Crypto World

Bitcoin Open Interest Surges Into Lows After US Dollar Hits New 40-Year Yen High

Bitcoin (BTC) fell toward $58,000 around Tuesday’s Wall Street open as the clock ticked down to a brutal quarterly close.

Key points:

- US stocks’ Q2 gains leave Bitcoin far behind as bulls nurse losses of nearly 20%.

- Bitcoin faces renewed pressure from the risk of Japanese government moves to support the yen.

- BTC price weakness is forcing capitulation by top buyers, says analysis.

Bitcoin “about to get spicy” amid 40-year dollar/yen high

Data from TradingView showed downside gaining the upper hand as volatility increased into the US session.

BTC/USD one-hour chart. Source: Cointelegraph/TradingView

With $60,000 increasingly looking lost as support, commentators saw the tussle between bulls and bears continuing on short time frames.

“Open Interest pumping, noticed some large longs entering on this dip, it’s about to get spicy,” commentator Exitpump wrote in fresh analysis on X.

BTC/USD order-book data. Source: Exitpump/X

Trader Killa eyed a repeat of weekly price patterns, in which Mondays formed the swing low or high of the following week.

“$BTC Keeps consolidating in this price range. Marginally higher lows and equal highs,” trader Daan Crypto Trades continued.

“Look out for whichever direction breaks first, I think a quick move should follow after that seeing how compressed this is becoming.”

BTC/USDT perpetual contract one-hour chart. Source: Daan Crypto Trades/X

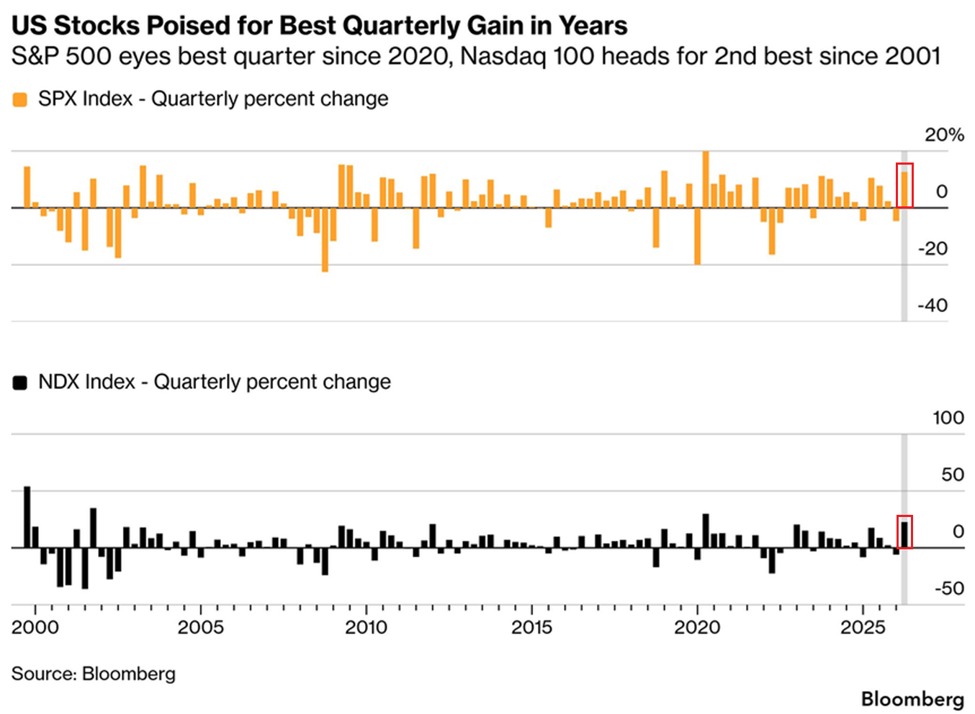

Bitcoin thus reinforced its divergence from US stocks with total Q2 losses nearing 20%.

By contrast, trading resource The Kobeissi Letter noted the S&P 500 was up 14% over the quarter, marking its best performance since 2020.

“This would mark the 2nd-largest quarterly gain since the 2008 Financial Crisis recovery,” it added in an X post alongside data from Bloomberg.

“At the same time, the Nasdaq 100 is up +25%, on track for its strongest quarter in 5 years. This would also mark the Nasdaq 100’s 2nd-best quarterly performance in 25 years.”

US stocks performance comparison. Source: The Kobeissi Letter/X

Kobeissi described an “accelerating” global stocks rally, with the US providing the impetus.

In a potential headwind for crypto, the US dollar hit new multidecade highs against the Japanese yen, increasing the odds of government intervention.

USD/JPY reached 162.50 on the day, its highest since the mid 1980s.

USD/JPY 12-month chart. Source: Cointelegraph/TradingView

“Whether it’s Japan, India, South Korea or MSTR, It’s the same problem,” analyst and YouTube personality George Gammon summarized to X followers on the day.

“You’ve got dollar liabilities and not enough dollars. So you sell assets to get dollars putting downward pressure on the asset. Yen, Rupees, Won, or Bitcoin.”

Bitcoin hodlers “appear to be cutting losses”

In new research, onchain analytics platform CryptoQuant warned of a fresh round of Bitcoin investor “capitulation.”

Related: BTC price RSI prints key 2026 signal: Five things to know in Bitcoin this week

At sub-$70,000 levels, contributor Crypto Sunmoon warned that those who had bought BTC around all-time highs were now selling at a loss.

“Since the break below $70K, exchange inflows have risen sharply, with the majority of this volume consisting of coins held for roughly six to twelve months, coins most likely accumulated near the cycle highs,” they wrote in a Quicktake blog post.

“This pattern is consistent with capitulation among cycle-top buyers, as holders appear to be cutting losses rather than continuing to hold through the drawdown.”

