Crypto World

Coinbase Returns to the Super Bowl with a Quirky Lo-Fi Karaoke Ad

Coinbase has returned to the Super Bowl with a bold, nostalgia-forward spot that eschews hard sells in favor of a shared cultural moment. Four years after its viral QR-code stunt, the exchange leaned into a Backstreet Boys karaoke-inspired concept, letting the lyrics of “Everybody (Backstreet’s Back)” flash across the screen in a one-minute montage. Marketing chief Catherine Ferdon described the creative as a deliberate attempt to spark a communal experience and to illustrate how the crypto community has evolved beyond a niche interest. The move comes as Coinbase seeks to sustain mainstream visibility at a time when crypto brands are navigating a dense regulatory backdrop and mixed public sentiment, rather than relying solely on direct product demonstrations.

The execution centers on text animation and a simple premise: a catchy, universally recognizable tune that listeners can sing along to, with the goal of memory and sharing rather than a traditional call to action. In that sense, the ad mirrors a broader approach in crypto marketing that prioritizes cultural resonance and broad memorability to drive top-of-munnel awareness, rather than relying on flashy product showcases alone. The spot’s design choices—minimal on-screen branding, a familiar chorus, and a single point of reference—signal Coinbase’s intent to let the moment carry the conversation rather than to funnel viewers immediately into signing up or downloading an app.

Coinbase’s 2026 appearance follows a notable high-water mark in 2022, when the company staged a color-shifting QR-code commercial that bounced across the screen and directed viewers to a sign-up link. The campaign, which offered BTC to new users, reportedly crashed Coinbase’s site and drew millions of visits in a matter of minutes, underscoring the game-changing reach of the Super Bowl for crypto marketing. The 2022 effort featured a simple hook and a sense of immediacy—an approach that Coinbase appears to be reinterpreting this year, albeit through a different cultural lens that hinges on shared experience rather than a direct promotional offer.

Key takeaways

- Coinbase returns to the Super Bowl with a one-minute, lyric-driven ad that emphasizes communal experience over a direct product pitch.

- The creative choice leans on nostalgia and a universally known song to foster memorability and discussion among a broad audience.

- The company’s earlier QR-code stunt in 2022, which steered viewers to a Bitcoin (CRYPTO: BTC) signup link, demonstrated the explosive potential of Super Bowl exposure for crypto brands, even as it overwhelmed the site.

- Public reactions online were mixed—some praised the simplicity and recall value, while others criticized the tone or timing amid market volatility and regulatory scrutiny.

- Coinbase executives defended the campaign as a breakthrough moment designed to “break through” in a crowded media landscape and to celebrate the crypto community’s growth.

Tickers mentioned: $BTC, $ETH

Sentiment: Neutral

Market context: The ad lands in a period of heightened attention to crypto brands in mainstream media, where reach and resonance compete with heightened regulatory scrutiny and evolving consumer attitudes toward digital assets. It underscores a trend of brands using high-visibility events to shape narrative and familiarity around crypto, even as market conditions and policy debates continue to influence user acquisition and brand trust.

Why it matters

The Super Bowl spotlight is a rare opportunity for a crypto brand to move beyond technical jargon and reach a broad audience in a single, high-impact moment. By leaning into a communal, sing-along moment, Coinbase aims to embed itself in cultural memory, potentially boosting long-term recognition even among viewers who may not immediately engage in on-chain activity. The choice to foreground lyrics over a product feature suggests a shift toward brand-building as a gateway to eventual product adoption, especially as consumer perception of crypto oscillates between curiosity and caution.

From an investor and builder perspective, the campaign signals that Coinbase is prioritizing media presence and narrative control as part of a diversified strategy to attract new participants to the ecosystem. The reference to past performance—most notably the 2022 QR-code stunt that prompted a flood of sign-ups and traffic—highlights the outsized impact that large-scale media events can have on user interest and platform exposure. In a market where liquidity and risk sentiment swing with macro headlines, such brand visibility can provide a unique form of non-price-driven traction, potentially widening the funnel beyond the usual crypto-native audience.

The ad also intersects with the evolving conversation around crypto advertising itself. As regulators scrutinize marketing claims and risk disclosures, the ability to generate positive topical chatter without triggering regulatory pushback becomes a delicate balancing act. Coinbase’s approach—opening a conversation through a shared cultural moment rather than a direct sign-up prompt—may influence how other players craft campaigns that are memorable yet compliant, especially when targeting mass audiences in the United States and abroad.

Within the content, the emphasis on community and accessibility is reinforced by public commentary from industry figures. An engineer from the Ethereum Foundation noted that many attendees enjoyed singing along and found the moment approachable, illustrating how a crypto-brand moment can resonate with developers and enthusiasts alike. At the same time, critics argued that such campaigns can feel performative or disconnected from the underlying realities of asset risk and regulatory risk, reminding readers that mass-media stunts do not obviate the need for transparent disclosure and responsible messaging.

Coinbase’s leadership echoed that dual message. CEO Brian Armstrong defended the ad on social media, arguing that most people engage with ads in fleeting, buzzed settings and that a distinctive moment is often required to break through. The company’s marketing chief emphasized that the objective was to create a memorable, shareable experience that mirrors the crypto community’s growth. Taken together, these statements reflect a strategic bet: that a well-timed pop-cultural moment can bolster brand familiarity and open doors for deeper engagement as crypto markets and products mature.

Looking ahead, the broader context for Coinbase and similar brands remains nuanced. Mainstream media moments can catalyze new user interest, but they also invite scrutiny about risk disclosure and the real-world implications of crypto ownership. In parallel, the industry will likely watch for how such campaigns influence long-run adoption, whether subsequent campaigns lean into similar cultural cues, and how regulators respond to creative advertising that touches on financial products without overtly directing purchases.

What to watch next

- Monitor Coinbase’s post-campaign metrics: social engagement, traffic spikes, and any uptick in new sign-ups or app activity following the ad.

- Watch for further brand campaigns from Coinbase or rival exchanges that blend pop culture with crypto messaging, testing the balance between reach and regulatory compliance.

- Assess regulatory and policy developments that could influence future advertising strategies for crypto services, including disclosures and consumer protections.

- Track sentiment shifts across social platforms as viewers reflect on the impact of the ad and potential influence on purchasing behavior or sign-up decisions.

- Follow public comments from Coinbase leadership for signals about how the company plans to sustain broad awareness while navigating market cycles and evolving consumer expectations.

Sources & verification

- Official statements from Coinbase marketing chief Catherine Ferdon describing the ad’s intent and experience-driven approach.

- Post by Coinbase CEO Brian Armstrong on X defending the campaign’s approach to break through with audiences.

- Historical reference to Coinbase’s 2022 QR-code Super Bowl spot and its reported traffic impact, including the sign-up link associated with Bitcoin (CRYPTO: BTC).

- Public comments from Ethereum Foundation engineer Chase Wright on reactions to the ad in social conversations.

- Media coverage and analysis of online reception, including diverse opinions on the ad’s simplicity, memorability, and timing amid market conditions.

Key figures and next steps

Coinbase’s campaign demonstrates a continued appetite for mass-media engagement as a path to broader crypto familiarity. While the short-term impact on sign-ups or asset prices remains debatable, the larger takeaway is clear: brands are experimenting with entertainment-led formats to connect with diverse audiences, and the crypto sector is not shying away from mainstream stages.

For readers and market participants, the episode underscores the importance of separating hype from fundamentals. A single advertising moment can raise awareness, but sustained growth hinges on clear disclosures, measured risk communication, and a product-and-ecosystem narrative that withstands scrutiny and evolves with user needs.

- StakeStone price jumped from $0.11 to above $0.26, going vertical amid a spike in daily volume.

- The sharp gain follows a whale accumulating over 25.5 million STO tokens.

- STO price could see a steep pullback amid profit-taking deals.

StakeStone (STO) price exploded during early trading on April 1, pumping more than 130% to hit a new all‑time high.

The vertical action, which occurred amid a broader consolidation across the crypto market, saw STO’s intraday trading activity surge.

The token is in price discovery, but can the lofty levels hold?

Why StakeStone jumped 136% today

STO token posted a sharp intraday surge on Wednesday, significantly outperforming the broader altcoin market.

