Crypto World

Gondor unlocks leveraged Polymarket bets with portfolio-backed credit

Gondor has introduced a portfolio-backed margin account that allows Polymarket traders to borrow against their entire prediction market holdings instead of individual positions.

Summary

- Gondor launches V1 with portfolio-backed borrowing for Polymarket traders.

- Cross-margin replaces isolated lending after a seven-month beta program.

- Private access begins next week, with a public launch planned for September.

According to Gondor’s announcement on Monday, the new product, called V1, uses a cross-margin system that evaluates a trader’s complete Polymarket portfolio as collateral before extending credit. Private access is scheduled to begin next week, while a public launch is planned for September. Gondor also said it does not take custody of user assets.

The release expands on the company’s original lending strategy announced after its August 2025 angel funding round. As previously reported by crypto.news, Gondor raised capital in a round led by Maven11 Capital, with participation from investors associated with Polymesh, Rhino.fi, Futuur, Salt, and others to develop lending products for Polymarket traders. V1 builds on that effort by replacing position-based borrowing with portfolio-backed credit.

Cross-margin model replaces isolated lending

Before introducing V1, Gondor spent seven months testing its lending system through a closed beta. According to the company, more than 150,000 users joined the waitlist, after which it reviewed applicants’ Polymarket activity and selected 1,000 of the platform’s most active traders to participate.

During the beta, borrowers initially used an isolated lending model that treated each prediction market position separately. Gondor said this approach exposed lenders to binary market risk because a position could rapidly lose nearly all of its value before liquidation became possible.

As a result, the company said lenders had to compensate for that risk by charging higher borrowing costs and imposing tighter conditions. Lending was limited to more liquid markets, borrowing capacity was capped, and some loans had to be closed before the related prediction markets reached resolution.

Gondor added that these safeguards protected lenders but reduced the borrowing experience for traders by limiting available credit and shortening the lifespan of loans.

Portfolio collateral supports larger credit lines

The company said V1 addresses those issues by allowing gains from one position to offset losses in another, similar to how traditional prime brokers extend credit against an investor’s overall portfolio rather than evaluating assets individually.

According to Gondor, this portfolio-based structure makes it possible to provide more borrowing capacity while lowering financing costs. The company also said the system can support a larger variety of prediction markets and lets traders keep positions open until market resolution instead of forcing early loan closures.

Although Gondor outlined how the cross-margin model works, several operating details remain undisclosed ahead of the private rollout. The announcement did not specify borrowing rates, collateral requirements, liquidation thresholds, or which prediction markets will be available when early access begins.

The company has not indicated whether those terms will be finalized before the September public release, but the upcoming private access period is expected to provide the first live test of the portfolio-backed lending model outside its closed beta.

On July 12, Uniswap founder Hayden Adams posted a number that would have sounded like satire during the governance-token winter: the protocol is generating 5.2 million dollars in daily fees, more than any protocol in crypto other than the two giant stablecoins, and far more than the perpetuals and memecoin venues that dominated the fee leaderboard for the past two years.

Summary

- Uniswap is generating more than 5 million dollars in daily fees, driven largely by Robinhood Chain activity.

- Robinhood Chain recorded 500 million dollars in daily Uniswap volume within eight days of launch.

- The UNIfication program burns UNI against protocol fees, turning fee capture into supply reduction.

- The key question is whether Robinhood Chain volume remains durable after gas subsidies expire.

- UNI’s repricing depends on fee-switch votes passing, sustained volume, visible burns, and regulatory stability around tokenized equities.

DefiLlama’s independent count for the same 24 hours, 5.16 million dollars, backs him up. The source of the surge is the least crypto-native venue imaginable: Robinhood Chain, the brokerage’s new Ethereum layer 2, supplied roughly 4.38 million dollars of that daily total, dwarfing Ethereum mainnet at 296,000 dollars and Base at 288,000.

The volume statistics behind those fees arrived at a pace no layer 2 debut has matched. Within eight days of the July 1 launch, Robinhood Chain recorded 500 million dollars in daily Uniswap trading volume, a tenfold jump from the day before, making it the second largest network for Uniswap activity after Ethereum mainnet. Cumulative swap volume crossed 1 billion dollars by July 10. Across the first seven days, the chain generated 10.98 million of Uniswap’s 20.1 million dollars in total weekly fees. Daily active Uniswap traders surged to roughly 220,000, more than ten times the prior week. Adams described the network as the most active blockchain layer outside Ethereum mainnet itself.

And this is the part that turns a volume story into an investment thesis: for the first time in the protocol’s history, that fee firehose is being plumbed directly into the token. The UNIfication program, passed by the DAO in December 2025 with 125.34 million UNI in favor and a rounding error against, burns UNI against protocol fees on 11 chains. A snapshot vote that ran from July 7 to July 12 asked holders to extend the mechanism to v4 pools, with binding on-chain votes following the week of July 13. A parallel temperature check, running July 10 through 15, proposes switching on protocol fees for the Robinhood Chain deployment itself. If both pass, the loudest new fee source in DeFi connects to a supply-destruction machine, and UNI completes a conversion that the entire sector is attempting: from governance token to cash flow asset.

This feature examines the machine, the money, and the two serious objections, that the volume is subsidized and that the fee switch drives away the liquidity it taxes.

From governance token to burn machine: how UNIfication works

For five years, UNI was the emblem of a category problem. The token governed a protocol that processed trillions in cumulative volume and captured none of it; every basis point of swap fees flowed to liquidity providers, and UNI’s value proposition reduced to voting rights over a treasury and the perpetual promise of a fee switch that governance never dared flip. The token traded at 3.23 dollars on July 7 against a 2021 peak of 44.97, a 93 percent drawdown that priced the promise at roughly nothing.

UNIfication changed the architecture. Under the system live since December, protocol fees collected on each chain flow into contracts called TokenJar. Anyone who wants to claim the accumulated assets, in practice arbitrage searchers, must first burn an equivalent value of UNI. The burned tokens are bridged back to Ethereum and sent to the dead address, permanently removing them from supply. The design is deliberately mechanical: no dividends, no staking claims, no legal distribution to holders that might attract securities analysis, just a standing market operation that converts fee revenue into supply reduction at whatever pace trading activity dictates. The program already runs on 11 networks: Ethereum, Arbitrum, Base, Celo, OP Mainnet, Soneium, X Layer, Worldchain, Zora, BNB Chain, and Polygon.

The July votes address the two gaps in coverage, and the v4 gap is the technically interesting one. Uniswap v2 and v3 pools carry fixed fee tiers, so collecting a protocol share is a matter of setting one rate per pool. v4 is built around hooks, smart contract plugins that let developers customize pool behavior, including fees that can change block by block. Taxing something that mutable required new machinery: the proposal introduces a V4FeePolicy contract that determines the protocol fee for any pool and a V4FeeAdapter that collects and routes it into the burn pipeline. More than 1,500 builders are working with v4 hooks, and institutional-scale flow has already arrived, with Spark, the liquidity arm of Sky, pushing 1.5 billion dollars in stablecoin volume through v4 in the past month. The Robinhood Chain temperature check would extend fees across the v2, v3, and v4 deployments there, using the expedited governance track that UNIfication authorized for fee-parameter updates.

The market has started doing the arithmetic. UNI rallied about 21 percent from its July 1 low of 2.70 dollars to 3.30 by July 8, touched moves of 14 percent on the volume headlines, and trades near 3.63 with resistance mapped at 3.73. A 2 billion dollar market capitalization against a protocol annualizing north of 1.8 billion dollars in gross fees, if the July run rate held, is the kind of ratio that makes traditional investors reach for spreadsheets, with the enormous caveat that only the protocol’s share of fees, not the LP share, feeds the burn: in the measured 24 hours, protocol earnings were about 73,454 dollars against the 5.2 million gross, because the switch is not yet flipped on the newest and largest sources.

The distribution deal of the cycle

The reason the fee conversation suddenly matters is distribution, and the scale of what Robinhood connected deserves to be stated plainly.

