Crypto World

Germany’s Bitcoin Sale Doesn’t Look So Foolish Anymore as BTC Tumbles

Key Takeaways

- In 2024, German authorities liquidated 49,858 BTC at roughly $57,900 each, generating approximately $2.89 billion

- Bitcoin currently hovers around $62,000—merely 7% higher than Germany’s average liquidation price

- A modest 6% price decline would sink Bitcoin below Germany’s exit level, completely flipping the narrative

- When Bitcoin hit its 2025 high, Germany’s move appeared catastrophic—the differential has collapsed from over 100% to less than 7%

- Consecutive outflows totaling $4.33 billion from spot Bitcoin ETFs over 13 days have intensified downward market momentum

When Germany liquidated almost 50,000 Bitcoin during summer 2024, the decision sparked widespread mockery. Today, as Bitcoin experiences significant downward pressure, that controversial move appears considerably more justified than it seemed mere months earlier.

The Origin of Germany’s Bitcoin Holdings

Saxony’s law enforcement agencies confiscated approximately 50,000 BTC in January 2024 during operations against Movie2K, an illegal streaming platform.

German regulatory frameworks mandate swift liquidation of confiscated assets. Authorities moved aggressively, selling the complete holdings across just 23 days—from June 19 through July 12, 2024.

Transactions were executed via prominent cryptocurrency platforms, including Kraken, Bitstamp, Coinbase, Cumberland, and Flow Traders.

The final tally showed an average execution price of $57,900 per Bitcoin, yielding total proceeds near $2.89 billion.

Initially, cryptocurrency advocates condemned the strategy. Bitcoin subsequently more than doubled in value, with retrospective analyses suggesting the holdings could have commanded over $6.6 billion if held for another year.

“I feel very sad for the German people. Among all the bad decisions being made for the country at the moment, this turns out to be the worst,” one Bitcoin investor said at the time.

Recent Price Action Changes the Calculus

Bitcoin recently dipped beneath $60,000 across Binance and Coinbase exchanges for the first time since 2024.

Blockchain analytics platform Arkham Intelligence has monitored this development closely. Their data indicates Bitcoin now trades merely 7% above Germany’s average sale price.

Another 6% contraction would position Bitcoin beneath Germany’s realized value—completely reversing the perception that authorities committed a monumental blunder.

When Bitcoin reached its 2025 zenith, Germany seemingly forfeited billions. That premium has evaporated from exceeding 100% to under 7%.

The downturn gained additional momentum as spot Bitcoin ETFs experienced $4.33 billion in redemptions across a 13-consecutive-day period—representing one of the most prolonged withdrawal streaks since these investment vehicles debuted.

Divergent Global Government Strategies

Germany wasn’t the only nation making consequential cryptocurrency decisions in 2024, though peer governments pursued contrasting strategies.

El Salvador and Bhutan actively accumulated Bitcoin throughout that period instead of divesting. Meanwhile, the United States under the Biden administration began reducing its own cryptocurrency reserves.

Combined actions by the US, Germany, and Ukraine—which completely eliminated its holdings—reduced government-controlled Bitcoin reserves by 12% during 2024.

China and the United Kingdom maintained static positions, neither acquiring nor disposing of any holdings.

These divergent national approaches have generated substantial discussion as Bitcoin retreats from previous peaks.

Ultimate judgment on Germany’s decision hinges entirely on Bitcoin’s future trajectory. Currently, however, the differential has contracted dramatically.

For the second time this year, the US Commodity Futures Trading Commission (CFTC) issued a warning to prediction markets operators to follow the rules when creating contract certifications that operators consider cover a broad swath of events contracts.

The CFTC, which claims to be the primary regulator of prediction markets, on Friday issued an advisory clarifying that, notwithstanding ongoing policy discussions and proposed rulemaking concerning prediction markets, the markets retain the ability to certify event contracts as compliant with the Commodity Exchange Act and CFTC regulations without prior commission approval, subject to the statutory framework governing self-certification.

The agency on Friday warned about the number of instances of events contracts that are “self-certified” by the platforms under the agency’s jurisdiction “without supplying the terms and conditions of each proposed permutation and a concise explanation and analysis with respect to the product’s terms and conditions, the underlying commodity, and the product’s compliance.”