While most cryptocurrencies traded near key support levels, STO jumped from around $0.11 to a new all-time high above $0.26.

The move marked a gain of roughly 136% and made it the top performer among the 500 largest cryptocurrencies by market capitalisation.

The rally appears to have been driven by a large transaction linked to a newly created wallet.

Data from Lookonchain shows the wallet withdrew more than 25.5 million STO tokens, valued at over $4.85 million, from Binance.

The holdings represent approximately 11.32% of StakeStone’s circulating supply, suggesting concentrated accumulation that may have contributed to the sharp price movement.

The price of $STO surged from $0.11 to $0.26 today, a 136% increase.

A newly created wallet(0x5e2E) withdrew 25.5M $STO($4.85M) from #Binance in the past 20 hours, 11.32% of the circulating supply.https://t.co/UhTfZhT8CS pic.twitter.com/GAI5Y2L8LE

— Lookonchain (@lookonchain) April 1, 2026

The transfer acted as an immediate and powerful demand shock, with the size of the order absorbing available sell liquidity near the market price.

It forced quotes higher as market makers and sellers adjusted to the sudden imbalance between bids and offers.

With limited resting supply at higher levels, the price moved rapidly upward as each successive fill occurred at incrementally higher prices.

Data from CoinMarketCap shows a 560% increase in intraday volume, with over $190 million traded in the past 24 hours.

StakeStone’s market cap was also sharply up, as STO printed a new all-time high.

Prices hovered around $0.25 at the time of writing, up more than 390% since the all-time low of $0.049 on February 6, 2026.

STO price outlook — is a sharp decline next?

From a technical perspective, STO’s chart now reflects a near‑vertical candle following the 136% single‑day move.

Price currently hovers well above recent consolidation zones and historical trading ranges.

Such abrupt expansions in price and volume often leave the token looking temporarily extended.

In the market, this type of structure frequently precedes volatile retracements as the market digests the move and short‑term participants reassess risk and reward.

Given the magnitude and speed of the rally, a period of profit‑taking and a potential steep pullback cannot be ruled out.

A rapid unwind of intraday positions could see STO test lower levels, with $0.19 key.

If selling intensifies, the next major support zone could be $0.15-$0.11.

However, the reduced circulating supply could help support prices and allow for an extended, though volatile, ride to new highs.

Bitcoin (BTC) finally closed a month with positive price performance for the first time since September, but it only snapped its five-month losing streak by the slimmest of margins.

BTC opened the month at $67,000 and closed at $68,221. In other words, the entire “gain” amounted to about $1,200 per coin, or 1.8%.

For context, BTC often fluctuates by that amount within a few minutes on an average day.

Energized by even the most pitiful shred of evidence that the crypto bear market might be ending, the BTC community celebrated the momentum shift.

The Fear and Greed Index hit an all-time low of five out of 100 on February 6, 2026. It’s now much higher, if you squint a bit less, at 31.

One less bad month for BTC

The streak that preceded March’s flicker of positivity was genuinely ugly.

BTC was worth more than $126,000 on October 6, 2025. By February 6, it had collapsed to $60,000.

Recent monthly losses have been relentless. Total crypto market capitalization fell by $200 billion in October, $610 billion in November, $110 billion in December, $300 billion in January, and $350 billion in February.

March paused that decimation with a $40 billion gain, the slimmest of margins.

Still, at least it’s not as bad as its absolute worst moment this year.

BTC is 14% higher than its $59,930 low set on February 6. It’s even rallied a bit since the onset of a typically bearish war and macro environment.

Read more: Bitcoin outperforms gold as Iran war shakes ‘safe-haven’ trade

The reaction on social media revealed just how desperate BTC traders had become for any glimmer of hope.

Bitcoin Magazine announced the green close with a breathless all-caps alert, as if BTC hadn’t just spent half a year losing nearly half its value.

One popular account called it a “massive dose of hopium” before adding, perhaps wisely, “Let’s hope this is not an April Fools’ joke.”

Read more: What is @inversebrah?

The longest continuous monthly bear streak prior to this stretch was a six-month long red streak from August 2018 through January 2019.

BTC is today priced at $68,300, 46% below its October high and 23% lower year to date.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

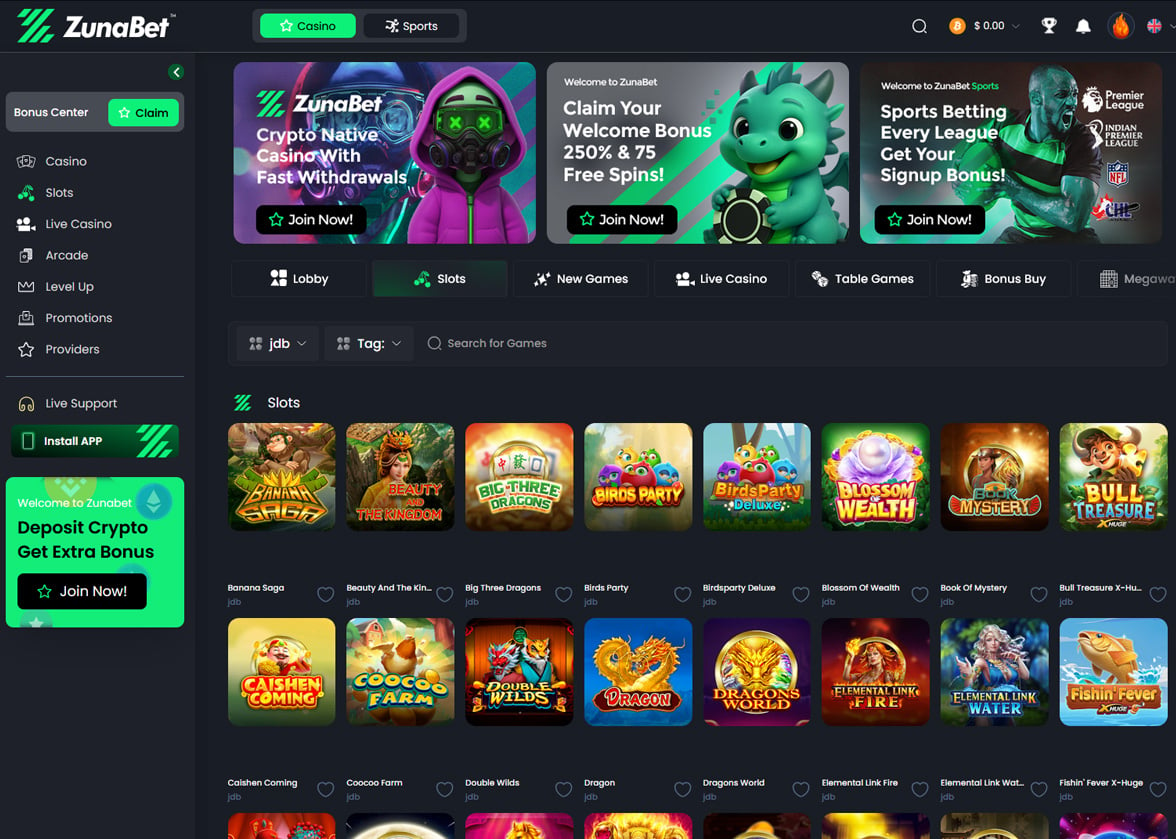

Something is shifting in the crypto casino market. Search volumes for terms like “Stake alternative,” “sites like Stake,” and “Stake.com replacement” have been climbing steadily throughout 2026. Stake.com remains one of the most visited crypto gambling platforms in the world, so the rising interest in alternatives is not about Stake failing — it is about players wanting more. More games, more bonuses, more ways to earn while they play. ZunaBet is one of the names that keeps appearing in those searches. Launched in 2026, it has quickly positioned itself as the kind of platform that players leaving or supplementing Stake are looking for. This article examines what is driving the trend and how the two platforms compare.

Stake.com: Where Things Stand

Stake.com has been a force in crypto gambling since 2017. Licensed in Curaçao, it grew rapidly by being one of the first platforms to build a serious gambling product entirely around cryptocurrency. Bitcoin, Ethereum, Litecoin, Dogecoin, and other major coins are all supported for deposits and withdrawals.

