The free festival, coming back to the city centre on Friday, February 27 and Saturday 28 is set to transform the streets of Durham with colourful light displays and ice carvings.

Visitors will have the opportunity to follow a themed trail of hand-crafted ice sculptures, witness live carving demonstrations, and see the city come alive with engaging and interactive experiences.

The displays will span a broad variety of themes.

Fire and Ice 2025. (Image: SARAH CALDECOTT)

Last year’s displays included a Beatles drum kit installation and an Elvis Presley tribute.

Advertisement

There will be entertainment for families, locals, and visitors.

Families can also anticipate interactive installations and fiery performances.

The event traditionally brightens up the end of February with live street entertainment and a lively, colourful atmosphere.

Harry Maguire was shown a red card in the 78th minute of Manchester United’s 2-2 draw away to Bournemouth last month, and his reaction has seen him charged by the FA

Referee Stuart Attwell’s decision was later ratified by VAR and the hosts scored the resulting penalty. Maguire was incensed by the decision, confronting both Attwell and the fourth official, Matt Donohue.

And his reaction has got him in trouble. A statement from the FA read: “Harry Maguire has been charged after being sent off in the 78th minute of Man Utd’s Premier League match against Bournemouth on March 20.

Advertisement

“It’s alleged that the defender acted in an improper manner and/or abusive and/or insulting words and/or behaviour towards the fourth official following his dismissal. Harry Maguire has until April 2 to provide a response.”

Maguire was hit with a one-match suspension, ruling him out of the Red Devils’ clash with Leeds United on Monday, April 13. But his ban could be extended given the charge.

United’s next game after Leeds is away to Chelsea on Saturday, April 18. Interim manager Michael Carrick was unhappy with Maguire’s red card, arguing that his side should’ve also got a penalty earlier in the game.

There will be more to follow on this breaking news story and Mirror Sport will bring you the very latest updates, pictures and video as soon as possible.

