Crypto World

India’s Central Bank Renews Push to Keep Crypto Out of the Financial System

The Reserve Bank of India (RBI), the country’s central bank, has reiterated its support for a cryptocurrency policy that favors a prohibition-oriented approach.

The RBI wants banks and financial institutions barred from any exposure to crypto assets and privately issued stablecoins.

Why India’s Central Bank Leans Toward Crypto Prohibition

The RBI has warned about crypto risks repeatedly and now argues for policies “leaning towards prohibition,” according to documents reviewed this week by Reuters. It wants digital assets kept outside the regulated financial system. Officials say the aim is to limit contagion risks to lenders.

The stance revives a fight the RBI lost in 2018, when a court struck down policies that had effectively banned crypto dealings. Since then, digital assets have existed in a grey zone.

Indian banks are currently allowed to engage with cryptocurrencies. However, most major lenders have stayed away from the sector after repeated cautionary statements from the RBI.

The containment line echoes caution seen across global frameworks, though most now favor regulation over isolation.

Government figures put the number of crypto traders at nearly 39 million. They held about $2.1 billion in digital assets at the end of May, according to the tax department estimates.

Follow us on X to get the latest news as it happens

Stablecoins and Offshore Trading Raise the Stakes

The RBI extended its warning to stablecoins, tokens pegged to fiat currencies. It said foreign-currency versions threaten monetary sovereignty. Rupee-backed tokens could cut the government’s currency income and strain stability during market stress.

It added that permitting stablecoins could make it harder to identify and tax cryptocurrency profits, as users would have less need to convert their holdings into fiat currencies.

Moreover, the tax department flagged offshore exchanges and private wallets as issues for tracking. Those channels make it harder to identify beneficial owners. Peer-to-peer trades in rupees also make taxable income difficult to trace.

Compliance already lags. Fewer than a quarter of the 645,000 people who traded crypto in the year ending March 2023 reported it on tax returns. India taxes crypto gains at 30% and levies a 1% tax on each trade.

The coming months will show whether the government turns the RBI’s prohibition lean into law or keeps crypto in limbo.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post India’s Central Bank Renews Push to Keep Crypto Out of the Financial System appeared first on BeInCrypto.

Marc Nachmann, Goldman Sachs global head of asset and wealth management.

CNBC

Goldman Sachs said Thursday it won deals to manage a combined $70 billion in retirement assets for Verizon Communications and Lockheed Martin, one of the larger recent announcements in the fast-growing market for outsourced corporate investing.

The mandates include about $30 billion in pension assets for Verizon and Lockheed Martin and $40 billion in Verizon defined-contribution retirement assets, which are typically 401(k)s, according to Goldman.

The moves underscore how some of America’s largest employers are increasingly handing responsibility for managing retirement assets to outside firms such as Goldman as portfolios become more complex and require expertise across public and private markets.

Competition in the multitrillion-dollar market for retirement assets is fierce among managers including Goldman, BlackRock, Russell Investments and Mercer, because the long-term institutional mandates generate steady fee revenue.

By growing that business, Goldman hopes to increase its share of revenues that are seen as stable and recurring, unlike the more volatile trading and investment banking operations.

“Large plan sponsors are consolidating responsibilities with one partner with the investment expertise and depth of platform to manage their bespoke needs,” Marc Nachmann, Goldman’s global head of asset and wealth management, said in a statement.

Goldman’s outsourced chief investment officer business had about $480 billion in assets as of March 31, while the firm’s broader asset and wealth management division oversees roughly $3.7 trillion worth of investments.

AscendEX has ceased all operations effective July 1, 2026, and told users it cannot guarantee full recovery of their balances, raising serious concerns about the exchange’s liquidity. The exchange published its official notice on July 6, five days after halting operations, citing MiCA compliance requirements, a failed strategic transaction, and deteriorating market conditions as the main reasons behind the crypto exchange shutdown.

The July 6 notice outlined the exchange’s financial challenges in unusually direct language. “We relied on an agreed strategic transaction that was to provide liquidity to grow the platform, and the counterparty did not perform; wider crypto market conditions have added further pressure,” AscendEX said. The exchange added that it is assessing available options for account holders while cautioning that it cannot guarantee withdrawal timing or recovery amounts.

— Coin Bureau (@coinbureau) July 9, 2026

JUST IN: ASCENDEX SHUTS DOWN AND USERS MAY NOT GET FULL BALANCES BACK

JUST IN: ASCENDEX SHUTS DOWN AND USERS MAY NOT GET FULL BALANCES BACK

Crypto exchange AscendEX has ceased operations on July 1, citing MiCA, regulatory, financial and operational pressure.

The company’s statement indicated that current liquidity issues may restrict users from… pic.twitter.com/am7MLyBhFg

MiCA also played a role in the decision. The EU’s Markets in Crypto-Assets regulation came fully into effect on July 1, and AscendEX does not hold authorization under that framework. However, the exchange also pointed to financial and operational pressures, suggesting multiple factors contributed to its closure rather than regulation alone.

Discover: The Best Crypto to Diversify Your Portfolio

ZachXBT Flagged Empty Hot Wallets Nine Days Before the Announcement

On-chain investigator ZachXBT publicly raised concerns on June 26 after receiving multiple reports of delayed withdrawals from AscendEX users. His review of the exchange’s publicly labeled hot wallet addresses found very low balances across ETH, USDT, USDC, and SOL.

![]()

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

According to reports citing ZachXBT’s Telegram post, the exchange’s hot wallets appeared insufficient to cover multiple seven figure withdrawal requests reported by users. He advised affected customers to file reports with financial regulators and law enforcement in their jurisdictions and warned against depositing additional funds.

