Unlock the US Election Countdown newsletter for free

The stories that matter on money and politics in the race for the White House

A man carrying illegal firearms, ammunition and fake passports was arrested near a Donald Trump rally in California on Saturday night in what a local sheriff described as a potential third assassination attempt on the former president.

Law enforcement officers from Riverside County Sheriff’s Department stopped a 49-year-old man from Las Vegas who was driving a black SUV at a security checkpoint close to Trump’s rally in Coachella Valley.

Advertisement

The man was taken into custody after he was found to be illegally carrying a shotgun, a loaded handgun with a high-capacity magazine, ammunition, and multiple fake passports and licences, the sheriff’s office said.

“If you’re asking me right now, we probably did have deputies that prevented the third assassination attempt,” said Chad Bianco, the sheriff of Riverside County, in a press briefing on Sunday evening.

Bianco said the suspect, who was charged with firearms offences before being released, was believed to be a member of the anti-government group Sovereign Citizens. Members maintain that the nation’s laws do not apply to them, Bianco said.

In a statement, the sheriff’s office said the incident did “not impact the safety of former President Trump or attendees of the event”.

Advertisement

Although law enforcement initially named the man as Vem Miller, officials said the man was carrying multiple passports and driving licences bearing different names in his vehicle.

Bianco said Miller’s vehicle was unregistered and carried a “homemade” licence plate. He had driven through a first security perimeter at the rally after claiming he was a reporter, before being arrested at a second. Bianco added that the sheriff’s office was in contact with the Secret Service and the FBI.

The arrest follows two assassination attempts on Trump which have sparked concern that America’s highly polarised election could trigger political violence. It comes as both Trump and Democratic presidential candidate Kamala Harris enter the final weeks of the race, which is all but tied in the polls.

Trump was grazed on the ear by a bullet in July while speaking at an election rally in western Pennsylvania. After ducking behind the podium, the former president stood up, pumped his fist and shouted “Fight, fight, fight” before he was rushed to hospital. Those words have become a potent campaign slogan.

Advertisement

Last month, the Secret Service opened fire on an armed man hiding in the bushes surrounding Trump International Golf Club as the president played, around 300 to 500 yards away. Law enforcement officials found an AK-47-style rifle with a scope in the foliage, along with two backpacks and a GoPro camera.

Earlier this month, Trump’s aides asked for security measures to be stepped up, including military aircraft, special armoured vehicles usually reserved for sitting presidents, decoy aircraft and flight restrictions over his residences.

CHRISTMAS is coming and an ongoing cost-of-living crisis means many families might be worried about affording the festivities this year.

And there is evidence that Christmas is costing more than ever. In fact, according to MoneySupermarket, families spent around £1,800 on their celebrations in 2023.

1

Cute little girl reaches up and carefully places a gold glittery bauble on the Christmas Tree. Festive and warm image with space for copy.

It’s important not to pay more than you can afford, and it’s worth having conversations with your family about what is – and isn’t – within reach.

Advertisement

After all, you don’t need to break the budget to have a good holiday season, and there are plenty of ways to cut back on spending.

But planning is equally important, and with just 11 weeks to go, there are lots of clever ideas that you use can to boost your budget.

We’ve rounded up 15 ways to make some quick cash, to help you cover the cost of Christmas – without breaking the bank.

Sell or rent things online

If you haven’t decluttered in a while, you could be sitting on hundreds of pounds worth of stuff that you don’t even use.

Advertisement

Whether it’s old handsets, clothes that don’t fit anymore, or even that board game someone bought you that you’ve never played, selling things online is a great way to make cash.

Platforms like Vinted and Depop are becoming increasingly popular, and eBay selling is still a great way to get rid of things you don’t want. There are also specialist companies that will buy anything from gold to CDs with very little effort.

Royal London’s Consumer Finance Specialist, Sarah Pennells, said: “This can be a great way to create a bit of extra cash for Christmas. Second-hand selling sites and apps are easy to use and every extra pound will help.”

And Amelia Murray, money expert at Be Clever With Your Cash, added: “We all think of Spring as the time to declutter, but why not do it before Christmas kicks off?

Advertisement

“Take a look around your house for clothing, old mobile phone handsets, books and other things you don’t use anymore to sell online.”

I taught myself to do DIY on TikTok and saved £4.5k on my kitchen upgrade

Francesca De Franco of The Parent Social says that Facebook is also a great platform for selling things you no longer need, allowing you to connect with people in your area.

