Crypto World

UNI cash flow token thesis

On July 12, Uniswap founder Hayden Adams posted a number that would have sounded like satire during the governance-token winter: the protocol is generating 5.2 million dollars in daily fees, more than any protocol in crypto other than the two giant stablecoins, and far more than the perpetuals and memecoin venues that dominated the fee leaderboard for the past two years.

Summary

- Uniswap is generating more than 5 million dollars in daily fees, driven largely by Robinhood Chain activity.

- Robinhood Chain recorded 500 million dollars in daily Uniswap volume within eight days of launch.

- The UNIfication program burns UNI against protocol fees, turning fee capture into supply reduction.

- The key question is whether Robinhood Chain volume remains durable after gas subsidies expire.

- UNI’s repricing depends on fee-switch votes passing, sustained volume, visible burns, and regulatory stability around tokenized equities.

DefiLlama’s independent count for the same 24 hours, 5.16 million dollars, backs him up. The source of the surge is the least crypto-native venue imaginable: Robinhood Chain, the brokerage’s new Ethereum layer 2, supplied roughly 4.38 million dollars of that daily total, dwarfing Ethereum mainnet at 296,000 dollars and Base at 288,000.

The volume statistics behind those fees arrived at a pace no layer 2 debut has matched. Within eight days of the July 1 launch, Robinhood Chain recorded 500 million dollars in daily Uniswap trading volume, a tenfold jump from the day before, making it the second largest network for Uniswap activity after Ethereum mainnet. Cumulative swap volume crossed 1 billion dollars by July 10. Across the first seven days, the chain generated 10.98 million of Uniswap’s 20.1 million dollars in total weekly fees. Daily active Uniswap traders surged to roughly 220,000, more than ten times the prior week. Adams described the network as the most active blockchain layer outside Ethereum mainnet itself.

And this is the part that turns a volume story into an investment thesis: for the first time in the protocol’s history, that fee firehose is being plumbed directly into the token. The UNIfication program, passed by the DAO in December 2025 with 125.34 million UNI in favor and a rounding error against, burns UNI against protocol fees on 11 chains. A snapshot vote that ran from July 7 to July 12 asked holders to extend the mechanism to v4 pools, with binding on-chain votes following the week of July 13. A parallel temperature check, running July 10 through 15, proposes switching on protocol fees for the Robinhood Chain deployment itself. If both pass, the loudest new fee source in DeFi connects to a supply-destruction machine, and UNI completes a conversion that the entire sector is attempting: from governance token to cash flow asset.

This feature examines the machine, the money, and the two serious objections, that the volume is subsidized and that the fee switch drives away the liquidity it taxes.

From governance token to burn machine: how UNIfication works

For five years, UNI was the emblem of a category problem. The token governed a protocol that processed trillions in cumulative volume and captured none of it; every basis point of swap fees flowed to liquidity providers, and UNI’s value proposition reduced to voting rights over a treasury and the perpetual promise of a fee switch that governance never dared flip. The token traded at 3.23 dollars on July 7 against a 2021 peak of 44.97, a 93 percent drawdown that priced the promise at roughly nothing.

UNIfication changed the architecture. Under the system live since December, protocol fees collected on each chain flow into contracts called TokenJar. Anyone who wants to claim the accumulated assets, in practice arbitrage searchers, must first burn an equivalent value of UNI. The burned tokens are bridged back to Ethereum and sent to the dead address, permanently removing them from supply. The design is deliberately mechanical: no dividends, no staking claims, no legal distribution to holders that might attract securities analysis, just a standing market operation that converts fee revenue into supply reduction at whatever pace trading activity dictates. The program already runs on 11 networks: Ethereum, Arbitrum, Base, Celo, OP Mainnet, Soneium, X Layer, Worldchain, Zora, BNB Chain, and Polygon.

The July votes address the two gaps in coverage, and the v4 gap is the technically interesting one. Uniswap v2 and v3 pools carry fixed fee tiers, so collecting a protocol share is a matter of setting one rate per pool. v4 is built around hooks, smart contract plugins that let developers customize pool behavior, including fees that can change block by block. Taxing something that mutable required new machinery: the proposal introduces a V4FeePolicy contract that determines the protocol fee for any pool and a V4FeeAdapter that collects and routes it into the burn pipeline. More than 1,500 builders are working with v4 hooks, and institutional-scale flow has already arrived, with Spark, the liquidity arm of Sky, pushing 1.5 billion dollars in stablecoin volume through v4 in the past month. The Robinhood Chain temperature check would extend fees across the v2, v3, and v4 deployments there, using the expedited governance track that UNIfication authorized for fee-parameter updates.

The market has started doing the arithmetic. UNI rallied about 21 percent from its July 1 low of 2.70 dollars to 3.30 by July 8, touched moves of 14 percent on the volume headlines, and trades near 3.63 with resistance mapped at 3.73. A 2 billion dollar market capitalization against a protocol annualizing north of 1.8 billion dollars in gross fees, if the July run rate held, is the kind of ratio that makes traditional investors reach for spreadsheets, with the enormous caveat that only the protocol’s share of fees, not the LP share, feeds the burn: in the measured 24 hours, protocol earnings were about 73,454 dollars against the 5.2 million gross, because the switch is not yet flipped on the newest and largest sources.

The distribution deal of the cycle

The reason the fee conversation suddenly matters is distribution, and the scale of what Robinhood connected deserves to be stated plainly.

