Crypto World

Miss foreign stock run in 2025? Still market money to be made overseas

After spending most of the past decade being trounced by the U.S. stock market, international equities are back and investing experts say the opportunity should last.

A brutal stretch of underperformance that lasted a decade ended in late 2024 and has sustained its momentum at the outset of 2026. After years of global allocations staying low for most U.S.-based investors because of the weak returns, the recent gains amid shifting macro conditions and growing concerns about U.S. market concentration are leading investors to take another look at the lack of international exposure in their portfolios.

It is not merely chasing hot recent performance, according to Tim Seymour, Seymour Asset Management chief investment officer. “This is not people saying … this is a time to trade global markets,” he said on this week’s CNBC’s “ETF Edge.”

Over the last ten years, global equities outside of the U.S. underperformed domestic markets by a wide margin, with Seymour noting that a major world equities benchmark ETF, the iShares MSCI ACWI ETF (ACWI), underperformed by about 60%. That gap shaped investor behavior and capital flowed into U.S. equities, particularly mega-cap technology stocks. Seymour described it as a generational dynamic among investors in which market capitalization growth in the U.S. “choked off a lot of international investing.”

But he says now the structural underweight that many U.S. investors have to global markets is a tailwind. While international equities represent roughly 30-40% of global market capitalization, Seymour estimates that at the high-end of the range, U.S. investor exposure to overseas markets is 12-15%, and in many cases much lower.

International equities began to outperform the U.S. in November 2024, and since that turn have beaten U.S. equities by roughly 15%, Seymour said. While that does not erase the decade of lagging returns, it marks a meaningful inflection point. “In a 14-month span, you’ve seen international outperform the U.S.” Seymour said. While the ten-year chart versus the U.S. stock market still looks poor, “it really is a story of where global growth has picked back up,” he added.

A popular exchange-traded fund choice among many U.S. investors to gain international exposure is the iShares MSCI Emerging Markets ETF (EEM), which has $26.55 billion in assets and has returned 42% over the past year. The iShares MSCI ACWI ETF is up 20% over the past year, besting the S&P 500’s return by about 5%. Seymour said while the potential returns from emerging markets are higher, investors who are looking to diversify overseas should tilt more heavily to developed market allocations, citing a 70%-30% split as a reasonable example.

Part of the renewed interest in overseas markets is tied to currency. A weakening U.S. dollar has improved returns for dollar-based investors holding foreign assets. Meanwhile, metals have surged as investors look for stores of value, an investing development that Seymour described it as a global trade rather than a U.S. only phenomenon.

“These are all providing tailwinds and a weakening dollar, of course, where this is leading investors to diversify their overall portfolios that had been previously U.S.-centric portfolios,” Jon Maier, J.P Morgan Asset Management chief ETF strategist, said on “ETF Edge.”

Seymour said the most important point for investors to understand when considering the additional of international stocks to a portfolio is that the fundamentals are improving. Earnings growth is appearing in places where stagnation once defined the outlook. Japan is a key example, he said, where years of corporate governance reform and shareholder focus is starting to boost returns.

Europe is also benefitting from lower interest rates, fiscal spending, and regulatory change. Seymour argued that deregulation in Europe may be a more powerful catalyst than similar efforts in the U.S. because it represents a sharper shift from the past. Banking, utilities, and industrials have all seen renewed momentum. He added that in additional to a decade of underperformance making these stocks cheap on a relative basis, many European banking stocks will benefit as much from central bank policy as U.S. banks and are better dividend plays, such as Barclays, Santander and SocGen.

Maier echoed this general view, saying that “developed international markets are certainly areas of interest to our clients.”

International markets also offer exposure to recent winning trades, including precious metals. Latin America has been one of the strongest performing regions this year, driven by gold and copper. Seymour said Chile and Peru are examples of international markets benefitting from rising commodity demand. Meanwhile, Brazil has gained on both commodity strength and shifting political expectations.

“Brazil’s the largest economy in Latin America,” Seymour said. “Some of this are the dynamics around commodities, but some of these are the dynamics around the geopolitics.”

The iShares MSCI Brazil ETF (EWZ), which has $8.91 billion in assets, is up almost 49% over the past year, while the iShares MSCI Peru and Global Exposure ETF (EPU) is up almost 118% during the same time period.

The dollar and metals trades came under pressure on Friday after President Trump announced Kevin Warsh as his pick to succeed Jerome Powell as Fed Chair, with market belief in Warsh as figure who will maintain Fed independence rather than force rates down at the president’s bidding. Gold, silver and platinum all crashed. However, these metals have seen enormous returns over the past year, with gold up over 90%, silver up roughly 200%, and platinum up 120%.

Market strategists say Trump administration global policies will continue to serve as longer-term tailwinds for international-themed trades. “Whether it is India and the EU cutting a trade deal or Canada cutting oil deals with China, the rest of the world is repositioning,” Seymour said.

Technology leadership is another trade where investors are reassessing the balance between U.S. and overseas holdings. Seymour highlighted South Korea as example, noting the country’s market is heavily weighted toward memory chip leaders like Samsung and SK Hynix, which make up around 46% of the South Korean stock market benchmark tracked by the iShares MSCI South Korea ETF (EWY), which is up 125% over the past year. “Memory has been on fire,” he said, making country level ETFs a practical way to gain exposure. Apple said on its earnings call on Thursday it can’t secure enough chips for iPhone demand, another sign supporting the strength of the memory trade.

Seymour noted other companies that are among the biggest chip players in the world, ASML and Taiwan Semi, also reside outside U.S., and there are many data center plays overseas as well.

The renewed interest in international equities reflects broader reallocation after years of neglect. Investors are responding to valuation gaps, earnings growth, and a world where capital and trade are increasingly multi directional. “These are global trades, not just U.S. trades,” Seymour said.

Michael Saylor has hinted his Bitcoin treasury firm is back on track with its weekly Bitcoin purchases after taking a rare week off at the end of March.

In an X post on Sunday, Saylor shared a screenshot from StrategyTracker with the caption “Back to Work.” He often posts the chart ahead of purchase announcements.

The firm took a week off from buying BTC at the end of March, breaking its weekly buying streak for the first time this year. The firm’s last purchase was reported on March 23, buying about $77 million worth of BTC at $74,326 per coin.

