CryptoCurrency

What Crypto Whales Are Buying as the Market Recovers?

The crypto market has grown by $238 billion over the last 48 hours, and the recovery signs are visible across the cryptocurrencies. Thus, it becomes crucial to check how the whales are acting at the moment to ascertain which crypto tokens investors should watch.

BeInCrypto has analysed three such altcoins that the crypto whales are buying at the moment.

Sponsored

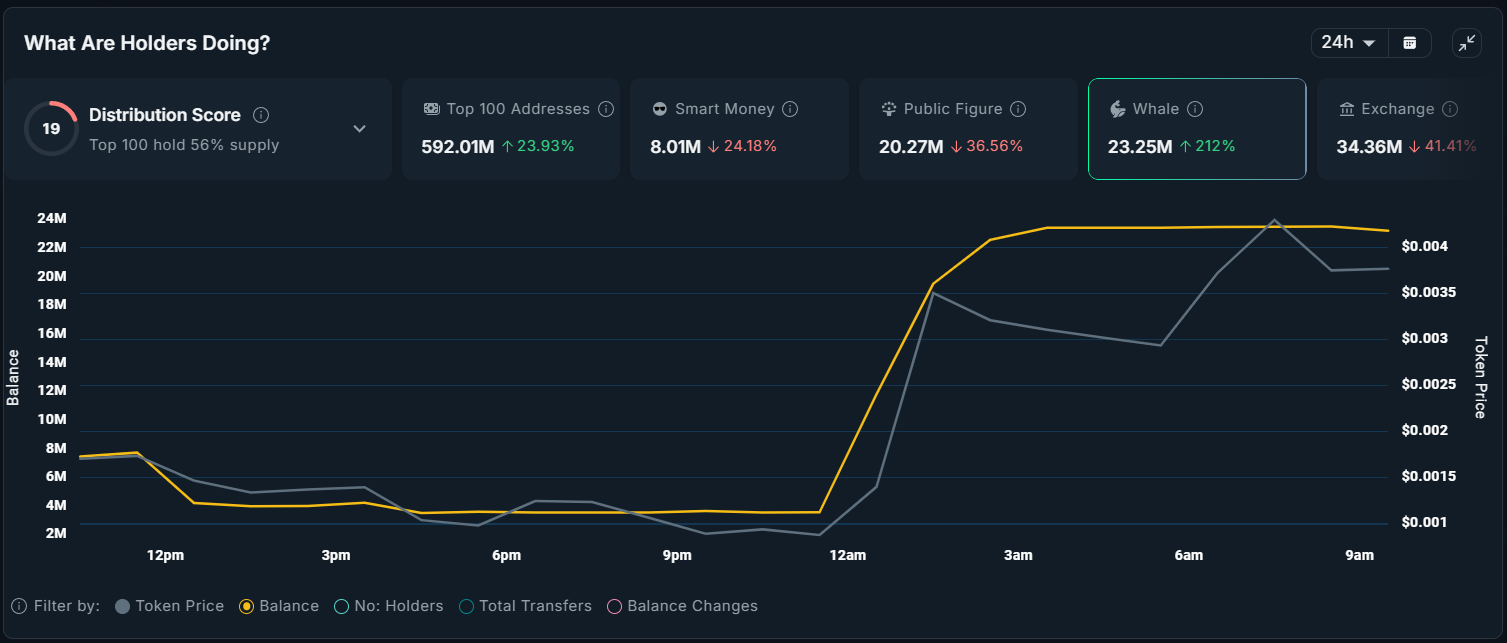

Franklin The Turtle (FRANKLIN)

TURTLE has drawn strong whale interest, with large wallets acquiring 15.77 million tokens in the past 24 hours. This accumulation highlights renewed confidence among major holders despite broader market weakness.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

The purchased supply, valued at more than $1.14 million, shows investors are buying the dip as TURTLE trades at $0.0723. The altcoin has been stuck in a month-long downtrend, but rising accumulation may signal an early shift in sentiment.

The Bollinger Bands are tightening, indicating an impending volatility spike. Combined with continued whale activity, this could help TURTLE break above $0.0760. This would end its downtrend and potentially climb toward $0.0942.

