Crypto World

Bitcoin at $62,500 and Waiting: Could Trump Iran Peace Deal Trigger a Major Rally?

Bitcoin is trading at $62,500, up by 4% from last week’s dip below $60,000 but still sitting nearly 40% below its all-time high. The BTC price recovery has been tentative, held back by a Fear & Greed Index reading in extreme fear territory. Now, Trump spoke about the Iran peace deal that could catapult the market.

U.S. President Donald Trump told reporters after attending the NBA Finals in New York on Tuesday that a deal to end the war with Iran could be reached in “two or three days,” and that the Strait of Hormuz would reopen “immediately” afterward.

For a Bitcoin market starved of macro catalysts, this geopolitical trigger could finally unlock the relief rally. But it’s not the first time Trump has teased the market with a peace deal; this has happened 37 times, per CNN.

Discover: The Best Crypto to Diversify Your Portfolio

Hormuz Reopening Could Move Bitcoin Price

The Strait of Hormuz carries 17–20 million barrels of crude per day, or 20% of global oil consumption, making it the single most critical energy chokepoint on the planet. A credible deal that reopens it immediately hits oil prices.

Lower oil feeds directly into inflation expectations. Cooler inflation expectations shift the Federal Reserve’s rate path calculus, softening real yields. A softer real yield environment weakens the U.S. dollar and loosens the liquidity conditions that have been strangling high-beta assets since mid-2025.

Bitcoin, sitting at the top of the risk spectrum, captures that rotation first and fastest. When Trump declared Netanyahu would have “no choice” but to accept a U.S.-brokered Iran agreement earlier this month, Bitcoin surged 5% to $64,000 in a single session, with Bitcoin ETF inflows reportedly topping $999 million across two days and cumulative spot ETF AUM hitting a 2026 record of $109 billion.

The counter-argument is valid. A headline-driven BTC moves mean-revert fast when structural confirmation doesn’t follow. Trump has previously predicted the Iran conflict would last four to six weeks, and it has now crossed 100 days.

The ceasefire frayed again over the weekend as Iran fired missiles toward northern Israel and Israel responded with what it described as a “large-scale strike on strategic defense systems.” Netanyahu said Tuesday the war “has not yet ended.”

Skepticism is warranted. But with volatility compressed to 30-day readings of just 8% and the Fear & Greed Index at its lowest print in months, even a partial credibility premium attached to a formal deal announcement could produce violent short-covering.

Discover: The Best Token Presales

Bitcoin and Iran Peace Deal: $75K Breakout or $59K Retest?

Bitcoin is currently wedged between immediate support at $62,000 and the next downside level at $61,500. On the upside, resistance clusters at $64,000 and $65,000. RSI is running at approximately 42, with the signal line sitting near 48, a 6-point gap between the two as sellers still have marginal control. Subdued volatility plus extreme fear is a classic setup for explosive moves in either direction when a macro trigger lands.

Discover: The Best Crypto to Diversify Your Portfolio

The post Bitcoin at $62,500 and Waiting: Could Trump Iran Peace Deal Trigger a Major Rally? appeared first on Cryptonews.

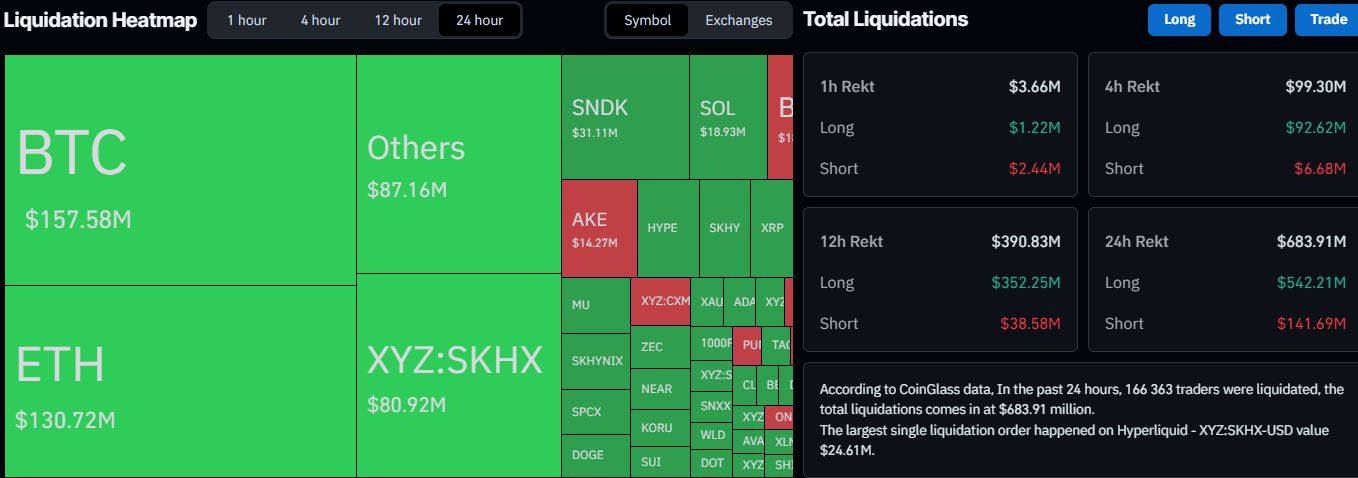

Bitcoin’s Monday rally that drove it to $65,600 on a couple of occasions has come to a screeching halt, as the asset has not only erased all gains but plummeted even more to a ten-day low.

Most altcoins have followed suit, which has skyrocketed the daily liquidations to approximately $700 million.

The chart above paints a clear and painful picture. BTC had maintained $64,000 over the weekend before it jumped to a multi-day peak of $65,600 on Monday. It tried to take down that resistance twice, but it was stopped each time.

The second rejection was quite violent as it drove the asset south by nearly $3,000 in hours. Thus, BTC plummeted to $63,000 for the first time since July 17.

Popular analyst CRYPTOWZRD weighed in on the latest move south, indicating that the largest digital asset had closed bearish. They believe it’s essential for BTC to remain above the currently tested support at $63,000; otherwise, it could slump to new local lows.

ETH was yesterday’s top gainer, surging to a two-month peak of $1,980. However, it has lost $100 since then and now sits well below $1,900. XRP has dumped by 4.5% to $1.06, thus slipping below the coveted $1.10 support. SOL is down by a similar percentage, while HYPE has plummeted by 6%.

Expectedly, this big market move has harmed over-leveraged traders, as more than 165,000 such participants have been wrecked in the past 24 hours. The total value of liquidated positions has risen to almost $700 million on a daily scale. Naturally, BTC and ETH lead the pack.

This morning’s market crash comes just a day before the US Federal Reserve is scheduled to announce its interest rate decision, and the uncertainty around a potential hike has harmed risk-on assets like crypto.

The post $700 Million in Liquidations as BTC, ETH, XRP Plunge Ahead of FOMC appeared first on CryptoPotato.

Cardano co-founder Charles Hoskinson has warned Bitcoin could lose its dominance if its governance system and community fail to coordinate a response to the quantum computing threat.

Bitcoin developers are already working on post-quantum solutions, including BIP 361, which proposes moving away from ECDSA and Schnorr signatures after a post-quantum system is selected.

Quantum Threat Could End Bitcoin Dominance

Hoskinson’s warning came during an interview with The Starting Block. The Cardano co-founder described Bitcoin as being “stuck in time” because any changes to the network require consensus across stakeholders including users, miners, node operators, and developers. According to Hoskinson, frustration with Bitcoin’s rigidity and inflexibility was one of the reasons behind the creation of Ethereum. Hoskinson was one of the original co-founders of Ethereum along with Vitalik Buterin. He stated during the interview, “The issue with Bitcoin is it’s frozen in time. It’s very difficult to change anything.”