The platform made its name with a lineup of provably fair original games. Crash, Plinko, Dice, Mines, and similar titles became synonymous with the Stake brand and built a community of dedicated players. Third-party games from providers like Pragmatic Play, Evolution, and Hacksaw Gaming fill out the rest of the casino with slots and live dealer tables.

Stake also operates a full sportsbook covering football, basketball, tennis, MMA, esports, and other markets. The odds are competitive and the interface is clean, which keeps experienced bettors engaged.

For years, Stake has held a dominant position in the crypto gambling space. But dominance invites scrutiny, and players who have spent time on the platform are increasingly vocal about the areas where Stake falls short of their expectations.

Why Players Are Looking Elsewhere

The search interest in Stake alternatives does not come from nowhere. Several recurring themes show up in community discussions, forums, and social media conversations about why players are exploring other options.

The most frequently mentioned issue is the lack of a welcome bonus. Stake does not offer any deposit match, free spins, or sign-up promotion for new players. You deposit and you play with exactly what you put in. All rewards are funneled through an invite-only VIP program that activates based on sustained high-volume wagering. For players who do not wager at that level, Stake offers no additional value beyond the games themselves.

The VIP program itself generates mixed opinions. Players who have earned an invitation generally speak well of the rakeback and bonuses they receive. But the closed nature of the system frustrates everyone else. There are no published tiers, no public requirements, and no way to track your progress toward an invitation. For many players, it feels like a program that exists for someone else.

Game library size is another factor. Stake carries a solid selection, but newer platforms have launched with significantly larger catalogs, making Stake’s offering feel less comprehensive by comparison.

These gaps have created an opening in the market, and platforms like ZunaBet have stepped directly into it.

ZunaBet: What the Alternative Looks Like

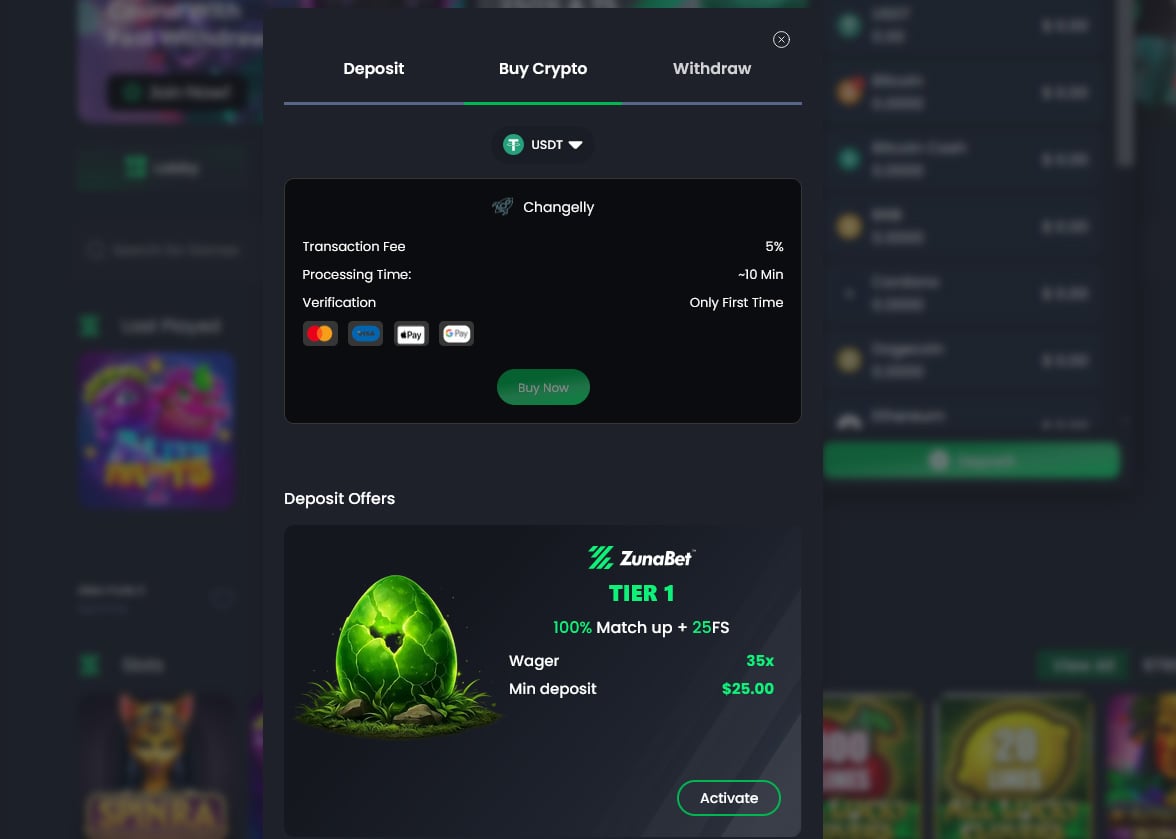

ZunaBet launched in 2026 under Strathvale Group Ltd with an Anjouan gaming license. The team behind it has more than 20 years of combined online gambling experience. The platform was built from scratch as a crypto-native operation — cryptocurrency is not a payment add-on but the foundation of the entire system.

The game library immediately addresses one of the most common complaints about Stake. ZunaBet offers over 11,000 games from 63 providers, including Pragmatic Play, Hacksaw Gaming, Yggdrasil, BGaming, and Evolution. That covers slots, RNG table games, and live dealer experiences. With 60+ studios contributing content, the range of game styles, themes, and mechanics is among the widest in the crypto casino space. Players moving from Stake to ZunaBet are unlikely to feel like they are downsizing.

The sportsbook is fully integrated. Coverage includes football, basketball, tennis, NHL, combat sports, virtual sports, and esports markets for CS2, Dota 2, League of Legends, and Valorant. One account and one balance handle everything, so switching between casino and sports is seamless.

ZunaBet supports more than 20 cryptocurrencies: BTC, ETH, USDT across multiple blockchains, SOL, DOGE, ADA, XRP, and others. No platform processing fees are applied. Withdrawals are built for speed. Apps are available for iOS, Android, Windows, and MacOS, with live chat running 24/7.

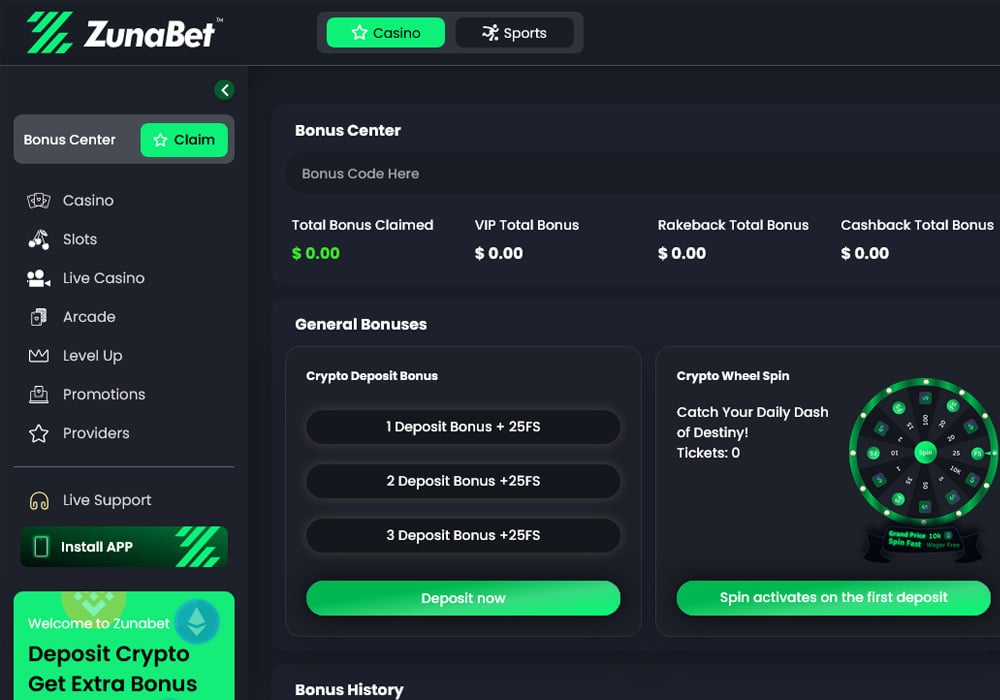

The Bonus Gap

This is the single biggest reason players search for Stake alternatives, and it is where ZunaBet makes its strongest first impression.

