Crypto World

The never-sell era is over

For six years, one rule anchored the most influential trade in crypto: Strategy buys Bitcoin and never sells it. On July 6 the company disclosed it sold 3,588 coins at a loss to pay dividends on the securities it issued to buy them. The amount is a rounding error. The direction changes everything, for Strategy and for the dozens of companies built in its image.

Summary

- Strategy’s Bitcoin sale ended the market’s assumption that its holdings only move one way.

- The sale was small relative to Strategy’s total BTC stack, but it changed the regime around the company’s treasury model.

- Preferred dividends have turned Bitcoin from a permanent reserve asset into a potential funding source.

- The BTC Monetization Program formalizes future sales as credit management rather than emergency action.

- Treasury companies built on the same never-sell story now face higher scrutiny around financing costs and forced selling risk.

The disclosure arrived the way Strategy’s most important announcements always have, in a Michael Saylor post and a securities filing, but this one inverted six years of them. Between June 29 and July 5, the company sold 3,588 Bitcoin for approximately $216 million, and used the proceeds to pay the quarterly dividends on four of its preferred stock series and the June dividend on a fifth. Strategy, the company that turned never sell into a corporate identity, a marketing engine, and the template for an entire sector, is now a Bitcoin seller.

The numbers make the point sharper than any commentary. The coins went out the door in two tranches at average prices near $59,256 and $60,773, against an average purchase cost of $75,476. The company did not sell into strength to rebalance; it sold at a roughly 20 percent loss because dividends come due on a calendar, not on a market cycle. It was the third disposal since a small tax-loss sale in 2022, and roughly one hundred times larger than the 32-coin transaction in late May that the market had debated for a week and mostly dismissed as housekeeping.

Strategy still holds 843,775 BTC, about 4.2 percent of all the Bitcoin that will ever exist, and the sale barely dents it. The company insists the long-term thesis is untouched, and mechanically that is true. But markets do not price mechanics; they price regimes, and a regime just ended. The most reliable bid in Bitcoin’s institutional era has disclosed the conditions under which it becomes an ask, and every treasury company, preferred shareholder, and Bitcoin allocator now has to model what that means.

This is the anatomy of the turn: why the dividends forced it, what the new monetization framework really institutionalizes, how the market absorbed the news, what it means for the treasury-company sector Strategy spawned, and what actually breaks or holds from here.

Six years of the taboo

Understanding what ended this week requires understanding what was built, because never sell was never merely a slogan. It was the load-bearing wall of a capital structure.

The position began in August 2020 as a treasury decision: a software company parking cash in Bitcoin as an inflation hedge. It became something else within a year, as the company discovered that markets would fund the trade. First came convertible bonds, zero and near-zero coupon paper that investors bought for the embedded equity option; then at-the-market equity sales into every rally; and finally, in the current era, the preferred complex, which replaced the convertibles’ patience with hard cash dividends. Each financing generation raised the stakes of the pledge. A company that never sells is a compelling story when its obligations are optional; it is a high-wire act when they are ten and eleven percent coupons payable in dollars.

The pledge itself was performed as much as stated. Saylor’s laser eyes, the orange-dot charts posted before each purchase announcement, the conference keynotes built around the phrase, all of it constructed what amounted to a public covenant, and the covenant had measurable value: for most of five years the equity traded at a large premium to the coins, a premium analysts explicitly attributed to the one-way-valve belief and to leverage on future purchases. Competitors noticed. The pledge was copied, cited in dozens of treasury-company prospectuses, and became the sector’s default liturgy.

The record shows exactly one prior breach before this year, and its context is instructive: a small December 2022 sale executed for tax-loss harvesting, promptly rebought, and universally accepted as accounting rather than apostasy. The May 2026 sale of 32 coins was the first ambiguous crack, debated precisely because everyone understood what a real breach would signify. The July disclosure removed the ambiguity. Covenants of this kind do not degrade linearly; they hold completely until they hold conditionally, and conditionally is a different product. The premium’s collapse toward net asset value over the first half of 2026 can be read, in hindsight, as the market pricing the covenant’s expiry before the company confirmed it.

The arithmetic that forced the turn

Strategy’s model was never just buying Bitcoin. It was funding Bitcoin purchases by selling securities against the story, at a premium, and the securities are where the obligation lives.

Over the past two years the company built out a complex of preferred instruments, STRF, STRE, STRK, STRD, and the retail-oriented STRC, marketed to income investors as high-yield exposure adjacent to Bitcoin. The senior tier pays a fixed 10 percent; STRC’s variable rate has run near 11.5 percent. Grayscale’s head of research has estimated the annual dividend load across the complex near $1.5 billion. Strategy’s software business generates only a fraction of that, which means the dividends must be paid from one of three sources: cash reserves, new securities issuance, or the coins.

For as long as capital markets stayed open at tolerable prices, issuance covered everything, and the machine compounded: sell paper, buy coins, watch the premium reinforce the story, repeat. The 2026 drawdown closed the loop’s easy path. With Bitcoin grinding to 21-month lows near $57,750 in June, record ETF outflows draining the demand side, and the company’s equity trading at, and briefly below, the value of its coins, issuing new securities meant selling dollar claims cheaply against a discounted asset. The company disclosed an $8.32 billion loss on its digital assets for the second quarter, almost all unrealized, took a full valuation allowance against the associated tax asset, and faced its dividend calendar with the least attractive issuance window since the strategy began.

The response came in two steps. On June 29, Strategy adopted what it calls a Digital Credit Capital Framework, formalizing a $2.55 billion dollar reserve for dividends and debt service and authorizing a BTC Monetization Program permitting up to $1.25 billion in Bitcoin sales for those purposes. A week later came the disclosure that it had already been selling: 1,363 coins in the final days of June, 2,225 more in early July, proceeds routed directly to the dividend bill, with the filing noting that the full $1.25 billion program capacity remains untouched by this particular sale.

Read together, the framework and the sale say something simple: the company examined its options for paying $1.5 billion a year in a closed issuance window and concluded that coins are now a funding source. Not the last resort. A source.

