Crypto World

Hyperliquid highlights how on-chain perps may disrupt Wall St

Perpetual futures—derivatives that typically trade without fixed expiry dates—are increasingly being positioned as a next-generation instrument for markets that never sleep. In a Wednesday post on X, blockchain-focused asset manager Pantera Capital argued that decentralized venues built around onchain infrastructure could make 24/7 perpetual trading materially more competitive with traditional finance by improving continuity of trading and simplifying contract mechanics.

Pantera, which is an investor in the Hyperliquid ecosystem, highlighted Hyperliquid as a leading example of that shift. The firm also pointed to growing interest from established market operators, including NYSE parent Intercontinental Exchange (ICE), and cited data suggesting onchain perpetuals have taken a meaningful share of total perpetual volumes over the last year-plus.

Key takeaways

- Pantera says perpetual futures offer structural advantages—such as 24/7 trading and continuous price discovery—over many traditional derivative formats.

- Hyperliquid is presented as the clearest onchain case study, extending perpetuals from crypto to equities, commodities, and stock indices.

- Pantera claims decentralized exchange (DEX) perpetual volumes have risen to 14% of centralized exchange (CEX) perpetual volumes, up from less than 1% in early 2023.

- Pantera estimates Hyperliquid represents about 40% of onchain perpetual trading volume and generated $13.5 million in weekly fees over the past seven days, according to DefiLlama data.

- Traditional finance firms are moving toward onchain 24/7 markets, with ICE leadership urging regulators to avoid a “level playing field” disadvantage for onchain perps.

Why perpetuals are attracting attention beyond crypto

Perpetual futures have long been a staple in crypto markets, but Pantera’s argument is that their core mechanics translate well to broader financial products. According to the asset manager, onchain perpetual venues benefit from several “structural advantages” relative to conventional derivatives: trading can run continuously, positions don’t face the same kind of scheduled contract expiries, position management can be simpler, and prices can reflect ongoing demand through uninterrupted markets.

The point matters for investors and market participants because it reframes the debate away from whether derivatives can be moved to blockchain and toward how the product’s operational characteristics change trading behavior. If market hours and contract roll cycles are reduced, liquidity dynamics and execution practices may shift—particularly for strategies that rely on staying continuously exposed rather than rebalancing around expiry windows.

Hyperliquid’s expansion and the push toward “housing all of finance”

Pantera specifically singled out Hyperliquid as evidence that perpetuals can spread quickly when the venue’s design supports both trading continuity and a growing menu of assets. The firm said Hyperliquid has gone beyond cryptocurrencies and expanded perpetual futures into equities, commodities, and stock indices as part of founder Jeff Yan’s vision of “housing all of finance.”

That expansion is significant because it introduces a compatibility question that often holds back experimental derivatives: whether an onchain trading venue can support complex, non-crypto underlyings while maintaining the user experience traders expect. By framing Hyperliquid’s asset diversification as a key driver, Pantera is effectively arguing that the perpetual model—paired with always-on trading—can serve as a general-purpose derivatives interface.

Onchain perps gain share, but central venues are watching closely

Pantera’s post also emphasized measurable traction in onchain perpetuals. The firm said DEX perpetual volumes rose to 14% of CEX perpetual volume, up from less than 1% in early 2023, when Hyperliquid first launched. It further claimed Hyperliquid accounts for roughly 40% of onchain perpetual trading volume.

To ground the growth narrative in revenue generation, Pantera cited fees performance: Hyperliquid, it said, generated $13.5 million in weekly fees in the past seven days, using DefiLlama data. While trading volume and fee totals are not the same metric, the combination is useful for readers because it suggests demand is not purely speculative—there is sustained activity sufficient to support protocol revenue.

Still, the numbers also highlight a transition phase. Even at 14% of CEX perpetual volume, the majority of perpetual activity remains centralized. Pantera’s figures therefore portray an emerging competitive set of venues rather than a complete replacement of traditional exchanges.

Traditional finance steps toward 24/7, and ICE calls for regulatory parity

Pantera’s thesis about perpetual futures has drawn parallels with moves already happening in traditional finance. The asset manager pointed to attention from ICE, where CEO Jeffrey Sprecher urged regulators to create a “level playing field” for launching 24/7 onchain perpetual futures contracts.

The underlying tension is straightforward: onchain derivatives aim to bring trading closer to continuous market mechanics, but regulatory frameworks and supervisory expectations may still treat onchain offerings differently than traditional venues. Pantera’s mention of ICE leadership implies that the competitive stakes are large enough that major incumbents are advocating for consistent rules rather than waiting for markets to converge naturally.

Momentum appears across multiple related announcements involving 24/7 trading ambitions. Cointelegraph previously reported that OKX announced plans to launch perpetual futures linked to ICE’s Brent crude and West Texas Intermediate benchmarks, citing a partnership with the exchange operator. Earlier coverage also noted the NYSE’s collaboration with tokenization platform Securitize to develop blockchain-based stock trading infrastructure with 24/7 trading and settlement for Wall Street, as well as ICE’s plans for a tokenized securities venue aimed at 24/7 trading and instant settlement, with stablecoin-based funding and onchain settlement.

Taken together, these developments show that the “always-on” market concept is no longer confined to crypto infrastructure. Instead, it is becoming a reference point for how TradFi platforms consider liquidity access, settlement speed, and funding workflows.

For readers, the next thing to watch is whether regulatory clarity accelerates the move from pilots to scaled onchain perpetual launches across more traditional asset classes. Pantera’s data suggests onchain perps are already carving out measurable share, but the pace of expansion beyond current players will likely depend on how the “level playing field” debate resolves and whether incumbents can align product rollouts with regulator expectations.

Spot Bitcoin and crypto ETFs have become the largest force in the market, absorbing and releasing billions of dollars of coins through a mechanism most of their own investors have never seen. This guide opens the machine: authorized participants, the creation and redemption loop, in-kind versus cash models, why a dollar of flow becomes a dollar of real buying or selling, how the arbitrage keeps ETF prices honest, and how to read the daily flow numbers everyone quotes.

Summary

- Spot crypto ETFs create and redeem shares through authorized participants, making ETF inflows and outflows translate into real buying and selling of cryptocurrencies.

- The creation and redemption process keeps ETF prices closely aligned with the value of the underlying coins through continuous arbitrage.

- Daily ETF flow data reflects actual spot market demand rather than investor sentiment alone, making it one of the market’s most closely watched indicators.

The most important trading desk in crypto does not trade on a crypto exchange. It sits inside a handful of Wall Street firms called authorized participants, and its job is to keep the price of spot crypto exchange-traded funds glued to the price of the coins they hold, by creating and destroying ETF shares in industrial quantities. When headlines report that Bitcoin funds bled $4.51 billion in a month, or took in $221.7 million in a day, they are reporting this machine’s output, and the machine’s mechanics, not sentiment, are why those flows translate directly into buying and selling of actual coins.

The spot ETF era has made these funds the marginal force in crypto’s market structure: they hold coins worth more than most national reserves, their daily flows are the most watched data series in the asset class, and their behavior in stress, as the recent record outflow month showed, can dominate price for quarters at a time. Yet the mechanism underneath, creation units, authorized participants, in-kind transfers, net asset value arbitrage, remains folk knowledge at best among the traders who quote its outputs daily.

This guide is the missing manual. It covers what a spot crypto ETF actually is and how it differs from the futures products and trusts that preceded it, the creation and redemption loop that is the entire engine, the in-kind versus cash distinction and why it matters for taxes and mechanics, the arbitrage that keeps the share price tracking the coins, why flows equal real spot demand and supply, what the daily flow numbers do and do not mean, and the honest list of what can go wrong.

What a spot ETF is, and what it replaced

A spot crypto ETF is a fund that holds the actual asset, real Bitcoin or Ether in institutional custody, and issues shares that trade on a stock exchange, each share representing a claim on a sliver of the coin pile. The design goal is simple to state and hard to engineer: make the share price track the coin price, continuously, within basis points, so that buying the ETF is economically equivalent to buying the coin, inside a brokerage account, with no wallets, keys, or crypto exchanges involved.