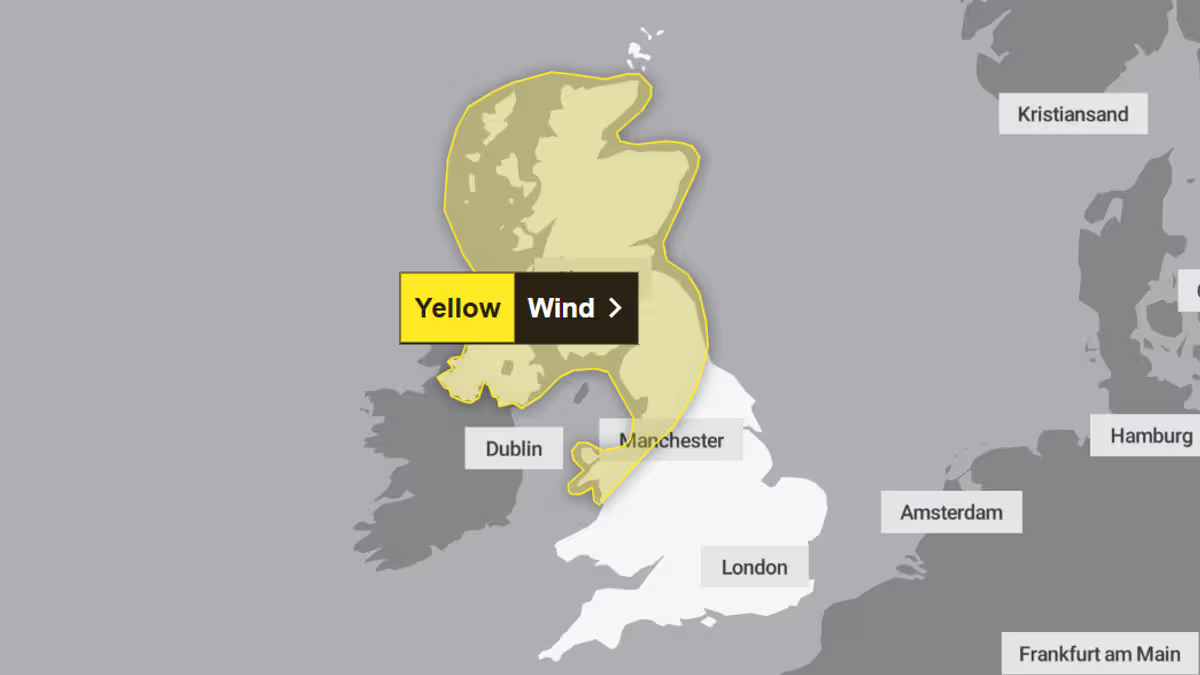

With thousands looking to get away for the long weekend, a “rapidly deepening area of low pressure” is likely to scupper many plans and cause transport chaos.

Lanarkshire homes face an Easter battering after the Met Office issued a weather warning.

Advertisement

With thousands looking to get away for the long weekend, a “rapidly deepening area of low pressure” is likely to scupper many plans and cause transport chaos.

Bridges could close with restrictions places on high-sided vehicles, especially on exposed routes. The Met Office says there is a “slight chance” of power cuts, as well as damage to buildings.

Households are being encouraged to secure loose items such as bins, garden furniture, trampolines, tents, sheds, and fences. The warning runs from 6pm on Saturday, April 4, until midnight on Sunday, April 5.

It states: “A rapidly deepening area of low pressure is likely to move northeastwards close to or across northwestern parts of the UK during Saturday evening and night, clearing to the North Sea by Sunday.

Advertisement

“Whilst there is some uncertainty over the exact track, intensity and shape of this area of low pressure, a period of strong west to southwesterly winds is expected during Saturday night and into the first part of Easter Sunday, before gradually easing through the day.

“Peak gusts of 50-60 mph will be possible fairly widely, with 60-70 mph in more exposed locations.

“There is a slight chance of some very strong winds across parts of Scotland, particularly in the west, where gusts of 80-90 mph may be possible in exposed areas for a time.”

The warning covers 20 of Scotland’s local council areas including North and South Lanarkshire.

The mum of a seven-year-old girl tragically discovered dead at a golf course had been suggested a new childminder on Facebook just days prior to the incident, close friends have revealed.

Nyla May Bradshaw was found in a pond at Owston Hall golf course, near Doncaster, on Monday. The autistic girl had been reported missing from the village of Skellow at 9.50am on the same day.

Advertisement

Heartfelt tributes have poured in from distraught family members, including Nyla’s mum Hailey, who referred to her as her “sweet little girl”. Charlotte Emma, a close friend of Nyla’s mother, has now disclosed that Hailey had sought recommendations for a childminder from a local Facebook group and had been suggested someone professing to be an autism specialist, reports YorkshireLive.

However, within two hours, the mother reportedly received a text informing her that Nyla was missing – and she was subsequently found in the pond.

Charlotte told The Metro: “A lot of us blame ourselves because Hailey doesn’t usually leave her with anybody, she goes to a special school. But the school holidays have come up and her mum was desperate for a child minder. She’d asked a Facebook group if anybody knew of any in the area.”

Advertisement

Kieran Bradshaw, her father, has paid tribute to his “best friend” and an “amazing daughter” in a heartfelt post on Facebook. He expressed: “Sat here feeling so alone with everybody around us but not knowing what the rest of our lives look like without our little girl, noises around the house, songs coming on and adding them to her own Spotify playlist for the car, seeing a McDonald’s and wanting it calling out, Thursdays we’re baking days and having a right good song along while dancing.

“You were so loved Nyla you touched everyone’s heart that ever met you. I’ll never ever go a moment without you in my thoughts.

“You saw the world as your playground free from any worries or fears and I learnt from you in my darkest of places that your smile and outlook was something so bright and I can’t believe I’ll not hear your voice again it took a long time for you to start saying ‘I love you’ or ‘I miss you’ only a year ago. You are my best friend and my amazing daughter. I hope grandad had a balloon waiting for you when you meet him he will look after you.”