Stake offers nothing when you sign up. No matched deposit. No free spins. No promotional credit. Your first session is funded entirely by your own money with zero cushion.

ZunaBet opens with a welcome package worth up to $5,000 plus 75 free spins across three deposits. First deposit: 100% match up to $2,000 with 25 free spins. Second deposit: 50% match up to $1,500 with 25 spins. Third deposit: 100% match up to $1,500 with 25 spins. The three-deposit structure keeps bonus value flowing across a player’s first several sessions rather than concentrating it all on day one.

For a player evaluating whether to try a new platform, this alone answers the question. ZunaBet gives you significantly more to work with from the start, which means more games explored, more bets placed, and more time on the platform before your own funds carry the full weight.

Loyalty: Closed System vs Open Progression

The loyalty comparison is the second major driver of the search trend.

Stake’s VIP program operates behind closed doors. Invitation is based on wagering volume, but the thresholds are not published. Players have no visibility into where they stand or how close they are to qualifying. Those who make it in report strong benefits — rakeback, recurring bonuses, and personal account management. Those who do not make it in see nothing. For a large portion of Stake’s user base, the VIP program might as well not exist.

ZunaBet takes the opposite approach with a dragon evolution loyalty system featuring six published tiers. Squire starts at 1% rakeback. Warden gives 2%. Champion gives 4%. Divine gives 5%. Knight gives 10%. Ultimate reaches 20%. Each tier also unlocks free spins scaling up to 1,000, VIP club membership, and double wheel spins. A dragon mascot named Zuno gives the program personality and makes the progression feel gamified rather than transactional.

Every element of ZunaBet’s loyalty program is visible from day one. Players see every tier, every reward, and every requirement the moment they create an account. There is no ambiguity and no closed doors. For players frustrated by Stake’s opaque VIP system, this transparency is exactly what they are looking for. The 20% rakeback ceiling at the Ultimate tier offers a return rate that matches or exceeds what many Stake VIP members report receiving, but without requiring an invitation to access.

The Broader Crypto Casino Shift

The surge in alternative searches is not just about Stake specifically. It reflects a broader maturation of the crypto gambling market. When Stake launched in 2017, the options were limited and any decent crypto casino attracted players almost by default. In 2026, the landscape is crowded with platforms competing aggressively on bonuses, game variety, coin support, and loyalty rewards.

Players have become more sophisticated in how they evaluate platforms. They compare wagering requirements, check rakeback percentages, count supported cryptocurrencies, and read the fine print on loyalty programs. The era of sticking with one platform out of habit or lack of alternatives is fading.

ZunaBet benefits directly from this shift. Supporting over 20 cryptocurrencies with no processing fees, offering a game library that dwarfs most competitors, and running a loyalty program with published tiers and up to 20% rakeback positions it as the kind of platform that informed players actively seek out. It was built for a market where players shop around, and it was designed to win that comparison.

Both Stake and ZunaBet sit firmly in the crypto camp, which already separates them from traditional fiat operators like DraftKings, BetMGM, FanDuel, and Caesars. Those platforms process payments through banks and cards with slower withdrawals and higher fees. For players whose finances already run on crypto, neither traditional platform is a natural fit. The real choice for crypto gamblers in 2026 is between established crypto platforms like Stake and newer ones like ZunaBet that are pushing the category forward.

What the Search Trend Signals

Rising search interest in Stake alternatives is not a sign that Stake is declining. It is a sign that the market has evolved past what any single platform established years ago can satisfy without adapting. Players want welcome bonuses. They want transparent loyalty programs. They want massive game libraries and broad crypto support. They want platforms that earn their loyalty rather than assume it.

ZunaBet checks every one of those boxes. A $5,000 welcome bonus with free spins. Over 11,000 games from 63 providers. More than 20 supported cryptocurrencies with zero fees. A six-tier loyalty program reaching 20% rakeback with full visibility. A complete sportsbook with esports. It is a platform built specifically for the player who typed “Stake alternative” into a search engine and wanted to find something better.

Stake wrote the early playbook for crypto casinos. ZunaBet is writing the updated version — with more generosity, more transparency, and more reasons to choose it over what came before. The search trends suggest that a growing number of players are ready for that next chapter, and ZunaBet is the platform best positioned to deliver it.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

The digital asset space has shifted a lot in 2026. The era of speculative retail frenzies is being replaced by a sophisticated, capital-heavy infrastructure driven by global institutions.

We are witnessing a historic migration. Crypto innovation is moving from hype-cycle headlines into the mission-critical backends of the world’s largest asset managers, banks, and payment networks.

As the border between TradFi and crypto effectively vanishes, the market requires something more effective than a “popularity contest” to identify its true leaders. It requires a data-backed standard of excellence.

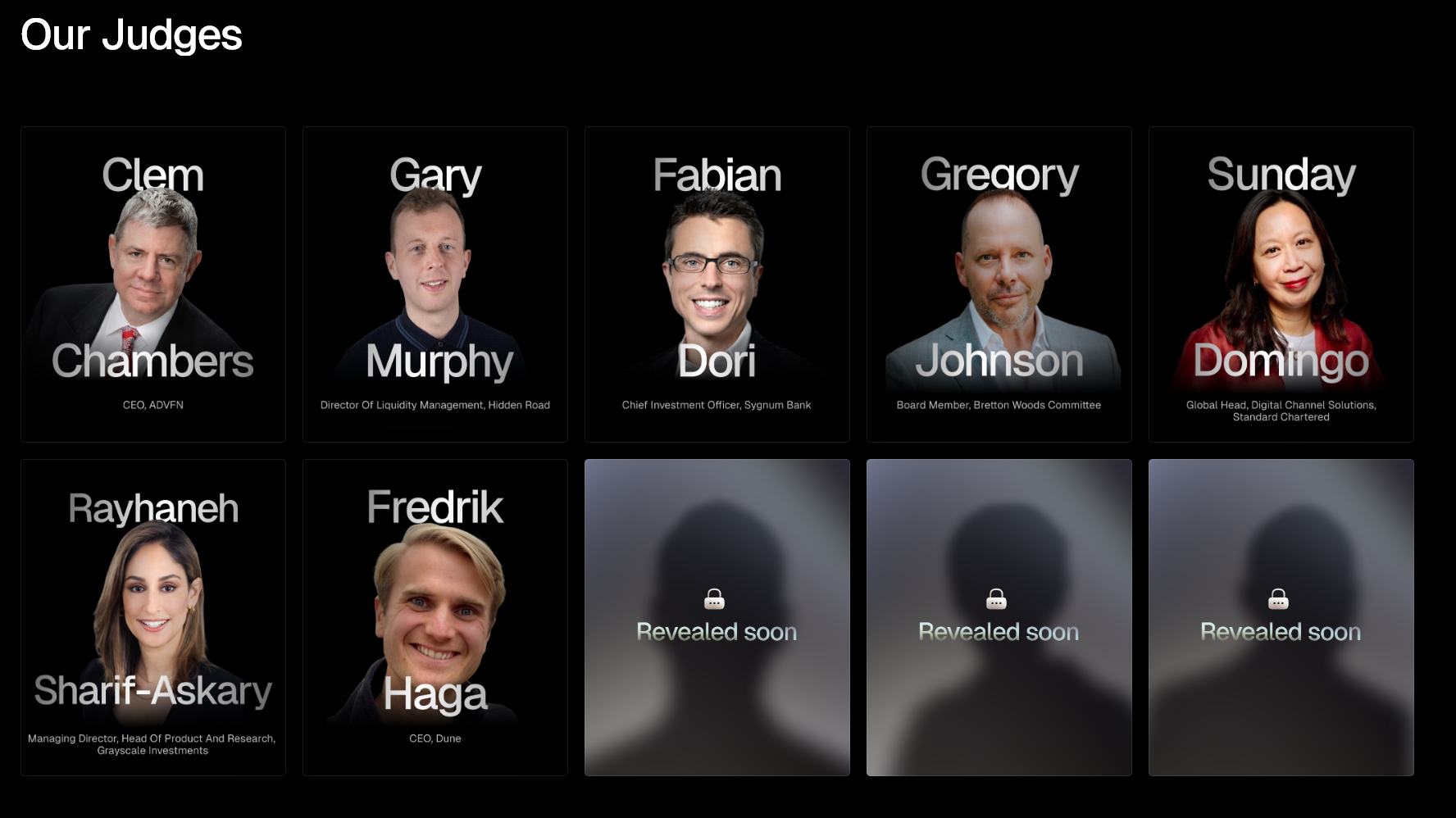

Enter the BeInCrypto Institutional 100 Awards.