Robinhood operates between 24 and 28 million funded accounts and posted record first-quarter revenue of 1.07 billion dollars. Its chain, built on Arbitrum’s stack with 100-millisecond blocks and full EVM compatibility, shipped with Uniswap v2, v3, v4, and UniswapX deployed from day one as the default liquidity layer. The flagship product is Stock Tokens: tokenized versions of more than 90 US equities and ETFs, tradable around the clock by eligible retail users in more than 120 countries, with Chainlink as the oracle layer, 1inch for routing, BitGo for custody, and Morpho powering a yield product on the USDG stablecoin. A trader in Manila can buy tokenized Nvidia exposure at 2 a.m. through Uniswap liquidity and settle instantly, no T+1, no market hours. Developers deployed more than 13,900 smart contracts in the first week. Ethena moved 50 million dollars into a Morpho vault in a single transaction, driving total value locked above 106 million dollars, up 159 percent in a day. Even the memecoin economy arrived on schedule, with Pump.fun integration and chain-native tokens amplifying volume, as crypto.news reported when the network crossed the 500 million dollar mark.

Standard Chartered’s head of digital asset research, Geoff Kendrick, argued the market was underpricing the partnership, calling it a real strategic alliance rather than a listing announcement. The structural point underneath his claim: DeFi protocols have spent years competing for the same recycled on-chain capital, and Robinhood represents something the sector has never had, a mainstream brokerage routing its retail flow through a decentralized venue by default. For Uniswap specifically, it means the protocol’s addressable market expanded overnight from crypto natives to anyone with a Robinhood account and a tokenized equity order, and the fee data shows the expansion is not theoretical. One venue, eleven days old, is out-earning Ethereum mainnet fifteenfold.

The rotation context makes the timing sharper. In a market where everything outside Bitcoin and Ethereum lost roughly 23 percent in six months, capital has crowded toward the handful of assets with verifiable revenue: perpetuals venues, stablecoin issuers, and now, abruptly, the largest DEX. The same repricing logic runs through the stablecoin wars, where volume quality has become the scoreboard, a shift crypto.news examined in the USDC-Tether flippening, and through Ethereum itself, which is rebuilding its entire execution roadmap around being credible settlement infrastructure for exactly this kind of institutional flow, the project crypto.news detailed in the Lean rebuild. UNI’s real revenue moment is one instance of a sector-wide migration from narrative to cash flow.

The comparables: what a fee-earning DEX token is worth

The rotation to cash flow gives UNI a peer group for the first time, and the comparisons cut in both directions.

The flattering comparison is to the fee leaders UNI just passed. Hyperliquid, Pump.fun, and the perpetuals venues built the template of the past two years: tokens with direct revenue linkage, aggressive buyback or burn mechanics, and valuations that survived the altcoin drawdown better than the governance-token cohort precisely because holders could point at income. Adams’ framing, more daily fees than anything except USDC and USDT, deliberately places Uniswap atop that leaderboard. On raw multiples, a 2 billion dollar capitalization against 20.1 million dollars in weekly gross fees puts the protocol at roughly two times annualized gross fees, a figure that looks absurd against any traditional exchange until the LP share is subtracted, at which point the multiple on actual protocol take becomes very large and entirely dependent on the pending votes. The valuation case is therefore not that UNI is cheap on current protocol revenue. It is that governance controls a dial connected to a gross fee stream of unprecedented size, and the July votes are the market’s first chance to watch the dial turn on the newest and largest sources.

The unflattering comparison is to the treasury-heavy tokens whose burns never outran their supply overhangs. UNI carries a circulating supply near 630 million against a total of 1 billion, with treasury and team allocations that dwarf any plausible near-term burn rate. At the current protocol take, the burn is symbolic; even at meaningfully higher fee capture, supply destruction measured in tens of millions of dollars annually meets a token with hundreds of millions of units yet to circulate. The burn thesis is a direction, not a floor, and direction gets repriced quickly when the underlying volume proves cyclical. The December UNIfication rally faded within weeks for exactly that reason: mechanics without volume are a press release. What is different now is that the volume arrived, from a source nobody’s model included, which is why the token’s 21 percent July move happened on the news of usage, not the news of tokenomics.

There is one more comparable worth naming because it frames the strategic stakes: the launch chain itself. Robinhood Chain’s opening fortnight has minted its own equity narrative, with HOOD shares up more than 40 percent in a month and insiders selling into the enthusiasm, and the network’s headline metrics, hundreds of millions in early volume against liquidity measured in the low tens of millions, drew immediate scrutiny about depth and durability. The tokenization trade rewards networks that convert launch attention into recurring activity, the pattern that has kept capital concentrated in venues with verifiable usage, as crypto.news observed when tokenized assets drove a rival network to record throughput. Uniswap is the venue where those questions get answered in public, block by hundred-millisecond block, because it is where the trades actually clear.

Objection one: subsidized volume is not revenue

The skeptics’ first argument is about the quality of the 500 million dollars, and it is not hand-waving.