The mantra, annotated

No company in crypto invested more in a slogan. Never sell your Bitcoin was Saylor’s speech title, his social media signature, and the emotional core of the investment case: Strategy was the vehicle through which Bitcoin left the market forever, a one-way valve, and the premium investors paid over the coins reflected, in part, faith in the valve.

The walk-back was carefully staged, which is itself revealing. At a Bitcoin conference in June, addressing the 32-coin May sale, Saylor drew a distinction that had never featured in the marketing: never sell your Bitcoin was advice for individuals, he said, not a description of corporate policy. Weeks earlier, discussing the quarter’s paper losses, he had already conceded the company would probably sell some Bitcoin. By the time the July disclosure landed, accompanied by a Saylor post about Bitcoin evolving by changing less at the protocol layer and mattering more everywhere else, the taboo had been pre-softened in three stages: hypothetical, trivial, material.

The choreography worked, in the narrow sense. There was no panic, no run on the preferreds, no death spiral. Bitcoin dipped below $62,000 on the headline and recovered above $63,000 within a day, holding a streak of gains; MSTR slipped about 2 percent in the premarket, snapping a five-day rally rather than starting a rout. The market had been given months to price the possibility, prediction markets had traded odds on exactly this event after a $30 million transfer to an exchange caught attention, and the actual number, 0.4 percent of holdings, landed closer to relief than to shock.

But absorbing a headline is not the same as forgetting it. The premium Strategy commanded for years rested on a story in which this disclosure could not exist. The story now has an asterisk, permanently, and asterisks compound. Every future dividend date arrives with a question attached that did not exist in May: paid how, exactly?

The calm itself deserves a second look, because two readings of it point in opposite directions. The benign reading is maturation: the market now values Strategy as a credit structure, credit analysts expected collateral to be used as collateral, and the orderly absorption proves the company can normalize without a crisis, which is the soft landing every leveraged holder of a volatile asset hopes for. The less benign reading is that the calm measures how much premium was already gone. A market that shrugs at the breach of a six-year covenant is a market that stopped paying for the covenant some time ago, and the muted reaction is not forgiveness but indifference, the response of investors who already migrated their Bitcoin exposure to the spot ETFs that do the same job without a dividend bill attached. Both readings will be tested by the same future data: what happens to the stock, and to the preferreds, the next time a dividend date arrives in a closed market.

What the monetization program really is

The instinct is to read the $1.25 billion authorization as an emergency measure. The more accurate reading is that Strategy is institutionalizing something the sector has avoided naming: a leveraged Bitcoin position has carrying costs, and carrying costs are ultimately paid in Bitcoin unless someone else keeps funding them.

The framework converts an unspoken dependency into a managed one. By pre-authorizing sales up to a stated ceiling, earmarked for the dollar reserve and dividends, the company transforms future disposals from narrative crises into program activity, the way a corporation’s standing buyback authorization turns each repurchase into routine. It is, in the language Strategy prefers, credit management: the preferreds are recast as a deliberate credit structure, the coins as collateral that can be partially liquefied to service it, and the whole arrangement as ordinary finance rather than broken faith.

The recasting is honest, and that is precisely its cost. Ordinary finance is what the premium was not. A closed-end fund that holds Bitcoin, pays double-digit preferred dividends, and sells assets to cover them when markets are closed is a comprehensible, analyzable, and entirely unmagical structure, and the market has spent 2026 pricing Strategy progressively closer to exactly that, with the closely watched mNAV ratio touching 0.99 in the June lows. The feud over whether the whole model was ever more than financial engineering erupted at those lows for a reason: the question stopped being rhetorical.

There is also a quieter arithmetic problem. Selling coins at $60,000 to pay dividends on paper issued to buy coins at $75,476 locks in the worst version of the trade, converting temporary drawdown into permanent capital loss at a pace set by the dividend calendar. At current prices, covering the full annual load from coins alone would consume roughly 24,000 BTC a year. Nobody expects that scenario while the reserve and the program exist; the point is that it now has a disclosed mechanism instead of an unthinkable one.

The disclosure machine, and how the market caught it

The mechanics of how this sale surfaced are worth recording, because they are the template for how every future one will be read.

Strategy discloses through overlapping channels: SEC filings, Saylor’s posts, and a public dashboard whose Bitcoin acquisition line updates with each period’s net change. The July revelation began as an anomaly hunt. On-chain watchers had flagged a transfer of a few hundred coins toward an exchange days earlier, and speculation built around a possible sale in the hundreds of BTC; prediction markets had been trading odds on whether Saylor would sell at all since a $30 million movement caught attention weeks before. The dashboard then printed the truth in two dry entries, negative 1,363 and negative 2,225, and the Form 8-K supplied the accounting: proceeds, prices, purposes, and the note that the monetization program’s capacity remained untouched because this sale was routed directly to dividends.

Notice what that sequence implies. The market’s early-warning system for the most watched balance sheet in crypto is now a combination of blockchain forensics, betting markets, and a corporate dashboard, each faster than the filing that confirms them. Anyone modeling treasury-company risk from here should internalize the cadence: coins move on-chain first, odds move second, dashboards print third, filings explain last. The gap between the first signal and the final explanation is measured in days, and in those days the story is written by whoever reads the mempool.

It also means the era of stealth is over in both directions. Strategy cannot quietly sell, but neither can it quietly not sell: every dividend date without a corresponding dashboard decrement is now itself a disclosure, proof the bill was paid from cash or paper instead. The company that made an art of announcing purchases has acquired, involuntarily, the same transparency on the way out, and the orange-dot ritual that once meant only accumulation now has a shadow calendar that everyone knows how to check.

The sector built on the taboo

Strategy was never just a company; it was a template. Dozens of digital asset treasury companies now exist across Bitcoin, Ether, Solana, and smaller tokens, all running versions of the same play: issue securities, buy the asset, trade at a premium justified by permanence and leverage. The original’s premium was the sector’s anchor, and the original’s taboo was the sector’s creed.