Everything distinctive about the structure exists to serve that tracking, and the point is sharpest against what came before. Futures-based ETFs held derivative contracts rather than coins and bled value to the cost of rolling those contracts month after month. Closed-end trusts held real coins but issued a fixed number of shares with no redemption mechanism, so their prices drifted to enormous premiums and discounts against their holdings, famously reaching double-digit discounts, because nothing forced the share price and the coin value together. The spot ETF’s innovation is precisely the forcing mechanism: an open-ended share supply that expands and contracts through arbitrage, executed by authorized participants. That mechanism is also, not incidentally, what separates an ETF from the treasury companies whose share prices float freely above and below their coin holdings: a treasury stock has no redemption loop, so its premium is a sentiment gauge; an ETF has one, so its premium is an arbitrage error measured in hundredths of a percent.

The engine: creation and redemption

The heart of every ETF is a wholesale market invisible to retail holders. ETF shares are not created when an investor clicks buy; they are created in bulk blocks called creation units, typically tens of thousands of shares at a time, by authorized participants, large trading firms and banks that hold agreements with the fund’s issuer.

The creation loop runs like this. When investor demand pushes the ETF’s market price even slightly above the value of the coins backing each share, its net asset value, an authorized participant sees free money: it buys the equivalent amount of actual coin on crypto markets, delivers it to the fund (or delivers cash the fund uses to buy the coin, a distinction the next section unpacks), receives newly minted ETF shares at NAV in exchange, and sells those shares into the stock market at the premium price. The AP pockets the spread; the share supply expands; the premium collapses back toward zero. Redemption is the mirror: when the ETF trades below NAV, an AP buys cheap shares on the stock market, returns them to the fund, receives coin (or cash from coin sales) worth full NAV, and sells the coin, pocketing the discount and shrinking the share supply until the price snaps back.

Read the loop again and notice what it implies, because it is the single most important fact in this guide: every net creation is real coin purchased on the market, and every net redemption is real coin sold. The flows are not sentiment surveys or paper reallocations; they are the visible exhaust of actual spot transactions, executed by the APs against crypto exchanges and OTC desks. A $500 million inflow day means roughly $500 million of coins were bought and moved into custody; a $4.51 billion outflow month means that much was sold out of it. This is why ETF flow data moves markets and why it deserves the obsessive attention it gets: it is the rare series that measures demand in the units that matter, coins actually changing hands, disclosed daily, to the dollar.

In-kind versus cash: the plumbing distinction

Creations and redemptions come in two flavors, and the difference, invisible to holders, shapes everything behind the scenes. In an in-kind model, the AP delivers and receives the actual asset: coins go in for shares, shares come back for coins, and the fund itself never trades. In a cash model, the AP delivers and receives dollars, and the fund’s own trading desk executes the coin purchases and sales. US spot crypto ETFs launched under a cash-creation regime, a regulatory choice that kept broker-dealers at arm’s length from handling coins, and the industry has since moved toward permitting in-kind, the structure ETFs use for every other asset class.

The distinction matters three ways. Mechanically, in-kind is cleaner: the fund holds coins and swaps them for shares, full stop, while cash models interpose a trading step where execution costs and timing slippage live. Tax-wise, in-kind is the quiet superpower of the ETF wrapper, letting funds shed appreciated assets through redemptions without realizing taxable gains, an efficiency cash models partially forfeit. And market-structure-wise, the cash model makes the fund itself a large, scheduled trader in the underlying market, whose execution patterns around creations and redemptions are studied, and sometimes anticipated, by everyone else. Either way, the coins end up in institutional custody, segregated wallets at qualified custodians, whose addresses on-chain observers track as a real-time audit of the funds’ holdings, one of the few places where traditional finance’s opacity meets crypto’s radical transparency and transparency wins.

The decade-long fight to exist

The mechanics above were nearly a decade in the courts and dockets before they were allowed to run, and the history explains several of the structure’s present quirks. The first spot Bitcoin ETF application was filed in 2013; the following ten years produced an unbroken record of rejections, with regulators citing manipulation risk in underlying crypto markets and the absence of surveillance agreements. The industry routed around the wall with inferior vehicles, the futures ETFs with their roll costs, the closed-end trusts with their wild premiums and discounts, and each inferior vehicle’s flaws became, ironically, evidence in the eventual case: the trust’s persistent discount showed concretely that investors were being harmed by the absence of a redemption mechanism, and a federal court’s 2023 ruling that rejecting spot products while approving futures ones was arbitrary broke the dam. The January 2024 approvals arrived as a batch, launching a dozen funds into simultaneous competition, which is why the market’s structure is a fee war among near-identical products rather than one dominant fund, and why issuer competition drove management fees to levels that undercut most of the world’s equity index funds within weeks of launch.

The cash-only creation requirement was the approvals’ regulatory fingerprint, imposed so that broker-dealers never touched coins directly, and its gradual relaxation toward in-kind is the quiet second act of the products’ regulatory story, unlocking the tax efficiency and mechanical cleanliness the wrapper was always meant to have. Ether funds followed Bitcoin’s, staking-enabled versions followed those, and the approval architecture built for two assets is now the template every other crypto asset’s ETF hopes, conditional on the classification framework Congress is deciding, to pass through. Ten years of rejection, in hindsight, built the most consequential piece of the structure: by the time the machine was switched on, the custody, benchmark, and surveillance infrastructure had been argued into institutional grade, which is a large part of why it has run through record inflows, record outflows, and a full market cycle without a single structural incident.

What holding the ETF actually costs

The wrapper’s convenience has a price list worth itemizing, because it is subtracted silently. The management fee, deducted daily from the fund’s assets, compounds into the tracking: a fund charging a quarter of a percent will lag its coin by exactly that much per year, before anything else. The NAV-timing gap adds a subtler cost for traders: the official NAV is struck once daily against an index snapshot, so orders executed at market prices far from the snapshot inherit tracking noise, trivial for holders, real for anyone trading the products tactically. Spreads and premiums cost basis points on entry and exit, tightest in the giant funds and wider in the small ones, and the arbitrage that minimizes them is weakest at the open and around crypto’s violent hours. And the structural exclusions, no staking yield in most products, no on-chain utility, no self-custody, are opportunity costs rather than fees, the value surrendered for the brokerage account’s convenience. Summed, the wrapper costs a diversified long-term holder a fraction of a percent annually against holding coins directly, which is, by the standards of what the access is worth to the capital that uses it, among the better bargains in finance, and knowing the itemization is what separates choosing the bargain from defaulting into it.

Why the tracking holds, and when it slips

The arbitrage loop keeps spot ETF prices within a whisker of NAV in normal conditions, but the whisker is worth understanding, because its width is a live diagnostic of market health.

The ETF trades during stock-market hours; the coins trade around the clock. Overnight and on weekends, the share price is frozen while the asset moves, so every open begins with a gap the APs arbitrage away in minutes, and the fund’s official NAV, struck once daily against a benchmark index of crypto exchange prices, is itself a snapshot of a moving target. Small premiums and discounts, hundredths to tenths of a percent, are therefore constant and meaningless. What matters is persistence: a discount that survives arbitrage signals that APs cannot or will not close it, because coin markets are too volatile to hedge, because borrowing shares is hard, or because redemption plumbing is stressed, and persistent dislocations in ETF land have historically been the smoke that precedes fire in the underlying market. The same logic runs through every wrapped-asset structure in finance, tokenized stocks keep their pegs by the identical mint-and-redeem loop, and the universal rule holds here: the wrapper is only as good as the arbitrage that binds it, and the arbitrage is only as good as the least reliable step in its loop.

One more participant deserves a paragraph: the basis trader. Because ETF shares can be held long against short futures positions, a meaningful fraction of ETF holdings at any time belongs not to investors who want crypto exposure but to arbitrageurs harvesting the spread between spot and futures prices. When that spread compresses, these holders redeem, mechanically, with no view on the asset, which means headline outflows always mix conviction selling with carry-trade unwinding in proportions no outside observer can fully separate. It is the single most important caveat when reading the flow numbers, and it cuts both ways: some of the most alarming outflow streaks in the products’ history were substantially plumbing, and some of the most celebrated inflow runs were substantially leverage.