Source: CryptoQuant

CryptoQuant data showed onchain movements increasingly involving coins that last moved around all-time highs, along with increasing inflows to exchanges.

“For some, this will be a painful stretch. That said, capitulation events of this kind among cycle-top investors have historically coincided with long-term bottom formation, a pattern observed in both the 2018 and 2022 cycles,” Crypto Sunmoon added.

Phantom, the largest Solana wallet by market share, said the team behind Ventuals is joining the company this week, weeks after the Hyperliquid-based perpetuals venue shut down. The hires are Ventuals co-founders Alvin Hsia and Emily Hsia, along with engineer Aris Samad, Phantom said in an… Read the full story at The Defiant

The same section also noted Trump holding up to $250,000 in USD, up to $15,000 in the USDC stablecoin, more than $50 million in Ethereum’s ether (ETH), more than $50 million in bitcoin and a combined $6 million and change in various other cryptocurrencies under DT Marks Defi LLC, the Trump Organization-affiliated entity that has the stake in World Liberty.

The president also disclosed a number of other crypto crypto holdings through CIC Digital LLC, a Trump Organization affiliated entity that is one of the two main owners of the president’s memecoin business, including:

- more than $50 million in bitcoin

- $25 million in Ethereum’s ether (ETH)

- $25 million in USDC

- an equity stake in Coreweave, the bitcoin miner that shifted toward AI

- another stake in a “stablecoin holdco” held under DT Marks SC LLC., a business that generated $8 million in revenue last year, tied to an investment from Abu Dhabi Sheikh Tahnoon bin Zayed Al Nahyan

White House spokespeople didn’t immediately respond to a request for comment on the disclosures. Wealth disclosed on government financial reports can be difficult to assess, because they include wide ranges of valuation.

Vice President James David Vance disclosed holding somewhere between $100,000 and $500,000 worth of Bitcoin through a Coinbase account in his own annual disclosure.

