Crypto World

What is a consortium stablecoin? Open USD model

Tether and Circle built their businesses by keeping the interest on the dollars behind their coins. A new kind of stablecoin, run and owned by a group instead of a single company, shares that money instead. Here is how the consortium model works and why it is spreading.

Summary

- A consortium stablecoin is a fiat-backed token issued and governed by a group of companies instead of a single issuer, with two defining features: shared governance and shared reserve income.

- It contrasts with single-issuer stablecoins such as Tether’s USDT and Circle’s USDC, where one company controls the network and keeps the interest earned on reserves.

- The model is spreading because stablecoin regulation has clarified, the market has grown past $300 billion, and partners increasingly want a share of the reserve income that has made incumbents enormously profitable.

- Leading examples include Open USD, backed by more than 140 companies, the Paxos-led Global Dollar Network, and Europe’s bank-led Qivalis, while the earlier Centre Consortium behind USDC shows the model can also fracture.

- The consortium approach aligns incentives and challenges incumbent economics, but it faces real risks around coordination, governance, and the difficulty of shipping a product agreed on by many stakeholders.

A consortium stablecoin is a digital dollar, or other fiat-pegged token, that is issued and governed collectively by a group of companies rather than controlled by one. The defining idea is shared ownership of both the decisions and the economics: a board drawn from the partner companies sets the rules, and the income earned on the reserves backing the coin is distributed among those partners instead of kept by a single issuer. That structure is a deliberate break from the model that built the stablecoin giants, and it has become one of the most important trends in digital money.

This explainer covers what makes a stablecoin a consortium stablecoin, why the model is emerging now, the leading examples, and the risks that come with running a coin by committee.

Consortium versus single-issuer stablecoins

To understand the consortium model, start with the model it is reacting against. Most of today’s major stablecoins are single-issuer coins. One company creates the token, holds the dollar reserves that back it, collects the interest those reserves earn, and keeps the profit. Tether, which issues USDT, and Circle, which issues USDC, are the dominant examples, and together they control roughly 80 percent of a stablecoin market worth more than $300 billion. Their businesses are simple and enormously profitable: take in dollars, park them in safe assets like Treasury bills, and keep the yield while the token circulates freely.

That reserve income is the heart of the matter. When interest rates are meaningful, the interest on billions of dollars of reserves adds up to billions in revenue. The single issuer keeps that money, which is what makes issuing a large stablecoin one of the best businesses in finance. A partial exception is USDC, where Circle shares a large portion of the economics with Coinbase in exchange for distribution, a hint of the shared-economics idea taken further by the consortium model.

A consortium stablecoin rearranges this in two ways. First, no single company controls the network; a group governs it collectively through a shared board. Second, the reserve income is not kept by one issuer but distributed among the participating companies, usually after a management fee that funds operations. The coin still works the same way for a user, redeemable one-for-one for a dollar held in reserve, but the ownership of the decisions and the money behind it is spread across many hands instead of being concentrated in one. That is the essential difference.

The two defining features: shared governance and shared economics

Every consortium stablecoin rests on the same two pillars, and it is worth being precise about each. The first is shared, neutral governance. Instead of one company setting the token’s rules, its reserve policy, its supported chains, and its product roadmap, a board made up of the partner companies makes those decisions collectively. The stated aim is neutrality: no single participant can steer the coin to serve its own interests at the expense of the others, which is meant to make the token trustworthy as shared infrastructure rather than one firm’s product. For businesses wary of building on a competitor’s rails, that neutrality is a selling point.

The second pillar is shared economics. In a consortium model, the interest earned on the reserves is returned to the partners who adopt and distribute the coin, minus a management fee for operating costs. This directly inverts the incumbent arrangement where the issuer keeps the yield. The logic is incentive alignment: if a payment company, bank, or platform earns a share of the reserve income by supporting the coin, it has a direct financial reason to promote adoption. The coin’s growth becomes a shared commercial project instead of one issuer’s private revenue stream.

Together, these two features aim to solve problems the consortium model’s backers say businesses face with existing stablecoins. Companies often pay fees to mint or redeem at scale, do not share in the reserve revenue their volume helps generate, and have little influence over an issuer’s roadmap. A neutral, revenue-sharing, collectively governed coin is pitched as the answer to all three. Whether it delivers depends on execution, but the structure is a coherent response to the incumbents’ weaknesses.

Why consortium stablecoins are emerging now

The consortium model is not new in concept, but it has gained momentum for specific reasons in the mid-2020s. The first is regulation. In the United States, the GENIUS Act, signed into law in 2025, created a federal framework for dollar-backed stablecoins, setting standards for reserves and licensing. That clarity lowered the legal uncertainty that had kept large, regulated institutions on the sidelines, and it drew banks, payment networks, and major enterprises into a market they had previously watched from a distance. A consortium of household-name financial firms is far more plausible once the rules of the road are defined.

The second reason is the sheer size and trajectory of the market. The stablecoin sector has grown past $300 billion, and some projections see it reaching into the trillions by the end of the decade as tokens move from crypto trading into cross-border payments, merchant settlement, and corporate treasury operations. A market that large attracts competitors who want a share, and it makes the reserve income at stake enormous.

When the prize is that big, the incentive to build an alternative to the incumbents grows accordingly.

The third reason is the economics itself. As the interest income earned by single issuers has become widely understood, partners have increasingly asked why they should drive adoption of a coin whose reserve revenue flows entirely to one company. The competitive frontier has shifted from simply issuing a token to controlling the underlying network and sharing its economics. Consortium stablecoins are the natural expression of that shift, giving a broad group of participants both a say in the network and a cut of the money it generates. The result has been a wave of consortium and shared-revenue projects entering the market.

The leading examples

The clearest way to understand the model is through the projects putting it into practice. The most prominent is Open USD, or OUSD, announced in 2026 by an independent company called Open Standard and backed by a consortium of more than 140 businesses spanning payments, banking, technology, and crypto, including Visa, Mastercard, Stripe, BlackRock, BNY, Coinbase, and Google. Open USD lets businesses mint and redeem the token with no fees and no volume limits, and it shares the reserve income with participating partners after a management fee, governed by a board drawn from those partners. It is positioned as a direct challenge to Tether and Circle, and its announcement sent Circle’s stock down sharply as the market priced in the competitive threat.