Bitcoin uses elliptic-curve cryptography to prove the ownership of funds. Quantum computers, in theory, could decipher private keys from the public keys and authorize transactions without the owner’s knowledge or approval. Hoskinson believes the quantum threat could pose a major risk to the flagship cryptocurrency and its $1.3 trillion market capitalization, eventually stripping it of its dominance unless its governance mechanism adapts without impacting the qualities that give it value. “What made Bitcoin so strong is it survived external threats … including the loss of its founder. Quantum computers are yet another threat … if Bitcoin’s governance is such that it’s impossible actually to make meaningful progress, or they compromise the core reason to use Bitcoin, I don’t think Bitcoin’s going to stay the number one cryptocurrency.”

Cardano Better Equipped for Technical Threats

Hoskinson argued that Cardano’s formal on-chain governance and ability to approve upgrades make it better at responding to threats like the one confronting Bitcoin.

“Cardano is, in many ways, a spiritual successor [to Bitcoin]. It reflects correcting a lot of things that I think that Satoshi couldn’t get around to because of expertise or time but was directionally moving there.”

Cardano moved to full community governance after the Plomin hard fork in January 2025. ADA token holders can vote or delegate their vote to representatives called DReps. A constitutional committee and stake pool operators also participate in key decisions. This system helps Cardano approve hard forks and treasury decisions on-chain. Hoskinson argued that Cardano could use the system to vote on migrating away from quantum-vulnerable infrastructure.

Hoskinson added that Cardano is preparing for its largest upgrade, which would make the network “60-times faster.”

Not a Perfect System

However, Cardano has yet to undertake or complete such a migration because its governance system must evaluate technical designs, approve funding, and organize users, developers, and service providers. Cardano’s governance system has also witnessed several disputes. Cardano delegates recently rejected and challenged several proposals linked to Hoskinson and Input Output, including a proposal to research Leios scaling and quantum-resistant cryptography.

Bitcoin Developers Exploring Post-Quantum Options

Bitcoin’s governance allows developers to propose code. However, users and node operators decide on its implementation. Miners, exchanges, and wallet providers also influence decision-making. While this helps avoid frequent changes, it makes urgent coordination difficult. The community is tracking BIP-361, a proposal that phases out legacy ECDSA and Schnorr signatures to protect the network against the quantum threat. Several other proposals are also under consideration, including ones advocating new address formats, hybrid signatures, and recovery paths.

However, any measure will require wallets, exchanges, custodians, and dormant holders to migrate their funds without splitting the network or creating conflicting ownership rules.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

Coinbase chief executive Brian Armstrong has argued that artificial intelligence will increase demand for crypto rather than replace it.

Summary

- Armstrong says AI agents will increase crypto demand by using programmable money for autonomous transactions.

- Chainalysis counted over 100 million x402 payments on Base, though meme-coin farming drove early growth.

- Coinbase combines Base, USDC, x402 and agent wallets to build its agentic finance payment stack.

In a July 27 post on X, he described Base, USDC and the x402 payment standard as the core of Coinbase’s “Agentic Finance,” or AiFi, strategy.

Armstrong wrote that “AI being a megatrend takes nothing away from crypto” and said AI agents would eventually complete more daily transactions than all people combined. The forecast has no set timeline. Current data shows growing x402 activity, but it does not prove that autonomous agents already exceed human payment use.

Armstrong links AI growth to programmable money

Armstrong rejected calls for crypto companies to pivot away from blockchain and focus only on AI. He said AI agents need programmable money because traditional bank accounts, cards and checkout pages depend on human identity checks and manual approval.

Under Coinbase’s model, software can hold a wallet, pay for an API request and receive a digital service without opening an account with each provider. Agents could buy data, computing power, research, media generation or storage through small payments that settle onchain.

The structure may raise transaction counts because one agent can make many low-value payments during a single task. However, transaction frequency does not show the total economic value of the activity. Armstrong’s claim therefore remains a company thesis rather than a measured outcome.

Base and x402 form Coinbase’s AiFi payment stack

Coinbase introduced Base in February 2023 as a low-cost Ethereum layer-2 network for onchain applications. The company did not build Base only for AI, but its lower fees and faster settlement later made it a main network for x402 payments.

Coinbase launched x402 in May 2025. The open protocol uses the HTTP 402 “Payment Required” status code to let websites and APIs request stablecoin payments. A client receives payment instructions, signs a blockchain transaction and gains access after the payment is checked.

USDC serves as a common settlement asset because its price tracks the U.S. dollar. Coinbase also offers Agentic Wallets, which let developers set spending and trading rules for AI systems. The wallets can pay for data and computing through x402 while operating without manual approval for each transaction.

As crypto.news previously reported, Coinbase also launched Coinbase for Agents, giving software access to trading, portfolio management and x402 payments under user-defined limits. The company later added x402 support for businesses that want to receive USDC directly from software agents.

Chainalysis counts more than 100 million Base payments

Chainalysis reported on June 3 that x402-linked payments on Base crossed 100 million transactions after about nine months of activity. The analytics company identified flows connected to the protocol and studied the wallets involved.

The report found that payments worth at least $1 made up 95% of the value transferred. It also said agentic payment wallets tended to be newer, held smaller balances and owned 550% more asset types than typical Base users.

Still, Chainalysis said meme-coin farming drove much of the early transaction growth. That detail limits claims that all 100 million payments came from independent AI agents buying useful services. Automated scripts, incentive campaigns and other software activity can also create x402 transfers.

As crypto.news reported in June, x402 had already passed 100 million Base transactions while Armstrong and other industry leaders promoted crypto as a payment layer for AI. Earlier crypto.news coverage also found that x402 activity reached 75.41 million transactions over one 30-day period, with Base and USDC leading usage.

Coinbase expands agent tools before quarterly results

Coinbase has continued adding products around the same strategy. Agentic.market allows software agents to find and purchase services using USDC. Developers can also use Coinbase tools to build wallets, set transaction policies and charge for API calls through x402.

Outside Coinbase, companies have begun testing the protocol for travel, cloud services and online content. Travala launched an AI hotel-booking system that lets agents search more than 2.2 million properties and pay with USDC on Base.

The market remains early. Coinbase’s products show that machines can initiate blockchain payments, but adoption figures depend on how analysts classify agent activity. Security, spending controls, identity rules and service quality will also shape wider use at present.

Coinbase will publish its second-quarter 2026 results on July 30 after U.S. markets close. The report may give investors more detail on stablecoin revenue, Base activity and developer products, although the company has not said it will disclose AiFi revenue separately.

Pseudonymous trader CrediBULL Crypto is calling for Ethereum (ETH) to reach $20,000 or higher, repeating a target he first laid out three weeks ago when the token was trading near $1,500.

According to him, Ethereum is finishing a multi-year base against Bitcoin (BTC) and is about to enter its first bull run since 2017.

The Charts Behind the $20K Call

Responding to a claim by alphatracker that ETH would go to $10K+, CrediBULL simply posted “$20K+,” and shared a link to a video where, instead of presenting the target as speculation, he built his case around long-term chart structures on both the ETH/USD and ETH/BTC pairs.

“I’ve always said $10K is the absolute minimum. I think $20K is realistic..,” the analyst said in the video. “I’m not going to say it’s a given… but $20K is super, super reasonable.”

He noted that Ethereum has spent years underperforming Bitcoin, leaving market sentiment at levels similar to previous cycle lows. But he argued that the ETH/BTC chart has finally reached what he considers to be a long-term accumulation zone after about four years of decline, and from there, he expects the world’s second-largest cryptocurrency to build a base before beginning what he described as the next impulsive move higher.