She said: “You’ll also find many selling pages for specific items/categories such as Mini Boden & Joules Children’s Clothes UK. Additionally, there are sites such as Mazuma for selling old mobile phones or tablets and great general selling sites such as Preloved and Gumtree.”

If you don’t want to sell things permanently, consider renting them out. There are plenty of specialist online services and peer-to-peer lending services that will let loan anything from parking spaces to musical instruments. You could even consider renting out a spare room.

Advertisement

Faris Khatib, CEO of Ideal Tax, said: “Declutter your home by selling items you no longer need or use. Online marketplaces and consignment shops can help you turn unwanted items into cash.

If you have extra space in your home, consider renting it out on platforms such as Airbnb or VRBO. This is a great way to earn passive income.”

Look for lost accounts

There is nearly £89billion in lost and forgotten pensions, bank accounts, premium bonds and even child trust funds.

According to data from finance firm Gretel, the average amount “lost” is £3,000.

Advertisement

Finding an old account can be a great way to put some extra cash towards Christmas, whilst also boosting your overall finances. Gretel helps customers track down lost money in less than three minutes and then reclaim it.

*Gretel’s updated figures for the UK’s lost assets by sector

Financial Product

Total lost/dormant

Estimated total volume

Average account value

Pensions

£64,750,000,000

2,800,000

£23,125

Bank & Building Society Accounts

£4,500,000,000

14,000,000

£321

Child Trust Funds

£5,755,050,000

2,646,000

£2,175

Securities

£2,500,000,000

2,000,000

£1,250

Investments & Wealth Management

£2,800,000,000

1,000,000

£2,800

Life Insurance

£8,115,311,795

3,409,795

£2,380

NS&I

£81,025,600

2,324,683

£35

Total

£88,501,387,395.00

28,180,478

£3,141

Take advantage of cashback

Cashback is a great way to boost your finances throughout the year, and there’s still plenty of time to make a few extra quid before Christmas.

Even better, if you take advantage for your planned Christmas spending, you’ll earn a little extra money to get January off to a good start too.

There are a few different options to consider. Some debit and credit card providers offer cashback schemes with certain retailers, so check whether your bank or building society does this.

Advertisement

Meanwhile, dedicated cashback credit cards often reward you with a set percentage of cashback every time you shop. However, you must make sure you pay off the full balance in full each month, or you could rack up more in interest charges than you earn.

Finally, there are dedicated cashback apps and websites that can track your online purchases and reward you with a percentage of your spending as cashback.

For example, if you buy something for £100 and the provider offers 5% cashback, you’ll pocket £5 credit. Once you’ve earned enough, you can withdraw it as cash, gift cards or vouchers.

Liz Hunter, director at Money Expert, said: “Imagine getting paid to do your Christmas shopping – sounds good, right? Well, with cashback websites and apps, you can earn money back on every Christmas present you buy.

Advertisement

“It’s a win-win. Save money on your Christmas shopping and keep the savings going into the New Year and beyond. The two biggest platforms in the UK are Topcashback and Quidco”

Switch bank accounts

Switching bank account is one of the quickest and easiest ways to make over £100 for very little effort.

Currently, the most you can get is by switching to Lloyds, which will pay you £200 for becoming a new customer.

The bank is also offering a choice of rewards between 12 months’ Disney+ with ads, six cinema tickets, a Coffee Club & Gourmet Society membership, or a subscription to a magazine.

Advertisement

You need to switch to one of Lloyds’ Club accounts. The cheapest one is Club Lloyds, which costs £3 per month unless you transfer in £2,000 per month.

The account gives you access to a regular saver paying 6.25% fixed interest for a year. The maximum you can pay in is £400 a month, which will net you £161 in free interest over the twelve months.

Meanwhile, First Direct is offering £175 to switchers along with a 7% regular saver and free overdraft worth £250.

Nationwide is also offering £175, which comes with 5% interest on balances up to £1,500 as well as 1% cashback for a year (to a maximum of £5 a month)

Advertisement

The Co-op bank offers an initial £75 to switch, plus £25 a month for three months – which brings the total to £150.

To get the additional payments, you need to have deposited £1,000 or more, set up at least two Direct Debits, registered for digital banking, added the debit card to a digital wallet and made at least 10 transactions – and this all needs to happen within 30 days of the switch completing.

Make the most of referrals

Several financial products including bank accounts, investment platforms, and credit cards provide referral bonuses.

Shops will often also do this, giving you free cash to spend in-store in return for sending them new business.

Advertisement

For instance, both Monzo and Paypal will give you £5 if you refer a friend and Snoop will give you a £5 Amazon voucher.