“The guidance reiterates that broad, template-style certifications should not be submitted,” the CFTC said in its July 24 announcement. The regulator issued a similar warning about overly generalized submissions on March 12.

The advisory was issued just days ahead of the CFTC’s July 27 deadline to submit comments on its proposed rule amendments governing public interest determinations for certain event contracts involving the Commodity Exchange Act’s enumerated activities.

The CFTC has proposed amendments to clarify how it determines whether certain event contracts are contrary to the public interest, establishing a three-step analytical framework for evaluation.

This framework will help assess contracts based on their involvement in activities like terrorism, assassination, or gaming, ensuring that only appropriate contracts are listed for trading.

The proposed rule, if adopted, would fundamentally reshape aspects of the regulatory landscape for prediction markets, law firm Ropes & Gray said in June.

The crypto market has remained volatile throughout 2026 as investors continue debating when Bitcoin (BTC) will establish a durable bottom.

While broader market sentiment remains uncertain, some altcoins have shown resilience. Among them, TRON (TRX) is now flashing technical and on-chain signals that raise questions about its bottom.

TRX Price Action Steadies After a 16% Slide

According to 10x Research, TRX fell around 16% from its May high before finding support in late June. It now sits above both the 7-day and 30-day moving averages.

The firm reads both reclaims as bullish momentum signals. The altcoin has gained 2.2% over the past week and recovered 6% from its lows. Still, TRX remains 11% below its May peak.

The token trades near $0.33, about 23% under its record high of $0.4313.

Follow us on X to get the latest news as it happens

Stablecoin Activity and Treasury Buying Support the Bullish Case

Beyond the improving technical picture, growing institutional accumulation and strong network usage are reinforcing the positive outlook for TRX.

Nasdaq-listed Tron Inc. has continued expanding its treasury, purchasing another 150,742 TRX on Sunday at an average price of $0.3317. The acquisition lifted its holdings to more than 706.9 million TRX.

The Nasdaq-listed company purchases roughly $50,000 of TRX daily under a 360-day accumulation plan.

“We are executing a deliberate accumulation strategy that reflects our confidence in TRON’s scalability, real-world utility, and long-term value creation,” Rich Miller, CEO, Tron Inc., noted in a filing.

Network fundamentals also remain strong. According to a July CryptoQuant report, the TRON blockchain now hosts roughly $90 billion in circulating Tether (USDT). The network processes around $24 billion in daily transfer volume across approximately 2.2 million USDT transactions.

“This surging stablecoin demand reinforces the network’s position as a primary global settlement layer for retail payments,” 10x Research wrote.

Lower transaction costs have further strengthened network activity. Following last year’s gas fee reduction, average transaction fees have fallen 65% year over year to around $0.49.

While TRX remains below its May high, the combination of improving technical momentum, continued treasury accumulation, and strong stablecoin activity suggests downside pressure may be easing.

Whether the token has established a lasting bottom will likely depend on broader crypto market sentiment and Bitcoin’s next major move.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Tron TRX Ends 16% Slide With Two Bullish Signals appeared first on BeInCrypto.

Sberbank, Russia’s largest bank, says it will put new crypto trading infrastructure in place as the country moves its digital-asset activity into a regulated financial system. Interfax reported that Sberbank plans to create a “digital depository” by Dec. 1, alongside client-facing wallet operations for deposits, withdrawals and transfers.

The bank’s approach aims to shift the mechanics of ownership tracking and many transactions away from the public blockchain layer. Interfax said the depository will record clients’ rights to cryptocurrency and handle most transaction processing off the main blockchain, while Sberbank also operates active wallets to support customer orders for moving funds in and out.

Key takeaways

- Sberbank plans a crypto “digital depository” to record ownership rights and process most transfers outside the main blockchain.

- Interfax reports the infrastructure is targeted for completion by Dec. 1.

- Russia’s regulated crypto framework includes central bank oversight and sets liquidity thresholds tied to market size and volume.

- The timeline matters because the law defines categories of regulated market participants effective Sept. 1, 2026.

- Regulatory progress in Russia is unfolding alongside intensifying EU and UK sanctions involving major crypto service providers.

Sberbank’s proposed “digital depository” and how it would work

According to Interfax, the planned digital depository will serve as an institutional ledger for customer cryptocurrency ownership. Instead of relying solely on on-chain records to reflect balances and account entitlements, the system would maintain records of clients’ crypto rights and account for transactions outside the main blockchain.