A worked example ties the machinery together. Suppose strong demand lifts a Bitcoin ETF’s market price 0.2% above its NAV during a rally. An authorized participant simultaneously buys, say, $50 million of Bitcoin across exchanges and OTC desks and shorts the equivalent in ETF shares at the rich price, locking the 0.2% spread, about $100,000, minus costs. It delivers the coins (or cash) to the fund, receives creation units at NAV, and uses the new shares to close its short. Net result: the AP earned a riskless spread, the fund grew by $50 million of coins in custody, the day’s flow report shows a $50 million inflow, and the ETF’s premium collapsed back to a basis point or two. Reverse every step for a redemption into a discount. Multiply by every AP, every fund, and every trading day, and the aggregate is the flow series the market watches: not a survey, but the arithmetic residue of thousands of such loops, each one a real spot transaction with a paper trail. When the loops run large in one direction for weeks, as they did through June’s record redemptions, the ETF complex is not reflecting the market’s direction; at the margin, it is the market’s direction.

One design detail rounds out the picture: creation units keep the wholesale and retail layers honest simultaneously. Retail investors trade shares among themselves on the exchange all day without touching the fund at all, and only the net imbalance, the demand the secondary market cannot internally match, flows through the APs into creations or redemptions. The fund’s coin pile therefore moves only when the market’s aggregate position actually changes, which is why the flow series is such a clean demand signal: it nets out all the churn and reports only the residual conviction.

Reading the flows like a professional

The daily numbers reward a few disciplined habits. Read trends, not days: single sessions are noise, dominated by one fund’s creation calendar or one AP’s book, while multi-week runs, like the ten-day outflow streak that marked June’s low, are regime information. Distinguish flows from assets: net asset values fall when prices fall even while money flows in, and rise in rallies even during redemptions, so AUM headlines are mostly price echoes; the flow line is the demand signal. Watch the spread of participation: inflows concentrated in one fund are a product story, inflows across all issuers are an allocation story, and the custody balances that flows build are a structural supply force in their own right. Note the interaction with market hours: flows print against a US trading day, so they lag and compress around-the-clock crypto moves, and Monday’s number carries the weekend. And always carry the basis-trade caveat: the flow series measures shares created and destroyed perfectly, and measures investor belief only through that imperfect proxy.

Held together, the mechanics justify a conclusion stronger than the usual disclaimers: the spot ETF is the most consequential piece of market structure crypto has ever imported, precisely because its plumbing converts distant, regulated, advised capital into spot demand and supply with industrial efficiency and daily disclosure. It made the asset class legible to the largest pools of money on earth, and it made those pools’ behavior legible to everyone else, a two-way window that did not exist before 2024. The machine is neutral; June proved it pumps out as efficiently as it pumps in. Understanding the loop, APs, units, NAV, in-kind, basis, is what separates reading the window from being read through it.

One forward note completes the manual: the machine described here is still being extended. In-kind creation is arriving, staking-enabled funds have begun passing yield through the wrapper, options markets on the ETFs have layered a derivatives complex on top of the flow machine, and the same creation-redemption architecture is being fitted to additional assets as the regulatory perimeter settles. Each extension changes the reading of the flow data slightly, staking funds attract different holders than pure price trackers, options hedging generates mechanical creations and redemptions of its own, and the professional habit is to re-learn the machine’s output as its parts change. What does not change is the core: an arbitrage loop, run by profit-seeking intermediaries, converting the world’s brokerage demand into spot transactions, in public, every day. Crypto spent a decade fighting for that machine, and understanding it is the closest thing the asset class offers to reading its own pulse.

The reader’s bookmark list, finally, is short: each issuer’s daily holdings and flow disclosures, the aggregated flow dashboards the market quotes, the funds’ premium-discount trackers, and the custodian wallet monitors that let anyone verify the coins on-chain. Fifteen minutes a week across those four sources reproduces everything in this guide with live numbers, and turns the most quoted data series in crypto from a headline you consume into a machine you can actually read.

A last piece of perspective for scale: the creation-redemption machine described here is not a crypto invention but a thirty-year-old piece of market technology, refined across equity and bond ETFs holding trillions, and its arrival in crypto was less an experiment than a transplant of proven plumbing into a new asset. That pedigree is why it worked immediately at record scale, and it is also the quiet reassurance inside the daily drama of the flow numbers: whatever the coins do, the machine that wraps them has been stress-tested by every market crisis since the 1990s, and it has never been the thing that broke.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Structural details are current as of July 9, 2026, and may change. Always do your own research.

Frequently asked questions

How does a spot crypto ETF work in simple terms?

The fund holds real coins in institutional custody and issues shares that trade on a stock exchange, with each share representing a fraction of the coin pile. Large trading firms called authorized participants create new shares by delivering coins or cash to the fund, and destroy shares by redeeming them for coins or cash, an arbitrage loop that keeps the share price tracking the coin price within tiny margins.

What is an authorized participant?

An authorized participant, or AP, is a large financial firm with an agreement to create and redeem ETF shares in bulk blocks called creation units. APs arbitrage gaps between the ETF’s market price and the value of its holdings: buying coins and minting shares when the ETF trades rich, redeeming shares for coins when it trades cheap. Their profit motive is the mechanism that keeps the ETF honest.

Why do ETF flows move the crypto market?

Because flows are real spot transactions. A net inflow means authorized participants bought actual coins to create new shares; a net outflow means coins were sold to fund redemptions. Unlike sentiment indicators, the flow data measures coins genuinely changing hands, which is why sustained flow trends have become one of the most powerful forces in crypto price formation.

What is the difference between in-kind and cash creation?

In-kind creation swaps coins directly for shares, with the fund never trading; cash creation has the AP deliver dollars, which the fund’s own desk uses to buy coins. In-kind is mechanically cleaner and more tax-efficient, and it is the standard across ETFs generally; US spot crypto funds launched cash-only for regulatory reasons, with the industry since moving toward in-kind.

Can a spot ETF trade at a premium or discount?

Briefly and slightly, yes, especially at market opens after the coins moved overnight, but arbitrage closes gaps within minutes in normal conditions. Persistent premiums or discounts are rare and diagnostic: they signal that the creation-redemption loop is stressed, which historically has been a warning sign worth taking seriously. This tight tracking is the key difference from closed-end trusts and treasury stocks, which can drift far from their holdings’ value.

Do ETF outflows always mean investors are bearish?

No. A significant share of ETF positions belongs to basis traders holding shares against short futures to harvest the spread, and when that spread compresses, they redeem mechanically with no market view. Headline outflows therefore mix genuine de-risking with carry-trade plumbing, which is why flow trends matter more than single prints and why context from funding and futures data helps.

Where are the ETF’s coins actually kept?

With qualified institutional custodians, in segregated cold-storage wallets whose addresses on-chain analysts track publicly. The holdings are disclosed daily by the funds and independently observable on the blockchain, making spot crypto ETFs among the most transparent pooled investment vehicles in existence.

Is buying the ETF the same as buying the coin?

Economically it is very close: the tracking is tight and the convenience is real. The differences are structural: ETF investors hold shares, not coins, cannot self-custody or use the assets on-chain, trade only during market hours, pay an annual management fee, and rely on the fund’s custody arrangements. For brokerage-account exposure those trade-offs are usually acceptable; for crypto-native uses they are disqualifying.

Decentralized finance (DeFi) tokens have held up unusually well against Bitcoin over the past month, suggesting the market may be “quietly re-rating” the sector, says crypto index fund maker Bitwise.

Bitcoin (BTC) fell about 22% in June, while Bitwise’s index tracking tokens from major DeFi protocols fell only 4% over the same period, Bitwise said in a report Thursday.

“DeFi usually swings much harder than Bitcoin, so holding up this well is unusual, and almost no one is talking about it,” it said.

DeFi tokens have a reputation for being highly volatile during crypto market swings, as they’re the first to be sold by risk-averse traders. However, Bitwise said this is changing as traditional institutions have begun to use the protocols, which have stabilized the wider DeFi ecosystem.

“We think DeFi is quietly re-rating,” Bitwise said. “Token economics are improving, the gap between usage and token value is closing, and real institutions are building on names like Morpho and Jupiter, with Aave alone generating ~$900 million in the past year.”