Robinhood is waiving gas fees on the chain for the first 90 days. Zero gas removes the single largest natural brake on wash trading, incentive farming, and volume inflation; when round trips cost nothing, volume statistics measure enthusiasm for free transactions as much as demand for the assets traded. Analysts made exactly this objection in the launch week, noting that enormous AMM volume does not automatically create value for UNI without activated fee capture, and that if a meaningful share of the headline number reflects farming, the late-September expiry of the gas subsidy becomes the first genuine stress test of the entire thesis. The launch-week TVL data reinforces the concentration worry: a single Ethena deposit produced most of the day’s growth, and liquidity that arrives in one transaction can leave in one.

The honest response is that swap fees, unlike gas, were never waived. Every dollar of the 4.38 million in daily Robinhood Chain fees was paid by traders to liquidity providers at market rates, which makes the fee number a harder signal than raw volume. Wash trading a pool with a 30 basis point fee costs 60 basis points per round trip; nobody launders volume at that price for long. But the composition question survives the rebuttal: how much of the activity is durable tokenized-equity demand from Robinhood’s international base, and how much is launch-window speculation in memecoins and farmed incentives? The September subsidy cliff will answer it empirically. Until then, annualizing an eleven-day-old fee run rate is exactly the kind of extrapolation that DeFi cycles exist to punish.

There is also a counterparty concentration risk that has no precedent in Uniswap’s history: the protocol’s second largest venue is controlled by a publicly traded brokerage with its own regulatory exposure, its own commercial incentives, and, eventually, its own ability to route order flow elsewhere or deploy a competing AMM. Uniswap earned its position on Robinhood Chain by being the best liquidity software available on day one. Nothing guarantees the position is permanent, and the SEC’s January guidance flagging tokenized equity products for scrutiny means the flagship use case operates under a regulatory question mark of its own.

Objection two: the fee switch taxes the people who make the venue work

The second objection comes from inside the machine, and it is the oldest tension in the protocol’s design. Every dollar routed to the burn is a dollar that no longer goes to liquidity providers, the capital that actually fills the pools traders swap against.

Panoptic founder Guillaume Lambert put the LP case bluntly during the v4 vote, warning that applying the fee switch to v4 leaves providers with nowhere to migrate except competing AMMs or Uniswap forks, and that the proposal risks killing the protocol by favoring token holders over the capital that makes it function. The v4 version of the proposal sharpens his point, since reports around the vote indicated LP economics on affected pools could be reduced by as much as a third relative to the status quo. Liquidity is the most mercenary capital in crypto; it moved for 50 basis points of incentives throughout DeFi summer, and a protocol that taxes it while competitors do not is running a live experiment in how much brand and routing dominance are worth.

The bull rebuttal rests on what LPs actually get in exchange. Uniswap’s aggregated depth, its integration surface, the API now embedded in MetaMask, Zerion, and OKX routing across 18 plus chains with more than 3,000 developer keys issued, and now the Robinhood flow itself all mean an LP on Uniswap sees order flow that no fork can replicate. A fork with zero protocol fee but a fraction of the volume pays LPs less in absolute terms than Uniswap does after the tax. That was the empirical result of the vampire-attack era, and the UNIfication rollout across 11 chains has so far produced no measurable LP exodus. But v4 raises the stakes because hooks make pools programmable, and programmable pools are easier to replicate elsewhere; the fee controller architecture being voted on will tax precisely the segment of liquidity most capable of leaving. The vote closing July 12 and the on-chain sequence in the following week are, in effect, governance pricing that migration risk in real time.

The third mechanism: fee discount auctions

Alongside the burn expansion, Uniswap quietly shipped a second monetization primitive in the same week, and it deserves attention because it answers the LP objection from an unexpected angle.

Protocol Fee Discount Auctions, rolled out for the first time in early July, let sophisticated participants bid for reduced protocol fees on specific flow. The design logic runs like this: the largest source of LP pain in an AMM is not the protocol fee but adverse selection, the losses providers take when arbitrageurs pick off stale prices faster than pools can update. Auctioning fee discounts to the searchers and market makers who generate that flow converts a pure extraction into a priced privilege, captures for the protocol some of the value that MEV bots previously kept entirely, and gives high-volume participants a reason to route through Uniswap even after the fee switch activates. It is, in effect, a mechanism for taxing the taxers.

The auctions matter to the cash flow thesis for two reasons. First, they diversify protocol revenue beyond the flat fee share, adding a component that scales with the competitiveness of order flow, not raw volume, which is more durable through volume downturns. Second, they are a structural answer to Lambert’s migration warning: if the auction design succeeds in reducing the toxic share of flow that LPs absorb, providers could end up better off under the taxed regime than the untaxed one, because their gross fee cut shrinks while their adverse selection losses shrink faster. That claim is unproven and the mechanism is days old, but it reframes the fee switch debate from a zero-sum split between holders and LPs into an engineering question about who pays for price discovery. The December governance package, the v4 fee architecture, and the auctions together read as a coherent program: convert every form of value the protocol creates, swap fees, flow priority, and MEV, into revenue, then convert revenue into supply reduction.

The program’s ambition invites one more skeptical note. Every additional mechanism is additional surface area for governance capture, parameter mistakes, and the slow bureaucratization that has damaged other DAOs. A protocol that once had a single immutable design now has fee policies, adapters, controllers, auctions, and an expedited voting track, each a dial someone can turn. The bet is that Uniswap Labs and the delegate ecosystem can operate a genuinely complicated fiscal machine better than competitors can copy a simple one. The early revenue data supports the bet. The history of DeFi governance urges keeping the champagne corked.