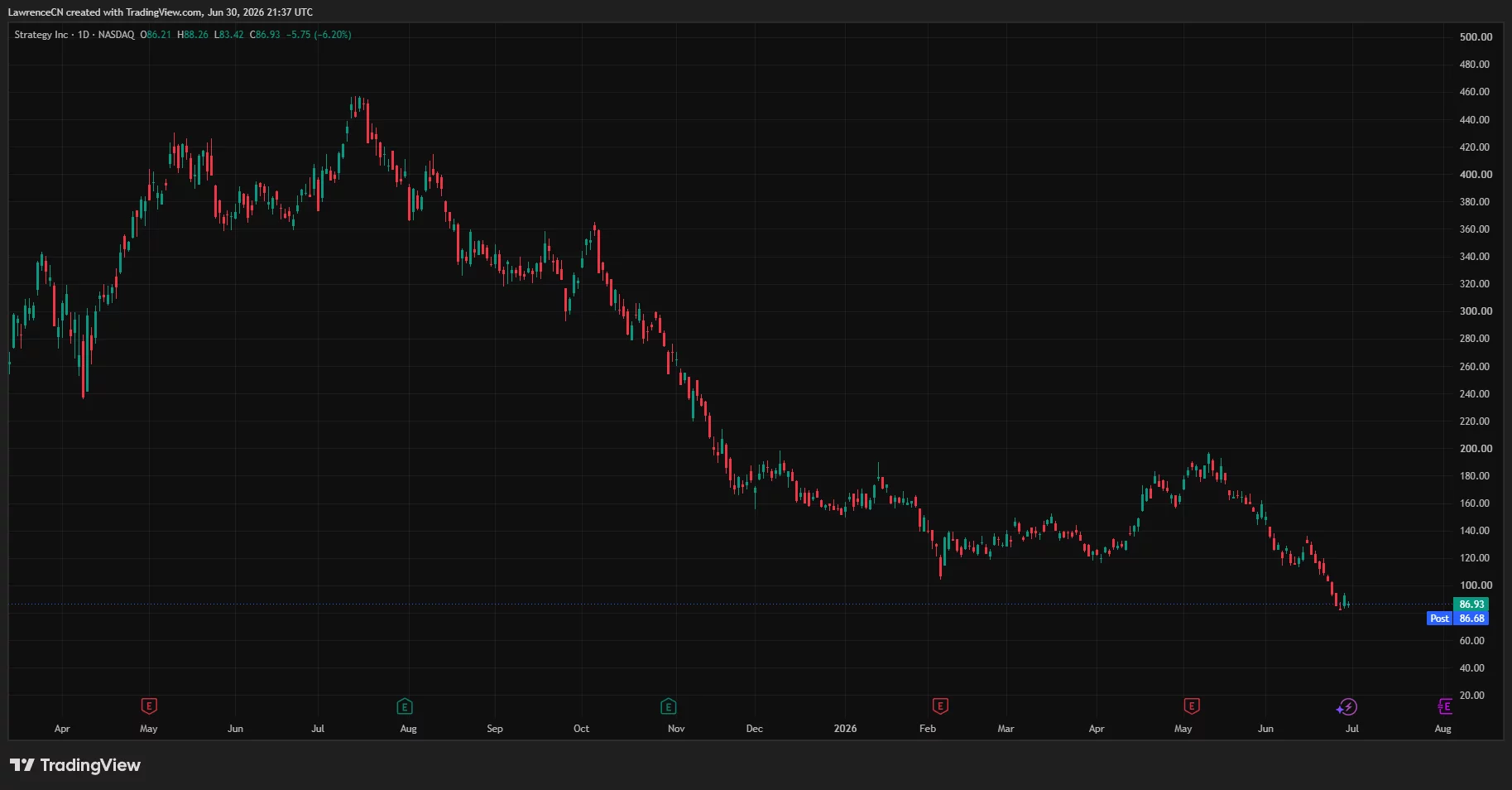

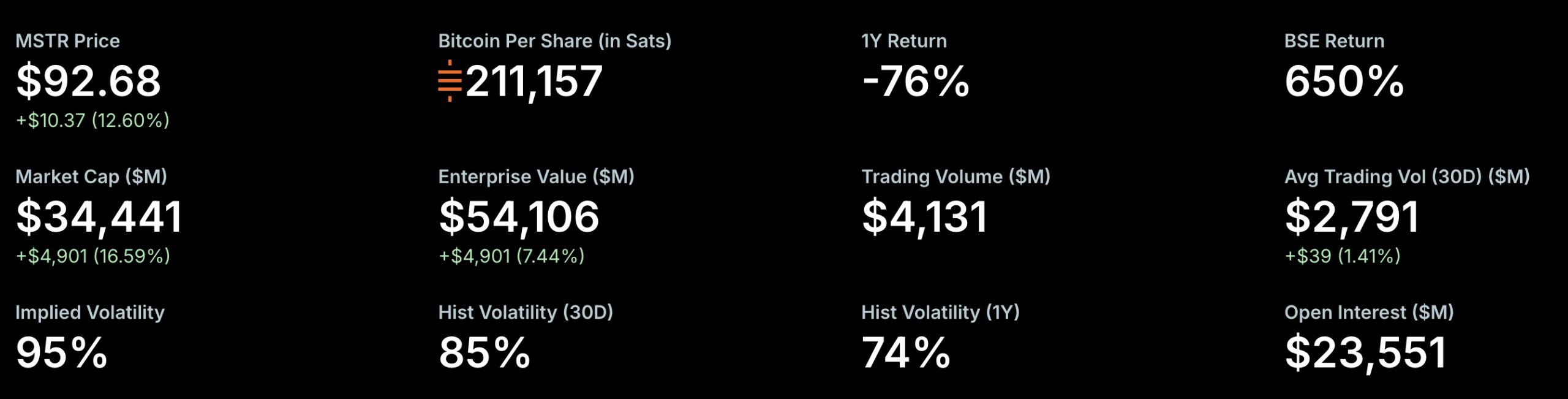

Strategy did not sell $1.25 billion of Bitcoin. It gave itself permission to do so, as part of a wider capital overhaul. The real driver of the stock is the premium to its Bitcoin holdings, and that premium has been shrinking.

Summary

- On June 29, 2026, Strategy’s board authorized a BTC Monetization Program allowing it to sell up to $1.25 billion of Bitcoin if needed, a cap and a framework, not a completed sale.

- The program is one piece of a new Digital Credit Capital Framework that also set up $2 billion of buybacks, $1 billion for common stock and $1 billion for preferred securities, and raised the STRC preferred dividend to 12%.

- Strategy holds 847,363 BTC bought for $64.10 billion, an average near $75,651 per coin, so the full $1.25 billion would be roughly 20,800 BTC, about 2.5% of its stack.

- The number that actually drives MSTR is mNAV, the premium the stock trades at relative to its Bitcoin holdings, and that premium has compressed toward 1x, which is why the company is pivoting from issuing equity to buybacks and selective Bitcoin sales.

- MSTR rose on the announcement even with Bitcoin near $60,000, but the forecast hinges on whether the premium can hold and where Bitcoin goes, not on the sale authorization itself.

The headline that traveled fastest was wrong in a way that matters. Strategy did not sell $1.25 billion of Bitcoin. On June 29, 2026, its board authorized a program permitting the company to sell up to $1.25 billion of Bitcoin if it needs to, as one component of a broad overhaul of the financing model that has funded years of aggressive accumulation.

The distinction is the whole story: this is Strategy formalizing Bitcoin as a funding source it can tap, not a fire sale of its holdings. Whether that is bullish or bearish for the stock depends on a number most headlines never mention: the premium MSTR trades at over the Bitcoin it owns.

This piece lays out exactly what Strategy announced, why mNAV is the real driver of the stock, how the pivot from never-sell to active capital management changes the picture, whether selling Bitcoin helps or hurts MSTR, the buyback and dividend math, the stock’s leverage to Bitcoin, and what it all means for the forecast. It closes with bull, base, and bear scenarios and a short FAQ. Note at the outset: MSTR is a stock, and nothing here is investment advice.

What Strategy actually announced

The June 29 filing introduced a Digital Credit Capital Framework that ties together Strategy’s Bitcoin holdings, its preferred securities, and its equity. Its most-discussed component is the BTC Monetization Program, which authorizes the company to sell Bitcoin primarily to raise up to $1.25 billion for a USD Reserve, and also to fund preferred dividends, interest, and buybacks.

Any Bitcoin sales beyond those stated purposes or amounts would require additional board approval. In Strategy’s own framing, sales would happen from time to time depending on market conditions and capital needs, not on a fixed schedule.

The framework did more than open the door to Bitcoin sales. It set up a board-approved USD Reserve that stood at roughly $2.55 billion as of June 28, dedicated to covering preferred dividends and interest, with a policy that the reserve stay above 12 months of coverage.

It authorized 2 separate buyback programs of up to $1 billion each, 1 for the Class A common stock and 1 for the Digital Credit preferred securities, $2 billion in total repurchase capacity. And it raised the dividend rate on the STRC preferred stock to 12% from 11.5%, effective for record dates on or after July 1, a move aimed at pushing that security back toward its $100 par value.

Alongside the framework, Strategy also disclosed it had raised about $1.15 billion selling common shares through its at-the-market program, and that it had paused Bitcoin buying, holding steady at 847,363 BTC.

