Crypto World

Chainlink connected SWIFT to crypto. LINK trades at $7

Chainlink has wired itself into the plumbing of global finance, with SWIFT, JPMorgan, UBS, and DTCC building on its infrastructure. Its token trades around $7, roughly 86% below its all-time high. The gap between the adoption and the price is the whole story, and it is the same story as XRP.

Summary

- Chainlink has embedded itself in traditional finance, with SWIFT, JPMorgan, UBS, DTCC, and others building on its cross-chain infrastructure, yet LINK trades near $7, about 86% below its 2021 high.

- The disconnect mirrors XRP almost exactly: the network’s adoption is real and growing, but the token captures the value only indirectly and slowly.

- Chainlink secures more value than any other oracle network and its cross-chain protocol processes billions of dollars a month, but the fees actually reaching LINK holders are tiny next to the headline adoption.

- A new strategic reserve converts protocol revenue into LINK and staking locks up supply, but neither yet offsets weak token-level demand and a soft market for high-risk altcoins.

- The gap closes only if bank usage scales into real, recurring fee demand for LINK, and the clearest test is whether SWIFT’s integration moves from pre-production into live settlement volume.

Chainlink may be the most widely adopted piece of infrastructure in all of crypto, and its token trades like an afterthought.

Over the past two years the network has wired itself into the core of traditional finance, with SWIFT, the messaging backbone that connects roughly 11,000 banks and moves on the order of $150 trillion a year, moving from pilot to pre-production on Chainlink’s cross-chain technology.

JPMorgan, UBS, ANZ, Fidelity International, SBI, DTCC, Euroclear, and Mastercard have also built around its infrastructure, while the value secured across its oracle network has climbed past $90 billion, many times that of any competitor.

By the measure of institutional adoption that crypto has chased for a decade, Chainlink has arguably won. And yet LINK, its token, trades around $7, roughly 86% below the all-time high near $53 it reached back in 2021.

The fundamentals keep setting records and the price keeps disappointing. That gap, between a network embedding itself in global finance and a token that acts like none of it is happening, is the entire story.

Anyone who followed XRP through 2026 will recognize it immediately, because it is the same adoption-versus-token gap.

This piece works through why Chainlink’s extraordinary adoption has not lifted its token. It covers what Chainlink actually does and why banks cannot easily avoid it, what SWIFT and the institutions signed up for, the central problem of how value is supposed to reach the token at all, the mechanisms Chainlink has built to try to close that gap, why the market still refuses to pay up, and what would finally have to change for the price to follow the adoption.

The aim is not to talk LINK up or down, but to explain one of the most striking disconnects in the market: how a project can win the institutional race it set out to win and watch its token languish anyway.

The most important company in crypto you do not trade

Start with what Chainlink does, because its importance is easy to miss precisely because it is infrastructure.

Blockchains have a built-in blindness: they cannot, on their own, see anything that happens outside their own network. A smart contract on a blockchain has no native way to know the price of a stock, the result of a shipment, the value of a currency, or whether a payment cleared in a bank account.

This is called the oracle problem, and it is a hard limit on what blockchains can do, because a contract that cannot react to real-world information is a contract that can only move tokens around inside its own walls.

Chainlink exists to solve exactly this. It is a decentralized network that feeds outside data onto blockchains and connects them to one another and to traditional systems, acting as the secure bridge between the on-chain world and everything else.

Without something like Chainlink, the entire edifice of decentralized finance, and the much larger project of tokenizing real-world assets, simply does not function.

That is why what oracles feed data to matters. Smart contracts are only as useful as the data and systems they can reliably touch.

Because that role is foundational, Chainlink has become close to unavoidable for anyone serious about putting financial activity on a blockchain.

Its price feeds underpin major lending and trading protocols across decentralized finance. Its cross-chain protocol has been adopted by large exchanges and protocols as a bridging standard.

Critically, its institutional push has landed the names that matter most. The roster of traditional-finance firms building on Chainlink reads like a directory of the global banking system, and the total value its oracle network secures runs into the tens of billions, many times that of the nearest competitor.

By the standard crypto has always used to define success, real institutions using the technology for real financial activity, Chainlink is at or near the top of the entire industry.

It is, in a sense, the most important company in crypto that most people never think to trade, because its product is the invisible plumbing rather than the visible coin.

And a token that trades like the adoption is not happening

Now place that adoption next to the chart, and the contrast is jarring.

LINK trades around $7, down roughly 86% from its 2021 peak near $53, and it spent the most recent stretch sliding rather than rising, sitting below the technical levels that traders watch for signs of strength.

The pattern across the last couple of years has been almost comically consistent: record after record on the fundamentals, the cross-chain protocol moving billions a month, the value secured hitting new highs, the bank partnerships piling up, while the token closed well below where it traded years earlier.

Analysts who follow Chainlink closely have taken to describing its recent history in exactly those terms, as a period of record fundamental milestones paired with significant price disappointment.

The ETF channel has not solved the problem either. Chainlink spot ETFs recently saw a net outflow, ending a six-month inflow streak and showing that even new institutional access does not automatically create uninterrupted demand.

This is what makes Chainlink such a clean case study, and such a frustrating holding for its believers.

It is not a story of a failing project ignored for good reason; the project is, by adoption metrics, thriving. It is a story of a thriving network whose token has decoupled from its success.

That forces an uncomfortable question that applies to a whole category of crypto assets: what is the actual link between a network being used and its token rising in value?

For Bitcoin the answer is relatively direct, since the asset itself is the product. For an infrastructure token like LINK, the answer is far murkier, and the murkiness is precisely what the price reflects.

The market is not saying Chainlink has failed. It is saying it does not yet see how all that institutional adoption turns into sustained demand for the token.

Until it does, the chart and the deal sheet point in opposite directions.

The oracle problem, and why it made Chainlink unavoidable

To understand both the strength of Chainlink’s position and the weakness of its token, it helps to sit with the oracle problem a moment longer, because it explains the moat.

A blockchain is a deterministic system: it is brilliant at agreeing on its own internal state, who holds what, but it is mathematically incapable of knowing anything about the outside world on its own.