Robinhood operates between 24 and 28 million funded accounts and posted record first-quarter revenue of 1.07 billion dollars. Its chain, built on Arbitrum’s stack with 100-millisecond blocks and full EVM compatibility, shipped with Uniswap v2, v3, v4, and UniswapX deployed from day one as the default liquidity layer. The flagship product is Stock Tokens: tokenized versions of more than 90 US equities and ETFs, tradable around the clock by eligible retail users in more than 120 countries, with Chainlink as the oracle layer, 1inch for routing, BitGo for custody, and Morpho powering a yield product on the USDG stablecoin. A trader in Manila can buy tokenized Nvidia exposure at 2 a.m. through Uniswap liquidity and settle instantly, no T+1, no market hours. Developers deployed more than 13,900 smart contracts in the first week. Ethena moved 50 million dollars into a Morpho vault in a single transaction, driving total value locked above 106 million dollars, up 159 percent in a day. Even the memecoin economy arrived on schedule, with Pump.fun integration and chain-native tokens amplifying volume, as crypto.news reported when the network crossed the 500 million dollar mark.

Standard Chartered’s head of digital asset research, Geoff Kendrick, argued the market was underpricing the partnership, calling it a real strategic alliance rather than a listing announcement. The structural point underneath his claim: DeFi protocols have spent years competing for the same recycled on-chain capital, and Robinhood represents something the sector has never had, a mainstream brokerage routing its retail flow through a decentralized venue by default. For Uniswap specifically, it means the protocol’s addressable market expanded overnight from crypto natives to anyone with a Robinhood account and a tokenized equity order, and the fee data shows the expansion is not theoretical. One venue, eleven days old, is out-earning Ethereum mainnet fifteenfold.

The rotation context makes the timing sharper. In a market where everything outside Bitcoin and Ethereum lost roughly 23 percent in six months, capital has crowded toward the handful of assets with verifiable revenue: perpetuals venues, stablecoin issuers, and now, abruptly, the largest DEX. The same repricing logic runs through the stablecoin wars, where volume quality has become the scoreboard, a shift crypto.news examined in the USDC-Tether flippening, and through Ethereum itself, which is rebuilding its entire execution roadmap around being credible settlement infrastructure for exactly this kind of institutional flow, the project crypto.news detailed in the Lean rebuild. UNI’s real revenue moment is one instance of a sector-wide migration from narrative to cash flow.

The comparables: what a fee-earning DEX token is worth

The rotation to cash flow gives UNI a peer group for the first time, and the comparisons cut in both directions.

The flattering comparison is to the fee leaders UNI just passed. Hyperliquid, Pump.fun, and the perpetuals venues built the template of the past two years: tokens with direct revenue linkage, aggressive buyback or burn mechanics, and valuations that survived the altcoin drawdown better than the governance-token cohort precisely because holders could point at income. Adams’ framing, more daily fees than anything except USDC and USDT, deliberately places Uniswap atop that leaderboard. On raw multiples, a 2 billion dollar capitalization against 20.1 million dollars in weekly gross fees puts the protocol at roughly two times annualized gross fees, a figure that looks absurd against any traditional exchange until the LP share is subtracted, at which point the multiple on actual protocol take becomes very large and entirely dependent on the pending votes. The valuation case is therefore not that UNI is cheap on current protocol revenue. It is that governance controls a dial connected to a gross fee stream of unprecedented size, and the July votes are the market’s first chance to watch the dial turn on the newest and largest sources.

The unflattering comparison is to the treasury-heavy tokens whose burns never outran their supply overhangs. UNI carries a circulating supply near 630 million against a total of 1 billion, with treasury and team allocations that dwarf any plausible near-term burn rate. At the current protocol take, the burn is symbolic; even at meaningfully higher fee capture, supply destruction measured in tens of millions of dollars annually meets a token with hundreds of millions of units yet to circulate. The burn thesis is a direction, not a floor, and direction gets repriced quickly when the underlying volume proves cyclical. The December UNIfication rally faded within weeks for exactly that reason: mechanics without volume are a press release. What is different now is that the volume arrived, from a source nobody’s model included, which is why the token’s 21 percent July move happened on the news of usage, not the news of tokenomics.

There is one more comparable worth naming because it frames the strategic stakes: the launch chain itself. Robinhood Chain’s opening fortnight has minted its own equity narrative, with HOOD shares up more than 40 percent in a month and insiders selling into the enthusiasm, and the network’s headline metrics, hundreds of millions in early volume against liquidity measured in the low tens of millions, drew immediate scrutiny about depth and durability. The tokenization trade rewards networks that convert launch attention into recurring activity, the pattern that has kept capital concentrated in venues with verifiable usage, as crypto.news observed when tokenized assets drove a rival network to record throughput. Uniswap is the venue where those questions get answered in public, block by hundred-millisecond block, because it is where the trades actually clear.

Objection one: subsidized volume is not revenue

The skeptics’ first argument is about the quality of the 500 million dollars, and it is not hand-waving.

Robinhood is waiving gas fees on the chain for the first 90 days. Zero gas removes the single largest natural brake on wash trading, incentive farming, and volume inflation; when round trips cost nothing, volume statistics measure enthusiasm for free transactions as much as demand for the assets traded. Analysts made exactly this objection in the launch week, noting that enormous AMM volume does not automatically create value for UNI without activated fee capture, and that if a meaningful share of the headline number reflects farming, the late-September expiry of the gas subsidy becomes the first genuine stress test of the entire thesis. The launch-week TVL data reinforces the concentration worry: a single Ethena deposit produced most of the day’s growth, and liquidity that arrives in one transaction can leave in one.

The honest response is that swap fees, unlike gas, were never waived. Every dollar of the 4.38 million in daily Robinhood Chain fees was paid by traders to liquidity providers at market rates, which makes the fee number a harder signal than raw volume. Wash trading a pool with a 30 basis point fee costs 60 basis points per round trip; nobody launders volume at that price for long. But the composition question survives the rebuttal: how much of the activity is durable tokenized-equity demand from Robinhood’s international base, and how much is launch-window speculation in memecoins and farmed incentives? The September subsidy cliff will answer it empirically. Until then, annualizing an eleven-day-old fee run rate is exactly the kind of extrapolation that DeFi cycles exist to punish.

There is also a counterparty concentration risk that has no precedent in Uniswap’s history: the protocol’s second largest venue is controlled by a publicly traded brokerage with its own regulatory exposure, its own commercial incentives, and, eventually, its own ability to route order flow elsewhere or deploy a competing AMM. Uniswap earned its position on Robinhood Chain by being the best liquidity software available on day one. Nothing guarantees the position is permanent, and the SEC’s January guidance flagging tokenized equity products for scrutiny means the flagship use case operates under a regulatory question mark of its own.

Objection two: the fee switch taxes the people who make the venue work

The second objection comes from inside the machine, and it is the oldest tension in the protocol’s design. Every dollar routed to the burn is a dollar that no longer goes to liquidity providers, the capital that actually fills the pools traders swap against.

Panoptic founder Guillaume Lambert put the LP case bluntly during the v4 vote, warning that applying the fee switch to v4 leaves providers with nowhere to migrate except competing AMMs or Uniswap forks, and that the proposal risks killing the protocol by favoring token holders over the capital that makes it function. The v4 version of the proposal sharpens his point, since reports around the vote indicated LP economics on affected pools could be reduced by as much as a third relative to the status quo. Liquidity is the most mercenary capital in crypto; it moved for 50 basis points of incentives throughout DeFi summer, and a protocol that taxes it while competitors do not is running a live experiment in how much brand and routing dominance are worth.

The bull rebuttal rests on what LPs actually get in exchange. Uniswap’s aggregated depth, its integration surface, the API now embedded in MetaMask, Zerion, and OKX routing across 18 plus chains with more than 3,000 developer keys issued, and now the Robinhood flow itself all mean an LP on Uniswap sees order flow that no fork can replicate. A fork with zero protocol fee but a fraction of the volume pays LPs less in absolute terms than Uniswap does after the tax. That was the empirical result of the vampire-attack era, and the UNIfication rollout across 11 chains has so far produced no measurable LP exodus. But v4 raises the stakes because hooks make pools programmable, and programmable pools are easier to replicate elsewhere; the fee controller architecture being voted on will tax precisely the segment of liquidity most capable of leaving. The vote closing July 12 and the on-chain sequence in the following week are, in effect, governance pricing that migration risk in real time.