Open USD is not the first of its kind. The Global Dollar Network, built around the USDG token and led by the regulated issuer Paxos, uses a similar shared-revenue structure, distributing reserve income to partners such as Robinhood, Kraken, and Galaxy Digital to encourage broad adoption. In Europe, a group of major banks including BNP Paribas, ING, UniCredit, and SEB formed a venture called Qivalis to launch a euro-pegged stablecoin, initially focused on crypto trading before expanding, as financial institutions seek shared digital-payment infrastructure they collectively control. These projects differ in detail, but they share the consortium DNA of collective governance and shared economics.

What unites the examples is a strategic bet: that the future of stablecoins is a fight over infrastructure and network control rather than individual tokens, and that a broad, aligned coalition can win it against entrenched single issuers. The breadth of the coalitions, spanning card networks, banks, technology platforms, and crypto firms, is meant to translate into real-world acceptance that a lone issuer would struggle to build. Whether that bet pays off is the open question, and history offers a cautionary example.

A cautionary precedent: the Centre Consortium

The consortium model has been tried before at the heart of the industry, and the result is instructive. When USDC launched in 2018, it was governed not by Circle alone but by the Centre Consortium, a governance body co-founded by Circle and Coinbase to oversee the coin as a neutral standard. In its early years, USDC was the shared project of two of crypto’s most important companies, with governance and economics split between them, a genuine consortium arrangement at the center of the stablecoin market.

That arrangement did not last. By 2023, Circle and Coinbase dissolved the Centre Consortium, with Circle taking full control of USDC’s issuance and governance and buying out Coinbase’s stake, replacing the shared structure with a revenue-sharing commercial agreement instead. The neutral, jointly governed body gave way to a single issuer with a distribution partner. The episode showed that a consortium can fracture, that aligning even two large partners over the long term is hard, and that the pull toward single-issuer control is strong once a coin becomes valuable.

The lesson for today’s consortium stablecoins is sobering but not disqualifying. Coordinating two founding partners proved difficult; coordinating 140 is a far larger challenge. At the same time, the Centre experience taught the industry a great deal about how to structure governance and economics, and the newer projects are designed with that history in mind. The precedent is a warning about durability, not a verdict that the model cannot work. It simply means the hardest part of a consortium stablecoin may not be launching it, but keeping the coalition together as the stakes rise.

Why the model matters

Consortium stablecoins matter because they attack the core economics of the incumbents and could reshape how digital dollars are built. By sharing reserve income, they threaten the single-issuer business model that has made Tether and Circle so profitable, and they put pressure on every issuer to justify keeping the float that stablecoins quietly earn. If businesses can earn a share of that income by supporting a shared coin, the competitive logic of the whole sector shifts, and that pressure is real regardless of which specific consortium succeeds.

The model also changes the incentives around adoption. A single issuer has to persuade partners to distribute its coin; a consortium gives those partners a financial stake in the coin’s success, turning distribution into a shared interest. Combined with neutral governance, this can make a consortium coin more attractive to businesses that do not want to depend on, or enrich, a single competitor. The breadth of backers in projects like Open USD is meant to convert that aligned interest into faster real-world acceptance across payments, banking, and commerce.

For the broader market, the rise of consortium stablecoins is part of a larger story in which crypto is replaying the history of banking, where whoever holds the deposit, or the digital dollar, ends up with more durable economics than whoever merely moves the transaction. The consortium model is an attempt to distribute that durable position across a coalition instead of concentrating it in one firm. That makes it a structurally significant development, not just another product launch, even though its ultimate success is far from guaranteed.

The risks of the consortium model

For all its appeal, the consortium model carries distinct risks that anyone evaluating it should weigh. The most fundamental is coordination. Aligning the interests of a large group of companies, each with its own priorities and competitors within the same coalition, is genuinely hard, and decision-making by committee can be slow and prone to deadlock. The Centre Consortium fractured with only two partners; a coalition of many faces a much steeper coordination challenge, and governance disputes could stall the roadmap or splinter the group.

A second risk is that consortiums have historically struggled to ship and sustain products. A launch-day roster of famous names is not the same as a working, widely adopted coin, and many industry consortiums across finance and technology have announced ambitious shared ventures that underdelivered. At announcement, a new consortium stablecoin typically has unproven contracts, reserves, and real-world usage, so the gap between a strong partner list and durable adoption is wide. The coin still has to win against the deep liquidity and entrenched network effects of incumbents like USDT and USDC, which will not stand still.

There are subtler concerns too. Concentrating governance among a group of large, powerful incumbents raises its own questions about who really controls the network and whose interests it ultimately serves. Regulatory clarity that favors well-capitalized entrants can entrench the biggest players instead of broadening competition. And a win for the consortium as a business does not automatically translate into benefits for the users, chains, or tokens associated with it. The consortium model is a serious and well-reasoned challenge to the single-issuer status quo, but it is an experiment whose durability will be settled by execution and by whether coalitions can hold together once the money at stake grows large.

Where consortium stablecoins fit among stablecoin types

To place the consortium model correctly, it helps to see the wider map of stablecoin designs, because the consortium approach is a variation on one branch of that map instead of a wholly separate species. The most common type is the fiat-backed stablecoin, where each token is backed by reserves of cash and safe assets like Treasury bills held by an issuer. Within that category sit the familiar single-issuer coins such as Tether’s USDT and Circle’s USDC, where one company holds the reserves and keeps the income. A consortium stablecoin is still a fiat-backed stablecoin; what changes is who governs it and who receives the reserve income, not what backs it.

Other branches of the map work differently. Crypto-collateralized stablecoins, such as those built on decentralized protocols, are backed not by dollars in a bank but by other cryptocurrencies locked in smart contracts, usually over-collateralized to absorb volatility. Algorithmic stablecoins attempt to hold their peg through supply-adjusting mechanisms instead of full reserves, a design that has repeatedly proven fragile and, in notable cases, collapsed. Yield-bearing stablecoins add a return for the holder on top of the peg, sharing reserve income or on-chain yield directly with users. These are distinct mechanisms for achieving or funding a stable value.

Seen against that backdrop, the consortium model is best understood as a governance-and-economics innovation layered onto the fiat-backed design. It does not change the fundamental promise, one token redeemable for one dollar held in reserve, and it does not introduce a new stability mechanism. What it changes is the ownership of the network: collective governance instead of a single controller, and shared reserve income instead of a single beneficiary. In that sense it sits alongside, not opposite, the single-issuer fiat-backed coins, offering the same product with a different distribution of power and profit.

