exchanges, and market cycles, including the FTX collapse of November 2022.

The median recovery time back to the bottom 55% of funding rates runs roughly two to five weeks after the streak ends.

BTC provides the clearest evidence. Its longest Binance bottom-15% streak lasted 11 weeks, beginning in March 2025.

Most other BTC streaks recovered within one to five weeks. An extended eight-week streak on Hyperliquid in mid-2023 resolved fully within five weeks of ending.

ETH’s most severe historical episode in late August 2022 averaged -18.6% over five weeks. That took 12 weeks to recover to the bottom 55%, the longest recovery on record for ETH.

More recent episodes, however, including early 2025 streaks, resolved in one to five weeks, suggesting the recovery window is compressing as the market matures.

SOL’s November 2022 streak, driven by the FTX collapse, averaged an extraordinary -468.9% annualized. Despite that severity, Binance SOL recovered to the bottom 20% within seven weeks.

Each of these cases points toward the same conclusion: deeply negative funding rates have historically acted as a contrarian signal for a coming recovery, not a permanent new baseline.

Funding Rate Markets on Boros Allow Traders to Position for the Rebound

If funding rates are indeed at a cyclical bottom, the question becomes how traders can express that view efficiently.

Boros, a funding rate derivatives platform, offers two structured approaches for traders looking to capitalize on a mean reversion in funding rates.

The first strategy targets traders who believe ETH prices will recover over the next three months. By longing ETH on any of the three platforms with June maturities — OKX, Binance, or Hyperliquid — and simultaneously longing the ETH funding rate market on Boros with the same notional amount, traders lock in a fixed funding rate. This protects against funding spikes while maintaining full upside exposure to ETH price recovery.

The second strategy is for traders focused purely on funding rate normalization, regardless of price direction. Longing ETH funding rate markets on Boros directly captures any upward move in implied or underlying APR.

The recommended approach is selecting the maturity with the lowest current implied APR to maximize the distance of a potential recovery move.

Implied APR across June ETH maturities currently sits between 2% and 5% annualized, reflecting cautious market expectations for a gradual recovery.

If underlying APR breaks its downtrend and flips positive, traders long on Boros benefit both from rising implied APR and from positive settlement payouts once underlying APR exceeds their entry point.

The Data Points to an Asymmetric Opportunity, But Margin Management Is Critical

Taken together, the February 2026 funding rate data builds a case for an asymmetric setup. Rates have reached historic lows across virtually every major token and exchange.

Historical recovery patterns are consistent. And crypto prices have already begun recovering despite ongoing geopolitical pressure, a divergence that traders are noting carefully.

Extended periods of negative funding have historically reflected consolidating or ranging markets. As Boros observed, those periods of extended low funding have always eventually ended. The question is not whether rates recover, but when — and whether traders are positioned to benefit when they do.

For those looking to long mean reversion, timing the exact bottom is not necessary. The historical data suggests the recovery window after a streak breaks is two to five weeks, giving traders a defined timeframe to manage positions. The risk is sustaining negative funding payouts during the remaining period of the streak before it turns.

Adequate margin is therefore the most important operational variable for this trade. A trader who enters too early with insufficient runway may be forced out before the recovery materializes.

The setup, however, remains compelling: deeply negative historical funding rates, a consistent track record of recovery, and structured tools through Boros that allow both fixed-rate locking and directional funding rate speculation.

TLDR:

-

- Gnosis is a founding contributor to the Ethereum Economic Zone alongside Jordi Baylina and the Ethereum Foundation.

- EEZ rollups allow smart contracts to call Ethereum mainnet contracts atomically within a single transaction.

- Protocols on EEZ rollups access Ethereum’s native liquidity directly without wrapping, bridging, or extra delays.

- Gnosis plans to define the role of GNO token and its validator set in any future EEZ implementation with its DAO.

- Gnosis is a founding contributor to the Ethereum Economic Zone alongside Jordi Baylina and the Ethereum Foundation.

Ethereum Economic Zone is the framework Gnosis is co-building to address Layer 2 fragmentation on Ethereum. Gnosis, active as a Layer 1 blockchain for seven years, is a founding contributor to this initiative.

Jordi Baylina, founder of ZisK and creator of Circom, also joins as a founding contributor. The Ethereum Foundation is also co-funding the entire development effort.

The framework centers on synchronous composability, enabling rollups to interact with Ethereum mainnet without bridges.

A Framework Built Around Composability

Ethereum scaling delivered on its core promise in recent years. Transactions became cheaper and network throughput increased steadily. However, the process fractured the ecosystem into disconnected chains rather than one unified economy.

Each rollup operates with its own liquidity, bridges, and tooling. Builders must redeploy the same products across multiple chains to reach all users. Users also face expensive bridging costs and assets scattered across chains they barely track.