If a smart contract needs to know the price of an asset to liquidate a loan, or whether a real-world bond has matured, it has to get that information from somewhere. If it gets it from a single source, it inherits that source’s vulnerability to error or manipulation.

That would undermine the security that makes blockchains worth using in the first place.

Chainlink’s design answers this by gathering data through a decentralized network of independent node operators, aggregating their inputs, and delivering a result that no single party can easily corrupt.

That decentralized, tamper-resistant design is why Chainlink became the default rather than one option among many.

Once a network of high-quality node operators is securing tens of billions of dollars across hundreds of applications, that track record itself becomes a moat. A bank deciding whose data and cross-chain infrastructure to trust with real money is going to choose the one with the longest, most battle-tested history.

This is the foundation of the institutional strategy.

Chainlink’s cross-chain protocol added a risk-management layer, an independent set of nodes that watches for anomalies and can halt transfers if something looks wrong. That is the kind of dual-layer safeguard large institutions demand before moving significant capital on-chain.

The result is that Chainlink occupies a position closer to critical utility than to speculative token: the oracle and interoperability standard that the tokenized-finance future is being built on.

The strength of that position is not in doubt. What is in doubt is whether holding the token captures any of it.

What SWIFT and the banks actually signed up for

The institutional adoption is concrete and worth spelling out, because it is genuinely impressive and it is also, on close inspection, the source of the token’s problem.

Chainlink built a suite of products aimed squarely at banks and asset managers: a cross-chain protocol for moving assets and messages between blockchains and legacy systems, a runtime environment that lets institutions build and manage tokenized-asset workflows, a compliance engine that embeds rules like identity checks directly into tokenized assets, a confidential-compute layer that lets sensitive institutional data be processed without exposing it on a public chain, and data services that bring benchmark and index information on-chain.

This is not a retail product suite. It is enterprise financial infrastructure, designed to slot into how large institutions already operate.

The marquee relationship is with SWIFT, and it captures both the scale and the nature of the adoption.

SWIFT connects roughly 11,000 banks and carries the messaging behind an enormous share of global settlement, and Swift and Chainlink’s ongoing work moved from early pilot toward pre-production.

The goal is to let banks send traditional SWIFT messages that trigger smart-contract actions across blockchains, without those banks having to rip out and rewrite their legacy systems.

That is a profound integration: it means the existing banking messaging layer could reach into the on-chain world through Chainlink as the connective tissue.

More recently, Chainlink also partnered with more than 50 banks on Project Pangea for T+0 foreign-exchange settlement, another sign that traditional finance is testing Chainlink as an institutional bridge rather than a crypto side experiment.

But notice the shape of it. What the banks signed up for is infrastructure, a way to connect their systems to blockchains using Chainlink’s technology.

They signed up to use the network. Nothing in a SWIFT pre-production integration, a JPMorgan tokenization pilot, or a bank FX settlement project necessarily requires anyone to buy, hold, or even think about the LINK token.

The adoption is real, and it is adoption of Chainlink the infrastructure. That is different from demand for LINK the asset.

That distinction is the hinge on which the entire price puzzle turns.

The value-accrual problem: adoption is not token demand

Here is the core issue, the one that explains the chart.

For a token to rise because its network is being used, there has to be a mechanism that converts that usage into demand for the token. For infrastructure tokens, that mechanism is often weak, indirect, or still being built.

When a bank uses Chainlink’s Cross-Chain Interoperability Protocol, it pays fees, and those fees are part of how value is meant to flow to the network.

But the fees generated even by substantial institutional usage are, so far, small relative to the headline numbers that make the adoption sound overwhelming.

The value secured across the network may be measured in tens of billions, but the value secured is not revenue. Revenue is not automatically token demand either.

A pilot or a pre-production integration generates little in the way of recurring fees, and even meaningful live usage produces fee flows that are modest next to LINK’s multi-billion-dollar market value.

This is the value-accrual problem, and it is the single best explanation for why LINK trades where it does.

The market is making a distinction that the celebratory headlines blur: between adoption of the infrastructure, which benefits the network and its users, and demand for the token, which is what actually moves the price.

It is the identical distinction that explains why XRP failed to rally on Ripple’s bank deals, because those deals ran through the company and its stablecoin while the token captured only a sliver.

For Chainlink, the question every prospective LINK buyer faces is simple and unforgiving: if SWIFT and JPMorgan can use the network without the token being central to the economics, then what exactly am I buying when I buy LINK?

The project has answers to that question, and they are improving. But the market has not yet been convinced that the answers are large enough to matter.

That is why the adoption keeps growing and the token keeps waiting.

The strategic reserve and staking: Chainlink’s answer

Chainlink is acutely aware of the value-accrual problem, and it has been building mechanisms specifically designed to tie network usage to token value.

That is the strongest part of the bull case.

The first is a fee model that converts revenue generated across the network, including from institutional and off-chain use, into LINK, accumulating it in the Chainlink Reserve.

The logic is that as adoption grows and generates more revenue, more of that revenue is converted into LINK and held, creating a structural source of buying tied directly to usage.

This is meant to be the bridge between adoption and token demand that infrastructure tokens so often lack.

It is a way to make sure that when the network earns, the token benefits. The reserve has been growing, adding millions of LINK, which is a tangible sign of the mechanism working, even if the amounts remain small relative to the total supply.

The second mechanism is staking.

Chainlink lets LINK holders stake their tokens to help secure the network’s data feeds and services, locking up supply and giving the token a direct role in the system’s security and economics.

As more high-value feeds and services come to rely on staked LINK as a security backstop, demand to stake, and therefore to acquire and lock the token, is meant to rise.

That makes Chainlink part of a broader move toward security-backed crypto networks. For context, another staking-secured network shows how tokens can accrue value when they are required to secure services rather than simply sit beside them.

Together, the reserve and staking are Chainlink’s answer to the question of why anyone should own LINK instead of simply admire the network.

The reserve ties revenue to token accumulation. Staking ties the token to the network’s security and to a yield.

These are real, well-designed mechanisms, and they are the reason the bull case is not empty.