Both are now gone at the source, and the copies have no better argument than the original. Treasury-company premiums across the class have compressed toward and below net asset value through the drawdown, the capital markets window that funded accumulation has narrowed with every mNAV that touches 1.0, and the demonstration that the flagship pays its bills in coins when paper will not sell reprices every balance sheet in the category. The record forced selling by miners earlier this year showed what happens when an industry’s structural holders become structural sellers; the treasury sector now carries a live version of the same question.

The divergences within the class are becoming the story. In the same week Strategy disclosed its sale, Japan’s Metaplanet raised $137 million in fresh capital to keep accumulating, and BitMine added more than 42,000 ETH to a stack now worth over $10 billion, evidence that the model still functions where local capital markets remain open or where the asset’s story retains a premium. The lesson is not that treasury companies die in bear markets. It is that they stratify: those that can still issue paper keep buying, those that cannot start selling, and the market learns to price which is which with brutal speed.

For Bitcoin itself, the structural meaning is modest but real. Roughly a million coins sit on corporate balance sheets funded by instruments with cash obligations. In every prior stress, the question was whether those coins were truly off the market. The honest answer, as of July 6, is: mostly, conditionally, and no longer axiomatically. Flow watchers who track ETF creations and redemptions as the demand-side signal now have a supply-side counterpart worth the same attention: treasury-company disclosure dates.

The second-order effect may land on the financing side before the coins ever move. Treasury companies do not just hold Bitcoin; they hold it against a pyramid of convertibles, preferreds, and structured paper sold to investors who priced permanence into the collateral. Every one of those instruments now reprices against a world where the collateral is spendable by policy, and the repricing shows up as wider yields demanded on the next issuance, tighter covenants, and, for the weakest names, no next issuance at all. The sector’s accumulation era was funded by cheap paper sold against an unbreakable story; the story’s amendment raises the sector’s cost of capital in a way no single sale ever could, and cost of capital, not sentiment, is what ultimately decides how many of the copies survive the cycle.

What would actually break, and what holds

It is worth being precise about what the sale did and did not change, because both the doom reading and the nothing-happened reading are wrong.

What holds: the balance sheet. A company holding 843,775 BTC against a $1.5 billion annual dividend bill, with $2.55 billion in cash and $1.25 billion in authorized sales capacity, has years of runway even in a market that stays closed, and any meaningful Bitcoin recovery reopens the issuance machine and makes this week a footnote. The coins-to-obligations ratio remains overwhelming; this was a liquidity event, not a solvency one. Holders of the preferreds arguably got the best news of anyone: the company has now proven it will liquidate collateral to pay them, which is what a credit investor actually wants to know.

What broke: the reflexivity. The old machine ran on a premium that fed issuance that fed buying that fed the premium. That loop required the market to believe the coins only moved in one direction, and the belief is not recoverable in its original form. The new equilibrium is a company managed like a credit structure, valued near its assets, whose equity is a leveraged Bitcoin tracker with a management team, which is a viable business and a diminished myth.

The watch list from here is short. First, the pace: whether future dividends are paid from the reserve, from reopened issuance, or from more coins, disclosed sale by sale. Second, the program: any draw against the $1.25 billion authorization, and above all any increase to it, which would signal the window staying shut longer than the buffers. Third, the stack: the line that matters psychologically is not any single sale but the first quarter in which holdings visibly decline and keep declining, the point at which the market stops asking whether Strategy sells and starts asking what it holds at the end. And fourth, the whale and institutional bid on the other side, because structural sellers only matter in markets that stop absorbing them.

The era that actually ended

The temptation is to write this as a fall, and the record does not quite support it. Strategy has not failed; it has normalized. The company that spent six years insisting it was a new kind of institution spent the first week of July behaving like a familiar one: facing a cash bill in a closed market, it sold assets, disclosed the sale, published a framework, and moved on. Credit analysts would call that discipline. It is only a scandal measured against the company’s own mythology, which is another way of saying the scandal was priced into the mythology all along, waiting for a dividend date and a closed window to collect.

But mythologies are load-bearing in this sector, and this one carried more than Strategy’s stock. Never sell was the retail investor’s shorthand for why corporate Bitcoin adoption mattered: the coins were leaving forever, supply was ratcheting away, and every balance-sheet announcement was a small halving. That story now requires a footnote about dividend calendars and issuance windows, which is to say it stops being a story and becomes a spreadsheet.

Saylor’s own framing this week, that Bitcoin will evolve by changing less at the protocol layer and mattering more everywhere else, reads as an attempt to relocate the narrative from his balance sheet to the asset itself. It may even be right. The never-sell era produced the largest corporate Bitcoin position in history and proved the accumulation trade at scale; the era that replaces it will test the less romantic proposition that the position can be financed through a full cycle. The first data point of that era printed on July 6, at $60,201 a coin, and the most honest summary is the one no press release will use: the machine still works, and it now runs in both directions. The market’s job, from here, is to price a two-way machine honestly, and history suggests it will overdo that too, in both directions, before it gets it right.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 7, 2026.

Vanguard is hiring its first Head of Digital Assets to build a multi-year crypto roadmap for Personal Wealth clients. The roughly $12 trillion asset manager still has no plans to launch its own Bitcoin ETF.

The role appeared on Vanguard’s careers portal on July 6 under requisition 179858. It lists hybrid seats in Malvern, Dallas, Scottsdale, and Charlotte.

From Blocking Bitcoin ETFs to Hiring a Crypto Chief

The job description positions the hire as Vanguard’s senior subject matter expert for digital assets across Personal Wealth. The mandate spans products, operating models, risk, and engagement with regulators.

“The Head of Digital Assets will lead Vanguard Personal Wealth’s digital assets strategy, roadmap, and enterprise execution,” the offer stated.

The posting marks a sharp break from Vanguard’s earlier stance. The firm blocked spot Bitcoin ETFs from its brokerage platform when they launched in January 2024. Executives long dismissed crypto as speculative.

