Crypto World

How Real Is the Threat?

Concerns that quantum computing could one day break Bitcoin’s cryptography have resurfaced. Yet, a new report by CoinShares argues that the quantum risks remain distant, with only a fraction of Bitcoin’s supply potentially vulnerable.

The report frames quantum computing as a long-term engineering challenge. It argues that Bitcoin has ample time to adapt well before quantum machines reach a cryptographically relevant scale.

Sponsored

The Quantum Threat Assessment For Bitcoin

In the report titled “Quantum Vulnerability in Bitcoin: A Manageable Risk,” CoinShares’ Bitcoin Research Lead Christopher Bendiksen explained that Bitcoin relies on elliptic-curve cryptography to secure transactions.

In theory, a sufficiently powerful quantum computer could use Shor’s algorithm to derive private keys from public keys. This could enable unauthorized spending.

However, Bendiksen noted that such an attack would require quantum machines with millions of stable, error-corrected qubits. This is far beyond today’s capabilities.

“Breaking secp256k1 within a practical amount of time (<1 year) needs 10-100,000 times the current number of logical qubits; relevant quantum tech at least 10 years off. Long-term attacks can take place over years—could become feasible within a decade; short-term (mempool attacks) need <10-min computations—infeasible in anything but the very long term (decades),” the report read.

The report also examined the scope of Bitcoin’s real exposure. According to Bendiksen, only about 1.6 million BTC, roughly 8% of the total supply, resides in legacy Pay-to-Public-Key (P2PK) addresses where public keys are already exposed. However, the true practical risk is significantly smaller.

Of that amount, the report estimated that only around 10,200 BTC could plausibly be targeted in a way that would have an impact. This represents less than 0.1% of Bitcoin’s total supply.

Sponsored

“The remaining ~1.6 million all sit in 32,607 individual, ~50 btc UTXOs, that would take millennia to unlock even in the most outlandishly optimistic scenarios of technological progression in quantum computing,” Bendiksen stated.

The remaining vulnerable coins are dispersed across tens of thousands of addresses. This distribution would make large-scale exploitation slow and operationally impractical even for advanced quantum systems, according to the analysis.

This limited exposure exists because of modern address types. Pay-to-Public-Key-Hash (P2PKH) and Pay-to-Script-Hash (P2SH) do not reveal public keys until coins are spent, sharply reducing the attack surface.

While post-quantum cryptographic proposals exist, Bendiksen cautioned against premature or forced changes. He warned they could introduce new risks, weaken decentralization, or rely on cryptographic schemes that have not yet been sufficiently tested in adversarial environments.

Sponsored

“For the perceivable future, market implications appear limited,” Bendiksen added. “The greater concern is preserving Bitcoin’s immutability and neutrality, which could be jeopardised by premature protocol changes.”

Meanwhile, this outlook aligns with views previously expressed by other industry figures, including Casa co-founder Jameson Lopp and Cardano founder Charles Hoskinson. Both of whom have argued that quantum computing poses no near-term threat to Bitcoin’s cryptography.

Quantum Risk No Longer Ignored as Investors and Developers Prepare

That said, not all market participants share this view. Some institutional investors are increasingly factoring quantum computing risk into their Bitcoin exposure rather than dismissing it as a distant concern.

BeInCrypto reported that strategist Christopher Wood reduced a 10% Bitcoin allocation from Jefferies’ model portfolio, reallocating capital toward gold and mining equities. This move came amid concerns that future advances in quantum computing could threaten Bitcoin’s security.

Sponsored

At the same time, several blockchain projects are already taking proactive steps. Coinbase, Ethereum, and Optimism have publicly outlined efforts to prepare for a post-quantum future.

Charles Edwards of Capriole Investments has also suggested that Bitcoin’s price may need to decline further before the network attracts sufficient attention to the issue of quantum security. He framed market pressure as a potential catalyst for broader technical discussion.

“$50K not that far away now. I was serious when I said last year that price would need to go lower to incentivize proper attention to Bitcoin quantum security. This is the first promising progress we have seen to date,” he said.

Edwards added that substantial work still lies ahead, warning that Bitcoin’s quantum preparedness efforts would need to accelerate in 2026.

The BNY headquarters in New York, US, on Wednesday, July 10, 2024.

Jeenah Moon | Bloomberg | Getty Images

At America’s oldest bank, 134 new workers don’t sleep or take sick days. They don’t even have names.

They’re what BNY calls “digital employees.” They work side by side with humans. They have unique roles and are evaluated by how well they do them. Some of their jobs were done by people last year.