Unlike traditional industry awards that often rely on subjective “vibes” or paid placements, BeInCrypto has unveiled a data-backed framework designed to measure excellence across the entire institutional value chain.

Whether the category is high-speed trading infrastructure, the tokenization of real-world assets, or large-scale enterprise rollouts, the 2026 evaluation process is anchored by one “gold standard” rule: Show us the receipts.

In crypto, we know that marketing often outpaces reality. So, how do you solve this? Every point a nominee earns must be backed by an auditable data source. If you can’t trace it to a specific metric, a regulatory filing, or a verified on-chain event, it doesn’t count.

BeInCrypto has built a “firewall” around its rankings. No entity can purchase, negotiate, or lobby for a spot on this list. Unlike traditional awards, where a small committee might pick winners based on personal connections or brand recognition, our process is entirely transparent and traceable.

To ensure total fairness, we use a two-stage evaluation designed to eliminate “anchoring bias,” that common human tendency to automatically favour “big names” over better-performing newcomers. Here is how the process works:

- Stage 1: The Data Filter

We start by looking at the numbers. This stage is purely mathematical, using hard metrics to filter dozens of candidates down to the top contenders. If the data doesn’t back up the hype, the nominee doesn’t move forward.

- Stage 2: The Expert Council

The top candidates are then reviewed by a panel of industry veterans. Their job isn’t to pick favorites, but to interpret the data profiles through the lens of real-world experience, strategic execution, and leadership.

- The Result

This creates a ranking where a disruptive, high-growth “underdog” can actually unseat a legacy giant, provided the data proves they are doing a better job.

A Methodology Built for Reality

Institutional finance is built on privacy and proprietary strategy. Many firms treat their specific user numbers and revenue splits as confidential, which often leaves researchers with a “data gap.”

BeInCrypto uses a specialized toolkit of Derived Estimation Methods to ensure these firms are still measured accurately.

Reverse-Engineering Impact

If a firm doesn’t disclose specific user counts, our analysts work backward. Using Revenue-Ratio Inference, we take reported segment earnings and apply industry benchmarks to find a realistic activity level.

The “Reciprocity” Test

We verify partnership claims by checking the other side of the deal. Through Partnership Reciprocity Testing, we search the communications of a nominee’s partners. A partnership that is actively acknowledged by both parties carries significantly more weight than a one-sided claim.

Regional Modeling

By combining a company’s total footprint with local crypto adoption data from sources like Chainalysis, we build an accurate map of their actual influence in specific global markets.

The Three-Track Architecture

You wouldn’t use a ruler to measure the temperature, and you shouldn’t use the same criteria to measure a Bitcoin ETF as you would a New York Law Firm. To keep things fair, the 2026 methodology splits all 25 award categories into three specialized “tracks” based on what kind of data is available.

Track A: The Data-First Track

- Best for: High-transparency products like ETFs, On-Chain Protocols, and Asset Managers.

- How it works: In this track, the numbers do 50% of the talking. Because we can see exactly how much money is moving on the blockchain or in a fund, the data carries equal weight with our experts.

- Example: When evaluating “Best Digital Asset Product,” we look at $AUM$ (Assets Under Management) and daily inflows. If a new Bitcoin ETF is growing at 300% month-over-month, the data automatically pushes it to the top of the pile.

Track B: The Hybrid Track

- Best for: Consumer-facing companies like Neobanks, Crypto Brokers, and Onramps.

- How it works: These companies often have “hidden” data, like how many monthly active users they actually have. This track rewards transparency. We give a 20% “bonus” weight to firms that voluntarily share their internal metrics with our researchers.

- Example: If two Digital Banks have similar public reputations, but Bank A provides verified data on their institutional client growth while Bank B stays silent, Bank A earns a higher “Transparency Score,” giving them the competitive edge.

Track C: The Expert-Led Track

- Best for: Complex areas like Governance, Regulatory Compliance, and Policy Leadership.

- How it works: You can’t measure “good leadership” with a spreadsheet alone. In this track, our Expert Council, veterans from traditional finance and legal sectors, provides 80% of the score. However, we still include a 20% “sanity check” based on measurable signals.

- Example: For “Best Compliance Program,” the Council looks at the quality of a firm’s legal framework. But we anchor that opinion with data, such as: How many licenses do they actually hold? or What is the ratio of compliance staff to total employees? This ensures even “expert opinions” are rooted in reality.

Negative Signals

Innovation shouldn’t come at the cost of integrity. Every nominee faces a mandatory Negative Signal Scan.

This isn’t just a Google search. Our team scours SEC and VARA enforcement databases, Immunefi bug bounty records, and the DefiLlama Hacks database.

An unresolved security breach or a major regulatory fine isn’t just a “red flag,” it’s often a disqualifier. By baking risk assessment into the core score, BeInCrypto ensures that the “Institutional 100” represents the most stable and reliable actors in the space.

Looking Ahead to June 2026

The BeInCrypto Institutional 100 is about setting a real-world benchmark for an industry that has finally found its footing.

By opening up our playbook and publishing this methodology in full, we’re doing more than just handing out awards; we’re inviting the entire market to hold us and the winners to a much higher standard.

When the winners are revealed this June, you’ll know exactly how they got there. In a market still crowded with noise, we’re placing our bets on the data.

The post The BeInCrypto Institutional 100: A Benchmark for the New Financial Stack appeared first on BeInCrypto.

Crypto World

Stanley Druckenmiller Doubles Down on Alphabet (GOOGL) and Amazon (AMZN) Stock Amid AI Cloud Boom

Quick Summary

- Stanley Druckenmiller continued accumulating Alphabet and Amazon shares for the second consecutive quarter

- His Alphabet holdings surged 277% while Amazon positions grew 69% during Q4

- The billionaire investor previously exited Nvidia and Palantir positions, rotating capital into these cloud giants

- Google Cloud delivered 48% year-over-year revenue growth while AWS reaccelerated to 24%

- Both companies currently trade at significant discounts compared to their historical cash flow valuations

Stanley Druckenmiller, who manages capital through Duquesne Family Office, expanded his holdings in Alphabet and Amazon during the final quarter of 2025. This marks consecutive quarters of accumulation for both technology giants.

According to his SEC 13F disclosure, Druckenmiller acquired 282,800 shares of Alphabet’s Class A stock alongside 300,870 Amazon shares. These purchases expanded his Alphabet stake by 277% and boosted his Amazon holdings by 69%.

The legendary investor earned his reputation delivering approximately 30% annualized returns between 1981 and 2010. Market participants and institutional money managers closely monitor his portfolio adjustments.

Druckenmiller previously maintained positions in Nvidia and Palantir but liquidated both holdings entirely. His capital has been redirected toward Alphabet and Amazon instead.

The strategic rationale behind both investments revolves around their dominant cloud computing platforms. Alphabet operates Google Cloud, which ranks as the third-largest cloud infrastructure provider globally. Amazon maintains AWS, the undisputed market leader.

Artificial Intelligence Fuels Cloud Platform Expansion

Google Cloud reported impressive 48% revenue expansion in the fourth quarter. AWS demonstrated renewed momentum with growth reaccelerating to 24% year-over-year.

Both cloud platforms are integrating generative artificial intelligence capabilities and advanced language models. These innovations are attracting fresh enterprise clients while encouraging existing customers to expand their spending.

Alphabet maintains approximately 90% dominance in worldwide internet search through Google. Amazon operates the leading e-commerce platform throughout the United States.