Sberbank’s state-affiliated press service quoted Alexander Vedyakhin, first deputy chairman of Sberbank’s management board, describing the depository as a core element of the new infrastructure. He said it would track clients’ rights and support transfers by enabling transactions connected to “active wallets” used for deposit, withdrawal and client transfer instructions.

For market participants, the practical significance is that an institutional depository model can change operational workflows—particularly around reconciliation, custody accounting, and settlement processes—while potentially reducing reliance on public-chain activity for day-to-day internal movement and bookkeeping.

Russia’s broader shift toward a regulated crypto market

Russia has been working toward its first comprehensive crypto market framework. Earlier this month, lawmakers moved closer to that goal after completing final readings on a bill that would regulate digital-asset activity, according to earlier reporting linked in the source text.

The framework would grant the Bank of Russia broad oversight of a regulated market. The central bank’s role, as described in the source, would include deciding which crypto assets may be offered through licensed intermediaries and issuing implementing regulations.

Liquidity requirements also feature prominently. The Bank of Russia has set thresholds including an average market capitalization of more than 5 trillion rubles (about $64 billion) and an average daily volume above 1 trillion rubles (about $12.8 billion) over a two-year period. These benchmarks are intended to narrow eligibility and help define which assets qualify under the licensing regime.

Once the framework takes effect, the law establishes five categories of regulated market participants: crypto exchanges, brokers, asset managers, custodians and exchange service providers. The effective date for defining who can buy, sell, hold and exchange crypto assets is set for Sept. 1, 2026.

Why the Dec. 1 deadline could matter for regulated operations

The reported Dec. 1 target date for Sberbank’s digital depository suggests a pre-launch phase where banks and regulated intermediaries build internal rails before the broader participant categories become fully operative in 2026. In other words, infrastructure timelines are starting to line up ahead of the formal market framework’s effective date.

That sequence matters for two reasons. First, custody and settlement mechanics tend to be among the most complex components of bringing crypto into a mainstream regulated financial model. Second, the Bank of Russia’s licensing and asset-selection approach likely depends on firms being able to demonstrate controlled handling of ownership and transaction processing.

Even though the source does not provide additional technical specifics beyond off-chain recordkeeping and wallet-based customer operations, the intended function—maintaining ownership records and processing most transactions outside the main blockchain—implies that Sberbank is aiming to standardize how balances and client entitlements are managed within regulated channels.

Sanctions pressure continues as Russia formalizes its crypto rules

Russia’s regulatory momentum comes as external pressure on crypto businesses remains high. The source notes that the European Union has continued to tighten sanctions targeting Russia and has extended crypto-related measures affecting service providers.

In a Thursday European Council decision, the bloc amended previous measures “in view of Russia’s actions destabilizing the situation in Ukraine.” The decision added HTX—formerly Huobi Global—to a list of 18 entities described as “providing crypto-assets services or payment services established outside of the Union” that significantly “frustrate the purpose of the prohibitions” against Russia. A decision published on the EU’s legal database is linked in the source text.

The HTX sanctions were reported as arriving the same day EU officials announced a prohibition on Belarusian nationals and residents owning, controlling or managing crypto exchanges and digital asset service providers under MiCA compliance requirements, according to the linked earlier coverage in the source.

Meanwhile, the UK government also imposed similar sanctions on HTX in May, citing “reasonable grounds to suspect” the exchange supported Russia’s government through financial services involving funds facilitated by sanctioned entities, based on the linked prior report included in the source.

Taken together, the developments highlight a split dynamic: while Russia is building domestic, regulated infrastructure for crypto trading, European and UK authorities are simultaneously restricting certain offshore service providers through sanctions and regulatory compliance measures.

Readers should watch how Sberbank’s digital depository plan progresses beyond the announced deadline and whether other regulated market players follow with similar custody and settlement infrastructure ahead of the Sept. 1, 2026 effective date for participant categories. At the same time, sanctions risk remains a moving variable—especially for cross-border access to services—so the practical impact on liquidity and venue availability may depend on enforcement and compliance decisions in Europe and the UK.

Sberbank, Russia’s biggest bank, plans to build cryptocurrency trading infrastructure including a digital depository no later than Dec. 1 as the country brings crypto trading, custody and settlement into its regulated financial system.