“The digital employee works 24/7, which is obviously very different to our human counterparts,” said Rachel Lewis, who oversees nine digital employees in addition to thousands of humans as head of payment operations for BNY. “It’s really focused on very specific repetitive tasks that allow our human employees to do much more human, intense, interesting-type roles.”

BNY employs 48,100 humans, down from about 53,400 in 2023, according to a recent earnings presentation. CFO Dermot McDonogh was asked on the firm’s fourth-quarter analyst call last month what the 134 digital employees mean for cost savings at the firm.

“Our head count has trended down a little bit, but that’s not really anything to do with AI yet,” McDonogh said. “We talk about, internally, AI is unlocking capacity. We don’t think about it in the narrow definition of efficiency. It’s all about growing with clients, increasing revenues and optimizing the potential for our employees.”

Across Wall Street, analysts and investors are starting to ask more questions about how the industry’s expenses on AI will translate into higher efficiencies and greater returns. BNY spent $3.8 billion on technology in 2025, or about 19% of its revenue. That’s the highest proportion among its large-bank peers, according to data collated by CNBC.

JPMorgan, Goldman Sachs, Bank of America, Wells Fargo, Citigroup, BNY

“There’s an AI arms race. The banks are part of that, said Wells Fargo analyst Mike Mayo. “But you don’t define success by who spends the most. You define success by who has the best results.”

“It’s a lot of ‘spraying and praying’ when it comes to spending on tech, generally,” he said.

However, BNY has been identified as one of the companies that could see the biggest benefits from AI. Goldman Sachs’ research team screened the Russell 1000 for potential productivity improvements, based on labor costs and wage exposure to AI automation. The firm ranked BNY toward the top of that list, saying the bank could see a potential 19% boost to earnings per share.

But in several conversations CNBC had with executives at BNY, they’ve been steadfast that the multitude of technology investments won’t come at the expense of human employees.

“I wouldn’t think about it that way,” said Michelle O’Reilly, BNY global head of talent. “I would think about it more as unlocking that productivity – enabling all employees to be productive.”

While the company is building more digital employees, it’s also upskilling the human ones. Shortly after ChatGPT was released in late 2022, BNY set up its AI Hub.

“That’s when we really doubled down and realized that this would be transformational for the bank,” said Leigh-Ann Russell, BNY’s chief information officer and global head of engineering. “Our biggest focus initially was enablement – getting some training rolled out to every one of our employees at the bank.”

BNY built a platform it calls Eliza, which pulls in a variety of open-source, commercially available models that are integrated with the firm’s internal data and compliance. Almost all of BNY’s workforce has completed a 10-hour training for Eliza, and thousands more have taken it a step further through a multi-day AI bootcamp that can help non-engineers find creative ways to automate parts of their jobs.

The name “Eliza” is a tribute to Elizabeth Schuyler Hamilton, the wife of the bank’s founder and America’s first Treasury Secretary, Alexander Hamilton.

“Democratization of this technology is one of our sweet spots on how we feel like we’ve been successful so far,” Russell said. “I have this juxtaposition of this original history of this amazing 241-year institution and being at the forefront of AI, and I think that’s just a lovely reminder of technology over the centuries.”

Shares of Strategy Incorporated (MSTR) suffered a severe collapse, falling by more than 75% from their July 2025 highs to last Thursday’s low. The main trigger was concern over the cryptocurrency market, as the company holds more than 700,000 coins on its balance sheet, with an average purchase price of around $76,000 per coin.

However, trading opened on Friday with a bullish gap, and MSTR surged by more than 20% during the session. Market sentiment shifted sharply due to two key factors:

→ Quarterly earnings release. Although earnings per share missed expectations, investors were reassured by statements from founder Michael Saylor and CEO Phong Le, who stressed that the decline in the price of the leading cryptocurrency does not threaten the company’s financial stability. Management confirmed that, despite unrealised losses, the core business generates sufficient cash flow to service debt, and the accumulation strategy remains unchanged.

→ Recovery in cryptocurrency prices. After forming a low on Thursday, the BTC/USD rate rebounded, finding support near the psychological $60,000 level.

Back in early December, we noted that:

→ signs of demand were emerging on the chart, giving bulls hope for a recovery;

→ much would depend on the direction of BTC/USD.

Since then, MSTR shares initially stabilised, finding support around $157, but the downtrend later resumed, driven by:

→ renewed weakness in the cryptocurrency market;

→ resistance at the median of the descending channel, as shown by the arrows. A breakout attempt in mid-January failed, allowing bears to regain control.