One of the main avenues Strategy uses to fund Bitcoin purchases is via the sale of its perpetual preferred stock, Stretch (STRC). The stock is designed to generally trade around its par value of $100, which is aided by a monthly dividend adjustment mechanism.

Related: Bitcoin and the US dollar have a ‘symbiotic’ relationship: BPI exec

Strategy issues new shares of STRC and then allocates the proceeds generated from the market into Bitcoin buys.

According to estimates from STRC.LIVE, Strategy could be set for a purchase of at least 1,821 BTC based on funds raised for the week ending April 3.

Despite the week off, the firm is showing no signs of slowing down. In late March, Strategy announced plans to raise $44.1 billion to fund BTC purchases primarily via the selling of its common MSTR shares and STRC.

According to Strategy’s website, the firm has acquired a total of 762,099 BTC for an average cost of $75,694 per coin. At current prices of about $69,100, Strategy’s holdings are in the red overall.

However, Bitcoin is in the green over the last month, increasing by 1.2% over the past 30 days, according to data from CoinGecko. The price is still down 20.9% year-to-date amid geopolitical tensions and a challenging macro climate.

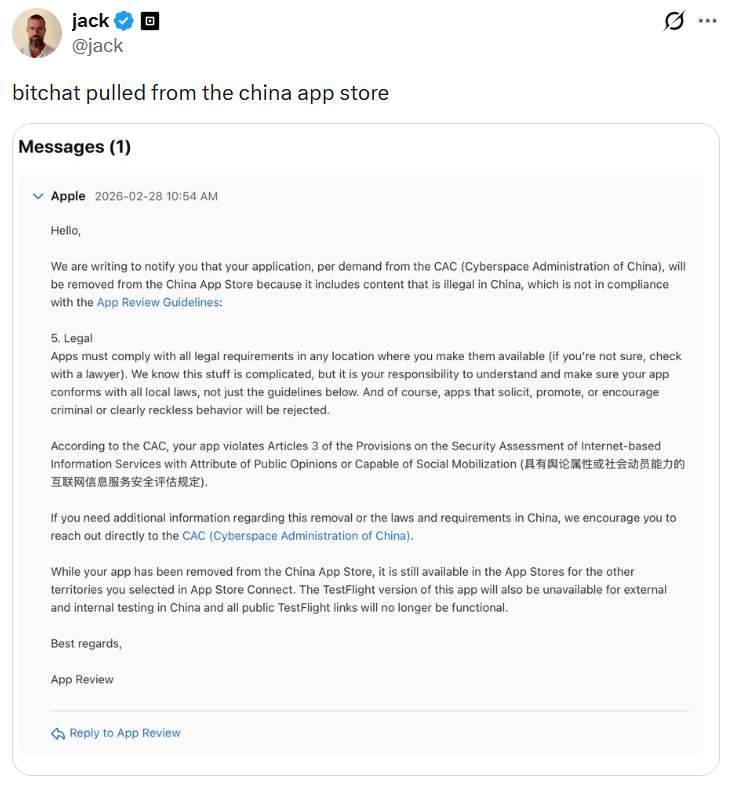

Bitchat, a decentralized peer-to-peer messaging app developed by Block CEO Jack Dorsey, has been removed from Apple’s App Store in China for allegedly violating its internet service regulations.

In an X post on Sunday, Dorsey shared a screenshot from Apple’s app review team informing him that Bitchat had been removed from the App Store in February and that the TestFlight beta version would no longer be available in China at the request of the Cyberspace Administration of China (CAC).

“Bitchat pulled from the China App Store,” he said.

Bitchat has seen its popularity rise during protests in Madagascar, Uganda, Nepal, Indonesia and Iran in recent months, as governments attempted to shut down regular communication channels and internet access to curb dissent.

The peer-to-peer encrypted messaging service runs entirely over Bluetooth and mesh networks and operates without an internet connection, which could put it at odds with China’s internet-censorship-prone regime.

Bitchat violated internet regulator’s provision

The CAC argued Bitchat violated Article 3 of its regulations governing online services with public opinion or social mobilization capabilities, which came into force in 2018.

Under the provisions, any online services that could influence public opinion or enable social mobilization are required to conduct a security assessment before launch and “be responsible for the assessment results,” according to a Google Translate version of the regulations.

The app review team also said all apps on its store must comply with local requirements in the countries where they are available.

Related: Dorsey shares AI-integrated workplace vision weeks after Block’s 40% staff cut

“We know this stuff is complicated, but it is your responsibility to understand and make sure your app conforms with all local laws, not just the guidelines below. And of course, apps that solicit, promote or encourage criminal or reckless behavior will be rejected,” they added.

Still available in other countries

Despite being pulled in China, Bitchat remains available in other countries, according to Apple’s app review team.

Chrome download stats show the app has been downloaded more than three million times, with more than 92,000 in the past week. The Google Play Store has recorded more than one million registered downloads.

However, neither specifies which regions were responsible for the bulk of downloads.

By comparison, WeChat, developed and operated by Tencent, one of China’s largest tech companies, has an estimated 810 million users in China, out of a national population of more than 1.4 billion.

Magazine: Bitcoin may take 7 years to upgrade to post-quantum — BIP-360 co-author

Xandeum, a scalable, smart contract-native storage layer for Solana, has officially launched STOINC (Storage Income) on mainnet.

With STOINC now live, Xandeum introduces a usage-driven, on-chain storage economy, enabling applications, node operators, and the broader network to participate in value creation tied to actual storage demand.

Unlike traditional reward mechanisms that rely on token emissions, STOINC is powered by actual storage usage. Every interaction with the Xandeum storage layer generates fees that are collected and distributed across the network.

At the end of each cycle, storage fees are distributed across the Xandeum network economy, rewarding pNode participation, supporting staking incentives as they come online, and funding continued ecosystem growth.

“Storage must become a first-class citizen in Web3,” said Bernie Blume, Founder of Xandeum. With mainnet live and community pNodes already online, STOINC marks the beginning of a usage-based storage economy designed to support the next generation of storage-enabled dApps on Solana. “With STOINC, we’re moving beyond theory into real usage, where storage activity directly translates into economic value.”

The launch addresses a key limitation in blockchain infrastructure: scalable, native storage for smart contracts. By enabling this, Xandeum supports a new category of applications known as storage-enabled dApps (sedApps).