AscendEX has since suspended automated withdrawals, with all requests now subject to manual review. The exchange also stated, “We are not in a position to give assurances about timing or amounts today. No account holder or group of account holders is being given priority outside the documented review process.”

— Coin Bureau (@coinbureau) June 26, 2026

ALERT: ASCENDEX WITHDRAWAL ISSUES SPARK LIQUIDITY CONCERNS

ALERT: ASCENDEX WITHDRAWAL ISSUES SPARK LIQUIDITY CONCERNS

On-chain sleuth ZachXBT flagged AscendEX for delaying user withdrawals while its hot wallets show critical shortages of large cap assets including ETH, USDT, and SOL, raising liquidity concerns.

Some users have… pic.twitter.com/zjMjY6S9cz

A Platform With a Prior Hack and a History as BitMax

AscendEX launched in 2018 as BitMax before rebranding in March 2021. Later that year, the exchange suffered a $78 million hot wallet hack that blockchain security firms attributed to North Korea’s Lazarus Group.

At the time, AscendEX said it would fully reimburse affected users. That response stands in contrast to its current position, where it says it cannot guarantee the timing or amount of any asset recovery. The scale of the current shortfall remains unclear.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

What Comes Next for AscendEX Users

The next major development will be whether AscendEX enters a formal insolvency process. Its July 6 notice states, “If any formal insolvency or similar process is commenced, the treatment of unresolved balances or claims may be subject to that process.” While no such proceeding has been announced, the exchange has acknowledged that possibility.

Users with funds on the platform should preserve account records and withdrawal requests. Following ZachXBT’s recommendation, affected customers may also consider reporting their cases to financial regulators and law enforcement in their jurisdictions. For now, withdrawals remain under manual review, and AscendEX has not provided a timetable for resolving outstanding claims.

Discover: The Best Token Presales

The post AscendEX Collapse: MiCA Deadline, Failed Financing, and Empty Hot Wallets appeared first on Cryptonews.

For Ethereum Institutional’s founders, becoming an independent nonprofit rather than remaining within the foundation was a deliberate choice.

“The EF has always been quite vocal about its principle of subtraction,” Dawson said, referring to the organization diving up responsibilities for the network to other organizations . “This is an example of that increasing decentralization, and the number of nodes participating in representing Ethereum.”

Operating outside the foundation also gives the organization greater freedom, Walsh said.

“We feel like we have a lot more autonomy and freedom to work as an independent entity,” he said. “We can get a bit more opinionated, and a bit more aggressive, in terms of being able to support these teams.”

For years, the Ethereum Foundation has walked a careful line in how much influence it exerts over the ecosystem. Its mandate has largely been to coordinate protocol development and steward Ethereum’s technical roadmap, rather than act as a central authority driving business development or adoption. But as the network grew, some in the community pushed for the foundation to take on a more active role in areas like institutional outreach and ecosystem coordination, responsibilities it has increasingly chosen to decentralize instead.

Ethereum Institutional joins a growing network of organizations taking on specialized roles within Ethereum. Last month, EthLabs launched to support ecosystem development, while firms such as Etherealize, launched in 2025, have focused on bringing institutions onchain through commercial products and services.

Key Takeaways

- Evercore ISI maintained its Outperform stance with a $1,100 price objective following Costco’s June sales figures

- Comparable store sales climbed 7.6% domestically and 7.0% worldwide, with gas prices and currency fluctuations stripped out

- Goldman Sachs continued its Buy recommendation at $1,159; J.P. Morgan sustained its Buy designation at $1,100

- Domestic foot traffic increased 3.2%, marking the seventh month in a row with two-year trends exceeding 6%

- More challenging year-over-year metrics anticipated for July and August, with traffic comparisons becoming tougher by 100–150 basis points

Costco (COST) stock continues to receive support from Wall Street analysts following the warehouse club’s June sales disclosure, with several prominent firms reaffirming their positive outlooks and target prices.

Costco Wholesale Corporation, COST

Evercore ISI confirmed its Outperform designation while maintaining a $1,100 price objective. Analysts at the firm highlighted Costco’s core comparable store sales advancement of 7.6% domestically and 7.0% on a worldwide basis, with both metrics adjusted to exclude gasoline and currency translation impacts.

COST was hovering near the $1,050–$1,060 zone when these ratings were issued, suggesting Evercore’s target represents moderate appreciation potential from present levels. Data from InvestingPro indicates the shares may be trading above their Fair Value calculation.

Domestic customer traffic expanded 3.2% during June. This performance maintained the two-year combined traffic comparison above the 6% threshold for a seventh straight month, a pattern that Wall Street observers have been monitoring attentively.

Fuel station revenues contributed positively to the overall picture. These sales surged in the low-30% territory on a year-over-year basis, powered by a 22% increase in average retail prices and high-single-digit volume expansion in gallons dispensed.

Domestic transaction size growth, excluding gasoline, registered at 4.3%. Evercore’s analysis suggested approximately 1–2% stemmed from price inflation, with the remainder attributable to increased items per shopping trip and product category mix shifts.

Global Markets Show Moderation

Beyond U.S. borders, performance showed some moderation. Canadian core comparables reached 4.9%, representing a 120-basis-point decline from the preceding three-month average. Additional international territories recorded 5.6%, likewise down 110 basis points from recent performance levels.

June’s aggregate comparable sales expansion totaled 8.8%, although core comparables of 7.0% marked a pullback from May’s 8.7% figure.