This placement matters for how users should evaluate a consortium stablecoin. Because the backing is the same fiat-reserve model, the safety questions are the same ones that apply to any fiat-backed coin: what exactly is in the reserves, who holds and audits them, and what regulatory framework governs them. The consortium structure adds considerations about coordination and governance, but it does not remove the need to scrutinize reserves and compliance. A consortium coin is not safer or riskier by virtue of its governance alone; it is a fiat-backed stablecoin whose distinctive feature is shared control, and it should be judged on the fundamentals every stablecoin shares.

Frequently Asked Questions

What is a consortium stablecoin?

A consortium stablecoin is a fiat-backed token issued and governed by a group of companies instead of a single issuer. Its two defining features are shared governance, where a board drawn from the partners makes decisions collectively, and shared economics, where the interest earned on reserves is distributed among partners after a management fee, instead of kept by one company.

How is it different from USDT or USDC?

USDT and USDC are single-issuer stablecoins: one company, Tether or Circle, controls the network, holds the reserves, and keeps the interest those reserves earn. A consortium stablecoin spreads both control and reserve income across many partner companies. USDC is a partial hybrid, since Circle shares a large share of the economics with Coinbase, but Circle still controls issuance and governance.

What is an example of a consortium stablecoin?

The most prominent example is Open USD, backed by more than 140 companies including Visa, Mastercard, Stripe, BlackRock, and Coinbase, and governed by an independent body called Open Standard. Others include the Paxos-led Global Dollar Network, which shares reserve income with partners like Robinhood and Kraken, and Qivalis, a euro stablecoin venture formed by major European banks.

Why are consortium stablecoins becoming popular?

Three forces are driving them: clearer regulation, such as the 2025 GENIUS Act, which brought large regulated institutions into the market; the growth of the stablecoin sector past $300 billion, which raised the stakes; and a growing desire among partners to share in the reserve income that single issuers have kept. Competition has shifted from issuing tokens to controlling and sharing the underlying network.

How do consortium stablecoins make money for partners?

They share the interest earned on the reserves. A stablecoin holds dollars in safe assets like Treasury bills that earn interest, and in the consortium model that income is distributed among the participating companies after a management fee covers operating costs. This gives each partner a direct financial incentive to promote adoption, unlike single-issuer coins where the issuer keeps the reserve income.

What happened to the Centre Consortium?

The Centre Consortium was a governance body co-founded by Circle and Coinbase in 2018 to oversee USDC as a neutral standard. It was dissolved in 2023, when Circle took full control of USDC’s issuance and governance and bought out Coinbase’s stake, replacing the shared structure with a revenue-sharing agreement. It is a cautionary example that even a two-partner consortium can fracture over time.

Are consortium stablecoins safer than single-issuer ones?

Not inherently. Safety depends on the quality of the reserves, the regulatory framework, and the operator, not on whether governance is shared. A consortium can add neutrality and distributed control, but it also adds coordination risk and, at launch, unproven contracts and reserves. Users should evaluate any stablecoin on its reserve backing, regulatory standing, and transparency instead of assuming a governance model makes it safer.

What are the main risks of the consortium model?

The biggest risk is coordination: aligning many companies, some of them competitors, is hard, and committee governance can be slow or prone to disputes. Consortiums have also historically struggled to ship and sustain products, so a strong partner list may not translate into adoption. New consortium coins must also overcome the deep liquidity and network effects of entrenched incumbents like USDT and USDC.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or legal advice. The stablecoin sector is evolving rapidly, and the status of specific projects can change. Nothing here is a recommendation to buy, sell, or use any asset or product. Always do your own research and consult a qualified professional before making financial decisions. Information is accurate as of July 2, 2026, and may change.

Standard Chartered has become the first Global Systemically Important Bank (G-SIB) to offer institutional clients direct access to USDC minting and redemption, through a partnership with issuer Circle announced on July 2.

Eligible clients can convert dollars to USDC and back inside their existing banking relationship, with no separate Circle accounts required. However, the launch covers Dubai only, and a rival bank rolled out similar services three days earlier.

Standard Chartered USDC Access Starts in Dubai

The capability, developed with Circle, runs through the bank’s Dubai International Financial Centre (DIFC) operations.

It gives institutions a single onboarding route into USDC, which commands a $73.2 billion market cap.

Standard Chartered says the service supports on-chain settlement, treasury operations, and liquidity management, with payment use cases planned later. Expansion into additional markets depends on regulatory approvals and market readiness.

“Digital assets are becoming an increasingly important component of global financial infrastructure, and institutional clients are seeking the same levels of trust and governance that underpin traditional markets,” Roberto Hoornweg, CEO of Corporate and Investment Banking at Standard Chartered, said in the announcement.

Follow us on X to get the latest news as it happens

The relationship runs deeper than one launch. Standard Chartered has helped design the Circle Payments Network since April 2025, alongside Santander, Deutsche Bank, and Société Générale.

This week, the bank also initiated coverage of the DeFi lending protocol Morpho.

Rivals are Already Moving on USDC

It is imperative to note, however, that Standard Chartered is not the first. On June 29, BNY enabled clients to mint, redeem, and hold USDC through its Digital Asset Custody platform.

BNY is no fringe player. It custodies USDC’s reserves and oversees $59.3 trillion in assets under custody or administration.

More may follow. BNY says it plans to add further stablecoin issuers over time, while Standard Chartered cites growing demand from institutions and corporations for regulated stablecoin infrastructure.

Circle, meanwhile, has its own reasons to court bank partners. Its stock fell 15% last week after 140 firms, including Visa and Coinbase, backed rival stablecoin Open USD.

Bank distribution hands USDC deeper institutional rails just as its enterprise lead comes under attack.

Regulation will set the pace. Circle kept its European listings under MiCA while Tether’s USDT exited, yet Standard Chartered’s global rollout still awaits approvals market by market.

Whether treasurers route real settlement flows through bank-issued USDC rather than pilots will determine how quickly the rest of the G-SIB pack moves.

The post Two Big Banks Adopt Circle’s USDC Stablecoin This Week appeared first on BeInCrypto.

Earlier this week, Strategy unveiled a capital framework allowing selective bitcoin sales to fund preferred dividends, while authorizing preferred share repurchases and stock buybacks. It also set a minimum cash reserve covering 12 months of preferred dividend and interest payments. Its $2.55 billion cash balance currently covers about 17 months.

Hougan said the episode marks a broader shift in Strategy’s role within bitcoin markets. Rather than serving as crypto’s dominant, one-way buyer, the firm is likely to become a more flexible participant whose bitcoin purchases or sales depend on market conditions.