The picture, then, is a company building a cash cushion, arming itself to buy back its own securities, and giving itself the option to sell a slice of Bitcoin to fund all of it.

The number that actually matters: mNAV

To forecast MSTR, you have to understand mNAV, the modified net asset value, which is the relationship between the company’s market value and the value of its Bitcoin holdings. For years, MSTR traded at a large premium to its Bitcoin, meaning the market valued the company well above the worth of the coins on its balance sheet. That premium was the engine of the entire model.

When a company trades above the value of its assets, it can issue new shares at that premium and use the proceeds to buy more of the asset, adding more Bitcoin per share than the dilution costs. Issue high, buy Bitcoin, watch the premium justify more issuance: a reflexive flywheel that worked as long as the premium held.

The problem driving the June overhaul is that the premium has compressed toward 1x, meaning MSTR has been trading close to the bare value of its Bitcoin. At or near 1x, the flywheel stalls, because issuing equity no longer adds Bitcoin per share; it just dilutes. That is why Strategy explicitly said it intends to be disciplined about issuing common stock when the shares trade near 1x mNAV.

With the equity lever jammed, the company turned to the other tools: buy back securities to support their value, and monetize a small portion of Bitcoin to fund obligations rather than selling stock into a thin premium. Read this way, the $1.25 billion authorization is not a panic move. It is the logical response to a compressed premium.

For the stock price, the implication is direct. MSTR is, in large part, a leveraged claim on Bitcoin plus or minus a premium. Where that premium goes, expansion back toward the old multiples or further compression toward 1x or below, will drive the stock as much as Bitcoin itself does.

From never-sell to capital management

The symbolic weight of the announcement comes from what it ends. For years, Michael Saylor built Strategy around one rule: raise capital, buy Bitcoin, and do not sell. That doctrine was the company’s identity. It cracked on June 1, 2026, when Strategy disclosed its first Bitcoin sale since 2022, a token 32 coins, negligible against holdings worth tens of billions but enormous in what it signaled. The June 29 framework formalizes the shift, turning a one-off sale into a standing capacity to monetize Bitcoin as part of routine capital management.

The scale keeps it in perspective. Strategy holds 847,363 BTC acquired for $64.10 billion, an average cost near $75,651 per coin. The full $1.25 billion, if ever executed, would be roughly 20,800 BTC, about 2.5% of the stack. This is not the company unwinding its Bitcoin thesis.

Saylor framed the existing reserve plus the new monetization capacity as providing around $3.8 billion of dividend coverage, close to 26 months, while keeping the commitment to long-term Bitcoin exposure. The pivot is from accumulation at all costs to disciplined balance-sheet management, which is a meaningful change in character even if the Bitcoin pile barely moves.

Does selling Bitcoin help or hurt the stock?

This is the question the market is actually debating, and there is a real case on each side. The constructive read is that the framework strengthens the company. A funded USD Reserve and the ability to monetize Bitcoin mean preferred dividends and interest are covered without forced equity sales into a weak premium, which reduces a key risk that had been weighing on both the common and the preferred securities.

Buyback capacity gives the company a tool to support its own securities when they trade cheaply. And the discipline around issuing stock near 1x mNAV stops the dilution that erodes value when the premium is gone. In this reading, the overhaul removes overhangs, and the stock should breathe easier, which is roughly how it reacted on the day, rising on the announcement.

The bearish read is that the framework is a tacit admission the old model is broken. Selling any Bitcoin at all, after building a brand on never selling, removes the accumulation flywheel that justified MSTR’s premium in the first place. If the company is no longer a one-way Bitcoin accumulator, the argument for paying a premium over its holdings weakens, which could keep mNAV pinned near 1x or push it below.

There is also a market-wide angle: Strategy selling Bitcoin, even a small amount, adds supply and dents sentiment in a leveraged, reflexive way, since the company’s buying had helped push Bitcoin higher on the way up. In this reading, the overhaul manages decline rather than reversing it.

The honest answer is that both can be true at once: the framework reduces short-term financial risk while confirming the premium era is over. That combination is exactly why the stock can rise on the news and still face a lower ceiling than it once had.

The buybacks and the dividend math

The capital tools deserve a closer look because they shape the floor under the stock. The $2 billion in buyback authority, split between common and preferred, gives Strategy a mechanism to return capital and defend its securities when they trade below intrinsic value, which can support the share price at the margin. Buybacks are most accretive precisely when the stock trades near or below the value of its assets, so authorizing them at compressed mNAV is internally consistent with the discipline message.

On the dividend side, raising the STRC rate to 12% is aimed at pushing that preferred security back toward its $100 par value, a sign the company is prioritizing the health of its credit stack. The USD Reserve at roughly $2.55 billion covers about 17 months of preferred dividends and interest on its own, with a policy floor of 12 months, and the reserve combined with the Bitcoin monetization capacity extends coverage to around 26 months by Saylor’s account.

That coverage is the point of the whole exercise: it buys time and reduces the chance of a forced, dilutive capital raise at the worst possible moment. For the common stock, a more stable credit structure underneath is a quiet positive, even if it is less exciting than the accumulation story it replaces.

The leverage to Bitcoin

Whatever happens with the premium, MSTR remains a high-beta proxy for Bitcoin, and Bitcoin is the larger variable. With Bitcoin near $60,000 as of late June, down sharply from its prior highs, Strategy’s average cost near $75,651 means a meaningful portion of the stack sits underwater on paper, which is part of the pressure that prompted the overhaul. The stock tends to move more than Bitcoin in both directions, so the Bitcoin path dominates the forecast.

If Bitcoin recovers, the value of the holdings rises, the premium has more room to expand, and the leveraged nature of the stock can produce outsized gains. If Bitcoin stays soft or falls further, the holdings lose value, the pressure on the credit structure grows, and the monetization program may be used more actively, which feeds the bearish reflexivity. In short, the $1.25 billion authorization changes how Strategy manages its balance sheet, but it does not change the fact that the single biggest input to MSTR’s price is where Bitcoin trades.