Gnosis noted on X that Ethereum had scaled into fragmented islands rather than a unified economy. The Ethereum Economic Zone is designed to resolve that at the infrastructure layer. The framework allows rollup smart contracts to call Ethereum mainnet contracts within one transaction.

Calls between different rollups within the same execution are also supported. This is what developers call synchronous composability. It removes the need for bridges, wrapping, or waiting on finality.

Protocols on EEZ rollups access Ethereum’s existing liquidity directly without bridging or wrapping. A protocol can use a Uniswap mainnet pool atomically, with the same L1 guarantees. These rollups also inherit Ethereum’s full validator security with no new trust assumptions added.

What the Ethereum Economic Zone Means for Gnosis Chain

Gnosis acknowledged that its neutral blockspace thesis did not develop as expected. Blockspace became largely commoditized across the industry over time. Running a standalone Layer 1 requires constant rebuilding of DeFi infrastructure and liquidity bootstrapping.

Synchronous interoperability changes the competitive dynamic for chains like Gnosis. Projects inside a composable Ethereum domain no longer need to replicate an entire ecosystem. They can rely on shared liquidity and canonical infrastructure instead.

That shift frees up capital and engineering bandwidth for differentiation. Gnosis plans to invest more in user experiences and products like Gnosis Pay and the Gnosis App. Real-world financial integrations also become more practical under a unified model.

The Ethereum Economic Zone also connects to Gnosis’s mission of giving every person financial access. A stablecoin can now compose with a lending protocol on another chain without a bridge. A consumer app can also access the best rates across the ecosystem without workarounds.

Gnosis noted that the GNO token and validator set may have a role in a future EEZ implementation. Those details will be worked out with the Gnosis DAO community over the coming months. Technical architecture, developer tooling, and integration guides are also planned for release soon.