Goldman Sachs analyst Kate McShane preserved a Buy recommendation with a $1,159 price objective. McShane observed that while June figures landed marginally below consensus forecasts, the shortfall was partially attributable to sales cannibalization from recently opened warehouses rather than any weakness in fundamental demand patterns.

McShane further emphasized that company leadership identifies no significant shifts in shopper behavior or the competitive landscape. Membership renewal patterns and customer traffic metrics remain healthy.

J.P. Morgan aligned with this perspective, likewise sustaining a Buy rating at a $1,100 price target.

Baird preserved its Outperform stance at $1,100. Gordon Haskett confirmed its Buy designation and elevated its target to $1,200, characterizing June’s 7.0% same-location sales expansion as marginally below expectations but nevertheless robust.

More Difficult Year-Over-Year Metrics Approaching

Not all analysts shared the same enthusiasm. DA Davidson and Citi both retained Neutral classifications, establishing targets at $1,000 and $1,020 respectively. Both institutions referenced the sequential slowdown in sales momentum from May through June.

Telsey confirmed its Outperform rating at $1,135 but conceded June’s performance fell short of its 10.6% forecast.

Evercore cautioned that year-over-year comparisons will intensify throughout the summer months. Traffic benchmarks become 100 basis points more demanding in July and 150 basis points more challenging domestically.

Costco’s aggregate revenue expansion over the trailing twelve-month period registers at 9.23%, underpinning a market capitalization of $422.69 billion.

Goldman’s McShane also referenced Costco’s pilot programs with standalone fuel facilities as a development worth monitoring, characterizing it as evidence of the company’s strategic focus on long-term member value enhancement.

Led by recent positive clinical results from Lilly, Roche, and AstraZeneca, the $100 billion market for GLP-1 could potentially include other medical areas like cardiovascular, kidney, liver, arthritis, and sleep apnea disorders as the drugs evolve to treat not just diabetes and obesity, but all kinds of metabolic conditions.

In Q1 2026, Lilly reported a quarterly earning of $19.8 billion worldwide, up 56% from last year, with Mounjaro and Zepbound together accounting for $12.9 billion. The company is also continuing to test new therapies to maintain its lead in the metabolic health market; a cholesterol-lowering treatment it’s developing with Verve has shown promising early efficacy.

Merck reported Q1 2026 revenues of $16.3 billion led by its strong portfolio in oncology and animal health. “We’re in the midst of initial launches of over 20 new products,” said CEO Robert Davis on the earnings call in April, “almost all of which have blockbuster potential across a broad set of therapeutic areas.” The move to diversify and re-design their portfolio is timely as the company’s blockbuster cancer immunotherapy, Keytruda (which accounted for $8 billion of their Q1 revenue), has patents set to expire in 2028.

The second dimension, Financial Performance, was assessed using data from Statista’s revenue database, which contains company financial data for the last five years. The companies had to meet certain criteria to be considered for the evaluation, including generating a revenue of at least $100 million in 2025. We evaluated financial performance on a variety of metrics, including short-term (2023-2025) and long-term (2021-2025) revenue growth, both in relative and absolute terms, changes in net income, asset growth, and the evolution of the company’s return on assets (ROA) (all 2023-2025).

The third dimension, Sustainability Transparency, was evaluated based on ESG data among standardized KPIs from Statista’s ESG Database and targeted data research. To formulate a comprehensive ESG index, multiple Key Performance Indicators were collected. For the environmental evaluation, this included the 2024 carbon emissions intensity and reduction rate compared to 2022, as well as the Carbon Disclosure Project (CDP) score. The social dimension assessed the share of women on the board of directors and the existence of a human rights policy. The governance dimension evaluated whether a company had a Corporate Social Responsibility (CSR) report adhering to the Global Reporting Initiative (GRI) guidelines and a compliance or anti-corruption guideline.

Nearly every transaction on Ethereum’s layer-2 networks passes through a single machine, run by a single company, called a sequencer. It orders trades, sets the pace of the chain, earns the fees, and can go dark or say no. This guide explains what sequencers actually do, why the most decentralized ecosystem in crypto runs its fast lanes through central operators, what can and cannot go wrong, and the roadmaps racing to fix it.

Summary

- Ethereum layer 2 networks rely on centralized sequencers that order transactions, collect fees, and can temporarily halt network activity during outages.

- Sequencers cannot steal user funds because Ethereum secures transaction validity, but they can influence transaction ordering, censorship, and network availability.

- Rollup developers are working toward decentralized sequencing models to reduce reliance on a single operator while preserving Ethereum’s security and scalability.

Here is an uncomfortable fact about the scaled, modern Ethereum: when you swap on an Arbitrum exchange, mint on Base, or pay on Optimism, your transaction is received, ordered, and confirmed by one machine, operated by one company. That machine is the sequencer, and it occupies a position of quiet, enormous power: it decides which transactions enter the chain and in what order, it collects the network’s fee revenue, and when it stops, as major sequencers have during outages, the entire network simply pauses, every app frozen at once.

The layer-2 rollups are how Ethereum scaled, moving execution off the congested base chain while inheriting its security, and they now carry a majority of the ecosystem’s activity. That success makes the sequencer the most consequential piece of centralized infrastructure in an ecosystem whose founding promise is decentralization, and the tension is not a secret; it is an engineering roadmap, with every major rollup publicly committed to fixing it and none finished. Meanwhile the base layer itself is being redesigned around adjacent ideas, with the coming Glamsterdam upgrade enshrining proposer-builder separation into the protocol, which will reshape the environment sequencers operate in.