A GoFundMe page has been established to assist the family with funeral expenses. The organisers stated that the family is “now facing the unimaginable pain of losing their beautiful daughter, alongside many unanswered questions and the overwhelming responsibility of arranging her funeral,” according to the fundraiser.

Advertisement

Get more Daily Record exclusives by signing up for free to Google’s preferred sources. Click HERE.

Advocacy groups and experts condemned YouTube for serving up low-quality artificial intelligence-generated videos to its most vulnerable audience: children.

In a letter to YouTube CEO Neal Mohan and Sundar Pichai, the CEO of YouTube’s parent company Google, children’s advocacy group Fairplay expresses “serious concern” about the spread of AI-generated videos on both YouTube and YouTube Kids. The letter, which was sent on Wednesday morning, was signed by more than 200 organizations and individual experts such as child psychiatrists and educators.

“This ’ AI slop ’ harms children’s development by distorting their sense of reality, overwhelming their learning processes and hijacking their attention, thereby extending time online and displacing offline activities necessary for their healthy development,” the letter reads. “These harms are particularly acute for young children.” The letter calls on YouTube to clearly label all AI-generated content and ban any AI-generated content on YouTube Kids. They also propose barring AI-generated videos from being recommended to users under 18 and implementing an option for parents to turn off AI-generated content even if their child searches for it.

The letter is signed by 135 organizations including the American Federation of Teachers and the American Counseling Association, and around 100 individual experts like “The Anxious Generation” author Jonathan Haidt. The letter is part of a larger campaign from Fairplay that also includes a petition.

Advertisement

Much of this AI-generated content is fast-paced with bright colors, lively music and clickbait titles that work to grab the attention of young viewers, the letter outlines. There has been a growing movement online against AI-generated content, particularly when it looks or feels low quality or leans into the meaninglessness of “ brainrot.”

Spokesperson Boot Bullwinkle said in a statement that YouTube has “high standards for the content in YouTube Kids, including limiting AI-generated content in the app to a small set of high-quality channels.”

“We also provide parents the option to block channels. Across YouTube, we prioritize transparency when it comes to AI content, labeling content from our own AI tools, and requiring creators to disclose realistic AI content,” Bullwinkle said. “We’re always evolving our approach to stay current as the ecosystem evolves.”

YouTube’s current policy regarding AI-generated content requires creators to disclose when content that’s “realistic” is made with altered or synthetic media, including generative AI. Creators are not required to disclose when generative AI is used to create content that is clearly unrealistic, including animated videos and those with special effects.

Advertisement

YouTube said it is actively working on developing labels for YouTube Kids.

In its letter, Fairplay argues that voluntary disclosure policy and what it sees as an “extremely limited” definition of altered and synthetic content mean kids still see a flood of AI-generated videos that are not labeled as such. They also argue that many children who watch YouTube videos are not yet able to read or to comprehend something like an AI disclosure. That leaves children “to fend for themselves or their parents to play whack-a-mole,” the letter reads.

Fairplay’s campaign comes shortly after Google’s AI Futures Fund invested $1 million into Animaj, an AI animation studio that makes videos for kids and draws in staggeringly high viewership numbers, according to Bloomberg.

The campaign follows a landmark verdict in a social media addiction trial in which a California jury found that YouTube designed its platform to hook young users without concern for their well-being. Meta was also found liable on the same counts as YouTube in the same case.

Advertisement

“Pushing AI slop onto young children is just another testament to how YouTube and YouTube Kids are designed to maximize children’s time online — including babies. AI slop hypnotizes young children, making it hard for them to get off their screens and move onto essential activities like play, sleep and social interaction,” said Rachel Franz, the director of Fairplay’s Young Children Thrive Offline program, in a statement. “What’s more, YouTube’s algorithm makes it impossible for kids to avoid AI slop.”

Earlier this year, YouTube head Mohan listed out “managing AI slop” as one of the company’s priorities for 2026. In a January blog post, he wrote that the company was “actively building on our established systems that have been very successful in combatting spam and clickbait, and reducing the spread of low quality, repetitive content.”