Sponsored

Zora (ZORA)

ZORA is seeing renewed whale accumulation, with large holders increasing their bags from 876,000 to 1.33 million tokens in just 24 hours. This surge reflects rising confidence as market conditions improve and buyers position for further upside.

Sponsored

The altcoin has climbed 18% in the past 48 hours and now trades at $0.0528, sitting above the $0.0506 support level. Sustained momentum could help ZORA push toward the $0.0568 resistance, as the MACD’s ongoing bullish crossover suggests and potentially move higher if demand strengthens.

If bullish sentiment cools, however, ZORA may lose its $0.0506 support and fall toward $0.0447. Such a decline would invalidate the optimistic outlook and signal a weaker short-term trend.

Sponsored

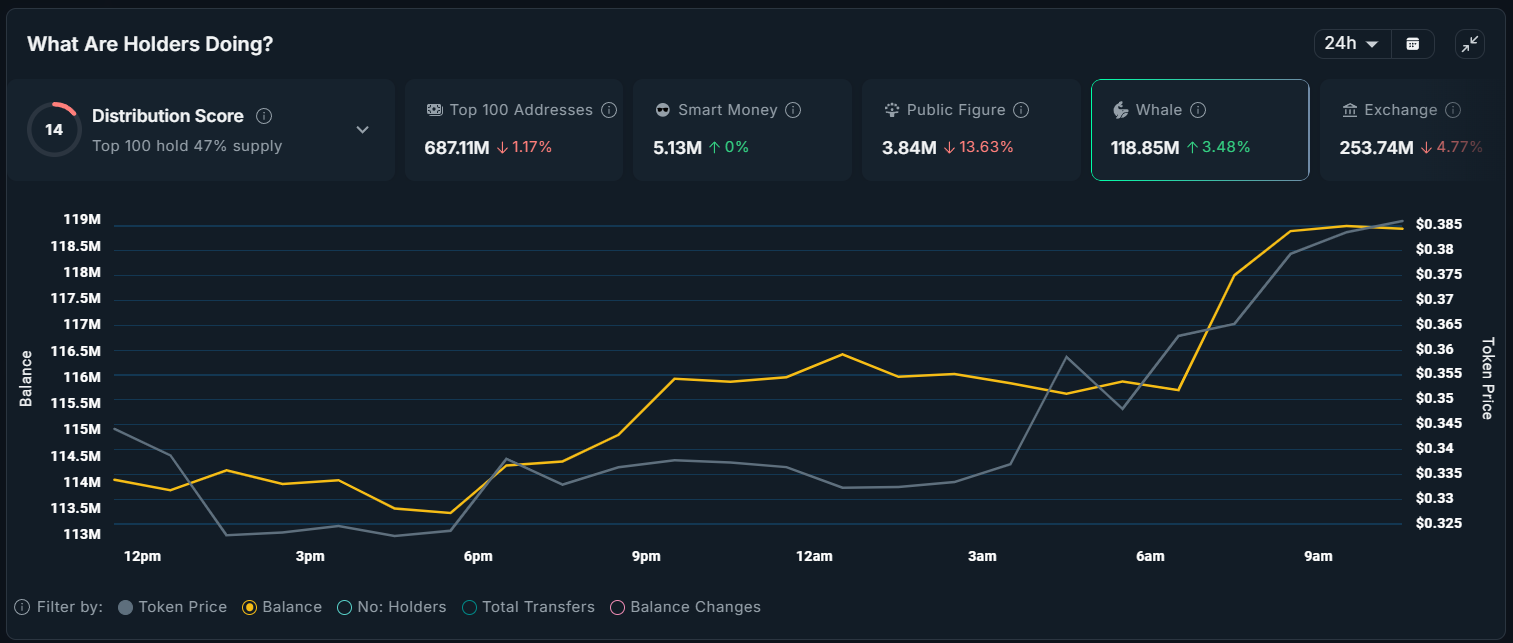