Upcoming developments include XAND staking to pNodes, deployment of native applications, and expansion into enterprise use cases.

As Web3 evolves toward real-world utility, scalable storage becomes critical infrastructure. STOINC positions Xandeum as a key player in this transition, where usage drives value creation.

About Xandeum

Xandeum is building a scalable, smart contract-native storage layer for Solana, enabling decentralized applications to access large-scale storage with seamless integration.

The post Xandeum Launches STOINC on Mainnet, Introducing Usage-Based Storage Income for Web3 appeared first on BeInCrypto.

A familiar voice is back with a familiar, and controversial, call on bitcoin .

Mike McGlone, senior commodity strategist for Bloomberg Intelligence, is reiterating that bitcoin could crash to $10,000.

But this time, he’s framed it with a very clear line in the sand: $75,000.

If bitcoin decisively reclaims and holds that level, the bearish thesis breaks. If it can’t, McGlone’s view is that the path of least resistance is sharply lower, with prices falling all the way to $10,000, the level last seen in early 2020.

The $10,000 magnet

McGlone’s uber bearish forecast of a crash to $10,000 isn’t new. It’s been circling for weeks, and it is based more on market structure than short-term catalysts.

The cryptocurrency spent a long stretch hovering around $10,000 before the massive wave of fiat liquidity hit the markets following the coronavirus-induced 2020 crash. That era of zero rates, stimulus checks and aggressive liquidity easing by central banks torched unprecedented risk-taking across all corners of the financial markets. It played a major role in lifting BTC permanently above $10,000.

“Before the biggest money pump in history in 2020-21, Bitcoin hovered around $10,000, and it may be reverting. Roughly $10,000 is also the first-born crypto’s most traded price since 2017, when futures were launched,” McGlone noted on LinkedIn.

With that era of abundant liquidity now behind us, McGlone suggests that bitcoin may revert to what he considers its equilibrium price — around $10,000.

According to him, $10,000 has been the most heavily traded price zone since 2017, when the CME futures began trading. In other words, $10,000 isn’t just a round number — it’s where a huge amount of historical volume sits.

McGlone also points to the crypto market’s explosive growth as a potential drag on bitcoin. In 2017, bitcoin largely defined the space, but today, millions of tokens compete for attention and drain capital away from the industry leader. In his view, that surge in supply has become a structural headwind rather than a tailwind.

“Unlimited crypto supply and use-case rivals are Bitcoin headwinds,” McGlone said on LinkedIn, adding that stablecoins represent “the most enduring trend” in crypto. He expects ether to become bigger than ether and eventually bitcoin.

“I expect the ‘flippening’ to continue, with Tether’s AUM topping Ethereum in 2026 and eventually Bitcoin,” he said.

The $75K invalidation level

McGlone’s bearish forecast hinges on prices staying below $75,000. This level has been a major turning point for market trends over the past 12 months. The March-April 2025 slide ran out of steam at around $75,000, while the early 2024 rally stalled there. Furthermore, $75,000 corresponds to key Fibonacci retracement levels.

Think of it as a market verdict threshold. A sustained move above it would suggest that bitcoin has re-established strong structural demand, ending the downtrend that began at October highs above $126,000. It would imply that institutional flows, macro conditions, or both are strong enough to override his reversion thesis.

Fail to get there — or get rejected again — and the argument flips: bitcoin may still be trapped in a longer-term decline to $10,000.

Franklin Templeton is setting up a standalone cryptocurrency division by acquiring 250 Digital, a firm spun off from venture capital outfit CoinFund earlier this year.

The $1.7 trillion asset manager is making its boldest digital-asset move yet, targeting pension and sovereign wealth funds.

What Franklin Templeton Is Building

The unit will operate under the name Franklin Crypto. Christopher Perkins and Seth Ginns, both former CoinFund executives, will run day-to-day operations. Sandy Kaul, who leads innovation at Franklin, will oversee the group.

Franklin has been in crypto since 2018 and currently employs more than 50 digital asset specialists. The firm already offers a bitcoin ETF and runs a tokenized money-market fund on Binance. This acquisition shifts its strategy from passive products toward actively managed institutional offerings.

Timing matters here. Bitcoin has shed roughly 45% since crossing $126,000 last fall. About $2 trillion has evaporated from total crypto market capitalization. Franklin’s leadership appears to view the downturn as a window to consolidate talent and build infrastructure cheaply.

Paying With Tokens

Perhaps the most unusual aspect is the payment structure. Franklin will use BENJI tokens, backed by its blockchain-based government money fund, to cover part of the purchase price. That makes this one of the first corporate acquisitions partially settled on-chain.

The deal should close by mid-2026. No financial terms were released.

The post Franklin Templeton Launches Crypto Unit Amid Market Slump appeared first on BeInCrypto.

Crypto World

New Crypto: Pepeto Hits $8.68M Racing Past Shiba Inu Numbers While Ethereum Price Prediction Eyes $10,000

