Crypto World

Ripple Receives Full MiCA License After EU Crypto Deadline

Ripple said it has received full authorization under the European Union’s MiCA crypto framework after Luxembourg’s financial regulator granted the company a Crypto Asset Service Provider (CASP) license.

The authorization follows Ripple’s preliminary approval in June and, together with the company’s existing Electronic Money Institution license, allows the blockchain payments company to offer regulated crypto-asset services across the European Economic Area (EEA).

Ripple said the approval makes it one of a small number of digital asset companies with full authorization under MiCA. The company now holds more than 75 regulatory licenses worldwide, including authorization from the United Kingdom’s Financial Conduct Authority secured in January.

“This CASP authorisation means Ripple enters the post-transitional MiCA era fully compliant and ready to scale,” said Cassie Craddock, Ripple’s managing director for the United Kingdom and Europe.

Source: Cassie Craddock

Related: Binance outflows triple to $1.2B as ETH withdrawals hit 3-year high

Europe begins enforcing MiCA crypto rules

Ripple’s approval follows the end of the European Union’s MiCA transition period on July 1, when crypto companies were required to obtain authorization or cease offering regulated services in the bloc. The framework allows authorized companies to generally passport regulated crypto services throughout the EEA under a single license.

On Friday, the European Securities and Markets Authority (ESMA) published an updated register listing 280 licensed crypto-asset service providers. The total rose from 243 a week earlier after 37 companies, including Standard Chartered, FalconX and Sygnum Europe, were added.

Not every company secured MiCA authorization before the deadline. Binance, the world’s largest cryptocurrency exchange by trading volume, withdrew its MiCA application in Greece ahead of the July 1 transition and said it would pursue authorization in another member state while taking steps to comply with the bloc’s new rules.

The bloc has now entered MiCA’s enforcement phase, with unauthorized crypto companies expected to wind down operations or face penalties. While ESMA coordinates supervision and maintains the bloc’s register of authorized crypto companies, day-to-day enforcement is carried out by national regulators, meaning implementation is likely to vary across member states.

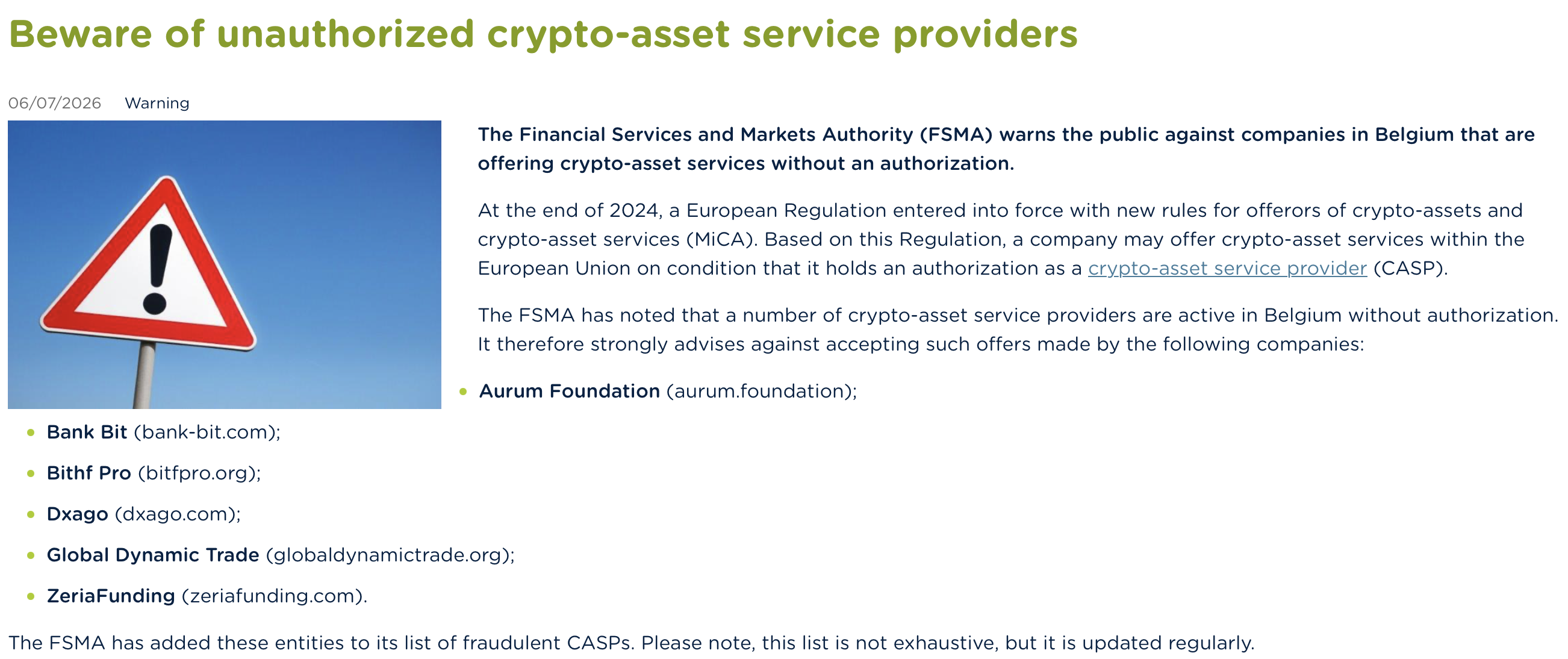

Belgium’s Financial Services and Markets Authority has already begun applying the new rules. On Monday, the regulator identified six crypto-asset service providers it said were operating without authorization and added them to its list of unauthorized crypto-asset service providers.