What it means for the MSTR forecast

Forecasting a stock like MSTR is not the same as forecasting a token, and it would be irresponsible to attach a precise price target to a security whose value depends on two moving parts, the Bitcoin price and the mNAV premium, that interact reflexively.

The useful framing is conditional. MSTR’s value can be thought of as the value of its Bitcoin per share, multiplied by whatever premium or discount the market assigns. The June overhaul mainly affects the premium term: by reducing forced-dilution risk and adding buybacks, it supports the premium at the margin, while the end of never-sell may cap how high that premium can climb. The Bitcoin term is set by the market.

That is why the scenarios below are built around those 2 drivers rather than a single number. They are illustrative, not predictions, and they are not advice.

How the flywheel worked, and why it stalled

To see why the June overhaul was necessary, it helps to trace the mechanism that built Strategy in the first place. The company would issue new securities, common stock, convertible debt, or preferred shares, and use the proceeds to buy Bitcoin.

Because the market valued MSTR above the worth of its Bitcoin, each issuance added more Bitcoin per share than it diluted away, so existing holders came out ahead even as the share count grew. More Bitcoin per share supported the premium, the premium justified more issuance, and the cycle compounded. For years this reflexive loop turned a software company into the largest corporate holder of Bitcoin on the planet, with 847,363 coins acquired for $64.10 billion.

The loop only works in one direction, and only above a certain line. That line is roughly 1x mNAV, the point where the stock trades at the bare value of its Bitcoin. Above it, issuing stock is accretive and the flywheel spins. At or below it, issuing stock is dilutive, because the company would be selling shares for less than the Bitcoin those shares represent, handing value to new buyers at the expense of existing holders.

When the premium compressed toward 1x in 2026, the most powerful tool in Strategy’s kit, the ability to print equity and buy Bitcoin, stopped being usable without harming shareholders. The flywheel did not just slow. It hit a wall.

That is the context that makes the new framework coherent. With the equity lever jammed, the company reached for the tools that work at a compressed premium: buying back its own securities when they trade cheaply, raising a cash reserve so it is not forced to issue stock at the wrong price to cover dividends, and giving itself the option to monetize a small slice of Bitcoin to fund those obligations. Each piece is a response to the same problem. The premium that powered everything is gone, so the company is building a structure that can function without it.

What to watch: the signals that move MSTR

For readers tracking MSTR instead of the daily noise, a few signals will indicate which scenario is taking shape. The first is Bitcoin’s price relative to Strategy’s roughly $75,651 average cost. While Bitcoin trades near $60,000, a meaningful portion of the stack sits underwater on paper, which keeps pressure on the credit structure. A recovery above the cost basis would ease that pressure and give the premium room to expand; further weakness would deepen it.

The second is the direction of mNAV itself. A premium rebuilding above 1x would signal the market is again willing to pay up for Strategy’s structure, the bullish path. A premium stuck at 1x or slipping to a discount would confirm the de-rating the bears expect.

The third is the pace of actual Bitcoin sales under the new program: sparing, opportunistic use would read as disciplined capital management, while heavy or frequent sales would read as forced and would reinforce the broken-model narrative. The fourth is buyback execution, whether the company actually repurchases common and preferred securities into weakness, which would support prices and show the framework is more than words.

The fifth is the health of the preferred stack, with the STRC dividend raised to 12% to push that security toward its $100 par and the reserve policy holding above 12 months of coverage. Stability there underpins the whole structure; stress there would signal trouble spreading.

Tracked together, these five map the two variables that decide the stock, the Bitcoin price and the premium, onto observable events. The $1.25 billion authorization changed Strategy’s toolkit. These signals will show whether the tools are working.

Bull, base, and bear scenarios for MSTR

The scenarios combine the Bitcoin path with the direction of the mNAV premium. They describe possible outcomes, not targets, and the figures are deliberately framed as conditions instead of prices.

Bull case

In the bull scenario, Bitcoin recovers from the $60,000 area, lifting the value of Strategy’s 847,363 coins back above the cost basis and easing the pressure that prompted the overhaul. The buybacks and the funded reserve reassure the market that the credit structure is sound, dilution risk fades, and investors regain confidence enough to pay a premium over net asset value again. mNAV expands back above 1x, and because MSTR is leveraged to both Bitcoin and its own premium, the stock outpaces Bitcoin to the upside. This case needs Bitcoin strength and a restored willingness to pay up for Strategy’s structure.

Base case

In the base scenario, Bitcoin chops sideways around current levels and the premium stays compressed near 1x. The framework does its job of stabilizing the credit stack and removing forced-sale risk, so the stock avoids a crisis, but with the accumulation flywheel gone, MSTR trades largely in line with the value of its Bitcoin, give or take a modest premium. The buybacks provide some support, the monetization program is used sparingly, and the stock tracks Bitcoin without the old multiplier. This is the “stabilized but de-rated” outcome where MSTR behaves more like a leveraged Bitcoin holding company than a premium growth story.

Bear case

In the bear scenario, Bitcoin weakens further from $60,000, pushing more of the stack underwater and forcing more active use of the monetization program to cover obligations. The market reads continued Bitcoin sales as confirmation the model is broken, mNAV slips below 1x to a discount, and the leveraged downside takes the stock lower than Bitcoin’s decline alone would suggest. Preferred-stack stress, despite the higher STRC dividend and the reserve, keeps sentiment fragile. In this case, the overhaul slows the bleeding without stopping it, and the stock re-rates toward or below the value of its Bitcoin.