His next thesis tracked the ETH/USD chart itself, with the trader saying that Ethereum has completed the first leg of a larger five-wave structure and is now holding above an invalidation level near $1,385.

According to him, if that support stays intact, then the next advance could push ETH to around $10,000 before a later wave carries it above $20,000. He also argued that historical ETH/BTC ratios point to similar price levels if Bitcoin returns to its previous highs or continues into another expansion phase.

Furthermore, Credibull drew a comparison to April last year, when Ethereum sat near the same price it’s at right now and was widely written off as finished, only to break its all-time high a few months later. He said that the setup looks similar today, with the price holding above its last low rather than breaking it, something he treats as a sign that the broader uptrend is still intact.

Similar sentiments were shared by trader Saiyan, who set a base case of $10,000 for the cycle, prompting a pushback from Cheds Trading, who simply wrote, “That’s not happening.” But another market watcher, Sykodelik, sided with the bulls, arguing that a move above $10,000 should not be treated as unrealistic, given that it was just 2 times the Ethereum all-time high.

Where ETH Stands Now

ETH was trading above $1,900 at the time of writing, having gained nearly 4% in 24 hours and about 24% over the past month, according to CoinGecko data.

The token is still 60% below its ATH, and other analysts have flagged similar bottoming signals in recent weeks. For example, NoName pointed to a pattern of four lower highs as evidence that the bear market has already found a floor, while chartist Ali Martinez noted a bullish crossover in the asset’s MVRV ratio.

Funding rates on Binance have also climbed to their highest level in six months, something analysts at CryptoQuant say shows that sentiment has started to turn even though the price is still well below where it was around the same time last year.

The post Ethereum Could Hit $20K as Multi-Year BTC Base Completes: Analyst appeared first on CryptoPotato.

Bitcoin moved higher at the start of the week’s first Wall Street session, testing fresh local highs as broader markets opened in positive territory. The latest push came alongside reports of a pause in US–Iran tensions and renewed efforts connected to the Strait of Hormuz—an outcome that traders viewed as a near-term reduction in geopolitical risk.

According to TradingView data cited in market coverage, BTC/USD spiked toward the $66,000 area as risk assets gained traction. At the time of writing, US equity benchmarks such as the S&P 500 and Nasdaq Composite were up by roughly 0.3%, while WTI crude oil dipped before a modest rebound, reflecting a less volatile energy backdrop than earlier in the month.

Key takeaways

- Bitcoin pushed toward new local highs near $66,000 after a reported easing in US–Iran strike activity.

- Iranian and Omani discussions tied to maritime traffic via the Strait of Hormuz supported sentiment, with oil moving less sharply.

- BTC held two key short-to-medium-term trend levels on the daily chart: the 21-day and 50-day SMAs near $64.3k and $63.3k.

- Despite the bounce, market commentary emphasized the price base as “fragile,” with traders watching for follow-through toward $66k–$67k.

- Crypto short liquidations increased as price rose, with CoinGlass data showing the figure nearing $250 million over 24 hours.

Geopolitics and risk assets lift BTC at the open

The immediate catalyst for Bitcoin’s uptick was macro-linked sentiment tied to the Middle East. TradingView data showed BTC/USD jumping toward $66,000 as traders responded to reports that there had been a pause in strikes between the US and Iran.

Additional reporting referenced statements by an Iranian foreign ministry spokesman indicating that Tehran and Oman were “trying to establish mechanisms regarding maritime traffic” through the Strait of Hormuz, a chokepoint for global oil flows that had been closed. While headlines about reopenings and “mechanisms” can remain fluid, the market impact was clear: energy risk eased at the margin, and that helped equities—and Bitcoin—start the session with momentum.

WTI crude oil, often treated as a proxy for near-term geopolitical stress, fell toward about $82 per barrel before recovering modestly. The combination of a steadier oil tape and higher equity futures aligns with a classic “risk-on” relationship that can temporarily benefit liquidity in major crypto markets.

Macro headwinds remain, but crypto’s July performance stands out

Even with the immediate tailwind, traders were careful not to overstate the durability of the move. One potential constraint mentioned in the coverage was the risk of higher US bond yields, which can weigh on assets with lower real-yield support.

QCP Capital argued that—despite a more challenging macro backdrop—digital assets had generally outperformed equities during July. In its “Market Color” analysis, the firm said BTC and ETH were up about 11.6% and 24.6% month-to-date, respectively, noting that higher Treasury yields and periodic risk-off episodes had pressured broader markets.

Importantly for investors focused on regulation, QCP also flagged attention around the proposed CLARITY Act. The analysis described ongoing interest from digital asset participants because the bill could affect the US regulatory framework for the sector. The CLARITY Act was referenced as being under consideration, with market participants watching for any progress that could shift expectations around how digital asset rules might evolve.

Support levels hold—yet traders want proof beyond the bounce

On the chart, the rally’s quality mattered as much as the direction. Crypto trader and analyst Michaël van de Poppe highlighted that BTC was holding the 21-day and 50-day simple moving averages (SMAs). The levels cited were approximately $64,289 for the 21-day SMA and $63,261 for the 50-day SMA—areas that often function as magnets for both discretionary traders and systematic strategies.

Van de Poppe characterized the holding as a “strong signal” for long-biased positioning, but added that the structure was still “a little fragile.” In a posted view on X, he indicated he would prefer to see a decisive advance into the $66,000–$67,000 band within the next 1–3 days, which would indicate more persistent demand rather than a single-session push.

That distinction is crucial. A market can rise quickly toward resistance levels and still fail if buyers don’t expand after the initial liquidity draw. For traders, the next test is not just whether BTC reaches the higher range, but whether it can keep the bid long enough to convert a “spike” into a sustained move.

Liquidations rise as shorts get squeezed

Alongside price strength, liquidation data suggested that the move was accompanied by short-covering. CoinGlass data referenced in the coverage showed crypto short liquidations increasing as BTC rallied, with the metric nearing $250 million over a 24-hour period.

Liquidation spikes can be interpreted in two ways: they may signal aggressive leverage being forced out, or they may reflect a crowded short position that becomes vulnerable when the market turns upward. Either way, when large liquidation prints occur near key technical levels, they often coincide with bursts of volatility—meaning traders may see both acceleration and faster reversals if price fails to hold.

What to watch next

With BTC holding important moving averages while testing the upper end of the near-term range, the market now appears to be waiting for confirmation. Traders are watching whether Bitcoin can sustain interest into the $66,000–$67,000 zone, while broader risk sentiment could hinge on continued developments around US–Iran tensions and any tangible progress related to Strait of Hormuz maritime arrangements.

The Hong Kong Monetary Authority (HKMA) has introduced a new assessment framework aimed at helping banks prepare for the potential impact of quantum computing on the cryptography underpinning distributed ledger and digital finance systems. The move signals that Hong Kong’s rapid push toward tokenization and blockchain settlement is now paired with a formal push to address “post-quantum” security risks.

In a white paper released Monday, the HKMA unveiled the sector’s first Quantum Preparedness Index (QPI). The HKMA assigned an overall readiness score of 2.3 out of 10 across surveyed institutions and said roughly half of them had no formal post-quantum planning in place. The regulator’s goal is to raise the sector to a QPI score of 10 by 2030.

Key takeaways

- The HKMA’s first Quantum Preparedness Index scores the banking sector at 2.3/10, indicating limited readiness for post-quantum upgrades.

- According to the HKMA, around half of surveyed institutions lack formal post-quantum planning.

- Hong Kong’s tokenization and distributed ledger initiatives heighten the urgency of cryptographic migration planning.