The third mechanism: fee discount auctions

Alongside the burn expansion, Uniswap quietly shipped a second monetization primitive in the same week, and it deserves attention because it answers the LP objection from an unexpected angle.

Protocol Fee Discount Auctions, rolled out for the first time in early July, let sophisticated participants bid for reduced protocol fees on specific flow. The design logic runs like this: the largest source of LP pain in an AMM is not the protocol fee but adverse selection, the losses providers take when arbitrageurs pick off stale prices faster than pools can update. Auctioning fee discounts to the searchers and market makers who generate that flow converts a pure extraction into a priced privilege, captures for the protocol some of the value that MEV bots previously kept entirely, and gives high-volume participants a reason to route through Uniswap even after the fee switch activates. It is, in effect, a mechanism for taxing the taxers.

The auctions matter to the cash flow thesis for two reasons. First, they diversify protocol revenue beyond the flat fee share, adding a component that scales with the competitiveness of order flow, not raw volume, which is more durable through volume downturns. Second, they are a structural answer to Lambert’s migration warning: if the auction design succeeds in reducing the toxic share of flow that LPs absorb, providers could end up better off under the taxed regime than the untaxed one, because their gross fee cut shrinks while their adverse selection losses shrink faster. That claim is unproven and the mechanism is days old, but it reframes the fee switch debate from a zero-sum split between holders and LPs into an engineering question about who pays for price discovery. The December governance package, the v4 fee architecture, and the auctions together read as a coherent program: convert every form of value the protocol creates, swap fees, flow priority, and MEV, into revenue, then convert revenue into supply reduction.

The program’s ambition invites one more skeptical note. Every additional mechanism is additional surface area for governance capture, parameter mistakes, and the slow bureaucratization that has damaged other DAOs. A protocol that once had a single immutable design now has fee policies, adapters, controllers, auctions, and an expedited voting track, each a dial someone can turn. The bet is that Uniswap Labs and the delegate ecosystem can operate a genuinely complicated fiscal machine better than competitors can copy a simple one. The early revenue data supports the bet. The history of DeFi governance urges keeping the champagne corked.

What the UNI repricing actually requires

Assembling the pieces, the cash flow thesis for UNI needs four things to stay true simultaneously, and each has a visible checkpoint.

The votes must pass. The snapshot for v4 fees closed July 12; on-chain votes run the week of July 13; the Robinhood Chain temperature check closes July 15. The December UNIfication vote passed with near-unanimity, so the base case is passage, but the LP backlash around v4 is the loudest internal opposition the program has faced, and a diluted compromise on fee rates would proportionally dilute the burn.

The volume must survive September. The gas subsidy expires roughly 90 days after the July 1 launch. Fee revenue that persists through the cliff is real demand for tokenized equities and on-chain trading; fee revenue that evaporates was a marketing expense on Robinhood’s income statement. This is the single most informative scheduled event in the entire thesis.

The burn must be visible at scale. TokenJar mechanics mean supply reduction tracks protocol fee accrual with a lag. Watching claimed-and-burned totals over the coming quarter, rather than gross fee headlines, measures the machine’s actual throughput, and the gap between 5.2 million dollars gross and 73,454 dollars of current protocol take is the distance the switch still has to travel.

And the regulatory perimeter must hold. Tokenized equities traded by a global retail base through a brokerage’s chain sit at the intersection of securities law, the pending market structure bill, and the SEC’s tokenization scrutiny. The same institutional wave lifting fee revenue is also pulling DeFi into fights it has historically avoided, including the yield and revenue-sharing battles that banks are waging against crypto’s cash-flowing products, a conflict crypto.news has covered at the stablecoin layer. A token whose value accrues from fee capture is a token whose classification arguments get harder, not easier, which is presumably why the burn was engineered as supply destruction rather than distribution in the first place.

The remarkable thing about the past two weeks is not the volume record or even the fee record. It is that the oldest criticism of the largest DEX, that the token captures nothing, is being retired by governance vote in the same fortnight that the largest new fee source in DeFi history came online. Whether UNI at 3.63 dollars is cheap depends on September’s subsidy cliff, next week’s on-chain votes, and how much of a brokerage’s retail flow proves durable. Whether UNI is finally a claim on something is, for the first time since 2020, no longer the question.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Crypto World

Crypto News, July 13: Stablecoin Market Cap Drops Amid Memecoin Rotation as CLARITY Act Advances, Bitcoin and Ethereum Price Hold Firm

The stablecoin market has lost more than $10 billion since May, but it might not be a warning sign. Instead, money is flowing into memecoins as investors chase higher returns on Robinhood chain. Bitcoin, Ethereum, and the CLARITY Act are now driving price sentiment, with lawmakers expected to unveil an updated version of the bill next week.

Japan added to the optimism during WebX 2026. Prime Minister Sanae Takaichi pledged stronger backing for Web3 through funding and friendlier policies. Fundstrat’s Tom Lee also grabbed headlines after calling Ethereum the settlement layer for the AI economy, a view that continues attracting institutional attention.

— Coin Bureau (@coinbureau) July 13, 2026

HUGE: JAPAN PM SANAE TAKAICHI REAFFIRMS SUPPORT FOR STARTUPS AND WEB3 AT WEBX 2026

HUGE: JAPAN PM SANAE TAKAICHI REAFFIRMS SUPPORT FOR STARTUPS AND WEB3 AT WEBX 2026

In a video address at WebX 2026, Japanese Prime Minister Sanae Takaichi pledged to strengthen support for Web3 startups through increased funding from government-backed institutions and further… pic.twitter.com/N9vMDTUKK2

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

CLARITY Act Progress Lifts Bitcoin Price Sentiment

The CLARITY Act could reach Congress as early as July 17, giving the crypto industry one of its biggest regulatory moments in years. Supporters believe the proposal will finally define which digital assets fall under securities laws and which qualify as commodities. If passed, the CLARITY Act could remove one of the biggest crypto obstacles.

Nevertheless, the Bitcoin price slipped below $63,000 over the weekend amid geopolitical tensions that rattled markets. The drop triggered more than $14 million in long liquidations, yet buyers quickly stepped in before losses snowballed. By Sunday, Bitcoin had settled back into the $63,000 to $64,000 range.

Fresh demand is also showing up elsewhere, with the Coinbase Premium Index climbing back toward neutral after spending 55 straight days in negative territory, showing U.S. buyers are becoming more active again. Not just that, spot Bitcoin ETFs also recorded net inflows after nine weeks of withdrawals, giving bulls another reason for confidence.

As of today, however, Fidelity’s Jurrien Timmer still expects one more shakeout before the next rally, with $60K acts as the bottom. Michael Saylor also fueled speculation of another purchase after sharing his latest Bitcoin tracker update. Another orange dot from him might come soon, as usual.

Another talking point is BIP 110, a proposal that would limit arbitrary data stored in Bitcoin transactions. Critics, including Adam Back and Michael Saylor, argue the change could split the community without solving a meaningful problem. So far, traders have shown little concern as attention stays fixed on the CLARITY Act.

Discover: The Best Crypto to Diversify Your Portfolio

Ethereum Price Draws Institutional Attention

Ethereum price has been moving in a tight range around $1,800 despite a quieter weekend across the crypto market. Price action has slowed, but institutional interest has not.

Speaking at WebX 2026, Tom Lee described Ethereum as the foundation for the coming AI economy. He pointed to growing adoption from financial firms, the Robinhood Chain launch, and improving macro conditions as reasons that Ethereum price may be entering a new cycle.