This guide covers the sequencer honestly: what a rollup is and what job the sequencer does inside it, the specific powers a centralized sequencer holds and their real-world failure record, the crucial distinction between what a sequencer can and cannot do to your funds, the economics of sequencing and why operators are slow to give it up, the decentralization designs, shared sequencing, based sequencing, sequencer sets, competing to replace the single machine, and how to evaluate any L2’s actual trust profile today.

Rollups in one section, and the sequencer’s job

A rollup is a blockchain that executes transactions on its own fast, cheap environment, then posts compressed records of everything it did to Ethereum, inheriting the base chain’s security for its history. Optimistic rollups post results and allow a challenge window for fraud proofs; validity rollups post cryptographic proofs that the results are correct. In both designs, Ethereum is the court of final record, and the rollup is a high-throughput execution venue whose state can always, in principle, be reconstructed and verified from the data it posts down below.

Someone, though, has to run the fast venue in real time: receive the flood of incoming transactions, decide their order, execute them, hand users instant confirmations, and batch the results down to Ethereum. That someone is the sequencer. It is best understood as three roles fused: the mempool and matching engine that orders the flow, the block producer that executes it, and the shipping department that posts batches to the base chain. The ordering role is the powerful one, because in any financial system, transaction order is money: who gets the arbitrage, whose liquidation lands first, who buys before the price moves. On Ethereum’s base layer that power is fragmented across thousands of validators and an entire adversarial supply chain built to capture it; on almost every major rollup today, it belongs to one operator, appointed by the team, running the official sequencer.

Why did the most decentralization-obsessed ecosystem in software ship its scaling layer this way? Because centralized sequencing is fast, simple, and safe to bootstrap: one machine gives instant confirmations, no consensus overhead, clean upgrade paths, and a single throat to choke during the inevitable early bugs. The architects’ wager was that sequencing could be centralized temporarily because the rollup design strictly limits what the sequencer can do, a wager the next two sections examine from both sides.

What the sequencer can do to you, and what it cannot

The sequencer’s powers are real, and enumerating them precisely matters more than the usual hand-waving in either direction.

What it can do. It can censor: refuse to include your transaction, whether by policy, error, or legal compulsion, and regulated operators have compliance obligations that make selective exclusion more than hypothetical. It can order: place its own or favored transactions ahead of yours, extracting the value that ordering confers, invisibly and profitably; most major operators publicly forswear this, and the forswearing is a policy, not a protocol guarantee. It can stop: sequencer outages have repeatedly frozen major rollups for hours, halting every application simultaneously, a failure mode with no analogue on the base chain, where thousands of validators mean the chain simply does not stop. And it can set the pace and price of inclusion, since it is the sole gateway to the network’s blockspace in real time.

What it cannot do, and this is the rollup design’s genuine achievement: it cannot steal. The sequencer cannot forge a transaction spending your funds, because every transaction requires your signature and the fraud or validity proofs posted to Ethereum would expose any invented state. It cannot rewrite settled history, because the history lives on the base chain. And, critically, it cannot permanently trap you, because well-built rollups include an escape hatch: a mechanism to force-include transactions directly through Ethereum, bypassing the sequencer entirely, so that even a fully censoring or dead sequencer can only delay users, not imprison their funds. The delay is real, force inclusion is slow and clumsy, but the distinction between a chokepoint that can inconvenience you and a custodian that can rob you is the entire difference between the rollup model and a centralized exchange, and it is why the ecosystem tolerated centralized sequencing at all. The trust profile resembles a bridge with a strong trust-minimized design rather than a multisig one: concentrated operationally, constrained cryptographically.

The honest risk summary, then: your assets on a major rollup are secured by Ethereum; your access, timing, and fair ordering are secured by one company’s machine, policies, and legal situation. For a casual user the distinction rarely bites. For a trader whose profits live in ordering, for a protocol whose execution quality depends on fair ordering and whose liquidations must land on time, and for anyone in a jurisdiction a compliant operator might be told to exclude, the sequencer is the trust assumption that matters most and is audited least.

The outage record: what centralization has actually cost

The sequencer risk is not theoretical, and the incident record is the best syllabus for what single-operator infrastructure means in practice. Every major rollup has suffered sequencer downtime: hours-long halts from surging inscription traffic, stalls from software bugs in batch posting, freezes during upgrades that went sideways. The pattern across incidents is consistent and instructive. Funds were never lost, the base-chain security model held every time, and the networks resumed with their histories intact, which is the design working as promised. What stopped, each time, was everything else: trading froze mid-move, liquidation engines could not reach positions as prices moved, arbitrage broke against live markets elsewhere, and users learned that force-inclusion, the theoretical escape hatch, was in practice too slow and too technical to matter inside an incident measured in hours.

The subtler lessons sit in the second-order effects. During one prominent outage, the network’s applications discovered their own emergency procedures assumed a working sequencer: pausing markets, updating oracles, and even communicating with users all routed through the machine that was down. During another, the resumption itself became a trading event, as hours of queued transactions landed in a burst against stale prices, a miniature of the reconciliation dynamics every gap-prone market knows. And across all of them, the operator’s incident response, status pages, engineer availability, post-mortems, was the de facto governance of a multi-billion-dollar economy for the duration, performed by a company under no protocol obligation to perform it well.

The record’s summary is fair to both sides of the argument: the constrained-power design has truly protected funds through every failure, and the single-machine design has just as surely imposed correlated, economy-wide halts that a decentralized system would not, which is precisely the trade the roadmaps exist to unwind.

