Crypto World

MercadoLibre (MELI) Stock: Why Major Investors Keep Accumulating Despite Earnings Miss

TLDR

- Capital Research Global Investors boosted its MELI holdings by 22.5% during Q4, purchasing an additional 408,939 shares to total 2,225,031 shares worth approximately $4.48 billion.

- Hedge funds and institutional investors now hold 87.62% of MercadoLibre’s outstanding shares.

- First-quarter revenue surged 49% compared to the prior year, reaching $8.85 billion and exceeding projections, while earnings per share of $8.23 fell short of the $8.75 analyst forecast.

- Board member Alejandro Nicolas Aguzin purchased 600 shares at $1,655.93 apiece during May, expanding his personal stake by 12.62%.

- The analyst community maintains a Moderate Buy rating with a mean price objective of $2,255.33, despite multiple firms reducing their targets post-earnings.

Shares of MercadoLibre (MELI) began Friday’s session at $1,607.80, declining 1.7% and trading substantially beneath the 52-week peak of $2,645.22. The stock currently sits below both its 50-day moving average of $1,720.81 and its 200-day moving average of $1,887.84.

Capital Research Global Investors emerged as the most significant institutional buyer. During the fourth quarter, the investment firm expanded its MELI stake by 22.5%, acquiring 408,939 shares to reach a total position of 2,225,031 shares valued at approximately $4.48 billion. This position now ranks as the firm’s 24th largest holding, accounting for 0.8% of its overall portfolio.

Several additional institutional investors expanded their positions throughout the same period. Hardy Reed, Rothschild Investment, Interchange Capital Partners, Cornerstone Select Advisors, and Mitchell Capital Management each made incremental additions. Collectively, institutional investors and hedge funds control 87.62% of outstanding shares.

Regarding insider activity, Board Director Alejandro Nicolas Aguzin acquired 600 shares on May 22nd at a mean price of $1,655.93, totaling approximately $994,000 in purchases. This transaction increased his direct ownership to 5,355 shares, currently valued at over $8.8 million.

Q1 Earnings: Revenue Beats, EPS Misses

MercadoLibre unveiled its first-quarter financial results on May 7th. The company delivered revenue of $8.85 billion, representing a 49% increase year over year and surpassing the analyst estimate of $8.29 billion. This marked an impressive top-line performance.

Earnings per share, conversely, disappointed investors. The company reported $8.23, falling short of the consensus forecast of $8.75 by $0.52. The prior year’s comparable quarter generated EPS of $9.74 — marking a year-over-year decrease that drew market scrutiny.

The company maintains a return on equity of 29.58% with a net profit margin of 6.04%. Wall Street analysts project full-year earnings per share of $40.97. The stock currently trades at a price-to-earnings ratio of 42.43 and a PEG ratio of 0.99.

Analyst Price Targets Trimmed

The earnings shortfall triggered a series of price target reductions, although most analysts maintained favorable ratings.

JPMorgan reduced its price objective from $2,100 to $1,900 while maintaining a neutral stance. UBS decreased its target from $2,050 to $1,750, also neutral. Morgan Stanley lowered its target from $2,600 to $2,450 but retained an overweight rating. Goldman Sachs established a $2,100 price target. Daiwa downgraded from buy to hold with an $1,800 target.

Among 18 analysts tracking the stock, one assigns a Strong Buy rating, eleven recommend Buy, five suggest Hold, and one maintains a Sell rating. The consensus mean price target stands at $2,255.33 — approximately 40% above MELI’s current trading level.

MercadoLibre carries a market capitalization of $81.52 billion, maintains a current ratio of 1.16, and reports a debt-to-equity ratio of 0.63. The stock’s one-year low reached $1,495.00.

Clarity may get a vote, but don’t get your hopes up yet

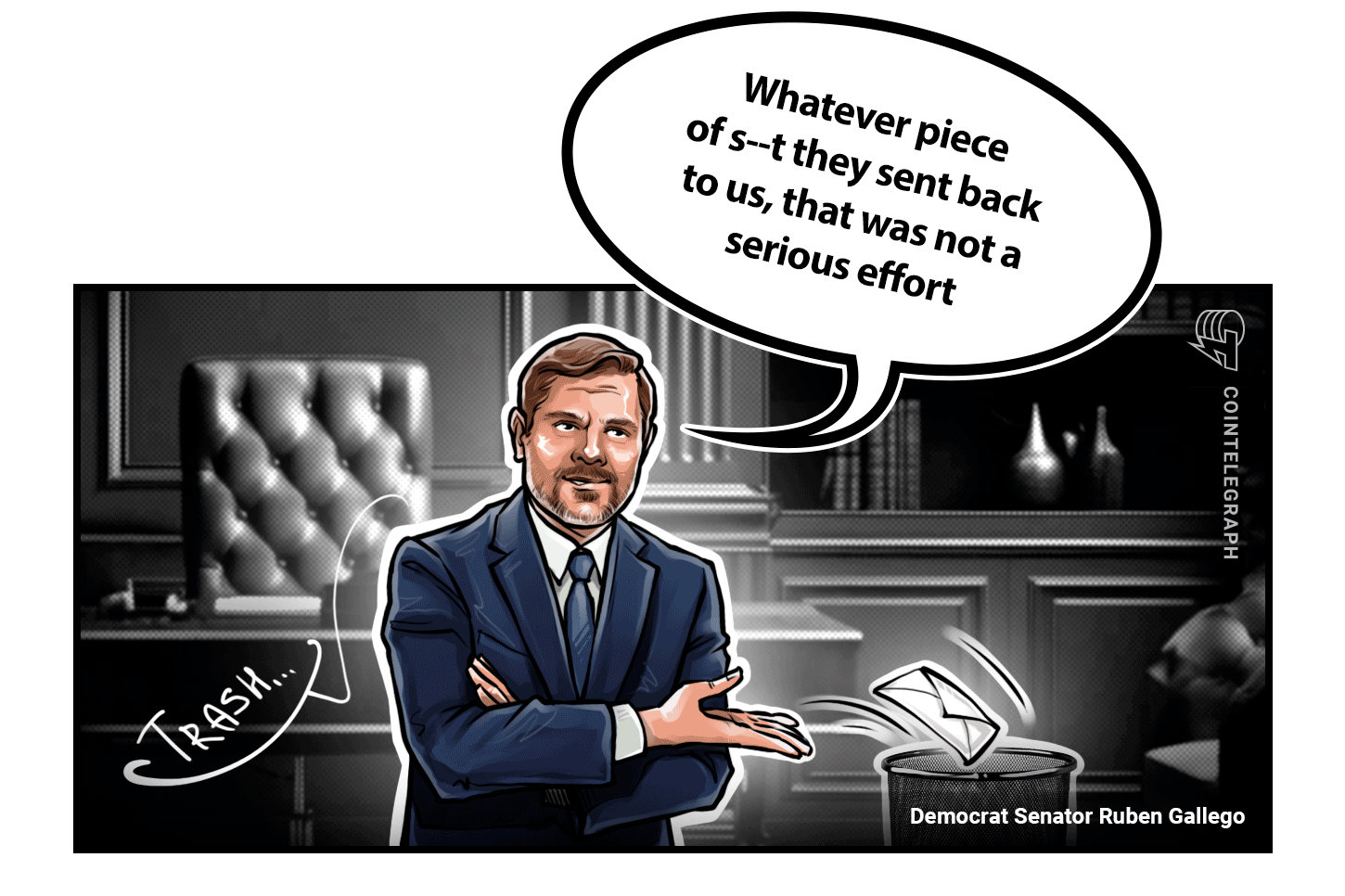

Despite wealthy memecoin entrepreneur Donald Trump agreeing to an ethics deal, the Clarity Act is floundering as the August recess deadline looms.