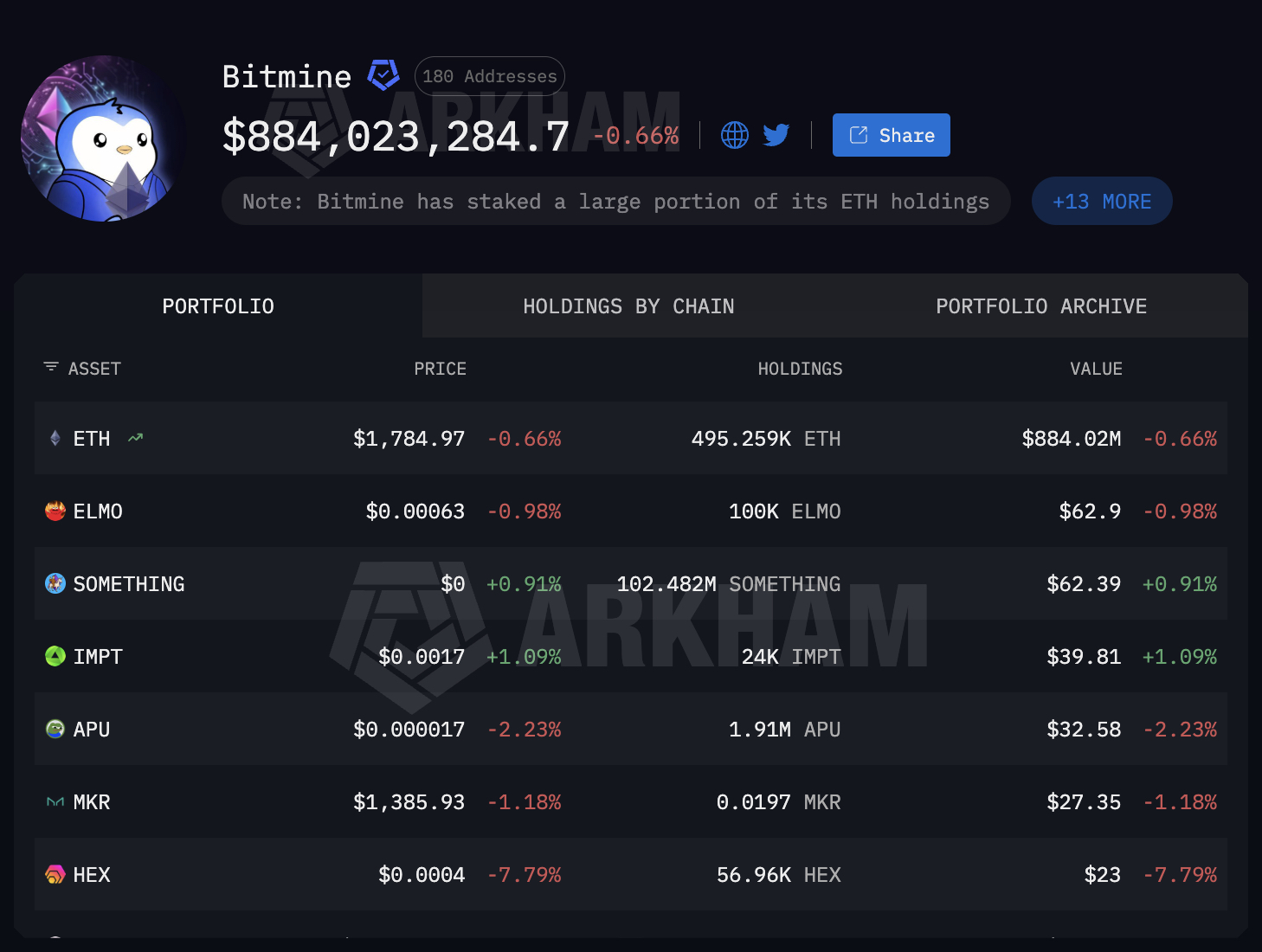

Not just the talk, Tom Lee’s firm, Bitmine, now holds 5.74 million ETH, or about 4.8% of the total supply, and plans to increase that stake. Agreeing with Lee,Ethereum whales also bought another $20.6 million worth of ETH even after several days of exchange outflows.

But that’s not all, ETH network development has also stayed active. The Ethereum Foundation confirmed one of its AI agents detected a validator crashing bug before human researchers verified the issue. A separate Cambridge study found Ethereum’s shift to Proof of Stake reduced electricity consumption by more than 99.9%, strengthening its case among institutions focused on sustainability.

So, with all that news, what should we be expecting this week?

The next few days could prove important for the market. We are watching the CLARITY Act for signs of regulatory progress while tracking institutional buying across both major coins. If those trends continue, Bitcoin and Ethereum price could build on their recent resilience. For now, the move out of stablecoins looks less like an exit from crypto and more like traders rotating into assets with higher upside, while the Ethereum price keeps finding support from long-term buyers.

Discover: The Best Token Presales

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post Crypto News, July 13: Stablecoin Market Cap Drops Amid Memecoin Rotation as CLARITY Act Advances, Bitcoin and Ethereum Price Hold Firm appeared first on Cryptonews.

Webull EU has secured MiCAR approval in the Netherlands, clearing the way to launch regulated crypto custody services for European clients later this year under the bloc’s digital asset rulebook.

Summary

- Webull EU has received MiCAR approval in the Netherlands to launch regulated crypto services.

- The company will provide crypto custody while Coinbase Luxembourg will execute client orders.

- The approval adds to a growing list of firms expanding across Europe under the EU’s MiCA framework.

Webull EU announced on Monday that the approval from the Netherlands’ Autoriteit Financiële Markten (AFM) allows the company to begin offering crypto-asset services under the European Union’s Markets in Crypto-Assets Regulation (MiCAR), with an initial rollout planned in the Netherlands before expanding across the rest of the EU through passporting.

The approval makes Webull one of the first dual-regulated investment firms in the Netherlands to receive MiCAR authorization, according to the company. Crypto assets held by clients will be custodied by Webull EU, while trade execution will be handled through a partnership with Coinbase Luxembourg S.A.

“We are pleased to have received MiCAR approval from the AFM, marking an important milestone in Webull’s European ambitions,” Andries van Luijk, CEO of Webull Securities (Europe), said. He added that the company intends to provide clients with regulated access to digital assets under the EU’s new framework.

Webull prepares EU crypto rollout

Once operations begin in late 2026, European users will be able to place crypto orders through the Webull platform across multiple asset classes. According to the company, the MiCAR approval also allows it to provide regulated custody services that meet the investor protection and operational standards required under the EU framework.

While the initial approval covers the Netherlands, Webull said passporting approval remains pending before it can extend the service across other EU member states under MiCAR’s single licensing regime.

The development comes as more financial and crypto firms secure MiCAR authorisation following the end of the regulation’s transition period on July 1. Under the framework, companies authorised in one member state can offer covered crypto services across the European Economic Area without obtaining separate licences in each country.

MiCAR approvals continue across Europe

Recent approvals have increasingly centred on Luxembourg, which has become a key licensing base for firms expanding regulated crypto operations in Europe.

Earlier this month, Ripple received a full Crypto Asset Service Provider (CASP) licence from Luxembourg’s Commission de Surveillance du Secteur Financier, allowing it to offer regulated crypto payment services across the European Economic Area. The company said the approval completed its MiCA requirements and expanded its regulated payments business to all 30 EEA countries.

Bridge also secured both a MiCA CASP authorization and an Electronic Money Institution licence in Luxembourg, enabling it to provide euro-backed stablecoin infrastructure, virtual IBANs and cross-border euro payment services throughout the European Union.

The regulatory transition has also prompted changes across the industry. As previously reported by crypto.news, Coinbase, Kraken and Crypto.com removed USDT trading for European users after Tether chose not to seek MiCA authorization, while Binance introduced service changes to comply with the new framework.

40% of what you read on LinkedIn is written by AI. And the executive who promised to fix it didn’t write that promise themselves.

The Most LinkedIn Thing That Has Ever Happened

A LinkedIn executive recently announced that the platform would detect and downrank AI-generated posts using an in-house algorithm.

The announcement itself was AI-generated.

Read that again. Let it land.

The person responsible for fighting AI inauthenticity on LinkedIn used AI to write the message telling users they were fighting AI inauthenticity.

This isn’t satire. This isn’t a hypothetical. This happened. And it is the most perfectly LinkedIn thing that has ever occurred on LinkedIn.