It is also worth placing the sequencer inside the rollup’s full trust stack, because it is the most visible dependency but not the only one. A rollup’s security rests on three legs: the data it posts to Ethereum, which is what makes reconstruction possible and which the blob-fee era made radically cheaper; the proof system, fraud or validity, that polices state correctness, several of which still run with training wheels, security councils and permissioned challengers standing in for mature proofs; and the sequencer, which governs liveness and ordering. Independent frameworks grade rollups across all three, and the grades routinely surprise users who assumed the marketing: networks celebrated as trust-minimized frequently carry upgrade keys and council powers that outrank the sequencer question entirely. The sequencer is the right place to start reading an L2’s trust profile. It is the wrong place to stop.

The economics: why giving it up is hard

Sequencing is not just power; it is revenue, and the revenue explains the pace of decentralization better than any technical obstacle. A sequencer collects the difference between what users pay for L2 transactions and what it costs to post their data to Ethereum, a margin that widened dramatically when Ethereum’s blob-based data pricing collapsed posting costs, plus whatever ordering value it chooses to capture or auction. For a major rollup this is a nine-figure annual business, and it currently flows to the operating company or foundation, funding development and, in several cases, constituting the primary revenue behind the network’s token.

Decentralizing the sequencer means distributing exactly this revenue, and the designs on the table are, among other things, proposals about who gets paid. That is not cynicism; it is the correct lens for evaluating the roadmaps, because a decentralization plan that never specifies where sequencing revenue goes is a plan that has not confronted its hardest question. It also frames the user’s side of the bargain today: centralized sequencing quietly subsidizes the networks users enjoy, the same revenue-and-token linkage question running through every fee-generating protocol, and every step toward neutrality redistributes a pie someone currently owns.

The numbers behind the revenue argument are worth one concrete paragraph. An L2’s gross margin is the spread between user fees collected and data costs paid to Ethereum, and the blob-fee era transformed that spread: posting costs for major rollups collapsed by orders of magnitude while user fees, though lower, fell less, leaving the large networks operating at gross margins that most software businesses would envy. Public dashboards track the arithmetic in real time, revenue in, data costs out, and the residual accrues today to whoever runs the sequencer. That residual funds engineering, subsidizes user fees during growth pushes, and, for token-bearing networks, constitutes the cash flow every valuation argument ultimately references.

Decentralization designs must answer where it goes: to a staked sequencer set as yield, to a shared network as service fees, to Ethereum validators under based sequencing, or to users as rebates, and each answer creates and destroys different constituencies. The engineering of neutral sequencing was largely solved on whiteboards years ago; the political economy of its revenue is the part still being negotiated, which is the single most clarifying fact about why the timelines are what they are.

The fixes: three roads to a neutral sequencer

Three families of designs compete to replace the single machine, each trading different things.

The first is the sequencer set: replace one operator with a permissioned or staked committee running consensus among themselves, rotating leadership, so that censorship requires collusion and outage requires correlated failure. It is the incremental path, and its critics note that a small committee of known entities is a smaller improvement than it appears, particularly against legal compulsion, which scales to committees easily.

The second is shared sequencing: independent networks whose business is providing decentralized ordering as a service to many rollups at once, with the added promise of atomic cross-rollup composability, transactions that execute across multiple L2s together or not at all, recreating some of the seamlessness the multi-rollup world fractured. The trade is a new external dependency and, again, the revenue question: a shared sequencer wants paying customers, and rollups guard their margins.

The third and most Ethereum-native is based sequencing: hand ordering back to Ethereum itself, letting the base chain’s validators sequence L2 transactions as part of block production. It maximally inherits Ethereum’s neutrality and censorship resistance, at the cost of Ethereum’s pace, confirmations at base-layer speed rather than the instant feel users have learned, though pre-confirmation designs aim to restore the speed. Based sequencing’s fortunes are entangled with the base layer’s own evolution: the Glamsterdam upgrade’s enshrined proposer-builder separation restructures exactly the block-production pipeline that based rollups would plug into, which is why sequencer roadmaps and Ethereum’s core roadmap now read as one document with two authors.

No major rollup has completed any of the three. The public commitments are real, staged plans, published designs, testnets, and the timelines have slipped for years, because the current arrangement works, earns, and only embarrasses its operators when something breaks. The realistic forecast is a long middle period of committees and hybrid designs, with full neutrality arriving network by network, unevenly, this decade.

A note on terminology prevents one common confusion: the sequencer is not the prover, and decentralizing one does nothing for the other. The prover, in validity rollups, generates the cryptographic proofs of correct execution; the sequencer orders and executes. A network can decentralize sequencing while proving remains one machine, or the reverse, and the two roles fail differently: a dead prover delays finality on Ethereum while the chain keeps running, a dead sequencer halts the chain while finality of past batches stands. Roadmap language blurs the roles constantly, and reading which one a decentralization milestone actually addresses is a small skill that pays for itself.

How to read an L2’s actual trust profile

For a user or builder choosing among rollups today, the sequencer question compresses into a practical checklist. Who runs the sequencer, and under what legal jurisdiction? Does the network have working force-inclusion, and what is its delay, the number that bounds worst-case censorship? What is the outage history, and did funds ever depend on the operator’s goodwill during one? Is there a published ordering policy, first-come-first-served, private mempool, auction, and any mechanism enforcing it beyond reputation? What stage is the decentralization roadmap actually at, running code versus blog post? And where does sequencing revenue go, because that answer predicts the roadmap’s pace better than the roadmap does.