Frequently Asked Questions

Did Strategy actually sell $1.25 billion of Bitcoin?

No. On June 29, 2026, Strategy’s board authorized a program permitting it to sell up to $1.25 billion of Bitcoin if needed, primarily to fund a USD Reserve and service obligations. It is a cap and a framework, not a completed sale. Any sales would happen over time depending on conditions, and selling beyond the stated purposes would require further board approval.

What is mNAV and why does it matter for MSTR?

mNAV, or modified net asset value, is the premium or discount at which MSTR trades relative to the value of its Bitcoin holdings. A premium lets Strategy issue stock and buy more Bitcoin accretively, powering its growth. That premium has compressed toward 1x, which jams the equity lever and is the core reason for the new buyback and Bitcoin-monetization tools. Where the premium goes is a primary driver of the stock.

How much Bitcoin does Strategy hold?

As of late June 2026, Strategy held 847,363 BTC purchased for an aggregate $64.10 billion, an average near $75,651 per coin. The full $1.25 billion monetization authorization would represent roughly 20,800 BTC, about 2.5% of the holdings. The company paused Bitcoin buying in the week of the announcement.

Is the announcement good or bad for the stock?

It is genuinely mixed. The framework reduces forced-dilution risk, funds dividends, and adds buyback capacity, which the market read positively on the day. But formalizing Bitcoin sales ends the never-sell model that justified MSTR’s premium, which may cap how high the premium can climb. Both effects can hold at once: lower near-term risk, lower long-term ceiling.

How does Bitcoin’s price affect MSTR?

MSTR is a high-beta proxy for Bitcoin and tends to move more than Bitcoin in both directions. With Bitcoin near $60,000, below Strategy’s average cost, part of the stack is underwater on paper. A Bitcoin recovery would lift the holdings and give the premium room to expand, while further weakness would deepen the pressure and could trigger more active Bitcoin monetization.

What is the STRC dividend change about?

Strategy raised the dividend on its STRC preferred stock to 12% from 11.5%, effective for record dates on or after July 1, 2026. The goal is to push the security back toward its $100 par value and signal commitment to the health of its preferred, or Digital Credit, stack. It is part of the broader framework aimed at stabilizing the company’s capital structure.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice, and the author is not a licensed financial adviser. MSTR is a publicly traded stock whose value depends on volatile inputs including the price of Bitcoin. Price scenarios are illustrative and speculative, not predictions or recommendations. Always do your own research and consider consulting a licensed professional before making financial decisions. Figures are accurate as of June 30, 2026, and will change.

Machi Big Brother, one of Hyperliquid's most-liquidated traders, was liquidated again on an Ethereum long and has now lost more than $80 million on the onchain derivatives exchange since September, according to onchain analytics firm Arkham. Arkham said the trader, whose real name is Jeffrey Huang,… Read the full story at The Defiant

Lighter, one of the largest decentralized perpetuals exchanges by trading volume, said it will start permanently burning the LIT tokens it buys back with exchange revenue and will fund staking rewards from its ecosystem token reserve. Lighter has bought back about 15.5 million LIT — roughly 6.3% of… Read the full story at The Defiant

Michael Burry attends “The Big Short” New York screening at the Ziegfeld Theater in New York, on Nov. 23, 2015.

Astrid Stawiarz | Getty Images

Michael Burry said Tuesday he has placed a bearish wager against Caterpillar, believing the construction-equipment maker has become one of the market’s most overvalued beneficiaries of the artificial intelligence investment boom.

The famed investor said he shorted Caterpillar shares at $1,060.98, alongside new bearish positions in Nvidia, Applied Materials, Tesla and the iShares Semiconductor ETF (SOXX), as he prepared for what he believes is an increasingly overextended rally in AI-linked stocks.

“Caterpillar jumped out at me,” Burry wrote in a Tuesday SubStack post. “I have never shorted Caterpillar. It has always done great for me on the long side in the past.”

Caterpillar shares just capped off the first half of 2026 with an 86% gain, making the construction equipment giant one of the best-performing stocks in the S&P 500 this year as investors increasingly embraced it as a proxy for the global AI infrastructure buildout.

Caterpillar year to date

Burry said Caterpillar’s stock valuation has reached levels that caught his attention. He shared a chart showing Caterpillar’s price-to-sales ratio climbing to the highest level in at least three decades at the same time the stock surged to record highs.

The investor, who famously predicted and profited from the subprime mortgage crisis in 2008, also reiterated his broader concerns about semiconductor valuations. He said the Philadelphia Semiconductor Index is trading about 65% above its 200-day moving average, a level he said was only reached previously during the dot-com bubble in 2000.

“The proximate cause of today’s rally is big spending announced out of Korea. Well, I see that as the beginning of the end,” Burry said. “It is only a matter of time now.”

Bitcoin is holding a narrow consolidation price range as its prediction hangs in the balance on Michael Saylor’s next move and macroeconomic catalyst. Strategy’s MSTR shares snapped a nine-day losing streak on Monday after the firm unveiled a formalized capital framework that could allow it to sell up to $1.25 billion in Bitcoin to strengthen its balance sheet.

The announcement centered on Strategy’s expanded USD Reserve alongside a “BTC Monetization Program” that formalizes potential Bitcoin sales as a cash management tool. Meanwhile, Michael Saylor raised its dividend for the eighth time, targeting a 12% annual yield through twice-monthly distributions.

As one analyst noted, Saylor’s recent $1 billion Bitcoin purchase was financed entirely through STRC preferred stock sales, with no dilution of MSTR common shares. However, the preferred share product STRC rebounded after the news and sent the company’s mNAV above 1.0.