The honest caveat is that they are still early and still modest in scale relative to a multi-billion-dollar market cap. They point in the right direction, but they have not yet generated token demand large enough to overcome the broader forces pushing the price down.

Why the chart still says no

Even granting the reserve and staking, several forces keep weighing on LINK, and naming them explains why the token has not responded to the adoption.

The first is the simple gravity of the broader market. LINK is a high-beta altcoin, meaning it tends to move more violently than the market as a whole, rising faster in booms and falling harder in downturns.

Through a stretch of macro pressure and a weak environment for risk assets, infrastructure tokens like LINK have been sold off regardless of their individual progress.

When capital flees risk, the quality of a project’s bank partnerships offers little protection, because the selling is driven by macro flows, not fundamentals.

The second force is competition. Chainlink leads the oracle space by a wide margin, but rivals are chasing the same market with different technical models, faster delivery in certain niches, or lower costs.

The existence of credible competitors caps the pricing power and the perceived inevitability that would justify a higher token valuation.

The third and deepest force is the value-accrual skepticism already described.

The market keeps treating Chainlink’s institutional milestones as proofs of concept instead of as recurring revenue, pricing a SWIFT pre-production integration as a promising experiment instead of as a stream of token demand, because that is what it currently is.

Until the pilots become production volume large enough to drive real fees into the reserve and real demand into staking, the market is, not unreasonably, declining to pay in advance.

This is the same discipline that kept XRP pinned through its own parade of bank wins. The chart is not ignoring the adoption; it is refusing to pay for token demand that has been promised but not yet delivered at scale.

What would finally make LINK follow the adoption

If you want to know when LINK might finally track its fundamentals, the analysis points to a specific set of conditions, and none of them is simply another partnership announcement.

The first and most important is the transition from pilots to production volume.

A SWIFT integration in pre-production is a promise; SWIFT-connected banks routing real, recurring settlement volume through Chainlink’s protocol would be a structural source of fee demand unlike anything in the token’s history.

Even a small fraction of the volume that flows through global bank messaging would dwarf current usage.

The clearest single catalyst to watch is whether that integration goes fully live and starts carrying real traffic, because that is the moment infrastructure adoption could begin converting into the recurring revenue that feeds the reserve.

The policy backdrop also matters. Chainlink executives have warned that delays in U.S. crypto rules benefit overseas competitors, because institutions need clarity before they can scale production deployments.

The second condition is the maturation of the token mechanisms themselves: the strategic reserve growing large enough that its accumulation of LINK becomes a meaningful, visible source of demand, and staking scaling to the point where locking the token to secure high-value services pulls significant supply off the market.

The third is the broader environment, since even strong fundamentals struggle against a hostile macro tape, and a friendlier market for risk assets would let Chainlink’s progress show up in the price.

The new exchange-traded products tracking LINK add another potential channel for demand if they gather assets. But as the recent outflow showed, the ETF channel must become a sustained buyer, not just another headline.

The honest synthesis is that Chainlink has done the hard part, winning the institutional adoption that the rest of crypto only talks about.

The remaining question is purely about conversion: whether all that adoption can be turned into durable, measurable demand for the token through fees, the reserve, and staking, at a scale large enough to matter.

Until it is, LINK will keep trading like the adoption is not happening, not because the market is blind to Chainlink’s success, but because it is watching the one number that has not yet moved. That number is demand for the token itself.

Frequently asked questions

Why does Chainlink have so much adoption but a low token price?

Because adoption of the infrastructure is not the same as demand for the token. Banks and protocols use Chainlink’s data feeds and cross-chain protocol, generating fees, but those fees are still small relative to LINK’s multi-billion-dollar market value, and nothing about a SWIFT or JPMorgan integration requires anyone to buy or hold LINK. The market distinguishes between the network being used, which benefits the infrastructure, and token demand, which moves the price. So far, the adoption has not converted into token demand large enough to lift the price, which is why LINK trades around $7 despite record fundamentals.

What does Chainlink actually do?

Chainlink solves the oracle problem. Blockchains cannot natively access information outside their own network, so a smart contract has no built-in way to know a price, a payment status, or a real-world event. Chainlink is a decentralized network that feeds outside data onto blockchains and connects them to one another and to traditional systems, using many independent node operators so no single party can easily corrupt the data. This makes it foundational infrastructure for decentralized finance and for tokenizing real-world assets.

What did SWIFT and the banks sign up for with Chainlink?

They signed up to use Chainlink’s infrastructure, chiefly its cross-chain protocol, which lets banks send traditional SWIFT messages that trigger smart-contract actions across blockchains without rewriting their legacy systems. JPMorgan, UBS, DTCC, Euroclear, and others are building on Chainlink’s suite of institutional products for tokenized assets, compliance, and data. Crucially, this is adoption of the infrastructure, not a commitment to buy or hold the LINK token, which is exactly why the impressive partnerships have not directly lifted the price.

How is Chainlink trying to connect adoption to the token?

Through two main mechanisms. A fee model converts revenue generated across the network, including from institutional use, into LINK and accumulates it in a strategic reserve, creating buying tied to usage. Staking lets holders lock LINK to help secure the network’s data feeds and services, taking supply off the market and giving the token a direct economic role. Both are well-designed attempts to bridge the gap between adoption and token demand, and the reserve has been growing, but they remain modest relative to LINK’s market value and have not yet offset the forces pushing the price down.

Will LINK go up if SWIFT fully adopts Chainlink?

It could, but the key is volume, not the integration itself. A pre-production SWIFT integration is a promise; SWIFT-connected banks routing real, recurring settlement volume through Chainlink would generate fee demand on a scale unlike anything in the token’s history, because even a fraction of global bank messaging volume would dwarf current usage. That fee flow could feed the strategic reserve and drive real token demand. So the catalyst to watch is whether the integration goes live and carries actual traffic, turning infrastructure adoption into recurring revenue, instead of the announcement of the integration alone.

Is Chainlink’s situation similar to XRP’s?

Very. Both are cases where a network or company achieved real institutional adoption while the token failed to follow, because the value flows first to the infrastructure and only indirectly to the token. Ripple’s bank deals ran through its stablecoin and ledger while XRP captured a sliver; Chainlink’s bank integrations run through its infrastructure while LINK captures fees that are still small relative to its valuation. In both cases the market prices the adoption as promising proof of concept instead of as token demand, and in both cases the token waits for pilots to become production-scale volume.