“We expect DeFi’s outperformance to keep playing out in Q3, the kind of shift the market tends to notice late,” it added.

Source: Bitwise

Bitwise’s DeFi index fund weighs assets by market capitalization, and its current holdings are weighted 61% toward Hyperliquid (HYPE), the native token used by the crypto perpetuals exchange of the same name that has gained more than 160% so far this year.

The index also holds Uniswap (UNI), Ondo (ONDO) and Aave (AAVE), among others, all of which have fallen by double-digit percentages year to date.

DeFi value locked drops over 2026

While HYPE has propped up the value of DeFi tokens, total value locked in DeFi has fallen nearly 40% so far this year through June, declining to just over $70 billion from roughly $115 billion in January, CryptoRank reported June 24.

The crypto data aggregator attributed the market decline to the major correction in early October, which came after the crypto market peak, when Bitcoin hit a high of more than $126,000.

However, the company said the current drawdown remains smaller than during the 2022 bear market, suggesting a more resilient DeFi market.

Bitwise says expect stablecoins, volatility if CLARITY fails

In its report, Bitwise also noted key upcoming events it expects will affect the crypto market.

It said it expects “a steady run of large firms to announce stablecoin projects” ahead of the GENIUS Act, a stablecoin-regulating bill the US made law last year that takes effect in January 2027.

Related: EU lawmakers urge assessing DeFi, staking, NFT regulation

Stablecoin supply has held amid the crypto market downturn, it added, and their growth will positively affect blockchains such as Ethereum and Solana this quarter as regulators finalize their rules for the GENIUS Act.

Bitwise said it also expects the next three months will be “make-or-break for the CLARITY Act,” the crypto market structure bill currently under review and negotiation in the Senate that Bitwise said has an unlikely chance of passing before the November elections.

“If it passes, we believe it likely marks this bear market’s bottom,” Bitwise said. “If it fails, expect volatility initially, then a clearing of uncertainty as the industry keeps building under a pro-crypto SEC and CFTC.”

Features: DeFi hacks shake institutional confidence as risks outpace yields

Shiba Inu saw its largest burn in the last six months, which is typically interpreted as a bullish signal.

However, SHIB’s price remains heavily suppressed in the bear market, and multiple factors point to further downside in the short term.

The Burn and More

On July 8, the SHIB team and community scorched almost 110 million coins. However, the USD equivalent of the coins sent to a dead wallet is negligible, and with roughly 585 trillion coins still in circulation, much bigger burns will be required to trigger a major upswing.

The burning mechanism was introduced in 2022, and its ultimate goal is to make the token scarcer and potentially more valuable (should demand remain stable or head north). It is also important to note that Vitaliк Buterin contributed a significant portion of the approximately 410.8 trillion tokens that have already been burned.

As of this writing, SHIB trades at around $0.00000429, an 8% decline for the past month and a whopping 95% collapse since the all-time high witnessed in 2021. Its market capitalization has dropped to around $2.5 billion, making the meme coin (once among the 20 biggest cryptocurrencies) the 37th-largest digital asset.

Back in the day, Shiba Inu was the subject of numerous optimistic price predictions, but lately the interest in it has faded, and the forecasts are rather grim. Not long ago, the popular trader James Wynn labeled the meme coin “old, dead, and boring,” predicting a potential revival in 5-10 years, when “a bit of nostalgia” could bring it back.

The Bearish Signals

SHIB’s downfall coincides with its falling daily trading volume. X account BSCN revealed that the figure has seen a steady decrease over the last 12 months, plummeting from $637 million in July 2025 to around $50-$100 million nowadays.

The stalled activity on Shibarium is another worrying sign. The layer-2 scaling solution, launched in the summer of 2023 to boost speed, enhance scalability, and lower fees, initially processed millions of transactions. However, following an exploit that disrupted operations last year, daily activity has fallen dramatically to mere thousands.

Weak interest in the broader meme coin sector is another factor that could limit SHIB’s ability to stage a decisive comeback. Dogecoin (DOGE) and many of its rivals were among the best-performing tokens during the last bull cycle, but they are now a pale shadow of their former glory. The market capitalization of the meme coin sector, which once crossed $120 billion, now stands at less than $23 billion.

The post Shiba Inu Burn Rate Goes Parabolic, Yet SHIB Keeps Bleeding: Details appeared first on CryptoPotato.

ZK STARKs are the best way to deal with the issues created with making Bitcoin quantum-safe — and to reach mass adoption at the same time — says StarkWare co-founder Eli Ben-Sasson.

What’s more, he claims Blockstream founder Adam Back agrees.

Ben-Sasson has been in the news this week for his controversial suggestion on X to increase Bitcoin inflation to 4% annually. Grok’s analysis of the replies found “zero clear support for the proposal.”

But as the co-inventor of STARKs — quantum-secure, hash-based zero-knowledge proofs — he’s on much firmer ground, with some leading Bitcoin researchers supporting the concept.

Ben-Sasson’s own project Starknet last week announced its own three phase project to become quantum secure.

The problem of large PQ signatures on Bitcoin

Adding zero-knowledge proofs to Bitcoin does not make the blockchain quantum secure by itself. ZK proofs are a way to deal with the problems caused by adding much larger post-quantum (PQ) signature schemes to Bitcoin.

The current crop of PQ signatures approved by the National Institute of Standards and Technology (NIST) is 10 to 100 times larger than Bitcoin’s existing ECDSA and Schnorr signature schemes.

Some argue this could slow the blockchain to fewer than 1 transaction per second. But all of the large transaction signatures for a block could be compressed into a tiny ZK STARK proof. Because the proof would be much smaller than even including the existing signatures, the blockchain may end up running faster.

“If they don’t allow for ZK STARK aggregation, then definitely it will be a very unfortunate move because it won’t really solve the problem … where the problem is ‘can everyone actually use Bitcoin?’” Ben-Sasson said.

“So for that you need massive scale. And for that, you need things like signature aggregation and just increasing the block size isn’t enough.”

Related: StarkWare CEO suggests 4% annual Bitcoin inflation to replace 21M cap

The quantum alternative: Increase Bitcoin’s block size

Marin Ivezic, author of PostQuantum.com and founder of Applied Quantum, told Cointelegraph that Bitcoin’s SegWit scheme reduced the impact of large signatures by up to 75%. But his modeling of NIST’s ML-DSA-44 scheme, which has 2,420 bytes per signature, “puts block capacity at roughly 500 to 700 transactions, down from 2,500 to 3,000 today. That is where the block-size debate comes in.”

Increasing Bitcoin’s block size is a genuine alternative, but the community split over a proposal to double the block size back in 2017. Many of the arguments against remain relevant, as it’s a blunt fix that requires every node to carry, store and verify much more data. That’s more expensive and requires more equipment, which critics argue pushes the network toward centralization.

Blockstream Research has been experimenting in recent months with compressing the size of hash-based post-quantum signature schemes for use with Bitcoin. It has come up with the promising SHRINCS and SHRIMPS schemes, which have everyday signatures around five times larger than Bitcoin’s current ones, but up to 40 times larger if you lose your wallet and need to resurrect it.

While SHRINCS has been used to sign real transactions on the Liquid sidechain, its development is at an early stage and there are drawbacks in terms of complexity and usability. The much larger signatures would also slow the blockchain down, unless the block size was increased.

“Raising capacity natively is the simple engineering answer and the hardest governance answer,” said Marin Ivezic, author of PostQuantum.com and founder of Applied Quantum, about a block size increase. “We just don’t have time for those debates.”

ZK proof aggregation has advantages

ncrease, but it would arguably be much better at preserving decentralization while also making Bitcoin more efficient.

At their simplest, ZK proofs are a way to mathematically prove that something exists without needing to include all the details. For example, a ZK proof could demonstrate that you know the combination to a safe, without telling the other person what the combination is.

Generating a ZK proof for a single block technically only needs to be done once (although it’s safer to generate additional backups for redundancy), and the equipment required to do so looks like it would be much less expensive than a commercial mining setup.