The last two candles on the chart form a bullish engulfing pattern, reinforced by exceptionally high trading volumes — a sign of “smart money” activity, which may view current prices as attractive.

Positive sentiment could persist this week, but the key question is whether it will be strong enough to break above the line dividing the lower half of the channel into two quarters. If successful, a crucial test for the bulls would be the area around the psychological $150 level, which stands out as a major resistance zone.

Buy and sell stocks of the world’s biggest publicly-listed companies with CFDs on FXOpen’s trading platform. Open your FXOpen account now or learn more about trading share CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

ETH is close to breaking below $2,000 again, XRP’s price is down by 3% daily.

Bitcoin’s price ascent to $72,000 on Sunday failed in its tracks, and the asset has retraced by over two grand since that unsuccessful attempt.

Most larger-cap altcoins are in the red today after charting some gains over the weekend. WLFI and XMR are among the few exceptions.

BTC Below $70K Again

The primary cryptocurrency nosedived on several occasions in the past few weeks. On January 31, for example, it dumped from $84,000 to just under $76,000 after it had already dropped from a local peak of $90,000.

The bulls tried to intervene at this point, but their best effort took BTC to $79,000 a few days later. However, that was short-lived as the bears remained the predominant force in the market. As the selling pressure intensified over the business week, it culminated on Thursday and Friday morning when bitcoin plunged to $60,000.

This became its lowest price tag since before the US presidential elections in November 2024. After losing $30,000 in just over a week, the cryptocurrency finally rebounded and surged to $72,000 on Friday and Saturday morning. It failed there and dropped to $68,000, but tried once again on Sunday. However, it was stopped at $72,000 once again.

It has declined by $2,500 since then and now sits below $70,000. Its market capitalization is down to $1.390 trillion on CG, while its dominance over the alts is just over 57%.

WLFI Defies Market Trend

As mentioned above, the altcoins are back in the red today. Ethereum is down by 3% to $2,030, XRP is down to $1.40 after a similar decline, while BNB has slipped to $623. SOL and DOGE have dropped by 4%, while CC has shed 5% of value.

WLFI is among the few exceptions, with an 8% surge that has pushed it to almost $0.11. SKY, LEO, and XMR are also slightly in the green, while JUP, ONDO, and ARB have lost the most value daily, of up to 8%.

The total crypto market cap has declined by around $70 billion in a day and is below $2.430 trillion on CG.

SECRET PARTNERSHIP BONUS for CryptoPotato readers: Use this link to register and unlock $1,500 in exclusive BingX Exchange rewards (limited time offer).

Disclaimer: Information found on CryptoPotato is those of writers quoted. It does not represent the opinions of CryptoPotato on whether to buy, sell, or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk. See Disclaimer for more information.

As shown by today’s XAU/USD chart, gold began the week on a bullish note: trading opened with a bullish gap above Friday’s high, lifting the price above the psychological $5,000 level.

The strengthening of gold has been driven by the following factors (according to media reports):

→ The US dollar, which is weakening ahead of key US economic data. The January employment report is due on Wednesday (it is expected to show signs of stabilisation in the labour market), followed by inflation data on Friday.

→ Political developments in Japan. The decisive victory of Prime Minister Sanae Takaichi has reinforced expectations of large-scale fiscal stimulus (“Sanaenomics”), which traditionally puts pressure on the yen and supports gold.

→ Demand from central banks. It has been reported that China’s central bank extended its gold purchases for the fifteenth consecutive month in January.

On 3 February, when analysing gold price fluctuations, we:

→ noted that the market was extremely oversold within the context of a long-term ascending channel;

→ suggested that a rebound from the zone of extreme oversold conditions could encounter a resistance area formed by the median of that channel and the classic Fibonacci levels (50% and 61.8%).

Indeed, on 4 February, after recovering into this area (with the formation of peak C), the market reversed lower and found support near the lower boundary of the aforementioned channel on Friday, 6 February.

Technical Analysis of the XAU/USD Chart

Price action (expanding amplitude) during the formation of low D points to aggressive demand, which may reflect the intentions of large capital.

At the same time, analysis of the market structure based on the A–B–C–D swing points suggests that, following the burst of extreme volatility at the turn of the month (highlighted by the peak in the ATR indicator), the market is searching for a new equilibrium.

It is therefore reasonable to assume that in the near term we may see a contraction in the amplitude of price fluctuations on the XAU/USD chart. It cannot be ruled out that supply and demand will find a temporary balance around the psychological $5k level.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

A real estate project under construction along the ancient Huai River in Huai’an City, Jiangsu Province, China on January 29, 2026.