This article is information, not investment advice. Cryptocurrency is volatile, and figures for Chainlink and LINK reflect reporting available as of June 26, 2026, which can change quickly. Do your own research and verify current data from primary sources before making any decision.

The Monetary Authority of Singapore (MAS) has added Hyperliquid to its Investor Alert List, flagging the decentralized perpetuals exchange as an entity that consumers may wrongly assume is licensed or regulated by the central bank.

MAS says the latest entry, published on Friday, names both the Hyper Foundation website and the Hyperliquid trading app. The Investor Alert List is designed as a consumer protection tool rather than a ban or an announcement of enforcement action.

Key takeaways

- MAS has included Hyperliquid on its Investor Alert List, associating the flag with the Hyper Foundation website and the Hyperliquid app.

- Being listed does not mean MAS has launched an enforcement action or imposed a prohibition.

- MAS’s move follows other crypto platform additions earlier in 2025, including Bybit (June 17) and listings that also include KuCoin and Bitget.

- Singapore continues tightening oversight, emphasizing consumer protection and alignment with global anti–money laundering and counter-terrorism financing expectations.

- Hyperliquid says it has not claimed MAS licensing or authorization, arguing its permissionless setup has not changed.

MAS adds Hyperliquid to the Investor Alert List

MAS’s Investor Alert List is meant to reduce the risk that members of the public interpret certain firms or websites as being authorized or overseen by the regulator. According to MAS’s description of the list, inclusion is not an indication that an activity is prohibited, nor does it itself represent a regulatory action.

The update lists Hyperliquid through its ecosystem: MAS references both the Hyper Foundation website and the Hyperliquid trading application in the same entry. The regulator added the new item on Friday.

Cointelegraph attempted to contact MAS for additional comment but did not receive a response prior to publication.

Hyperliquid responds: no MAS authorization claim

Hyperliquid pushed back on any implication that it sought or received MAS approval. The platform said it has never presented itself as licensed or authorized by MAS and argued that nothing about its permissionless infrastructure has changed.

In a Friday post on X, Hyperliquid wrote that it remains committed to engaging with regulators and institutions globally while supporting “clear, well-designed frameworks” for onchain finance.

How Hyperliquid fits the broader Singapore crackdown

Singapore has tightened crypto regulation in recent years, with MAS repeatedly emphasizing that the industry must comply with licensing requirements and anti-financial crime standards. The regulator’s approach has included clarifying how firms serving foreign customers are treated under Singapore’s framework.

In May 2025, MAS ordered crypto companies that served overseas customers to either obtain the necessary licenses or stop operating. MAS characterized the decision as consistent with its long-standing stance rather than a sudden policy shift.

MAS said the directive targeted a loophole that had allowed certain firms headquartered in Singapore to avoid licensing by focusing on customers outside the jurisdiction. In MAS’s framing, the move effectively ended a transition period for firms that continued operating without a license while serving only overseas users.

MAS also explained that its measures aim to strengthen consumer protection and bring Singapore’s crypto oversight in line with international expectations relating to Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT).

What the market data suggests—and what remains unclear

While MAS’s Investor Alert List is a consumer-facing notice, traders and investors often read these updates as signals about how Singapore-based oversight is tightening across both centralized and decentralized crypto offerings.

According to CoinGecko, Hyperliquid ranks as the ninth-largest decentralized exchange by trading volume. Separately, DefiLlama estimates Hyperliquid’s total value locked (TVL) at around $5.7 billion.

At the same time, the regulatory message conveyed by MAS’s Investor Alert List is not a direct restriction. That distinction matters for users trying to understand what changed in practice: the list signals potential consumer misunderstanding around regulatory status, but it does not, on its own, spell out whether specific Singapore-based intermediaries or local distribution channels will face separate action.

Readers should watch for whether MAS follows up with additional clarifications on how its licensing expectations interact with permissionless infrastructure and whether any related entities—such as service providers or interfaces that could influence access—are later referenced in the regulator’s consumer warnings.

For now, the key question is how Singapore will translate its licensing and AML/CFT enforcement posture into the decentralized layer—especially as major protocols like Hyperliquid continue to grow in usage—while keeping the boundary clear between consumer alerts and actual regulatory prohibitions.

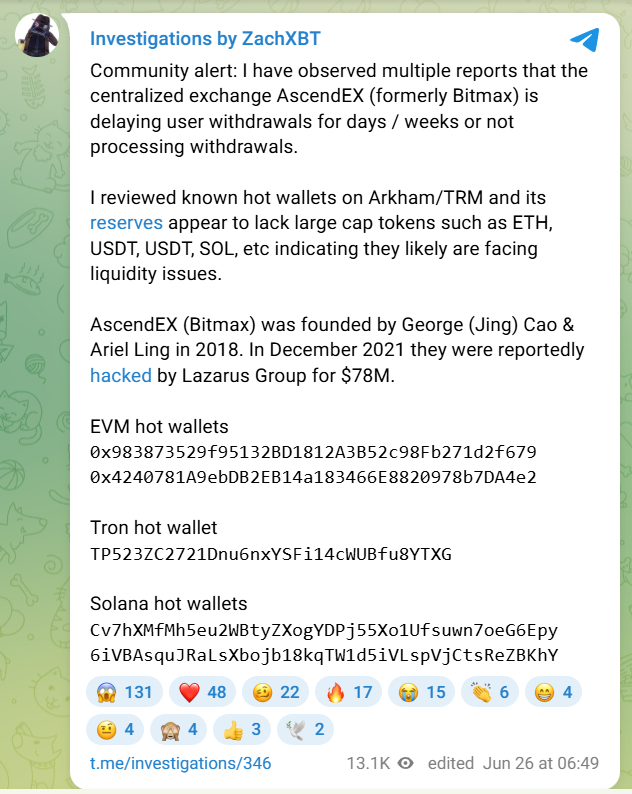

Multiple users have reported issues withdrawing funds from cryptocurrency exchange AscendEX, which blockchain investigator ZachXBT said may be showing signs of liquidity issues.