Senate Majority Leader John Thune doesn’t believe the Act has the votes to pass just yet, but may bring it to a vote anyway to “get Clarity started. We’ll see where the votes are.”

The ethics deal would prohibit all US officials from issuing or sponsoring digital assets, but contains some “get out of jail free” provisions for the President that the Democrats are unhappy with, including the fact the rules expire the day he is scheduled to leave office in 2029.

The ethics provisions will also be enforced by the Attorney General that Trump appointed. The Democrats instead want state Attorney Generals to enforce it — but Trump seems unlikely to agree to empower dozens of state AGs to attempt to prosecute him.

The White House described the bill as the “most comprehensive and wide-ranging ethics provision in history,” while Democratic Senator Ruben Gallego described it as a “piece of shit” and “not a serious effort.”

Negotiations are continuing to find a deal both sides can live with, but given the lack of trust, it’s not going to be easy to find a compromise.

Goldman Sachs CEO David Solomon conceded the bill is “not perfect” but has supported it anyway, along with Fidelity and Charles Schwab who represent many trillions in assets under management each.

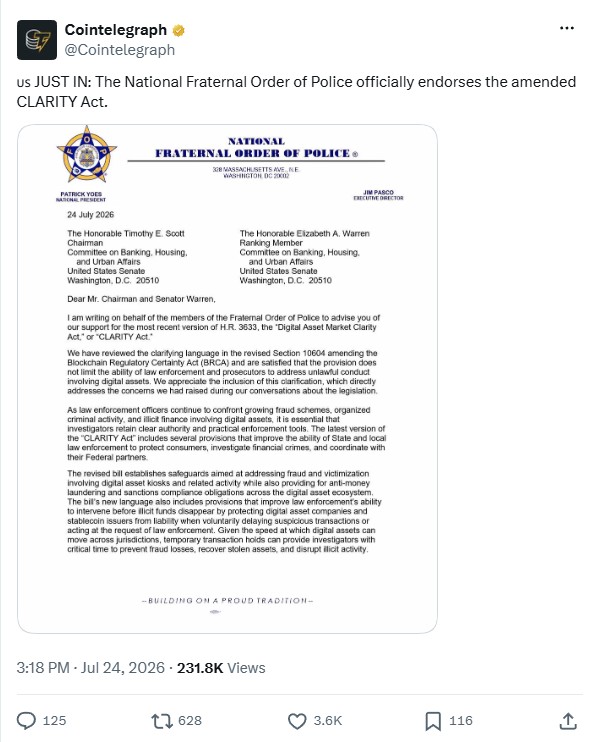

Law enforcement organizations have also begun to signal support, with The National Fraternal Order of Police representing hundreds of thousands of members, stating the latest version of the BRCA (which protects developers of decentralized protocols) would not impede investigations into money laundering and fraud.

The odds of the bill passing this year are at 38% on Polymarket.

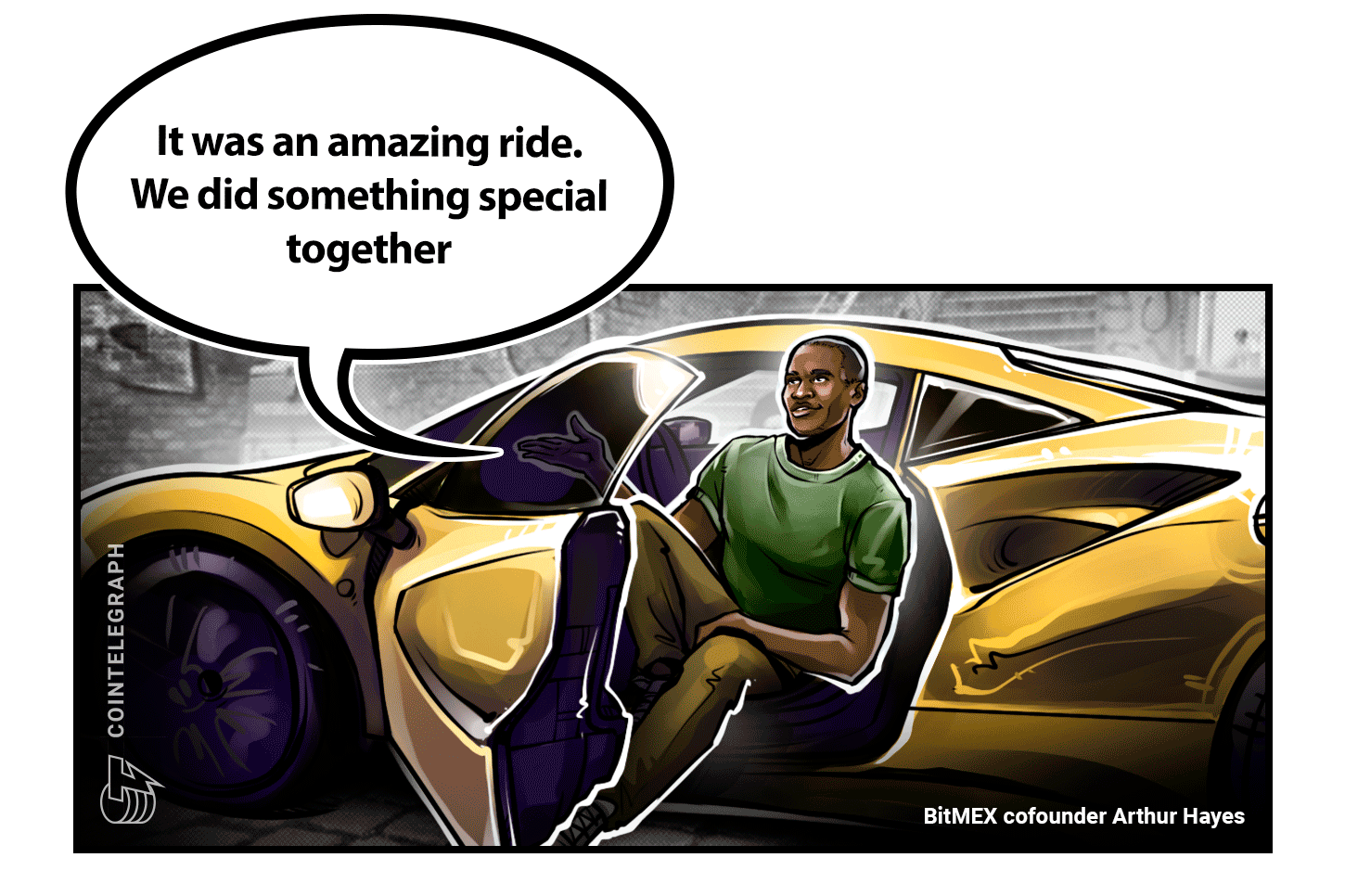

BitMEX to shut down after 11 years as class action launched against it

BitMEX, one of the pioneers of cryptocurrency derivatives trading, announced it will shut down operations in September after 11 years.

BitMEX launched in 2014 and became known for introducing the 100x leverage perpetual swaps.

In recent years volumes have tanked increased competition from major exchanges like Binance and decentralized protocols like Hyperliquid.

CryptoQuant CEO Ki Young Ju said BitMEX’s share of the Bitcoin futures market has fallen to just 0.08%, with roughly $84 million in daily trading volume.

“It was a great exchange that helped shape the industry, and now it is passing the torch to the next generation of exchanges it inspired,” Ju said.

BitMEX’s utility token BMEX collapsed in value after the announcement. That same day, news emerged of a class action lawsuit accusing the crypto derivatives platform of fraudulently engineering customer liquidations to seize traders’ collateral. BitMEX denied the allegations and said it had successfully defended itself against similar claims in the past.