The Numbers Behind The Irony

Pangram, a research-first AI detection company, just released data from 1 million posts scanned across LinkedIn, X/Twitter, Reddit, Medium, and Substack.

The findings are worse than you think:

LinkedIn is the most AI-saturated platform on the internet.

More than 40% of longform LinkedIn posts are fully AI-generated. LinkedIn posts made up a third of all scanned items, but accounted for nearly two-thirds (62%) of all AI content flagged across every platform.

For context:

- Reddit: 4.4% AI content

- X/Twitter: 10% AI content

- Substack: 21.9% AI or AI-assisted

- LinkedIn: 40%+ fully AI-generated longform

The platform built around professional identity and real names is more AI-saturated than the platform built around anonymity.

Let that sink in.

The Uncomfortable Truth About Professional Identity

Here’s what the data reveals that nobody wants to say out loud:

People are more willing to fake their professional voice than their anonymous one.

On Reddit, where nobody knows who you are, 98.1% of replies are human-authored. People show up as themselves, messy, unpolished, real.

On LinkedIn, where your real name, photo, job title, and company are attached to every post, 40% of longform content is generated by AI.

The platform designed around authentic professional identity is the least authentic platform on the internet.

Why? Because professional stakes are higher. On LinkedIn, every post is supposed to demonstrate your expertise, your thought leadership, your professional value. The pressure to perform is enormous.

So people outsource the performance to AI.

They’re not being lazy. They’re being strategic, in the most self-defeating way possible.

You’re building a professional reputation on LinkedIn using words you didn’t write, ideas you didn’t develop, and a voice that isn’t yours. And everyone’s doing it. So nobody notices. Until now.

What One In Four Longform Posts Actually Means

When you scroll LinkedIn, one in four posts over 250 words was written by an AI system.

Not AI-assisted. Not AI-edited. Fully AI-generated.

That means:

- The “thought leadership” you just liked? Probably AI.

- The “personal story” that resonated? Possibly AI.

- The “industry insight” you shared? Potentially AI.

- The connection request that seemed so genuine? Maybe AI.

And here’s the part that’s genuinely unsettling: you can’t tell. That’s the point. The AI is good enough now that the average reader can’t distinguish it from authentic human writing.

So you’re building professional relationships, making hiring decisions, forming opinions about people’s expertise, based on content a machine generated.

LinkedIn has become a platform where humans connect with AI personas attached to human faces.

LinkedIn’s Response Made Everything Worse

When LinkedIn discovered their platform was flooded with AI content, what did they do?

They announced, via AI-generated text, that they would use an in-house algorithm to detect and downrank AI content.

The layers of irony here are almost artistic:

- The platform is flooded with AI content

- A human executive presumably decides to address this

- That executive uses AI to write the announcement

- The announcement is about fighting AI inauthenticity

- The announcement is itself inauthentic

- Nobody at LinkedIn apparently caught this before publishing

This isn’t just ironic. It’s revealing. It shows how normalized AI-generated professional communication has become, even inside the companies trying to fight it.

The executive didn’t think twice. Of course you use AI to write a professional announcement. Everyone does. Even when the announcement is about everyone doing it.

The Feedback Loop Nobody’s Talking About

Here’s what happens when 40% of LinkedIn content is AI-generated:

Step 1: Humans post AI content because they see other humans getting engagement on AI content.

Step 2: LinkedIn’s algorithm surfaces the most engaging content, which includes AI content optimized for engagement.

Step 3: More humans see AI content performing well and generate more AI content to compete.

Step 4: LinkedIn’s feed becomes increasingly AI-saturated.

Step 5: LinkedIn announces they’ll fight AI content. Using AI.

Step 6: Repeat.

The platform has created a race to the bottom where authentic human content is algorithmically disadvantaged against AI content optimized for engagement. And the humans losing that race respond by also using AI.

This is not a technology problem. It’s an incentive problem.

LinkedIn rewards engagement. AI optimizes for engagement. Humans use AI to compete. Authenticity becomes economically irrational.

The Professional Reputation Paradox

LinkedIn exists for one reason: to build professional reputation and relationships.

Your reputation on LinkedIn is supposed to represent your actual professional value. Your writing demonstrates how you think. Your posts show your expertise. Your voice distinguishes you from the thousand other people with your job title.

Now 40% of that is generated by machines.

Which means 40% of professional reputations on LinkedIn are built on a foundation that doesn’t belong to the person claiming it.

When a recruiter reads your posts and thinks “this person thinks clearly and writes well,” are they evaluating you? Or evaluating GPT-4’s ability to impersonate a professional in your field?

When a client reads your thought leadership and trusts your expertise, is that trust earned? Or borrowed from a model trained on millions of documents you had no part in creating?

Professional reputation used to be built slowly, through demonstrated expertise over time. Now it can be generated in seconds.

And when everything can be generated in seconds, nothing signals actual expertise anymore.

The Platform That Knows And Doesn’t Care

LinkedIn knows about the AI slop problem. They announced they’d fight it.

But LinkedIn also has a built-in “Write with AI” button, recently rebranded “Enhance post,” but still offering AI writing assistance. The platform simultaneously fights AI content and encourages users to create it.

This isn’t hypocrisy. It’s business logic.

LinkedIn earns revenue from premium subscriptions and advertising. Premium subscriptions sell partly on the promise of greater visibility. Advertising revenue depends on engagement. AI-generated content drives engagement. More engagement means more advertising revenue.

LinkedIn’s financial incentives are aligned with more content, not more authentic content.

So they announce they’re fighting AI slop (using AI) while keeping the “Write with AI” button active (for engagement). They want the reputation of authenticity without the economics of it.

And they can maintain this contradiction because most users don’t notice, because 40% of what they’re reading is already AI and they’ve stopped being able to tell the difference.

What Real Authenticity Costs

Here’s the thing nobody’s saying:

Authentic content is expensive. AI content is cheap.

Writing a genuine thought leadership post takes hours. Thinking through a real position, finding the right language, editing for clarity. Hours.

Generating an AI post takes 30 seconds.

In a world where LinkedIn’s algorithm treats both the same, where engagement metrics don’t distinguish authentic from generated, the rational economic choice is AI.

The people choosing to write their own posts are paying a time premium for authenticity that the platform doesn’t reward.

Until LinkedIn structurally rewards authentic content with algorithmic visibility, with verified human authorship badges, with something that makes authenticity economically rational, the 40% will become 50%, then 60%, then 70%.

Not because people don’t value authenticity. Because the platform makes inauthenticity free and authenticity expensive.

The Question For Every LinkedIn User

When you post on LinkedIn, are you trying to communicate? Or perform?

Because those are different things. Communication is about sharing what you actually think with people who might actually care. Performance is about generating engagement metrics using whatever tool works best.

AI is a performance tool. It’s very good at generating engagement-optimized content that sounds like professional communication.

But it’s not communication. It’s simulation.

And LinkedIn has become a platform full of simulated professional communication, people performing expertise they may or may not have, in voices that may or may not be theirs, to audiences that increasingly can’t tell the difference.

The LinkedIn executive who announced they’d fight AI slop using AI content didn’t do it maliciously. They did it because it’s become completely normal.

That normalization is the actual problem.

What Comes Next

LinkedIn will deploy their algorithm. It will catch some AI content. The AI will get better at evading detection. LinkedIn will update the algorithm. Repeat.

Meanwhile, the 3% of users who write authentic content will keep getting outpaced by the 97% using AI until LinkedIn makes authenticity worth something.

Or until users start demanding it.

The Pangram Chrome extension lets users scan posts and flag AI-generated content as they scroll. It’s a band-aid on a structural wound. But it’s also evidence that some users are starting to care.

They’re not the majority. But they exist.

And they’re the audience worth writing for.

American Bitcoin Corp. (ABTC) crossed 8,000 Bitcoin (BTC) this month, yet its stock trades more than 95% below its peak. The gap asks whether the Trump name or the business model is to blame.

The company keeps buying Bitcoin and reporting strong mining margins. Its shareholders, however, have watched the equity collapse since its September 2025 debut.