Belgium’s FSMA warns against unauthorized crypto providers. Source: FSMA

Magazine: Japanese pension fund tips 1% in crypto, G7 urges action on NK hackers: Asia Express

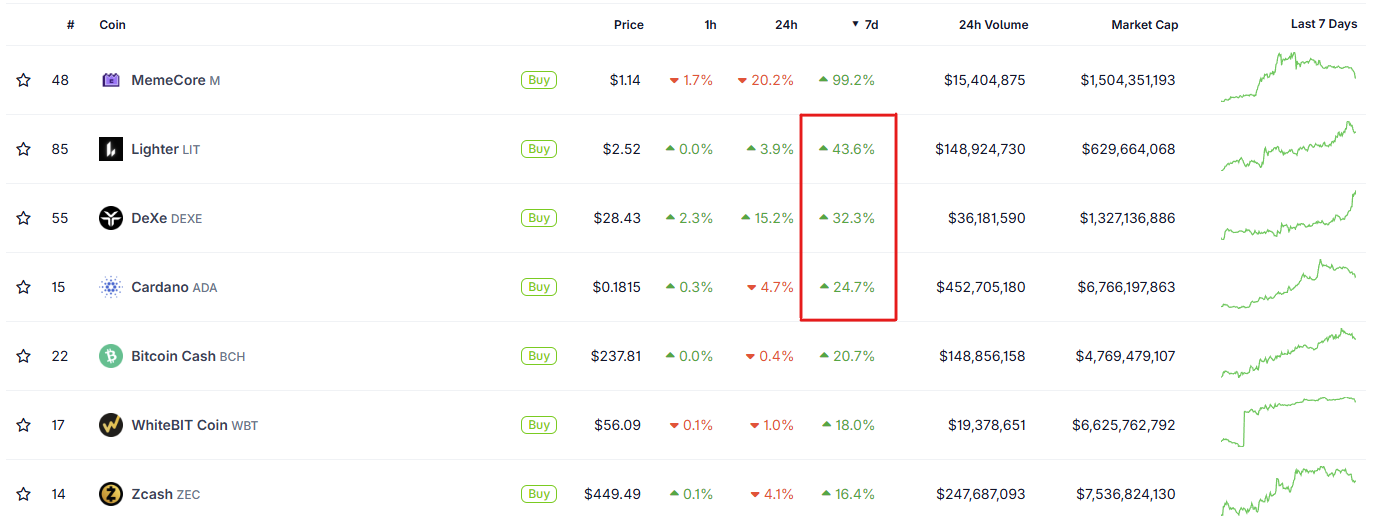

DeXe (DEXE), Lighter (LIT), and Cardano (ADA) rank among the biggest weekly gainers in the top 100 cryptocurrencies, making them the top coins to watch this week. Each enters the second week of July at a different stage of its trend.

According to CoinGecko, MemeCore (M) posted a larger seven-day gain, but a 20% daily drop disqualified it from this list. The three remaining leaders present two breakouts and one contested rebound.

Coins to Watch: DEXE Cup and Handle Breakout Targets $30

The DEXE weekly chart shows a completed cup-and-handle pattern. The token broke out in May 2026, then retested the 0.618 Fibonacci retracement near $15.62 before resuming its climb.

The retest started a three-week rally, and DEXE now trades near $28.39 after gaining 30% in seven days. As a result, the token is holding above the $24.20 resistance zone, its highest price in over a year. DEXE also led the previous altcoin watchlist at the start of July.

The first target from the formation sits at $30.31, which matches the 1.272 external Fibonacci level. The second waits at $38.09, the 1.618 extension. Reaching it would require a new record above the 2021 peak of $32.38.

However, volume has declined during the rally, which suggests the market remains calm rather than overheated. A second bearish divergence may also form on the weekly RSI. Continued price growth would cancel that signal and keep the structure healthy.

LIT Rally Extends Beyond Its First Target at $2.42

Lighter’s daily chart shows the token trading at its highest level since January. LIT gained nearly 48% over seven days and now trades near $2.54.

The rally already reached its first target at $2.42, the 1.272 external Fibonacci level. The next objective stands at $2.87, the 1.618 extension.

An ascending trendline supports the move, together with a strong demand zone near the $2.00 January high. Meanwhile, a recent tokenomics overhaul introduced permanent burns and a revamped staking model, providing the rally with a fundamental base.