Lean Ethereum’s specs are for proving equipment that costs under $100,000 (and can be run from an ordinary home). Verifying a ZK proof, meanwhile, can be done on almost any equipment, including a Raspberry Pi.

Ben-Sasson said that early Bitcoin devs like Greg Maxwell and Mike Hearn were “very bullish about ZK STARKs, which are post-quantum secure and have no trusted setup,” and that he believes Bitcoin Core developer Luke Dashjr and Blockstream founder Adam Back are coming around to the idea.

“I heard this myself from them. They are bullish on things related to and using ZK STARKs. I think each of them has spoken well, definitely privately but also publicly, in favor. Adam Back and Luke Dashjr don’t exactly see everything eye to eye, but on this I think they actually agree that it’s a great technology that, under the right terms, could find its way to Bitcoin.”

Cointelegraph contacted Back for comment, but did not receive a response.

Ethereum researcher Justin Drake has spoken publicly about his desire for Bitcoin to adopt Lean Ethereum’s ZK proof aggregation technology so that it becomes standard across the industry. This may be unfeasible for political reasons.

Ethereum aims to be post quantum by 2029. Source: Ethereum Foundation

Bitcoin specific ZK proposals

Given Bitcoin’s conservative culture, the most politically pragmatic way to add ZK to Bitcoin would likely be to re-enable OP_CAT, which is nine lines of code written by Satoshi.

“[He] even introduced and then he removed it,” said Ben-Sasson said. “And if you add that, you can get things like STARK proofs and then aggregation and post-quantum security.”

“I think it’s the best and safest solution that will really, really just jump-start again this journey that Satoshi really started and wanted.”

But despite a flurry of interest in OP_CAT about 12 to 24 months ago, it seems to have lost momentum more recently (although Bitcoin governance moves in mysterious ways).

There are also more speculative proposals, including OP_STARK_VERIFY, that would add opcodes specifically designed to more efficiently verify STARKs on Bitcoin. And BIP-360 co-author Ethan Heilman proposed aggregating Bitcoin’s signatures and public keys into a single STARK proof under the name BitZip.

Heilman told Cointelegraph earlier this year there are two main ways to achieve the desired result:

“Either add a bunch of general purpose opcodes to Bitcoin and then build something like a ZKRollup in Bitcoin or support STARKs at the consensus layer of Bitcoin. Alternatively, other less powerful aggregation schemes, such as CISA [Cross Input Signature Aggregation] might help here as well.”

What are the chances though?

Ivezic says Bitcoin governance, rather than technological capability, is the sticking point.

“Eli’s cryptography is rock solid: pure hash assumptions, no trusted setup, thousands of signatures compressed into one small proof. The problem is everything around the cryptography,” he says.

“Bitcoin Script cannot verify a STARK today, and a production verifier is a massive consensus surface compared with a narrow hash-signature opcode. Given that a tiny opcode like OP_CAT has spent years in debate, a base-layer STARK verifier is realistically a 2030s conversation.”

Meanwhile, Ethereum is targeting 2029 for its transition to post-quantum, and Solana has also been experimenting with adding post-quantum signatures. StarkNet’s three-phase transition will benefit from account abstraction, which enables the underlying cryptography to be upgraded without making every user manually transfer to new accounts.

As a result, Ben-Sasson said that Solana and Ethereum’s post-quantum roadmap will be “extremely hard.”

“On Starknet, we have this big advantage that we have already native account abstraction and smart wallets, which means that nothing is enshrined so its very easy to upgrade the wallets and the infrastructure to be post quantum.“

Features: The biggest blockchain upgrades still to come in 2026

Meta launched Muse Spark 1.1 on July 9. The company priced its first paid AI model far below Anthropic’s Claude and OpenAI’s ChatGPT. The move puts Meta squarely in the coding and agentic AI market, which both rivals currently dominate.

The launch marks a sharp shift from Meta’s open-source Llama strategy. AI chief Alexandr Wang said Meta built the pricing to compete directly with the two market leaders.

Muse Spark’s Aggressive Pricing Play

Meta priced the new model at $1.25 per million input tokens and $4.25 per million output tokens. New accounts get $20 in free credits before billing starts.

Muse Spark 1.1 undercuts all major AI rivals on price. Its $1.25 input rate runs 37% below Sonnet 5’s introductory $2 and 75% below Opus 4.8 and GPT-5.5, which both charge $5.

The output side shows an even wider gap. Meta’s $4.25 rate sits 58% below Sonnet 5’s introductory $10, 83% below Opus 4.8’s $25, and 86% below GPT-5.5’s $30.

That pricing gap could matter most for heavy, high-volume workloads. A developer running the same task across all four models would pay Meta’s rate for less than a third of what GPT-5.5 charges on output alone. The gap also lands amid the broader OpenAI price war with Anthropic.

The gap narrows once Sonnet 5’s introductory pricing expires on August 31, though Meta still comes out cheaper on both ends even against the standard $3/$15 rate.

“Very aggressive and attractive.”

Alexandr Wang, Meta AI chief, to CNBC

Meta detailed the specifics in Meta’s paid API pivot. It marks the company’s first ever charge for AI model access after years of free Llama releases.

Can Muse Spark Overthrow Claude and ChatGPT?

Muse Spark 1.1 reportedly rivals GPT-5.5 and Claude Opus 4.8 on agentic benchmarks, per posts from developers tracking the launch. Meta has not published independent scores against either rival.

Access remains limited. The public preview covers only US developers, requires a waitlist, and stays off third party marketplaces like OpenRouter.

Cheaper access could pull developers toward Meta’s model over time. Whether Muse Spark can match Claude and ChatGPT on real world coding tasks remains unproven.

The post What Is Meta’s AI Muse Spark and Can It Overthrow Claude and ChatGPT? appeared first on BeInCrypto.

Every token launched on Pump.fun, every fair-launch memecoin, and a surprising share of DeFi’s core machinery runs on the same idea: a mathematical formula that sets a token’s price from its supply, with a smart contract as the only market maker. This guide explains how bonding curves actually work, the worked math of buying up a curve, the graduation model that industrialized token launches, the sniper and bundler attacks that exploit it, and where the elegant idea breaks.

Summary

- Bonding curves use a mathematical formula to set token prices based on supply, allowing tokens to launch without order books or external market makers.

- Platforms such as Pump.fun use bonding curves to bootstrap liquidity before moving successful tokens into automated market maker pools through a graduation process.

- While bonding curves make token launches transparent and permissionless, they remain vulnerable to sniper bots, bundled buys and liquidity limitations during exits.

Somewhere in the time it takes to read this paragraph, a new token will be created on a bonding curve. It will have no order book, no market maker, no seeded liquidity, and no listing process, and it will nevertheless be instantly tradable, with a live price, from its first second of existence. The mechanism making that possible is a bonding curve: a mathematical function, enforced by a smart contract, that maps the token’s supply to its price, so that every purchase mints tokens and pushes the price up the curve, and every sale burns tokens and slides it back down.

Bonding curves are among the oldest ideas in decentralized finance, sketched by Simon de la Rouviere in 2017 and formalized in Bancor’s early work, and for years they lived in the ecosystem’s academic corners, pricing continuous tokens and DAO shares. Then the memecoin era found them. Pump.fun built its entire launch machine on a bonding curve, over a million tokens have entered the world through it, and the curve became the defining market structure of an entire trading culture, the trenches, where fortunes are made and lost inside a formula most participants have never read.

This guide reads the formula. It covers what a bonding curve is and how the mint-and-burn mechanism works, the worked arithmetic of buying up a curve, the main curve shapes and what each one incentivizes, the launchpad graduation model that turned curves into an industrial process, the attack playbook, snipers, bundlers, and the exit-liquidity geometry, that exploits them, how bonding curves relate to the automated market makers that power DeFi’s exchanges, and the honest assessment of what the mechanism fixes and what it merely relocates.

The core mechanism: price as a function of supply

A bonding curve is, at bottom, one equation: price equals some function of supply, P = f(S). The smart contract implementing it holds a reserve of a base asset, SOL on Pump.fun, ETH or a stablecoin elsewhere, and stands ready, permanently and automatically, to be the counterparty to anyone.