American Express have some of the most generous referral programmes out there.

The bank says you can earn up to a maximum of 90,000 Avios, Membership Rewards, Nectar Points or bonus points per calendar year. You can earn up to £150 cashback per calendar year if you hold a cashback product.

Check with your utility providers too. For instance, Octopus Energy will give you £50 for making a referral.

Advertisement

Make sure you don’t annoy your loved ones by pestering them with links, but if you know someone is looking to make a switch or use a particular shop, they’ll often get a discount too by using your referral code.

Do online surveys

Online surveys and market research can be a nice little earner, but you’ll usually have to put a bit of effort in to complete enough to get any meaningful money.

De Franco said: “There are plenty of companies willing to pay you for your views and feedback about brands or for telling them about your shopping habits, or even your personal and social habits!”

YouGov is one of the better-paying sites. For every 5,000 points you amass, you’ll get £50. Generally, you can expect to get around 50 points for a 15-minute survey.

Advertisement

Check for supermarket points or vouchers

Plenty of us spend the year using our Tesco Clubcard, Nectar card, and Boots loyalty card, but if you’ve not checked your balance recently you might have valuable points to spend.

This can be a great way to cut the cost of Christmas, either by spending those points in-store, or – where allowed – spending them with partner retailers to boost their value.

Murray said: “Have a think about where you may have built up little pots of cash, such as in cashback or points… You may also have some gift cards left in the back of your wallet or your inbox, and it is better to spend them soon rather than wait until they expire.

“These extra bits of cash can help to boost your Christmas spending.”

Advertisement

Ban Mahsoub, spend and save director at Tesco Bank added: “Many retailers have offers or loyalty schemes for customers to receive discounts and rewards for shopping with them, so it’s worth looking at what’s available or whether you have any points to redeem.

“If you haven’t already, then it’s worth signing up now, especially as there may be extra incentives for new joiners to collect extra points.”

Look at supermarket saver schemes for a free extra bonus

Lots of supermarkets offer savings clubs that allow you to stash cash for Christmas, in return for some bonus cash.

Often, these clubs won’t pay as much as a top savings account but there is a clever hack that means you can get the best of both worlds.

Advertisement

Many of the schemes will calculate your bonus based on how much money you have put in the scheme by a specific deadline. So, that means you can put your money in the top paying easy access you can find, and then transfer it across right before the final date for an added boost.

Some banks and building societies are paying up to 5% on easy-access accounts, which can give you a nice little boost before Christmas. If you’ve got spare money in your bank account or in an old savings account, you might only be earning a fraction of that.

Pennells said: “Just remember that if you’re transferring a cash ISA for a better rate, you need to be mindful that some products don’t accept transfers in and money you move could count against your current year’s tax allowance – so pick your new account and transfer carefully. If you close your cash ISA and switch into a non- ISA product you will lose the tax benefits.”

Advertisement

Get rid of old lego

If your children are growing up and you’ve got a house full of Lego, getting rid of it could be a great way to declutter and make some money. Even if you’ve sets with pieces missing you can still sell them on.

De Franco explained: “Sites such as musicMagpie buy old LEGO by weight, so no need to worry about complete sets. You can sell anything from 500g up to 10Kg.

“Just put your LEGO bricks into a plastic bag and seal/tie it.

“Then, weigh and round up to the nearest 500g (0.5Kg) and select the weight from the dropdown. You’ll get an instant quote and you can send it for free. Then sit back and receive a same-day payment.”

Advertisement

Recycle old clothes

If you’ve got clothes that aren’t fit for selling online, you might still be able to make money by recycling them, whilst also doing your bit for the planet.

For instance, H&M has an in-store garment recycling service, which accepts clothes by any brand, in any condition. It promises that the clothes you donate will be used and won’t end up in landfill and for each carrier bag full you’ll get a £5 voucher to spend at the store.

De Franco said: “M&S has an initiative in place with Oxfam. Donate any item of M&S-labelled clothing or soft furnishings to the charity store and you’ll receive a £5 voucher for Marks & Spencer, which you can use at any participating store when you spend £35 or more.”

Find out where money is slipping through your fingers

New research from Citizens Advice has found that over 13 million people (26% of UK adults) have accidentally taken out a subscription in the last 12 months.

Advertisement

These subscriptions cover services from fitness apps to food delivery services and repeat pet food to magazine subscriptions.

Scouring your bank statements can be a great way to generate cash savings. Simply check your bank and credit card statements and look for unexpected direct debits and standing orders. Check whether you’re in contract, and if not cancel – and save some quick cash.