Restructuring adviser Roshan Dharia told Cointelegraph the exchange’s demise shows the industry is consolidating.

The top five platforms now control an estimated 80% of global spot volume, leaving mid-tier and regional exchanges with shrinking margins and no viable path to scale… The headwinds are structural, not cyclical.

As if to undescore the point, BitMart subsequently announced it would also close in the coming months.

S&P launches blockchain fundamentals index for digital assets

S&P Dow Jones Indices and Pantera Capital have launched a digital asset index that tracks the major crypto assets — but doesn’t include Bitcoin or XRP.

The S&P Pantera Digital Asset Index is designed to be the benchmark crypto index for institutions, but it screens out blockchains based on minimum thresholds for protocol revenue, market capitalization and liquidity.

The index launched with 18 constituents, with Ether (ETH), BNB (BNB), Solana (SOL), TRON (TRX) and Hyperliquid (HYPE) as its five largest holdings, while Bitcoin (BTC) and XRP (XRP) are the largest non-constituents.

The latest index follows a broader industry push to develop institutional-grade benchmarks for digital assets, with similar products including the Nasdaq Crypto Index US ETF, the Franklin Crypto Index ETF and the the Coinbase Store of Value Index among others.

Robinhood to expand prediction markets as CFTC issues new warning

Robinhood is reportedly discussing plans to expand its existing prediction markets offerings with crypto exchange Crypto.com.

According the Wall Street Journal the talks involve integrating yes-or-no event contracts supplied by Crypto.com. Robinhood launched its prediction markets in March 2025, initially facilitated by Kalshi in order to comply with regulatory requirements from the US Commodity Futures Trading Commission (CFTC).

Bernstein analysts last week raised its price target on Robinhood (HOOD) stock to $160 from $130 per share, based on the company’s outlook for prediction markets and tokenized equities.

Meanwhile the CFTC, which aims to become the primary regulator of prediction markets, issued a shot across the bow of providers last week, telling platforms they need to get a lot more specific about event contracts certifications.

The advisory addresses concerns about the practice of submitting broad, template-style certifications that combine many potential event contract variations into a single certification.

Carl Kennedy, a partner at New York law firm Katten Muchin, also told a House Agriculture Committee hearing last week, that the CLARITY Act could help the CFTC’s efforts to oversee the “explosive growth of prediction markets.”

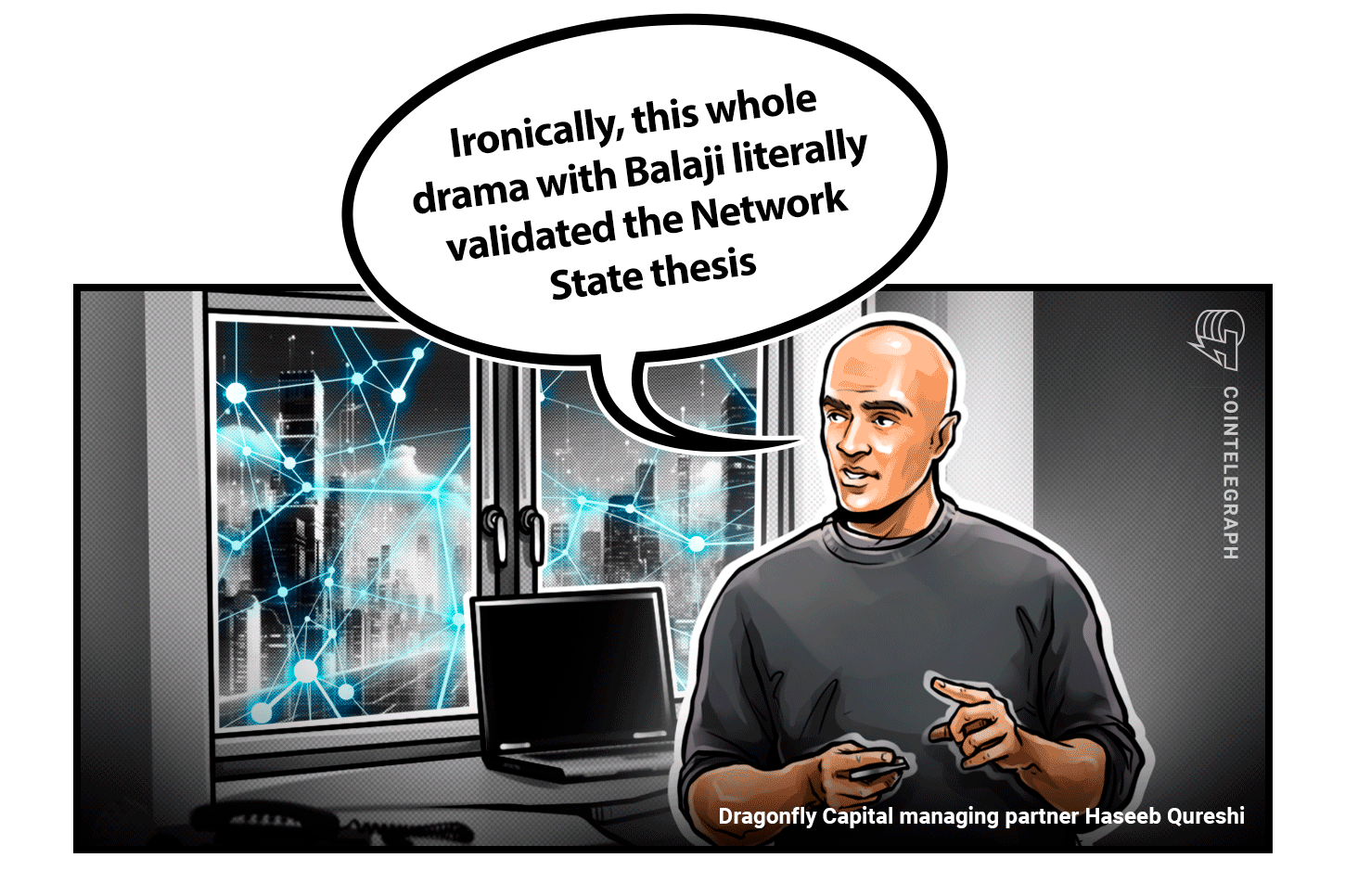

Balaji’s Network School turns to Kazakhstan amid Malaysia setback

Balaji Srinivasan’s Network School, a community of “digital nomads,” is eyeing a new campus in Kazakhstan after its Forest City campus had its business license in Malaysia revoked over alleged premises-use violations.

A memorandum of understanding was signed between Kazakhstan’s relevant Minister Zhaslan Madiyev and Srinivasan to establish the first Network School campus in the country, which aims to become a digital hub.

The School was forced out of Johor in Malaysia, following a controversy in Malaysia over allowing Israeli dual citizens to attend. The Muslim majority country has no diplomatic relations with Israel. Despite an investigation finding no visa violations, the Network School was ordered to shut down on another pretext.

Dragonfly Capital managing partner Haseeb Qureshi said the drama has validated Balaji’s Network State thesis.

“The whole idea of a network state is taking a dense group of talent and capital, and collectively negotiating with states. The Malaysia drama set up Balaji to negotiate better terms with another state to copy and paste the network there.“

Winners and losers

At the end of the week, Bitcoin (BTC) is at $65,395, Ether (ETH) is at $1,958, and XRP (XRP) is at $1.11. The total market cap is at $2.24 trillion according to CoinMarketCap.

Among the biggest 100 cryptocurrencies, the top three altcoin winners of the week are Audiera (BEAT), which gained 53%, Shinba Inu (SHIB) with a 29% gain, and Venice Token (VVV), which increased 19%.