These investments aren’t pure-play artificial intelligence bets. Both corporations generate substantial, diversified revenue streams beyond their cloud computing segments.

Stock Valuations Present Historic Opportunities

Alphabet currently trades at 14.3 times its forecasted 2027 cash flow. Amazon appears even more attractively priced at just 9.7 times projected cash flow for the same period.

When measured against their five-year historical averages, Alphabet trades at a 20% discount while Amazon shows a substantial 48% discount. Both stocks represent historically attractive entry points based on cash flow metrics.

PwC research projects that artificial intelligence will contribute over $15 trillion to worldwide economic output by 2030. Druckenmiller’s recent purchases indicate his conviction that Alphabet and Amazon will capture significant portions of this value creation.

His fourth quarter filing revealed a 29% reduction in Taiwan Semiconductor Manufacturing holdings. This adjustment signals a strategic pivot away from semiconductor manufacturers toward companies deploying AI applications.

The 13F filing documents holdings as of December 31, 2025, and was submitted before the February 17, 2026 regulatory deadline.

Key Highlights

- Alphabet’s President of Global Affairs and Chief Legal Officer, John Kent Walker, divested 9,093 Class C shares on March 27, generating approximately $2.48 million

- Transaction prices ranged between $273.91 and $278.30 per share

- Needham maintained its Buy rating on March 27 with a $400 price objective

- Wells Fargo increased its price objective to $397 from $387, maintaining an Overweight stance

- The company finalized its $32 billion purchase of Wiz, a cloud security provider, on March 11

John Kent Walker, serving as Alphabet’s President of Global Affairs and Chief Legal Officer, executed a sale of 9,093 Class C shares on March 27, 2026, netting approximately $2.48 million. The sale occurred through several transactions, with share prices spanning from $273.91 to $278.30.

Additionally, on March 31, Walker completed a disposal and re-acquisition of 8,993 Class C shares through a transaction valued at $0 — a structure commonly linked to equity compensation plan activities.

The insider transaction hasn’t dampened investor enthusiasm, as the stock has posted an impressive 84% gain over the trailing twelve months.

Two prominent Wall Street analysts expressed optimistic views on GOOGL during the same timeframe.

Laura Martin from Needham reaffirmed her Buy recommendation on March 27, setting a $400 price objective. This target was initially elevated in February from $330, subsequent to Alphabet’s fourth-quarter earnings disclosure.

Wells Fargo similarly acted on March 27, elevating its price objective to $397 from the prior $387 while sustaining its Overweight designation.

Analyst Ken Gawrelski highlighted that GOOGL possesses “all the pieces necessary to be an AI winner,” citing its computational infrastructure, Google Cloud Platform, extensive distribution channels, and consumer data assets as critical competitive strengths.

Wiz Deal Reaches Completion

Alphabet successfully concluded its $32 billion acquisition of Wiz, the cloud and AI security solution provider, on March 11. Wiz will operate within Google Cloud while preserving its independent brand identity.

Wells Fargo anticipates the transaction will enhance Google Cloud’s platform revenue streams and operating profitability throughout fiscal years 2026 and 2027.

On the innovation front, Google has introduced enhancements to its Gemini AI assistant. Recent features enable users to transfer chat histories from competing AI applications — a strategic capability designed to attract users from alternatives like ChatGPT.

Gemini Enhancements and Developer Capabilities

Google unveiled the Gemini 3.1 Flash Live audio model, engineered for real-time conversational interactions with enhanced accuracy and reduced latency. The technology is currently accessible to developers and enterprise clients across various platforms.

Citizens has retained a Market Outperform rating on Alphabet, emphasizing expansion in AI-driven advertising solutions and cloud infrastructure.

Regarding legal developments, Evercore analysts highlighted a Delaware court decision that may affect insurance coverage disputes for companies including Alphabet. The decision is viewed as beneficial to insurance providers.

Based on InvestingPro analysis, the stock is presently trading marginally above its estimated Fair Value.

Brazil’s main stock exchange B3 will begin offering six new derivatives contracts on April 27 that allow investors to bet on the likelihood of future events, ranging from the price of bitcoin to movements in the dollar and Ibovespa index.

The instruments, called Event Contracts, operate on a framework similar to prediction markets like Kalshi and Polymarket. Prices range up to 100 reals ($19), with each contract’s price reflecting the market’s estimated probability of an outcome.

B3’s contracts are regulated by Brazil’s securities authority (CVM) and designed for professional investors, the exchange said.

The six contracts cover mini futures and spot prices for the Ibovespa index, the U.S. dollar, and bitcoin. They are structured with fixed payouts and known risks from the outset, like crypto price prediction markets on Kalshi and Polymarket.

Traders won’t take delivery of the underlying assets, and settlement is instead cash-based. For now, only investors with more than 10 million reals ($1.9 million) in assets or CVM certification can trade the new products.

B3’s vice president of Products and Clients, Luiz Masagão, said the launch is part of a broader push to modernize derivatives trading in Brazil.

The exchange already offers contracts tied to central bank decisions in several countries and has watched the growth of predictive platforms abroad closely, Masagão added.

The exchange late last year revealed it’s working on its own tokenization platform and stablecoin, both expected to be launched this year.

B3’s launch marks the first federally regulated prediction market in Brazil, though it enters an increasingly crowded field. Platforms like Prévias and Palpitada have been operating domestically in a regulatory gray area, while U.S.-based Kalshi recently partnered with XP International, Brazil’s largest brokerage, to offer event contracts tied to Brazilian economic outcomes.

The move also comes amid a global prediction market boom. Notional volume is now nearing $160 billion, according to a Dune dashboard, while unique users have crossed the 3 million mark.

Polymarket and Kalshi dominate the space globally, accounting for most of the notional volume. Intercontinental Exchange, the owner of the New York Stock Exchange, recently doubled down on Polymarket and bringing its total commitment to nearly $2 billion.

Still, the regulatory landscape remains unsettled on both sides of the equator. In Brazil, legal experts say it’s unclear whether oversight of prediction markets should ultimately fall to the CVM, the Central Bank, or the Ministry of Finance.

[The stream is slated to start at 10:30 a.m. ET. CNBC Television will start the stream when the event begins. Please refresh the page if you do not see a player above.]

Federal Reserve Chair Jerome Powell speaks Monday to the Harvard University Principles of Economics class.

This will be one of Powell’s final scheduled public appearances before his term ends in May. The discussion comes with markets anticipating the central bank will be on hold regarding interest rates through the end of the year.

In his most recent comments, Powell characterized the economy as growing at “a solid pace” and said he is not concerned with worries of stagflation, low growth with high inflation. However, he noted that policymakers are taking a cautious approach as multiple factors play out this year, including the Iran war, tariffs and a stagnant labor market.

Powell’s term ends officially on May 15, and there is only one more policy meeting between now and then. However, it’s possible he will stay in the position longer if the Senate does not confirm is designated successor, former Governor Kevin Warsh.

The nomination currently is being held up in the Senate Banking Committee as U.S. Attorney Jeanine Pirro continues an investigation into the renovations at the Fed’s headquarters. A judge already has quashed a subpoena Pirro’s office sent to Powell, though she is appealing that decision.