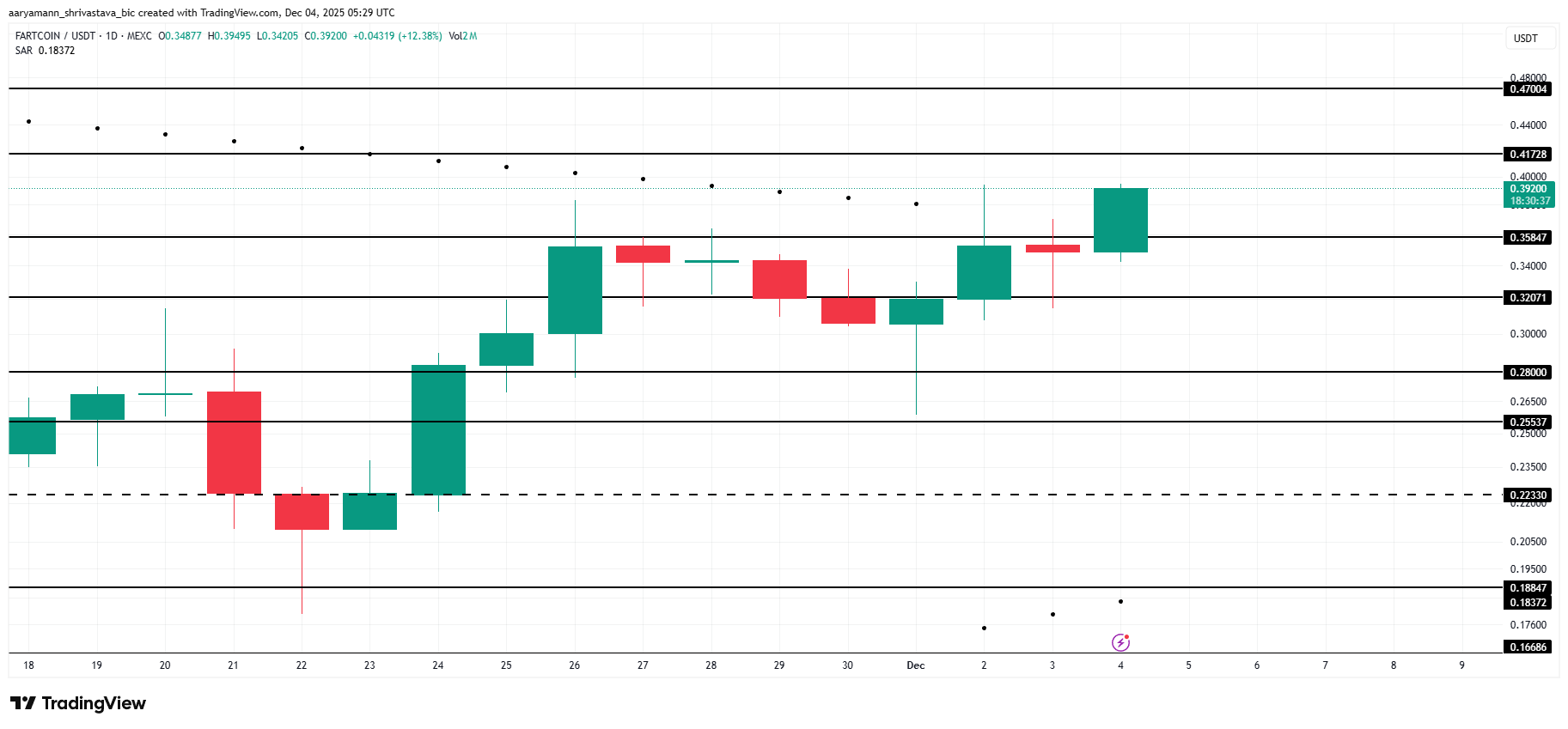

Fartcoin (FARTCOIN)

FARTCOIN whales increased their holdings by 3.42% in the last 24 hours, rising from 114 million to 118 million tokens. The additional 4 million FARTCOIN, valued at more than $1.56 million, signals renewed confidence from large holders during a volatile market phase.

This accumulation could extend FARTCOIN’s 12% rise today, with the altcoin trading at $0.392 under the $0.417 resistance. The Parabolic SAR indicates an active uptrend, suggesting the price may continue climbing toward $0.470 if momentum remains intact and buyers stay engaged.

If bullish strength weakens or investors move to take profits, FARTCOIN could slip below its $0.358 support level. A breakdown from there may push the price to $0.320, and losing this floor would invalidate the current bullish thesis.