Proactively track your energy bills.

As the nights turn colder, finding ways to reduce unnecessary energy spending can be a great way to cut bills, but Pennells also says that now is a good time to find a cheaper tariff.

She said: “Energy providers are beginning to offer new deals following a period of high tariffs when there was little opportunity to switch. Energy is one of the biggest bills for many households, any savings can go a long way.”

Advertisement

See if you can get benefits or grants

Policy in Practice estimates that the total amount of unclaimed income-related benefits across Great Britain is now £22.7 billion a year. Claiming what you’re owed could get you hundreds or even thousands of pounds extra a year.

Ms Pennells said: “There are billions of pounds unclaimed in state benefits and you could be one of those missing out.

“These days it’s easier than ever to find out what state benefits you could claim. The charity Turn2us has a free-to-use benefits calculator and grant search tool on its website.”

A quick way to pool money is to see what foreign cash you may have lying around at home.

Despite the rapid rise of card and mobile phone payments, most people still use some notes and coins when they travel abroad – to pay for an emergency taxi or an unexpected round of drinks.

Research by Leftover Currency found that this forgotten holiday money amounts to a staggering £2.7billion across the UK, which could be exchanged back into sterling and provide a welcome boost for any Christmas savings.

The £2.7billion figure would give each of the 40.5million 18- to 64-year-olds in the UK £66.67 in their pockets.

Advertisement

Mario Van Poppel, founder and owner of Leftover Currency, said: “People are often very surprised to discover the value of the notes and coins they have tucked away.

“The good news is even the out-of-date currencies that are no longer legal tender can be easily exchanged and boost your bank account.”

Top tips for selling on eBay

NEW to eBay? It’s head of secondhand, Emma Grant, reveals how to optimise your listings:

Advertisement

Use key words – eBay automatically filters listing titles for key words, so it’s crucial to use the terminology people search for – especially brand and product names.

Choose the right category for your product – It might sound obvious but it’s important to always choose the most specific category to sell in.

Pictures are important – Most users will not bid on items they cannot see. For best results, take photos in natural light against a neutral background and be honest about any scratches or damage to the item.

Be as detailed as possible – Be honest about the condition of the product and be sure to note any wear and tear.

Look at past sold items– eBay has a function that allows you to search for the item you want to sell and then filter the results by sold items. Here, you can view the price the item has sold for and get insight into how others have listed it.

Selling Sundays – Get the timing right. The busiest time for buyers is Sunday evenings, so schedule your listings to end around that time. Opt for seven-day auctions to ensure the max number of bids. The longer your item is listed, the more chance of people seeing it, so unless it’s time-sensitive, pick seven days. December is the busiest month on eBay.

Be realistic with pricing – Try searching for similar items on eBay, to make sure you’re going for the right price and always ask yourself “would I pay this price for this item?”

Donate to charity – When listing your item, consider donating a percentage of the sale to a cause of your choice – from 10% to 100% – you can donate the funds raised from your item straight from the platform.

Welcome to FT Asset Management, our weekly newsletter on the movers and shakers behind a multitrillion-dollar global industry. This article is an on-site version of the newsletter. Subscribers can sign up here to get it delivered every Monday. Explore all of our newsletters here.

Does the format, content and tone work for you? Let me know: harriet.agnew@ft.com

Hi! Me again, filling in while my esteemed colleague Harriet Agnew seeks a little autumn sunshine, of which I’m definitely not jealous at all. No, it’s fine, really. My own little stream of consciousness on the asset management industry this week spans AI, CIOs and the CIA, and some OATs for good luck, so if alphabet soup is your thing, read on.

One thing to start . . .

Advertisement

“Our strategy is ambitious, and our strategy is working,” BlackRock CEO Larry Fink said of the asset manager’s earnings on Friday. It’s hard to argue. Assets under management surged to an all-time high of $11.5tn last quarter, reflecting a rally in markets but also record inflows of new cash from investors, which helped push revenues up 15 per cent to $5.2bn, surpassing analysts’ expectations.

In today’s newsletter:

CIOs, coming to a desktop near you

Super diligent due diligence

Le spread

The AI disruption coming for CIOs

Fund managers are generally very good at talking about artificial intelligence as an investment theme. At the drop of the hat, asset management executives and portfolio managers can rattle off a list of industries and functions ripe for robotic disruption. The same people are, however, generally pretty bad at articulating how it will affect them. “Er, I think the customer service department uses it?”