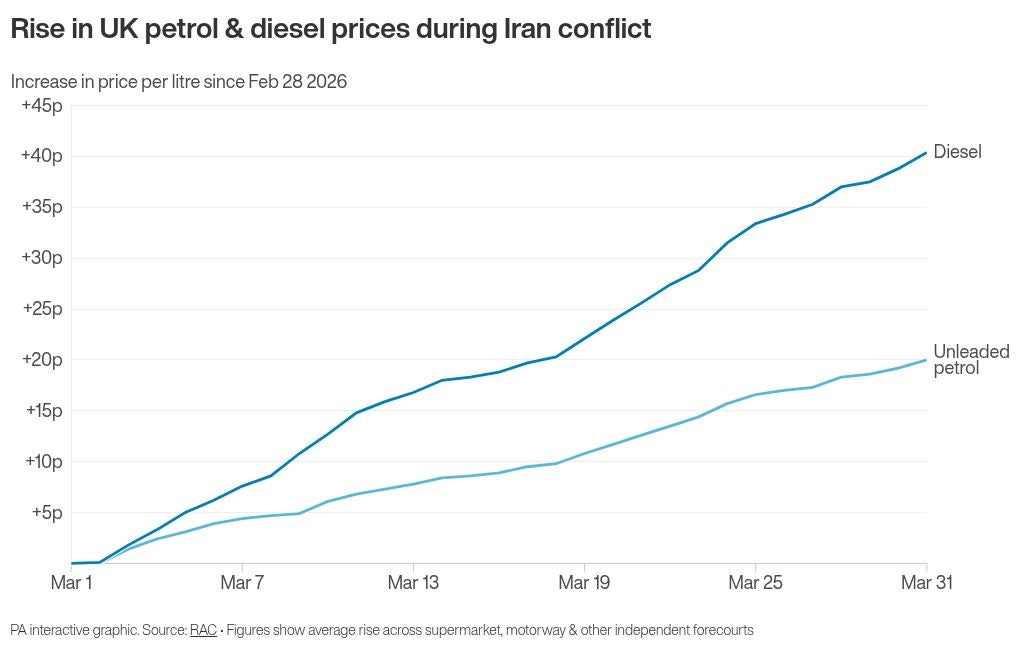

Around 1.3 million more UK households are facing a jump in their mortgage costs following the economic “shock” caused by the conflict in the Middle East, the Bank of England has warned.

The Bank’s latest financial stability report (FSR) said the UK economic outlook has “deteriorated”, increasing pressure on UK households and businesses.

It came as Sir Keir Starmer warned the coming weeks “will not be easy”, adding that “how we emerge from this crisis will define us for a generation”.

Oil and gas prices have increased sharply since the conflict began between US-Israeli forces and Iran at the end of February, with equity markets also shaken by the significant volatility.

“The shock will weigh on growth, increase inflation and tighten financial conditions,” according to the report.

Advertisement

Nevertheless, the central Bank’s financial policy committee said the UK financial system has been “resilient so far”.

It added, however, that the global macroeconomic backdrop is more unpredictable following the conflict, with this coming at a time when global risks were “already elevated”.

Giving a Downing Street press conference to address the cost of living spike caused by the war, the prime minister signalled the government would seek stronger ties with the EU as part of an attempt to mitigate the conflict’s impacts.

Sir Keir said the “volatile” international situation caused by the US-Israeli conflict with Tehran meant Britain’s “long-term national interest requires closer partnership with our allies in Europe and with the European Union”.

He added: “As the chancellor has rightly pointed out, Brexit did deep damage to our economy, and the opportunities to strengthen our security and cut the cost of living are simply too big to ignore.”

Advertisement

Meanwhile, Rachel Reeves has insisted that any cost of living support offered by the government will be based on household income and refused to commit to immediate support for drivers amid rising fuel costs.

Sir Keir Starmer says he will act in the national interest as he reiterates Britain will not get ‘dragged into’ the conflict in the Middle East (PA Wire)

“I want to learn the lessons of the past because when Russia invaded Ukraine, the richest, the best-off third of households got more than a third of the support. That makes no sense at all”, the chancellor told the BBC on Tuesday.