That digital depository, Interfax reported, will record ownership of cryptocurrency and process most transactions outside of the main blockchain. Sberbank will operate active wallets for client-initiated deposits, withdrawals and transfers.

“One of the key elements of the new infrastructure will be a digital depository, which will maintain records of clients’ cryptocurrency rights and account for transactions outside the main blockchain,” said Alexander Vedyakhin, first deputy chairman of Sberbank’s management board, the state-affiliated press service said. “It will also facilitate transactions on active wallets to fulfill clients’ currency transfer orders.”

Russia’s lawmakers earlier this month moved the country closer to its first comprehensive crypto market framework after completing final readings on a bill that would regulate digital asset activity.

The bill would give the Bank of Russia broad oversight of the regulated market, including authority to determine which crypto assets may be offered through licensed intermediaries and to issue implementing regulations.The central bank has set liquidity thresholds, including an average market capitalization of more than 5 trillion rubles (~$64 billion) and an average daily volume of more than 1 trillion rubles (~$12.8 billion) over two years.

Once in place, it also establishes five categories of regulated market participants, including crypto exchanges, brokers, asset managers, custodians and exchange service providers, defining who can buy, sell, hold and exchange crypto assets as of the framework’s effective date of Sept. 1, 2026.

Recommended: Bitcoin advocacy group to join US State Department’s ‘digital freedom’ program

Moscow adopts crypto framework as EU tightens sanctions

Moscow is moving to put a working crypto infrastructure in place as the European Union turns up the heat on the country with a package of sanctions targeting Russia amid the country’s war on Ukraine. Last week, the bloc listed cryptocurrency exchange HTX, formerly Huobi Global, in its sanctions.

In a Thursday decision, the European Council amended its previous measures “in view of Russia’s actions destabilizing the situation in Ukraine” to include HTX in a list of 18 entities “providing crypto-assets services or payment services established outside of the Union that are significantly frustrating the purpose of the prohibitions” against Russia. The country continues to face sanctions globally over its war in Ukraine following a military invasion in 2022.

The sanctions against HTX came the same day EU officials announced they would prohibit Belarusian nationals and residents from owning, controlling or managing crypto exchanges and digital asset service providers in compliance with the region’s Markets in Crypto Assets (MiCA) framework.

The UK government imposed similar sanctions on HTX in May, saying there were “reasonable grounds to suspect” that the exchange supported Russia’s government by using financial services and funds facilitated by sanctioned entities.

Magazine: Will the US get CLARITY this week? Bitcoin’s new $80K target: Hodler’s Digest, July 19

The spot exchange-traded funds tracking Ripple’s cross-border token started the week strong, hitting a fresh all-time high in terms of total net inflows, but a familiar and slightly worrisome scenario repeated in the following days.

At the same time, the HYPE ETFs have broken their streak and were deep in the red for a second consecutive week.

XRP ETFs: The Good and the Worrisome

Data from SoSoValue shows that the spot XRP ETFs attracted $2.49 million on Monday and $5.66 million on Tuesday. That’s the good news. However, the other side of the coin was what happened during the remaining three business days of the week. And, it was something that has repeated and even accelerated in recent weeks.

The same data aggregator shows that there were no reportable net flows during those three days, with $0.00 pointing at each. Something similar was observed last week, when only one day was in the green, while the other four were at $0.00. If we look back, we can see that 10 out of the last 15 trading days have seen zero net flows.

Thus, even though the XRP ETFs ended two consecutive weeks in the green, a more in-depth look into the numbers shows a clear sign that investors’ interest has dwindled lately. Before these two weeks, the funds were on a massive nine-week streak in which they attracted over $150 million.

Nevertheless, the overall data shows that the cumulative total net inflow has risen to almost $1.5 billion, according to SoSoValue, which is an all-time high.