One intriguing application of the newfangled technology comes from German investment house DWS and its chief investment officer, Björn Jesch.

Advertisement

Jesch is a cheerful soul, which he puts down to being from Düsseldorf. I did not previously know this city had a reputation as Germany’s Fun Central but every day’s a school day. For all his cheerfulness, though, he can’t be in more than one place at once. He posts his daily markets notes on LinkedIn, he writes the outlook pieces, he talks to colleagues and clients, and puts up with annoying phone calls from journalists like me seeking to figure out the state of stocks and bonds. Now, he says, AI is going to help him be everywhere all the time.

He tells me DWS is launching a podcast, in his voice, talking about markets, but without him having to make a recording. Instead, AI will “read” his daily CIO notes in his voice, first of all in English and later in other languages too. Further down the line, another possibility is a desktop avatar in his image so staff in, say, a meeting with clients, can see and hear an image of Jesch talking about his outlook for the Fed or for European stocks, or whatever. Again, this would draw on his written work. Desktop CIOs are an interesting concept, like Clippy figured out that yields go up when prices go down and developed a view on the European Central Bank’s reaction function.

This all reminds me of a question that bugs me sometimes: What are CIOs for? I don’t mean this rudely — in my experience they are almost always insightful, interesting and generous with their time. But it’s striking that at some firms, they chair the investment committee and their view is the house view — if you disagree, you know where the door is. Sometimes they are there for challenge and input, but their key function is as a public face — portfolio managers are left to their own devices to make their own decisions. Some are more managers than markets wonks, and a few firms don’t have a CIO at all. It’s a really mixed bag.

In any case, AI disruption raises the possibility of threading CIOs’ thoughts through organisations in a new way. I’ll be interested to know how clients and colleagues react.

Advertisement

Enhanced interrogation, fund manager style

From AI CIOs to the CIA. Bear with me.

I had an interesting morning last week at the FT’s direct neighbour to the west of its London HQ, Fidelity International. (We could genuinely wave at each other through the windows but we don’t because that would be weird.)

The event was focused on UK equities and marked the 30th anniversary of the launch of the Fidelity Special Values investment trust. Oasis, Blur, UK investment trusts . . . it was all going on three decades ago, I remember those heady days. Golden years.

As part of the discussion, Alex Wright, who has been running the trust for the past 12 years, spoke about the extensive due diligence he performs on companies before he brings them in to his portfolio. He talks to management, but he also talks to competitors, to suppliers, to customers, to try and get a more holistic view and to cut through the polished presentation skills of the bigger companies.

Advertisement

And where does he develop the tricks of the trade in getting answers? Why, from the CIA of course. He has taken training from former CIA agents who know, as he put it, “how to ask the right questions”. They sure do. He declined to give further details, claiming this was the “secret sauce”.

White noise? Bright lights? I’m guessing not but will keep a closer eye on our neighbour just in case. If you’ve had this training and you have looser lips, or if you’re a CFO who really can’t remember what happened in a weird afternoon around St Paul’s, I’d love to know more so drop me a line: katie.martin@ft.com

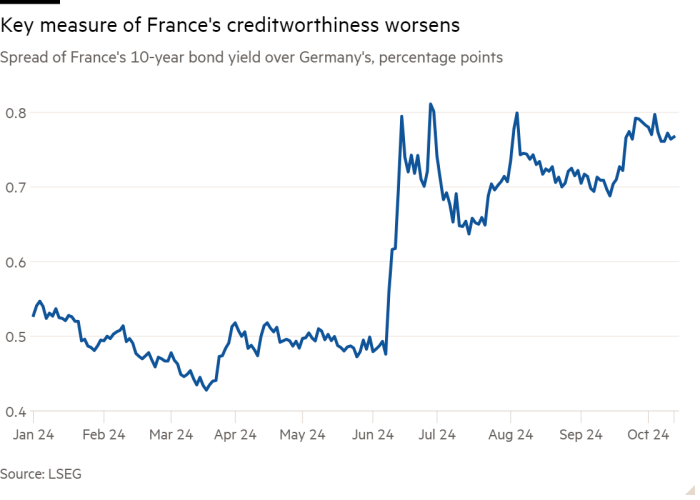

Chart of the week: Mind le gap

Bond fund managers are getting jittery about France, as our new senior markets correspondent Ian Smith writes. (Ian is fresh from the insurance beat and I’m sure he’d love to hear from you: ian.smith@ft.com.)