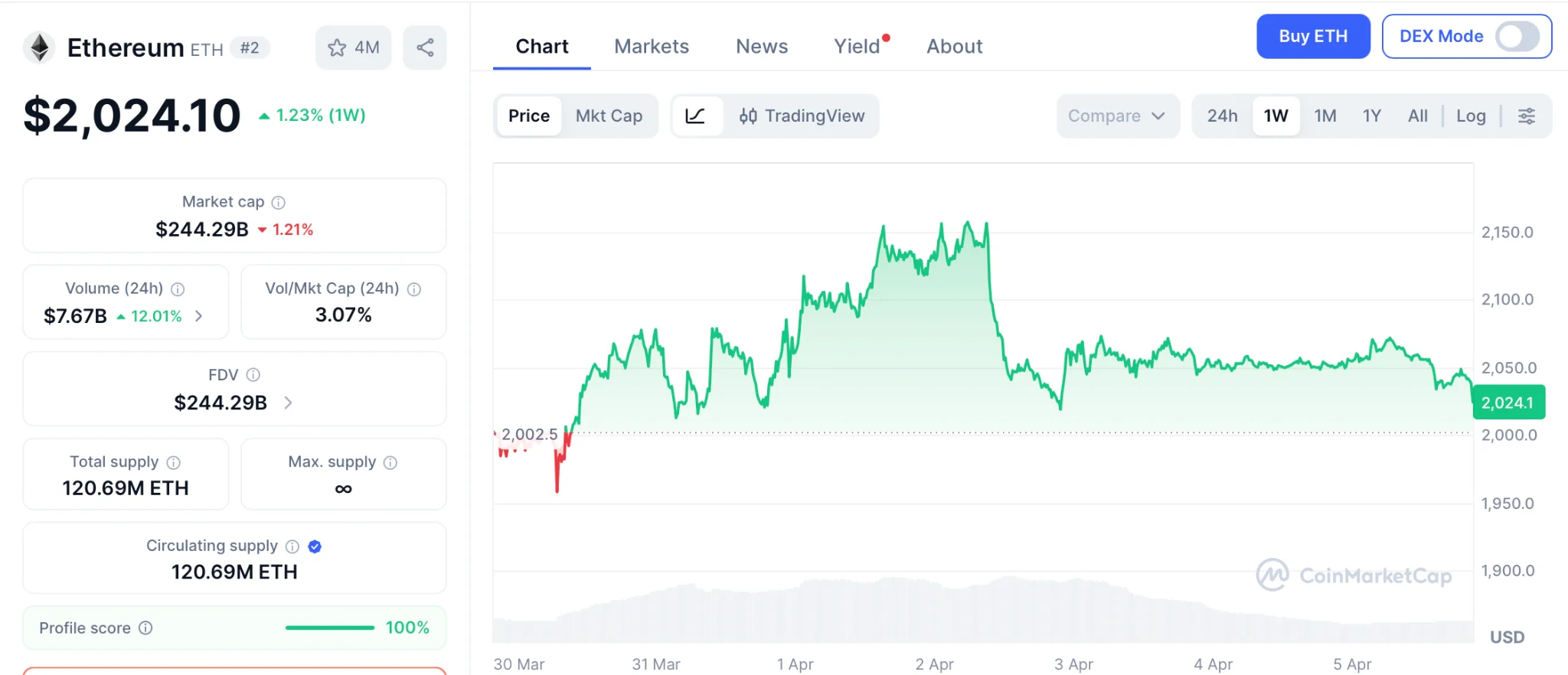

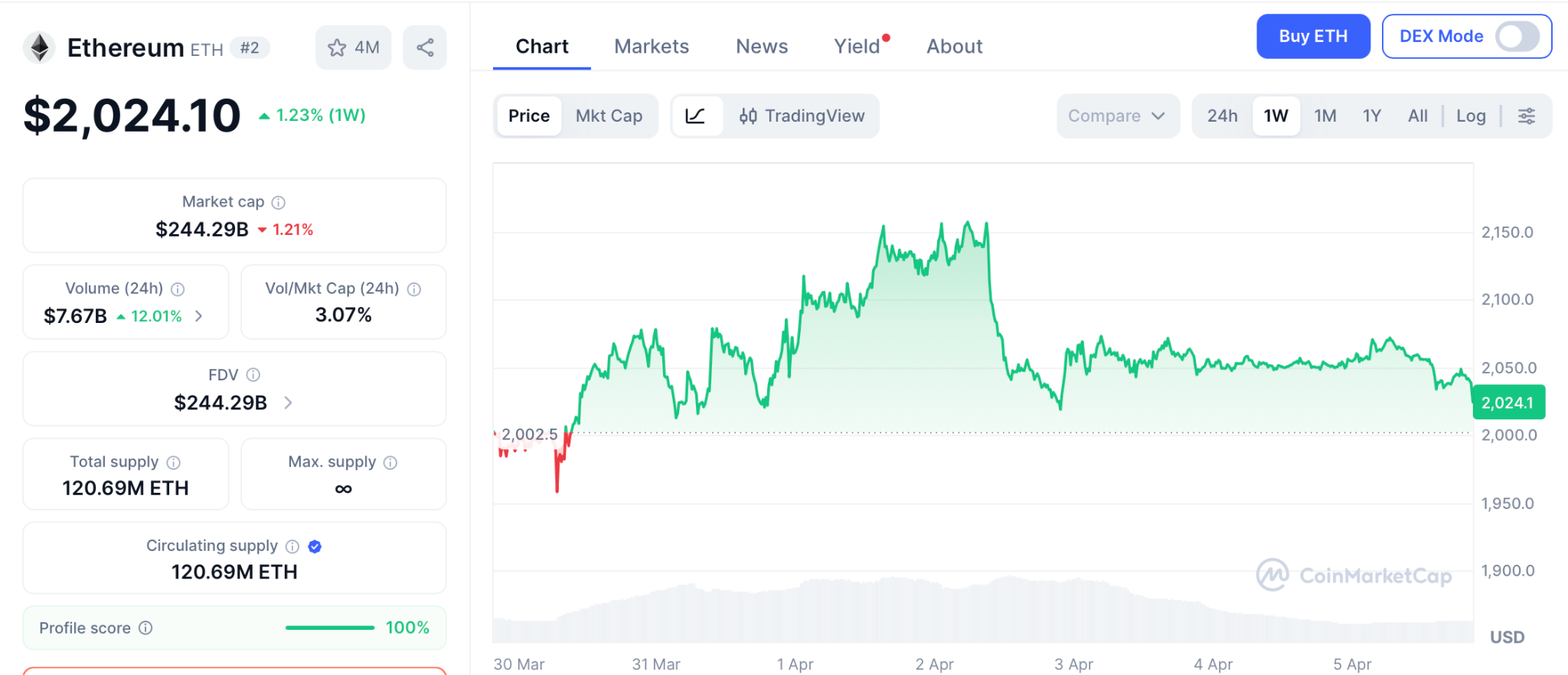

The ethereum price prediction keeps drawing attention as ETH sits at $2,024, down 58% from its $4,953 high. Standard Chartered holds a $7,500 year-end target, and Arthur Hayes projects $10,000 to $20,000 before this cycle ends. Over 30% of ETH supply now sits in staking, the Foundation completed its 70,000 ETH target this month, and institutional infrastructure keeps growing.

The best way to understand the opportunity is to examine the ethereum price prediction, look at the path to $10,000, and see why wallets are rushing into Pepeto before the listing closes the window. Pepeto is built on Ethereum with the goal of solving the problems that still limit the network, and the presale just crossed $8.68 million at a pace that mirrors what Shiba Inu did before its breakout.