Looking ahead, Bitwise believes institutional investors, including asset managers, banks, pensions, endowments and sovereign funds, are positioned to replace Strategy as bitcoin’s primary source of demand.

More broadly, STRC volatility is seen as part of the leverage unwind that typically marks the late stages of every crypto cycle. As speculative excess is flushed from the system, the market moves closer to establishing a durable bottom, though the exact timing remains impossible to predict, the report added.

Wall Street bank JPMorgan said Strategy’s new policy allowing selective bitcoin sales to fund preferred dividends creates avoidable two-way risk, increasing uncertainty and market volatility.

Read more: JPMorgan says Strategy’s bitcoin sales policy adds ‘two-way risk’ to crypto markets

Arm Holdings (ARM) stock is up 194% this year. However, it has stalled and slipped since mid-June, and big investors are quietly selling. The reason is simple. Arm is the chip stock most exposed to rising interest rates.

The next test comes on July 14, when new inflation data is due. A hot reading would push the Federal Reserve closer to a rate hike. And Arm has the most to lose.

Big Money Started Leaving in Mid-June

The clearest warning comes from money flow. Chaikin Money Flow (CMF), a proxy for institutional buying, peaked at 0.37 around June 15 and has since fallen to 0.01. In plain terms, big buyers nearly vanished.

Note: Arm is based in the United Kingdom, but its shares trade in New York in US dollars, so Federal Reserve rate moves drive it like any American chip stock.

The timing is not random. Inflation hit 4.2% for the year on June 10, the hottest in three years. Days later, on June 17, the Federal Reserve held rates but signaled it may raise them. More so, institutional money began leaving in the run-up to the June 17 Fed meeting.

Since then, markets have gone back to pricing hikes. Robin Brooks, senior fellow at the Brookings Institution and former chief economist at the IIF, says one number will set the tone.

Here is why that hits Arm (ARM) hardest. A hot inflation report makes the Fed more likely to raise interest rates. Higher rates make profits expected years from now worth less today. Arm is the priciest big chip stock, and most of its profits sit far in the future. Investors are paying mainly for growth from its AI chip designs in the coming years, not for the money it makes today.

That makes Arm the most rate-sensitive name in its sector. Its price tends to move in the opposite direction of interest rates, and by more than any other big chip stock.

So it falls more than the average chip when rate fears rise. When a major bank warned of up to three more hikes on June 23, Arm dropped over 10% in a day.

Options Traders Turned Defensive Too

The options market flashed the same signal. Arm’s put-call ratio compares bets on a fall against bets on a rise. On June 15, with Arm near $412, the volume ratio was 0.51, so traders still bought more calls than puts.

Yet the open interest ratio was already 1.22, meaning longer-standing bets leaned bearish.

By July 1, with Arm near $337, both had turned bearish. The volume ratio jumped to 1.75, and open interest sat at 1.17.

In short, traders went from hopeful to defensive as rate-hike talk grew louder. The ARM price chart tells the same story.

The ARM Stock Chart Confirms the Warning

The rally was already running on empty. From May 6 to June 30, Arm rose, but the buying volume behind each move kept shrinking.

Want more insights like this? Sign up for Editor Harsh Notariya’s Daily Newsletter here.

That weakness stalled Arm at about $362. The stock now trades near $337, just under the $340 level it needs to hold.

If it breaks lower, $303, then $298, come into view. Far deeper support sits near $198 if the selling speeds up. To turn things around, Arm must reclaim $362 with strong buying, which would pull money flow back up. The real line, though, is $399 (the $400 zone).

Above $400, ARM regains genuine strength. Below it, with a hot July 14 report threatening another rate scare, every bounce is likely to be sold. The $400 mark separates a fresh leg higher from more selling into every rally.

The post Why a Hot July CPI Print Could Hit This Semiconductor Chip Hard appeared first on BeInCrypto.

Perpetual futures, once a niche crypto product, have become one of the industry’s fastest-growing markets. Alongside cryptocurrencies like bitcoin, trading platforms are increasingly listing contracts tied to equities, commodities and other real-world assets, blurring the line between crypto-native and traditional financial markets.

Led by former Revolut crypto head Ruslan Fakhrutdinov, Extended had processed more than $245 billion in trading volume as of June and supports more than 100 perpetual markets, according to the company.

The firm said it plans to expand into spot trading, tokenized real-world assets and multi-asset collateral.

“The first phase was building for DeFi natives,” Fakhrutdinov said in a statement. “The next is expanding the infrastructure and partnerships needed to support the next stage of onchain derivatives.”

The investment points to a broader race to become what is best described as the “everything exchange” or “everything app” for financial markets. Coinbase (COIN) has expanded into perpetual futures, Robinhood is pairing tokenized stocks with event contracts and commodity perps, and prediction market operator Kalshi recently entered the perpetual futures business.

As trading increasingly moves onto a blockchain environment, the lines separating brokerages, crypto exchanges and prediction markets are becoming harder to distinguish.

“Capital markets are increasingly converging with digital asset infrastructure,” Zengo managing director Ouriel Ohayon, said in a statement. “eToro’s investment in Extended reflects a mutual conviction that the future of trading will be digital, accessible and can operate 24/7, beyond the traditional trading week.”

[PRESS RELEASE – Victoria, Seychelles Islands, July 2nd, 2026]

Lizex.io, a rapidly growing instant cryptocurrency exchange platform, announces the full launch of its B2B partnership program targeting crypto wallets, exchangers, rate aggregators, and fintech products. The company is opening access to its infrastructure for business partners worldwide.

About the Partnership Program

Lizex.io provides partners with direct access to an API for cryptocurrency exchange, offering aggregated liquidity across 5,000+ coins, including BTC, ETH, XMR, USDT, SOL, BNB, and other major assets. Integration takes just a few hours, backed by dedicated 24/7 technical support.

Lizex.io acts as a liquidity layer for both crypto wallets and aggregators, delivering a continuous stream of competitive quotes and instant order execution on the partner’s side. This allows B2B clients to offer their users best-in-class exchange rates without having to independently aggregate liquidity sources.

Key features for B2B partners:

- Access to 5,000+ crypto coins with deep aggregated liquidity

- Fixed and floating exchange rates at the partner’s discretion

- White-label integration: no Lizex.io branding in the partner’s interface

- Competitive revenue share of up to 60% of transaction fees

- Embeddable widget requiring no development from scratch

- Full transparency: all fees are displayed before transaction confirmation

Market & Positioning

According to the company, in the first six months of 2026, the volume of exchange transactions via the Lizex.io API exceeded $380 million. The platform currently serves more than 40 active B2B partners across 20 countries, with an average swap completion time under 4 minutes.