The yield on France’s 10-year bonds (known as OATs) now stands at more than 3 per cent, above Spain’s for the first time since the 2008 crisis. A proposed Budget from new prime minister Michel Barnier has not succeeded in soothing anxiety about the county’s fiscal trajectory.

Advertisement

“Bottom line, OATs are still not floating our boat,” said analysts at Barclays.

The gap in yields between French and German bonds, or spread in the market parlance, is the key thing to watch for signs of growing anxiety, as Ian illustrates here.

Five unmissable stories this week

UK investors are really loosening up over corporate remuneration. The Investment Association, a trade body representing 250 big investors with over £9tn in assets, has “simplified” its remuneration guidelines to enable UK-listed companies to flash more cash at top execs.

Ares Management has agreed to pay up to $5.2bn to buy the international arm of real estate investment manager GLP Capital Partners, in one of the largest combinations in the private investment industry in recent years.

On a similar note, BlackRock has emerged as a potential buyer of private credit specialist HPS. One person familiar with the talks called it a “giant AUM land grab” by BlackRock in alternative assets.

A counterweight to the argument that higher UK capital gains taxes would be the end of the world, from an unusual source: General Atlantic‘s chief executive Bill Ford.

And finally

By the time you read this, I will have topped up my (extremely depleted) culture vulture credentials with a trip to the Frieze art fair with my now alarmingly grown-up Kid A, who is on an art foundation course and clearly didn’t get her arty abilities from me. I kind of love Frieze because it’s not a museum, as such, and stepping out of that setting strips muppets like me of a comfort blanket. I end up looking at stuff and thinking “is this crap? Is it good? I have no idea”. I like to think that’s a healthy process rather than evidence that I’m a woeful philistine, but no doubt Kid A will tell me otherwise and then demand that I take her out for dinner.

Have a good week.

Advertisement

Thanks for reading. If you have friends or colleagues who might enjoy this newsletter, please forward it to them. Sign up here

We would love to hear your feedback and comments about this newsletter. Email me at harriet.agnew@ft.com

Recommended newsletters for you

Due Diligence — Top stories from the world of corporate finance. Sign up here

Working It — Everything you need to get ahead at work, in your inbox every Wednesday. Sign up here

This article is an on-site version of our Europe Express newsletter. Premium subscribers can sign up here to get the newsletter delivered every weekday and Saturday morning. Standard subscribers can upgrade to Premium here, or explore all FT newsletters

Good morning. A scoop to start: Armenia and Azerbaijan are targeting a peace deal before Baku hosts the COP29 summit next month, Armenia’s president told the Financial Times.

I’m in Luxembourg, where the EU’s foreign ministers — and a British special guest — are gathering for a council meeting which I preview below. And my climate colleague reveals new green policy proposals ahead of a meeting of environment ministers taking place concurrently.

Amongst frenemies

British foreign secretary David Lammy will seek to keep up momentum around warmer relations between the UK and the EU today, as the special guest at a regular meeting of the bloc’s foreign ministers.

Advertisement

Context: The UK left the EU in 2020 after a slim majority of Brits voted to exit in a 2016 referendum. After years of Brexit negotiations and right-wing rule in London strained ties, Keir Starmer’s Labour party came to power in July pledging to “reset” those relations.

Lammy’s trip to Luxembourg, where he will start the day with a breakfast with the EU’s chief diplomat Josep Borrell, before joining the 27 EU ministers for lunch, comes 12 days after Starmer came to Brussels for talks.

His job should be easier than Starmer’s. The context — geopolitical crises such as the wars in Ukraine and the Middle East — means he can talk about security and defence collaboration. That’s far less controversial than issues such as closer alignment on trade, regulation or migration.

“We’re all hoping to hear something about British ideas on how to deepen the relationship . . . especially in the area of the security policy,” said a senior EU diplomat who will be present today. “More co-operation in areas like, maybe, [peacekeeping] missions.”

Advertisement

But there are still landmines. Most prominently: France’s objection to British involvement in EU-supported defence industrial joint projects, which Paris wants to keep inside the bloc.

“The willingness to turn up and attend means I think he will get a good reception,” said Mujtaba Rahman of Eurasia Group. “He’s been one of the [UK] ministers that has given the most definition to the ‘reset’ idea, including a far-reaching security pact.”

Lammy won’t be the first Brit to join a foreign affairs council since Brexit: Liz Truss attended an emergency edition in March 2022 in response to Russia’s full-scale invasion of Ukraine. But he’s the first in the best part of a decade to come with a positive agenda for EU-UK relations.