The daily RSI reads about 77 with no bearish divergence, and volume remains high. However, readings this elevated often precede short cooling periods, so a dip toward $2.00 would not break the structure.

ADA Rebound Faces Its First Major Test at $0.205

Cardano was the strongest large-cap gainer last week, rising 26% in seven days. The move began at a multi-year low of $0.1382 and lifted ADA to about $0.20 before a pullback to $0.1818.

That peak almost matches the 0.382 Fibonacci retracement at $0.2052. Historically, this area marks a typical zone for a corrective bounce within a downtrend rather than a reversal.

ADA broke down from a descending parallel channel in early June and reached its support target near $0.15. If the recovery continues, the price may retest the channel’s lower band. The next resistance stands at the 0.5 retracement near $0.2259.

Volume remains high, but the daily RSI peaked near 65 and has slipped to about 56. In contrast, on-chain data shows the network added almost 15,000 new wallets after June’s crash, which supports the recovery case.

Key Levels for This Week’s Coins to Watch

A confirmed RSI divergence and fading volume would weaken the DEXE setup, while a LIT close below $2.00 would end its breakout structure. For ADA, the difference between a corrective bounce and a trend change rests on a daily close above $0.2259.

MemeCore’s recent crash shows how fast vertical rallies can unwind, which is why these invalidation levels matter this week.

The post Top 3 Crypto to Watch in the Second Week of July 2026 appeared first on BeInCrypto.

Key Takeaways

- Rivian manufactured 12,613 vehicles and handed over 12,194 units in Q2 2026, surpassing its projection of 9,000–11,000 deliveries

- Full-year 2026 delivery expectations were increased to 65,000–70,000 vehicles from the previous 62,000–67,000 range

- Shares of RIVN climbed approximately 6% following the announcement, building on the prior week’s 10.2% increase

- Investment firm Baird maintained its Outperform rating with a $23 price objective, suggesting about 23% potential upside

- The quarterly performance benefited from EDV commercial van sales, R1 vehicle lineup, and initial R2 model shipments

Rivian (RIVN) is currently changing hands at $19.76, climbing roughly 6% on Monday, building momentum from the previous week’s 10.2% surge after the electric vehicle manufacturer reported quarterly delivery figures that substantially exceeded its own projections.

Rivian Automotive, Inc., RIVN

The automaker manufactured 12,613 units and completed deliveries of 12,194 vehicles throughout the three-month period concluded June 30. These numbers significantly outpaced Rivian’s internal projections of 9,000 to 11,000 deliveries.

Year-over-year delivery volume expanded by nearly 14%. The outperformance stemmed from robust demand for its electric commercial vans and R1 product line, combined with the commencement of R2 shipments — a development investors have been eagerly anticipating.

In response to these results, Rivian elevated its full-year 2026 delivery projections to a range of 65,000 to 70,000 vehicles. This represents an increase from the previous bracket of 62,000 to 67,000 — marking a 3,000-vehicle boost at the median point.

This represents an unusual positive development for a company whose public market history has been characterized more by missed projections than exceeded expectations.

Wall Street Analysts Express Support

Baird confirmed its Outperform rating and maintained its $23.00 price objective after reviewing the delivery data. With current trading levels between $18.63 and $19.76, this target suggests potential appreciation of approximately 23%.

Canaccord and Needham similarly reaffirmed Buy ratings, contributing to the favorable analyst sentiment surrounding the stock this week.

Baird’s projection had represented the most optimistic forecast among Wall Street firms, and Rivian’s actual delivery number fell marginally short of it — though still exceeded the broader consensus. The firm adjusted its financial model to incorporate the Q2 results while maintaining its rating.

One concern analysts highlighted: Rivian’s gross profit margin currently stands at merely 1%, which continues to represent a significant challenge despite improving production volumes.

R2 Introduction Provides Growth Narrative

The second quarter represented the beginning of R2 deliveries. Although volumes remain modest, production acceleration is anticipated throughout the latter half of 2026.

The R2 represents a more compact, affordably-priced vehicle targeting a wider consumer audience compared to the R1 trucks and SUVs. Rivian has characterized it as the product capable of achieving meaningful production scale.

Commercial van shipments through the EDV initiative also bolstered quarterly performance. This business segment has demonstrated consistent results, despite receiving less market attention than the consumer vehicle division.

Visible Alpha analysts forecast Rivian will achieve 63,138 total vehicle deliveries for the complete year — modestly under the midpoint of the revised guidance range, indicating some Wall Street observers maintain cautious expectations regarding production acceleration.

Looking Ahead

Rivian plans to release complete Q2 2026 financial results on July 30, following market closure. A live audio presentation is scheduled for 5:00 p.m. ET to discuss operational performance and forward outlook.

RIVN has gained 1.8% year-to-date but remains 12% beneath its 52-week peak of $22.45, established in December 2025.