The top three altcoin losers of the week are DeXe (DEXE), which lost 89%, Midnight (NIGHT), which fell 26%, and Pyth Network (PYTH), which dropped 10%.

Prediction of the Week

Bitcoin will get ‘lift’ from Hyperliquid, Robinhood in next crypto bull market

Bitcoin (BTC) is “finally showing signs of a bottom,” according to Matt Hougan, chief investment officer at Bitwise.

Houghan predicts that TradFi integrations, particularly Hyperliquid and Robinhood, will drive the next crypto bull market, and the resulting tide should “lift” the largest cryptocurrencies including Bitcoin and Ether.

Houghan believes crypto is bringing major benefits like 24/7 trading to traditional markets, and noted that today “nearly half the volume on Hyperliquid is in conventional assets like oil, silver, and the S&P 500 [and] it’s expanding into spot commodities, prediction markets, and options,”

Bitwise data also suggests apparent demand for BTC is showing signs of reversal. The metric measures the difference between newly-mined BTC and the supply inactive for at least one year.

Top FUD of the Week

Home invasions became most common crypto wrench attack in H1 2026: CertiK

Home invasions became the most common form of crypto wrench attacks during the first half of 2026, rising to 20 publicly reported incidents from just one a year earlier, according to blockchain security firm CertiK.

On Thursday, CertiK said it verified 52 wrench attacks worldwide in the first half of 2026, up 33.3% from 39 incidents during the same period in 2025. Kidnappings rose to 16 from 12, while robberies declined from five incidents to one.

CertiK said the recorded financial exposure linked to the attacks reached about $124.1 million, up from $10.5 million a year earlier.

The increase in home invasions suggests criminals are increasingly bypassing digital safeguards by physically coercing crypto holders and their families.

Hackers steal $31.6M in 2 crypto bridge attacks within 7 hours

Hackers stole more than $31.6 million across two unrelated crypto bridge exploits spaced just hours apart, targeting bridges operated by decentralized perpetual exchange AFX and Verus Protocol.

According to Blockaid, AFX, a decentralized perpetual exchange operating on Arbitrum, reportedly lost $24.15 million on Wednesday through a hack targeting one of its cross-chain bridges. Hours later, Blockaid said it detected an exploit targeting the Verus Ethereum Bridge that resulted in about $7.5 million in crypto being stolen.

“Another bridge, another exploit. Bridges will always be a weak link, until security is upgraded,” onchain investigator TheCrypticWolf said in a post on X.

Ethereum ETFs close week in red, end 5-day inflow streak

US-listed spot Ethereum exchange-traded funds (ETFs) logged $70.62 million in net outflows on Friday, ending a five-day inflow streak.

Ethereum funds saw $211.25 million in net inflows over the previous five sessions from July 17, according to SoSoValue data. They still posted $103.9 million in net inflows for the week ended Friday.

Despite the outflows, Ethereum ETFs extended their weekly inflow streak to three straight and have attracted $337.74 million in net inflows so far in July.

The Bitcoin ETFs reversed gains made earlier in the week to end up with $33.9 million of inflows.

Top Magazine Stories of the Week

Both parties say they want US crypto market structure legislation, but a dispute over ethics rules and who enforces them is becoming the bill’s biggest obstacle.

A Bitcoin development roadmap that addresses quantum computing risks could see the price surge by “double digits” very quickly, according to Charles Edwards.

Are the fears of an AI driven hacking epidemic totally overblown, or is this just the lull before the storm?

Cointelegraph publishes long-form journalism, analysis and narrative reporting produced by Cointelegraph’s in-house editorial team with subject-matter expertise. All articles are edited and reviewed by Cointelegraph editors in line with our editorial standards. Content published in here does not constitute financial, legal or investment advice. Readers should conduct their own research and consult qualified professionals where appropriate. Cointelegraph maintains full editorial independence.

POSCO International, South Korea’s largest trading company, has begun tokenizing trade receivables on blockchain in a test that could speed up commercial payments between its global subsidiaries.

The company, which generated $22.2 billion in revenue last year from businesses spanning steel, energy and battery materials, is working with LG CNS, the technology arm of LG Group, to issue, transfer and settle receivables on layer-1 blockchain Injective , the firms told CoinDesk in a press briefing.

The pilot is using receivables generated by real trade between POSCO’s overseas operations and their counterparties rather than simulated transactions.

Trade receivables represent money owed to a company after goods have been shipped but before payment is received. Today, those claims are typically tracked separately by buyers, sellers and banks, with reconciliation often taking days before cash can be released.

The companies said putting receivables on a shared blockchain ledger creates a single record that can be transferred and settled while carrying compliance rules with the asset itself.

WEMIX suspended bridges, liquidity-pool trading and several services after an attacker compromised a WEMIX$-linked contract and moved 724,198 USDC.e.