The sequencer is the honest asterisk on Ethereum’s scaling triumph: the rollup ecosystem genuinely extended the base chain’s security to vastly more activity at vastly lower cost, and it did so by concentrating, temporarily and by design, the one power the base chain had most successfully dispersed. The asterisk is shrinking, slowly, under public pressure and published plans, and until it is gone, the single most useful thing a user can know about any L2 is exactly what its one important machine can and cannot do to them.

The wider stakes deserve a closing frame, because the sequencer question is Ethereum’s decentralization thesis meeting its scaling success, and the resolution will define what the ecosystem actually is. If the rollup era ends with a handful of corporate sequencers ordering most on-chain activity, then Ethereum will have rebuilt, at the execution layer, the intermediated structure it was designed to replace, with the base chain reduced to a settlement court for private venues. If the decentralization roadmaps deliver, based sequencing, credible committees, shared networks, then the scaling will have been genuine: more activity, same neutrality, the original promise kept at a hundred times the throughput. Both futures are still open, the incentives lean toward the first and the culture toward the second, and the outcome will be decided not by white papers but by the unglamorous engineering and revenue negotiations described above, network by network, over the next several years. Users are not spectators to that contest: the trust profiles are public, the alternatives are one bridge away, and where activity settles is the only vote the operators have ever reliably counted.

A practical postscript for builders, finally: sequencer risk is inherited. An application deployed on a rollup imports its sequencer’s outage record, censorship surface, and ordering policy as silent dependencies, and the mature practice, visible in how serious protocols now deploy, is to treat chain selection as a security decision, document the force-inclusion path in the runbook, and design liquidation and oracle machinery to fail safely through a halt. The sequencer is infrastructure, and the first rule of infrastructure applies: it is invisible until the day it is the only thing that matters.

The reader’s shortlist for following the story: the independent rollup-risk frameworks that grade each network’s sequencer, proofs, and upgrade keys; the networks’ own decentralization roadmap pages, read with dates, not adjectives; the outage post-mortems, which teach more per paragraph than any documentation; and the base-layer upgrade calendar, since Glamsterdam-era changes to Ethereum’s block pipeline reshape what based sequencing can offer. The chokepoint is well documented by everyone except the marketing, and the documentation is where the truth lives.

If one image should survive this guide, make it the geometry: Ethereum scaled by turning one broad, slow, neutral road into a system of fast toll lanes, each with a single operator at the booth. The lanes carry the traffic, the operators are competent, and the toll revenue is building better booths. But the map of who can stop which cars, and where, is now the most important map in the ecosystem, and every reader of this piece can pull it up for any network in about five minutes. Do that, once, for wherever your funds live. It is the highest-yield five minutes in crypto self-custody.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Network designs and roadmaps described are current as of July 9, 2026, and change frequently. Always do your own research.

Frequently asked questions

What is an L2 sequencer in simple terms?

A sequencer is the machine that runs a layer-2 rollup in real time: it receives transactions, decides their order, executes them, gives users instant confirmations, and posts compressed batches of the results to Ethereum. On nearly every major rollup today, the sequencer is a single server operated by the network’s founding company, making it the most centralized component in Ethereum’s scaling stack.

Can a sequencer steal my funds?

No. The sequencer cannot forge transactions from your account, because everything requires your signature, and it cannot fake results, because the rollup’s proofs posted to Ethereum would expose invalid state. Its powers are limited to ordering, delaying, censoring, and halting. Well-designed rollups also include force-inclusion mechanisms that let users push transactions through via Ethereum directly, so even a hostile sequencer can delay but not permanently trap funds.

What happens when a sequencer goes down?

The network effectively pauses: no new transactions confirm, and every application on the rollup freezes simultaneously until the operator restores service. Major rollups have suffered such outages lasting hours. Funds remain safe throughout, secured by Ethereum, but access stops, which matters greatly for time-sensitive positions like loans near liquidation.

Why are sequencers centralized if Ethereum is decentralized?

Because centralized sequencing was the pragmatic way to launch: one operator provides instant confirmations, simple upgrades, and clean incident response while the technology matured. The rollup design constrains what the operator can do, and every major network has published a decentralization roadmap. The trade-off was consciously temporary; its length is the controversy.

What is based sequencing?

Based sequencing hands transaction ordering back to Ethereum itself, letting the base chain’s validators sequence the rollup’s transactions during block production. It gives the rollup Ethereum’s full neutrality and censorship resistance, at the cost of slower confirmations, which pre-confirmation designs aim to offset. It is the most Ethereum-aligned of the decentralization paths.

What is a shared sequencer?

A shared sequencer is an independent network that provides decentralized transaction ordering as a service to multiple rollups simultaneously. Beyond decentralization, its selling point is atomic cross-rollup composability, the ability for transactions to execute across several L2s together, which single-rollup sequencers cannot offer.

Do sequencers extract MEV from users?

They can, since ordering power is exactly what MEV extraction requires, and a sequencer sees every transaction before it lands. Major operators publicly commit to neutral policies like first-come-first-served ordering, and some route ordering value into public goods or auctions. These are policies rather than protocol guarantees, which is a core argument for decentralizing the role.

How do I check how centralized a specific L2 is?

Ask five questions: who operates the sequencer and where; whether force-inclusion exists and how long it takes; the network’s outage history; the published ordering policy; and the actual stage of the decentralization roadmap. Independent trackers grade major rollups on these dimensions, and the grades differ far more than the marketing does.