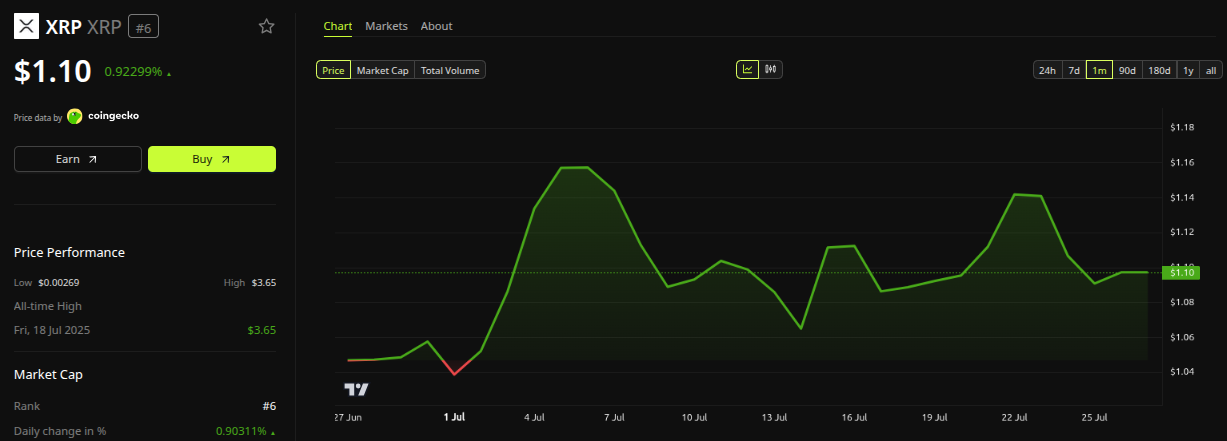

Meanwhile, the underlying asset pumped at the beginning of the week, perhaps due to the growing ETF net flows, went from under $1.09 to a multi-day peak of $1.16. However, it was halted there and has returned to below $1.10 as of press time.

HYPE ETFs Break Form

The spot HYPE ETFs quickly joined the XRP funds as a fan favorite, especially during one week in which they attracted over $110 million to set a record of their own. However, investors have turned their back on those funds in the past two weeks, as net outflows dominate.

During the past five-day trading period, they pulled out over $8.6 million, following another red one in which the net outflows stood at $7.26 million. Thus, the cumulative total net inflows have dropped from an all-time high of $308.60 million to $292.73 million as of Friday’s close.

The post Ripple (XRP) ETF Inflows Set Another Record, but One Problem Remains appeared first on CryptoPotato.

A post asking whether 20,000 XRP is enough for retirement savings drew heavy criticism on X, exposing how far optimistic price targets sit from current reality.

The debate cuts to a question every crypto holder eventually faces: how much is actually enough?

The $2 Million Math Behind the XRP Theory

A savings threshold is the portfolio size needed to generate a reliable income without depleting the principal. Jake Claver, chairman of DAG Family Office, applied that idea to XRP holdings this week.

His scenario rested on a single assumption. If XRP reached $100 per token, a 20,000 XRP position would be worth $2 million. From there, the math looked simple enough.

A conservative 5% annual return on that sum would produce roughly $100,000 in pre-tax income each year.

Follow us on X to get the latest news as it happens.

Claver framed the exercise as personal financial arithmetic rather than a forecast. He encouraged followers to run their own numbers, emphasizing patience over hype.

Current prices complicate the picture considerably. XRP trades near $1.10, according to BeInCrypto data, valuing 20,000 tokens at roughly $22,000.

Reaching $100 would require the token to climb nearly 90x from current levels. Its all-time high sits at $3.65, still far below that threshold.

The replies turned hostile quickly. Several users pointed to years of development and regulatory progress that failed to translate into sustained price appreciation.

One critic argued the token should already trade far higher if the technology delivered as promised. Another dismissed the $100 target outright, calling it unreachable.

Why Do Critics Say the Numbers Fall Short

Practical objections went beyond price skepticism. Even at $2 million, taxes, inflation, healthcare, and housing costs would erode purchasing power substantially over time.

For younger investors needing funds across 30 to 50 years, financial planners often cite $5 to $7 million as a more realistic independence target.

Concentration risk compounds the problem further. Holding a single volatile asset exposes savings to sudden drawdowns that diversified portfolios typically absorb more comfortably.

“Jake seriously, I am even getting tired of your crap. I know you are trying to build your business, but honestly your stuff isn’t coming true at all either. You get excited when you see some BS Japan or Oil going on. Price is still $1.10. You say XRP doesn’t need Clarity, yet, it’s still $1.10. If XRP was so great, it should be $20 by now. Why isn’t it? Crypto is crap, it’s all BS, just call it what it is already,” one user replied on X.