Macro context adds a layer of uncertainty. The Bank of Japan’s upcoming rate decision, a potential hike to the highest levels in 30 years, remains a live risk-off trigger for BTC and risk assets. So, until the BoJ verdict lands, directional conviction is thin.

Discover: The Best Crypto to Diversify Your Portfolio

Bitcoin Price Prediction: Break $70,000 This Week?

Bitcoin is trading around $60,000, 52% below its all-time high. Price remains locked inside a defined range after several failed breakout attempts. Meanwhile, MACD still favors buyers, although bullish momentum has weakened over the past two days. RSI is also trying to move above its signal line.

If buyers defend support near $58,800 and momentum strengthens, Bitcoin could challenge resistance around $64,100. A successful breakout would expose the next upside target near $71,700. However, the market still needs stronger buying pressure to confirm a sustained recovery.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The most likely outcome remains continued consolidation while traders wait for the Bank of Japan’s policy decision and any fresh announcement from Strategy regarding additional Bitcoin purchases. On the downside, a surprise rate hike or disappointing corporate demand could drag Bitcoin toward support near $55,000.

We might still see some short-term volatility as traders adjust their exposure. Although Michael Saylor continues projecting Bitcoin could eventually reach $150,000 and later $1 million, price direction will ultimately depend on liquidity and sustained capital inflows rather than long-term forecasts.

Discover: The Best Token Presales

Bitcoin Hyper Targets Early-Mover Upside as Bitcoin Tests Key Levels

Bitcoin consolidating 50% below its high is the textbook setup where established-asset upside gets slowly priced in. It’s also where early-stage infrastructure plays attract rotational interest from traders who’ve done the math on BTC’s remaining percentage moves.

At the current rate, a 10x from here would make BTC a $10 trillion asset; that’s a very different probability calculus than it was at $1,000. That’s the context to keep in mind when evaluating what gets built on top of Bitcoin’s base layer.

Bitcoin Hyper ($HYPER) is positioning itself as the first Bitcoin Layer 2 with SVM (Solana Virtual Machine) integration, targeting the performance gap between Bitcoin’s security and Solana-grade execution speed.

The presale has raised close to $33 million at a current price of $0.01368, with staking available and a decentralized canonical bridge for native BTC transfers. The core pitch: fast, low-cost smart contracts on Bitcoin without sacrificing the trust layer.

Research Bitcoin Hyper before the presale window closes.

The post Bitcoin Price Prediction: How Michael Saylor’s Capital Strategy Could Impact BTC appeared first on Cryptonews.

Spot bitcoin ETFs just posted their third-worst week on record, bleeding $1.79 billion in net outflows between June 22 and June 26، and BTC hasn’t been able to hold the $60,000 handle since.

Ethereum is trading near $1,585, up a marginal 0.7% over 24 hours but still down roughly 8% on the week, while ether ETFs just extended their outflow streak to seven consecutive weeks.

There’s a detail buried in the fund-flow breakdown that most headline readers are missing.

BlackRock’s IBIT alone accounted for $1.3 billion of the bitcoin ETF exodus, with Fidelity’s FBTC adding $314.9 million and Grayscale’s GBTC shedding another $135.3 million. Smaller pockets of demand, Grayscale’s Bitcoin Mini Trust picked up $71.7 million, Morgan Stanley’s MSBT brought in $26.2 million, were nowhere near enough to offset the tide.

Meanwhile, analysts are flagging BTC’s current state as a fragile recovery phase, with roughly $448 million in leveraged long liquidations clearing out in the last 24-hour window alone. The macro backdrop isn’t helping: Federal Reserve meeting minutes and U.S. Treasury General Account movements are the two catalysts traders are stacking their scenarios around this week.

What happens at $60,000 over the next 48 hours will answer most of the near-term questions.

Can Bitcoin and Ethereum Hold Support as ETF Outflows Mount?

Bitcoin is currently oscillating between $60,000 and $59,400. The $60,000 level has now been a firm rejection zone across multiple breakout attempts, with sell-side pressure consistently materializing as the price approaches that level.

Rebuilding open interest suggests some traders are re-entering, but short-dated put options are still trading at a premium to calls; the market is hedging downside, not loading for upside.

Key support sits at $59,000, with a deeper floor in the mid-$50,000s if that level fails. The bull case depends on Fed minutes landing dovish enough to trigger a risk-on rotation; if that materializes, a move back toward the $64,000–$66,000 prior resistance zone becomes credible.

The base case is a continued range chop between $59,000 and $62,000 until a macro catalyst forces a directional decision. Bear case invalidation: a clean close below $59,000 with volume opens the mid-$50,000s as the next structural reference.

Ethereum’s picture is marginally more stable but not materially better. At $1,585, ETH is holding above the $1,530–$1,550 intraday low zone, and the $1,500 level remains the line that matters. A break there, per technical consensus, opens further downside with limited structural support until the low-$1,400s.

The recovery target is $2,000, but ETH needs to reclaim $1,700 first, and seven straight weeks of ETF outflows don’t suggest that institutional rotation is imminent. The $3 billion-plus outflow pattern is becoming a structural overhang, not a one-week anomaly.

Bitcoin Hyper Could be The Next 1000x In Crypto And Here is Why

When BTC consolidates in a range defined by macro uncertainty and institutional de-risking, the asymmetric opportunity shifts to early-stage infrastructure with direct Bitcoin exposure, but without the ETF wrapper or the spot price ceiling.

Smart money accumulation in Bitcoin Layer 2s during ETF outflow cycles is a pattern that’s begun attracting serious attention precisely because the infrastructure thesis doesn’t require BTC to immediately reclaim $64,000.

Bitcoin Hyper ($HYPER) is positioning itself as the first Bitcoin Layer 2 with full Solana Virtual Machine (SVM) integration, targeting the core limitations that have kept Bitcoin’s programmability behind Ethereum and Solana: slow transactions, high fees, and no native smart contract layer.