Cfoto | Future Publishing | Getty Images

BEIJING — S&P Global Ratings has lowered its forecast for China property sales this year, barely two months into 2026.

The firm said Sunday that primary real estate sales will likely drop by 10% to 14% this year, worse than the 5% to 8% decline for 2026 sales predicted back in October.

“This is a downturn so entrenched that only the government has capacity to absorb the excess inventory,” the analysts said in a note. They added that the state could buy more unsold property to create affordable housing, but that so far these efforts have been piecemeal.

China’s property market, once accounting for more than a quarter of the economy, has seen its annual sales volume halve in just four years. Beijing’s crackdown on developers’ high reliance on debt for growth sparked the initial slump, while consumer demand for homes has yet to pick up.

Economists have long warned of overbuilding in China’s property market. But developers have only kept up construction despite the sales slump, leading to a sixth-straight year of completed, unsold new housing, according to the ratings agency.

“China’s glut of primary housing is keeping a property market recovery out of reach,” the S&P analysts said, noting the oversupply pressures prices to fall by another 2% to 4% this year, following a similar decline last year.

“Falling prices erode homebuyers’ confidence,” S&P’s report said. “It’s a vicious cycle with no easy escape.”

What’s particularly concerning, S&P said, is that the price decline in China’s biggest cities worsened in the fourth quarter of last year. “We previously viewed these markets as healthy, and as the likely starting place of any national property recovery,” the report said.

The cities of Beijing, Guangzhou and Shenzhen reported home price declines last year of at least 3%, the report said, noting Shanghai was the only major city to report an increase, up 5.7% in 2025 from 2024.

Getting worse

China’s property slump progressively worsened throughout 2025.

In May, S&P predicted a 3% decline in sales of new homes, only to revise that in October to an 8% drop. Sales ended up falling by 12.6% to 8.4 trillion yuan ($1.21 trillion) — less than half the annual sales of 18.2 trillion yuan seen in 2021.

That’s ramping up the pressure on China’s struggling real-estate developers.

If sales end up falling 10 percentage points below S&P’s base case for this year and next, four of the 10 Chinese developers that the company rates could see downward rating pressure, the analysts said.

That excludes China Vanke, once one of the country’s largest developers, which, late last year, asked to delay repayment on some of its debt.

Subscribe now

Chinese authorities have yet to release significant new support for real estate, preferring to double down on efforts to develop advanced technologies.

Last month, U.S.-based research firm Rhodium Group said that China’s push into high-tech industries isn’t large enough to offset the country’s property slump, leaving the economy more reliant on exports for growth and more exposed to trade tensions.

Top policymakers are set to release economic goals for the year at a parliamentary meeting next month.

A wallet linked to the Infini exploit has resurfaced after months of dormancy, spending $13.32 million to buy Ethereum during the recent market dip.

Summary

- A wallet linked to the Infini exploit purchased 6,316 ETH worth $13.3 million during the recent price dip before sending funds to Tornado Cash, on-chain data shows.

- The address had been inactive for more than 200 days, according to alerts from Lookonchain, PeckShield, and CertiK.

- Past transactions suggest the exploiter has repeatedly bought ETH near local lows and sold near cycle highs, highlighting precise market timing.

The funds were later routed through the crypto mixing service Tornado Cash, according to on-chain data and multiple blockchain security firms.

Blockchain analytics firm Lookonchain flagged the activity, showing that the exploiter purchased 6,316 ETH at an average price of $2,109 roughly eight hours before the transfers were detected.

Shortly after the purchase, the wallet consolidated its holdings and sent a total of 15,470 ETH, worth about $32.6 million, to Tornado Cash.

The transactions were also identified by PeckShield and CertiK, both of which confirmed that the address, labeled as the Infini exploiter, deposited the full Ethereum (ETH) balance into the privacy protocol. Thus, marking a resumption of laundering activity after more than 200 days of inactivity.

Pattern of buying lows, selling highs

On-chain records suggest the wallet has repeatedly demonstrated precise market timing. According to Lookonchain, the same entity:

- February 2025: Exploited Infini by stealing $49.5 million in USDC, later converting the funds into 17,696 ETH at $2,798.

- July 2025: Sent 5,000 ETH to Tornado Cash and sold 1,770 ETH for $5.88 million at $3,322.

- August 2025: Sold 1,771 ETH at $4,202, near local cycle highs.

- February 2026: Bought 6,316 ETH at $2,109, before transferring the full balance to Tornado Cash.