The underlying fundamentals offer some counterweight. XRP powers the XRP Ledger, built for fast, low-cost cross-border payments with transaction finality in three to five seconds.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

It functions as a bridge asset for currency swaps, and institutional interest has grown steadily. Spot ETFs arrived in late 2025, while real-world asset activity on the ledger continues to expand.

Competition remains fierce, however. Traditional payment systems and rival blockchains contest the same use cases, and much of the roughly 62.5 billion circulating supply sits idle.

Community responses split predictably. Some celebrate any XRP holding that clears a mortgage, while others argue that positions closer to 50,000 tokens make far more sense.

The disagreement highlights a broader point about crypto investing. Bag size alone guarantees nothing without diversification, disciplined withdrawal planning, and expectations grounded in probability rather than in hope.

The post Is 20,000 XRP Enough for Savings? The Dream Meets Brutal Reality on X appeared first on BeInCrypto.

Morgan Stanley kept Alibaba (BABA) stock as a “top pick” ahead of late-August earnings. Analyst Gary Yu made the call over two weeks after cutting his target to $180 from $190.

That target sits roughly 60% above where BABA shares closed on Friday at $112.14. Thus, Wall Street is telling clients the stock is worth far more than buyers are currently willing to pay.

Why the Target Cut Came First

Yu lowered his Alibaba target in early July. He still kept an overweight rating on the stock.

Other banks pivoted in the same direction. HSBC cut its target to $170 from $176 in July. The bank still maintained its buy rating.

Daiwa moved earlier, cutting to $175 from $200 on June 24. The firm pointed to weak sales during China’s 618 shopping festival.

Follow us on X to get the latest news as it happens

What Yu Wants Investors to Watch

Yu framed the reiteration by pointing to Alibaba’s cloud infrastructure, which he described as the largest in China.

“We expect Alibaba, having the largest cloud infrastructure in China, to win share in the current evolutionary AI cycle in China,” Yu said.

The bank also cited cash generation, dividends, and share buybacks as support. Morgan Stanley noted the online regulatory environment appears to be easing, with Alibaba positioned to benefit.

Yet, the bullish calls sit against a run of bad news. The European Commission fined AliExpress 550 million euros on July 20 for breaching the Digital Services Act (DSA).

AliExpress called the fine disproportionate and has until October 20 to file an action plan.

Meanwhile, Alibaba shares have gained about 18% over the past month. They remain well below their 52-week high of $192.67.

The late-August report will test whether the cloud growth Yu describes arrives fast enough to close a 60% gap.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Morgan Stanley Cuts Its Alibaba Stock Price Target appeared first on BeInCrypto.

Ripple’s token is showing signs of stabilization after the sharp decline from higher levels, but the recovery remains limited by a series of resistance zones that continue to attract sellers. While buyers have defended the recent lows, the market still needs a clear structural breakout before a stronger upside move can be considered.

Ripple Price Analysis: The Daily Chart

On the daily timeframe, XRP continues to trade inside a broader descending channel that has shaped the price action for months. The recent rebound from the $1.02 to $1.04 demand zone has helped the asset recover, but the move has not yet changed the larger bearish structure.

The main challenge for buyers remains the $1.17 to $1.2 supply zone, which sits near the upper boundary of the descending channel. A successful breakout above this region could open the path toward the next resistance area around $1.28. However, as long as XRP remains below this level, the current recovery may still represent a corrective move within the broader downtrend.

A rejection from the current resistance area could send the price back toward the $1.05 to $1.07 support region, while a deeper decline would bring the $1.02 to $1.04 buyers’ base back into focus.

XRP/USDT 4-Hour Chart

The 4-hour chart highlights the ongoing struggle between buyers attempting to build a base and sellers defending the overhead supply. XRP recently pushed toward the $1.16 to $1.18 resistance zone but failed to secure a breakout, keeping the short-term structure vulnerable.

The $1.16 – $1.18 supply range remains an important barrier, with price action still showing difficulty reclaiming the area above it. Until the asset breaks above this price region and confirms strength above it, upside attempts may continue to face selling pressure.

On the downside, the ascending wedge’s lower trendline remains the key support area. Holding above this zone would preserve the possibility of another recovery attempt, while a breakdown below it would weaken the current setup and increase the risk of further downside.

The post Ripple Price Analysis: XRP Could Be Heading for a Major Move Next Week appeared first on CryptoPotato.