“This visit is an opportunity for the UK to be back at the table, discussing the most pressing global issues with our closest neighbours and tackle the seismic challenges we all face,” Lammy said last night. “UK security is indivisible from European security.”

Russia’s sanction-busting shadow fleet of oil tankers has grown by almost 70 per cent year on year despite western efforts to clamp down on the trade.

Double down

Eleven EU countries have launched rearguard action to push the clean energy agenda, calling for Brussels to take up 17 different policy ideas to boost renewable power, writes Alice Hancock.

Context: In the wake of the EU’s gas crisis, development of wind and solar power shot up as countries rapidly tried to decrease Russian fossil fuel use. But that effort is not enough to meet the EU’s ambitious decarbonisation goals, according to the group led by Austria and including Germany, Italy and the Netherlands.

“While we have already made significant progress in recent years, there are crucial next steps needed to accelerate the deployment of affordable and sustainable renewable energy sources and fully integrate them into our energy systems,” Leonore Gewessler, Austria’s climate minister, told the FT.

Advertisement

Among the demands sent to the European Commission are more guidance for member states to share costs and benefits of renewable energy resources, more targeted legislation to speed up permitting processes and clearer rules for hydrogen.

The countries also recommend introducing a “Green Loan Standard”, akin to the bloc’s Green Bond Standard, which defines “green” activities for investors in line with the EU’s financial taxonomy.

The paper was sent to the commission ahead of what is set to be a fraught meeting of EU environment ministers today amid deep divisions over whether to support nuclear power in the bloc’s negotiating position for the UN’s COP29 climate conference in November.

France, backed by several eastern European countries, wants nuclear power to be included as part of a pledge to “accelerate zero-and low-emission technologies”, according to the latest draft of the negotiating document — a stance in line with the final decision of last year’s COP28 conference in Dubai.

Advertisement

But Germany is staunchly opposed to even one mention of nuclear in the document, according to an EU diplomat, while other countries that signed the renewables document, such as Denmark, are not anti-nuclear but are against using EU funds to support atomic projects.

Trade Secrets — A must-read on the changing face of international trade and globalisation. Sign up here

Swamp Notes — Expert insight on the intersection of money and power in US politics. Sign up here

Are you enjoying Europe Express? Sign up here to have it delivered straight to your inbox every workday at 7am CET and on Saturdays at noon CET. Do tell us what you think, we love to hear from you: europe.express@ft.com. Keep up with the latest European stories @FT Europe

ibis, the world’s leading economy hotel brand, has launched its new global campaign, “Go Get It,” celebrating 50 years of democratising travel. Since 1974, ibis has made quality travel experiences accessible worldwide, redefining economy hospitality.

The effective altruism movement has been on a wild ride over the past decade. EA started – in the popular consciousness, at least – as a forum for mindful questions about where best to put charitable dollars. Think bed nets and de-worming pills. But, since then, EA seems to have devolved into rationalisations for making tons of money, freak-outs about AI and the end of humanity. Today, on the show, Soumaya and guest Martin Sandbu, the FT economics editorial writer, discuss EA’s evolution, its future and whether it even makes any sense.

Soumaya Keynes writes a column each week for the Financial Times. You can find it here

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

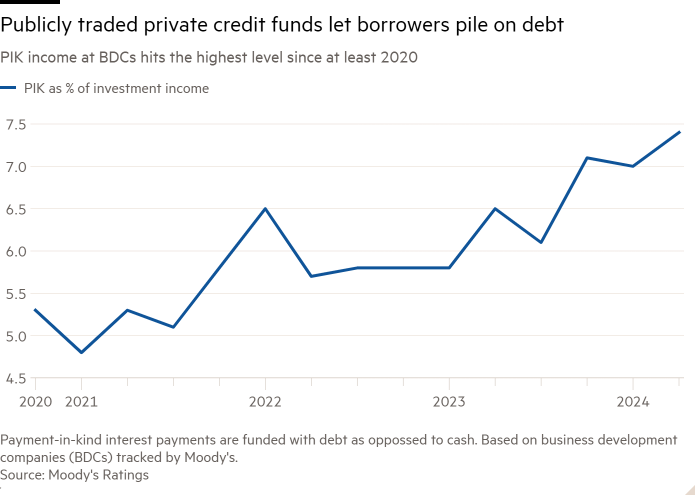

A growing list of cash-strapped companies have turned to their lenders at private credit funds for relief in recent months, seeking to conserve capital by delaying payments on their debt.