The Bank of England’s report said: “This increases the possibility of large, frequent and potentially overlapping shocks, and periods of intense volatility.”

Experts at the Bank indicated there is a risk that pressure on the global economy could result in “multiple vulnerabilities” crystallising at the same time.

This would have an increased impact on financial stability and “the provision of vital financial services to UK households and businesses”.

Advertisement

The report highlighted that UK households are set to face greater financial pressure following the conflict, due to increased energy prices and elevated mortgage rates.

Last month, the Bank’s monetary policy committee held the UK interest rate – which heavily influences mortgage rates offered by lenders – at 3.75 per cent but hinted they could lift this in future due to inflationary pressures.

Banks have therefore significantly increased the mortgage rates they offer and pulled a number of products from the market.

Households are set to face greater financial pressure following the conflict in Iran (Alamy/PA)

The FSR said average rates for two-year fixed-rate mortgages have increased by around 0.8 percentage points, while five-year fixed-rate mortgages have seen a roughly 0.7 percentage point rise.

Current rates indicate that about 5.2 million UK mortgage holders could face an increase in their repayments by the final quarter of 2028.

Advertisement

This compares with a prediction of 3.9 million from the Bank’s previous report before the start of the conflict in the Middle East.

Typical increases in mortgage payments would “remain modest” compared to many rises seen in recent years, it added.

The Bank also reported that the total number of mortgage products available in the UK had fallen from 8,500 to 7,000.

This is nevertheless still higher than following the initial Covid-19 period and during the gilt market stress amid the 2022 mini-budget by Liz Truss’s government.

Before having a daughter, I admit I was completely oblivious to this problem (Picture: Neil G)

My daughter was on the bus home when a boy at her school began making rude gestures towards her.

Elodie told me he was egged on by his friends, who were all laughing about it. I was horrified when I heard about this – and that was just the start.

She was just 12 when she first experienced public sexual harassment.

Now aged 16, Elodie has told me something like this happens regularly, around once a month, and she worries about being harassed and humiliated almost every time she goes out.

But my main concern is still raising awareness. Without this, harassment will still happen and the impact on the victim will still be felt.

I hope new laws like this can put these issues forefront in the minds of the public.

Advertisement

Before having a daughter, I admit I was completely oblivious to this problem.

Yes, I’d always felt some of the things I heard men say to girls and women were unacceptable. But what I see now really scares me – the nastiness and abusive comments are not ‘banter’, they’re controlling and hurtful. There is a real intention to cause harm behind these words.

This Is Not Right

On November 25, 2024 Metro launched This Is Not Right, a campaign to address the relentless epidemic of violence against women.

With the help of our partners at Women’s Aid, This Is Not Right aims to shine a light on the sheer scale of this national emergency.

Advertisement

You can find more articles here, and if you want to share your story with us, you can send us an email at vaw@metro.co.uk.

Read more:

Advertisement

So many men I speak to when discussing Elodie’s experiences, like friends and family members, are shocked when I tell them what is ‘acceptable’ within the law, like making sexually explicit comments or sexually propositioning someone in public.

They think about their wives and daughters, and cannot believe so much harmful behaviour is legal, particularly when these same behaviours are specifically banned in the workplace through the Equality Act.

And what is more devastating is that Elodie is not alone. Research from Plan International UK found 75% of girls, some as young as 12, in the UK have experienced some form of public sexual harassment.

For some girls, this is a daily occurrence that affects their walk to school, where they exercise and where they spend time with their friends. Some have even avoided school altogether.

Advertisement

Despite my fears, I try my best to reassure my daughter (Picture: Neil G)

I worry about Elodie experiencing public sexual harassment all the time: my fear is she’s at risk of assault, or even abduction, when walking alone. She shares my concern that a comment could quickly escalate.

When Elodie is planning to go out, I have a real mental battle with myself. Should I raise the subject of staying safe and put this issue on the table, or leave it and hope nothing happens?