Key Highlights

- Virax Biolabs entered into an exclusive distribution agreement with Fosun Diagnostics for six Southeast Asian countries

- The partnership encompasses the company’s ImmuneSelect immune profiling portfolio for research applications

- Thailand will serve as the initial launch market with a focus on tuberculosis research before regional expansion

- Fosun Diagnostics operates under Fosun Pharma, a healthcare giant with approximately $5.8 billion in 2025 revenues

- Shares of VRAX climbed more than 241% following the announcement; the company maintains a market capitalization of $2.53M

On July 9, 2026, Virax Biolabs (VRAX) revealed that its United Kingdom-based subsidiary has entered into an exclusive commercial distribution agreement spanning multiple countries with Fosun Diagnostics. The announcement triggered a dramatic 241% surge in VRAX shares during trading.

Virax Biolabs Group Limited, VRAX

The partnership establishes Fosun Diagnostics as the exclusive distributor of Virax’s ImmuneSelect portfolio — a collection of research-grade immune profiling tools — throughout six key Southeast Asian territories: Thailand, Vietnam, Indonesia, the Philippines, Singapore, and Malaysia.

Fosun Diagnostics operates as part of Fosun Medtech, itself a segment of Fosun Pharma. With Fosun Pharma recording RMB 41.662 billion in 2025 revenues (approximately $5.8 billion), Virax has secured a partnership with a financially robust distribution network throughout the region.

According to the agreement’s terms, Virax will deliver products such as ELISpot assay plates — specialized tools designed to evaluate cellular immune reactions — to Fosun through a purchase order system. The pricing model incorporates volume-based discount structures.

The collaboration launches immediately with product availability and initially concentrates on tuberculosis research initiatives in Thailand, with subsequent rollout planned for the remaining five markets.

The exclusive nature of the partnership depends on achieving specified minimum purchase volumes and performance benchmarks. Failure to reach these targets could result in modifications to the exclusivity provisions.

The agreement structure also provides flexibility for future expansion into supplementary product categories, increased supply volumes, and possible OEM or white-label manufacturing arrangements.

Understanding ImmuneSelect

ImmuneSelect represents Virax’s commercially available portfolio of research-only products. This line operates independently from ViraxImmune, the company’s diagnostic platform currently undergoing clinical trials and regulatory review processes.

This differentiation is significant. ImmuneSelect has already achieved market availability and is attracting commercial partnerships. ViraxImmune remains in the development pipeline.

James Foster, Chairman and CEO of Virax Biolabs, characterized the partnership as “a major step forward in the commercial rollout” of the ImmuneSelect platform throughout Southeast Asia.

Leon Zhang, International Commercial Head for China Domestic Business at Fosun MedTech, indicated that Fosun is exploring ELISpot-based research opportunities across the regional markets.

VRAX Company Overview

Virax Biolabs operates with a market capitalization of merely $2.53 million, positioning it firmly in micro-cap territory. The stock’s average daily trading volume hovers around 1.05 million shares.

The latest analyst coverage on VRAX assigns a Buy rating, accompanied by a $1.00 price target.

Current technical sentiment indicators classify the stock as Sell, creating a notable contrast with today’s substantial upward price movement.

The 241%+ gain places significant attention on the stock, though price volatility of this magnitude is relatively common for companies operating at this market capitalization level.

As of July 9, 2026, the distribution framework is operational and Fosun can immediately begin submitting purchase orders under the terms of the agreement.

This is the fork worth fighting over, and it is being missed because the debate is stuck on the wrong axis. Legislators frame the choice as safety versus freedom; critics frame it as protection versus privacy. Both accept a false premise, that keeping children out of adult spaces requires identifying the adults. It does not. The real choice is between two ways of verifying age: one that minimizes data and forgets you the instant you pass, and one that maximizes data and remembers everyone forever. Only the second is surveillance, and only the second is currently the path of least resistance.

The window to insist on the first is now, while these bills are still moving. The KIDS Act heads to a skeptical Senate. Chat Control 2.0 is targeting political agreement in July. In both cases the principle, that platforms should be able to tell adults from children, has effectively been settled. What has not been settled is whether that capability is built on privacy-preserving proofs or on a mountain of uploaded passports. That is a technical decision with civil liberties consequences, and it is being made, right now, largely by default.

There is a larger reason to settle this well, and settle it now. The old sorting of internet traffic into “bot or human” is already breaking down: a verified third category is arriving, AI agents acting, with authorization, on behalf of people, companies and governments, and they will soon need to prove what they are permitted to do without unmasking whoever stands behind them. “Know Your Agent” will demand the very same privacy-preserving architecture we are arguing over now for people. Decide it well for human age checks, and we set the pattern for everything that follows. Decide it badly, and we hard-wire surveillance into the identity layer of the internet, for humans and machines alike.

XRP’s price has approached $1 in recent weeks, and now the key question is whether that level can halt the decline.

Ripple (XRP) Price Predictions: Analysis

Key support levels: $1

Key resistance levels: $1.3, $1.6, $2

Sellers are Returning

After a short relief rally towards $1.18, sellers have returned and seem to have full control over XRP. In the last four days, the price has been falling without any bounce and appears ready to test the key support at $1 again.

In late June, the price hovered just above $1 for several days before buyers managed to push XRP higher. However, this could turn out to be a dead cat bounce before new lows. That’s because the overall trend remains bearish.

Buyers Vanished

Since last Sunday, buyers have vanished from the order book. As soon as the price touched $1.18, buy pressure collapsed, paving the way for sellers to take control.

The only positive thing about XRP right now is the falling volume. Even if sellers appear in control, the volume continues to decline. This indicates a lack of conviction, which could mean that buyers are waiting for an opportunity to return.