In December 2025, however, Vanguard opened its platform to third-party crypto ETFs and mutual funds. The decision gave more than 50 million brokerage clients access to funds holding Bitcoin, Ethereum (ETH), XRP, and Solana (SOL).

The reversal came under Salim Ramji, who became Vanguard’s first externally hired CEO in July 2024. At BlackRock, he ran the iShares unit that launched the iShares Bitcoin Trust (IBIT). That fund alone held about $54 billion as of March 31, per an iShares fact sheet.

Why Vanguard Still Won’t Launch a Bitcoin ETF

Vanguard has never filed for a proprietary crypto ETF. The firm’s published guidance favors assets with transparent cash flows, and it offers crypto exposure only through third-party products, much like gold.

BlackRock and Fidelity, in contrast, run their own spot Bitcoin funds. Competition among issuers has since fueled a Bitcoin ETF fee war that pushed expense ratios as low as 0.14%. Meanwhile, Schwab’s index fee cuts raised the cost of standing still in traditional products.

Client demand also remains measurable. US spot Bitcoin ETFs held $74.37 billion in net assets as of July 2. That day, Bitcoin ETF inflows returned with $221.72 million after a 10-day outflow streak. As of this writing, total net assets stood at $77.32 billion.

Therefore, the new role looks broader than any single fund. A multi-year Personal Wealth roadmap could span custody, advised portfolios, and tokenization across global finance rather than a product launch.

The open question is whether the roadmap stays exploratory or produces client-facing offerings. The chief’s first moves may show which way Vanguard leans.

The post Vanguard Spent Years Fighting Crypto, Now It’s Planning for It appeared first on BeInCrypto.

Ctrl Wallet has announced the permanent shutdown of its services after a recent security exploit, giving users until Aug. 3 to move their crypto assets before core wallet functions go offline.

Summary

- Ctrl Wallet will permanently shut down on Aug. 3 and has urged users to move funds before wallet services end.

- Users can still recover assets later by importing their 12- or 24-word recovery phrase into compatible wallets.

- The shutdown follows a recent Cardano-related exploit and comes amid a string of crypto wallet and bridge security incidents.

Ctrl Wallet said in a blog post published Tuesday that it will disable sending, receiving, swapping and all other wallet functions from Aug. 3, leaving users with only the ability to export their recovery phrases.

The company also confirmed it will immediately stop new downloads and remove the application from browser extension and mobile app stores as part of the shutdown process.

The decision comes just weeks after Ctrl Wallet disclosed a security incident affecting some Cardano wallets. On June 23, the wallet provider said it had placed parts of its platform into temporary maintenance mode while engineers investigated the issue and worked to protect user assets.

Users have one month to transfer assets

Ahead of the shutdown deadline, Ctrl Wallet has strongly advised customers to move their funds to another wallet or exchange instead of waiting until services are disabled.

According to the company, users who do not transfer assets before Aug. 3 will still be able to access their funds by importing their 12-word or 24-word recovery phrase into another compatible wallet.

Ctrl Wallet identified MetaMask, Trust Wallet and Phantom as compatible alternatives for importing recovery phrases. The company stressed that users should securely back up their seed phrases before attempting any migration.

Alongside the shutdown notice, Ctrl Wallet warned that there will be no migration token, token swap, or airdrop linked to the closure. The wallet provider urged customers to ignore social media posts or websites claiming to offer compensation or rewards tied to the shutdown, cautioning that such offers are likely to be scams.

Formerly known as XDEFI Wallet, Ctrl Wallet lists more than 650,000 monthly users and a workforce of between 11 and 50 employees on its LinkedIn profile. The wallet supported more than 2,500 blockchain networks, including Cardano and Midnight.

Security incidents continue across crypto platforms

The shutdown follows a transition announced on April 29, when Ctrl Wallet said it had come under the Emurgo umbrella and that its multichain technology would continue through the SecondFi wallet. SecondFi, a self-custodial wallet developed by Emurgo after rebranding from Yoroi in April 2026, later suffered its own security incident.

On June 24, attackers exploited a vulnerability in SecondFi that resulted in the theft of about 16 million ADA, worth roughly $2.4 million at the time.

SecondFi later said it had secured about 129 million ADA through emergency measures, transferred those funds to an independent third-party custodian, and introduced a recovery process covering the 374 affected wallet addresses.

The latest shutdown also comes during a series of security breaches affecting crypto infrastructure. As previously reported by crypto.news, blockchain security firm Blockaid detected an active exploit against the DeFi platform Summer.fi that had drained about $6 million before the attack was disclosed.

Separately, Taiko urged users to withdraw assets from all bridges on its network after confirming its chain state verification mechanism had been compromised, while Blockaid estimated losses from the related ERC20 Vault attack at more than $1 million.

Days earlier, interoperability protocol Axelar disabled its Secret Network bridge connections after an exploit led to the loss of roughly $4.7 million in bridged assets.

According to Axelar, early findings indicated the issue originated in the Secret Network’s ICS-20 smart contract rather than Axelar’s core infrastructure, prompting the protocol to suspend affected connections while its investigation continues.

EDX Markets, an institutional cryptocurrency trading platform, said it raised $76 million in a Series C funding round led by SBI Holdings.

The company plans to use the funds to develop new products and grow internationally. EDX operates an institution-only crypto marketplace that separates trading from custody and settlement through a central clearinghouse. The model is designed to reduce counterparty risk and mirrors the structure used in traditional financial markets.

SBI Holdings has been one of Japan’s most active financial groups in crypto. Its SBI VC Trade unit offers access to Ripple’s RLUSD stablecoin in Japan, while SBI Shinsei Trust Bank recently issued JPYSC, a yen-denominated stablecoin developed with Startale Group.

Last month, SBI agreed to acquire crypto exchange Bitbank for 46.7 billion yen ($289 million), adding to its existing SBI VC Trade platform.

EDX has been moving beyond spot trading. The firm earlier this year introduced FlowConnect, a crypto-as-a-service product that allows financial firms to offer crypto trading to their customers.