Key Takeaways

- MRNA reached a 52-week peak of $81.42, representing a 169.2% annual increase

- Six-month performance shows a remarkable 124% climb

- InvestingPro identifies the stock as trading above its Fair Value calculation

- Wall Street analysts hold an average “Reduce” stance with a $37.13 mean target

- Corporate insiders have offloaded 125,088 shares totaling more than $6.1 million over 90 days

Moderna shares peaked at $81.42 on July 6, establishing a fresh 52-week record and continuing what has become one of biotech’s most dramatic rallies this year. Trading hovered around $81.51 shortly thereafter, pushing the company’s market capitalization to approximately $32.2 billion.

The 52-week floor stands at $22.28. This positions MRNA with more than a triple-digit gain from its nadir — specifically, a 169.2% total return over twelve months.

The half-year climb alone registers at 124%, fueled partly by revitalized enthusiasm for Moderna’s mRNA technology and multiple developmental announcements.

During its Science Day presentation, Moderna disclosed that mRNA-6007, its in vivo CAR-T initiative, is advancing into preliminary development targeting autoimmune conditions, particularly systemic lupus erythematosus and related B cell-driven disorders.

Regulatory developments also contributed momentum. An FDA advisory panel delivered a unanimous endorsement for Moderna’s experimental seasonal influenza vaccine, mRNA-1010, for the 50-and-over demographic — representing a significant validation for the company’s expanding portfolio.

Options market participants responded actively. Contract volume reached 121,257, with substantial interest concentrated in the June 18, 2026 $65 call option.

Wall Street Remains Unconvinced

Notwithstanding the share price momentum, the analyst consensus tells a starkly different story. Moderna holds an aggregate rating of “Reduce” with a consensus price objective of merely $37.13 — representing less than 50% of current trading levels.

Goldman Sachs elevated its projection from $43 to $49 while maintaining a “neutral” stance. Bank of America adjusted upward from $32 to $34 but preserved an “underperform” rating. Barclays increased from $25 to $48 with “equal weight.” Both Jefferies and UBS maintained “hold” recommendations.

Among analysts tracking MRNA, two assign it a Buy rating, eleven suggest Hold, and five recommend Sell.

InvestingPro analytics position the equity among the platform’s most overextended securities when measured against its Fair Value assessment.

Corporate Leadership Reduces Positions

While institutional investors have been accumulating shares, company insiders have been liquidating positions. Board member Abbas Hussain divested 5,682 shares at $46.63 on May 1, trimming his holdings by 32%. Board member Noubar Afeyan sold 9,263 shares at $46.84 on May 21, decreasing his position by 70.24%.

Cumulatively, corporate insiders have liquidated 125,088 shares valued at more than $6.1 million during the previous 90-day period. Insider ownership currently represents 10.80% of outstanding shares.

Regarding institutional activity, the trend appears more constructive. Louisiana State Employees Retirement System established a fresh position of 17,700 shares valued at approximately $899,000 during Q1. AQR Capital, NewEdge Advisors, and American Century Companies similarly expanded their holdings. Institutional ownership now accounts for 75.33% of MRNA.

The company’s latest quarterly disclosure, published May 1, revealed Q1 revenue of $389 million — representing a 260.2% year-over-year expansion and significantly exceeding the $236.37 million analyst estimate. Earnings per share registered at -$3.40, falling short of the consensus forecast of -$3.02. The stock’s 50-day moving average currently sits at $53.50, while its 200-day average rests at $48.22.

In 2025, OpenAI raised funding at a $300 billion valuation. That number didn’t come from a single product launch or a breakthrough sitting in a lab somewhere. It came from usage, hundreds of millions of people opening ChatGPT every day, asking it questions, writing code with it, drafting emails through it, editing documents, building entire workflows around it, for years on end. That accumulated usage is the actual asset behind the valuation. It’s what proved the product worked at scale, what justified the pricing, and what ultimately convinced investors the company was worth funding at that number.

However, none of the people who generated that usage own any part of what it built. They paid a subscription, used the product, and walked away with nothing beyond the product itself. Stargate LLM is built around a different premise: that the people generating a platform’s usage should have a way to benefit from the value that usage creates, not just the company running it.

Where the $300 Billion Actually Came From

This isn’t a criticism of OpenAI’s business model so much as a description of how it works, and how every major AI platform’s valuation works. A company’s worth is built on engagement, retention, and the size of its active user base. ChatGPT’s usage numbers are the reason a $300 billion valuation was possible at all. Anthropic followed a similar trajectory, crossing $30 billion in annualized revenue in April 2026, again driven by daily usage from people using Claude for work, research, and everyday tasks.

The structure is consistent across the industry: users generate the data, the engagement, and the subscription revenue that make these companies valuable. The equity upside from that value sits with venture capital firms and early investors. The people doing the actual using never had an ownership stake to begin with, so there’s nothing for them to be paid out from.

Why This Structure Exists

This isn’t unique to AI. It’s how venture-backed software has worked for two decades. Google’s search engine ran on free usage from billions of people while a small group of early backers and employees became billionaires. The pattern repeats because private companies aren’t required to offer public equity, and by the time an IPO happens, if it happens at all, the earliest and steepest growth has usually already occurred. The users who built the company’s value in the meantime were never in a position to hold any of it.