Ethereum trades at $2,024 on April 5 after snapping a six-month losing streak in March, per CoinMarketCap. The Foundation locked $143 million in ETH into staking instead of selling, cutting one of the biggest sources of sell pressure in the market, per CoinDesk.

The ethereum price prediction sits on the $2,000 level. Holding it opens $2,500 and then $3,000. Standard Chartered holds $7,500 for year end, and Hayes calls for $10,000 to $20,000 before the cycle peaks.

At $10,000, ETH’s market cap would reach roughly $1.2 trillion, a level that needs strong post-halving dynamics and broad macro recovery but sits within reach if institutional adoption continues at this pace. With 30% of supply staked and the Foundation no longer selling, the structural case for higher prices keeps improving.

That long-term direction benefits Pepeto directly. On-chain data shows that several of the biggest presale buys trace back to ETH whale wallets, addresses that know this blockchain inside out.

New Crypto Pepeto Fixes Ethereum Pain Points With Exchange Tools Built by Experts

Pepeto targets the problems draining Ethereum wallets every day. Ethereum gas fees eat into small trades before they even fill. Pepeto built an exchange layer that processes trades inside the protocol so traders pay zero fees.

PepetoSwap handles every swap at zero cost using the way Binance powers its ecosystem with BNB, where the token drives the engine.

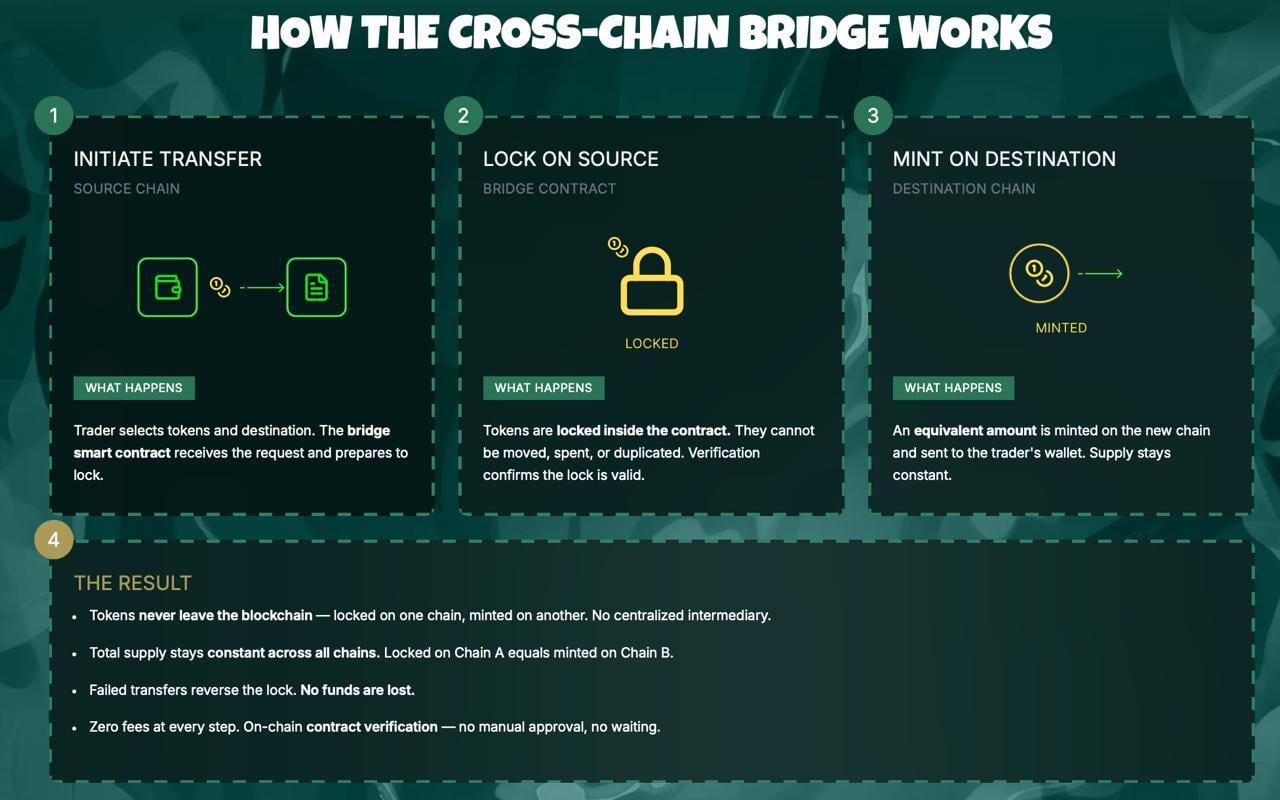

The cross-chain bridge moves assets between Ethereum, BNB, and Solana at zero cost, so holders across chains combine positions without losing capital. The contract scanner checks every token before capital commits, catching traps that cost users $1.3 billion in 2025.

SolidProof verified the full codebase, a former Binance executive shaped the platform, and the founder who took the original Pepe token to $11 billion on a 420 trillion supply designed the entire exchange. Staking at 188% APY compounds positions while the listing gets closer.

Why Crypto Presales Have Always Produced the Biggest Returns and Where Pepeto Fits

For context, the best example is Ethereum itself. ETH went to market at $0.31 in its presale and climbed to $4,953, converting every $1,000 position into more than $15 million. The wallets that got in at that stage made the returns most investors spend whole careers trying to match, and the only thing behind Ethereum at that point was a whitepaper and a handful of developers.

Pepeto runs a stronger presale setup: $8.68 million in committed capital, the founder of the original Pepe coin and a former Binance executive running the build, with live tools generating real demand for the token from day one. The crypto market today is ten times bigger than the one Ethereum entered in 2015, and reaching just a small fraction of Ethereum’s $233 billion market cap would deliver 100x or beyond from the current entry of $0.0000001862.

The biggest presale winners in crypto history all shared one moment: the crowd was frozen in fear while they quietly loaded, and Pepeto at $0.0000001862 with a Binance listing weeks away is that moment playing out right now.

Conclusion

The ethereum price prediction points to new highs long term, and when ETH rallies, the projects running on its network have historically beaten it every single time. That is exactly where Pepeto sits right now. The presale crossed $8.68 million with the Binance listing close enough that stages sell in days, and investors who saw Shiba Inu turn small wallets into millions in 2021 are looking at Pepeto and seeing the same signals.