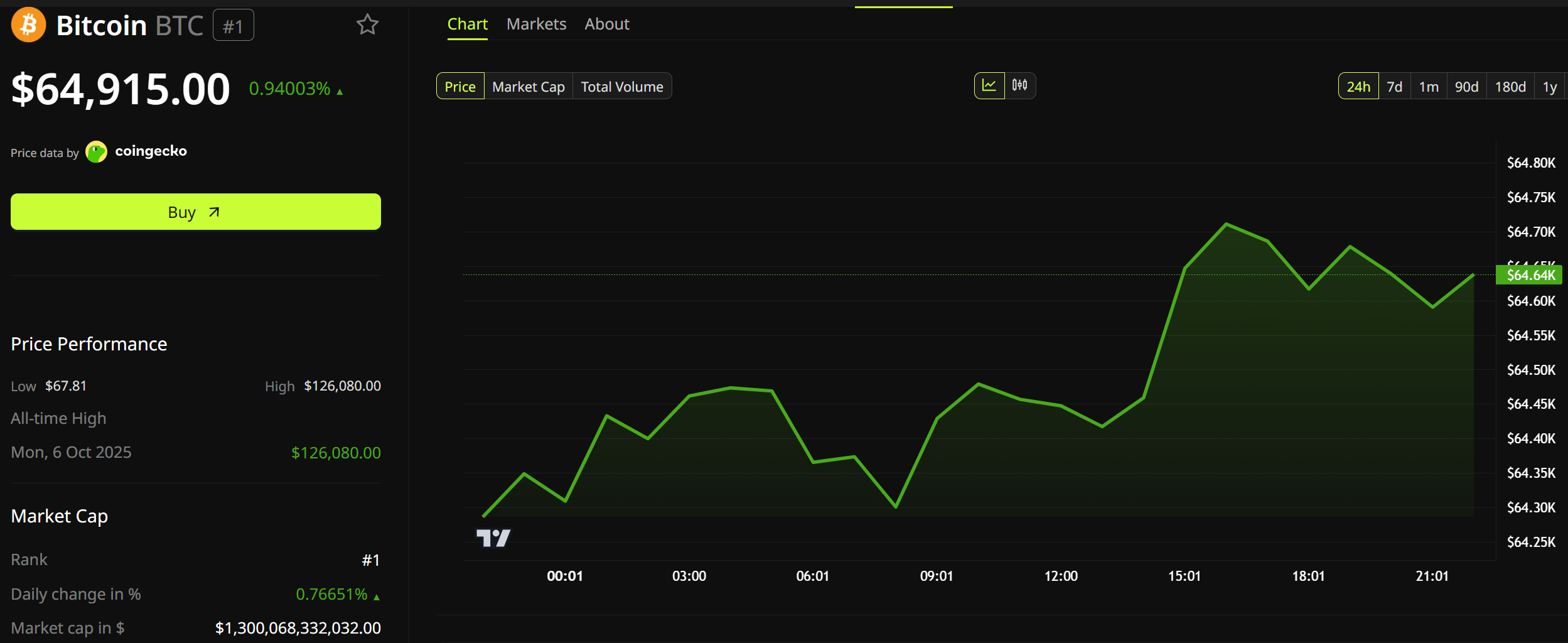

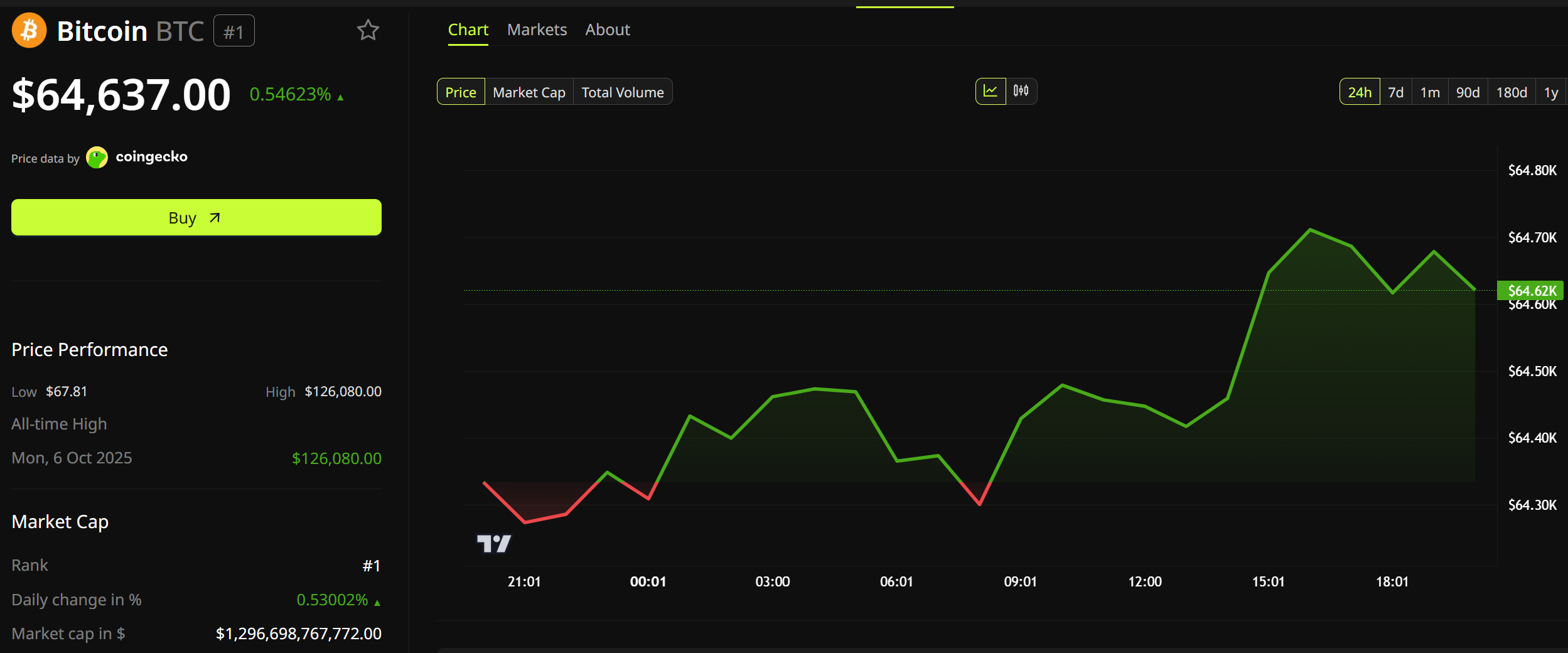

The Federal Reserve (Fed) decides on interest rates this Wednesday. Almost every economist expects no change. Traders are far less sure.

That gap matters. If the Fed surprises, stocks, bonds, oil and Bitcoin (BTC) all move fast. Bitcoin traded near $64,915 on Monday, up 0.7%.

Economists Say Hold, Traders Say Maybe Not

The Fed’s main interest rate has sat between 3.50% and 3.75% for four meetings. The FactSet consensus says it stays there.

Reuters asked 104 economists in mid-July. All 104 said hold. Fully 78 expected no change through December.

Traders tell a different story. Fed funds futures put the chance of a rate rise at 13% a week ago. By Friday it had jumped to 38%. It now sits near 36%.

“We are currently seeing the biggest indecision by the markets regarding the expected outcome for some time,” analyst The Martini Guy noted.

Follow us on X to get the latest news as it happens

The two camps are not really arguing. Economists name the single likeliest outcome. Futures price every outcome, including the unlikely ones.

The panel is also shifting. Most of those same economists now rate the chance of a hike later in 2026 as high. A month ago, most said low.

Why the doubt? Chair Kevin Warsh has stopped hinting at what comes next. The Fed will not publish new forecasts either. That leaves traders guessing ahead of this week’s central bank decisions.

“Absent, also, is so-called forward guidance, which we agreed was not well suited to the current policy conjuncture,” said Warsh.

Gregory Daco of EY-Parthenon calls a July hike unlikely. Even so, he puts the rest of the year at 60-40. Larry Meyer, a former Fed governor, expects a hold but sees Lorie Logan and Beth Hammack voting against it.

Oil and Tariffs Brought Inflation Back

Oil is the trigger. Brent crude closed at $100.69 on July 23, its first close above $100 since May 26. Prices are up over 30% this month.

Costlier oil means costlier fuel, and that lifts inflation. A weekend pause in Iran strikes has calmed things a little.

Tariffs came next. On Friday, the US added new import taxes of 10% and 12.5% on goods from 60 trading partners.

These replace tariffs the Supreme Court threw out in February, using a law that is harder to challenge.

Bond markets reacted. The 10-year Treasury yield closed Friday at 4.69%, its highest since January 2025. That is the rate the US government pays to borrow for a decade.

The two-year yield is the real tell. It ended the week at 4.33%, above the Fed’s own 3.75% ceiling. Bond traders are already braced for higher rates.

What It Means for Bitcoin

Bitcoin trades near $64,915. That is roughly 49% below its record of $126,080, set in October 2025.

When safe bonds pay 4.69%, risky bets look less appealing. That has capped Bitcoin all month.

A rate rise would be the Fed’s first since July 2023, ending three years of pauses and cuts.

A calm hold could do the opposite. Bitcoin stalled near $66,000 earlier this month, when AI-driven inflation worries capped the rally.

Warsh speaks 30 minutes after the decision. With forecasters and traders this far apart, his tone will matter more than the vote. Priced-in outcomes rarely move markets. Surprises do.

The post Fed Rate Decision Pits 104 Economists Against a 36% Hike Bet appeared first on BeInCrypto.

Bitcoin ended the first half of 2026 near $60,000 after falling about 32% since January, Binance Research reported. Its Half-Year 2026: Macro & Bitcoin report described the decline as a third consecutive quarterly loss across broader financial markets worldwide.

The weak first-half performance also extended Bitcoin’s longer-term drawdown. According to the report, the asset has fallen more than 50% from its October 2025 record high near $126,000. It has also spent 275 days below that peak, underscoring the depth and persistence of the current market downturn.

On-Chain Data Signals Market Stress

On-chain data showed 10.83 million BTC ended the period in unrealized loss, while 9.22 million units remained profitable instead. Binance Research said this marked the first loss-over-profit crossover during the current market cycle, making conditions important for analysts.

The researchers noted similar crossovers have historically appeared near major Bitcoin market bottoms before stronger recoveries eventually followed. However, they cautioned that historical patterns alone cannot confirm the current cycle will produce the same outcome.