A Trump Premium that Inflated the Debut

The Trump connection gave American Bitcoin its launch. Eric Trump co-founded the firm and serves as chief strategy officer, while Donald Trump Jr. advises it. That branding drew heavy retail demand as the company merged with Gryphon Digital Mining.

It was listed on Nasdaq in September 2025. Forbes later reported that investors valued the firm at nearly $13.2 billion at its debut. It held only about $270 million of Bitcoin at the time.

The structure sat quietly behind the story. American Bitcoin is a majority-owned subsidiary of Hut 8, which holds roughly 80% after transferring its self-mining operations. The Trump family controls about 20%, and Eric Trump’s personal slice sits near 6%.

That same association cuts both ways. Data now puts the stock more than 95% below its peak.

The same Forbes report found retail holders lost about $500 million since the debut. Eric Trump’s own fortune, by contrast, rose about $90 million, since the founders bought in early and cheaply.

He dismissed the Forbes report as propaganda, yet no scandal or governance failure explains the collapse.

Follow us on X to get the latest news as it happens

A Treasury that Grows as the Stock Sinks

Operationally, American Bitcoin has hit its marks. It mined 817 BTC in the first quarter, a company record. Margins held near 52% even as Bitcoin fell about 22%, the company reported.

Eric Trump says the fleet mines at a 47% discount to spot. Forbes disputed that math, pegging the all-in cost near $90,000 per coin after depreciation and overhead are factored in.

Yet the equity tells the opposite story. To fund that accumulation, the company leaned on share issuance, and its float ballooned. Each raise bought more coins but handed existing holders a thinner claim.

A 1-for-15 reverse split then cut the count from more than 1.09 billion shares to about 73 million. The move, effective in early July, aimed to keep ABTC above Nasdaq’s minimum bid price.

The math shows the strain. Satoshis Per Share rose about 20% in the first quarter, yet the share count kept climbing. A $117.2 million non-cash markdown on its Bitcoin drove a $118.2 million operating loss. CEO Mike Ho said the underlying business stayed profitable and that the firm did not sell a single coin.

That stance holds as it keeps buying Bitcoin through the slump. Eric Trump framed the 8,000 BTC milestone as vindication rather than a warning.

“Thrilled to announce American Bitcoin crossing the 8,000 BTC mark! … we continue to differentiate ourselves, mining at a 52% profit margin in Q1 and continually adding to our treasury, all while maintaining one of the lowest SG&A ratios in the industry … The stacking continues,” Eric Trump shared recently.

The AI Pivot American Bitcoin Refused

The wider market has moved on. Through 2026, rivals repurposed mining power for artificial intelligence, where margins looked richer. Stocks such as TeraWulf, IREN, and Hut 8, the majority owner, climbed as they leaned into AI infrastructure.

Others, including Riot, sold Bitcoin to fund the shift, while Empery Digital cut its holdings by nearly half. Their shares increasingly tracked AI demand rather than Bitcoin’s price.

American Bitcoin knows that trade well. It began in February 2025 as American Data Centers, a venture tied to the Trump-linked firm Dominari Holdings.

A month later, it pivoted to pure Bitcoin mining through the Hut 8 deal. In effect, it walked away from data centers just before the market began paying up for them.

The comparison it invites now cuts the wrong way. American Bitcoin’s hybrid model mines coins and buys more, echoing the MicroStrategy accumulation playbook now run by Strategy. Michael Saylor pioneered that approach in 2020, and for years his stock traded far above its Bitcoin.

Strategy’s own filings show 843,775 BTC today after withholding from selling any BTC last week. Yet even that premium has flipped to a discount, with the stock valued below its coins in mid-2026.

If the market has soured on the model’s pioneer, a smaller and diluted copy has little cover.

What the Disconnect Reveals

The evidence points to a hard bet in a shifting market, not broken trust. The Trump name inflated the debut, which made the correction look political. Yet the market now values American Bitcoin near $430 million, below the roughly $500 million of Bitcoin it holds.

The same repricing has humbled Strategy, the model’s own pioneer. What sank the stock was a diluting wager on Bitcoin that skipped the sector’s richest trade. Public shareholders absorbed the loss, while the venture’s insiders did not.

The post Why Did Trump’s American Bitcoin Stock Flatline In Just 1 Year? appeared first on BeInCrypto.

Binance’s futures desk is showing signs of a renewed momentum spike, reaching a 2026 high even while spot trading on centralized exchanges remains subdued. According to CryptoQuant analyst Maartuun, Binance logged $1.6 trillion in futures volume in June—its strongest month of the year—despite Bitcoin trading in the mid-$60,000s and a broadly cautious tone from many market participants.

The contrast between accelerating derivatives activity and weak spot volumes highlights a tension investors are watching closely: whether leverage is re-entering the market ahead of a broader risk rebound, or simply reflecting short-term positioning in an otherwise lethargic trading environment.

Key takeaways

- Binance futures volume hit $1.61 trillion in June, up 80% from May’s $893 billion, marking a 2026 high.

- OKX and Bybit also grew in June, but Binance outpaced them by volume and again led the market.

- Quarterly CEX futures volume continued to decline: Q2 fell to $15.7 trillion, down 11% from Q1, according to CryptoRank.

- Spot volumes on CEXs remain weak, with Q2 spot trading at $3 trillion—the weakest quarter in two years.

- Binance’s uptick arrives near regulatory changes in the EU, including the MiCA transition schedule and related licensing developments.

June’s derivatives rebound at Binance

CryptoQuant’s Maartuun said Binance processed $1.61 trillion in futures trading volume in June, the highest monthly figure recorded so far in 2026. The jump was stark: June volume rose by about 80% versus May’s $893 billion.

The strength wasn’t limited to Binance. OKX reported $609 billion in June futures volume, while Bybit recorded $434 billion. Both exchanges increased versus May—OKX up 9% and Bybit up 18%—suggesting the rise was broad-based across major venues rather than isolated to a single platform.

Even so, Binance’s lead stood out. Maartuun noted that the trio of exchanges has not seen futures activity near these levels since January 2026, when Binance moved roughly $1.5 trillion and OKX and Bybit reached $667 billion and $502 billion respectively.

Broader market still shows hesitation: futures down overall, spot at multi-year lows

While June’s spike looks encouraging for derivatives activity, the bigger picture remains mixed. CryptoRank data cited in the report shows that total CEX futures volume fell to $15.7 trillion in Q2 2026, down 11% from $17.6 trillion in Q1. This represented the third consecutive quarterly decline for centralized exchange futures.

The pace of contraction did ease compared with Q1, when futures volume dropped 31% versus Q4 2025. In Q2, Binance maintained its position as the largest futures venue, holding approximately 28% market share.

Spot markets, however, were more clearly impaired. CEX spot volume reportedly fell to $3 trillion in Q2, the weakest quarter in two years and an 18.9% decline from Q1. Binance remained the largest spot exchange by volume, with $731 billion for the quarter, but its market share slid from 27% to 24%, signaling that the downturn wasn’t just a dip in overall activity—it also came with share erosion.

Taken together, the numbers suggest June’s futures surge may reflect traders seeking exposure through leveraged instruments even when broader spot participation has not recovered. For investors, that distinction matters: derivatives volume can rise during periods when spot demand is still muted, but it can also precede volatility rather than stable trend formation.

EU MiCA transition: Binance futures activity continues after the shift

The timing of June’s futures strength also lands near Europe’s Markets in Crypto-Assets (MiCA) transition period. Earlier coverage noted that the end of the transition schedule raised questions about how major exchanges would adapt operationally and how quickly trading patterns would normalize under the new compliance framework.

In late June, Binance withdrew its application for a license in Greece just days before the framework moved into its next phase on July 1. Against that regulatory backdrop, early July data from CryptoQuant indicated Binance’s futures market remained active after the transition, recording $418 billion in futures volume in the first 10 days of July.

That continuation doesn’t confirm that regulation improved trading conditions; it does, however, provide at least an early signal that activity did not abruptly stall at the transition boundary. The next key question for traders and exchange operators will be whether this level of derivatives throughput persists over subsequent weeks and whether spot volumes begin to respond as regulatory uncertainty fades.