Lizex.io positions itself as a reliable liquidity backbone for the crypto ecosystem — an alternative to building in-house exchange infrastructure for services looking to add swap functionality without high operational costs.

How to Become a Partner

Companies interested in joining the Lizex.io B2B program can apply via the official website at lizex.io or contact the partnership team directly. A first response is guaranteed within 24 hours.

About Lizex.io

Lizex.io is a non-custodial instant cryptocurrency exchange platform operating since 2024. The service enables fast, secure, and private transactions with no registration required. Lizex.io offers both a retail interface for end users and B2B infrastructure for business clients, including API access, embeddable widgets, and white-label solutions.

Website: https://lizex.io

Telegram: https://t.me/Lizex_Partnership

The post Lizex.io Launches Large-Scale B2B Partnership Program for Crypto Services appeared first on CryptoPotato.

Circle is facing one of its biggest challenges following the announcement of Open USD (OUSD), a new stablecoin backed by major financial and payments companies, including Visa, Mastercard, American Express, BlackRock, and Coinbase.

As speculation grew over what the new initiative could mean for USDC, Circle’s stock came under pressure. It has fallen about 12.7% over the past five trading days.

While incumbents still control the vast majority of the market, industry experts believe OUSD could significantly reshape the competitive landscape.

OUSD vs. USDC

In a conversation with CryptoPotato, Alex Witt, General Partner at Verda Ventures, said that “distribution is king” and value will accrue to built-in distribution networks. He explained,

“Circle, unlike Tether, does not own its primary distribution channels, as evidenced by Circle sharing 90% of USDC reserve yield with Hyperliquid, demonstrating its weak competitive position.”

As a result, Witt believes OUSD could “dramatically erode” the company’s first-mover advantage.

Meanwhile, Trace Finance co-founder and CEO Bernardo Brites described Open USD as “a real structural break” in the stablecoin market.

He said markets read the announcement as a direct threat to Circle, but also noted that skeptics have flagged real execution risks, including bootstrapping liquidity from zero, the lack of trading pairs against major crypto assets, governance friction from coordinating many stakeholders, and a thin fee model that could leave OUSD under-resourced.

Even so, Brites argued that Open USD’s consortium is “bigger than anything the USDG consortium assembled,” referring to the consortium behind Paxos-issued USDG.

“Getting the major card networks, processors like Adyen, and banks like BNY and Cross River behind a single stablecoin is unprecedented. Distribution has always been the hardest problem in stablecoins, and OUSD is launching with more of it than any issuer before.”

Allaire: OUSD’s Model Could ‘Starve an Infrastructure’

Circle CEO Jeremy Allaire, however, pushed back against many of the arguments made in favor of the new stablecoin. In a tweet, Allaire said that stablecoin networks are platform and network effect businesses that tend towards “winner-take-most market structures,” while suggesting that years of network building matter more than newly announced consortia.

Responding to OUSD’s revenue-sharing model, the exec said Circle already shares the majority of its income with distribution partners, and added that “giving away all the income is a recipe for starving an infrastructure.” He also remains skeptical of OUSD’s governance model and argued that the track record of consortium products achieving scale, product-market fit, or even basic product agility is “absolutely dismal.”

“We actually tried this in the early days of USDC, and even with a very small group, ran into endless challenges and complexity.”

While acknowledging the new entrant, Allaire said Circle’s partnership with Coinbase “remains as strong as ever” and went on to say that he expects many of OUSD’s founding members to remain USDC partners and customers.

The post Can Circle Defend Its Stablecoin Lead Against OpenUSD? Experts Weigh In appeared first on CryptoPotato.

While Ethereum’s overall market structure is still dominated by the sellers, recent price action suggests sellers may be losing momentum after the market was held by the $1.5K support region twice. The emergence of a potential double bottom and improving short-term momentum could pave the way for a relief rally if buyers reclaim the next resistance cluster.

Ethereum Price Analysis: The Daily Chart

On the daily timeframe, ETH is still trading within the same long-term descending channel that has remained intact for months, with both the long-term moving averages sloping lower just above the channel’s higher boundary. The price remains well below the 100-day and 200-day moving averages, which are currently positioned around the $2K to $2.2K region, confirming that the macro trend is still bearish.

After the sharp sell-off a few weeks ago, the cryptocurrency found strong demand inside the $1.5K support zone. The price has now tested this area twice, raising the possibility of a double-bottom formation. Although the pattern is not confirmed yet, the repeated defense of this support suggests that bearish momentum is fading.

The RSI has also recovered from near-oversold conditions and is gradually pushing higher toward the midline, indicating improving momentum without reaching overbought territory.

For the bullish scenario to gain credibility, ETH needs to reclaim the $1.8K resistance zone to validate the double bottom setup. A successful move above that level would also expose the next major supply area around $2K to $2.2K, where the 100-day and 200-day moving averages converge.

Conversely, losing the $1.5K support zone could likely prove catastrophic, as it would invalidate the potential reversal structure and likely trigger a deeper leg lower within the broader downtrend.

ETH/USDT 4-Hour Chart

The 4-hour chart presents a clearer short-term picture. The price has built liquidity beneath the $1.5K lows, as buyers stepped back into the market, preventing a lower low. This demand is gradually pushing ETH toward the first area of overhead supply.

The price is currently approaching a key fair value gap at approximately $1.7k. This imbalance coincides with the latest bearish impulse and is likely to attract selling interest. A decisive breakout above this zone would signal improving short-term strength and could open the path toward the $1.85K resistance.

Momentum has also noticeably improved on the lower timeframe, with the RSI climbing toward bullish territory while printing higher lows alongside price. This suggests buyers have regained some control after the recent rebound.

However, unless ETH successfully clears the fair value gap and establishes higher highs, the current advance could still develop into nothing more than a corrective rally within the larger bearish trend.