What the UNI repricing actually requires

Assembling the pieces, the cash flow thesis for UNI needs four things to stay true simultaneously, and each has a visible checkpoint.

The votes must pass. The snapshot for v4 fees closed July 12; on-chain votes run the week of July 13; the Robinhood Chain temperature check closes July 15. The December UNIfication vote passed with near-unanimity, so the base case is passage, but the LP backlash around v4 is the loudest internal opposition the program has faced, and a diluted compromise on fee rates would proportionally dilute the burn.

The volume must survive September. The gas subsidy expires roughly 90 days after the July 1 launch. Fee revenue that persists through the cliff is real demand for tokenized equities and on-chain trading; fee revenue that evaporates was a marketing expense on Robinhood’s income statement. This is the single most informative scheduled event in the entire thesis.

The burn must be visible at scale. TokenJar mechanics mean supply reduction tracks protocol fee accrual with a lag. Watching claimed-and-burned totals over the coming quarter, rather than gross fee headlines, measures the machine’s actual throughput, and the gap between 5.2 million dollars gross and 73,454 dollars of current protocol take is the distance the switch still has to travel.

And the regulatory perimeter must hold. Tokenized equities traded by a global retail base through a brokerage’s chain sit at the intersection of securities law, the pending market structure bill, and the SEC’s tokenization scrutiny. The same institutional wave lifting fee revenue is also pulling DeFi into fights it has historically avoided, including the yield and revenue-sharing battles that banks are waging against crypto’s cash-flowing products, a conflict crypto.news has covered at the stablecoin layer. A token whose value accrues from fee capture is a token whose classification arguments get harder, not easier, which is presumably why the burn was engineered as supply destruction rather than distribution in the first place.

The remarkable thing about the past two weeks is not the volume record or even the fee record. It is that the oldest criticism of the largest DEX, that the token captures nothing, is being retired by governance vote in the same fortnight that the largest new fee source in DeFi history came online. Whether UNI at 3.63 dollars is cheap depends on September’s subsidy cliff, next week’s on-chain votes, and how much of a brokerage’s retail flow proves durable. Whether UNI is finally a claim on something is, for the first time since 2020, no longer the question.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

EU crypto compliance is entering a potentially turbulent phase after the Markets in Crypto-Assets Regulation (MiCA) transitional period ended on July 1, pushing more businesses—and more customers—into the post-transition licensing environment. Bruna Szego, chair of the EU’s anti–money laundering authority AMLA, warned that a wave of user migration could create operational and compliance strain for virtual asset service providers (VASPs) across the bloc.

Speaking during a briefing with the European Parliament’s Committee on Economic and Monetary Affairs on Wednesday, Szego said providers should expect pressure as customers “rush to withdraw” and as licensed firms take on new users. Her comments underline a key risk for the next stage of EU crypto supervision: whether firms can keep anti–money laundering controls effective while business models and customer flows shift quickly.

Key takeaways

- AMLA chair Bruna Szego warned that end-of-transition customer movement could intensify operational and compliance pressure on EU crypto VASPs.

- As MiCA’s transitional period ended on July 1, firms that are not properly authorized were expected to wind down EU activities “immediately,” per ESMA guidance.

- AMLA has advised both licensed providers onboarding new customers and firms winding down to keep anti–money laundering controls functional through the transition period.

- AMLA says it will publish a report before year-end assessing money laundering risks and supervisory practices, including differences between EU member states.

- The authority is also expanding its blockchain analytics capabilities to strengthen oversight of crypto-asset service providers.

Why MiCA’s transition ending raises compliance stress

MiCA’s transitional period was designed to give the market time to adapt to a new regulatory framework. But with the clock now fully expired, Szego suggested the change could trigger behavior that compliance departments may not be able to absorb smoothly at scale.

In her remarks, she focused on two pressure points. First, entities winding down their EU operations may face customer withdrawal surges, which can strain internal processes and monitoring systems. Second, licensed crypto firms that remain active under MiCA may see onboarding volumes increase as they absorb users migrating away from less-compliant platforms.

The practical implication is straightforward: even if firms are formally compliant, rapid customer migration can still challenge the day-to-day execution of know-your-customer and transaction monitoring controls—especially if migration happens faster than expected.

AMLA’s advisory note and the compliance balancing act

Ahead of the July 1 deadline, AMLA published an advisory note highlighting money laundering risks linked to the end of the transitional period. According to the advisory guidance, firms should take targeted steps depending on where they sit in the transition—either scaling down EU activities or onboarding customers within the licensed perimeter.

Szego emphasized that AMLA expects providers to maintain efficient compliance procedures during the transition rather than treating the changeover as a mere administrative milestone. For winding-down firms, the focus is on ensuring controls do not degrade during periods of change. For licensed providers, the concern is that adding customers rapidly should not dilute anti-money laundering safeguards.

AMLA’s positioning also suggests a supervisory priority: AMLA is effectively drawing attention to “transition risk”—the idea that business continuity and compliance discipline can be hardest during periods of structural adjustment.

ESMA’s wind-down expectation after the deadline

MiCA’s end-state requirement is that crypto asset service providers must be licensed to keep serving EU customers after the transitional period. The deadline was paired with expectations for what unauthorized providers must do next.

Cointelegraph previously reported on the July 1 transition ending, citing ESMA’s view that service providers still not authorized by then must take “immediate” steps to wind down their EU activities. That regulatory posture matters for Szego’s concern because wind-down periods can produce concentrated customer actions—such as withdrawals—that may test operational readiness.