- The regulator warns that sufficiently powerful quantum computers could eventually break RSA and elliptic-curve cryptography used in financial systems.

- The HKMA is targeting full sector preparedness by 2030 and is urging earlier inventories and risk assessments.

Why HKMA is turning to quantum preparedness now

The HKMA’s quantum framework arrives as the city expands how it uses tokenization in mainstream finance. Hong Kong has already issued three batches of tokenized green bonds totaling about HK$16.8 billion (around $2.1 billion) since 2023, according to government disclosures published on the government information site and related bond issuance updates since that period.

At the policy level, the HKMA is also advancing tokenized deposits and digital-asset settlement. It has been working on these capabilities under Project Ensemble, an initiative that Cointelegraph previously covered in the context of tokenization efforts and wholesale CBDC-related infrastructure.

Within this broader push, the HKMA’s central argument is that distributed ledger applications and payment networks rely on cryptography for core functions—and that a successful cryptographic compromise would create systemic vulnerabilities. The white paper states that if those protections were undermined, it could lead to severe disruption across the systems that depend on them.

The QPI score and what the assessment found

The white paper and the accompanying index formalize how the HKMA expects banks to think about readiness. With an overall QPI score of 2.3/10, the HKMA essentially portrays the sector as being in an early stage—before deep technical migrations and long-running system updates.

Two findings stand out from the HKMA’s release. First, it reports that around half of the surveyed institutions had no formal post-quantum planning in place. Second, it describes examples of early technical work: the HKMA says one institution completed a proof of concept applying post-quantum cryptography to distributed-ledger connectivity.

The HKMA also points to real-world experience in the industry, noting HSBC’s 2024 use of quantum-safe technology to move tokenized gold across distributed ledgers. This detail is included in the HKMA’s white paper as an example of post-quantum considerations being explored in connection with tokenized asset settlement.

Quantum risk: what could be broken, and why timelines matter

In the HKMA’s framing, the major threat comes from the possibility that quantum computers could run Shor’s algorithm at scale. In its view, that capability could eventually undermine widely used public-key systems such as RSA and elliptic-curve cryptography.

If that were to happen, the HKMA warns it could enable attackers to decrypt protected data or forge digital signatures—mechanisms used to authorize transactions, verify identities, and establish trust within financial systems.

The regulator emphasizes practical urgency rather than alarm. According to the white paper, replacing cryptographic systems embedded across infrastructure can take years. For that reason, it urged banks to begin with foundational work now—such as inventories of cryptographic assets, risk assessments, and migration planning—before machines with the required capability become available.

Hong Kong’s tokenization strategy raises the bar for security upgrades

The HKMA’s quantum effort aligns with its broader Fintech 2030 direction, announced as a strategy in 2025 that made tokenization a key pillar. Cointelegraph previously reported that tokenization was one of four strategic pillars within an overall plan of more than 40 initiatives in coverage of HKMA’s Fintech 2030 strategy.

The HKMA has signaled that its tokenization agenda includes acceleration of real-world asset (RWA) tokenization, regularization around tokenized government bond issuance, and exploration of tokenized Exchange Fund papers. It has also described blockchain settlement work supported by e-HKD, tokenized deposits, and regulated stablecoins.

Meanwhile, the business momentum behind digital assets and tokenized deposits appears to be building. In a speech, Hong Kong Financial Secretary Paul Chan said banks in the city held more than HK$14 billion (about $1.785 billion) in digital assets under custody at the end of 2025, up about 180% year over year. He also cited tokenized deposits reaching HK$29 billion (about $3.7 billion).

That combination—growing tokenization activity alongside a regulator-led push for cryptographic resilience—helps explain why the HKMA is moving beyond generic cybersecurity guidance and instead introducing a measurable readiness score. For market participants, the QPI structure may translate into clearer expectations for governance and technical planning as they integrate DLT into more of their regulated operations.

Going forward, banks in Hong Kong will likely need to watch how the HKMA tracks QPI progress toward the 10/10 by 2030 target and whether additional guidance is released on timelines, assessment methods, and post-quantum migration priorities. With the assessment showing low current readiness, the next phase to monitor is how quickly institutions turn plans into concrete inventories, testing, and system upgrades across ledger connectivity and transaction authorization layers.

Cointelegraph is committed to providing independent, high-quality journalism across the crypto, blockchain, AI, and fintech industries.

All news, reviews, and analyses are produced with full journalistic independence and integrity. For more details on our standards and processes, please read our Editorial Policy.

Zcash is expected to activate its NU6.3 “Ironwood” network upgrade at block height 3,428,143 on July 28.

Summary

- Ironwood activates at block 3,428,143, replacing Orchard with a separately tracked shielded transaction pool system.

- The turnstile blocks more ZEC leaving Orchard than entered, strengthening public supply verification after migration.

- Quantum-recoverable notes support future recovery, but Ironwood does not make Zcash quantum-secure today by itself.

The Zcash Foundation’s Zebra 6.0.0 release places the estimated activation near 13:00 UTC and tells every node operator to upgrade before the fork.

The upgrade introduces a new shielded pool and a v6 transaction format. It follows the disclosure of a flaw in the older Orchard pool that could have allowed an attacker to create counterfeit ZEC without an obvious public record.

Developers patched the flaw through emergency upgrades in June. They said they found “no evidence” of exploitation, but Zcash’s privacy design prevents them from proving that hidden inflation never occurred.

Ironwood creates a separately tracked shielded pool

According to the Zebra 6.0.0 release notes, Ironwood reuses Orchard’s Action structure and Halo2 proof system. However, it adds a separate note commitment tree, nullifier set, chain value pool and chain-history data. These records let nodes track the new pool independently from Orchard after activation.

Zebra also updates several node commands so operators can inspect the pool’s value and commitment-tree state. The Zcash Foundation’s GitHub release labels the upgrade critical for operators because older software will not follow the correct chain after the activation height.

Turnstile limits value leaving Orchard

Ironwood’s main supply safeguard is a turnstile between Orchard and the new pool. After activation, Orchard will stop accepting new outputs and internal transactions. Funds can move out, but the accounting rule prevents more ZEC from leaving Orchard than the amount that legitimately entered it.

The Ironwood design explanation says the mechanism gives users a public check on circulating supply without exposing private balances or transaction details. Instead, it would leave any excess hidden value trapped inside Orchard once the pool becomes exit-only.

As crypto.news previously reported, Zcash scheduled the July 28 hard fork after developers concluded that the patched bug still left a supply question they could not answer with certainty. Zcash founder Zooko Wilcox said the flaw was “unlikely to have been exploited,” while also stating that users should not need to rely on that assessment.

Notes gain a future quantum-recovery path

Ironwood also changes how shielded notes are created so they may be recovered through a future post-quantum protocol. The official ZIP 2005 specification calls the feature quantum recoverability. It binds more note data into the note construction, allowing a later recovery system to verify ownership without relying only on cryptography that a powerful quantum computer could break.

The change does not make current Zcash transactions quantum-secure. The specification says a separate recovery protocol must still be designed and activated later. Funds that remain in Sprout, Sapling or Orchard would not gain this recovery option. Wallets must move them into Ironwood notes to receive the new protection.

The same specification says existing Orchard addresses can receive Ironwood notes, reducing changes for users. Wallet developers must still add migration support. Users whose wallets do not update may face delays when moving Orchard funds, while exchanges may briefly pause deposits or withdrawals around the fork.

Zebra becomes mandatory as zcashd support ends

The upgrade also completes Zcash’s move away from the older zcashd node software. The network set zcashd’s end-of-support halt at block 3,417,100, before Ironwood activation. The official deprecation schedule says zcashd will not support NU6.3, leaving Zebra as the required node implementation for the new rules.