What to watch next for traders and exchange users

June’s futures surge is a clear data point: Binance’s derivatives volume jumped sharply to a 2026 high while broader quarterly trends show that CEX spot and futures volumes remain under pressure. Investors should watch whether July sustains similar momentum and whether spot trading starts to recover alongside futures—or whether the market continues to concentrate activity in leveraged instruments as traders navigate ongoing regulatory and macro uncertainty.

Humanoid robot startup LimX Dynamics shows off its products at its Shenzhen, China, office on July 3, 2026.

Evelyn Cheng | CNBC

BEIJING — Humanoid startup LimX Dynamics is getting ready to go public, just over four years after it was founded during the pandemic.

“Listing is a must,” said founder Will Zhang, emphasizing the importance of timing. He was speaking to reporters ahead of the company’s announcement Tuesday that it had raised $200 million in a pre-IPO round.

Zhang compared the situation to Chinese electric car startups Nio, Xpeng and Li Auto, which successively listed in the U.S. from 2018 to 2020. “Once the technology is mature, if [the company] doesn’t list, then like WM Motor, it may disappear,” he said in Mandarin, translated by CNBC.

Several overseas investors, including UAE-based Stone Venture, Italy-based GGG and Germany-based Redstone VC participated in LimX’s latest round, which valued the startup at 15 billion yuan ($2.21 billion), according to a press release.

The startup said it was already preparing for its IPO, likely in Hong Kong, and is in a confidential phase of review.

The urgency comes as China now has well over 100 humanoid companies, which fall under the national push for “embodied AI.”

Reflecting a rapid surge in interest, investment in the sector hit 47.09 billion yuan ($6.95 billion) in the second quarter, more than double that of the first quarter — and up over six times versus the same period last year, according to industry data provider Xiniu.

A new phase

China has fast-tracked approval for humanoid company Unitree to list in Shanghai, while Hong Kong processes applications from more than 500 companies across sectors.

“With more industrial and collaborative robot companies potentially coming to IPO, competitive pressure is likely to persist,” Morgan Stanley said in a report last week, noting sector players DeepRobot and Leju that are looking to list soon.

The investment firm forecasts 18% growth in China’s industrial robots market this year, and shipment of 50,000 humanoids.

LimX aims to create fully autonomous commercial service robots. The company said it will kick off a multi-year plan to ship thousands of humanoids to the Middle East, and is delivering its entertainment-focused Luna humanoid to customers in South Korea.

To founder Zhang, the technology behind humanoid robots has already crossed the “0 to 1” line of innovating from scratch. The next barrier to entry, he said, lies in making a good product that meets users’ needs.

Other backers in the latest funding round include Chinese precision parts company Lens Technology, IDG Capital, WestSummit Capital, Nio Capital and Hefei Binhu Industry Development Group, the release said.

Bolivia is considering adding Tether’s USDT to its national payments infrastructure, a potential milestone for stablecoin adoption in Latin America amid a long-running shortage of US dollars. The government says it is working on a regulatory approach that would treat USDT as a payment instrument alongside the boliviano and the US dollar—rather than a fringe asset outside the formal economy.

Economy and Public Finance Minister Jose Gabriel Espinoza said at a press conference on Monday that the state is assessing a framework to allow USDT “to circulate as just another currency.” Any rollout, he added, would need strong oversight and anti-money laundering controls because Bolivia remains on the Financial Action Task Force (FATF) grey list.

Key takeaways

- Bolivia is evaluating whether USDT could be recognized for everyday transactions such as payments, savings and trade.

- The proposal would require a regulatory structure that can place USDT inside the country’s formal payments system.

- Bolivia’s FATF grey-list status means anti-money laundering safeguards are expected to be central to any approval process.

- The move comes as the country confronts a widening gap between official and parallel exchange rates that has increased demand for dollar-denominated alternatives.

USDT would be treated as part of everyday payments

According to CriptoNoticias, the regulatory framework being considered is still under review. If adopted, it would aim to formally recognize USDT for retail and commercial activity, including payments, savings and trade, without relying solely on cash or the traditional banking channel.

Espinoza’s framing matters because it suggests Bolivia is not merely allowing crypto trading or occasional transfers, but contemplating a system design where USDT functions as a practical alternative for transactions. For consumers and businesses, that could mean more predictable settlement options when local access to dollars is constrained.

Regulatory hurdles tied to FATF monitoring

Espinoza also emphasized that any implementation would depend on a “robust regulatory framework” and effective anti-money laundering protections. His comments connect directly to Bolivia’s placement on the FATF grey list, which flags jurisdictions with increased monitoring needs due to deficiencies in preventing money laundering and terrorist financing.

That context helps explain why the government is taking a cautious, framework-first approach. Moving stablecoins into a national payments role typically requires clear responsibility lines—who can distribute or process them, how compliance checks are performed, and how suspicious activity reporting would operate. For Bolivia, those requirements could become a gating factor for how quickly a USDT rollout can move from proposal to practice.

Dollar scarcity and exchange-rate strain push demand toward stablecoins

The policy discussion comes against a backdrop of persistent dollar shortages in Bolivia. Reuters previously reported that Bolivia kept an official exchange rate of 6.86 bolivianos per US dollar for purchases and 6.96 for sales for years, before later abandoning the long-standing peg after pressure on foreign exchange reserves.

As Reuters noted, the abandonment of the peg contributed to the expansion of a parallel foreign exchange market where the dollar traded at a steep premium relative to the official rate. When the cost of dollars diverges sharply between official channels and informal markets, demand tends to shift toward instruments that track or approximate dollar value. In this environment, stablecoins such as USDT can become appealing for payments because they offer a dollar-denominated unit of account without requiring direct access to physical dollars.

Industry research also points to growing activity. Chainalysis’ 2025 evaluation of crypto adoption across Latin America reported $14.8 billion in total transaction volume over a 12-month period for Bolivia included within the regional assessment. While this figure does not isolate stablecoins alone, it supports the broader claim that digital assets—often used in response to currency pressures—have become more integrated into real economic behavior across the region.

Bolivia’s return to crypto-friendly policy after the 2024 ban

The USDT payments initiative fits into a broader pivot by Bolivia toward digital assets following the lifting of its longstanding cryptocurrency ban in 2024. Since taking office in late 2025, President Rodrigo Paz Pereira’s administration has pledged to incorporate digital assets into the formal financial system, an approach described by earlier coverage from Cointelegraph as paving the way for banks to introduce crypto-related products and services, potentially including stablecoin-based accounts.

What’s notable now is the specificity: instead of focusing only on banking products or general “blockchain integration,” the government is explicitly weighing how USDT could fit into everyday payments. That difference could determine how quickly stablecoins move from parallel usage toward regulated, widely accepted channels.

Readers should watch how Bolivia’s draft regulatory framework is shaped—particularly around compliance obligations given its FATF grey-list status—and whether authorities set measurable timelines for pilot programs or bank participation. The next question is not only whether USDT will be recognized, but how the state plans to govern distribution, monitoring and settlement in a way that can survive both financial controls and real-world liquidity constraints.

A Bitcoin wallet dormant since the cryptocurrency traded near $6,500 has transferred 2,931 BTC worth about $188 million, reviving onchain activity after seven years.

Summary

- A Bitcoin wallet inactive for seven years has moved 2,931 BTC worth about $188 million.

- Onchain data showed the wallet last became active when Bitcoin traded near $6,500, leaving the holder with an estimated tenfold gain.

- Whale sized transfers continue to dominate Bitcoin exchange inflows, a trend that analysts have historically linked to selling pressure.

Blockchain intelligence platform Arkham reported that the long-inactive holder moved the Bitcoin from wallet “356my” to a new address, “bc1qn”, on Sunday. The transfer is the wallet’s first recorded onchain movement since it last became active when Bitcoin was priced at roughly $6,500.

With Bitcoin now changing hands at around $64,000, blockchain analytics platform Onchain Lens estimated the holder is sitting on nearly a tenfold gain from the original position.

Whale transfers continue to dominate exchange flows

The latest movement comes as large Bitcoin holders continue to account for most transfers into cryptocurrency exchanges, a trend that onchain data has linked to rising selling pressure.