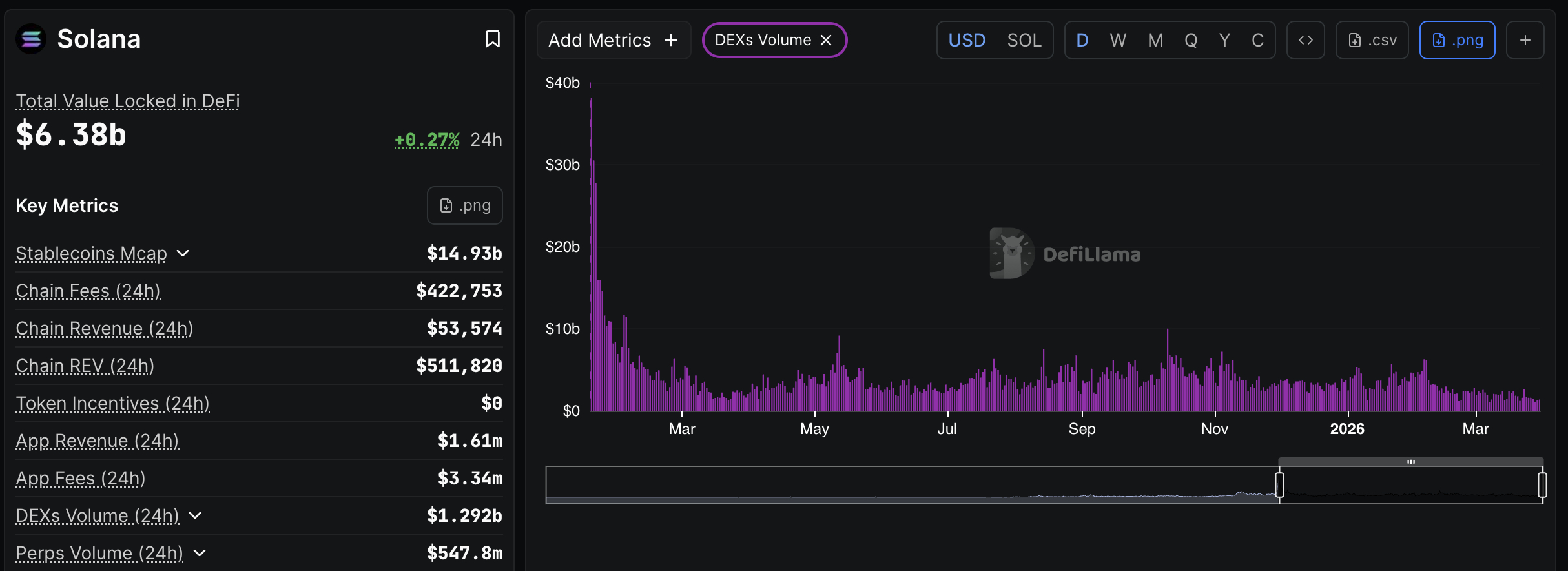

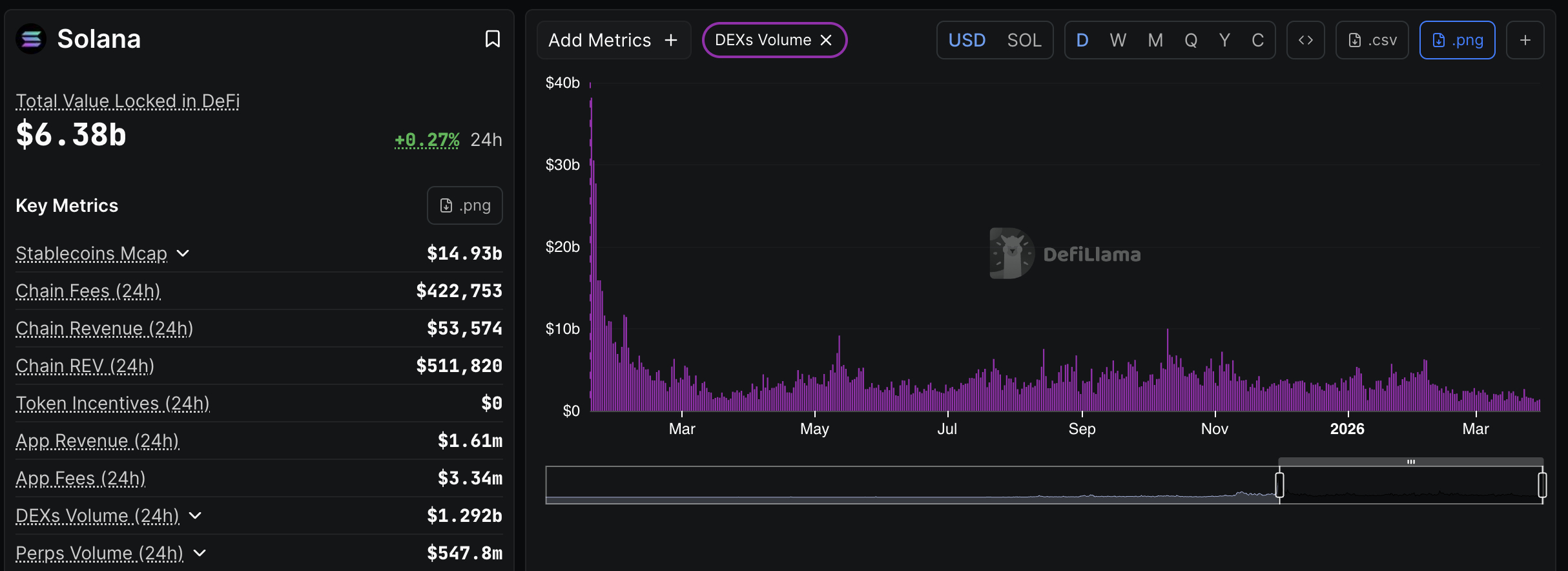

Solana is trading at $84, the price is down 71% from its January 2025 peak of $293, as weekly DEX volume collapses to levels not seen since early 2025, even with bullish prediction and hope. The memecoin engine that once powered Solana’s on-chain dominance is stalling.

For Solana, the next 72 hours around the Federal Reserve’s March 17–18 meeting could determine whether $80 holds or gives way entirely. One technical pattern already has a $59 target in view.

Weekly DEX volume across all networks registers at just $1.2B, way down from its $41B peak. Broader crypto market weakness in Q1 2026 hammered token speculation, with DEXs now capturing just 14.1% of centralized exchange volume, down sharply from a 21%+ peak in summer 2025.

Solana still commands the largest individual network share at $11.42B, its 30th consecutive month leading peers, propped up by persistent PumpSwap and Pump.fun activity, but even that moat is narrowing as “star token” launches dry up.

The macro and technical backdrops are converging at a critical juncture. Here’s what the data suggests about SOL’s near-term path, and where traders are repositioning capital while waiting for clarity. Deep dive into our Solana Price Prediction

Discover: The best pre-launch token sales

Solana Price Prediction: Can Solana Reclaim $96 Support?

SOL sits at $84, pinned below the $86 pivot that separates consolidation from any credible recovery attempt. Volume metrics have been deteriorating alongside price, a combination that technically confirms distribution rather than accumulation.

RSI sits at a neutral 50 area, not oversold enough to trigger mean-reversion buying on its own, while the 50-, 100-, and 200-day SMAs all signal sell. The 200-day MA has been rising since March 9, which is the one structural bright spot bulls can point to.