Sentiment Analysis

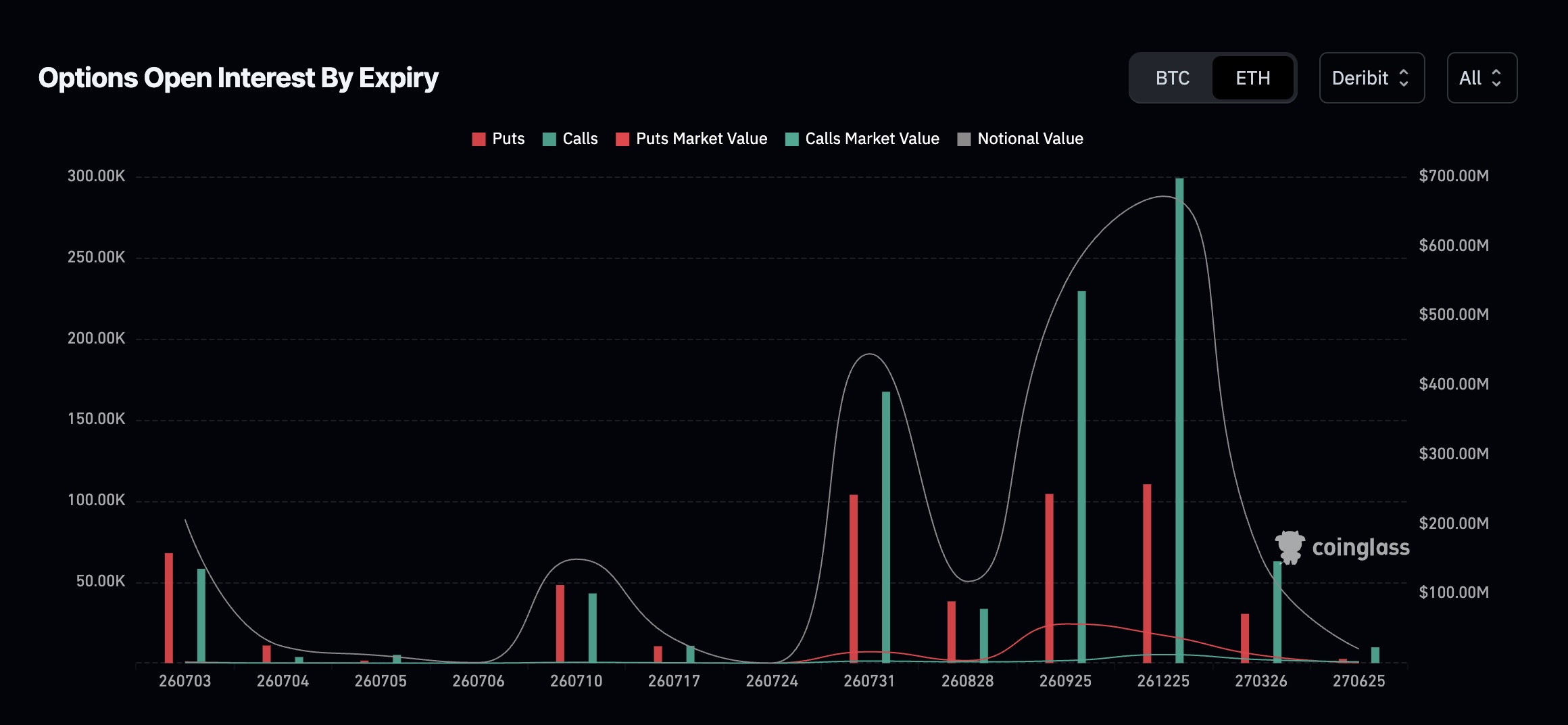

The distribution of open interest in options contracts shows that the largest concentration is positioned around the late December 2026 expiry, where call open interest significantly outweighs put open interest. Several other major expiries, including late September and late July, also display a clear dominance of call positioning.

This skew toward call options suggests that derivatives participants continue positioning for higher prices over the medium to long term despite Ethereum’s recent weakness. At the same time, the substantial notional value concentrated around the larger expiries indicates that these dates could become important volatility catalysts as expiration approaches.

While options positioning alone does not guarantee a bullish outcome, the current distribution reflects a market that still maintains longer-term upside expectations even as spot price remains trapped below major technical resistance. If ETH confirms the developing double-bottom structure and breaks above the nearby resistance cluster, the optimistic options positioning could provide additional tailwinds through improved market sentiment.

The post Ethereum Eyes Relief Rally as Double Bottom Forms Near $1.5K (ETH Price Analysis) appeared first on CryptoPotato.

Pi Coin price has edged higher after Pi Network introduced three ecosystem upgrades, while buyers stepped in following the token’s fresh all-time low and a broader crypto market rebound lifted sentiment.

Summary

- Pi Coin edged higher after Pi Network launched SoloHost, Pi Sign-In, and PiVerify during its Pi2Day event.

- A rebound from oversold conditions lifted PI, but a potential bearish flag continues to weigh on the short-term outlook.

- Large monthly token unlocks and limited exchange listings remain the biggest obstacles to a sustained recovery.

According to data from crypto.news, PI price traded near $0.115 on July 2, up around 0.5% over the past 24 hours after the Pi Core Team unveiled SoloHost, Pi Sign-In, and PiVerify during the Pi2Day event. The move also came as derivatives activity improved, with open interest climbing back above $20 million after falling during last week’s selloff.

Pi Network said SoloHost allows developers to build AI-powered applications on its infrastructure, while Pi Sign-In offers a unified authentication system for decentralized applications. PiVerify gives third-party businesses access to Pi’s network of more than 18 million KYC-verified users, creating an additional use case that requires developers and businesses to interact with the ecosystem.

At the same time, macro conditions favored risk assets. Bitcoin climbed back above $61,000 and briefly traded beyond $62,000 after weaker-than-expected U.S. June jobs data strengthened expectations that the Federal Reserve could cut interest rates later this year. The rally added roughly $50 billion to the total crypto market capitalization and helped several altcoins post intraday gains alongside PI.

Oversold bounce meets bearish chart structure

PI’s latest uptick followed a sharp decline that pushed the token to a fresh all-time low near $0.1141 on July 1. The daily Relative Strength Index dropped to around 27 before buyers returned, giving the token a foothold around the $0.115 support zone.

The 4-hour chart, however, continues to favor sellers. PI has formed what appears to be a potential bearish flag, with price moving inside a narrow ascending channel after the steep decline from roughly $0.132. A descending trendline has rejected every recovery attempt since late June, while the Supertrend indicator remains above price near $0.121.

The MACD has started to improve, with the histogram returning above zero and the MACD lines curling upward. Buyers still need to reclaim several resistance levels before the short-term structure changes. Fibonacci retracement levels place the first barriers near $0.116, $0.120, and $0.123, while a move above the descending trendline and Supertrend would weaken the bearish setup.