Zebra 6.0.0 includes a separate mempool security fix. The issue allowed peers to send expensive-to-check, non-standard transactions that could reduce node responsiveness while the traffic continued. The fix rejects those inputs before the costly verification step. The Foundation said the flaw affected availability only and did not allow invalid blocks, lost funds or consensus failure.

Related crypto.news coverage detailed Zcash’s two-step response to the Orchard vulnerability. Developers first disabled Orchard activity, then activated the NU6.2 hard fork with corrected code before restoring the pool. Ironwood now adds a separate accounting boundary rather than another patch inside the same pool.

The upgrade remains tied to block production, so its exact clock time may shift. If the chain reaches block 3,428,143 as expected, Ironwood will activate on July 28 and begin the Orchard-to-Ironwood transition.

Charles Hoskinson says Cardano’s “best days are ahead,” even as its native token, ADA, trades 95% below its all-time high.

The Cardano founder made the remark during a recent X AMA. He was responding to ADA’s prolonged slump and the criticism that has followed it.

Why Cardano is Feeling the Pressure

ADA trades near $0.16 today. The token hit its all-time high of $3.09 in September 2021 and has fallen 53% so far this year alone.

Governance disputes, builder shutdowns, and Cardano’s canceled 2026 summit have deepened the pressure. Hoskinson has also faced mounting criticism from the community over the slide. He stepped back from social media at one point, then returned to address the backlash directly.

“I still do believe our best days are ahead of us, and I still do believe that we can succeed despite the demons we’ve let in. We just have to change the approach, and we just have to change the strategy.”

— Charles Hoskinson, on X

Hoskinson Has a Plan

The comment echoes Hoskinson’s recent push for a funding overhaul. He wants to clear a backlog of more than 600 million ADA in treasury requests. He argues that the network’s security and utility drive ADA’s price, not short-term speculation.

The bottleneck comes down to a hard cap. Cardano’s treasury allows only 350 million ADA in net funding changes at a time, well short of what builders are requesting. Hoskinson has proposed spreading development across more independent companies instead of leaning on Input Output Global, the firm he leads, to carry the load alone.

Whether a strategy shift can turn Cardano’s price trend around remains an open question. ADA still trades far below its 2021 peak, leaving Hoskinson’s optimism as the main counter to a bearish market narrative.

The post Cardano’s Hoskinson Says ‘Best Days Are Ahead’: ADA Price Down 95% From Top appeared first on BeInCrypto.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

The guide examines crypto and multi-asset proprietary trading firms, comparing funding, supported markets, and features to help traders choose the right platform.

Crypto traders, like any other retail traders, often want to grow the positions they take in the market, especially after they feel they have enough experience to handle the responsibilities. This desire would have been a pipe dream just a decade ago because retail traders cannot easily raise the kind of capital required to take meaningful positions in the market. But now, traders can actualize that desire, thanks to proprietary trading firms.

Estimates show that active prop firms number in above 2,000 as of this writing. Nearly 70% of these firms offer some kind of access to crypto as a tradable asset, and about 50 of them offer only crypto. This wide range of options is great, except that, in a way, it complicates the decision of picking the right firm. For instance, should someone go for a multi-asset firm or opt for one that is dedicated to crypto alone?

In that light, this article is an effort to simplify the decision. It explains the difference between multi-asset and crypto-focused prop firms, and then ranks the different kinds of firms. The goal is to give users sufficient information to know what option suits their crypto trading activities.

Prop firms can be multi-asset or crypto-only; how do they differ?

Once someone decides that a funded account is the route they want to take, the next fork in the road is choosing what kind of firm to sign up with. Here, users will have to choose between a multi-asset firm and a crypto-native, or crypto-only, one.

What are multi-asset firms?

These ones offer tradable assets from several markets. They are the most familiar kind of prop firms mainly because they came first.

A typical multi-asset prop firm offers CFDs and futures instruments, and it operates mostly as a broker. The assets such a firm offers include foreign exchange, or forex, commodities, metals, stocks, indices, and crypto. So, in this setup, crypto is simply bolted on as another instrument to select from a dropdown menu.

Methodology

All the firms in our selection had to satisfy at least one of the six criteria we developed for our research. That means the firm at the top ticked most of the boxes. The table below shows each criterion and its description:

- Payout speed and reliability — how long it takes to get paid once a user earned it, and how consistent that timeline is

- Drawdown consistency across plans — whether the same drawdown model applies to every evaluation path, or whether it switches between static and trailing depending on which plan a trader buys

- Rule transparency and consistency — whether the rules stay the same across plans, and whether restrictions are disclosed before payment

- Jurisdictional clarity — whether the firm discloses where it’s registered and where trading services are delivered

- Plan flexibility — whether the firm offers paths that fit different trader profiles without forcing everyone into one rule set

- Crypto-native payout rails — whether traders can withdraw in USDT or USDC at any account size, or are locked into slower bank transfers

Multi-asset firms

For those who prefer firms through which they can trade forex and other instruments in addition to crypto, then focus on this section. This research identified five firms in this category, which are as follows:

1. OneFunded

OneFunded leads on every criterion above more cleanly than any other firm on this list and was named Fastest Growing Prop Firm, Global, at UF Awards 2026. It processes crypto payouts in roughly an hour, applies a consistent rule framework across four evaluation paths, and pays out in USDT from the smallest account size.

The firm operates under Brynex Tech Limited, registered in the United Kingdom, with trading services delivered through a Saint Lucia-registered unit, OneFunded Capital Ltd. It has built its brand directly against the industry’s “failure factory” reputation, positioning transparency and rule consistency as its core differentiators rather than marketing claims layered on top of the same rules everyone else uses.

What does OneFunded offer?

- Payouts are processed within one hour of approval, the fastest turnaround among the multi-asset firms in this guide

- Four funding paths: Value, Core, Flash, and Instant Funding, each with its own risk profile and price point

- Entry from $29 on the Value plan

- Account sizes from $5,000 to $200,000

- 100% refundable evaluation fee on Value, Core, and Flash after a successful pass

- No time limit on any evaluation phase

- Low spreads and low commissions across supported instruments

- Overnight trading permitted, though swap or rollover fees may apply

- 200+ tradable instruments across forex, crypto, global indices, metals, and US/EU stocks

- 1:2 leverage on crypto

- Trading available via MT5, cTrader, and TradeLocker

- A scaling plan that can grow a funded account up to $1,000,000

Challenge types compared

| Parameter | Value | Core | Flash | Instant |

|---|---|---|---|---|

| Evaluation steps | 2-Step | 2-Step | 1-Step | No evaluation |

| Positioning | Lowest price, strict discipline | Most popular, classic rules | Fast funding | Immediate access |

| Min price | $29 | $35 | $56 | $79 |

| Account sizes | $5k–$100k | $5k–$200k | $5k–$200k | $5k–$25k |

| Profit target | 8% / 6% | 8% / 5% | 10% | None |

| Minimum trading days | 4 days | 3 days | 1 day | None |

| Daily loss limit | 4% | 5% | 4% | 3% |

| Overall loss limit | 8% | 10% | 6% | 6% |

| Consistency rule | Off | Off | 50% | 20% |

| Trading period | Unlimited | Unlimited | Unlimited | Unlimited |

| Crypto leverage | 1:2 | 1:2 | 1:2 | 1:2 |

| Profit split | Up to 90% | Up to 90% | Up to 90% | 80% |

| Refundable fee | Yes | Yes | Yes | No |

| Best for | Disciplined traders | Most traders | Confident, fast traders | Experienced traders |

How does it pay?