“He seems very good at buying low and selling high,” Lookonchain noted, pointing to the consistent timing of the exploiter’s trades across multiple market cycles.

Background on the Infini exploit

Infini suffered the exploit in February 2025 after attackers compromised administrative privileges, resulting in a total loss of approximately $49.5 million. The stolen funds were rapidly swapped across stablecoins and ETH before being dispersed through multiple wallets, complicating recovery efforts.

While Tornado Cash remains operational at the smart-contract level, its use has drawn heightened scrutiny from regulators and blockchain investigators due to its frequent role in laundering illicit funds.

As of press time, there has been no indication that the funds sent to Tornado Cash have been frozen or recovered. Investigators continue to monitor the wallet’s activity for further movement.

Crypto World

Bitcoin (BTC), major tokens drop as traders position for downside protection: Crypto Markets Today

Crypto markets opened the week under pressure, extending losses after a volatile weekend as bitcoin showed tentative signs of stabilizing below $70,000.

Even though the largest cryptocurrency dropped more than 2.8% in the last 24 hours, it remains well off its recent lows of around $60,000. Still, it has struggled to regain momentum after last week’s steep drop that reignited debate over whether the market has entered a deeper bear phase or is nearing a bottom.

Bitcoin bulls pointed to slowing downside moves as a sign of exhaustion, even as critics took victory laps. Nevertheless, attention is being paid to software stocks, some of which started to rebound as concerns of a deeper collapse ease.

The CoinDesk 5 Index (CD5) fell 3.4%, with all five of the largest cryptocurrencies declining. Ether dropped about 5%, underperforming bitcoin as traders cut risk across major tokens, but held above the psychological support at $2,000. The broader CoinDesk 20 (CD20) index is down 3.7%.

Derivatives Positioning

- BTC futures are seeing a clear bearish shift after open interest (OI) slid from $19 billion to $16 billion over the last week, marking a period of sustained deleveraging.

- Funding rates on Bybit (-2.24%) and Binance (-0.5%) have flipped neutral-to-negative, signaling that short sellers are now leading the narrative. With the three-month basis compressing to 3%, institutional demand has cooled, reflecting a broader derivatives landscape dominated by risk-off sentiment.

- Options data confirms this defensive shift, with one-week 25-delta skew for BTC rising to 20% and call dominance dropping to 48%.

- The implied volatility (IV) term structure is now in extreme backwardation, with front-end volatility at 85.03% dwarfing long-term expectations (~50%). That’s a massive premium for immediate protection against near-term price drops.

- Coinglass data shows $397 million in 24-hour liquidations, with a 45-55 split between longs and shorts. BTC ($234 million), ETH ($74 million) and SOL ($14 million) were the leaders in terms of notional liquidations.

- The Binance liquidation heatmap indicates $68,160 as a core liquidation level to monitor in case of a price drop.

Token Talk

- Crypto wallet Rainbow debuted its RNBW token last week, but the launch wasn’t smooth.

- The Ethereum-based project introduced the token on the layer 2 network Base, with the price tumbling to $0.025, a 75% drop from its $0.10 initial coin offering (ICO) just two months earlier. It has since risen to $0.031

- That drop wiped out expectations from speculators betting on a $100 million fully diluted valuation (FDV). On Polymarket, odds of that bet reached a near 80% high earlier in the year. The FDV is now hovering closer to $31 million.

- At the heart of the chaos were delays in token distribution to early buyers and participants in Rainbow’s onchain rewards program. Some users said they had not received their airdropped tokens hours after the launch.

- Rainbow’s cofounder Mike Demarais blamed backend infrastructure buckling under demand. U.S.-based investors won’t be able to fully access their tokens until December 2026, according to vesting terms.

- Rainbow raised $18 million in a 2022 Series A led by Reddit cofounder Alexis Ohanian’s firm, Seven Seven Six. The wallet is known for gamified features and a points system tied to the RNBW token.

The FDIC will pay $188,440 and revise its disclosure rules after a Coinbase FOIA lawsuit exposed “pause letters” telling banks to curb or halt crypto services.

Summary

- The FDIC settled Coinbase’s FOIA suit by agreeing to cover $188,440 in legal fees and update how it handles bank supervision documents tied to crypto.

- Courts found the FDIC improperly blanket‑withheld records, leading to the release of dozens of “pause” or cease‑and‑desist‑style letters targeting banks’ crypto activities.

- Coinbase CLO Paul Grewal says the case proves regulators told banks to steer clear of crypto, fueling claims of a quiet “debanking” push against the industry.