Buying works like this: a user sends the reserve asset to the contract; the contract consults the curve, calculates how many new tokens that payment purchases given the current supply, mints them, and delivers them; the supply is now higher, so the curve dictates a higher price for the next buyer. Selling reverses it: the user returns tokens, the contract burns them and pays out reserve assets at the curve’s current rate, and the price steps down. Nobody quotes prices, nobody provides liquidity, and nobody can refuse the trade; the contract is issuer, exchange, and market maker fused into one piece of code, a vending machine whose price tag adjusts after every sale.

Two properties follow immediately, and they explain the mechanism’s appeal. The first is guaranteed liquidity: because the contract always stands on the other side, a curve-launched token can never be unsellable in the way an order-book token with no bids can; there is always an exit price, however low. The second is deterministic pricing: the formula is public and fixed, so the price impact of any trade can be computed exactly in advance, slippage as a published schedule rather than a surprise. Together they solve the cold-start problem that killed a decade of token launches: how to make a brand-new asset tradable before any market exists for it. The curve is the market, from block one.

The worked math: buying up the curve

Numbers make the mechanism honest, so walk one simple example. Suppose a token launches on a linear curve where the price starts at $0.001 and rises by $0.001 for every 100,000 tokens minted. The first buyer spends $100: at prices between $0.001 and roughly $0.0011, they receive a bit over 95,000 tokens, an average price near $0.00105, already above the starting tick because their own purchase moved the curve. A second buyer now spends $1,000 into the higher range and receives proportionally fewer tokens per dollar, perhaps 600,000 tokens at an average near $0.0016. A third spends $10,000 and pushes the price past $0.006.

Notice what the arithmetic did. The first buyer’s 95,000 tokens, bought for $100, are now worth nearly $600 at the marginal price, an unrealized 6x for simply being early, and that is the entire psychological engine of curve trading: the formula converts earliness itself into profit, mechanically, visibly, in real time. Notice also what it did not do: create any external demand. The third buyer’s $10,000 is what values the first buyer’s position, and if the third buyer sells back into the curve, the price retraces down the same path it climbed. A bonding curve is a perfectly transparent game of musical chairs in which the music, the chair count, and everyone’s seat are published on-chain, and it is precisely this transparency that its defenders cite as the fairness: unlike a rigged order book or an insider allocation, the curve cheats no one, because everyone can read exactly what they are stepping into.

The curve’s shape sets the game’s temperature. Linear curves rise gently and reward early buyers modestly; exponential curves, where each purchase raises the price by a percentage rather than an increment, produce the vertical charts and 100x-in-an-hour outcomes that memecoin culture selects for; logarithmic and flattening curves front-load the appreciation then stabilize, a design used when a project wants early supporters rewarded but later prices calm. Bancor-style designs parameterize this with a reserve ratio, the fraction of the token’s market value held as reserve collateral, where lower ratios mean steeper, more explosive, more fragile curves. Every launchpad’s choice of shape is a statement about what behavior it wants, and the memecoin era’s revealed preference has been unambiguous: steep.

Graduation: the model that industrialized launches

The design that conquered the market, Pump.fun’s, added one crucial idea to the classic curve: an ending. Tokens on the platform begin life on a bonding curve, and when buying pushes the market value to a threshold, historically in the $60,000-70,000 range, the token graduates: the curve phase closes, and the accumulated reserve is deposited, together with tokens, into a conventional automated-market-maker pool on the platform’s own venue, where the token trades like any other from then on.

Graduation solved the curve’s deepest historical problem, which is that a pure bonding curve is a closed economy: its price can only reflect flows into and out of itself, it cannot arbitrage against external markets, and its reserve is a honeypot whose smart-contract risk grows with size. By using the curve only as a launch chamber, a price-discovery and liquidity-bootstrapping phase, and then handing the survivors to a normal market, the graduation model captured the curve’s cold-start magic while shedding its long-term liabilities. It also created, deliberately, a tournament structure: the overwhelming majority of launched tokens never graduate, dying quietly on their curves, while the few that cross the threshold receive instant liquidity, visibility, and the implicit endorsement of survival. The platform collects fees at every stage, an economics this publication examined through its own token’s stress test, and the tournament runs continuously, thousands of times a day, the purest expression of permissionless market Darwinism crypto has produced.

It is worth being precise about what fair launch means in this structure, because the term does heavy marketing work. The curve guarantees procedural fairness: no presale, no allocation, identical rules for every participant, and a price schedule known in advance. It does not and cannot guarantee distributive fairness, because identical rules reward unequal speed, information, and capital, which is where the attack playbook begins.

Where curves came from, and where they went

The bonding curve’s biography explains its present better than any specification. The idea emerged from 2017-era token engineering, de la Rouviere’s continuous organizations, Bancor’s reserve-ratio formalism, as an answer to a governance-age question: how should communities issue and price membership continuously, without discrete sales? The early implementations were earnest and mostly ignored, curation markets, DAO shares, continuous funding for public goods, sophisticated designs waiting for a use case that never arrived at scale. The idea survived the 2018 winter in academic corners and resurfaced wherever cold-start liquidity was the binding problem: SocialFi’s creator keys priced follower access on steep exponential curves during the Friend.tech moment, NFT projects experimented with curve-priced mints, and stablecoin architectures quietly used flattened curves to hold pegs between correlated assets.

Then Solana’s memecoin culture supplied the use case the theorists never imagined: not funding organizations, but manufacturing lottery tickets at industrial scale. Pump.fun’s January 2024 launch stripped the concept to its essentials, one standard steep curve, one graduation rule, one-click creation, and the result processed more token launches in its first two years than the rest of crypto’s history combined. The pattern spread instantly: every major chain grew launchpad clones, incumbent platforms bolted on curve launches, and the bonding curve, born as a tool for patient community capital, became the engine of the fastest, most disposable market ever built. There is a genuine irony in the arc, and also a lesson about mechanisms: the curve did not choose its culture. It priced earliness deterministically, and the market that valued earliness most, the memecoin trenches, adopted it hardest. Mechanisms are amplifiers of the demand they meet, and the curve’s history is the cleanest proof in crypto’s archive.

The creator’s side of the modern launchpad economy deserves its own accounting, because the curve reshaped it too. Launching a token once required capital: liquidity to seed, market makers to hire, listings to buy. The curve reduced the cost to a transaction fee, which transformed token creation from an investment into a lottery ticket, and creators responded rationally by buying thousands of tickets: serial launches, A-B testing of tickers and memes, portfolios of hundreds of attempts awaiting one graduation. Platform fee-sharing programs, paying creators a slice of their token’s trading fees, industrialized the incentive further, producing a professional class of launchers whose economics resemble content creation more than entrepreneurship: volume, iteration, and the occasional viral hit subsidizing the long tail of duds. Whether that economy is a democratization of finance or a spam machine with a fee switch is the debate that follows the launchpads everywhere, and the honest answer is that the curve, as always, executes whichever game arrives.

The attack playbook: snipers, bundlers, and exit geometry

Every property that makes curves fair in principle is exploitable in practice, and the exploits are now industries.

The first is sniping. Because the earliest positions on a steep curve capture the largest mechanical gains, bots monitor token-creation transactions and buy within the same block a token launches, frequently faster than the creator’s own community can. The playing field is level in exactly the way a footrace against professional sprinters is level, and the same latency-and-priority infrastructure that powers all on-chain extraction dominates curve entry.

The second is bundling: a launcher, or an attacker, splits a large early buy across dozens of wallets in the launch block, manufacturing the appearance of broad organic demand while concentrating the curve’s cheapest supply in one pair of hands. Bundled launches are the modern rug’s preferred anatomy: the bundler rides the crowd up the curve and exits into it, and because the curve guarantees liquidity, the exit always executes; the guarantee that no holder can be trapped is equally the guarantee that no dumper can be refused. Detection tools now score launches for bundling patterns, and the arms race between bundlers and detectors is a permanent feature of the trenches.