In other words, even if the licensing rule is clear on paper, the market’s adjustment phase can create real-world friction points that AMLA intends to monitor closely.

What AMLA plans to publish—and what to watch next

AMLA chair Bruna Szego said the authority will publish a report before the end of the year covering money laundering risks in the crypto sector and describing supervisory practices across the EU. She added that AMLA is expanding blockchain analytics capabilities to improve its ability to oversee crypto-asset service providers.

The report is also expected to assess how national authorities supervise crypto-asset service providers and highlight differences in supervisory approaches across member states. For market participants, this matters because uneven enforcement can translate into uneven compliance expectations and timelines—particularly during periods of rapid migration and customer churn.

Szego indicated AMLA intends to use the findings to coordinate follow-up work with national regulators where needed, aiming for more consistent anti-money laundering oversight throughout the bloc.

For investors, traders, and users, the main question for the coming months is whether licensed platforms can maintain strong onboarding and monitoring standards as they absorb new customers—and whether winding-down firms can handle withdrawal waves without compliance controls becoming secondary. AMLA’s year-end assessment and its growing analytics focus will likely determine how regulators refine expectations for the post-transition phase.

Welcome to The Protocol, CoinDesk’s tech newsletter covering the most important stories in blockchain. I’m Margaux Nijkerk, a reporter at CoinDesk.

We’re giving you a deeper look at the biggest trends, breakthroughs and debates shaping blockchain technology each week.

This week, we’re unpacking the timeline of all the changes at the Ethereum Foundation since the year began.

Crypto World

Open USD poses new threat to Circle by challenging USDC’s core business model, CoinShares says

USDC’s circulating supply has fallen to about $73 billion from nearly $80 billion in March, trimming its share of the roughly $312 billion stablecoin market as competition from newly regulated issuers intensifies.

Circle shares fell more than 17% on the day Open USD was announced, though CoinShares said the decline was likely amplified by technical selling linked to the Russell index reconstitution.

Still, the report argued the market may be overreacting. Open USD has yet to launch, important details remain unresolved and Circle retains a significant advantage through USDC’s deep liquidity and years of integrations across exchanges, DeFi and payments.

Open USD is unlikely to pose a major threat to Tether, whose dominance in emerging markets and offshore dollar liquidity gives USDT, the largest stablecoin by far, a different competitive moat, the report added.

For now, investors should watch whether Circle changes its distribution strategy and whether Open USD can convert its high-profile backing into adoption, CoinShares said. Until then, the project remains a credible, but unproven, challenge to USDC.

CoinShares is not alone in noting the challenge posed by Open USD. Japanese investment bank Mizuho downgraded Circle to underperform from neutral and slashed its price target to $50 from $85 in a note to clients on Tuesday, arguing that the new rival’s business model threatens the stablecoin issuer’s long-term economics.