Token unlocks remain the biggest downside risk

Supply pressure continues to overshadow the network’s new utility releases. PiScan data shows between 76 million and 149 million PI tokens are scheduled to unlock during rolling 30-day periods, while more than 1.7 billion tokens are expected to enter circulation over the next 12 months.

The steady increase in liquid supply has consistently outpaced demand and remains the main reason PI continues to trade near record lows. Liquidity also remains limited because Binance, Coinbase, and Bybit have yet to list the token.

A breakdown below the lower boundary of the four-hour bearish flag and the recent $0.111 low would strengthen the bearish case and expose fresh all-time lows.

On the upside, sustained buying above $0.120-$0.121, supported by growing adoption of SoloHost, Pi Sign-In, and PiVerify, would invalidate the current bearish pattern and open the door for a recovery toward $0.123-$0.125.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

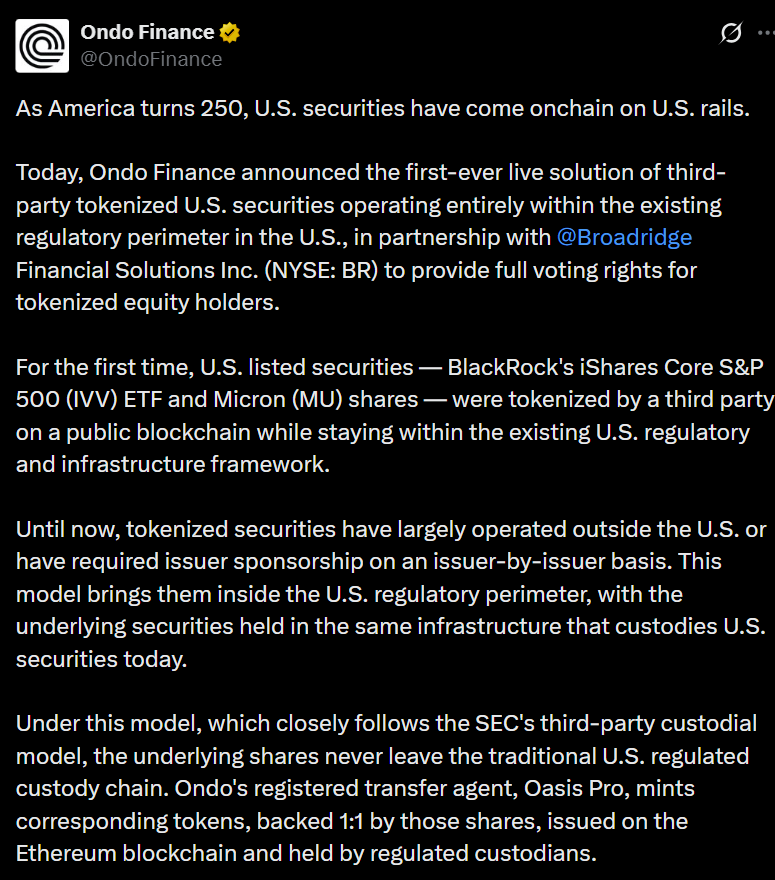

Ondo Finance is adding shareholder voting rights to its tokenized stocks and exchange-traded funds (ETFs) through a partnership with financial infrastructure provider Broadridge, addressing one of the key limitations of blockchain-based securities.

The companies announced Thursday that holders of more than 250 tokenized securities issued through Ondo will be able to participate in proxy voting and access corporate communications, including regulatory filings and other shareholder documents.

The integration uses a Web3-enabled version of Broadridge’s investor communications platform, allowing users to authenticate with blockchain wallets while accessing governance services typically reserved for shareholders in traditional markets.

The move comes as tokenized equities gain momentum among digital asset companies seeking to bring conventional financial products onchain. While tokenization promises faster settlement and around-the-clock trading, questions have remained over whether investors would receive the governance rights that accompany traditional direct stock ownership.

Source: Ondo Finance

Ondo said the governance features will accompany the launch of its first US custodial tokenized securities, including tokenized versions of BlackRock’s iShares Core S&P 500 ETF (IVV) and Micron Technology (MU). The company said the assets are the first issued under the US Securities and Exchange Commission’s third-party custodial framework for tokenized securities.

Related: Blockchain.com deepens onchain stock offerings as tokenized equities market grows

Competition heats up in tokenized equities

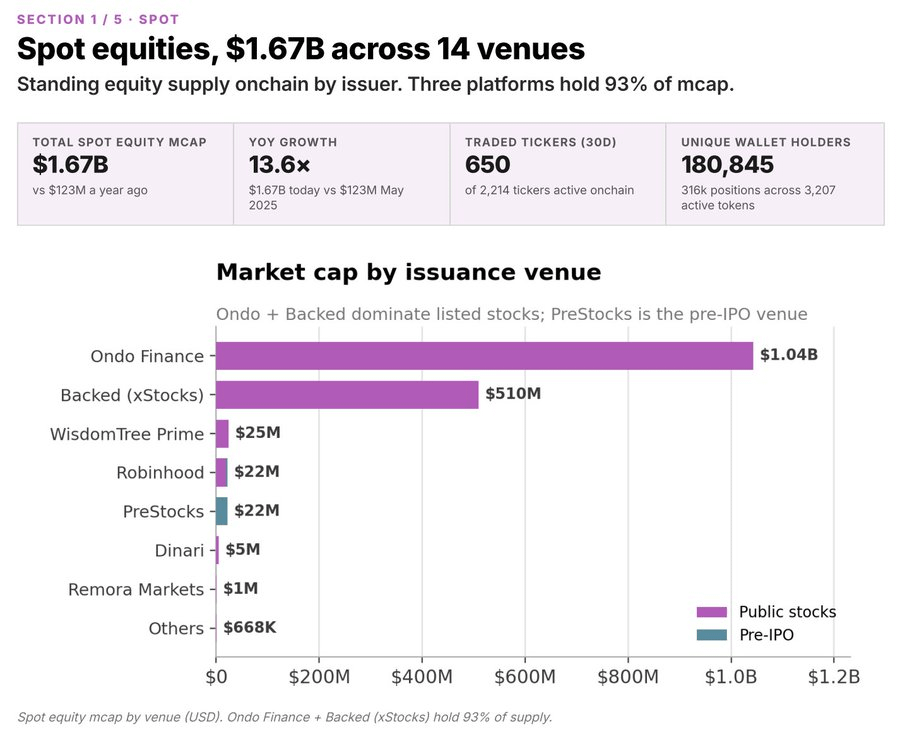

The market for tokenized stocks has expanded rapidly this year, as its total value first surpassed $1 billion in March, according to Foresight Ventures. Data published by Ondo on Wednesday showed the market has since grown to $1.67 billion, with nearly 181,000 unique holders.