Presales have always ranked as the highest-return entries in crypto. With ETH proving presale potential at $0.31 to $4,953 and Shiba Inu proving meme coins can deliver massive returns, the data behind Pepeto points to a setup where small entries could produce outsized gains for those who move before listing.

Click To Visit Pepeto Website To Enter The Presale

FAQs

Can Ethereum reach $10,000 based on the ethereum price prediction?

Possible if post-halving momentum and institutional adoption accelerate. $10,000 means $1.2 trillion market cap, realistic by 2027-2028.

Which is the best new crypto presale to buy now?

Pepeto leads with $8.68 million raised, SolidProof audit, Pepe founder, and Binance listing at Pepeto official website.

Where is the ethereum price prediction heading in 2026?

Standard Chartered targets $7,500, Hayes projects $10,000 to $20,000. ETH must hold $2,000 for recovery to begin.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

The National Bank of Rwanda (NBR) has warned the public that crypto payments and trades using the local currency remain illegal in the country after Bybit added support for the Rwandan franc for its peer-to-peer platform on Friday.

“Crypto-assets are NOT authorized for payments, FRW conversion, or P2P trading involving FRW under the current framework,” the central bank posted to X on Sunday, urging citizens to avoid crypto due to “serious financial risks and no recourse in case of loss.”

The central bank’s comments were in response to an X post from Bybit on Friday, stating that the Rwandan franc (FRW) can be used to buy and sell crypto through its Bybit P2P service.

In a separate X post, the NBR noted that the FRW “remains the only legal tender in Rwanda” and that “NBR-licensed financial institutions are prohibited from converting FRW into crypto-assets or vice versa.”

Cointelegraph reached out to Bybit for comment but did not receive an immediate response.

Rwanda has been trying to strengthen the FRW’s presence in the country with a central bank digital currency, the e-franc rwandais, which is currently in the proof-of-concept stage and may progress to a pilot phase.

Rwanda is one of many countries that have pushed back against crypto services in an effort to preserve monetary sovereignty and have more control over its financial system, restricting crypto use since 2018.

Incoming crypto regulation seeks to further restrict crypto

However, in March, Rwanda’s Capital Market Authority released a draft framework to regulate virtual asset service providers, a step it said would promote “responsible innovation.”

Related: Taiwan should reconsider Bitcoin reserve in case of war, says think tank

The bill, which is making its way through Rwanda’s legislature, seeks to prohibit crypto as legal tender while banning crypto mining, mixer services and tokens pegged to the FRW.

It also seeks to provide a pathway for crypto service providers to operate under a license and supervision.

Data from blockchain analytics firm Chainalysis shows Rwanda ranks low in crypto adoption during 2024 and 2025, with locals receiving only a fraction of the crypto value seen in higher-adopting African countries like Nigeria and South Africa.

Magazine: What’s a ‘Network State’ and are there real-life examples? Big Questions

Rising Japanese bond yields are quietly draining global liquidity, and Bitcoin is caught in the crossfire.

That’s the core argument from XWIN Research’s latest analysis, which connects Japan’s surging government bond yields to Bitcoin’s sluggish price action.

How Japan’s Bond Market Hits Bitcoin

Japan’s 10-year bond yield recently hit 2.39%, its highest level since 1999. With roughly ¥390 trillion in government bond holdings, even a 1% rise in yields can trigger tens of trillions of yen in unrealized losses for banks, insurers, and pension funds.

These institutions must then shore up their balance sheets. That means selling risk assets and pulling capital home. Since Japan is the world’s largest foreign creditor, this repatriation shrinks liquidity everywhere.

Bitcoin, as a risk asset, depends heavily on global liquidity. History shows it rises during easy-money periods and stalls when rates climb. The current environment fits that pattern.

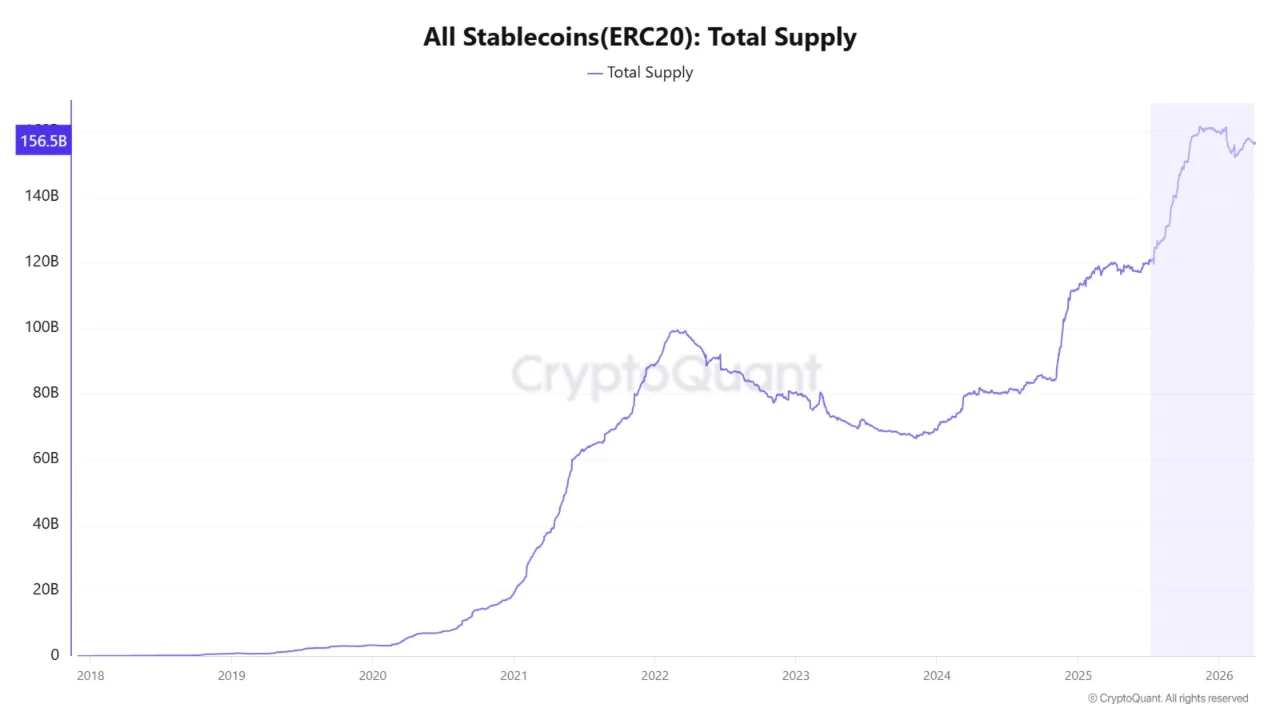

Stablecoin data adds nuance. ERC-20 stablecoin supply has returned to all-time highs, suggesting plenty of sidelined capital exists. Yet that money is not flowing into Bitcoin. Early 2026 saw roughly $9.6 billion exit BTC, with funds rotating into stablecoins instead.