The CLARITY Act picked up its first major public law enforcement endorsement on July 1 when the National Organization of Black Law Enforcement Executives (NOBLE) formally backed the bill, and two days later Major County Sheriffs of America withdrew its opposition entirely, shifting to neutral.

Two organized law enforcement bodies moving constructively on the same digital asset legislation within 72 hours is not coincidental, it reflects deliberate outreach and signals that the Senate floor fight is now a live negotiation, not a procedural formality.

Discover: The Best Token Presales

NOBLE’s Endorsement: What the Organization Said and Why It Matters

NOBLE’s July 1 letter to Senate Majority Leader John Thune and Minority Leader Chuck Schumer was addressed to the two officials who control Senate floor timing, a deliberate signal that the endorsement was meant to move the legislative calendar, not just the public narrative.

The organization, which represents more than 3,000 members across nearly 60 chapters worldwide including chief executives and command-level officials, cited four specific provisions driving its support: expanded regulatory obligations on digital asset businesses, enhanced forfeiture authorities, new transparency requirements, and oversight rules for digital asset kiosks.

Critically, NOBLE addressed the enforcement-gap argument head-on. The organization stated explicitly that the legislation does not alter the federal criminal authorities investigators and prosecutors rely on daily, money laundering, unlicensed money transmitting, conspiracy, aiding and abetting, and sanctions enforcement statutes all remain intact under the bill’s current text.

— Eleanor Terrett (@EleanorTerrett) July 3, 2026

NEWS: The Major County Sheriffs of America (MCSA) has shifted to a “neutral” position on the Clarity Act after what it describes as “continued discussions in recent days regarding parts of Section 604,” aka the Blockchain Regulatory Certainty Act.

NEWS: The Major County Sheriffs of America (MCSA) has shifted to a “neutral” position on the Clarity Act after what it describes as “continued discussions in recent days regarding parts of Section 604,” aka the Blockchain Regulatory Certainty Act.

In a letter to Senate Banking… pic.twitter.com/24XIZTfWHR

That framing directly rebuts the criticism that had dogged earlier CLARITY Act drafts, where anti-corruption groups argued the bill could create exploitable gaps in illicit-finance enforcement.

Stand With Crypto, the crypto advocacy group representing more than 2.6 million U.S. supporters, called NOBLE the first major law enforcement organization to publicly endorse the CLARITY Act.

That distinction matters for Senate Democrats who have been most vocal about enforcement preservation, an endorsement from a respected law enforcement body with NOBLE’s institutional standing provides political cover that no industry lobbying group can supply.

“Law enforcement voices are engaging constructively on digital asset legislation, and the first major endorsement is on the books.”

Stand With Crypto said this after the NOBLE letter was made public, per reporting on the NOBLE endorsement development.

Discover: The Best Crypto to Diversify Your Portfolio

Major County Sheriffs Move to Neutral on Section 604

Major County Sheriffs of America, whose members collectively serve more than 130 million citizens through offices employing at least 700 personnel each, sent its own letter on July 3, this one addressed to Senate Banking Committee Chairman Tim Scott and ranking member Elizabeth Warren.

MCSA’s position shift from opposition to neutral turned on Section 604, the provision incorporating the Blockchain Regulatory Certainty Act, which establishes liability protections for blockchain developers and service providers who do not custody or control digital assets.

MCSA said continued review and discussions around Section 604 clarified how the administration interprets and plans to implement that provision.

The organization stopped short of endorsement, it explicitly noted room to further strengthen the legislation to support both responsible innovation and state and local law enforcement needs, but it withdrew formal opposition.

Removing an active opponent from the ledger is not the same as gaining a supporter, but in a Senate that requires 60 votes for floor passage, eliminating organized resistance from an association representing major population centers carries real procedural weight.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post NOBLE Endorses CLARITY Act as Major County Sheriffs Drop Opposition appeared first on Cryptonews.

Crypto World

AI trade loses steam as Samsung earnings fail to lift chip stocks amid open source AI shift

The AI trade, which incorporates semiconductors and memory stocks, is showing signs of fatigue as investors reassess whether the extraordinary spending boom on chips and data centers can be sustained.

Semiconductor and memory stocks such as Micron Technology (MU) and Sandisk (SNDK) came under heavy pressure on Tuesday, after Samsung Electronics (005930) reported record second-quarter earnings but missed revenue estimates.

Shares still fell nearly 7%, extending a broader selloff across AI-linked chipmakers. Concerns are growing that hyperscalers could slow AI infrastructure spending.

Meanwhile, rival SK Hynix is down 25% from its all-time high ahead of its U.S. listing this week, a deal that is also drawing investor capital away from existing chip stocks.

Adding to the changing narrative, China’s Zhipu AI, one of the country’s leading artificial intelligence startups, is exploring a custom AI chip as demand for its open-source GLM models surges, highlighting the rise of lower-cost AI ecosystems built around domestic hardware rather than cutting-edge US chips.

The shift comes just weeks after SpaceX’s blockbuster IPO and amid elevated valuations across AI-related stocks. Investors are increasingly questioning whether the next phase of AI will require ever more GPUs and high-bandwidth memory, or whether more efficient models will reduce demand for the infrastructure that has powered the AI rally.

Over the past year, bitcoin and the broader crypto market have suffered from the AI trade, and if investor enthusiasm for AI continues to fade, crypto bulls could see capital rotate back into digital assets.

Wall Street analysts have begun coverage of SpaceX (SPCX) following the expiration of the 25-day quiet period after the company’s June initial public offering (IPO), with nearly every major brokerage launching their coverage with a bullish rating.

The aerospace and satellite company, which held 18,712 bitcoin as of March 31, went public in June, raising $75 billion in one of the year’s largest IPOs. Shares were priced at $135 in the offering. The stock was trading at $150.93 on Tuesday, down more than 6% from recent post-listing highs but still above its IPO price.

The two lead underwriters, Goldman Sachs and Morgan Stanley, both initiated coverage with buy-equivalent ratings. Goldman analyst Eric Sheridan set a price target of $205, while Morgan Stanley’s Adam Jonas assigned a $300 target.