Beyond the on-chain signals, Binance attributed Bitcoin’s weak performance mainly to broader macroeconomic conditions rather than crypto-specific developments. The report said markets shifted from liquidity-driven expectations toward economic fundamentals as monetary policy remained restrictive throughout the first half of 2026.

Expectations for interest rates also changed as hopes for aggressive cuts faded. Futures markets instead reflected an 80% probability of another Federal Reserve rate increase before December, adding pressure across financial markets.

Macro Pressures Weigh on Bitcoin

The report also said higher real yields, a stronger U.S. dollar, and tighter liquidity continued to weigh on Bitcoin. While technology stocks rebounded on optimism around artificial intelligence, BTC lagged behind many major asset classes during the same period.

A resilient U.S. economy also reduced expectations that the Federal Reserve would cut interest rates soon. Binance Research said artificial intelligence was a key driver of first-quarter economic activity. At the same time, core PCE inflation rose to 3.4%, its highest level since late 2023, reinforcing concerns that price pressures remain stubborn.

That backdrop also weakened demand for crypto. U.S. spot Bitcoin ETFs recorded $5.4 billion in net outflows during the first half of the year.

The post Down 32% in 6 Months: What Binance Research Says About Bitcoin’s Next Move appeared first on CryptoPotato.

Storj filed for bankruptcy protection on Sunday. The company says its network still works and STORJ tokens still work. Its owner made similar promises nine months ago.

Storj now wants to hand token holders a slice of the rebuilt company. But a judge must approve that. And creditors get paid first.

Why Storj Filed Chapter 11

Storj Labs filed in a federal bankruptcy court in West Virginia. The case number is 5:26-bk-00512.

Follow us on X to get the latest news as it happens

Chapter 11 is not a shutdown. It lets a company keep trading while a court helps it clear its debts.

Storj says those debts are old. They came from an earlier phase of the business. The company cannot grow its way out of them.

“The business underneath is strong and right-sized. What holds it back are legacy obligations from an earlier chapter.”

That was Kaloyan Raev, Storj’s director of software engineering. He also signed the letter to token holders, not Chief Executive Colby Winegar.

What It Means for STORJ Holders

Nothing changes for the token today, Storj says. Data still moves across tens of thousands of storage locations in more than 100 countries.

The company plans to offer holders equity in the new Storj. Equity means part-ownership. The rules for who qualifies have not been written yet.

Those rules will matter. About 143.8 million STORJ trade freely out of 425 million in total. Two-thirds of the supply sits elsewhere.

Bankruptcy also has a payment order. Creditors come before owners. Storj’s letter to token holders admits it can promise intent, not results.

The Warning Sign From October

Inveniam Capital Partners announced it was buying Storj on Oct. 22, 2025. It promised no changes to contracts, pricing, or leadership.

“We’re particularly excited to integrate the STORJ token into our ecosystem, driving greater utility and alignment across our platforms.”

That was Patrick O’Meara, Inveniam’s chairman and chief executive. STORJ traded near $0.1872 that day. It has fallen about 60% since.

A closer warning came this month. MVMT Labs filed Chapter 11 in Delaware on July 15. Its Movement (MOVE) token hit a record low of $0.00964 ten days later.

STORJ has held up so far. It trades near $0.0745, up 1.5% on the day. Volume is $5.6 million and market value is $10.7 million.

The wider sector is soft too. Storage and infrastructure tokens have lagged even as network usage grew.

Storj says it will share court dates as they land. But the fine print of the equity offer will decide what holders actually get.

The post Storj Chapter 11 Raises the Biggest Question for STORJ Token Holders appeared first on BeInCrypto.

Some analysts say Bitcoin (BTC) could reach $200,000 if the CLARITY Act becomes law. That is a very big if. Seven roadblocks now stand between the bill and a Senate vote.

The CLARITY Act would decide which US agency polices crypto. It has sat on the Senate’s to-do list since June 1 without a vote.

Why $200,000 Depends on One Bill

Start with the number. It describes one scenario, not a firm forecast. Research desk FM Intelligence sees Bitcoin between $135,000 and $200,000 over the next year. It gives that outcome one-in-four odds, and only if the bill is signed before the November midterms. Its main case is far lower at $95,000 to $130,000, per its published scenarios.

Now look at the gap. Bitcoin trades at $64,671, up 0.48% in a day, with a market value of $1.29 trillion.

Reaching $200,000 means the Bitcoin market price would need to roughly triple. It already sits about 49% below its record of $126,080, set on October 6, 2025.

Sentiment has turned this month, though. Treasury Secretary Scott Bessent said on July 21 that Congress was on the “1-yard line.” Bitcoin jumped toward $67,000, ending roughly 15% above its early July low.

“The formal passage of the Clarity Act into law will be the ultimate catalyst, sparking a new bull market as institutional allocators race to gain exposure out of a fear of missing out,” Forbes reported, citing CK Zheng of ZX Squared Capital.

CK Zheng once ran risk for Credit Suisse. He now runs the hedge fund ZX Squared Capital.

Wall Street Has Already Priced In Some Failure

Big banks have moved the other way. Citi cut its 12-month Bitcoin target to $82,000 on July 1. That was its second cut of 2026. The bank opened the year expecting $143,000, then trimmed that to $112,000 in March.

Its target has fallen 43% this year. Each time, Citi blamed the stalled bill rather than Bitcoin.

Alex Saunders leads the bank’s macro and decentralized finance (DeFi) research. He warned in March that the window for US legislation was closing.

Standard Chartered is warmer but still modest. Geoffrey Kendrick kept its year-end target at $100,000 in mid-July, which would need a 55% climb.

7 Roadblocks in the Bill’s Way

The following roadblocks make the case for what may make the Clarity Act not get the passage analysts are wagering their passage best on.

1. The senators blocking it are not crypto opponents

Seven Democrats rejected the current text in a joint statement on July 22. They are Catherine Cortez Masto, Angela Alsobrooks, Cory Booker, Ruben Gallego, John Hickenlooper, Mark Warner and Raphael Warnock.

Here is the surprise. All seven voted for the GENIUS Act, the stablecoin law, in June 2025.

That bill passed 68-30 with 18 Democrats behind it, Senate records show. Trump signed it into law weeks later.

Elizabeth Warren voted against it and remains opposed today. She was never a winnable vote, so she is not the obstacle.

The wall is built from proven crypto supporters.

2. Republicans cannot reach 60 without them

Senators can stall any bill by refusing to end debate. Breaking that stall takes 60 votes. Republicans hold 53 seats, so seven must come from Democrats.

3. Trump earned $1.4 billion from crypto

Senate Banking’s minority staff reviewed the President’s financial disclosures. They found more than $1.4 billion in crypto income for 2025 alone.

World Liberty Financial, the Trump family’s DeFi venture, supplied $799 million. The $TRUMP meme coin added another $636 million.

4. Only Trump’s Justice Department could enforce the new rules

Republicans released fresh ethics language on July 22, and Trump agreed to it. Ranking Member Warren says it has holes.

State attorneys general could not enforce it, she argues. The rules would also expire once Trump leaves office.

“Donald Trump raked in more than $1.4 billion from cryptocurrency ventures, and this bill does nothing to prevent him from vacuuming up his next $1.4 billion in crypto profits… This bill should be dead on arrival,” said Senator Elizabeth Warren.

Follow us on X to get the latest news as it happens

5. The real deadline is August 7

The Senate’s summer break starts August 10, its own calendar shows. Friday, August 7 is therefore the last working day before members head home.

6. September offers only 14 working days

Senators return on September 14. They leave again on October 5 to campaign for the midterms.

