Nearly all of Puerto Rico was without power Tuesday after the fragile electricity grid collapsed, triggering an island-wide blackout.

Nearly all of Puerto Rico was without power Tuesday after the fragile electricity grid collapsed, triggering an island-wide blackout.

Mirumi is the latest strange robot from Yukai Engineering It hangs on your bag It can “react” Gadgets that elicit comments like “Why?” and “Is [more…]

Get the free Morning Headlines email for news from our reporters across the world Sign up to our free Morning Headlines email Sign up to [more…]

[matched_con] Source link

Get the free Morning Headlines email for news from our reporters across the world Sign up to our free Morning Headlines email Sign up to [more…]

Match of the Day 2 pundit Alan Shearer analyses Liam Delap’s performance in Ipswich Town’s 2-2 Premier League draw with Fulham and says England manager [more…]

Why not try learn how to prepare a variety of your favourite traditional Catalan dishes and other worldwide favourites, during your visit to the beautiful [more…]

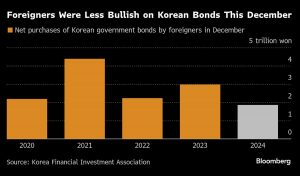

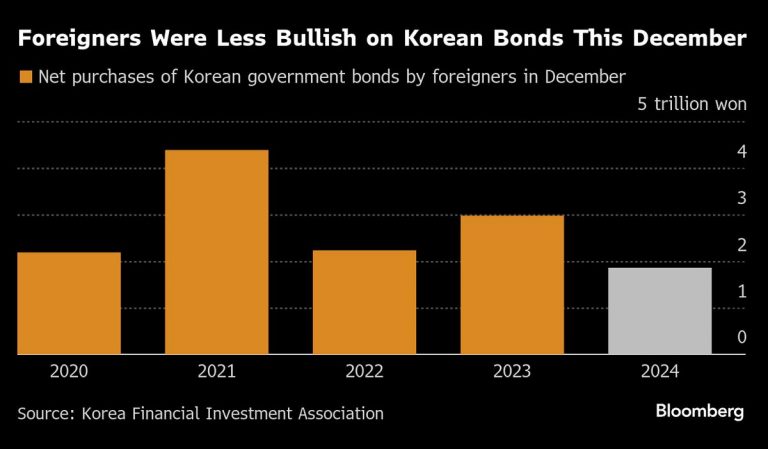

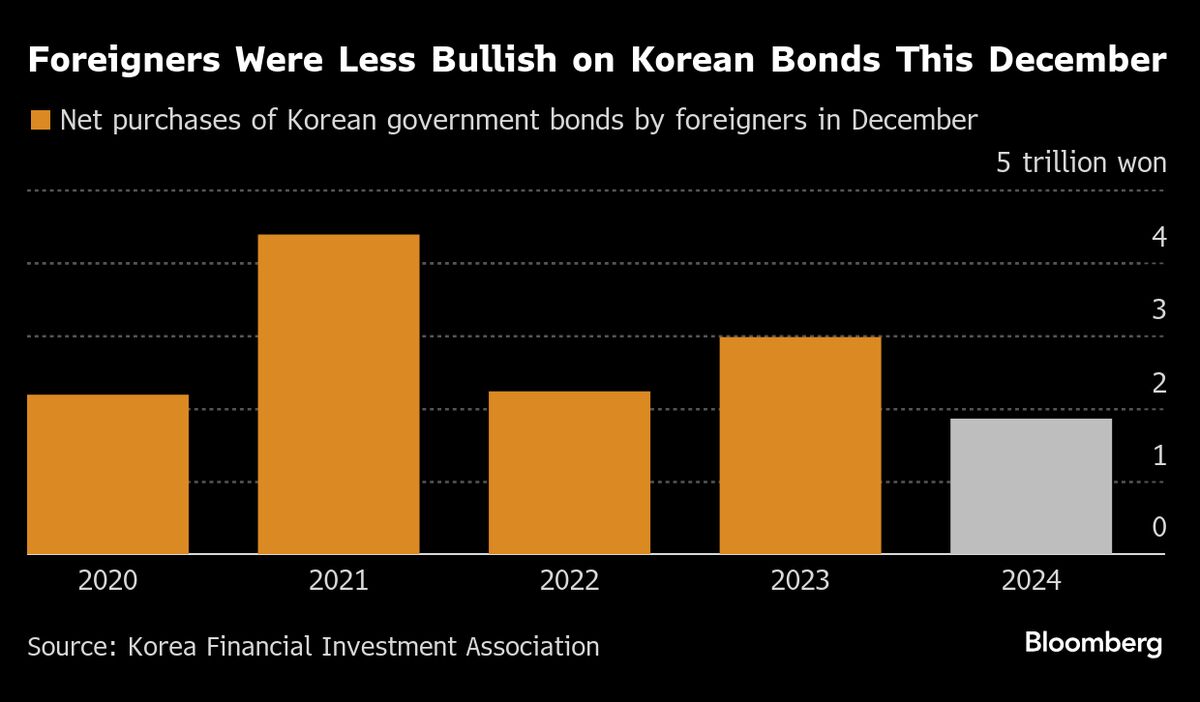

South Korea was spared a financial maelstrom even as it battles a political crisis, underscoring the extent to which its markets have matured, bolstered by [more…]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

+ There are no comments

Add yours