The rate at which companies are opting to increase their principal balance instead of paying cash, known as “payment-in-kind” or PIK, edged higher during the second quarter, according to a recent report from rating agency Moody’s. These types of loans have a catch: while they provide temporary relief, they often come with a higher interest rate on a mounting debt load as the deferred payments pile up.

Advertisement

The publicly traded private credit funds that the rating agency keeps tabs on reported the highest levels of PIK income since it began tracking the data in 2020 — though the income is paper profit and it is not clear how much of the gains will actually be realised.

The growth in these types of loans is one signal of stress in corporate America even as the broader economy expands, particularly for businesses that were leveraged to the hilt by their private equity owners and are now struggling with those interest burdens.

“PIK was born out of necessity and is something that people in the market viewed as a temporary situation,” said Sheel Patel, a partner at King & Spalding, referring to recent high interest rates. “Even though the interest rate environment has changed, I think that sponsors will continue . . . trying to keep it in their documents.”

While the Federal Reserve’s move to cut interest rates in September is the first step in alleviating pressure on borrowers, rates are expected to remain far higher than the rock-bottom level they hit in the immediate aftermath of the Covid-19 pandemic, when private equity firms went on a debt-fuelled buyout binge.

Advertisement

Companies could afford the interest burden then. But as rates surged above 5 per cent, interest costs for many highly levered businesses began to eat up most of their cash. That financial distress is showing up, in part, through the swell of PIK income reported by credit funds, fuelling worries that some borrowers are wrestling to stay afloat.

The shift to PIK borrowing is just one risk being borne by the burgeoning private credit industry, where asset managers lend directly to businesses. The loans — while risky — can generate lucrative returns to the lenders who are willing to provide the capital.

Moody’s estimated that 7.4 per cent of the income reported by private credit funds was in the form of PIK during the most recent quarter. Analysts at Bank of America pegged the figure at 9 per cent and said its analysis showed that these funds had gone one step further: 17 per cent of the loans they hold give the borrower an option to pay at least part of their interest with more debt going forward, even if they are not doing so now.

In the second quarter, Blue Owl’s technology fund reported that 23.6 per cent of the income it was earning was in the form of PIK. It was followed closely by Prospect Capital at 18.6 per cent, New Mountain Finance at 17.7 per cent and Ares Management’s ARCC — one of the largest of the funds — at 15.4 per cent.

Prospect did not respond to a request for comment. New Mountain declined to comment.

Advertisement

Beauty Industry Group, a maker of hair extensions backed by private equity group L Catterton, was among the companies seeking to reduce its cash interest burden this year. Its lender, Blue Owl, agreed to take roughly a fifth of its interest payments in PIK. In exchange for the option, the company’s overall interest bill went up.

The same was true for Avalign Technologies, which sought flexibility from Ares this year. The manufacturer of medical implants amended its loan so that, while it would pay more over time, it could put off roughly 30 per cent of its interest payments.

While PIK income is counted as income each quarter, the funds do not receive cash payments until the loan is refinanced or matures. That can create a liquidity crunch for funds, which are required to pay out 90 per cent of their income to investors, even when they have not received cash on those debts.

The uptick in PIK income itself can make investment income at these funds look more attractive, even though the companies bearing the debts are struggling — and the funds are not yet getting paid in full.

PIK is not always a worrying sign, said Clay Montgomery, a Moody’s analyst. Some funds offer PIK to allow healthy businesses to direct their cash towards expansion plans. But it can be difficult for investors to discern when PIK is being extended to give a lifeline during a time of financial stress, or ambition.

Advertisement

For investors, understanding the difference is crucial. Lenders said that if built into a loan at the start, PIK did not indicate stress. Ares said that more than 90 per cent of second quarter PIK income at one of its funds was structured at the start of the investment. Blue Owl said more than 90 per cent of the loans in its technology fund that can defer payment were structured that way from the start.

Because PIK income compounds at a higher rate than cash interest payments, it can be a boon to lenders. But by the same token, once it starts rising, it can become too onerous for some companies to pay back. It can also be used as a tool to avoid impairing debt until a later date, with some investors worried it allows companies to kick the can on what will still end with a default and resulting loss.

Khoros, a software company owned by Vista Equity Partners, is one such company that struggled to repay its PIK interest bill as its business deteriorated. Earlier this year it began to defer the entirety of its debt payments — at an interest rate of more than 16 per cent — and several lenders marked it as a troubled loan.

Advertisement

Vista and L Catterton declined to comment. Linden Capital Partners, the owner of Avalign, did not respond to a request for comment.

You must be logged in to post a comment Login