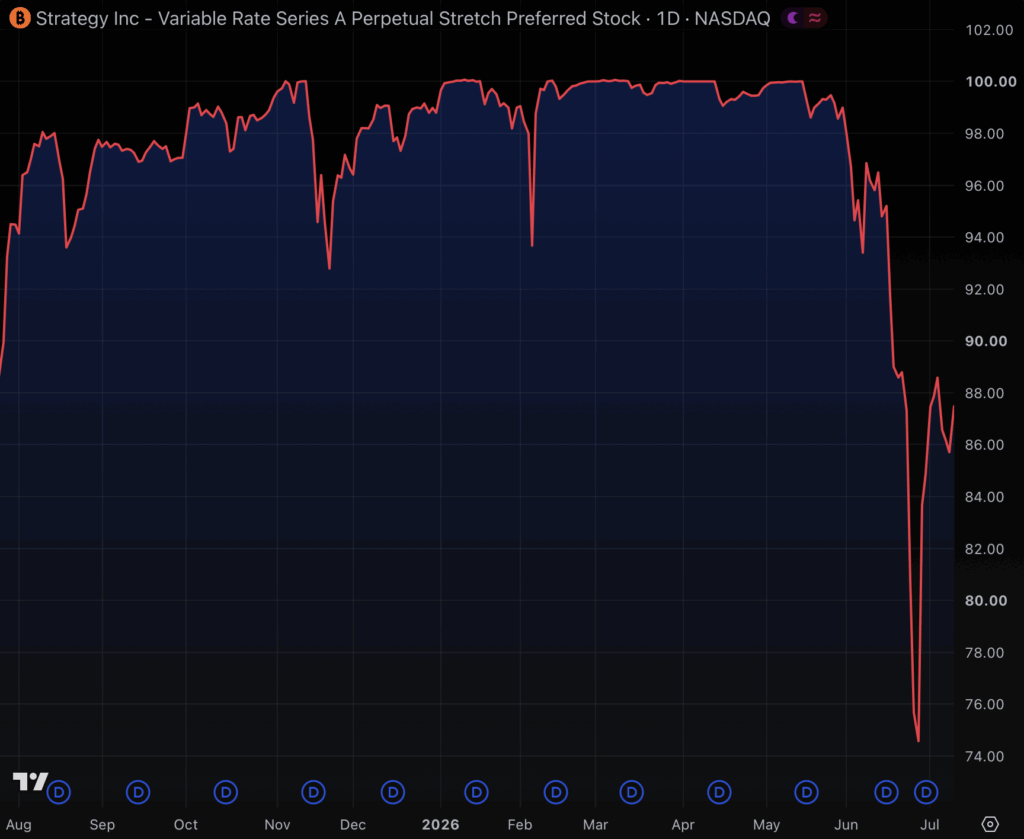

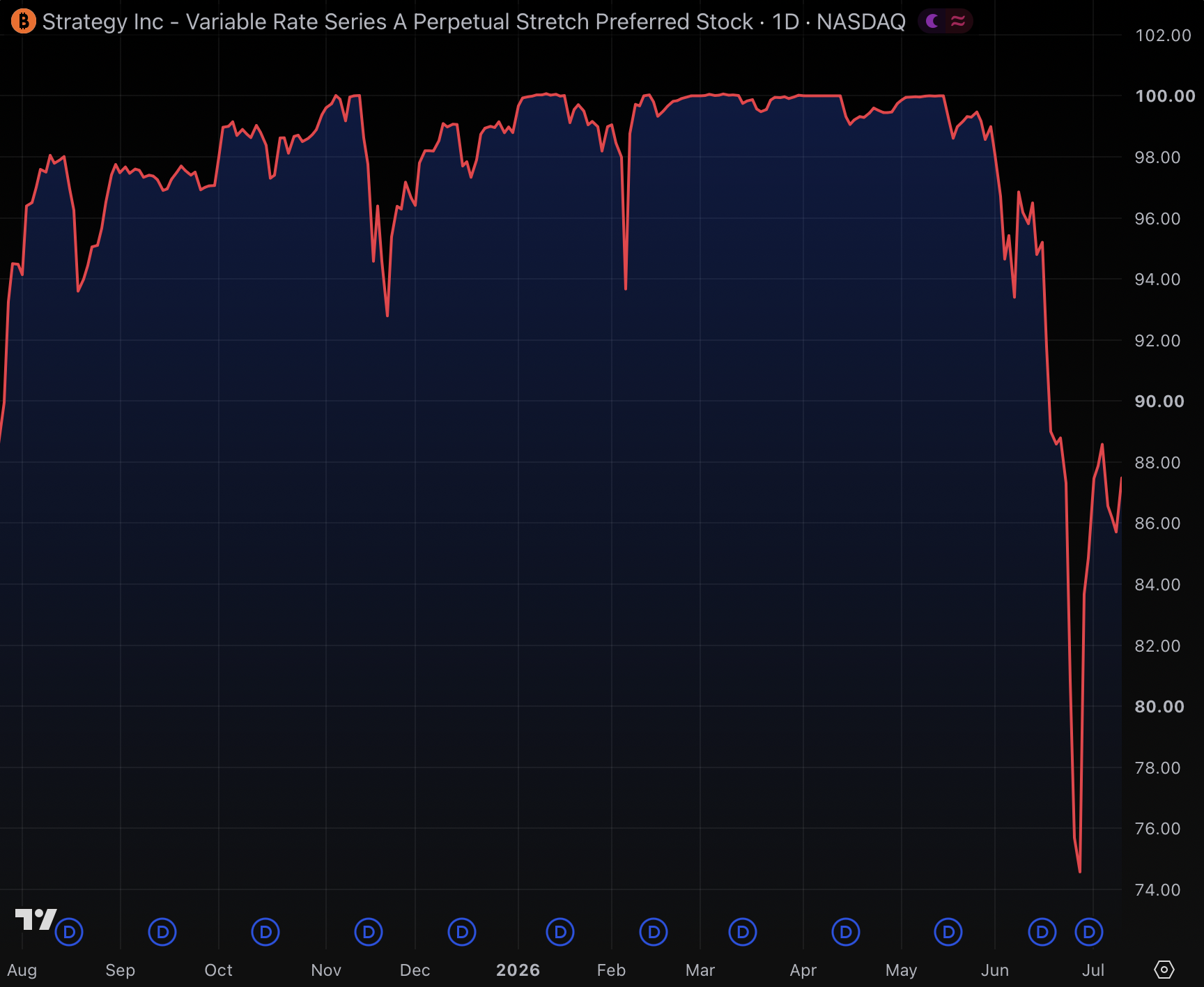

Following Michael Saylor’s advertisements likening STRC to a high-yield bank account or money market, Strive swapped $50 million of the cash it had in March for STRC, and soon added another $500,000.

As of a new filing, the asset manager quietly disclosed that its shares were worth just $44.18 million as of July 10, a paper loss of roughly $6.3 million excluding dividends.

Although it published a glowing press release about its purchase, the admission of loss sat otherwise unannounced in an SEC filing, tucked between cash and BTC balances.

Unlike the purchase, no press campaign trumpeted the loss.

The instrument that Strive pitched as a cash-like hold has lost about 12% of its value relative to cash, and the dividends it received from holding STRC came nowhere close to closing that gap.

Strive used over a third of its cash holdings at the time for its STRC purchase.

What Strive said it was buying

CEO Matt Cole, who serves at Strive after years managing money at the California pension giant CalPERS, initially sold the trade as prudent treasury management.

Incredibly, he claimed at the time that Strive opted for STRC “instead of holding idle cash earning low yields in money market funds.”