They were joined by analysts at Bank of America, Citigroup, Deutsche Bank, JPMorgan, Macquarie, RBC Capital Markets, UBS and Wells Fargo, all of which launched coverage with buy or equivalent recommendations.

The most optimistic forecast came from Raymond James, where analyst Brian Gesuale initiated coverage with a Strong Buy rating and an $800 price target.

Vanguard has opened the search for a head of digital assets, creating a senior role that would oversee the firm’s strategy for cryptocurrencies and blockchain-based financial technology.

The position, listed within Vanguard Personal Wealth, calls for an executive to develop the firm’s digital asset vision, identify business opportunities and lead execution across product, technology, operations, legal and compliance teams. The candidate will also advise senior leadership on changes in digital asset markets, represent Vanguard in discussions with regulators and industry groups and help shape the firm’s long-term approach.

It also highlights other areas of the ecosystem, including tokenization, stablecoins, digital wallets, custody, blockchain-enabled settlement and operating models as areas the executive will evaluate, as well as determining whether Vanguard should build new capabilities internally, partner with third parties or delay entering certain parts of the market.

The search marks another step in Vanguard’s gradual shift toward digital assets after years of resisting the sector. The asset manager, which oversees roughly $10 trillion, remained one of crypto’s largest institutional skeptics while peers such as BlackRock, Fidelity and Franklin Templeton rolled out spot bitcoin ETFs and other blockchain initiatives.

Crypto World

1win Announces the Expansion of Its Web3 Ecosystem with the Upcoming Launch of 1win Token

[PRESS RELEASE – Curaçao, Willemstad, July 7th, 2026]

Crypto casino 1win is expanding its Web3 strategy with the development of its native ecosystem token, 1win Token ($1WIN). The initiative combines a dual-chain infrastructure, Telegram-based user engagement, and an ecosystem designed to connect platform activity with token utility.

The upcoming launch represents another step in the growing convergence of blockchain technology and online entertainment. Rather than positioning cryptocurrency solely as a payment method, the company is developing a broader ecosystem in which digital assets play an active role across platform services.

Unlike traditional platform tokens that primarily function as payment instruments, 1win Token has been designed with a strong focus on iGaming utility. The token will be integrated across the 1win platform, allowing users to utilize $1WIN in casino games, sports betting, exclusive lotteries, and future platform services.

The project introduces two independent tokenomic mechanisms designed to support the long-term sustainability of the ecosystem. Through its Weekly Buyback program, 1win will use 10% of the revenue generated from gameplay conducted with $1WIN to repurchase tokens from the open market. The buyback mechanism is intended to create continuous market demand while reinforcing the token’s long-term utility within the ecosystem.

Alongside this model, the ecosystem implements a Daily Token Burn mechanism. Every day, 10 percent of all 1win Token spent across supported platform products – including games, lotteries and other ecosystem activities – will be permanently removed from circulation. By gradually reducing the total token supply over time, this mechanism is designed to reinforce long-term scarcity while supporting the broader economic balance of the ecosystem.

Beyond token utility, the launch introduces several benefits for both platform users and cryptocurrency enthusiasts. Players will have access to crypto deposit bonuses of up to 600 percent, with a combined value of up to $2,000, while cryptocurrency deposits and withdrawals are expected to be processed in less than 90 seconds. Token holders will also gain access to exclusive lotteries and dedicated airdrop campaigns through the 1win Telegram Mini App, where users can complete tasks, participate in community activities, and prepare for future token distribution events.

To keep up with the 1win Token news and updates, users can follow on X.com (@1winToken) and other social media platforms.

About 1win

1win is an international iGaming platform offering sports betting, online casino entertainment, and cryptocurrency payment solutions to users worldwide. Since its launch, the company has continued to invest in blockchain technologies and Web3 products, including the development of 1win Token and its Telegram Mini App ecosystem.

Website: https://1wintoken.com

The post 1win Announces the Expansion of Its Web3 Ecosystem with the Upcoming Launch of 1win Token appeared first on CryptoPotato.