AI has simply made this pattern more visible, because the scale is bigger and the growth is faster. A $300 billion valuation built substantially on usage is a bigger number than most historical examples, which is part of why it’s drawing more attention now than the same dynamic did with earlier tech platforms.

What Stargate LLM Does Differently

Stargate LLM is built around a different assumption: that usage itself should generate a return for the person doing the using, not just for the company running the platform. The mechanism for this is Proof of Usage, one of the largest allocations in Stargate’s tokenomics, with 50% of the total 150 billion coin supply, 75 billion Stargate coins, set aside specifically to reward users for real platform activity: conversational AI queries, image and video generation, referrals, staking, and structured feedback that improves the models.

This is a structural difference, not a marketing claim. The Stargate coin is required for core platform functions, subscriptions, credits, premium model access, which means usage and coin demand are directly connected from day one. Staking in the Stargate Vault adds a second layer: locked coins earn rewards drawn from platform revenue and the usage rewards pool, with governance votes determining how a portion of that revenue gets distributed to stakers over time. It means that the people generating the platform’s usage have a mechanism to benefit from that usage that ChatGPT and Claude’s user bases simply don’t have.

Stargate’s presale is where early access to this model is currently priced. It runs across ten escalating batches, from $0.0005 up to $0.0125, building toward a $0.025 launch price target, with Batch 1 entering at a 50x ratio to that target. Of the fixed 150 billion coin supply, 96% is allocated to community, ecosystem, and presale participants, with just 1% going to the core team, a deliberate contrast to the ownership concentration typical of venture-backed AI companies.

The Bottom Line

OpenAI’s $300 billion valuation and Anthropic’s $30 billion in revenue are both real, and both were built substantially on usage from people who hold no stake in either outcome. That’s not a flaw specific to those two companies; it’s how the current AI industry is structured almost everywhere, from Google to SpaceX to every major venture-backed platform before them. Stargate LLM’s bet is that a meaningful share of AI’s next phase of growth can be built differently, with usage rewarded directly rather than only benefiting the platform running it. The mechanism for that already exists in the tokenomics: Proof of Usage rewards, Vault staking, and governance-directed revenue distributions, all tied to the same coin users are already spending on the platform. The presale is where that structure starts, open to anyone with a wallet, not just the investors who got there first.

Explore Stargate LLM:

Website: Stargate.org

Buy: own.Stargate.com

Telegram: https://t.me/StargatellmOfficial

Twitter/X: https://x.com/Stargatellm

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Jim Cramer doubled down on Nvidia on Monday, urging investors to buy the stock as the chipmaker rejected claims that its next-generation AI rack systems face delays until 2028.

The clash pits Nvidia against research firm SemiAnalysis, which alleges manufacturing setbacks have hit the Kyber NVL144 architecture showcased at GTC earlier this year.

SemiAnalysis Claims Put Nvidia’s Kyber Timeline in Doubt

SemiAnalysis claims the high-density rack design built for Rubin Ultra GPUs has slipped by more than 12 months. The firm blamed persistent manufacturing problems with the system’s complex PCB midplane.

The firm also claimed Nvidia scrapped its NVL72x2 back-to-back rack after pushback from hyperscaler customers.

Nvidia’s supply chain felt the report within hours. Japan’s Ibiden, which counts Nvidia as its largest client, fell as much as 10% on Monday, Bloomberg reported.

Kingboard Laminates tumbled 18% in Hong Kong, while Samsung Electro-Mechanics slid 11% in Seoul.

Nvidia rejected the claims, telling media outlets that its roadmap remains intact. The chipmaker, fresh off launching a revenue-sharing compute program for AI startups, has faced this script before.

When Blackwell delay reports surfaced in August 2024, Nvidia insisted production would ramp on schedule. It then fixed a design flaw and shipped several billion dollars of Blackwell hardware within months.

Jim Cramer Backs Nvidia Despite the Noise

Cramer reaffirmed his bullish stance and urged investors to buy Nvidia. He told CNBC that chip stocks are staging a “revenge trade” after last week’s “misguided selling.”

The numbers frame his conviction. The Philadelphia Semiconductor Index gained 87.8% in the second quarter, its best quarter since records began in 1994, Axios reported.

Nvidia missed most of that rally. The stock traded near $196.58 at this writing, up almost 2% over the last 24 hours.

Last week tested the sector’s nerve. AI chip stocks cracked after Michael Burry’s bubble warning, while memory stocks plunged sharply on supply glut fears.

Cramer, however, sees the pullback as an opportunity. He named his five AI stock picks earlier this month, favoring chip suppliers over Big Tech giants.

Nvidia’s next earnings report will show whether rack-level friction reaches data center revenue. Until then, investors must weigh Cramer’s conviction against a laggard chart and SemiAnalysis’ supply chain warnings.

The post Jim Cramer Says Buy Nvidia as Chipmaker Rejects 2028 AI Delay Claims appeared first on BeInCrypto.