Elodie is a very level-headed young woman and I trust she is aware of the risks, so I don’t want to limit her life experiences by raising my own fears. But, of course, that doesn’t mean that I don’t sit and watch both the clock and the phone when she is away from home.

My anxiety increases later in the day – evenings are particularly bad because I fear she could be assaulted after dark, and winter is worse again as everyone is bundled up and less aware of what’s going on around them.

I also really worry when she’s on public transport. Anyone could sit next to her and touch her inappropriately or prevent her getting off at her stop, and my wife and I wouldn’t know until it’s too late. That fills me with dread and it’s so easy to see it happening.

Advertisement

We often pick Elodie up when she’s been out and always check she doesn’t walk home on her own. We’ve also all agreed to use an app on her phone so we can check where she is.

But it’s a tough balancing act – she’s a young woman and we want to give her freedom. We don’t want her to feel she’s being watched all the time by her parents, and we also don’t want to worry ourselves silly as that isn’t healthy for us or Elodie.

Despite my fears, I try my best to reassure my daughter. Until today, there was no single piece of legislation to protect girls and women from public sexual harassment.

New strong and effective legislation would send a clear signal that public sexual harassment is not OK (Picture: Neil G)

It was a law that my Elodie had a part in, and I’m so proud of my daughter and the fact she has been involved in something that will make such an important difference to girls across the country. She feels empowered by how her hard work and commitment to this issue is starting to pay off.

. We need to do everything we can to help create a society where this kind of behaviour is seen by everyone for what it is: harmful and unacceptable.

Advertisement

As parents, we have a crucial role to play in educating both boys and girls that this kind of behaviour, far from being harmless or even a way of complimenting a girl, is always wrong.

Men also need to model good behaviour for their sons and grandsons, as well as calling out friends or colleagues if they see them sexually harassing someone.

This has really changed how I behave when I’m out too: I’ll often try to walk in front of a woman so she can see me, instead of hearing me behind her and potentially worrying about who is there.

No-one should feel uncomfortable going about their daily life and the long-term psychological impact on girls is severe, let alone any physical threats they may also face. All I want is for Elodie – and all girls in the UK – to feel safe. I don’t think that’s too much to ask.

Advertisement

A version of this piece was published in April 2023

Many years ago, it began. I noticed tiny, flesh-coloured bumps on my fingers ― they itched so badly I was tempted to bite my hand (no, really), an urge which only subsided when the little blisters finally burst and flaked.

Then, a month later, the process started again. It’s happened about once every six weeks since.

If that sounds familiar, you might be struggling with a condition called dishydrotic eczema, or pompholyx.

The writer’s finger with bumps on it, left: with cracked skin at a later stage, right

They’re very small, extremely itchy, and might leak fluid for the first couple of weeks (oh, good).

After the blisters burst, people with the condition are usually left with dry, scaly, potentially broken skin. This is when the risk of infection is at its highest, as the skin barrier has been broken down.

The whole process usually takes about two to three weeks, the NHS says.

Advertisement

According to the National Eczema Society, “This condition can occur at any age but is usually seen in adults under 40, and is more common in women.”

We don’t know exactly what causes it, but some people think it could flare up during times of stress, due to excess heat and sweating, and/or sensitivity to metals like nickel, cobalt or chromate.

Half of people with the condition either have atopic eczema or a family history of it too.

You should see your doctor if you think you have pompholyx, partly because symptoms like it can be caused by conditions like hand, foot, and mouth disease.

Advertisement

That’s one of the reasons why the NHS says you shouldn’t try to diagnose yourself with the condition.

It might seem odd to mix three fruits for this, but it’s an incredible combination. The apples give the fruit a bit more structure and the raspberries create wonderful juice, which mixes with the rhubarb and apple juice.

As it’s only a small amount, I used fresh raspberries for it. Some of them have an astonishing flavour of violets. Mix a couple of tablespoons of marmalade into whipped cream to serve on the side, if you want to echo the marmalade in the sponge.