Read more:

Recession odds climb on Wall Street as economy shows cracks beneath the surface

Fed’s Goolsbee says he’s worried about inflation in ‘fraught but intense’ climate

Fed Governor Waller urges caution for now, says rate cuts possible later in the year

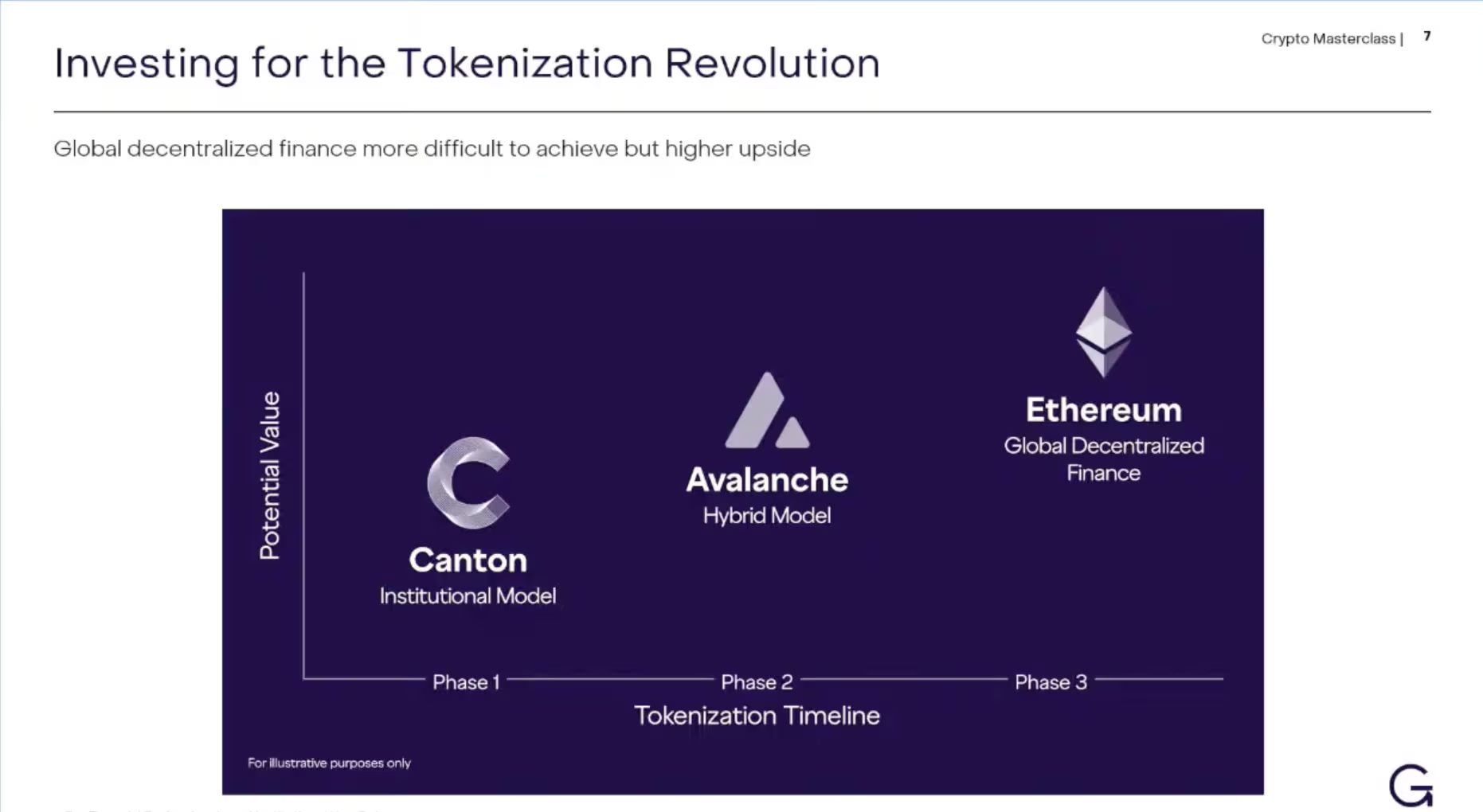

Tokenization has become one of crypto’s favorite buzzwords, but Grayscale head of research Zach Pandl said investors should think about it less as a single trade and more as a long roadmap with different winners at different stages.

Speaking at EthCC conference in Cannes, France, Pandl said that the trend is still in its infancy. Tokenized assets — the process of using blockchain rails to settle, transfer and record ownership of all kinds of financial assets such as bonds, funds and equities — is rapidly growing. However, currently at $27 billion, it still represents roughly 0.01%, a tiny fraction, of global capital markets. That’s projected to swell to near $19 trillion by 2033, according to BCG and Ripple.

Big banks and asset managers already understand the opportunity. “The two things that institutions are aware of are stablecoins and tokenization,” Pandl said. But they are still trying to figure out where to allocate capital to actually benefit from these innovations.

From here, Pandl expects tokenization to unfold in phases, with different types of networks and models capturing value at each stage.

The first winners, he said, may be projects that look more like traditional finance, not less.

“In the early stages of the tokenization process, you will see things that have success that look more similar to how the financial system works today,” he said.

That means institution-centric, permissioned systems that solve practical issues like privacy, identity and control.

Pandl pointed to the Canton Network (CC), backed by Wall Street giants like DRW, TradeWeb, Goldman Sachs and Nasdaq, as a potential winner in this early phase of tokenization.

He said it is “a perfectly reasonable investment” for investors who want nearer-term traction, even if Canton’s approach represents only “a slightly different, slightly upgraded version” of today’s financial system.

The second phase

The second phase of tokenization could be a hybrid model where we have both institution-owned blockchains and a global shared state, with those networks interconnected and speaking to each other. One example for that is Avalanche (AVAX), with hundreds of sovereign, corporate-owned chains (called subnets) live but connected to a primary, layer-1 network.

Ethereum’s ether (ETH), in his view, is the bigger but slower bet. Pandl said he believes the market will eventually move toward “global decentralized finance,” but added that “the tech is not fully ready” and that institutions are not ready either.

That makes ETH the more ambitious investment for those willing to wait for the longer-term shift away from financial intermediaries.

There are also picks-and-shovels plays. Pandl highlighted chain-agnostic service providers such as Chainlink as another way to get exposure, saying they may be “even more compelling” than some blockchains.

Read more: How tokenized assets could become a $400 billion market in 2026

Network News

GOOGLE SAYS BREAKING BITCOIN IS EASIER THAN PREVIOUSLY THOUGHT: Breaking the Bitcoin blockchain with quantum computers may not be as difficult as once thought, and Bitcoin’s Taproot technology, which enables more efficient, private transactions, may be partly to blame, Google’s Quantum AI team said in a blog post and newly published whitepaper. The team said the computing power required to break Bitcoin’s security may be far lower than previously assumed, raising fresh questions about how soon quantum threats could become a reality.In a new whitepaper, researchers found that cracking the cryptography used by Bitcoin and Ethereum could require fewer than 500,000 physical quantum bits, or qubits, well below the “millions” often cited in recent years. Google has previously pointed to 2029 as a potential milestone for useful quantum systems, saying migration needs to come before that, making the paper’s finding that attacks may require less computing power more significant. Quantum computers use qubits instead of traditional bits and can solve certain problems much faster than today’s machines. One of those problems is breaking the type of encryption that protects crypto wallets.Google said it designed two potential attack methods, each requiring roughly 1,200 to 1,450 high-quality qubits. That is a fraction of earlier estimates and suggests the gap between current technology and a viable attack may be smaller than investors think. The research also outlines how such an attack could work in practice. Rather than targeting old wallets, a quantum attacker could go after transactions in real time. When someone sends bitcoin, a piece of data called a public key is briefly revealed. A fast enough quantum computer could use that information to calculate the private key and redirect the funds. — Sam Reynolds Read more.

OPENAI RAISES RECORD $122 BILLION: Artificial intelligence giant OpenAI has closed $122 billion in committed capital at an $852 billion post-money valuation, a round that dwarfs anything raised in private markets and cements the company as the most valuable startup in history by a wide margin. The funding was anchored by Amazon, Nvidia, and SoftBank, with continued participation from Microsoft. SoftBank co-led alongside a16z, D.E. Shaw Ventures, MGX, TPG, and accounts advised by T. Rowe Price. The investor list reads like a who’s who of global capital — BlackRock, Blackstone, Fidelity, Sequoia, Temasek, Coatue, and ARK Invest all participated. For the first time, OpenAI opened participation to individual investors through bank channels, raising over $3 billion from that tranche alone. OpenAI said it is generating $2 billion in revenue per month, up from $1 billion per quarter at the end of 2024. ChatGPT has more than 900 million weekly active users and over 50 million subscribers. The company claims 6x the monthly web visits and mobile sessions of the next largest AI app, and 4x the total time spent of all other AI apps combined. — Shaurya Malwa Read more.