The third is the exit geometry itself, subtler and universal. On any curve, the reserve held by the contract equals the area under the curve up to the current supply, which is always less than the current supply times the current price, the market cap. On steep curves the gap is enormous: a token can show a $60,000 market value while its curve holds a fraction of that in actual reserve, meaning that if every holder tried to exit, the average exit price would sit far below the last trade. The curve never lies about this, the math is public, but the market-cap number is what trades on screens and in heads, and the difference between marked value and extractable value is where most curve-trading losses actually live. It is the same lesson every thin market teaches,the gap between the last price and the liquidation reality, rendered in its mathematically purest form.

One number from the tournament’s own accounting calibrates the odds honestly. Across the launchpad era, graduation rates, the fraction of launched tokens that ever cross the threshold into a real market, have run in the low single digits, and the fraction that sustains any liquidity a month later is a fraction of that fraction. The curve’s defenders and critics both own this statistic: defenders because it proves the tournament filters ruthlessly at near-zero cost per attempt, an efficiency no venture process approaches, and critics because it quantifies the base rate every buyer of a fresh launch is fighting. Neither reading changes the practical arithmetic for a participant: the expected value of a random curve entry is set by that base rate times the payoff distribution, both of which are public, and the traders who survive the trenches are, almost by definition, the ones who stopped treating the odds as someone else’s problem. The curve publishes everything. The tournament’s mortality table is part of everything.

Curves and AMMs: the same family, different jobs

A final clarification earns its place because the terms blur constantly: bonding curves and automated market makers are siblings, not synonyms. An AMM like Uniswap uses a curve, the constant-product formula x*y = k, to price swaps between two tokens that already exist, with liquidity supplied by outside providers who bear the divergence costs of that role. A bonding curve in the issuance sense uses its formula to govern the minting and burning of a token against a reserve, with the contract itself as issuer and sole liquidity source. The mathematics rhyme; the jobs differ: AMM curves make secondary markets, issuance curves make primary ones, and the graduation model is precisely a pipeline from the second to the first. Knowing which kind of curve a token sits on is the first diligence question in this corner of the market, because it determines who holds the reserve, who can change the rules, and what the sell-side guarantee actually is.

One boundary condition also deserves a sentence: curves are single-market objects, and their guarantees end at the contract’s edge. The moment a token graduates, or trades simultaneously on external venues, its price becomes an arbitrage between markets, the curve’s determinism dissolves into ordinary microstructure, and the trader’s toolkit reverts to the standard one of depth, spreads, and flows. The curve is training wheels with perfect physics; the road afterward is the road.

The honest assessment

Bonding curves deserve both their reputation and their notoriety, and an honest summary holds both. What they genuinely fixed is real: the cold-start problem is solved, launch gatekeeping is gone, insider allocations are structurally impossible on a pure curve, and pricing is the most transparent in all of finance, a formula anyone can read. What they merely relocated is equally real: the advantage moved from insiders with allocations to insiders with infrastructure, the risk moved from being unable to sell to being mathematically last, and the fairness became procedural while the outcomes stayed as skewed as ever, because the curve prices earliness and earliness is not evenly distributed. The mechanism is a mirror: it executes exactly the game its participants bring to it, faster and more honestly than any structure before it. For a user, the practical wisdom compresses to three habits: read the curve’s shape before buying, because it is the payout table; check the launch block for bundling, because the table may be seated; and never confuse the marked price with the exit price, because the area under the curve, not the last tick, is what everyone is actually fighting over.

A closing thought on where the mechanism goes next, because the design space is not finished. Dynamic curves that adjust steepness to demand, anti-sniping randomization of launch blocks, creator-fee structures that reward holding over flipping, and curve designs that route a share of the ride into locked liquidity or holder distributions are all live experiments across the launchpad ecosystem, each an attempt to keep the cold-start magic while sanding down the extraction. The direction of travel is legible: first-generation curves optimized for launch velocity, and the survivors of the current era are optimizing, under competitive and community pressure, for what happens after the launch, retention, distribution, durability, the boring variables that decide whether a mechanism that can create a million tokens can ever create a lasting one. The formula will keep evolving. The lesson it has already taught is permanent: in permissionless markets, the launch mechanism is the market structure, and reading it is not optional homework but the trade itself.

And for readers who arrived here from a chart rather than a curiosity, the fifteen-second version: find the token’s curve page, note its shape and its distance from graduation, check the launch block for clustered wallets, compare the contract’s reserve to the displayed market value, and size the position as a ticket in a tournament whose mortality table you have now read. The formula will do exactly what it says. Everything else is the crowd.

The bonding curve, in the end, belongs to a small class of crypto inventions, alongside the flash loan and the automated market maker, that could not have existed in prior financial systems: it requires a machine that can hold reserves, enforce a formula, and stand as a tireless counterparty, all without an operator, and it converts the oldest problem in market design, who makes the first market, into a line of arithmetic. That the memecoin era found it first says something about crypto’s culture; that it works, flawlessly and continuously, across millions of launches says something about the technology, and both statements will outlive whatever the trenches are trading this month.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Memecoin and DeFi markets are extremely volatile and you can lose your entire investment. Details are current as of July 9, 2026. Always do your own research.

Frequently asked questions

What is a bonding curve in simple terms?

A bonding curve is a formula, enforced by a smart contract, that sets a token’s price based on how many tokens exist. Buying mints new tokens and pushes the price up the curve; selling burns tokens and moves it down. The contract holds a reserve of a base asset and acts as the permanent counterparty, so the token is tradable from the instant it is created, with no order book or market maker.

How does a bonding curve launch work on platforms like Pump.fun?

A creator launches a token onto the platform’s standard curve for a tiny fee. Buyers purchase directly from the curve, moving the price up as supply grows. If demand pushes the token’s value to the graduation threshold, the accumulated reserve and tokens are moved into a normal trading pool and the token trades conventionally from then on. Most tokens never graduate and simply fade on their curves.

Why does the price rise when people buy?

Because the formula ties price directly to supply. Each purchase mints tokens, raising supply, and the curve assigns a higher price to every subsequent token. The steeper the curve’s shape, the faster the price accelerates, which is why memecoin launches can multiply in minutes on relatively small inflows.

Can a bonding curve token become unsellable?

Not in the order-book sense: the contract always buys tokens back at the curve’s current rate, funded by its reserve, so an exit price always exists. The real risk is that the exit price after others sell is far below what you paid, and that the total reserve is always less than the token’s headline market value, so not everyone can exit near the last traded price.

What is a fair launch, and are bonding curves actually fair?

A fair launch means no presale, no team allocation, and identical rules for all buyers from block one, which pure bonding curves deliver procedurally. In practice, speed and infrastructure decide who gets the cheapest supply: sniper bots buy in the launch block and bundlers split large buys across many wallets to disguise concentration. The rules are equal; the race is not.

What is the difference between a bonding curve and an AMM like Uniswap?

Both use formulas to set prices, but an AMM curve governs swaps between two tokens that already exist, using liquidity deposited by outside providers, while an issuance bonding curve governs the minting and burning of a token against a reserve held by the contract itself. Launch curves create primary markets; AMMs run secondary ones.

What are the main risks of buying on a bonding curve?

Being late on a steep curve, where the mechanical advantage belongs entirely to earlier buyers; bundled launches, where one actor secretly holds the cheap supply and exits into the crowd; smart-contract flaws in the curve itself; and the reserve gap, since the contract’s reserve is always smaller than the token’s marked value. The formula is transparent, so most losses come from not reading it.

Are bonding curves used for anything besides memecoins?

Yes. They price continuous tokens and DAO shares, bootstrap liquidity for new projects, structure token sales that replace ICOs, and underpin stablecoin and pegged-asset designs using flattened curves. The memecoin launchpad is the most visible application, but the mechanism is general-purpose market infrastructure.