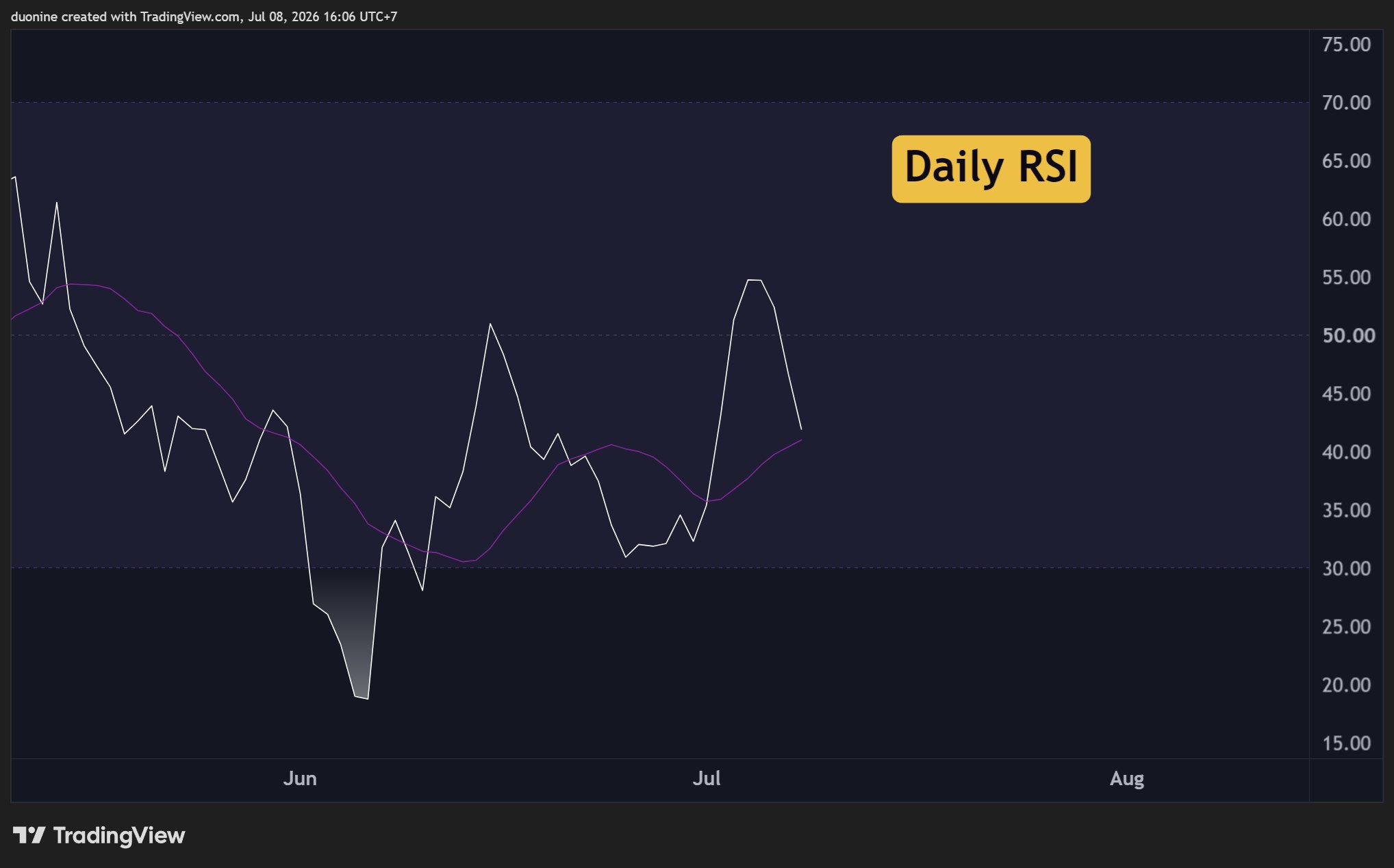

Daily RSI Remains Bearish

This summer, the RSI on the daily timeframe made two attempts to move beyond 50. However, each time, the price did a full reversal, erasing any hopes of a sustained rally. This can be interpreted as bearish.

On the other hand, the RSI is making higher lows and higher highs. This is encouraging, but unless the price does the same, it will remain a bullish divergence that is not confirmed.

The post Ripple (XRP) Price Predictions for This Week (July 9) appeared first on CryptoPotato.

Heatwave drives office working boom as employees ditch sweaty WFH in favour of air con

Goldman Sachs wins $70B in asset management for Verizon, Lockheed Martin

Leandro Andrés Bertazzo Jumps From Plane Midflight, Dies

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: High Hopes

-

NewsBeat4 days ago

NewsBeat4 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Crypto World6 days ago

Crypto World6 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Fashion3 days ago

Fashion3 days agoOpen Thread: What Great Books Have You Read Recently?

-

Politics6 days ago

Politics6 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Fashion4 hours ago

Fashion4 hours agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

News Videos2 days ago

News Videos2 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Tech2 days ago

Tech2 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Business3 days ago

Business3 days agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports2 days ago

Sports2 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Crypto World6 days ago

Crypto World6 days agoESMA Expands Crypto Register by 37 Firms Following MiCA Transition Period

-

Crypto World3 days ago

SK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

Crypto World4 days ago

Crypto World4 days agoSouth Africa proposes crypto tax guidance under existing rules

-

News Videos3 days ago

News Videos3 days agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech4 days ago

Tech4 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Business6 days ago

Business6 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Sports2 days ago

We have punished the disrespect

-

Crypto World7 days ago

Crypto World7 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

-

News Videos3 days ago

News Videos3 days agoAvoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

-

Crypto World6 days ago

Crypto World6 days agoAlibaba bans Claude Code over alleged backdoor security concerns

You must be logged in to post a comment Login