Why This Matters Now

Rising rates do more than create selling pressure. They raise borrowing costs, reduce leverage, and discourage new capital from entering risk markets. The yen’s relative strength also pulls funds away from dollar-denominated assets, including crypto.

XWIN Research argues that understanding Bitcoin now requires looking beyond on-chain metrics. Rates, currencies, and capital flows tell the deeper story.

The post Japan’s Bond Crisis Is Quietly Strangling Bitcoin’s Rally appeared first on BeInCrypto.

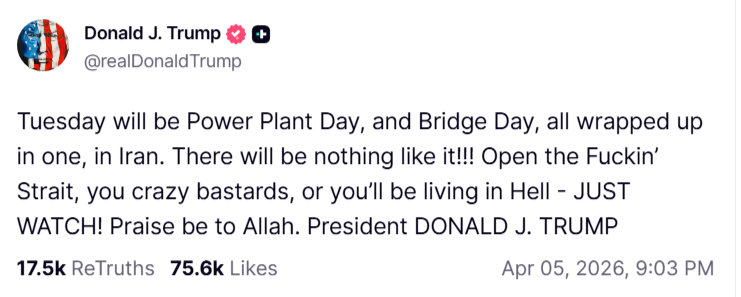

Oil prices extended gains in early Asian trading on Monday as President Donald Trump sharply escalated threats against Iran. He vowed to strike power plants and bridges unless Tehran reopens the Strait of Hormuz by Tuesday.

The latest ultimatum signals that the six-week-old conflict is entering a more dangerous phase with no diplomatic off-ramp in sight.

Trump’s Ultimatum: ‘Power Plant Day, and Bridge Day’

In a social media post, Trump declared Tuesday would be “Power Plant Day, and Bridge Day” and demanded Iran “open the f—ing Strait,” warning Tehran would “be living in Hell.” The unprecedented language signals Washington’s growing frustration with stalled diplomacy over the critical waterway.

Brent crude climbed above $111 a barrel, up 1.9%, while West Texas Intermediate traded near $112 during the Asian morning session. Tehran rejected the demands, and the Strait of Hormuz remains closed to most shipping traffic. The war has triggered a supply shock now threatening to become a full-blown global energy crisis.

Rising oil and fuel prices are stoking inflation, slowing economic growth, and squeezing businesses and consumers worldwide. US gasoline pump prices have risen by roughly $1 per gallon since the conflict began. Analysts expect the March consumer price data on Friday to show the sharpest monthly increase since 2022.

OPEC+ members approved a modest 206,000 barrel-per-day output increase for May after a weekend meeting. However, the move was largely symbolic, as key producers cannot increase output due to the war. Russian supply has also been disrupted by Ukrainian drone strikes on its Baltic Sea export terminal.

Market stress indicators are flashing red. Brent’s prompt spread widened beyond $10 a barrel in backwardation. That gap exceeds peaks seen during Russia’s 2022 invasion of Ukraine. Physical market prices tell an even starker story. Dated Brent surged past $140, reaching levels not seen since 2008.

Diplomacy Stalls as Attacks Continue

Iran has officially told mediators it will not meet US officials in Islamabad, and ceasefire efforts have stalled. Tehran has allowed limited passage through the Strait of Hormuz for select vessels from countries it deems friendly. Iraq received an exemption from Iran’s shipping curbs, though carriers remain cautious about entering the strait. Oman said it discussed options with Tehran to restore shipping flows.

Global buyers are now aggressively bidding for alternative crude supplies from the US Gulf Coast and the North Sea. Israeli strikes continued across Iran over the weekend, while Tehran hit Kuwait Petroleum Corp. headquarters and shut down an Emirati petrochemicals plant.

Asian equity markets opened cautiously. Japan’s Nikkei rose 0.7% and South Korean shares gained 2%. Gold fell about 1% to around $4,630 as surging energy costs undermined expectations of interest rate cuts.

The post Trump’s Hormuz Ultimatum Sends Oil Past $110, Highest Since March appeared first on BeInCrypto.

The Drift Protocol, a Solana-based decentralized finance platform, is drawing renewed scrutiny after a $280 million exploit exposed persistent gaps in its security posture. A post-incident review and commentary from legal counsel frame the breach as something that could have been prevented with basic operational security measures, prompting discussions about civil negligence and the broader risk landscape facing DeFi projects.

Attorney Ariel Givner described the scenario as a failure to safeguard user funds, saying, “In plain terms, civil negligence means they failed their basic duty to protect the money they were managing.” Her assessment followed Drift’s post-mortem detailing how the attack unfolded and how the platform responded. The comments come as critics question the adequacy of Drift’s procedures in a space where attackers frequently rely on social engineering and supply-chain compromises to breach multi-signature setups and other critical controls.

“Every serious project knows this. Drift didn’t follow it,” she said, adding, “They knew crypto is full of hackers, especially North Korean state teams.” Givner continued, “Yet their team spent months chatting on Telegram, meeting strangers at conferences, opening sketchy code repos, and downloading fake apps on devices tied to multisignature controls.”

The debate underscores a larger concern: social engineering and project infiltration remain among the most effective attack vectors in crypto, capable of draining user funds and eroding trust in platforms that users otherwise rely on for high-stakes liquidity and yield opportunities.

Key takeaways

- Drift Protocol is facing scrutiny over basic security practices after a $280 million exploit, with legal perspectives labeling the incident as civil negligence in light of alleged operational shortfalls.

- Experts point to missteps such as storing signing keys on non-air-gapped systems and insufficient vendor and developer due diligence, particularly with personnel encountered at conferences.

- The attackers’ approach reportedly involved months of planning, culminating in targeted social engineering and malware introduced through developer machines.