Ondo is one of several companies competing for a share of the fast-growing market. Backed Finance, which issues tokenized stocks through its xStocks platform, has also expanded its footprint, with its products now available across multiple crypto exchanges and blockchain networks.

The market for tokenized stocks has grown nearly 14-fold since May 2025. Source: Ondo Finance

Tokenization has emerged as one of crypto’s fastest-growing sectors in 2026, defying broader market weakness. A recent 21shares report attributed the trend to rising institutional adoption and improving infrastructure. Separate data from Binance showed the value of tokenized real-world assets, including stocks, has surged nearly 600% over the past year.

Related: Crypto Biz: The cost of stacking sats

DeFi lending protocol Aave has expanded its multi-chain footprint by deploying its V3 lending markets on Monad, a layer-1 network designed to run Ethereum-compatible applications. The rollout introduces Aave on Monad with 12 supported assets at launch, aiming to give Monad users an established borrowing venue and to accelerate liquidity formation via incentives.

In its announcement on Thursday, Aave said the initial markets include USDT, USDC, Aave’s GHO stablecoin, USDe, mUSD, AUSD, WETH, cbBTC, wstETH, weETH, syrupUSDC, and sUSDe. It also highlighted that this is Aave’s first deployment with Chainlink Smart Value Recapture enabled from day one, a mechanism that redirects part of the value generated from liquidations back to the protocol.

Key takeaways

- Aave V3 is live on Monad with markets for 12 assets, including GHO and multiple stablecoin and wrapped-asset pairs.

- Chainlink Smart Value Recapture is enabled from launch, redirecting a portion of liquidation-generated value back to Aave.

- Governance materials show Monad’s ecosystem support includes $15 million in incentives over the first 12 months and additional GHO commitments.

- A risk assessment cited concerns about early activity on Monad compressing after an initial strong start, with liquidity remaining concentrated in established protocols.

What Aave V3 brings to Monad

The deployment matters for Monad because it moves beyond isolated DeFi activity and adds a battle-tested lending framework with liquidity incentives and a mature stablecoin ecosystem. Aave’s governance proposal notes that Monad is compatible with Ethereum’s application environment, meaning developers can reuse existing Solidity contracts and Ethereum tooling with minimal changes.

Aave also positioned the launch as more than a deployment checklist: it is meant to connect Monad’s users to GHO and to borrowing/lending liquidity designed for sustained market use. In addition to the asset list, Aave underscored the strategic role of Chainlink Smart Value Recapture in its liquidation flows, which can affect how value accrues on the protocol side and how incentives are structured during early adoption.

Incentives to jump-start liquidity—plus a reality check

Aave’s governance documentation indicates that the Monad Foundation committed $15 million in incentives during the first 12 months following activation. The foundation also agreed to acquire and retain 10 million GHO for more than six months, while the Aave DAO committed an additional 500,000 GHO in incentives to support onboarding on Monad.

That funding structure is designed to reduce early friction for borrowers and suppliers, but it does not automatically guarantee long-term utilization. A risk assessment by LlamaRisk pointed to a key uncertainty: while Monad’s mainnet launched on Nov. 24, 2025, network usage reportedly softened after a strong start. As of June 8, LlamaRisk estimated Monad’s total value locked at about $359.5 million, while noting that liquidity remained concentrated in already established protocols.

LlamaRisk backed the Aave deployment with conservative initial parameters, explicitly citing Monad’s short operating history at the time of evaluation. The practical takeaway for investors and traders is that incentive-backed liquidity often looks strong early, but the sustainability of borrow/supply activity will be tested as rewards decline and market participants decide whether to stay without continued subsidization.

Why tokenized assets could make lending more important

The Aave-on-Monad rollout lands as tokenized real-world assets (RWAs) increasingly intersect with DeFi lending strategies. Earlier coverage noted that institutions are looking at ways to bring tokenized assets into DeFi lending markets, and Standard Chartered previously said that tokenized assets entering DeFi could drive deposits into Aave. According to that same earlier reporting, Aave’s deposit base reached roughly $75 billion at its October 2025 peak.

Meanwhile, Centrifuge has discussed bringing tokenized Treasurys, private credit, and AAA-rated collateralized loan obligations to Monad for use across lending, collateral, and secondary-market activity. While the input does not indicate that Centrifuge assets have been integrated into Aave yet, the logic for Monad users is straightforward: if tokenized asset issuers expand into Monad, having an established lending venue such as Aave V3 can lower the barrier for turning those assets into productive borrowing and collateral workflows.

What to watch after the launch

Aave’s deployment gives Monad an immediate, Ethereum-compatible lending destination with a defined set of markets and liquidation value-sharing mechanics. The next signal that will matter most is whether borrowing demand and supply growth persist after early incentives—particularly given LlamaRisk’s observation that activity compressed after Monad’s initial strong start and that liquidity was concentrated in established venues. Readers should watch for changes in utilization across the new Aave markets and for any confirmed integration of tokenized asset products into Aave on Monad as the ecosystem develops.

Why can’t the US appeal against Balogun’s red card?

‘Good growth’: Manchester summit debates what Andy Burnham’s big vision for the UK might look like

Two Big Banks Adopt Circle’s USDC Stablecoin This Week

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics6 days ago

Politics6 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World3 days ago

Crypto World3 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics7 days ago

Politics7 days agoPotential 2028er World Cup attendee leaderboard

-

Business6 days ago

Business6 days agoAsia stock markets slide as tech shares slump

-

News Videos4 days ago

News Videos4 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech7 days ago

Tech7 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World7 days ago

Crypto World7 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World5 days ago

Crypto World5 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Tech3 days ago

Tech3 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Business3 days ago

Business3 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World6 days ago

Crypto World6 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports6 days ago

Sports6 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World7 days ago

Crypto World7 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech5 days ago

Tech5 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech5 days ago

Tech5 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World6 days ago

Crypto World6 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRTX holders must register wallets before token distribution begins

-

Crypto World6 days ago

Crypto World6 days agoTether (USDT) Passes Ether in Market Cap as ETH Drops Toward $1.5K

-

Sports1 day ago

Sports1 day agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

You must be logged in to post a comment Login