The head-and-shoulders pattern on the three-day chart is the dominant concern. A confirmed break below $80, assigned a 38.5% probability by current market structure, triggers the measured move toward $59. That would represent a further 28% decline from current levels. Resistance to reclaim sits at $96 first, then $105.

Discover: The best crypto to diversify your portfolio with

Maxi Doge Is an Early Mover With Upside Potential

When a leading L1 trades 70% off its highs, and DEX volumes hit annual lows, the rotation question becomes unavoidable: where does speculative capital go while waiting for the cycle to reset? Memecoin sentiment hasn’t disappeared; it has compressed, historically a precursor to violent repositioning once fear fades.

Maxi Doge ($MAXI) is a meme token built on Ethereum’s ERC-20 standard, positioning itself around what it calls “1000x leverage trading mentality,” with a canine mascot embodying the grind-and-hold bull market ethos.

The project has raised $4,7 million at a current presale price of just $0.000281, with 60% staking APY available to holders. Standout mechanics include holder-only trading competitions with leaderboard rewards and a Maxi Fund treasury allocated toward liquidity and partnerships.

Research MAXI DOGE here, and join the army.

This article is for informational purposes only and does not constitute financial advice. Crypto assets are highly volatile. Always conduct your own research before investing.

The post Solana Price Prediction: DEX Activity Slumps to 1 Year Low as Memecoin Frenzy Fades appeared first on Cryptonews.

The Ethereum Foundation is stepping up its efforts to put treasury assets to work, with data from Arkham showing it staked more than 20,000 ETH on Monday, expanding its validator footprint even as yields hover below 3% and ether trades near $2,045.

Arkham data shows the transfers were split into uniform chunks of roughly 2,047 ETH.

THE ETHEREUM FOUNDATION IS STAKING ETH

The Ethereum Foundation just staked $46.2M of ETH. This is more ETH than they have EVER staked before. pic.twitter.com/gCCc0qK6VN

— Arkham (@arkham) March 30, 2026

The deposits extend a strategy first outlined in February, when the foundation said it would stake 70,000 ETH to generate yield for operations. That initial roll-out began with a 2,016 ETH deposit and positioned staking rewards as a funding source for research, ecosystem development and grants, turning long-held reserves into a steady income stream.

Based on the CoinDesk Composite Ether Staking Rate (CESR), the foundation will get a 2.7% yield from its staked ETH. This is down from 3.4% earlier in the year.

Onchain data shows that the Ethereum Foundation has another 147,400 ETH ($303 million) in its treasury.

XRP, Bitcoin, and USDC users are earning up to $11,600 daily using Confluxcapital

Israeli settler attacks intensify against Palestinians in West Bank

French football team ends American friendlies on high success

-

NewsBeat5 days ago

NewsBeat5 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

News Videos4 days ago

News Videos4 days agoParliament publishes latest register of MPs’ financial interests

-

Sports7 days ago

Sports7 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

NewsBeat3 days ago

NewsBeat3 days agoThe Story hosts event on Durham’s historic registers

-

Business4 days ago

Business4 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

News Videos7 days ago

News Videos7 days agoCh 9 Financial Management Part 1 | Detailed One Shot | Class 12 Business Studies Boards 2026

-

NewsBeat5 days ago

NewsBeat5 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Entertainment7 days ago

Entertainment7 days agoCynthia Bailey Dishes on ‘RHOA’ Season 17, Discusses Kandi

-

Tech7 days ago

Tech7 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

Entertainment2 days ago

Entertainment2 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Fashion6 days ago

Fashion6 days agoDoes It Matter What You Wear When You’re Laid Off and Looking?

-

NewsBeat7 days ago

NewsBeat7 days agoColombian military plane with 110 soldiers onboard crashes following takeoff

-

Business6 days ago

Business6 days agoMore women enter wealth management, but few in advisory roles: study

-

Fashion7 days ago

Fashion7 days agoFringe Bags for the Season

-

NewsBeat6 days ago

NewsBeat6 days agoEntrepreneurs Forum survey reveals optimism in North East

-

NewsBeat6 days ago

NewsBeat6 days agoNASA Artemis II Astronauts enter 14-Day quarantine as moon rocket reaches launchpad

-

Business6 days ago

Business6 days agoLate-paying firms face multimillion-pound fines under new crackdown

-

Politics7 days ago

Politics7 days agoHow Media Platforms Balance Performance and Accessibility in Image Delivery

-

Crypto World6 days ago

Crypto World6 days agoBTC gives up $70,000 level as markets mull higher interest rates

-

Sports5 days ago

Sports5 days agoFantasy Baseball Week 1 Preview: Top sleeper hitters for both five- and 12-day period led by Munetaka Murakami

You must be logged in to post a comment Login