Although STRC is nothing like a money market and has, in fact, lost 28% of its value at its June 26 low, Strive initially claimed that STRC would “provide strong yield dynamics while maintaining stable price behavior.”

Obviously, it hasn’t.

Unlike a bank account or money market, STRC fluctuates in price daily on the Nasdaq stock exchange. Strategy says it should trade close to its $100 par value due to its fine-tuning of dividend rates, a dubious mechanism Protos has documented at length.

Strive even counted its STRC shares toward its own so-called “reserve” backing dividends on its competing product, SATA, another quasi-stable, dividend-paying stock.

Unlike an insured savings product, neither STRC nor SATA offer guarantees to preserve principal, offer deposit insurance, nor provide rights to redeem at par from the company.

Whatever a Nasdaq trader will pay is what the shares are actually worth.

Read more: No amount of cash can fix STRC’s trust problem

Strive starts wishing it had just held cash

Strive’s $5.8 million unrealized loss on its $50 million purchase actually understates the extent to which it bet went poorly.

To be precise, the company bought 500,000 shares at STRC’s full $100 par in March. It never bothered to bid for a discount — a mistake that cost it dearly.

Sometime before April 2, Strive quietly added about 5,000 more shares. The extra stake was worth roughly $500,000, lifting the true outlay to about $50.5 million. Indeed, its April 6 filing pegged its holdings at $50.5 million.

From there, STRC began to drift lower, soon collapsing into free fall and shedding roughly a quarter of its value within two weeks.

As leverage unwound and prices of every BTC treasury company collapsed alongside the asset itself, STRC bottomed at an all-time low of $71.25 on June 26.

At that price, Strive’s 505,000 shares were worth $36 million. That is, in other words, a hole of more than $14 million against the $50.5 million it once held.

After negative $14 million, negative $6 million is less worse

As of July 10, the price of STRC had “recovered” to make Strive’s $14 million unrealized loss “only” roughly negative $6 million.

That volatility and commensurate risk is sadly comparable to the cost of doing nothing with all of its $50.5 million initial cash position.

Measured against Strive’s $50.5 million cost basis, the company’s unrealized loss excluding dividends is roughly $6.3 million, or 12.5%.

Strive’s loss stood at about $1.8 million, or 3.7%, when Protos checked in early June.

The numbers are now more than three times as bad.

Dividends haven’t made up for STRC’s crash

To be fair, STRC has paid dividends along the way, so those payments have softened the blow ever so slightly.

Over Strive’s holding period since March, STRC’s annualized dividend rate has been close to 11.5%, and Strive has been holding long enough to collect 4.5 months worth of dividends.

In other words, it’s received roughly 4.4% on its principal — still far from enough to recover from its 12.5% unrealized loss on the lower value of its shares.

Even after adjusting for dividends received, Strive had still lost over $4 million holding STRC versus simply holding cash as of July 10. STRC closed yesterday a mere 1% higher than July 10, so updating the math to current prices would barely budge.

In summary, Strive’s failed swap of cash for STRC is simply a consequence of believing advertisements from Strategy and its founder. Strategy’s own BTC treasury is deeply underwater to the tune of billions of dollars, and STRC’s slide reflects doubt that Strategy can sustain the stock anywhere close to $100 per share

Companies holding STRC and Strategy’s other securities have paid the price.

Strive told shareholders STRC would be better to hold than idle cash. Idle cash, it turns out, would have at least maintained its dollar value.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

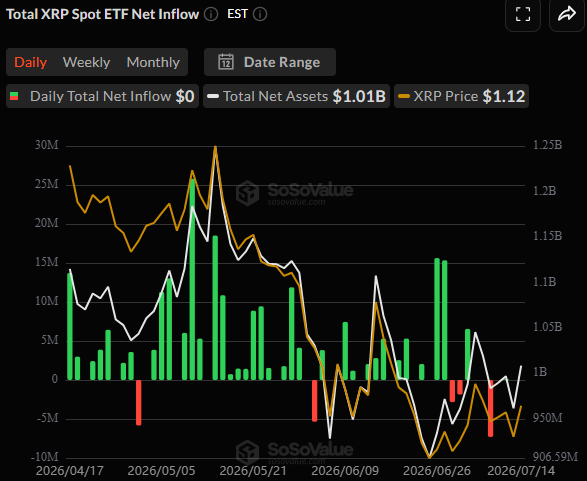

The company behind the popular cryptocurrency XRP has been quite active lately, announcing strategic partnerships and unveiling interesting initiatives.

The token remains the subject of numerous price predictions, with analysts split between ultra bulls and those calling for a brutal crash in the near future.

All the Latest Stuff

On July 4th, the USA celebrated its 250th Independence Day, and Ripple joined the festivities. The company teamed up with a nonprofit dedicated to helping unemployed veterans find high-quality jobs after service. The mission is to assist 200,000 people by 2030, with Ripple matching donations up to $10,000. Earlier today, the firm announced that 25 veterans have been selected to receive a $10K grant.

Another recent development also shows Ripple’s growing presence outside traditional crypto initiatives. It joined the x402 Foundation as a premier member alongside Coinbase and Circle.

The project focuses on building open-source standards for AI-powered payments, allowing agents to send, receive, and verify transactions across various networks. Speaking on the collaboration was Markus Infranger, senior vice president of RippleX, who said:

“Open standards like x402 help lay the foundation for trusted, interoperable machine-to-machine payments.”