JPMorgan's JLTXX tokenized money market fund has grown its onchain assets under management by roughly 250% over the past month, according to data platform Token Terminal. The bank runs the fund exclusively on Ethereum. JLTXX, formally the OnChain Liquidity Token Money Market Fund, launched May 13… Read the full story at The Defiant

TeraWulf has secured a 20-year lease with Anthropic expected to generate nearly $19 billion in contracted revenue, sending the Bitcoin miner’s stock sharply higher despite weakness across crypto-related equities.

Summary

- TeraWulf signed a 20-year lease with Anthropic worth an estimated $19 billion in contracted revenue.

- The AI data center will deliver up to 401 MW of capacity, with full deployment expected by early 2028.

- TeraWulf shares climbed more than 12% as the company also announced a $450 million AI-focused asset sale.

AI infrastructure becomes TeraWulf’s biggest growth driver

According to a press release from TeraWulf, the Bitcoin miner has signed a 20-year lease agreement with Anthropic for its Justified Data campus in Hawesville, Kentucky.

The company said the agreement is expected to produce nearly $19 billion in contracted revenue over the initial lease period, making it one of the largest infrastructure commitments announced between an AI developer and a crypto mining company.

Under the agreement, the Kentucky campus will support about 401 megawatts of critical IT load and will be built in several phases. TeraWulf said the first capacity is expected to come online during the second half of 2027, while the full 401 MW deployment is scheduled for early 2028.

The project adds to a growing list of Bitcoin miners expanding beyond digital asset mining into AI infrastructure, where existing power capacity and data center expertise have become increasingly valuable. TeraWulf has been repositioning its business to serve high-performance computing and AI workloads alongside its Bitcoin operations.

The announcement also comes as Anthropic continues to expand its computing footprint following recent regulatory developments. As crypto.news reported earlier, the company has restored public access to its Claude Fable 5 and Mythos 5 models after U.S. authorities lifted export restrictions that had suspended public availability since June 12. According to Anthropic, the rollout resumed after discussions with the U.S. government and now includes new classifiers designed to identify and block cybersecurity-related misuse.

Those export controls had temporarily forced Anthropic to disable both advanced models for all users after a U.S. government directive required the company to block access for foreign nationals. Anthropic said the additional safeguards were introduced to address government concerns over potential misuse through jailbreak techniques.

Asset sale strengthens funding for AI expansion

Alongside the lease announcement, TeraWulf disclosed that it has entered into a definitive agreement to sell its 50.1% ownership stake in the Abernathy Joint Venture to an investor group led by its joint venture partner, Fluidstack.

According to the company, the transaction monetizes roughly $450 million of invested capital at a premium and frees additional resources for wholly owned AI infrastructure projects. The divestment complements the Anthropic lease by increasing capital available for future data center development.

Investors reacted positively to both announcements. TradingView data showed TeraWulf shares rising more than 12% to around $24, outperforming many publicly traded crypto companies that traded lower during the broader market downturn.

Anthropic has also remained at the center of geopolitical discussions over AI access. As crypto.news previously reported, Austria last month urged the European Union to consider establishing Anthropic within the bloc after U.S. export restrictions limited foreign access to the company’s most advanced AI systems.

In a letter released by the Austrian government, State Secretary for Digitalization Alexander Proell argued that the EU could offer the company legal certainty, investment, market access, and what he described as a values-based environment, while encouraging European policymakers to reduce dependence on technology decisions made outside the region.

Separately, Anthropic is also reportedly considering an initial public offering at a valuation of as much as $1 trillion, adding another catalyst as the company continues expanding its AI infrastructure and global operations.

Key Takeaways

- GE Vernova reached a record peak of $1,182.31 on July 6, climbing 121.61% over 12 months and 70.6% since the start of 2026

- Jim Cramer declared GEV his top pick in the power sector and disclosed it represents a “very big position” in his Charitable Trust portfolio

- First quarter 2026 revenue reached $9.3 billion, marking a 16% year-over-year increase, while EPS of $1.98 surpassed analyst projections

- The company secured $18.3 billion in orders during Q1, reflecting 71% organic growth, pushing total backlog to $163 billion

- Management elevated 2026 free cash flow projections to $6.5–$7.5 billion from the previous range of $5.0–$5.5 billion

GE Vernova (GEV) established a fresh all-time peak at $1,182.31 on July 6, 2026, continuing its impressive ascent with shares hovering around $1,183 and commanding a market capitalization of $310.9 billion. This milestone caps a remarkable rally that has delivered more than 120% gains over the past twelve months.

Shares have surged 70.6% since January, positioning GEV among the energy sector’s top-performing equities. Such dramatic appreciation inevitably attracts scrutiny from market observers and institutional investors alike.

During the June 30 edition of Mad Money’s Lightning Round, Jim Cramer singled out GE Vernova as his preferred play in the power generation space. He revealed the stock occupies substantial real estate in his Charitable Trust holdings—a transparent, trackable stake rather than casual commentary.