- There are signals of a possible link to North Korea–aligned threat actors, with Drift stating a “medium-high confidence” that the same group behind the Radiant Capital hack (October 2024) was involved.

- Radiant Capital’s 2024 incident has become part of the narrative tying industry-wide risks to well-known escalation patterns in state-sponsored cyber operations.

Attack narrative and defensive lessons

Drift Protocol published an update detailing how the breach unfolded, asserting that the assault was the product of six months of planning. The attackers reportedly approached Drift at a major crypto industry conference in October 2025, signaling interest in potential integrations and partnerships. Over the following months, the bad actors cultivated relationships with Drift developers, ultimately delivering malicious links and embedding malware that compromised the developers’ machines used to manage the protocol’s multisignature controls.

Drift’s account emphasizes that those involved were not North Korean nationals, though the firm conceded that the threat actors were linked to a broader pattern associated with state-backed cyber campaigns. In a contemporaneous assessment with “medium-high confidence,” Drift tied the incident to actors believed to have previously orchestrated the October 2024 Radiant Capital hack. Radiant Capital had disclosed that its breach involved malware spread via Telegram from an operator posing as an ex-contractor connected to North Korea. While Drift’s update stops short of confirming a direct line of responsibility, these correlations highlight a persistent threat environment in which sophisticated adversaries leverage social channels to compromise engineering workflows.

Legal and security observers highlight a recurring theme: even mature crypto teams can underestimate the risk of supply-chain and social-engineering exploits if governance practices do not enforce strict separation between development activities and sensitive credentials. Givner’s critique goes beyond the specifics of Drift’s incident, pointing to a universal expectation that “air-gapped” signing keys should be kept separate from day-to-day developer work, and that engaging with third-party developers or contractors requires rigorous vetting and ongoing due diligence. In her words, many projects already adhere to these principles because the crypto landscape is “full of hackers,” and a lapse can be costly both financially and reputationally.

Industry context: echoes of a broader security paradigm

The Drift incident arrives as a broader discussion unfolds about how DeFi projects manage risk in a period of heightened adversarial activity. Social engineering, phishing, and malware campaigns targeting developer ecosystems have been repeatedly implicated in high-profile hacks. The Radiant Capital case from late 2024, which involved a North Korea–linked operator impersonating an ex-contractor to disseminate malware, is frequently cited in security analyses as a cautionary tale about the limits of conventional defensive measures when human factors become the weakest link.

Industry observers note that the Drift episode reinforces the need for robust governance frameworks around key management, formal vendor assessment processes, and stringent controls on how and where signing keys are stored and used. If the attackers exploited trusted relationships with developers and relied on compromised devices to gain access to multisignature controls, the path to remediation likely involves reinforcing air gaps, implementing hardware security modules for key management, and institutionalizing continuous monitoring and key rotation practices. The emphasis on “due diligence” also raises questions about how conferences, hackathons, and third-party collaborations are vetted, and whether drift toward more rigorous third-party risk management will become standard practice across the sector.

What this means for investors and builders

For investors, the Drift incident is a reminder that risk management remains a primary driver of platform credibility and capital allocation in DeFi. Projects that can demonstrate resilient onboarding, robust key management, and rigorous vendor scrutiny may distinguish themselves in a market where security shocks can quickly alter perceptions of value and reliability. Builders, in turn, face a delicate trade-off between openness and security. While collaboration and rapid integration are hallmarks of DeFi innovation, the Drift episode suggests that even well-resourced teams must normalize security drills, red-teaming, and clear separation of duties to prevent supply-chain breaches from translating into user losses.

As regulators and industry groups debate standardized best practices, Drift’s experience could accelerate conversations about mandatory security benchmarks for on-chain protocols, particularly those relying on multi-party computation and multisignature frameworks. In the meantime, users should monitor how Drift and similar platforms respond—through security upgrades, partner vetting, and transparent post-incident reporting—as a practical barometer for the sector’s willingness to translate rhetoric about security into measurable safeguards.

Meanwhile, Drift has not publicly detailed its next steps beyond the immediate remediation measures described in its update. The extent to which the platform will overhaul its governance, vendor risk management, and incident response cadence remains to be seen, as does the broader industry adoption of stricter security controls that could alter how quickly and fluidly DeFi protocols can operate with external partners.

What remains uncertain is how quickly the market will react to these revelations and whether Trust signals built on vulnerability disclosure will translate into a longer-term commitment by users to platforms that publicly address security gaps. For now, the incident underscores a recurring lesson: in DeFi, the difference between resilience and ruin often hinges on the discipline with which teams implement and enforce fundamental security practices—before a breach, not after.

As the investigation and remediation continue, market watchers will be paying close attention to Drift’s communications, the evolution of industry security standards, and any subsequent movements by competitors to raise the bar for securing developer environments and signing-key management. The path forward for the sector will be shaped by whether this incident catalyzes meaningful adoption of stronger controls and more rigorous third-party risk governance across the ecosystem.

Michael Saylor Hints at Return to Weekly Bitcoin Purchases

Sanjiv Goenka’s Unmissable Reaction Viral As Mohammed Shami And LSG Tear SRH Apart

iCloud email goes down for some users in an Easter Sunday outage

-

NewsBeat3 days ago

NewsBeat3 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business3 days ago

Business3 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Spanx – Corporette.com

-

Entertainment7 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Crypto World4 days ago

Crypto World4 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business5 hours ago

Business5 hours agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Crypto World6 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Sports1 day ago

Sports1 day agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business4 days ago

Business4 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech6 days ago

Tech6 days agoEE TV is using AI to help you find something to watch

-

Tech7 days ago

Tech7 days agoApple will hide your email address from apps and websites, but not cops

-

Sports6 days ago

Sports6 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Politics6 days ago

Politics6 days agoShould Trump Be Scared Strait?

-

Tech6 days ago

Tech6 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Fashion7 days ago

Fashion7 days agoThe Best Spring Trends of 2026

-

Tech6 days ago

Daily Deal: StackSkills Premium Annual Pass

-

Crypto World6 days ago

Crypto World6 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Sports6 days ago

Sports6 days agoWomen’s hockey camp eyes fitness boost, tactics ahead of WC 2026 campaign | Other Sports News

-

Tech6 days ago

Tech6 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Politics7 days ago

Politics7 days agoBBC slammed for ignoring author of The Fraud

You must be logged in to post a comment Login