OneFunded pays up to a 90% profit split to the trader, with 10% retained by the firm. The first payout unlocks 14 days after opening the first position on a funded account, once the account holds at least $100 in profit, and processes within 1 hour. Recurring payouts follow every 14 days after that, and can be shortened to every 7 days with the Weekly Payout Add-on. Payouts go out via crypto (USDT, TRC20), bank transfer, or Rise, with the same $100 minimum payout threshold and 1-hour processing time across all three methods.

Where does it fall short?

OneFunded imposes a consistency rule of 50% on Flash and 20% on Instant programs.

Verdict

OneFunded best suits patient and disciplined multi-asset traders who value an unlimited evaluation period, clear drawdown parameters, and a choice of MT5, cTrader, or TradeLocker over high-leverage crypto exposure.

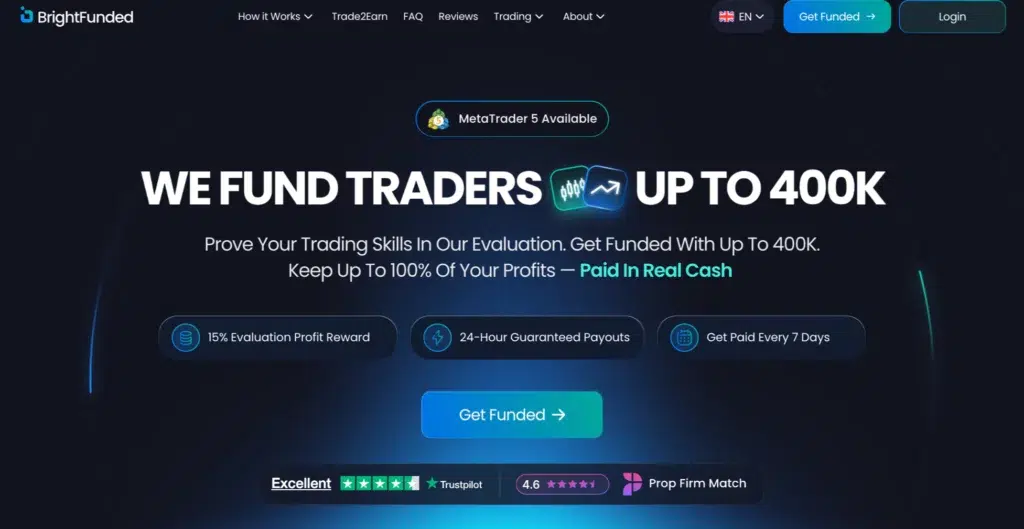

2. BrightFunded

BrightFunded is a Dubai-based prop firm operated by BrightFunded Co LLC and Bright Global FZCO, launched in 2023. It positions itself around simple rules, fast payouts, and a loyalty-driven scaling structure.

What does BrightFunded offer?

- Three evaluation tracks: 1-step, 2-step Bright, and 2-step Classic

- Account sizes from $5,000 to $200,000

- Over 48 crypto pairs, including BTC/USD, ETH/USD, XRP/USD, and SOL/USD

- 1:5 leverage on crypto

- A 15% profit reward paid during the evaluation phase

- Scaling Plan that can push profit split up to 100% and capital to $400,000

- No minimum reward threshold; even $0.01 profit qualifies for a payout request

- Evaluation fee refunded after first payout or first scaling milestone

Challenge types compared

| Parameter | Bright 2-Step | Dark 2-Step | 1-Step |

| Profit target P1 | 8% | 10% | 10% |

| Profit target P2 | 5% | 5% | – |

| Daily loss limit | 5% | 5% | 4% |

| Max overall loss | 10% static | 10% static | 6% static |

| Min trading days | 5 / 5 | 5 / 5 | 5 |

| Time limit | Unlimited | Unlimited | Unlimited |

| Drawdown type | Static (balance) | Static | Static |

| Crypto leverage | 1:5 | 1:5 | 1:5 |

| Account sizes | $5K–$200K | $5K–$200K | $5K–$200K |

| Starting fee | from €47 | from ~€55 | from ~€89 |

| Profit split | 80% → 100% via scaling | Same | Same |

| Payout cycle | Bi-weekly (weekly add-on) | Same | Same |

| 1st payout | 30 days after 1st funded trade | Same | Same |

| Trade2Earn | Yes | Yes | Yes |

How does it pay?

The default profit split is 80%, and the firm’s scaling program can raise this to as much as 100% for consistently profitable traders. Once they have something in their account, traders can request the first payout 30 days after the first trade, then bi-weekly (or weekly with an add-on). BrightFunded processes the payouts within 24 hours of approval, and the firm supports both cryptocurrency and bank transfer as withdrawal methods.

Where does it fall short?

BrightFunded only offers evaluation paths, which leaves out traders who may prefer instant funding.

Verdict

BrightFunded suits news-driven and event-based traders, since its offer of No Consistency Rules paired with only a brief 5-minute news trading restriction lets traders capitalize on high-volatility events.

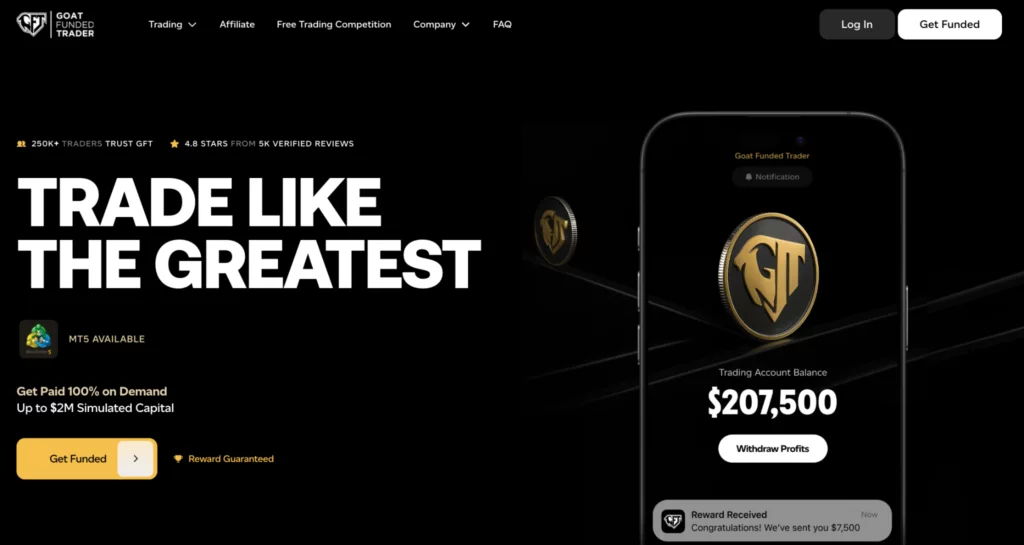

3. Goat Funded Trader

Goat Funded Trader (GFT) is a trade name of Hong Kong-registered Wishes Tower International Limited. The firm has built a large user base of over 250,000 traders on the promise of near-total profit splits and a heavily gamified, points-based loyalty structure.

What does GFT offer?

- Four challenge types: 1-Step (GOAT), 2-Step (GOAT and Standard), 3-Step (GOAT), and Instant (GOAT, Pro, and Premium).

- Account sizes range from $5000 up to $400,000, which can reach $2 million via the scaling plan.

- Lowest entry fee of $17, which is an offer on the $5k 2-step track (both GOAT and Standard).

- A promise to process payouts within 2 business days, and failure will see GFT pay an extra $1000.

- 1:2 on crypto

- More than 500 crypto assets; this depends on the trading platform to choose

- A $3,000 daily profit cap on step-based funded accounts, with excess profit deducted rather than triggering a breach.