“GE Vernova of those is my favorite. It’s one that the Charitable Trust has a very big position… I say still buy GE Vernova,” Cramer stated.

The endorsement came with shares already trading at elevated levels. GEV finished July 2 at $1,113.11, yet its three-year cumulative return of 867.92% demonstrates how dramatically the investment narrative has transformed.

First Quarter Results Validate Bullish Thesis

The company’s first quarter 2026 financial performance, disclosed April 22, provided concrete evidence supporting the optimistic outlook.

Topline revenue reached $9.3 billion, representing 16% year-over-year expansion. Earnings per share of $1.98 exceeded the Street’s $1.84 consensus by 7.6%.

Order momentum stole the spotlight. First quarter bookings totaled $18.3 billion, surging 71% on an organic basis, with robust contributions from Power, Wind, and Electrification divisions. The cumulative backlog swelled to $163 billion, expanding by $13 billion in just three months.

Free cash flow generation of $4.8 billion represented more than a fourfold increase from the prior year. Adjusted EBITDA nearly doubled to $0.9 billion, while margins widened 390 basis points to 9.6%.

CEO Scott Strazik highlighted accelerating demand for gas turbines. Gas Power equipment backlog and slot reservations expanded from 83 gigawatts to 100 gigawatts during the quarter. Management now aims to reach at least 110 gigawatts by the close of 2026.

Management Lifts Full-Year Projections

Following the strong quarterly performance, GEV elevated its full-year 2026 outlook across all primary financial metrics.

Revenue expectations now span $44.5–$45.5 billion. Adjusted EBITDA margin guidance increased to 12–14% from the prior 11–13% range. Free cash flow projections jumped significantly to $6.5–$7.5 billion versus the earlier $5.0–$5.5 billion target.

The company concluded Q1 holding $10.2 billion in cash and distributed $1.4 billion to shareholders via share repurchases and dividends.

Wall Street coverage has grown increasingly supportive. Bernstein launched coverage with an outperform recommendation. Jefferies boosted its price objective to $1,210 while reaffirming a Buy rating, citing a robust order book extending through 2031.

InvestingPro’s valuation model suggests the stock currently trades above its Fair Value calculation—an important consideration for investors contemplating entry points.

From a technical perspective, shares encountered resistance around the $1,170–$1,180 zone on July 2 before retracing. The 50-day, 100-day, and 200-day moving averages currently rest near $1,052, $959, and $794 respectively.

Second quarter 2026 results are scheduled for July 22. Analysts assign a Zacks Rank of 2 (Buy) accompanied by a positive Earnings ESP of 10.35%, with estimate revisions trending favorably ahead of the release.

Coinbase CEO Brian Armstrong has said the exchange is investigating an AI-generated prediction market alert after the platform mistakenly sent users a “breaking news” notification of a supposed Norway 3-2 win against Brazil in the ongoing FIFA World Cup before the match had even kicked off at the MetLife Stadium.

The flash news also showed that Manchester City forward Erling Haaland scored twice to send the Vikings to the quarterfinals.

What was interesting, though, was that Coinbase’s own prediction market page showed the match had been delayed due to poor weather conditions, but even more fascinating was that Norway did indeed end up beating Brazil when the game was finally played, even if with a different scoreline, and Haaland did find the back of the net two times.

Coinbase AI Bashed for Fake News, CEO Vows Probe

The discrepancy was first brought to light by Relay Digital managing partner Jay Drain Jr., who posted on X that the Coinbase AI was “hallucinating results for a World Cup game that hasn’t even been played yet,” calling the notification it was sending to millions of the exchange’s users “factually incorrect” and terming it as “dangerous and irresponsible.”

Some time later, Coinbase chief Brian Armstrong responded to the post, insisting that the company had begun reviewing the incident. This was followed by an update from the firm’s head of consumer and business products Max Branzburg, who said that the team had “fixed the incorrect story” and made some updates to make sure similar errors don’t happen in the future.

“It’s awesome to see the power of AI-enabled 24/7 insights for trading, but obviously still need to tune it to address these types of issues,” stated Branzburg. “And hey, it turns out Norway did win and Haaland did score 2 goals, so maybe the AI knew something we didn’t!”

Polymarket Trader Suffers $11.6M World Cup Loss in 10 Days

As CryptoPotato reported, World Cup fever has seen trading volumes on leading prediction markets skyrocket from around $65 million in early June to a high of $5.6 billion toward the end of that month, with Kalshi seeing most of that action.

And with all that money flowing, quite a few traders have been caught on the wrong side of bets, including one Polymarket user highlighted on June 6 by blockchain analytics platform Lookonchain, who reportedly lost $11.63 million during a 10-day betting spree on World Cup markets.

According to Polymarket records, “Coldsway” placed bets on 15 soccer markets and traded a total of $48.19 million. They counted wins on only four positions, while 11 closed at a complete loss, putting their win rate at 26.7%.