An X account using the name Lorenzo Navarro Rodriguez said in a Tuesday post that a 4,196 USDT withdrawal had remained stuck in an “initiating” state since June 10. The account also said repeated customer support inquiries had gone unanswered.

At least five other users replied to the post over the following days, reporting similar withdrawal issues.

On Friday, ZachXBT said in a Telegram post that the exchange lacked large-cap reserves for tokens such as Ether (ETH), USDT (USDT) and Solana (SOL), indicating potential “liquidity issues” on the platform. ZachXBT urged the platform to respond to the reports about delayed withdrawal requests and provide more clarity on why its hot wallets have low liquidity.

Related: Polymarket hit by $2.9M theft, users to be refunded

Exchanges rely on liquid reserves of widely traded assets to process customer withdrawals. A shortage of those assets can lead to delayed withdrawals or, in severe cases, insolvency.

ZachXBT flags liquidity and withdrawal issues on AscendEX via Telegram. Source: ZachXBT

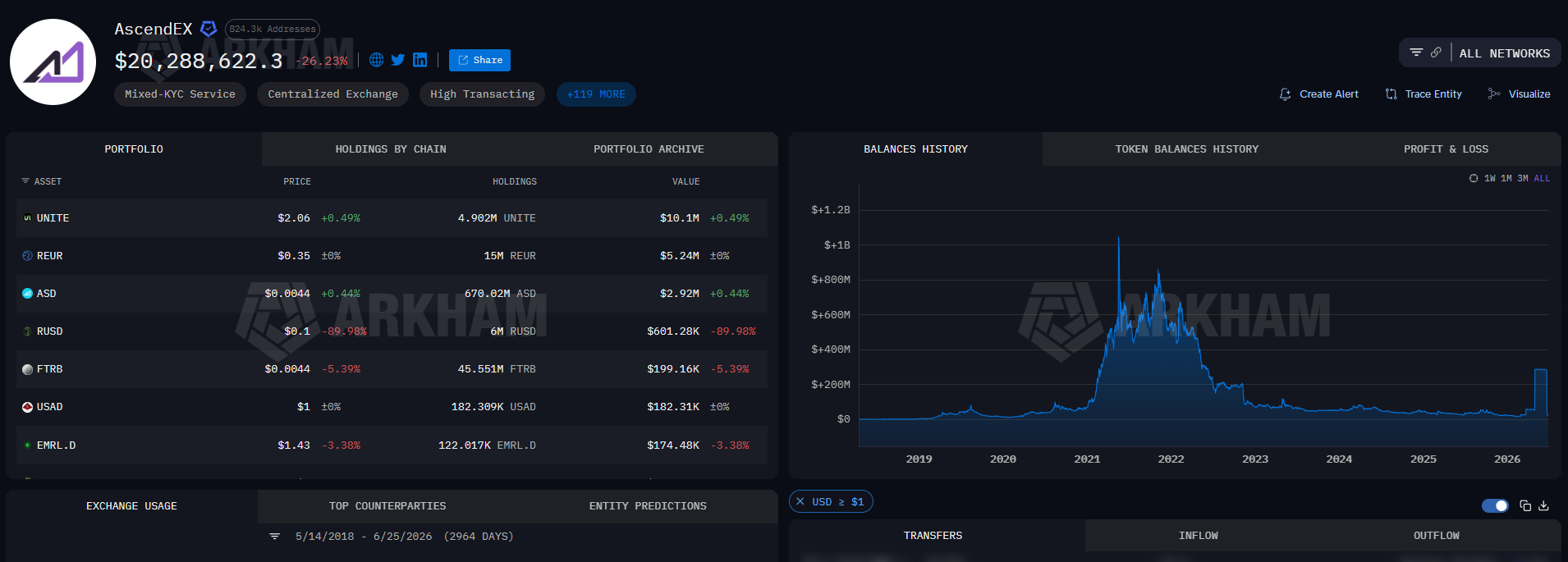

AscendEX’s reserves are dominated by small-cap holdings

Blockchain data on Arkham viewed by Cointelegraph on Friday showed that AscendEX-tagged wallets held about $20.2 million in crypto. Arkham-tagged wallets were concentrated in smaller-cap assets, with relatively limited holdings of major cryptocurrencies.

AscendEx had $10 million in UNITE tokens as its largest holding, followed by $5.24 million worth of REUR, $2.9 million in ASD and $600,000 worth of Reservoir rUSD stablecoins, among other smaller tokens.

AscendEX-tagged wallet, top token holdings. Source: Arkham

Cointelegraph has approached AscendEX for comment but not received a response before publishing.

Questions about an exchange’s liquidity are highly sensitive in the crypto industry following the collapse of FTX in 2022, when customer withdrawal requests exposed a multibillion-dollar shortfall that ultimately led to the exchange’s bankruptcy.

The failure triggered a wave of customer withdrawals across the industry, intensified regulatory scrutiny and prompted many exchanges to publish proof-of-reserves reports in an effort to reassure users.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

New U.S. Federal Reserve Chairman Kevin Warsh holds a press conference following a two-day meeting of the Federal Open Market Committee (FOMC), at the U.S. Federal Reserve in Washington, D.C., U.S. June 17, 2026.

Eric Lee | Reuters

Federal Reserve Chairman Kevin Warsh has added two more key advisors as he seeks to remake how the central bank approaches its views on the economy and monetary policy, people familiar with the moves confirmed to CNBC.

Though Warsh has talked about broad changes that need to be made at the Fed, he instead reached inside for these appointments, naming economists Daniel Covitz and Eric Engstrom to the posts. Covitz is one of three deputy directors in the research and statistics division while Engstrom is an associate director in monetary affairs.

The appointments come a little more than a week after Warsh announced five task forces aimed at addressing broad aspects of the Fed’s operational structure. Among the focuses will be communication, data, inflation, technology and the Fed’s balance sheet.

Warsh has touted the importance of re-examining how the Fed views each of the key metrics and said he will deploy resources both inside and outside the institution to tackle the projects.