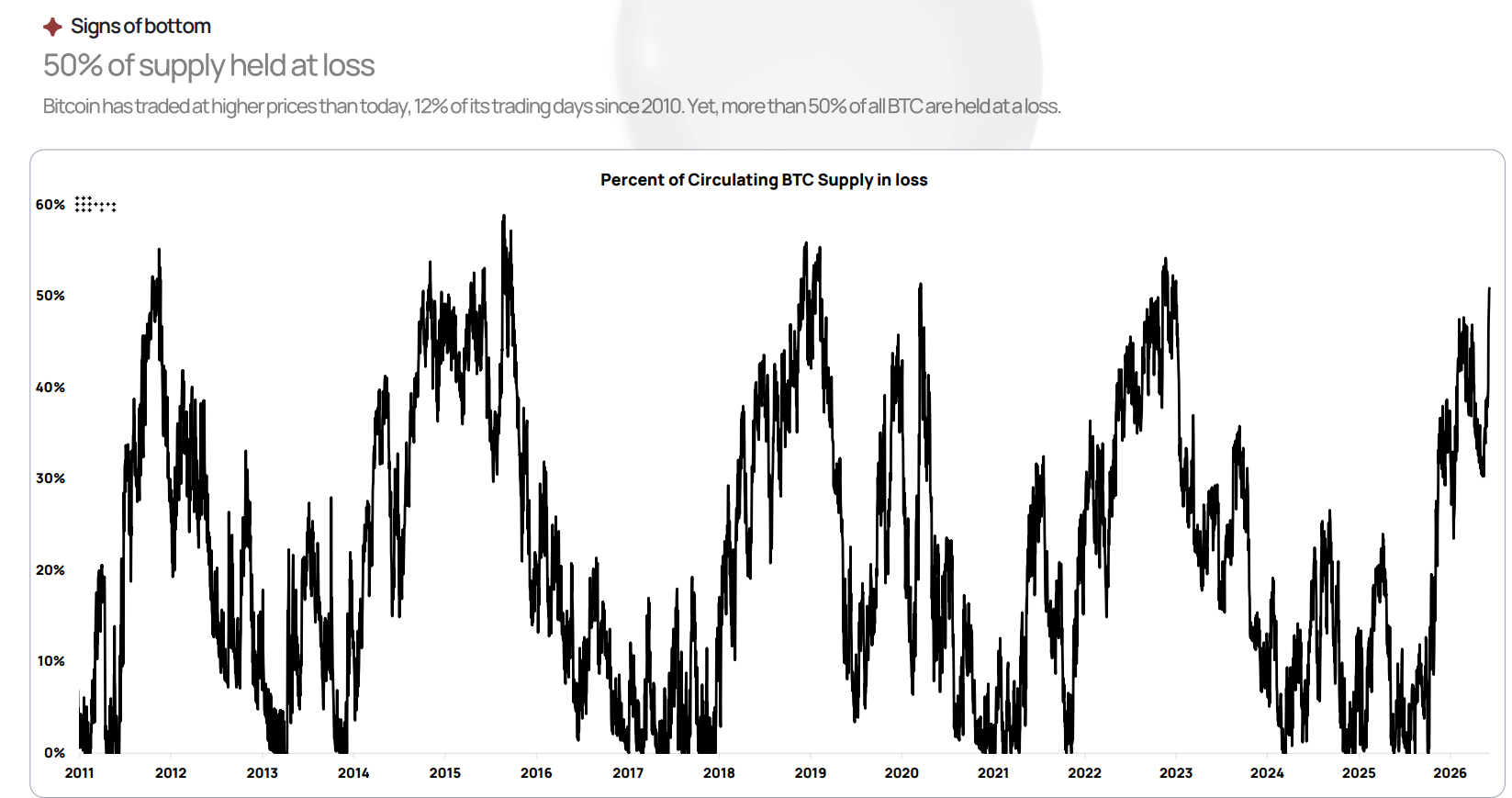

The growing Bitcoin supply held at a loss suggests that the crypto market is nearing its cycle bottom, according to digital asset brokerage company K33.

Over 50% of all Bitcoin (BTC) is currently held at a loss, K33 said in a report published Tuesday.

K33 added that because the past year’s bull market was less extreme than previous cycles, the current downturn could also be less severe.

Historically, when more than half of the circulating supply has been underwater, Bitcoin has tended to be in the late stages of a bear market, making the metric one of several indicators analysts use to assess whether selling pressure may be nearing exhaustion.

Percent of the circulating BTC supply in loss. Source: K33

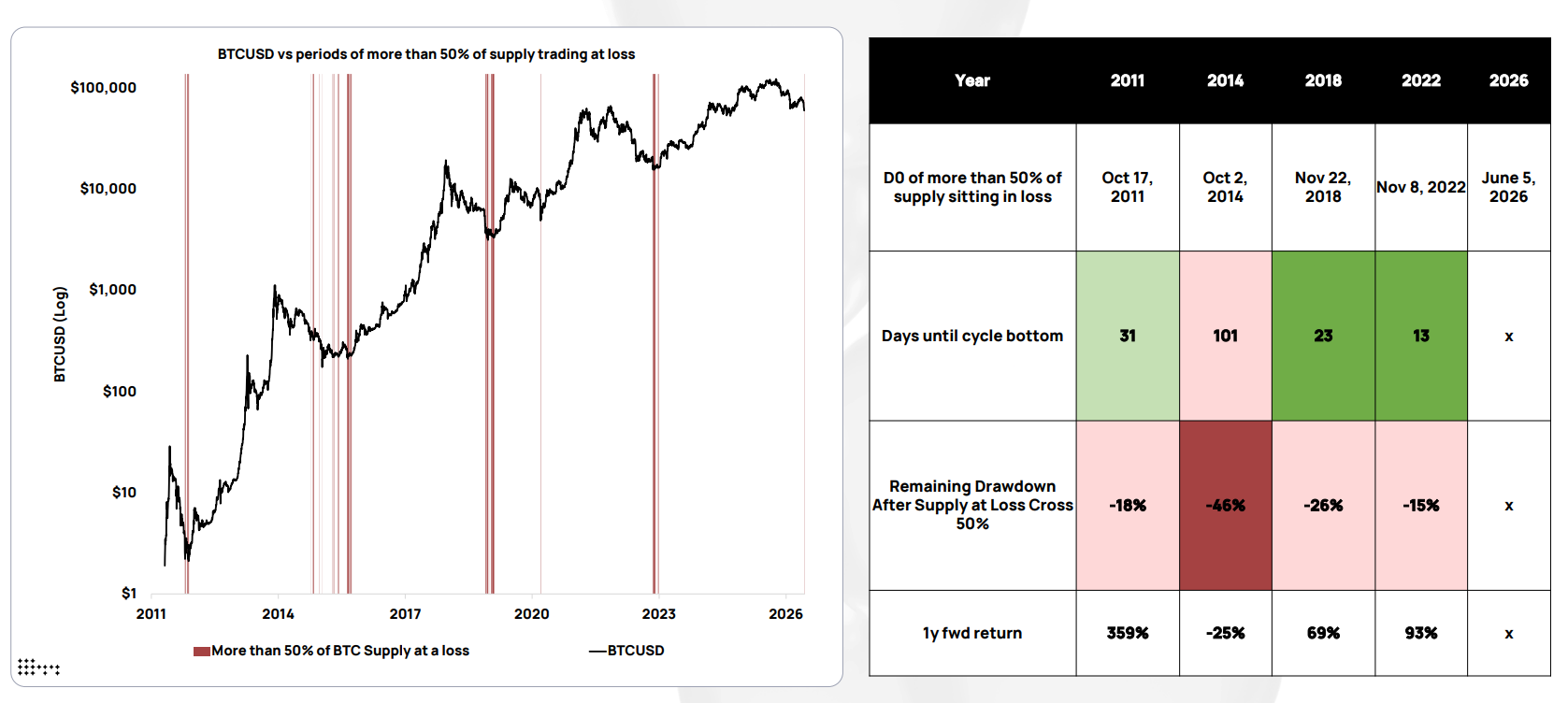

Past Bitcoin cycles bottomed within weeks of the signal

K33 said previous bear markets typically bottomed within weeks of more than half of Bitcoin’s supply being held at a loss.