- Trading via MetaTrader 5, MatchTrader, TradeLocker, cTrader, and Volumetrica FX

Challenge types compared

| Parameter | 1-Step GOAT | 2-Step Standard | 2-Step GOAT | Instant GOAT |

|---|---|---|---|---|

| Profit target | 10% | 8% / 5% | 9% / 6% | — |

| Daily loss limit | 4% | 5% | 5% | 3% |

| Overall loss limit | 6% | 10% | 10% | 6% |

| Drawdown model | Trailing | Static | Static | Trailing |

| Starting fee | from ~$45 | from $17 | from $17 | from ~$199 |

| Fee refund | 100% | 100% | 100% | — |

| Profit split | 80% → 100% | 80% → 100% | 80% → 100% | 80% → 100% |

How does it pay?

The default profit split is 80%, which can rise to 100% through the firm’s scaling and loyalty points system. For those who opt for the GOAT Model’s first “On-Demand Reward,” the firm reduces that specific payout to a 40% split, even if the 100% add-on is purchased. After the first on-demand reward, subsequent payouts revert to the full standard split (80% or 100% if upgraded).

Payout cycles run bi-weekly on the GOAT and Pro models, and every 10 days on the Standard model. GFT caps the first two payouts on funded accounts at 6% of the initial account size or $10,000, whichever is lower, and this cap lifts after the second successful withdrawal. Withdrawals go out via Rise, Skrill, or crypto, and the firm promises to process payouts within two business days.

Where does it fall short?

For the first two reward requests only, GFT caps withdrawals at 6% of the initial account balance or $10,000 (whichever is lower). This restricts how much users can cash out early on.

Verdict

GFT is best suited for high-capital, disciplined traders who can maintain steady daily gains within the firm’s limits. This is because the $3,000 daily profit cap, consistency rule, and 5-minute news-trading profit cap all reward slow, controlled scaling.

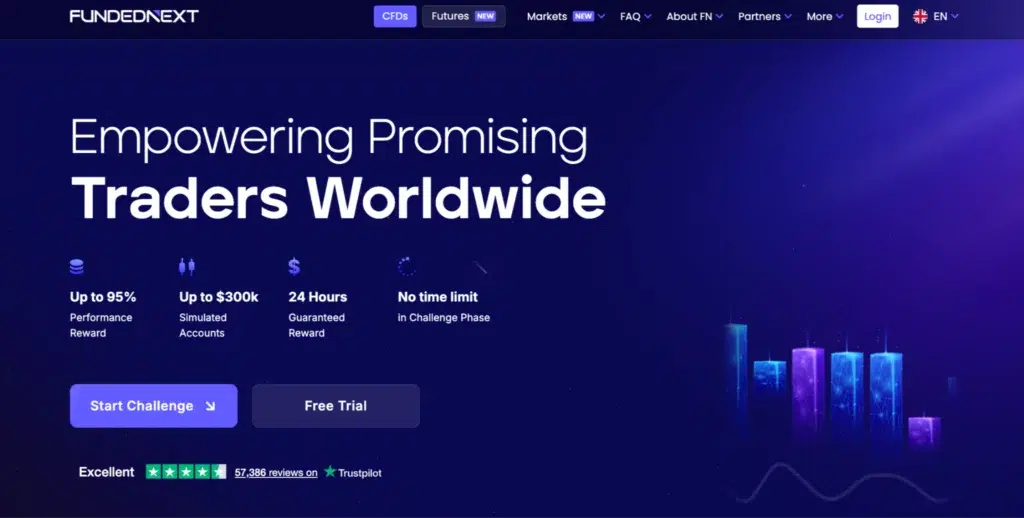

4. FundedNext

FundedNext is operated by FundedNext Ltd, registered under the laws of the Comoros Islands. The firm markets itself as officially based in Ajman, the United Arab Emirates, and has built its brand around one of the fastest payout promises in the industry. It offers a $1,000 bonus if it fails to process a reward within 24 hours.

What does FundedNext offer?

- CFDs where users can trade crypto, currencies, and more, and Futures where they can trade CME-listed active contracts.

- CFDs plan includes Stellar 2-Step, Stellar 1-step, Stellar Lite, and Stellar Instant.

- Account sizes range from $2,000 to $200,000

- 9 cryptocurrency pairs in total, traded as CFDs, including BTCUSD, ETHUSD, LNKUSD, LTCUSD, and XMRUSD.

- 1:1 crypto leverage

- Crypto trading runs 24/5, meaning it is closed weekends

- A 3x swap charge on crypto positions held open on Fridays, to account for weekend rollover.

- Reward share of up to 95%

- Trading via MT4, MT5, cTrader, and Match-Trader

Challenge types compared

| Parameter | Stellar 2-Step | Stellar 1-Step | Stellar Lite 2-Step | Evaluation 2-Step |

| Profit target P1 | 8% | 10% | 10% | 10% |

| Profit target P2 | 5% | – | 5% | 5% |

| Daily loss limit | 5% | 3% | 5% | 5% |

| Max overall loss | 10% static | 6% static | 10% | 10% static |

| Time limit | Unlimited | Unlimited | Unlimited | 4 wks P1 / 8 wks P2 |

| Drawdown type | Static (balance) | Static | Static | Static |

| 15% challenge reward | Yes (add-on) | Yes | No | No |

| Account sizes | $6K–$200K | $5K–$200K | $5K–$200K | – |

| Starting fee | from $59.99 | from $59.99 | from $32.99 | from $32 |

| Profit split | 80% → 90% via scaling | 80% → 90% | 80% → 90% | 80% → 90% |

| 1st payout | Day 21 | Day 21 | Day 21 | – |

How does it pay?

FundedNext pays traders through a Reward Share that starts at 80% for Stellar 2-Step, Stellar 1-Step, and Stellar Lite accounts opened from January 12, 2026, onward, and this share can climb to 90% through the firm’s Scale-Up plan and up to 95% with paid addons. Splits for Express Accounts start at 60% on the first withdrawal before rising to 75% and then 90% on subsequent payouts. The firm also offers a 15% reward on Challenge profits once the trader meets Scale-Up eligibility criteria.

FundedNext’s payouts start 21 days after the funded account starts, then every 14 days after that. The subsequent cycle can be five business days for Stellar 1-Step traders, and on-demand for Stellar Instant Account holders. The firm supports payouts via USDT (ERC20, TRC20), USDC (ERC20), Confirmo, RiseWorks, Bank Transfer, and direct deposit to FNmarkets.

Where does it fall short?

Crypto positions incur a triple swap charge specifically on Fridays to account for weekend rollover.

Verdict

FundedNext suits patient traders who can wait out 21-day funding cycles and 14-day payout intervals while scaling toward higher reward shares.

Crypto-native firms

We know that this category of prop firms only offers digital assets as the tradable instruments. This means the options suit traders who have no interest in forex, indices, or stocks.