However, the latest announcements indicate that he will rely heavily on the Fed’s own experts as he charts the course ahead. Both Engstrom and Covitz bring decades of Fed experience to their new positions. A Fed official noted that the two will serve in these positions on a rotating basis while maintaining their positions in their respective divisions.

Warsh earlier selected Paul Winfree, an architect of the controversial Project 2025 document that sought to decrease the Fed’s influence on the economy, and Daniel Heil of Stanford, who had previously worked with Warsh.

The two latest appointments were first reported in the Wall Street Journal.

Crypto World

Johnson & Johnson (JNJ) Stock Reaches New Peak on Analyst Upgrade and Strong Drug Performance

Key Highlights

- Johnson & Johnson reached a record price of $251.76 on June 26, 2026, delivering a 65.12% total return over 12 months

- Guggenheim elevated its target from $266 to $270 while maintaining a Buy rating, designating JNJ as a leading large-cap biopharma selection

- Second-quarter 2026 results expected July 15; Guggenheim projects $25.48B revenue and $2.87 EPS, surpassing consensus estimates

- Robust prescription performance for Tremfya, Caplyta, and Erleada supported the upgraded outlook

- Company faces $32 million verdict in Los Angeles talc-related mesothelioma lawsuit

Shares of Johnson & Johnson climbed to an unprecedented $251.76 on Thursday, June 26, before settling near $251.18 — marking just a 0.97% decline from that record level. This performance brings the pharmaceutical giant’s trailing 12-month total return to 65.12%, with its market valuation standing at $604.8 billion.

The surge coincided with Guggenheim’s announcement raising its valuation target on JNJ to $270 from the previous $266, while reaffirming its Buy recommendation. The investment firm simultaneously highlighted JNJ as a premier choice within the large-capitalization biopharmaceutical sector.

Guggenheim’s forecast for the second quarter of 2026 anticipates revenues reaching $25.48 billion alongside earnings per share of $2.87. These projections exceed the prevailing Street consensus, which calls for $24.96 billion in sales and $2.85 per-share profit.

Catalysts Behind the Optimistic Outlook

The enhanced valuation stems from prescription velocity data that exceeded expectations across three important medications: Tremfya, Caplyta, and Erleada. Performance metrics for each surpassed Guggenheim’s proprietary forecasts.

Analysts noted that prescription tracking for two recently introduced therapies — Icotyde and Inlexzo — remains too preliminary for meaningful incorporation into models. These products will receive heightened scrutiny as data sets become more comprehensive.

Guggenheim anticipates the July 15 earnings discussion will emphasize Tremfya’s volume expansion, the commercial rollout of Icotyde, the company’s multiple myeloma pipeline, alongside updates on Caplyta and Spravato.

JNJ boasts an impressive 55-year streak of annual dividend increases, solidifying its appeal among yield-oriented portfolio managers.

Corporate Initiatives and Challenges

Beyond market performance, JNJ unveiled plans to invest over $1 billion in its Jacksonville, Florida facilities. These funds will support enhanced manufacturing, packaging, and logistics infrastructure for the Vision segment, particularly ACUVUE contact lens production.

The organization also broadened domestic distribution of its TECNIS PureSee intraocular lens, designed for cataract procedures. On the research front, JNJ disclosed encouraging Phase 2/3 data for Imaavy in treating warm autoimmune hemolytic anemia patients.

However, legal headwinds persist. A jury in Los Angeles determined JNJ bore responsibility in Maria Lozano’s mesothelioma case, resulting in a $32 million judgment for her family. The verdict relates to asbestos contamination allegations in the company’s baby powder products — a prolonged litigation concern.

InvestingPro’s current assessment suggests the shares may be trading at a premium relative to fundamental metrics, despite the compelling upward momentum.

TLDR:

- Securitize expects about $400 million in gross proceeds after fewer than 30% of SPAC shares were redeemed.

- The proposed business combination is expected to close on July 1 after shareholder approval on June 29.

- Securitize Corp. is scheduled to begin trading on the NYSE under the ticker SECZ on July 2, 2026.

- Securitize currently tokenizes more than $4 billion in real-world assets across its investment platform.

Securitize SPAC Deal is moving toward completion after the company confirmed its proposed business combination with Cantor Equity Partners II is expected to raise approximately $400 million in gross proceeds.

Fewer than 30% of CEPT Class A shareholders redeemed their shares, allowing most trust proceeds to remain available.

Subject to shareholder approval on June 29 and customary closing conditions, the transaction is expected to close on July 1, with the combined company targeting a New York Stock Exchange listing on July 2 under the ticker SECZ.

Securitize SPAC Deal Secures $400 Million Before Public Listing

Securitize and Cantor Equity Partners II announced the final redemption results on June 26 through an official company statement.

Less than 30% of CEPT Class A shareholders elected to redeem their shares before the proposed business combination.

The redemption outcome means Securitize expects to receive approximately $400 million in gross proceeds. The amount includes related PIPE financings but excludes all transaction-related expenses.

The companies also confirmed that 71.5% of the CEPT trust was retained. The proposed business combination remains subject to shareholder approval during the special meeting scheduled for June 29.

If shareholders approve the transaction and the remaining conditions are satisfied or waived, the companies expect to complete the merger on July 1.

The combined entity is then expected to begin trading on the New York Stock Exchange under the ticker SECZ on July 2.

CEO Discusses Public Market Plans as Tokenization Business Grows

Following the completion of the transaction, the combined company will operate as Securitize Corp. The company currently tokenizes more than $4 billion in real-world assets across its platform.

Commenting on the upcoming listing, Securitize Co-Founder and Chief Executive Officer Carlos Domingo said, “Reaching the public markets is a milestone for Securitize and a reflection of the growing momentum behind tokenization.”

He added that the company began more than eight years ago when institutional adoption of tokenized securities remained largely theoretical.

Domingo continued, “Today, tokenization is moving into the mainstream, and we believe becoming a public company gives us the visibility, credibility, and capital to lead that next phase of growth.” The remarks accompanied the company’s announcement of the expected closing timeline.