During the 2017 bear market cycle, Bitcoin bottomed 31 days after over 50% of the BTC supply was held at a loss. Similarly, Bitcoin bottomed 23 days after half the supply was held at a loss in November 2018 and about 13 days after the same development in November 2022.

The 2014 cycle was an outlier, as Bitcoin only bottomed 101 days after half the supply was held at a loss. It was also the only cycle in which Bitcoin was lower one year after the signal, falling 25%.

Bitcoin during periods when 50% of the supply was held at a loss and its annual returns table for the following years. Source: K33

However, the report noted that large sellers, such as spot Bitcoin exchange-traded fund (ETF) holders, could make this cycle behave differently from previous ones because of their impact on price.

The spot Bitcoin ETFs registered two consecutive days of inflows, with $265 million on Monday, but saw $4.51 billion in net outflows in June, marking their worst month on record, according to Farside Investors data.

Related: Strategy sells 3,588 Bitcoin for $216M to fund dividends, keeps $2.55B reserve intact

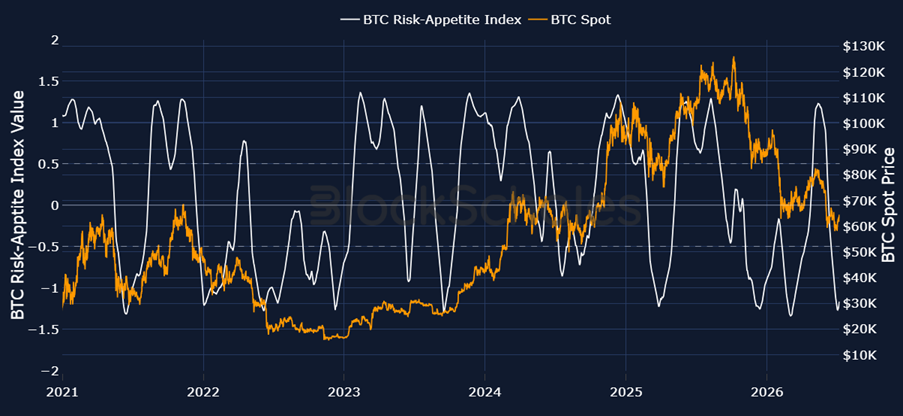

Bitcoin risk appetite signals imminent bottom: Block Scholes

Other indicators are also suggesting an imminent bottom, such as the Block Scholes Risk Appetite Index, which measures bullish and bearish momentum in digital assets.

BTC risk appetite index and spot BTC price. Source: Block Scholes

Bitcoin’s risk appetite fell to a low of -1.27 on July 3 and has since bounced higher, which historically preceded a median spot return of 12% over the following 100 days, according to the eight prior instances identified by Block Scholes.

“Historically, such a move has preceded a more bullish outperformance in spot prices and could lead to further allocation towards risk assets such as crypto,” a spokesperson for Block Scholes told Cointelegraph.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Richard Heathcote, who until March was Tether’s chief investment officer, is planning to sell part of his 1.26% stake in the stablecoin giant, according to a Bloomberg report.

Heathcote is working with PJT Partners to sell his holding in the San Salvador, El Salvador-based company, Bloomberg said, citing sources close to the matter. The sources said discussions with potential buyers were ongoing. They declined to comment on the company’s potential valuation.

Heathcote took on a non-executive advisory role at the issuer of USDT, the largest stablecoin by market capitalization, in March, and was replaced by his deputy Zachary Lyons.

In February, Tether scaled back from plans to raise as much as $20 billion after facing investor resistance to a proposed $500 billion valuation that would rank the stablecoin issuer among the world’s most valuable private companies. Tether advisers then followed up with plans to raise $5 billion. Tether reported a full-year profit of more than $10 billion for 2025.

Tether did not respond to a CoinDesk request for comment. PJT Partners declined to comment. Heathcote could not be reached.

Music to Attract Fast and Urgent Money | Treasure of Abundance | Spiritual Wealth | 432 Hz

Trump Provides Bizarre Reason For Keir Starmer Quitting As PM

Strangeways regeneration: Apartments set to be approved

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Weekend Open Thread: Staud – Corporette.com

Music to Attract Fast and Urgent Money | Treasure of Abundance | Spiritual Wealth | 432 Hz

XRP v RLUSD, SHOCKING NeW OUSD, Stablecoin SANDWICH spreads, Flare is NEXT LEVEL, Validator Attacks

Bitcoin $57K – Have We Hit The Bottom?

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: High Hopes

-

Fashion22 hours ago

Fashion22 hours agoOpen Thread: What Great Books Have You Read Recently?

-

Politics4 days ago

Politics4 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

NewsBeat2 days ago

NewsBeat2 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Crypto World6 days ago

Crypto World6 days agoAirdrop Registration Becomes Key Focus For Remittix As RTX Launch Updates Approach

-

Sports6 days ago

Sports6 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Crypto World5 days ago

Crypto World5 days agoBinance stock trading tops $1B in first month after launch

-

Crypto World4 days ago

Crypto World4 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

NewsBeat7 days ago

NewsBeat7 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

-

Business20 hours ago

Business20 hours agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Crypto World6 days ago

Crypto World6 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

Crypto World20 hours ago

SK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

News Videos23 hours ago

News Videos23 hours agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Crypto World2 days ago

Crypto World2 days agoSouth Africa proposes crypto tax guidance under existing rules

-

Tech2 days ago

Tech2 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Business6 days ago

Business6 days agoMeta Platforms Stock Jumps 7% Today as Bloomberg Reports Company Plans to Enter the Cloud Business

-

NewsBeat5 days ago

NewsBeat5 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

News Videos11 hours ago

News Videos11 hours agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Business4 days ago

Business4 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Crypto World5 days ago

Crypto World5 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

You must be logged in to post a comment Login