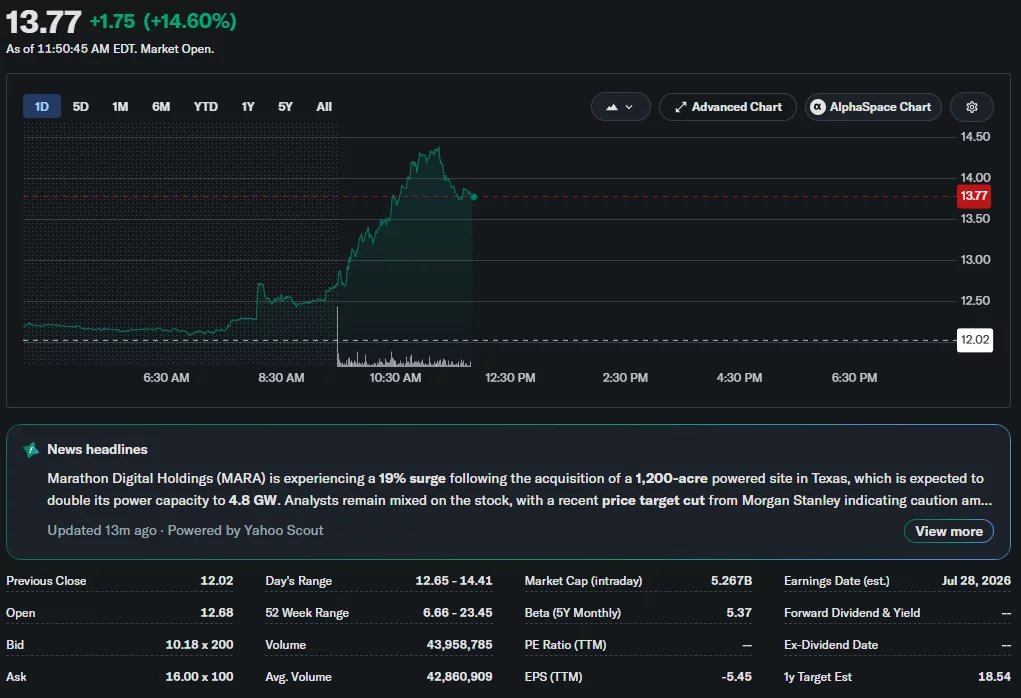

MARA Holdings has expanded its AI and digital infrastructure footprint by acquiring a 1,200-acre powered land site in Texas, helping lift its shares more than 12% as the Bitcoin miner continues to outperform many publicly traded crypto companies.

Summary

- MARA has acquired a 1,200-acre powered site in Texas with up to 2 GW of planned grid capacity.

- The company plans to build an AI and high-performance computing campus alongside Bitcoin mining operations.

- MARA shares jumped more than 12% after the announcement, extending gains to over 45% this year.

According to a company press release, MARA has signed a definitive agreement to acquire the Texas property from HIF. The site is expected to provide access to an initial 1 gigawatt of grid capacity by October 2027, with total available capacity projected to reach 2 gigawatts by April 2028.

The company said the location is designed to support large-scale digital infrastructure alongside its existing Bitcoin mining operations.

The announcement extends MARA’s investment in artificial intelligence infrastructure, an area that has attracted increasing attention from Bitcoin miners looking to diversify revenue sources.

Yahoo Finance data showed MARA shares climbing to $13.77 following the announcement, leaving the stock up more than 14.6% on the day and over 53% year to date despite continued weakness across much of the crypto mining sector.

Texas site adds capacity for AI and Bitcoin mining

Beyond expanding its mining operations, MARA said it plans to develop the property with Starwood Digital Ventures into a large-scale digital infrastructure campus capable of supporting high-performance computing workloads, flexible compute services and Bitcoin mining. The company added that the site has already generated interest from potential high-performance computing tenants.

Once an HPC lease is executed, MARA said HIF will retain a minority ownership stake in the project. Construction is expected to begin in phases later this year, subject to regulatory approvals.

Earlier this year, MARA strengthened its digital infrastructure portfolio by acquiring Long Ridge Energy & Power in a $1.5 billion transaction, adding another large energy asset to support its computing strategy. The Texas purchase builds on that expansion as the company continues investing in facilities that can serve both blockchain and AI workloads.

Bitcoin miners continue expanding AI infrastructure

MARA joins a growing list of publicly traded Bitcoin miners investing in AI-focused infrastructure instead of relying solely on cryptocurrency mining. As crypto.news reported earlier, IREN Limited recently completed its acquisition of Spain-based Ingenostrum, also known as Nostrum Group, adding roughly 490 megawatts of secured grid-connected power and establishing its first operating base in Europe for AI cloud services.

Meanwhile, crypto.news previously reported that TeraWulf signed a 20-year data center lease with AI company Anthropic. According to TeraWulf, the agreement could generate nearly $19 billion in revenue over its lifetime, highlighting the growing commercial demand for high-performance computing capacity.

The trend extends beyond infrastructure operators into corporate Bitcoin treasury strategies. Earlier this week, crypto.news reported that American Bitcoin Corp. increased its Bitcoin holdings to more than 8,000 BTC.

BitcoinTreasuries data ranked the company among the largest publicly traded corporate Bitcoin holders in the United States, ahead of GD Culture Group and Galaxy Digital, illustrating how companies across the sector are pursuing different approaches to strengthen their positions as institutional interest in digital assets and AI computing continues to grow.

Goldman Sachs has told employees to confine their prediction market activity to sports and entertainment. The bank hopes to limit compliance risks tied to betting on elections, interest rates, and other market-moving events.

The bank issued the policy through an internal memo. It warned that repeated violations could lead to termination, a person familiar with the matter told the Financial Times.

Kalshi and Polymarket Face Insider Trading Scrutiny

Both platforms have drawn scrutiny over users profiting from advance knowledge of major events. Lookonchain flagged three wallets that netted more than $630,000 betting on Nicolás Maduro’s removal hours before his capture. Nobel Peace Prize organizers separately investigated a possible leak after a run of successful wagers on the eventual winner.

Kalshi and Polymarket have since rolled out new rules targeting insider trading and market manipulation. The scrutiny comes as Kalshi pursues a $40 billion valuation in a new funding round, underscoring how fast institutional capital is flowing into the sector.

Why Wall Street Banks Are Wary of Prediction Bets

Banks like Goldman sit close to material non-public information that can move markets. That proximity forces strict limits on what trades employees can make, and prediction platforms complicate those controls.

Kalshi and Polymarket let users wager on outcomes ranging from elections to where the S&P 500 will land at a given moment, blurring the line between entertainment and market-sensitive speculation.

Both platforms still earn most of their revenue from sports betting. Kalshi, meanwhile, is pushing into financial services with a new block-trading operation, a sign prediction markets want a permanent seat at Wall Street’s table.

The post Goldman Sachs Limits, but Doesn’t Stop, Employees Using Kalshi and Polymarket appeared first on BeInCrypto.

The Bank of Korea has reaffirmed that won-denominated stablecoins should initially be issued through bank-led consortiums, reinforcing its position as South Korea’s digital asset legislation remains stalled.

Summary

- Bank of Korea has reaffirmed support for bank-led issuance of won-backed stablecoins.

- The central bank plans to expand deposit-token pilots for public payments and services.

- Disagreements over stablecoin rules continue to delay South Korea’s Digital Asset Basic Act.

According to local reports from Digital Asset and EDaily, the Bank of Korea (BOK) restated its position in documents submitted on Thursday to the National Assembly’s finance committee.

The central bank argued that bank-led consortiums should receive priority when issuing won-backed stablecoins and also proposed creating a statutory policy body that would bring together financial regulators and other relevant government agencies to oversee the sector.

The latest submission continues a policy position the BOK has maintained for months as lawmakers work on South Korea’s Digital Asset Basic Act. The central bank has consistently argued that banks should retain a leading role in stablecoin issuance, saying existing banking oversight provides a stronger foundation for financial stability and consumer protection.

Deposit-token development remains on the agenda

Alongside its stablecoin recommendations, the BOK said it will continue expanding practical uses for deposit tokens during the second half of the year. According to the materials submitted to lawmakers, planned applications include government subsidy payments, public vouchers, electric vehicle charging infrastructure, and additional real-world payment services available to the general public. Deposit tokens are blockchain-based digital representations of commercial bank deposits.

The latest update follows earlier policy steps taken this year. In April, BOK Governor Hyun-Song Shin used his first public address to express support for both deposit tokens and central bank digital currencies (CBDCs).

During the same month, South Korea’s Ministry of Economy and Finance announced a pilot program that would use tokenized bank deposits for government operational spending, signaling continued institutional support for tokenized payment infrastructure.

Legislative disagreements continue to delay reforms