The Federal Deposit Insurance Corporation agreed to pay $188,440 in legal fees and revise its public disclosure policy to settle a Freedom of Information Act lawsuit filed by Coinbase, according to court documents.

FDIC and the settlement resolved

The settlement resolves a multi-year legal dispute over the FDIC’s refusal to disclose documents that allegedly directed banks to halt or restrict cryptocurrency services, according to Decrypt.

The case centered on correspondence the FDIC sent to banks, characterized as “cease and seek letters,” which requested financial institutions refrain from offering new cryptocurrency-related services or expanding existing digital asset operations.

Coinbase filed the FOIA request seeking disclosure of these documents after confirming their existence. The FDIC declined to release the materials, prompting the legal action.

The court ruled the FDIC’s response violated the Freedom of Information Act by withholding all documents collectively under a blanket claim that “such documents are not subject to disclosure” without conducting individual document reviews, according to the ruling.

The settlement resulted in the disclosure of dozens of cease and desist letters from the FDIC ordering banks to cease cryptocurrency-related activities, according to legal experts familiar with the case.

Paul Grewal, Chief Legal Officer at Coinbase, stated in a press release following the settlement that the litigation confirmed documents directing banks to avoid cryptocurrency operations existed.

The FDIC is an independent government agency that operates under federal authority to insure bank deposits and supervise financial institutions in the United States.

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

For over a decade, the idea of money moving on-chain has hovered between promise and pause. The technology was always ahead of behaviour. Infrastructure matured faster than trust. Capital, especially institutional capital, preferred to observe rather than participate.

Summary

- The shift is behavioral, not technical: Infrastructure was ready years ago — 2025 is when institutions started asking “how does this fit?” instead of “how fast can it go?”

- Serious capital has arrived quietly: Family offices and HNWIs are allocating to on-chain assets as long-term infrastructure, not speculative trades — and that kind of money sticks.

- Regulation + tokenization make 2026 inevitable: Clear rules, real-world asset tokenization, and remittances as a killer use case are turning on-chain money from theory into financial plumbing.

That gap has started narrowing. By the end of 2025, the conversation shifted subtly but meaningfully. On-chain activity stopped being framed as a speculative side-show and began appearing in serious discussions around portfolio construction, asset efficiency, and cross-border value movement. As we look at 2026, it is worth asking whether this is the year money meaningfully transitions on-chain; not as a trend, but as an operating layer of global finance.

What changed in 2025 was behaviour, not technology

The biggest shift in 2025 was not technological innovation. It was behavioural maturity. Bitcoin’s (BTC) evolution captures this well. Once viewed almost entirely through the lens of volatility, it is now increasingly discussed as a long-duration asset with specific portfolio characteristics. That change in framing matters far more than price cycles.

Markets mature when participants begin asking better questions. In 2025, the questions shifted from “How fast can this grow?” to “How does this fit?” Custody, governance, auditability, and regulatory alignment became central themes. That is usually the moment when an asset class moves from experimentation to early adoption.

Serious wealth has entered quietly

In light of the turbulent times we’re living in, one of the more understated developments has been the steady participation of high-net-worth individuals and family offices in alternative assets like VDAs. This has not been loud capital. It has been careful, structured, and incremental. Many are allocating a modest percentage of their portfolios to digital assets, not to chase upside but to hedge concentration risk and gain exposure to a parallel financial infrastructure that is largely uncorrelated to traditional assets.

This matters because such capital tends to be sticky. It enters slowly, but it rarely exits impulsively. Once digital assets are treated as an allocation decision rather than a tactical trade, the foundation for long-term participation is laid. In 2026, this segment is likely to deepen its engagement; not necessarily by increasing risk, but by increasing conviction.

Regulation is not the enemy of on-chain money

India’s regulatory tightening has often been interpreted as resistance. In reality, it signals something more important: acknowledgement. Markets are regulated when they become too large to ignore. From a long-term perspective, regulation is not a brake on institutional participation; it is a prerequisite.

Clear rules, even strict ones, allow capital to assess risk with precision. Ambiguity deters serious money far more than compliance does. As India sharpens its regulatory posture and global frameworks such as CARF gain traction, the cost of participating on-chain becomes more predictable. Predictability, not permissiveness, is what institutions look for.

The quiet maturation of assets

Another reason 2026 feels different is asset maturity. Digital assets are no longer limited to cryptocurrencies. The conversation has expanded to tokenised representations of real-world value: real estate, land, funds, and potentially other long-duration assets.

