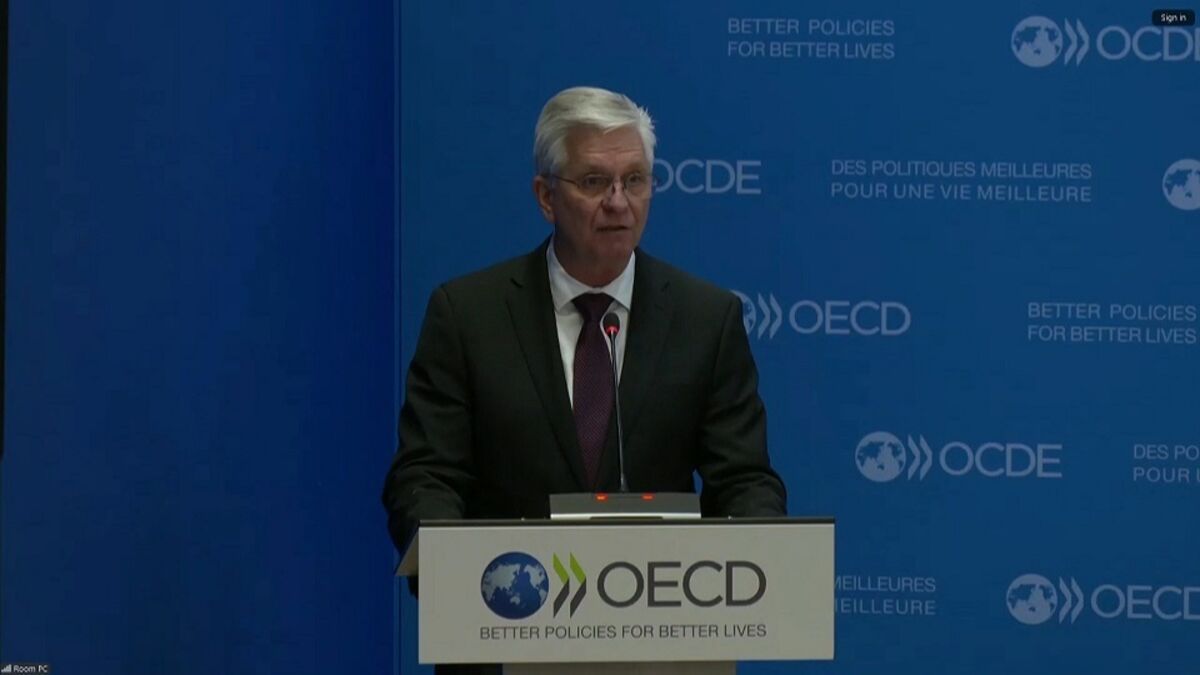

Federal Reserve Governor Christopher Waller said, “if the outlook evolves as I have described here, I will support continuing to cut our policy rate in 2025,” as he believes inflation will continue to cool toward the central bank’s 2% target. Waller also cast doubt on the idea that tariffs would have a significant effect on inflation, saying they “are unlikely to affect my view of appropriate monetary policy.” He spoke Wednesday at an Organization for Economic Cooperation and Development event i

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

+ There are no comments

Add yours