After staging an impressive rebound from its local bottom, Ethereum is beginning to test increasingly important resistance levels. The coming sessions should provide more clarity on whether this recovery has enough momentum to continue.

Ethereum Price Analysis: The Daily Chart

The daily chart shows ETH holding above the previously broken descending trendline, confirming that the medium-term structure has improved compared to the aggressive selloff seen in June. Following the breakout, the market has successfully established a sequence of higher highs and higher lows while consolidating above the $1.76K to $1.82K support region.

However, the recovery is now approaching a major technical barrier. The $1.88K to $1.91K supply zone is acting as the first resistance, while the declining 100-day moving average sits just overhead near the $1.95K area. This creates a confluence of resistance that could cap the current rally before ETH attempts to challenge the broader long-term supply zone between roughly $2K and $2.15K.

As long as the price remains above the $1.76K to $1.82K support, buyers maintain the short-term advantage. Losing that area, however, would expose the next support around $1.55K to $1.64K and weaken the current bullish structure.

ETH/USDT 4-Hour Chart

On the 4-hour timeframe, Ethereum has slipped slightly below the ascending trendline that had guided the recovery throughout July. While the break is not yet decisive, it signals that bullish momentum is beginning to weaken as the price trades inside the $1.88K to $1.91K supply zone. The current structure suggests that buyers are losing some control after failing to extend the recent rally.

If ETH remains below the broken trendline, the move could evolve into a deeper retracement toward the notable demand zone around $1.76K to $1.79K, where buyers would be expected to step in. Conversely, reclaiming the trendline and securing a breakout above the $1.88K to $1.91K resistance would invalidate the short-term weakness and increase the probability of another push toward the $1.95K to $2K region.

Sentiment Analysis

The one-month Binance ETH liquidation heatmap shows a substantial concentration of liquidity around the $1.5K level. Although Ethereum is currently trading well above that region, this cluster remains an important magnet from a derivatives perspective.

If the current rally loses momentum and sellers regain control, a deeper correction toward the $1.5K liquidity pocket could attract price as leveraged long positions are unwound.

Such a move would likely coincide with a break below the key technical supports visible on the chart. Until then, the prevailing structure remains constructive, but the presence of this large liquidity cluster highlights that downside risk has not completely disappeared despite the recent recovery.

The post Ethereum Price Analysis: ETH Hits a Decision Point as Major Resistance Comes Into Play appeared first on CryptoPotato.

Dormant Bitcoin activity fell to its lowest level since Q3 2022, suggesting long-term holders have slowed distribution after heavy profit-taking.

Former NFL Passer Gives Embattled Vikings QB Some Film Room Praise

‘No matter how carefully you plan, a new challenge can always appear’

Setting Financial Boundary with Her Family: The Exact Number, and How to Say No | Day 14 of 100

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World5 days ago

Crypto World5 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

Tech6 days ago

Tech6 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech6 days ago

Tech6 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

NewsBeat6 days ago

NewsBeat6 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Business5 days ago

Business5 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment5 days ago

Entertainment5 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Tech6 days ago

Tech6 days agoWatch Flock Safety CEO Garrett Langley discuss the future of surveillance at TechCrunch Disrupt 2026

-

Crypto World4 days ago

Crypto World4 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

NewsBeat6 days ago

NewsBeat6 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Crypto World6 days ago

Crypto World6 days agoCircle’s President Sold Over 360,000 Shares, The Filings Explain Why

-

Tech7 days ago

Tech7 days agoSubway Sandwich Computers Get a Second Life as Gaming Machines

-

News Videos3 days ago

News Videos3 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Sports3 days ago

Sports3 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Tech7 days ago

Tech7 days agoHow To Use Claude’s Reflect Dashboard And Learn When It’s Time To Touch Grass

-

Fashion3 days ago

Fashion3 days ago16 Dresses for the High Summer Event

-

Entertainment7 days ago

Entertainment7 days agoStephen Colbert Returns to Social Media After Late Show End

-

Tech6 days ago

Tech6 days agoThe 35 Best Board Games for Family Game Night

-

Crypto World6 days ago

Crypto World6 days agoAndrew Cuomo joins OKX board as crypto exchange expands in U.S.

-

Politics5 hours ago

Politics5 hours agoSpain sweeps the board at 2026 World Cup with individual awards

You must be logged in to post a comment Login