India saw several announcements in 2025 around real estate and land tokenisation. Elsewhere, the New York Stock Exchange has announced a parallel exchange that will trade in tokenized assets with blockchain-based settlements, making T+1, T+2, and market hours history. While large-scale execution across the globe may take time, these developments are significant catalysts. Tokenisation is not about disruption for its own sake. It is about improving liquidity, reducing friction, and increasing transparency in asset classes that have historically been opaque and inefficient.

The real impact will not come from mass adoption overnight, but from selective, compliant use cases where on-chain records offer operational advantages. That is where credibility is built.

Remittances may be the first true test case

If there is one area where on-chain money has a clear functional advantage, it is global remittances. Speed, cost efficiency, and transparency are not theoretical benefits here; they are measurable outcomes.

Traditional systems remain slow, expensive, and fragmented. On-chain rails offer a way to move value across borders with fewer intermediaries and greater traceability. As regulatory clarity improves, remittances could become one of the first mainstream use cases where on-chain money moves from “alternative” to “obvious.”

India’s unresolved stablecoin question

One critical issue that 2026 will force into sharper focus is India’s stance on stablecoins. The RBI has articulated its position clearly, favouring sovereign digital currency models. However, globally, stablecoins continue to play a growing role in on-chain liquidity and settlement. Apparently, India has also proposed linking BRICS’ digital currencies on the back of CBDCs. The real question is whether stablecoin rails will continue to remain global liquidity havens or will the network effects settle on sovereign rails?

India will eventually need to articulate a more detailed position, whether through restriction, regulation, or selective allowance. This decision will shape how seamlessly India integrates into global on-chain financial systems. Avoiding the question may no longer be viable as cross-border capital flows increasingly intersect with digital rails.

So, is 2026 the turning point?

2026 is unlikely to be remembered as the year money fully moved on-chain. But it may be remembered as the year key decisions were made. The year when on-chain money stopped being debated as a possibility and started being evaluated as infrastructure.

The shift will be gradual, uneven, and heavily regulated. That is how financial systems evolve. What feels different now is the convergence of behaviour, regulation, and asset maturity. When those three align, capital tends to follow.

Money rarely moves where excitement is highest. It moves where systems are stable, rules are clear, and long-term value is visible. 2026 may not deliver headlines, but it may quietly mark the beginning of money finding its place on-chain.

Kris Marszalek, the founder and CEO of crypto exchange Crypto.com, spent $70 million to buy ai.com, the highest publicly disclosed price paid for a website domain, the FT reported.

The acquisition signals the executive’s move into artificial intelligence, a sector that reached nearly $1.5 trillion in worldwide spending in 2025, according to Gartner. The momentum will intensify this year, with Bloomberg reporting that the four largest U.S. tech giants alone, Alphabet, Amazon, Meta and Microsoft, plan to invest a combined $650 billion in AI infrastructure this year.

The transaction, finalized in April 2025, was conducted entirely in cryptocurrency, the FT said in its report on Friday, citing Larry Fischer of GetYourDomain.com, who brokered the transaction. The price tag more than doubled the previous $30 million record held by Block.one’s 2019 purchase of Voice.com. Block.one is the owner of CoindDesk’s parent, Bullish (BLSH). Marszalek spent $12 million to acquire crypto.com in 2018.

Ai.com announced the debut of a consumer platform featuring autonomous AI agents. Unlike traditional chatbots, these agents are designed to operate on a user’s behalf — executing tasks such as trading stocks, managing calendars and automating workflows. Marszalek said the platform aims to be the “front door to AGI” through a decentralized network.

“We are at a fundamental shift in AI’s evolution as we rapidly move beyond basic chats to AI agents actually getting things done for humans,” said Marszalek. “Our vision is a decentralized network of billions of agents who self-improve and share these improvements with each other.”

The platform announced its debut with a Super Bowl LX commercial on Sunday, generating a surge in traffic that crashed the website for several hours. Writing on X on Monday, Marszalek cited “insane traffic levels” from the 30-second ad, noting that while the team had prepared for scale, the volume of interest was unprecedented.

Kim Kardashian’s Pamela Anderson makeover for date night with Lewis Hamilton

Tech, Media & Telecom Roundup: Market Talk

America’s oldest bank spends billions on tech

-

Video6 days ago

Video6 days agoWhen Money Enters #motivation #mindset #selfimprovement

-

Tech5 days ago

Tech5 days agoWikipedia volunteers spent years cataloging AI tells. Now there’s a plugin to avoid them.