The ‘harrowing’ true crime documentary features exclusive CCTV and bodycam footage of real murder cases

Aaliyah Rugg Senior reporter

12:20, 01 Apr 2026

A harrowing true crime documentary with a twist is currently available to stream online at no cost, with a fresh series due for release shortly.

Killers: Caught on Camera first premiered in 2023 on the True Crime channel, running for three seasons. Following its debut, the documentary was hailed as essential viewing for true crime enthusiasts.

Advertisement

This distinctive series presents exclusive footage alongside comprehensive psychological evaluation of video and audio evidence by expert Dr Julia Shaw, which ultimately secured killers’ convictions.

Each episode examines a different case, with Killers Caught on Camera investigating disturbing murders throughout the UK and US, incorporating devastating first-hand testimonies as well as previously unseen CCTV and home surveillance combined with police bodycam recordings.

Scrutinising the suspects and their motivations, this true crime programme is ideal for genre devotees to binge-watch, though a cautionary note has been issued to potential viewers. Before watching, it’s important to be aware that the programme contains “strong language, real crime footage and graphic discussions of crimes”, reports the Mirror.

All episodes are also available to stream online via ITVX. An ITV synopsis for the first harrowing episode states: “In the UK, the dismembered body of a woman leaves a couple, obsessed by serial killers, in the frame. In the US, a hidden camera provides vital evidence to help bring justice to a family.”

The disturbing documentary has garnered a devoted following amongst true crime enthusiasts, with one viewer commenting on IMDB: “Although the scenes being shown in each episode are disturbing and graphic I am always left feeling so sad that the victims lives ended so horrifically.”

Another remarked: “A perfect true crime production for the nerdy true crime documentary viewer, so I give it a 10 of gratitude to the people that’s lost their loved ones, and in the memory to those almost 30 victims connected to this series.”

Advertisement

A third viewer noted: “Love the show, for obvious reasons its true crime stories are new well put together.” On X, one fan wrote: “@drjuliashaw excellent job on #KillersCaughtOncamera I’m learning so much from you!”

Another commented: “The Grace Millane case is insane! How do you meet someone, and they kill you on that very same day. The world we live in.”

A fourth series is scheduled to launch on the True Crime channel later this month, debuting at 10pm on 21 April. New episodes will air weekly on Tuesdays through to 23 June.

Advertisement

The series has been described as follows: “Killers: Caught on Camera is an access-driven series revealing exclusive footage and psychological analysis behind killers’ convictions in the US and UK. Combining unseen CCTV, police bodycam and mobile phone footage with expert insights, it explores how everyday interactions escalate into lethal violence.

“The series highlights high-profile cases and never-before-seen footage, uncovering stories of intimate partner violence, stalking, and familicide.

“Friends and family share memories, investigators explain how digital forensics connect cameras, data, and social media to build critical evidence. Featuring Dr. Julia Shaw, it reveals the science behind solving murder… We are all witnesses in a monitored world.”

New Zealand all-rounder Amelia Kerr hit a stunning 179 not out off 139 balls to inspire her side to chase down 346 against South Africa in the highest successful run chase in women’s one-day international history.

Laura Wolvaardt’s 69 from 74 balls, a 91 from 90 balls by Anneke Bosch and Chloe Tryon’s 25-ball 52 helped South Africa post 346-6 in the second ODI of their series against the Kiwis.

Kerr came in at 21-1 in New Zealand’s reply and struck 23 fours and one six at a strike rate of 128.78 during her match-winning knock.

She was helped by Izzy Gaze, who made 68 from 48 balls, as the Kiwis made 350-8 in reaching their target with two balls to spare and levelling the series.

Advertisement

The previous highest successful chase in women’s ODI cricket was when India made 341-5 in reaching a 338 target set by Australia in their World Cup semi-final last October.

Kerr is no stranger to producing heroics, especially against South Africa, as she inspired New Zealand to victory against them in a T20 World Cup final in 2024.

She was also the ICC’s women’s cricketer of the year in 2024.

Kerr also holds the record for the highest individual innings in a women’s ODI, having hit an unbeaten 232 against Ireland when aged 17 in 2018.

You must be logged in to post a comment Login