The trader’s biggest winning position generated $1.12 million after placing a $689,318 bet that Australia and Egypt would finish in a draw. They also made $962,940 from a $1.48 million position predicting Egypt would not win the July 3 fixture.

However, several unsuccessful million-dollar wagers outweighed all profits Coldsway made, with the largest single loss reaching $4.95 million as a result of Morocco’s 3-0 win against Canada on July 4. They also lost $3.10 million on a prediction that Canada would not beat South Africa on June 28.

The post Coinbase Prediction Market AI Claims Norway Beat Brazil Before Match Even Started appeared first on CryptoPotato.

SpaceX shares have remained under pressure ahead of their Nasdaq-100 debut, even as the upcoming index inclusion is expected to trigger roughly $4.3 billion in passive fund buying.

Summary

- SpaceX joins the Nasdaq-100 on July 7, with JPMorgan estimating about $4.3 billion in passive fund buying.

- The stock is holding above $155 support while traders watch for a breakout above $160 and $165.

- Limited public float and heavy insider ownership could increase volatility during the index rebalancing.

According to Nasdaq, SpaceX will officially join the Nasdaq-100 before the opening bell on July 7 after qualifying under the exchange’s updated rules that allow certain large newly listed companies to enter the benchmark much sooner than under the previous seasoning requirements. The company, which made its public market debut in June, will become one of the fastest IPOs to reach the technology-heavy index.

Nasdaq-100 inclusion brings major institutional demand

JPMorgan estimates that the index addition could generate about $4.3 billion in compulsory purchases from index-tracking exchange-traded funds and passive investment portfolios. Those funds are required to rebalance their holdings to match the Nasdaq-100, creating a one-time surge in demand for SpaceX shares.

The accelerated inclusion follows Nasdaq’s rule revision for qualifying large IPOs. Under the updated framework, companies with sufficiently large market capitalizations no longer need to wait as long before becoming eligible for the index. The change has allowed SpaceX to enter the benchmark only weeks after listing, a timeline that would previously have taken much longer.

Despite the expected buying, the stock’s ownership structure remains a potential source of volatility. Elon Musk and other insiders continue to control a significant portion of the company’s equity, leaving a relatively small public float available for trading. As passive funds compete for those shares during the rebalance, limited supply could amplify price swings in either direction.

While forced buying often provides temporary support, the effect typically fades after index funds complete their purchases, leaving subsequent price action dependent on normal investor demand and company fundamentals.

Technical levels keep $180 in focus

SpaceX traded around $157.62 on Monday, down about 2.7%, after failing to hold gains near the $160 resistance zone. The pullback has left the stock testing support around $155, a level traders are watching closely ahead of Tuesday’s index inclusion.

A move back above $160 would indicate that buyers are regaining short-term control. If trading volume strengthens alongside the breakout, the stock could revisit resistance near $165 before attempting another move toward $170.

A sustained push above $170 would strengthen the bullish case for a rally toward $180 during the week. If momentum continues beyond that level, technical traders could begin monitoring the next upside objectives around $190 and $200.

On the downside, maintaining support at $155 remains critical for the current recovery attempt. A break below that level could expose the stock to a decline toward $152, while heavier selling pressure may extend losses to the next support area near $150.

For now, the Nasdaq-100 addition remains the primary catalyst for SpaceX. The expected wave of passive buying may provide near-term support, but whether the stock can build on that demand will likely depend on its ability to reclaim resistance around $160 and sustain buying interest after the index rebalance is complete.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Form 4 Sight Sciences Inc For: 6 July

Top 3 Crypto to Watch in the Second Week of July 2026

Bellatrix Star set for 2026 return in Sir John Monash Stakes

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: High Hopes

-

Politics3 days ago

Politics3 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Crypto World7 days ago

Crypto World7 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Fashion7 hours ago

Fashion7 hours agoOpen Thread: What Great Books Have You Read Recently?

-

News Videos7 days ago

News Videos7 days agoHow to Build INSANE Live Financial Dashboards With Claude

-

NewsBeat2 days ago

NewsBeat2 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Tech7 days ago

Tech7 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Business7 days ago

Business7 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World5 days ago

Crypto World5 days agoAirdrop Registration Becomes Key Focus For Remittix As RTX Launch Updates Approach

-

Sports5 days ago

Sports5 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Crypto World5 days ago

Crypto World5 days agoBinance stock trading tops $1B in first month after launch

-

NewsBeat6 days ago

NewsBeat6 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

-

Crypto World5 days ago

Crypto World5 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

Crypto World3 days ago

Crypto World3 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Crypto World1 day ago

Crypto World1 day agoSouth Africa proposes crypto tax guidance under existing rules

-

News Videos8 hours ago

News Videos8 hours agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

NewsBeat5 days ago

NewsBeat5 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Business5 days ago

Business5 days agoMeta Platforms Stock Jumps 7% Today as Bloomberg Reports Company Plans to Enter the Cloud Business

-

Tech1 day ago

Tech1 day agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Business4 days ago

Business4 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

You must be logged in to post a comment Login