The company confirmed that the planned schedule remains unchanged following the redemption results. Subject to shareholder approval on June 29, Securitize expects to complete the business combination on July 1 before its shares begin trading on the NYSE under the SECZ ticker on July 2.

Hyperliquid has been added to the Investor Alert List (IAL) maintained by the Monetary Authority of Singapore (MAS). The perpetual futures platform clarified that the listing does not represent a regulatory violation, enforcement action, or ban.

In a statement shared on X, Hyperliquid said that inclusion on the IAL should not be interpreted as evidence of wrongdoing while adding that the list is intended to identify entities that may be incorrectly viewed as being licensed, authorized, or regulated by MAS.

MAS Investor Alert List

Hyperliquid noted that several major crypto exchanges and decentralized finance protocols have also appeared on the list in the past. According to MAS, the Investor Alert List contains names of entities that, based on information available to the regulator, may have been wrongly perceived as being licensed or otherwise regulated by the central bank.

The regulator also stated that the list may include entities offering investments or investment-related products that could be mistakenly viewed as being authorized, recognized, registered, or accompanied by documents lodged with MAS.

Responding to the development, Hyperliquid asserted that it is a permissionless infrastructure and has never claimed to be licensed or authorized by MAS and that users should not regard the platform as holding such approval. The platform added that users continue to maintain self-custody of their assets and that transactions on the network remain transparent and fully settled on-chain.

“The Hyperliquid ecosystem remains committed to engaging collaboratively and constructively with regulators and institutions globally and to supporting clear, well-designed frameworks for onchain finance.”

The MAS had also placed Bybit Fintech Limited on its Investor Alert List earlier this month. In response, Bybit said it has maintained regular and constructive engagement with MAS and has implemented measures to restrict access for users in Singapore. The exchange said these measures include restrictions in its terms of service and geo-blocking of Singapore IP addresses.

HYPE Cools but ETF Interest Accelerates

Hyperliquid’s native token, HYPE, showed little reaction following the development. HYPE traded largely around $62 over the past 24 hours. The token had previously rallied above $75 in mid-June before retreating amid broader market volatility.

Meanwhile, institutional demand for the token appeared to remain strong. Data from SoSoValue revealed that US spot HYPE ETFs recorded more than $108 million in net inflows on June 25, which is the largest single-day inflow since the products launched last month. The inflows came after five trading days in June that recorded no net flows.

The post Hyperliquid Responds After Appearing on Singapore’s Investor Alert List appeared first on CryptoPotato.

Veteran investor Jeremy Grantham thinks the artificial intelligence boom has pushed the U.S. stock market to its most expensive level ever and could eventually lead to a historic decline.

“Based on the value of the stock market compared to GDP, with modifications, this is the most expensive market in American history,” Grantham told CNBC’s “Squawk Box.”

While the GMO co-founder said he wasn’t sure there was a comparable period, the tech bubble of 2000 is the closest analogy. He also highlighted the so-called Buffet indicator, which compares the total value of the U.S. stock market valuation with the size of the economy in terms of GDP.

The market capitalization to GDP ratio referenced by Grantham is estimated to be at 235%, according to Longtermtrends.com. It means that the value of the total stock market is more than two times the size of the U.S. economy.

Legendary investor Warren Buffett used this indicator, saying years ago that when it “approaches 200% — as it did in 1999 and a part of 2000 — you are playing with fire.”

Graham said that, while the timing was terribly uncertain, markets could potentially peak.

Grantham is a famed investor known for his history of calling bear markets and has issued similar dire warnings in the past, including in March 2024.

At the time, he predicted the long-term outlook for U.S. stocks was almost as poor as at any other point in history but the stocks continued to advance after that warning.

“The long-run prospects for the broad U.S. stock market here look as poor as almost any other time in history,” Grantham had said in a blog post released by Boston-based GMO at the time.

Grantham on SpaceX

Grantham also discussed SpaceX following its blockbuster IPO. The stock raced higher in the first few days of trading but has sine lost steam. The investor said that while AI is where investors want to put all their money in, this also creates the conditions for excessive investment.

He pointed out that Amazon shares fell 92% after the dot-com bubble before the company eventually “inherited the earth.”

SPCX 5-day chart

“The long term is complicated, I don’t know, but is it going to have a crash like Amazon? Yes, very likely. And then what happens is indeed it may float away debris on the waves of time, or it will inherit a lot of the market, like Amazon did,” he said.

SpaceX and its roughly $2 trillion valuation, he believes, is another sign of extreme market enthusiasm.

He said historians may eventually view the company’s public-market debut as “one of the defining peaks of all time.”

“It’s the thing you see around the top,” Grantham said.

Securitize, one of the largest providers of tokenization infrastructure for Wall Street, expects to raise about $400 million as it prepares to go public through a merger with a Cantor Fitzgerald-backed special purpose acquisition company.

The company said Friday that, following lower-than-expected shareholder redemptions, the business combination with Cantor Equity Partners II (CEPT) is expected to generate roughly $400 million in gross proceeds, including private investment in private equity (PIPE) financing.

CEPT was 8% higher following the news.

The transaction is scheduled to close on July 1, pending shareholder approval on June 29 and other customary closing conditions. The combined company is expected to begin trading on the New York Stock Exchange the following day under the ticker SECZ.

Tokenization — the process of representing assets such as funds, bonds and private credit on blockchain networks — has become one of Wall Street’s fastest-growing digital asset initiatives. The market for tokenized real-world assets has grown to more than $30 billion excluding stablecoins, according to rwa.xyz, while Boston Consulting Group and Ripple project it could reach $18.9 trillion by 2033.

CEO of OpenAI Sam Altman waves as he speaks with reporters, following meetings on Capitol Hill, in Washington, D.C., U.S., June 3, 2026.

Kylie Cooper | Reuters

The outlook for an initial public offering from artificial intelligence platform OpenAI is changing after a New York Times report said the company may delay a debut on the public market until next year.

So when might the company formally announce an IPO? Traders on prediction market platform Kalshi think it will now arrive early next year.

Speculators say that there’s a 59% chance that an IPO by OpenAI is officially announced by March 1, 2027. Traders place only about one-in-three odds that an IPO is announced before January 1, but think there’s a 73% chance of an announcement by June 2027.