HOW BITCOIN, ETHEREUM, AND SOLANA ARE PREPARING FOR Q-DAY: As quantum computing edges closer to practical reality, the crypto industry is beginning to confront a question it has long deferred: what happens if the cryptography underpinning trillions of dollars in digital assets no longer holds? The answers, so far, are anything but uniform. Across many of the most well-known ecosystems like Bitcoin, Ethereum, and Solana, responses are diverging along familiar lines: what to do on social consensus and technical iteration, and community members are split between caution and acceleration. Quantum computing is a fundamentally different approach to computation that uses the principles of quantum mechanics rather than classical physics. Instead of traditional bits that are either 0 or 1, quantum computers use “qubits,” which can exist in multiple states at once, a property known as superposition, allowing them to process many possibilities simultaneously. Combined with another feature called entanglement, this enables quantum machines to solve certain complex problems far more efficiently than classical computers, particularly tasks like factoring large numbers that underpin modern encryption. How threatening is quantum computing? Consider this: Quantum computers can solve extremely complex problems within seconds, whereas ‘Supercomputers,’ the most powerful computing machines available today, would take thousands of years for the same problems, according to IBM. And that’s why the threats to cryptographic networks stemming from quantum computing are concerning. And even Google, developer of Willow, a quantum supercomputer, is setting a 2029 deadline to migrate its authentication services to post-quantum cryptography, citing progress in the technology. — Margaux Nijkerk Read more.

BASE TEAM RELEASES 2026 ROADMAP: Base, the layer-2 network from Coinbase (COIN), is doubling down on its push to build what it calls a “global onchain economy,” outlining a 2026 strategy centered on markets, payments and developers. Base is one of the most widely used layer-2 networks in the Ethereum ecosystem, having opened to public use in August 2023. It was initially built using Optimism’s OP Stack as part of the broader “Superchain” ecosystem, though the project has since signaled plans to differentiate its infrastructure as it scales. In February, the Coinbase team said the chain will increasingly rely on its own, in-house code. Layer-2 blockchains are built on top of Ethereum and aim to increase speed and lower costs by processing transactions themselves, while still relying on Ethereum for security. The model has become a key part of Ethereum’s scaling strategy, enabling cheaper and faster transactions without moving activity entirely off the network. More recently, however, some Ethereum leaders, including co-founder Vitalik Buterin, have signaled a shift in focus toward scaling the base layer itself, leaving open questions about how layer-2 networks will fit into Ethereum’s evolving roadmap. For 2026, Base said it will focus on three areas: expanding onchain markets, scaling stablecoin-based payments and growing its developer ecosystem — a push that comes as onchain trading venues and stablecoins see rising adoption among institutional players. — Margaux Nijkerk Read more.

In Other News

- Bitcoin’s reputation has historically been built on extreme boom-and-bust cycles, with steep drawdowns of up to 90% following all-time highs. This cycle, however, the decline has been closer to 50%, a shift that analysts said reflects the maturation of BTC as an asset class. “Bitcoin’s drawdowns compressing to about 50% is a sign of a maturing market structure,” AdLunam co-founder and market analyst Jason Fernandes told CoinDesk. “As liquidity deepens and institutional participation increases, volatility naturally compresses on both the upside and the downside,” he added, saying that “at that point, the narrative shifts from questioning its legitimacy to optimizing allocation.” Fernandes’ comments are in response to Fidelity Digital Assets analyst Zack Wainwright’s X post Tuesday, in which he noted growth is becoming “less impulsive,” with a reduced probability of extreme downside events as bitcoin matures. — Olivier Acuna Read more.

- In Jack Dorsey’s view of the world, the job most at risk from the AI revolution is the middle manager. Dorsey argues in a new essay, “From Hierarchy to Intelligence,” published with Roelof Botha, Sequoia Capital’s managing partner, an investor in Block, that his company’s decision to cut approximately 4,000 of its more than 10,000 employees was not a cost reduction but a permanent restructuring to replace middle managers with AI. Corporate hierarchy, the essay argues, has always existed to solve one problem: routing information through organizations too large for any single person to oversee. Managers aggregate context from below, act as messengers from above, and maintain alignment across teams. AI can now perform those functions continuously and at scale, the authors argue, making the messenger redundant. In place of management layers, Dorsey and Botha proposes two AI-driven “world models.” One aggregates internal data from code, decisions, workflows, and performance metrics to create a continuously updated picture of company operations, replacing the context that managers traditionally carried. The other maps customer and merchant behavior using transaction data from Cash App and Square. — Sam Reynolds Read more.

Regulatory and Policy

- Australia passed legislation creating its first comprehensive regulatory framework for digital assets that requires crypto exchanges and custody providers to obtain financial services licenses. The Corporations Amendment (Digital Assets Framework) Bill 2025 cleared both houses on April 1, bringing firms that hold digital assets on behalf of customers into the existing Australian Financial Services Licence regime. Australia’s bill creates two new regulated categories under the Corporations Act: digital asset platforms, which hold crypto on behalf of users, and tokenized custody platforms, which hold real-world assets and issue a corresponding digital tokens. Operators of both must obtain an Australian Financial Services License from ASIC, bringing them under the same core rules as brokers or fund managers, including requirements to safeguard client assets, provide standardized disclosures, avoid misleading conduct, and maintain dispute resolution and compensation systems. Instead of regulating crypto itself, the law targets the companies in the middle that control customer funds, aiming to reduce risks like commingling, insolvency, and misuse of assets that have caused losses in past crypto failures. — Sam Reynolds Read more.

- Hong Kong has missed its own March timeline for HKD stablecoin licensing, with the Hong Kong Monetary Authority (HKMA) yet to approve any issuers despite public signals that the rollout would begin last month. At Consensus Hong Kong in February, Financial Secretary Paul Chan Mo-po said licenses would begin to be issued in March as part of the city’s push to position itself as a regulated hub for stablecoins and tokenized finance. The lack of approvals so far pushes that timeline into April and raises questions about how quickly the framework will move from policy to implementation. “In giving our licenses, we ensure that licensees have novel use cases, a credible and sustainable business model and strong regulatory compliance capabilities,” he said at CoinDesk’s Hong Kong conference.— Sam Reynolds Read more.

Calendar

- Mar. 30-Apr. 2, 2026: EthCC, Cannes

- Apr.15-16, 2026: Paris Blockchain Week, Paris

- May 5-7, 2026: Consensus, Miami

- Sept. 29-Oct.1, 2026: Korea Blockchain Week, Seoul

- Oct. 7-8, 2026: Token2049, Singapore

- Nov. 3-6, 2026: Devcon, Mumbai

- Nov. 15-17, 2026: Solana Breakpoint, London

Top 3 Best Cars under $10,000 #shorts #credit #money #finance #credit #carbuyingtips #carbuying

West Yorkshire officer who sexually assaulted vulnerable single mum is jailed

Delivery firm Evri creates 150 jobs with new Yorkshire fulfilment centre

-

News Videos7 days ago

News Videos7 days agoParliament publishes latest register of MPs’ financial interests

-

Business6 days ago

Business6 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Tech6 days ago

Tech6 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

NewsBeat5 days ago

NewsBeat5 days agoThe Story hosts event on Durham’s historic registers

-

Sports5 days ago

Sports5 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment2 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment4 days ago

Entertainment4 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World1 day ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Sports1 day ago

Sports1 day agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech3 days ago

Tech3 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Entertainment7 days ago

Entertainment7 days agoHBO’s Harry Potter Series Will Definitely Fail For One Big Reason, And It’s Not J.K. Rowling Or Snape

-

Crypto World2 days ago

Crypto World2 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Fashion6 days ago

Fashion6 days agoEn Vogue in Brown Leather and Tailored Neutrals by Atelier Savoir, Styled by J Bolin

-

Politics2 days ago

Politics2 days agoShould Trump Be Scared Strait?

-

Tech1 day ago

Tech1 day agoEE TV is using AI to help you find something to watch

-

Tech1 day ago

Tech1 day agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Fashion6 days ago

Fashion6 days agoWhat Are Your Favorite T-Shirts for the Weekend?

-

Fashion5 days ago

Fashion5 days agoWeekly News Update, 3.27.26 – Corporette.com

-

Fashion4 days ago

Fashion4 days agoAmazon Sundays: Soft Spring Layers

-

Tech3 days ago

Tech3 days agoElon Musk’s last co-founder reportedly leaves xAI

You must be logged in to post a comment Login