-

Politics19 hours ago

Politics19 hours agoWhy Israel is blocking foreign journalists from entering

-

Sports2 days ago

Sports2 days agoJD Vance booed as Team USA enters Winter Olympics opening ceremony

-

Tech3 days ago

Tech3 days agoFirst multi-coronavirus vaccine enters human testing, built on UW Medicine technology

-

NewsBeat13 hours ago

NewsBeat13 hours agoWinter Olympics 2026: Team GB’s Mia Brookes through to snowboard big air final, and curling pair beat Italy

-

NewsBeat6 days ago

NewsBeat6 days agoUS-brokered Russia-Ukraine talks are resuming this week

-

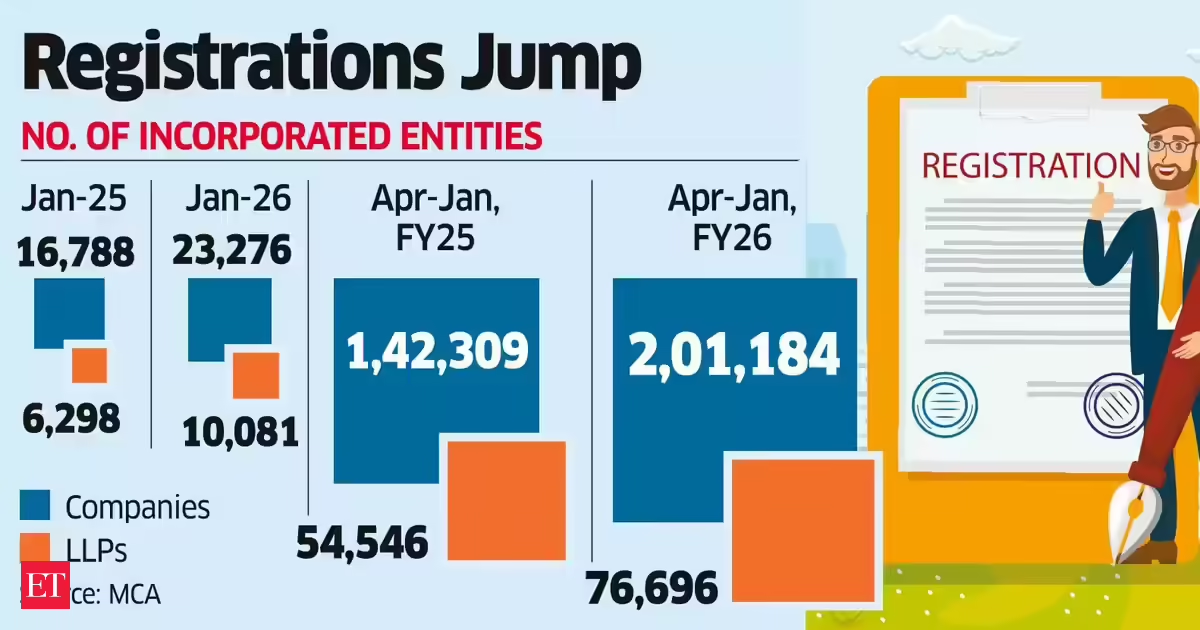

Business18 hours ago

Business18 hours agoLLP registrations cross 10,000 mark for first time in Jan

-

Sports8 hours ago

Sports8 hours agoBenjamin Karl strips clothes celebrating snowboard gold medal at Olympics

-

Politics21 hours ago

Politics21 hours agoThe Health Dangers Of Browning Your Food

-

Sports2 days ago

Former Viking Enters Hall of Fame

-

Sports3 days ago

New and Huge Defender Enter Vikings’ Mock Draft Orbit

-

Business1 day ago

Business1 day agoJulius Baer CEO calls for Swiss public register of rogue bankers to protect reputation

-

NewsBeat3 days ago

NewsBeat3 days agoSavannah Guthrie’s mother’s blood was found on porch of home, police confirm as search enters sixth day: Live

-

Business4 days ago

Business4 days agoQuiz enters administration for third time

-

NewsBeat3 hours ago

NewsBeat3 hours agoResidents say city high street with ‘boarded up’ shops ‘could be better’

-

NewsBeat7 days ago

NewsBeat7 days agoGAME to close all standalone stores in the UK after it enters administration

-

NewsBeat4 days ago

NewsBeat4 days agoStill time to enter Bolton News’ Best Hairdresser 2026 competition

-

NewsBeat2 days ago

NewsBeat2 days agoDriving instructor urges all learners to do 1 check before entering roundabout

-

Crypto World6 days ago

Crypto World6 days agoRussia’s Largest Bitcoin Miner BitRiver Enters Bankruptcy Proceedings: Report