That leaves 14 scheduled working days. It is a thin window for a bill that took a year to negotiate.

7. The House may reject the Senate’s version

Chairman Tim Scott moved the bill through committee 15-9 on May 14. The Senate then swapped in its own text.

The House passed a different version 294-134 in July 2025. It must now accept the 300-page Senate draft text or negotiate a compromise.

The Trap at the Center of the Bill

Traders have turned optimistic quickly. On Kalshi, the odds of passage before April 2027 jumped to 52% from 33% in one week.

Yet the bull case contains a trap. Bitcoin needs the bill signed before the midterms. The unresolved fight is over how much the President may keep earning from crypto.

Passing it would hand Trump a win weeks before voters decide control of Congress. Blocking it costs Democrats little, since the hurdles facing the bill run out the clock anyway.

Seven senators who already backed crypto once must decide whether this version is worth the price.

The post Analysts See Bitcoin at $200,000 on CLARITY Act Passage, But 7 Roadblocks Remain appeared first on BeInCrypto.

Sberbank, Russia’s largest bank, says it plans to roll out cryptocurrency trading infrastructure by Dec. 1, including a “digital depository” designed to record customers’ crypto ownership and handle transactions largely outside the public blockchain.

Interfax reported that the depository will track rights in clients’ cryptocurrency positions and process most transfers off-chain, while Sberbank will also run active wallets for deposits, withdrawals, and client-initiated transfers.

Key takeaways

- Sberbank’s scheduled Dec. 1 rollout would add a regulated-style custody and settlement layer, using a digital depository to record ownership and process transactions off-chain.

- Russia’s crypto market framework is progressing toward an effective date of Sept. 1, 2026, defining regulated participant categories and expanding central bank oversight.

- Regulatory preparation is unfolding alongside intensifying EU and UK sanctions affecting crypto-asset service providers linked to Russia-related activity.

- Investors and market participants should watch how Russia’s central bank sets licensing rules and eligibility for which assets can be offered through intermediaries.

Sberbank’s digital depository: custody and off-chain settlement

According to Interfax, the digital depository will serve as the core component of Sberbank’s planned infrastructure. It is intended to maintain records of customers’ cryptocurrency rights and to account for transactions outside the main blockchain.

The state-affiliated press service quoted Alexander Vedyakhin, Sberbank’s first deputy chairman of the management board, explaining that the depository would also support transfers requested through “active wallets.” In other words, customers’ interactions—depositing, withdrawing, and moving crypto via the bank—would be handled through a banking-operated system that mirrors custody and payment workflows more than traditional on-chain exchange mechanics.

The practical implication is that, if implemented as described, Sberbank could reduce reliance on direct peer-to-peer blockchain settlement for everyday client movements, instead concentrating transaction processing and ownership accounting inside the bank’s infrastructure.

Russia’s regulated crypto framework heads toward 2026

The Sberbank announcement arrives as Russia’s legislators have advanced the country’s first comprehensive crypto market framework. Earlier in the month, lawmakers completed final readings on a bill intended to bring crypto trading, custody, and settlement into a regulated financial system.

Earlier coverage from Cointelegraph noted that the bill would grant the Bank of Russia broad oversight of the regulated market. That oversight would include determining which crypto assets may be offered via licensed intermediaries and issuing implementing regulations.

Cointelegraph’s reporting also highlighted that the central bank has established liquidity thresholds for participating in the regulated market. Those thresholds include an average market capitalization above 5 trillion rubles (about $64 billion) and an average daily volume above 1 trillion rubles (about $12.8 billion) over a two-year period.

Once the framework takes effect, it establishes five categories of regulated market participants: crypto exchanges, brokers, asset managers, custodians, and exchange service providers. The framework is set to define what market participants can do—such as buying, selling, holding, and exchanging crypto assets—as of the effective date, Sept. 1, 2026.

Infrastructure rollout meets tightening sanctions environment

While Russia builds out domestic infrastructure, external compliance pressure continues to rise. The move toward a working crypto system inside Russia is unfolding as the European Union expands sanctions targeting Russia amid its war on Ukraine.

Last week, the EU listed cryptocurrency exchange HTX (formerly Huobi Global) among sanctioned entities. In a Thursday decision, the European Council amended earlier measures “in view of Russia’s actions destabilizing the situation in Ukraine,” adding HTX to a list of 18 entities “providing crypto-assets services or payment services established outside of the Union that are significantly frustrating the purpose of the prohibitions” against Russia.

Earlier, Cointelegraph reported that EU officials said they would prohibit Belarusian nationals and residents from owning, controlling, or managing crypto exchanges and digital asset service providers, aligning the approach with the EU’s Markets in Crypto Assets (MiCA) framework.

The sanctions on HTX were not limited to the EU. The UK government imposed similar measures in May, stating there were “reasonable grounds to suspect” HTX supported Russia’s government by using financial services and funds facilitated by sanctioned entities.

For market participants, the key tension is that Russia is tightening domestic regulation while many foreign-facing crypto service providers remain exposed to sanction risks and compliance constraints. That gap can shape where liquidity flows, which counterparties can operate with certain clients, and how banks and exchanges structure their services.

What to watch next: licensing mechanics and depository operations

Sberbank’s planned digital depository—alongside the broader Russia framework set for Sept. 1, 2026—puts the spotlight on implementation details. Readers should watch how the Bank of Russia operationalizes licensing requirements, how asset eligibility is defined under the liquidity thresholds, and whether bank-operated off-chain custody and transfer accounting becomes a model for other regulated intermediaries.

Outside Russia, the sanctions trajectory suggests that cross-border partnerships and access to international payment rails may remain a moving target for crypto businesses tied to the region.

It was less than a year ago when the Ethereum validator exit queue had stretched for 45 days as millions of tokens waited to be unlocked from staking.

Today, that queue has completely emptied out, while the number of ETH actually staked continues to grow to a new record.

No One Wants to Unstake ETH

Current data from ValidatorQueue shows that there are zero ETH waiting to be unstaked from the network. This means that if anyone decides to unstake their altcoin holdings, they can do so immediately, subject only to the protocol’s normal withdrawal process.

This is a significant turnaround from Q3 last year, when the exit queue had swelled to roughly 2.6 million coins. Validators were forced to wait up to 45 days before they could withdraw their holdings. At the time, Ethereum co-founder Vitalik Buterin defended the extensive period, arguing that it’s an important element of the network’s defense.

The narrative has completely flipped now. ValidatorQueue shows that over 2.5 million ETH is currently waiting to enter staking, translating into an estimated activation delay of nearly 44 days. Investors are willing to wait for a month and a half just to begin earning staking rewards on their ETH holdings.

This shifted imbalance suggests that investors are confident in Ethereum’s long-term outlook to remain strong despite the year-to-date price retracement. It also removes one of the most significant concerns from last year – that millions of staked ETH could suddenly flood exchanges if validators decide to cash out.

Record ETH Is Locked

The broader staking picture has also continued improving as the total number of active validators securing the network has neared 900,000. Almost 41 million ETH is currently staked, which is equivalent to roughly 33.6% of the entire circulating supply. This is the highest percentage in the network’s history, and it means that every one out of three ETH is locked in staking rather than sitting on exchanges or actively circulating.

Tom Lee’s Bitmine remains a leader in this field, having staked over 4.9 million tokens through its institutional platform MAVAN.

Although staked ETH is not permanently removed from supply, it is generally considered less liquid because validators must go through Ethereum’s withdrawal process before they receive access to those holdings.

However, Merlijn The Trader reported a rather intriguing and unexpected twist. The record amount of staked ETH comes even as staking rewards are down to 2.62% per year from 3.05% and issuance has increased from 0.757% to 0.842%.