Kalshi considers an IPO confirmed, and thus resolves the contracts to “yes,” if any of the following occur: the Securities and Exchange Commission declares a company’s S-1 form effective, the IPO has an official price or if the company receives a trading ticker.

Previously, OpenAI was widely expected to go for an IPO in 2026, and the company led by CEO Sam Altman confidentially filed to go public on June 8.

The New York Times said SpaceX’s public market debut — the first of what was expected to be several megacap IPOs this year — has made OpenAI’s advisers more cautious. OpenAI has worried that Elon Musk’s company’s initial rally and subsequent fall signals retail investors may have less interest in buying, the report said.

At the beginning of June, OpenAI’s chief rival Anthropic confidentially filed for an IPO. Traders on Kalshi think there’s a 70% chance Anthropic officially announces a public market debut by December.

Key Takeaways

- Singapore’s financial authority flags Hyperliquid for operating without proper licensing credentials.

- The platform maintains it never represented itself as authorized by Singapore regulators.

- Alert listing doesn’t constitute an operational ban or indicate imminent legal action.

- Singapore continues strengthening regulatory framework for cryptocurrency platforms targeting domestic users.

- Despite regulatory spotlight, Hyperliquid maintains position as leading decentralized exchange.

On June 26, Singapore’s financial watchdog placed Hyperliquid on its official Investor Alert List, citing the platform’s absence of domestic regulatory approval. The warning encompasses both the Hyper Foundation’s web presence and its decentralized trading application. Importantly, this designation doesn’t constitute an outright prohibition or signal immediate enforcement measures.

Singapore Authority Issues Public Warning

The Monetary Authority of Singapore maintains this registry to spotlight financial operations lacking mandatory domestic approval. The authority uses this mechanism to identify services that Singapore residents might mistakenly believe are regulated entities. This alert serves to clarify Hyperliquid’s standing under Singapore’s regulatory framework.

The public alert mechanism dates back to 2004, established as a consumer safeguard initiative. Updates occur regularly, incorporating websites, corporate entities, and digital financial platforms. Appearing on this registry doesn’t necessarily imply fraudulent activity or criminal operations.

The designation indicates MAS hasn’t granted Hyperliquid permission to deliver regulated financial services within Singapore’s borders. Consequently, platform users cannot access the safeguards typically provided through domestically supervised financial organizations. No financial penalties or judicial proceedings against the platform have been disclosed by the regulator.

Platform Emphasizes Decentralized Framework

Hyperliquid responded by stating it never portrayed itself as possessing Singapore regulatory authorization. The platform emphasized the alert hasn’t impacted its permissionless operational model. Trading activity continues flowing through its blockchain-based network infrastructure.

The decentralized trading venue enables participants to maintain direct custody of their digital assets throughout transactions. Settlement occurs transparently via blockchain verification mechanisms. The platform contends its architectural design fundamentally differs from conventional centralized financial services.

According to the platform, its broader network will maintain ongoing dialogue with regulatory bodies and institutional players globally. It advocates for transparent regulatory guidelines governing decentralized finance and blockchain trading environments. Nevertheless, Hyperliquid hasn’t revealed intentions to pursue Singapore licensing.

Regulatory Pressure Intensifies Across Crypto Sector

MAS has expanded its alert roster to include multiple cryptocurrency trading platforms. Bybit received the same designation on June 17, joining previously listed exchanges KuCoin and Bitget. These inclusions demonstrate Singapore’s systematic approach toward unauthorized digital currency operations.

During May 2025, MAS mandated that Singapore-domiciled cryptocurrency companies servicing international clientele obtain proper licenses or cease activities. This directive eliminated a regulatory loophole permitting certain operators to bypass domestic approval requirements. The authority emphasized it had communicated this regulatory stance consistently since 2022.

These enforcement measures connect to enhanced consumer safeguards and strengthened financial crime prevention protocols. The regulator also aims to better harmonize with global anti-money laundering frameworks. Cryptocurrency enterprises based in Singapore now confront more demanding licensing requirements.

Exchange Sustains Leading Industry Status

Hyperliquid continues ranking among the most prominent decentralized trading venues notwithstanding regulatory attention. According to CoinGecko metrics, it holds ninth position among decentralized exchanges measured by transaction volume. DefiLlama data suggests the protocol secures approximately $5.7 billion in total value locked.

The venue concentrates primarily on perpetual futures contracts and additional blockchain-enabled trading instruments. Its architecture merges self-custodial features with high-speed transaction execution. Regulatory authorities may still evaluate how such platforms extend services to users within specific jurisdictions.

MAS hasn’t signaled whether additional measures targeting Hyperliquid will follow. The current alert primarily serves to inform Singapore residents about the platform’s regulatory standing. Meanwhile, the exchange maintains operations through its permissionless blockchain systems.

Surprise: CBS’ ‘Ombudsman’ Has Been A Useless Trump Lackey

Compass Pathways stock hits 52-week high at 14.77 USD

Hyperliquid Enters Singapore’s Investor Alert List

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment6 days ago

Entertainment6 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports3 days ago

Sports3 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech4 days ago

Tech4 days agoMicrosoft accidentally kills epic Outlook email threads

-

Business6 days ago

Business6 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics10 hours ago

Politics10 hours agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics6 days ago

Politics6 days agoAndy Burnham and the meaning of Makerfield

-

Politics14 hours ago

Politics14 hours agoPotential 2028er World Cup attendee leaderboard

-

NewsBeat7 days ago

NewsBeat7 days agoKeir Starmer Allies Question His Chances For No 10

-

Tech20 hours ago

Tech20 hours agoA Look At A Gaggle Of Transputer Boards

-

Crypto World3 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World2 days ago

Crypto World2 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World22 hours ago

Crypto World22 hours agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Business3 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Business7 days ago

Business7 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Crypto World6 days ago

Crypto World6 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Entertainment7 days ago

Entertainment7 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Crypto World7 days ago

Crypto World7 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World6 days ago

Crypto World6 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Tech5 days ago

Tech5 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

You must be logged in to post a comment Login