The presale is currently priced at $0.0136824, with $32,898,380.61 raised to date. Staking is live with a high APY, and the architecture includes a Decentralized Canonical Bridge for BTC transfers alongside sub-second finality claims that, if delivered, would make it faster than Solana on its own infrastructure. The $32M raised during the current BTC dip isn’t noise; it reflects genuine appetite for scalable Bitcoin infrastructure ahead of a potential macro pivot.

The post Bitcoin ETFs Just Posted Their Third-Worst Week Ever And BTC Can’t Hold $60,000 appeared first on Cryptonews.

A dispute over Bitcoin’s proposed BIP-110 soft fork has intensified after critics argued that the upgrade could break certain wallets and leave some users with permanently unspendable BTC if it activates.

This is according to crypto investment advisor Farside Investors, who were challenging claims made by BIP-110 supporter Fred Krueger in a June 28 post on X.

BIP-110 Could Break Wallets and Freeze Funds

In his Sunday post, Krueger stated that BIP-110 would leave Bitcoin’s monetary properties untouched, with the 21 million coin supply, proof-of-work, Lightning, multisig wallets, self-custody and address functionality all being unchanged.

“The primary effect is that large arbitrary data used by Ordinals, Runes, and similar protocols would no longer be valid,” he noted.

However, Farside disputed that assessment, saying that BIP-110 would ban several Taproot scripting features, including the OP_IF opcode used by Miniscript. According to its explanation, after the fork activates, wallets that support Miniscript will still let users generate and send funds to addresses built on the now-banned scripts.

While those transactions will look valid under BIP-110’s own rules, the BTC sent to them will become unspendable because the required spending conditions will no longer apply under the new consensus rules.

Ironically, the latest version of Bitcoin Knots, one of the node implementations supporting BIP-110, could itself create these incompatible addresses.

Farside went further, pointing out that BIP-110 will also ban the creation of new pay-to-public-key (P2PK) outputs, a script type that was used extensively during Bitcoin’s early days and is holding more than 1.7 million BTC.

However, spending the existing P2PK outputs would still be allowed, although under certain circumstances, per the investment company, the proposal could temporarily freeze funds or expose users to theft risks, despite including safeguards such as grandfathering older outputs and limiting enforcement to about one year.

The proposal can become active either if 55% of miners signal support during a difficulty adjustment period or, if that does not happen, through a mandatory signaling process starting at block 961,632, which is expected to be reached in August 2026.

Debate Extends Beyond Wallet Compatibility

The fight over BIP-110 is part of a wider argument about what’s clogging Bitcoin’s network space, with Krueger and other supporters saying that inscriptions, BRC-20 tokens and similar uses have created unnecessary bloat on the network, and the new proposal is a way to discourage such transactions without changing BTC’s monetary policy.

But others, including the Block Runner podcast account, have rejected that reasoning, insisting that the 126.7 million inscriptions on Bitcoin account for just 1.267 BTC of value, a fraction it likened to a coin dropped in the ocean.

According to them, miners actually profiting from that activity, including AntPool, ViaBTC, SpiderPool, F2Pool, and Luxor, are helping offset Bitcoin’s declining security budget, while BIP-110 itself has only thin miner and node support.

The network’s activity has stayed high through this period despite price action. Recent data from CryptoQuant showed that usage was near record territory even with BTC plunging below $60,000, a sign that demand for blockspace, whether contested or not, isn’t going away any time soon.

The post Critics Say BIP-110 Could Break Self-Custody and Risk User Funds appeared first on CryptoPotato.

Crypto World

Crypto wallet Phantom pushes deeper into perps hiring team behind Hyperliquid’s OpenAI, Anthropic markets

The race is also spreading beyond crypto. Last month, prediction market operator Kalshi launched its own perpetual futures business after regulatory approval, joining exchanges betting that always-on derivatives will become a larger part of financial markets.

For Phantom, the hires are part of a broader push into trading.

Best known as one of crypto’s largest self-custody wallets, Phantom has steadily expanded beyond asset storage into swaps, staking and derivatives as wallets increasingly compete to become full-service financial apps rather than simple interfaces for holding tokens.

The company said it has become the largest distribution partner in the Hyperliquid ecosystem and plans to deepen its focus on perpetual futures.

“Open markets have become a major focus for us,” Millman wrote. “We’ve gone deep on perps, and we intend to go deeper.”

Millman described Hyperliquid as “one of the best examples anywhere of what open markets make possible,” pointing to its global liquidity and transparent onchain infrastructure.

Bringing on the Ventuals team will help Phantom accelerate its efforts to build trading products around the ecosystem, he said.

Phantom Hires Ventuals Founders After Hyperliquid Perps Venue Winds Down

France vs Sweden Live Score, 3-0, FIFA World Cup 2026 Round of 32: Mbappé adds another to secure brace as France dominate

Cargo thieves are now stealing millions in data center hardware, not just GPUs and consoles

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics5 days ago

Politics5 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World20 hours ago

Crypto World20 hours agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics5 days ago

Politics5 days agoPotential 2028er World Cup attendee leaderboard

-

Business5 days ago

Business5 days agoAsia stock markets slide as tech shares slump

-

News Videos2 days ago

News Videos2 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech5 days ago

Tech5 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World7 days ago

Crypto World7 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World7 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World5 days ago

Crypto World5 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World3 days ago

Crypto World3 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business7 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World4 days ago

Crypto World4 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Business19 hours ago

Business19 hours agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Sports4 days ago

Sports4 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech3 days ago

Tech3 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech3 days ago

Tech3 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World4 days ago

Crypto World4 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

You must be logged in to post a comment Login