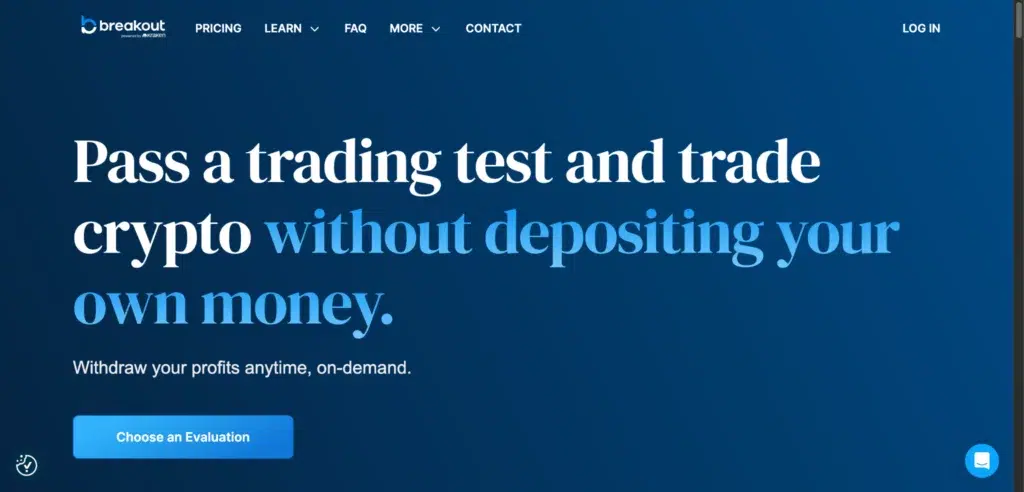

5. Breakout

Breakout started operating in November 2023 and was acquired by Kraken, one of the world’s largest cryptocurrency exchanges, in late 2025. That means Breakout is the only firm in this list directly owned by an exchange. The firm runs its own trading platform backed by Kraken’s liquidity.

What does Breakout offer?

- 1-Step Classic and 1-Step Pro evaluation paths

- Account sizes from $5,000 to $200,000

- Entry fees from $33 on the smallest 1-Step Pro account

- 62 tradeable crypto pairs

- Leverage up to 1:5 on BTC and ETH and 1:2 on altcoins

- No news trading restrictions of any kind

- Positions can be held overnight, over weekends, and over holidays

- On-demand payouts as long as the account has at least $50

- Trading fees of 0.04% per side, or 8 basis points per round trip

Challenge types compared

| Parameter | Classic 1-Step | Classic 2-Step | Pro 1-Step | Turbo 1-Step |

| Profit target P1 | 10% | 5% | 12–24% | Lower than Pro |

| Profit target P2 | – | 10% | – | – |

| Daily loss limit | – | 4% | 5% | 3% |

| Max overall loss | 6% static | 6% trailing | 5% static | 3% static |

| Drawdown type | Static | Trailing | Static | Static |

| Time limit | Unlimited | Unlimited | Unlimited | Unlimited |

| News trading | Fully permitted | Fully permitted | Fully permitted | Fully permitted |

| BTC/ETH leverage | 1:5 (alt 1:2) | Same | Same | Same |

| Max account size | $100K | – | $200K | $200K |

| Starting fee | from $45 | from $250 ($25K) | from ~$399 | from $45 |

| Profit split | 80% → 90% (add-on) → 95% after 3 mo | Same | Same | Same |

| Payout | On-demand 24/7 · USDC ERC-20 · 12–24 hrs · min $50 | Same | Same | Same |

How does it pay?

The default profit split is 80% to the trader, and which is upgradable to 90% at checkout at a fee. Breakout allows traders to request withdrawals anytime as long as the account has at least $50. The firm also promises “no approval queue and no minimum waiting period”, meaning a trader’s first payout can arrive the same day they get funded. Perhaps this is because the only payout method the firm supports is USDC on the ERC-20 network.

Where does it fall short?

The firm supports only one payout method.

Verdict

Breakout suits strictly crypto-focused traders who prefer on-demand payouts.

How the firms compare

| Firm | Type | Crypto Assets Offered | Payout Speed | Drawdown Type | Payout Cycle | Is Crypto Payout Method Available? |

| OneFunded | Multi-Asset | 15+ pairs | Within 1 hour of approval | Static | Weekly and Bi-Weekly | Yes |

| BrightFunded | Multi-Asset | 48+ pairs | Within 24 hours of approval | Static (1-Step);Trailing to high-water mark (2-Step) | 30 days, then bi-weekly | Yes |

| Goat Funded Trader | Multi-Asset | 500+ pairs (platform-dependent) | Within 2 business days | Static (GOAT evaluation models);Trailing (Instant models) | Bi-weekly (GOAT/Pro), every 10 days (Standard) | Yes |

| FundedNext | Multi-Asset | 9 pairs | Within 24 hours of approval | Static (Stellar plans); Trailing (Stellar Instant) | 21 days first cycle, then every 14 days | Yes |

| Breakout | Crypto-Native | 62 pairs | Same day, on-demand | Static (1-Step); Trailing to high-water mark (2-Step) | On-demand | Yes |

Matching a trading style to a firm

The chosen firm ultimately comes down to what the user is looking for beyond the advertised features. And a great approach to use is to do a self-evaluation and fit demands into a profile, such as the ones we will discuss below. Once a profile is known, they can easily tell which option suits them.

The multi-asset trader

This trader wants crypto in the same account as forex, indices, or metals, and has no interest in juggling separate platforms for each. If a trader fits into this profile, they will likely select OneFunded because it pairs a broad instrument list with a refundable evaluation fee and no deadline pressure during the challenge phase.

The altcoin specialist

This trader’s edge lives outside Bitcoin and Ethereum. HyroTrader is the strongest fit here, since its direct Bybit API connection unlocks more than 700 tradable pairs. Crypto Fund Trader is a close second because of its 550-plus pairs through the same Bybit connection, plus 556 additional pairs through MetaTrader 5 and Match-Trader.

Final word

It is much easier for crypto traders today to grow their careers because of the funding opportunities prop firms offer. The challenge is that lots of options are available, and the nature of prop firms itself is also fluid, which complicates decision-making.

However, one only needs to be clear on what they want, which will help them know whether a multi-asset firm suits them or they would be better off choosing a crypto-native one. Oftentimes, multi-asset options like OneFunded are ideal because they consolidate everything into one account.

Be that as it may, a funded account only works in someone’s favor if they approach it with a few non-negotiables in place. For instance, they must:

- Confirm the firm’s registration details independently

- Read the drawdown rules closely enough to know whether they are working against a static floor or a trailing one.

- Test the payout process with a small withdrawal request before scaling up their trading activity on the account.

- Treat the evaluation fee as the maximum amount they are willing to lose

- Revisit leverage caps on crypto specifically, since they are almost always lower than what the same firm offers on forex or indices.

It is also worth going in with realistic expectations about the odds. That means not being too certain that a user will easily get the funded account, because not everyone passes the evaluation. The most important thing is to have a solid strategy, one that will carry them through evaluation and at the funded stage.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

$700 Million in Liquidations as BTC, ETH, XRP Plunge Ahead of FOMC

‘Thrilled’ 76ers sign LeBron James with eyes on NBA title run

DeepSeek reportedly halts funding round after Wenfeng’s comments

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World7 days ago

Crypto World7 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat6 days ago

NewsBeat6 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech1 day ago

Tech1 day agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Business6 days ago

Business6 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment6 days ago

Entertainment6 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Crypto World5 days ago

Crypto World5 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics17 hours ago

Politics17 hours agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Sports4 days ago

Sports4 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Sports1 day ago

Sports1 day agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Fashion4 days ago

Fashion4 days ago16 Dresses for the High Summer Event

-

News Videos4 days ago

News Videos4 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Politics2 days ago

Politics2 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Entertainment4 days ago

Entertainment4 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

News Videos1 day ago

News Videos1 day agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

NewsBeat7 days ago

NewsBeat7 days agoNADINE DORRIES: I have witnessed first-hand what happens to new Prime Ministers when they enter No 10… and this is why Andy Burnham will be out by May

-

Crypto World5 days ago

Crypto World5 days agoUniswap (UNI) pushes deeper into tokenized RWAs with permissioned trading pools

-

Crypto World6 days ago

Crypto World6 days agoSablier Labs Enters Maintenance Mode, Halts Development

-

Crypto World5 days ago

SEC Agrees to Overhaul Recordkeeping After Settling Coinbase Lawsuit Over Gensler’s Lost Texts

You must be logged in to post a comment Login