CryptoQuant’s exchange whale ratio chart showed that about 99% of Bitcoin deposited to exchanges currently comes from the 10 largest individual transfers. The metric stood at 0.99 at the time of publication, indicating that whale-sized transactions continue to dominate exchange inflows.

According to CryptoQuant, elevated whale exchange ratios have historically been associated with bearish market conditions because large deposits are more likely to precede sizeable sell orders than routine transfers from retail investors.

Separately, data from Coinglass classifies transfers worth at least $10 million as whale transactions. Such movements have accounted for most Bitcoin flowing to exchanges in recent months, increasing trader focus on whether large holders are preparing to sell.

Selling pressure has also persisted from another direction. Data from Farside Investors showed that U.S. spot Bitcoin exchange-traded funds recorded $197 million in net inflows during the week leading up to Friday, although the products posted $4.51 billion in net outflows throughout June, their weakest monthly performance on record.

Dormant wallets remain under close watch

Older Bitcoin wallets have continued attracting market attention because many are associated with early miners, long-term holders, or defunct trading platforms.

Earlier this year, crypto.news reported that a dormant whale destroyed 107 BTC worth about $8.3 million by sending the coins to an unrecoverable burn address after nearly 11 years of inactivity. Blockchain security firm AMLBot said the transactions may have been linked to the collapsed Mt. Gox exchange, although no entity behind the transfers was identified.

In a separate case reported by crypto.news, another Satoshi-era holder transferred 2,650 BTC worth more than $200 million to trading firms FalconX and Cumberland while retaining nearly 6,000 BTC.

Although those transfers did not confirm an immediate sale, market participants closely tracked the movement because large transactions from early Bitcoin holders can introduce additional supply if the coins eventually reach exchanges.

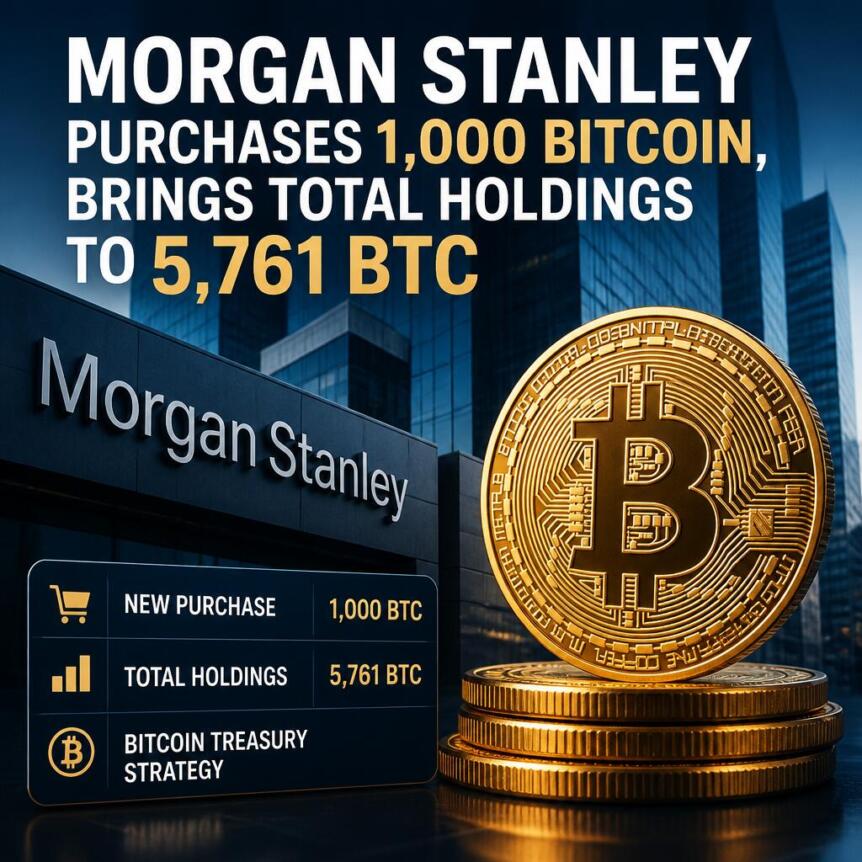

Banking giant Morgan Stanley acquired nearly 1,000 BTC over the past two weeks, taking its total holdings to 5,761 BTC, worth roughly $370 million.

According to data from Arkham, the bank added BTC to its existing stash during the market pullback through its spot Bitcoin investment product.

Morgan Stanley Adds To Bitcoin Stash

Morgan Stanley added to its Bitcoin holdings during the recent market pullback. The banking giant currently holds 5,761 BTC, making it one of the biggest institutional holders of the flagship cryptocurrency.

The acquisition was executed through a series of transfers instead of a single purchase. Arkham data shows large transfers from Coinbase Prime wallets. The transaction history also includes a 1 BTC transfer back to Coinbase Prime along with minor operational transfers.

The inflows originated from Coinbase Prime custody and deposit addresses, indicating the transfers were completed via Morgan Stanley’s spot Bitcoin investment product.

Buying The Dip

Arkham classifies Morgan Stanley as a fund, an exchange-traded product, and a Bitcoin whale. It has also linked the banking giant’s portfolio to 11 wallet addresses. The latest round of purchases is in line with Morgan Stanley’s strategy of accumulating during price dips.

However, Arkham or Morgan Stanley have not disclosed whether the purchases are direct purchases, client subscriptions, or operational inflows into its investment vehicle. Arkham has also not identified the underlying investors or whether the assets are being managed on behalf of clients or are firm-based holdings.

Morgan Stanley Increasing Its Crypto Footprint

Morgan Stanley Wealth Management recently announced a partnership with Galaxy Digital to expand its digital asset footprint. Under the partnership, high-net-worth individuals can lend their digital assets, including Bitcoin (BTC), Solana (SOL), and Ethereum (ETH), to Galaxy Digital in return for shares in spot crypto investment products, including the Morgan Stanley Bitcoin Trust. The program allows investors to gain crypto exposure in a regulated environment without selling their digital assets.

Morgan Stanley and Galaxy Digital claim the partnership also reduces the in-kind crypto-to-exchange-trading product onboarding times by 75%. The offering is part of a growing trend of on-chain accumulation as institutional interest and participation rise.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

UNI cash flow token thesis

Consolidated Financial Statements 1

Woman, 20, arrested in relation to Dovestone Reservoir fire

-

News Videos7 days ago

News Videos7 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Fashion5 days ago

Fashion5 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Tech7 days ago

Tech7 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Sports4 days ago

Sports4 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports6 days ago

Sports6 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Tech6 days ago

Tech6 days agoAnthropic brings Claude Cowork to mobile and web as usage data shows most users aren’t coding

-

Sports4 days ago

Sports4 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Sports6 days ago

We have punished the disrespect

-

Crypto World7 days ago

Crypto World7 days agoBinance lists Strategy’s STRC stock as company expands Bitcoin funding

-

Tech4 days ago

Tech4 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Business7 days ago

Business7 days agoEnbridge: AI Tailwind Priced In (Rating Downgrade)

-

Crypto World7 days ago

Crypto World7 days agoClaude AI Created Something Anthropic Never Designed

-

News Videos7 days ago

News Videos7 days ago“What’s going on?!” Carl Froch discusses Floyd Mayweather Jr financial issues

-

Crypto World6 days ago

Crypto World6 days agoNasdaq arthritis company holding Moshe Hogeg crypto hits all-time low

-

Crypto World7 days ago

Crypto World7 days agoMicrosoft Cuts 4,800 Jobs as Xbox Loses 3,200 Roles in Reset

-

News Videos5 days ago

News Videos5 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

Tech6 days ago

Tech6 days agoKeychron is stepping outside keyboards with a $349 Thunderbolt 5 dock aimed at power users

-

Business6 days ago

Business6 days agoASX 200 Slides Over 0.6% as Rare Earths and Lithium Stocks Tumble Amid Global Semiconductor Sell-Off Today

-

News Videos7 days ago

News Videos7 days agoWhy Bitcoin Could Enter Another Parabolic Cycle!

You must be logged in to post a comment Login