The post Nobody Wants to Unstake Ethereum Anymore: Here’s Why It’s a Big Deal appeared first on CryptoPotato.

People shared private chats with Claude. Then strangers found those Claude chats indexed by Google, wallet details and all.

The chats also held access keys, CVs and company files. Anthropic, the company behind Claude, had not addressed the matter as of this writing.

Claude Chats Indexed by Google, Explained

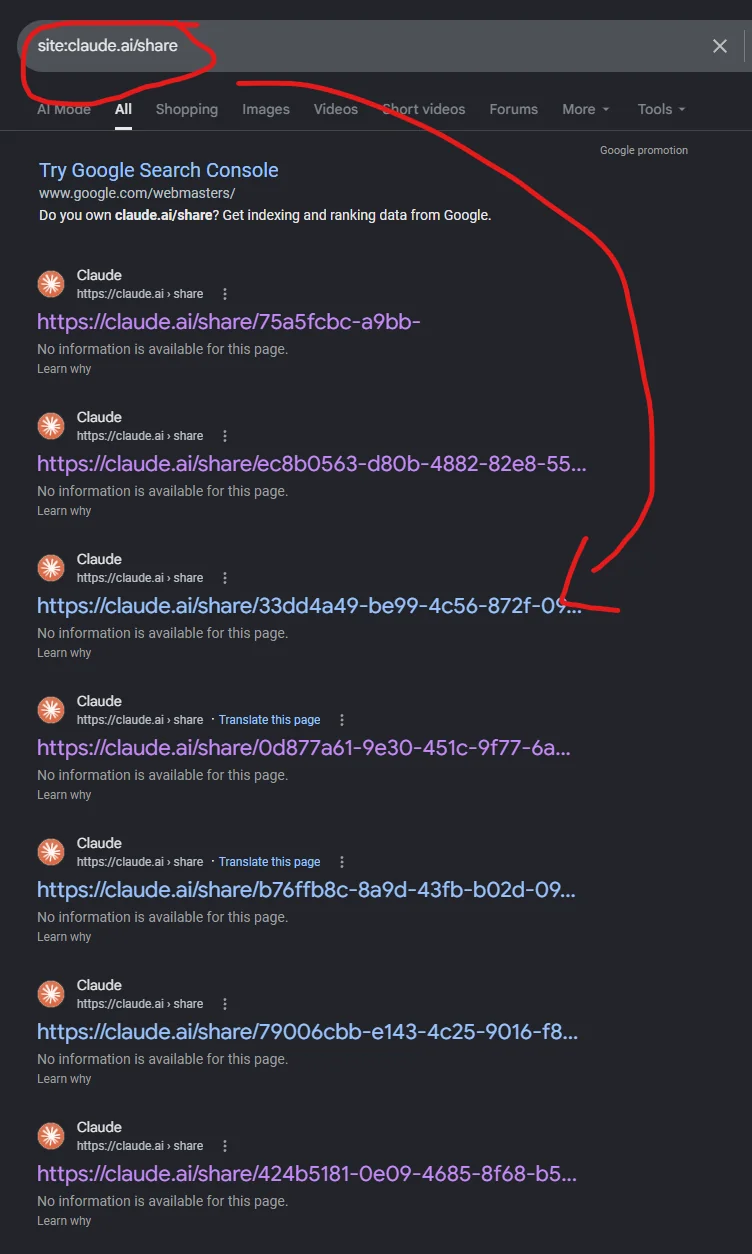

A Reddit thread over the weekend showed the problem. One simple search brought up page after page of shared Claude chats.

People in the thread blamed a missing “noindex” tag. That tag tells Google to hide a page. The real cause looks different. Anthropic’s robots.txt file tells search engines to skip its share pages.

Here is the catch. Google will not open a blocked page. So it never sees the hide tag inside.

Picture a locked door with a note taped behind it. Nobody gets in. Nobody reads the note either.

Google can still show the web address. Other sites link to it, so Google knows it exists. Google just cannot see what sits on the page. Its own guide spells this out.

That fits the screenshots going round on X. Under each Claude link, Google said “No information is available for this page.” Bing showed a similar line.

So the chats never appeared in search previews. But anyone who spotted a link could click it and read the lot.

What the Share Button Really Does

Claude chats are private by default. That changes only when a user clicks Share.

Share builds a public web page. It holds every message sent up to that moment.

Two things stay out, according to Anthropic’s own help pages. Uploaded files are not included. Nor is raw data pulled in by connected tools.

Team and Enterprise accounts cannot share in public at all. This one lands on free, Pro and Max users.

Old links sit under Settings, Privacy, then Shared chats. Click Unshare to kill one.

Why Crypto Users Should Care

Developers flagged it, noting that wallet details and login credentials sat among the results, with some allegedly being able to read strangers’ chats through Brave Search.

For crypto, the stakes differ. A leaked password can be changed. A leaked private key cannot, as BeInCrypto has shown in past private key leak losses.

Small wallets are already the main target. Chainalysis counted 158,000 personal wallet hacks in 2025. Those hit 80,000 people and cost $713 million.

The 2022 figure was 54,000. None of it is tied to AI chats. It simply shows where thieves now spend their time.

More traders also connect AI to wallets to move funds and check code. Researchers have flagged tools that could expose wallet seed phrases as well.

One caution belongs here. Nobody has confirmed a seed phrase or a working key in the indexed chats. Nobody has reported stolen funds either.

Some developers pushed back too. Those pages were public by choice, they argued.

What Happens Next

The pages have gone from search. They have not gone away. Anyone with a saved link can still open the chat. Only the owner can stop that, by unsharing.

This has happened before. Google indexed just under 600 Claude chats in September 2025, as Forbes reported. OpenAI had dropped its own public sharing option a month earlier. It now faces a ChatGPT data sharing lawsuit.

A clean fix exists. Let Google open the share pages, then add the hide tag there.

Whether Anthropic does it will decide if this happens a third time.

The post People Found Crypto Wallet Data in Claude Chats Indexed by Google appeared first on BeInCrypto.

10 Lechon Belly Business Name Ideas Philippines

3M Open: Rookie Jackson Koivun holds nerve to beat Scottie Scheffler for first PGA Tour win

Intel is reversing course and bringing hyper-threading back to its server chips

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World6 days ago

Crypto World6 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat5 days ago

NewsBeat5 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech6 days ago

Tech6 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech6 days ago

Tech6 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

NewsBeat7 days ago

NewsBeat7 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Business5 days ago

Business5 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment5 days ago

Entertainment5 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Tech6 days ago

Tech6 days agoWatch Flock Safety CEO Garrett Langley discuss the future of surveillance at TechCrunch Disrupt 2026

-

Crypto World4 days ago

Crypto World4 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

NewsBeat6 days ago

NewsBeat6 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Crypto World7 days ago

Crypto World7 days agoCircle’s President Sold Over 360,000 Shares, The Filings Explain Why

-

Tech7 days ago

Tech7 days agoSubway Sandwich Computers Get a Second Life as Gaming Machines

-

Sports4 hours ago

Sports4 hours agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

News Videos3 days ago

News Videos3 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Sports3 days ago

Sports3 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Fashion3 days ago

Fashion3 days ago16 Dresses for the High Summer Event

-

Entertainment7 days ago

Entertainment7 days agoStephen Colbert Returns to Social Media After Late Show End

-

Tech7 days ago

Tech7 days agoThe 35 Best Board Games for Family Game Night

-

Crypto World6 days ago

Crypto World6 days agoAndrew Cuomo joins OKX board as crypto exchange expands in U.S.

You must be logged in to post a comment Login