Other major Ripple achievements as of late include its full authorization as a Crypto Asset Service Provider (CASP) in the European Union and the company’s marketing partnership with the Kansas Jayhawks.

The ETFs Lose Momentum

The launch of the first spot XRP ETF in the US, with 100% exposure to the asset, was a long-awaited event and was expected to increase interest in the token. This became reality in November 2025 when Canary Capital introduced its product, while Bitwise, Franklin Templeton, 21Shares, and Grayscale followed suit shortly after.

The financial vehicles were indeed met with great investor enthusiasm, and for many months inflows consistently exceeded outflows. However, there was a sudden turn towards the end of June, and the red days started popping up.

This indicates that conservative investors, such as pension funds and hedge funds, have started reducing their exposure to XRP, which can negatively impact its price. Data from last week shows that the multi-month green-only streak was finally broken, with over $7 million leaving the funds.

XRP Price Outlook

As of press time, the asset trades at around $1.11, representing a 3% increase on a daily scale. Recall that the entire crypto market headed north on July 14 after news that US inflation came in lower than expected.

Crypto X is rammed with analysts who, despite the recent volatility and overall weakness, keep calling for new all-time highs. Among them are Crypto Patel, envisioning an explosion to $9, and Celal Kucuker, projecting a possible rise to $7 later this year.

The bears, though, also have their strong arguments. X user Diana noted that XRP recently briefly lost the $1.08 support, which could trigger a short-term sell-off to as low as $0.87.

The post Ripple (XRP) News Today: July 15 appeared first on CryptoPotato.

Bitcoin is trading near $64,700, up about 4% over the past day after rebounding from an ETF-driven selloff. The latest Bitcoin price prediction now hinges on whether buyers can defend key support levels. The drop briefly pushed BTC below $63,000 and wiped out nearly $1 billion in leveraged positions. Even so, Bitwise Asset Management still views the correction as a setup rather than a breakdown.

Bitwise’s Q3 2026 Crypto Market Review lays out the damage before making its bullish case. Bitcoin fell 13.4% in Q2 and remains 32.9% lower year to date. It also sits roughly 49% below its October peak near $126,000. Meanwhile, U.S. spot Bitcoin ETPs lost $4.9 billion in Q2, marking their weakest quarter since launching in January 2024.

CIO Matt Hougan summed up the mood, saying crypto sentiment is the worst he has seen in eight years. That is hardly a party invitation.

— Coin Bureau (@coinbureau) June 16, 2026

BITWISE: BITCOIN’S BOTTOM IS THE WRONG QUESTION

BITWISE: BITCOIN’S BOTTOM IS THE WRONG QUESTION

Bitwise CIO Matt Hougan says long-term investors should focus on where the cycle could TOP, not whether Bitcoin has already BOTTOMED. pic.twitter.com/MMoZ0djfcl

Still, Bitcoin price prediction has held up better than many major cryptocurrencies. Its 32.9% decline remains smaller than Ethereum’s 46.9%, Solana’s 40.6%, and Cardano’s 56.5%. At the same time, Bitcoin dominance has climbed to 64.2% as investors continue favoring the market leader.

ETF flows have also started turning positive again after the heavy Q2 outflows. That shift offers bulls something to cheer, although it is still too early to call victory. The real question is whether fresh demand can build a lasting floor or if this rebound is simply a pit stop before the next move.

Discover: The Best Crypto to Diversify Your Portfolio

Bitcoin Price Prediction: Reclaim $65,000 or Is a Retest of $57K Still in Play?

Bitcoin’s technical picture remains complicated after a confirmed bearish breakdown from a multi-month symmetrical triangle, a pattern TradingView analysts viewed as a structural shift rather than routine volatility. The move triggered roughly $780 million in long liquidations before buyers stepped in around the $60,000 level. That support now remains the key level for bulls to defend.

Bitcoin now trades around $64,600 to $64,800 across major exchanges after rebounding sharply from Tuesday’s low of $62,271.9. The 52-week low remains $57,832.5. Former triangle support has flipped into resistance near the mid $60,000 region, making a decisive break above that zone essential to invalidate the bearish setup.

Three scenarios remain in play. The bullish case sees stronger ETF inflows helping Bitcoin reclaim the mid $60,000 resistance area, opening a move toward $70,000 and eventually previous highs. The base case keeps price ranging between $60,000 and $65,000 as macro data and Federal Reserve guidance temper institutional appetite while ETF demand stays steady.

The bearish scenario emerges if Bitcoin closes below $60,000 on a daily basis. That would expose the high $50,000 region again, with $57,832.5 acting as the next significant technical support. Bitwise’s view that the recent weakness represents an accumulation opportunity carries credibility because of its ETF expertise. However, its position as an ETF issuer also creates an incentive to present pullbacks constructively.

Several catalysts could determine Bitcoin’s next major move. Daily U.S. spot ETF flows, upcoming inflation data, and Federal Reserve commentary remain the most important near-term drivers. Although longer-term Bitcoin price models continue pointing higher, the current technical setup still favors patience over aggressive positioning.

Trade Bitcoin on Bybit and Don’t Miss Out on Our $1,000 USDT Airdrop

Bitcoin Hyper Eyes Early-Mover Upside While Spot BTC Tests Key Support

Bitcoin at $62,000 is still 52% off its all-time high. Even in a recovery scenario, the asymmetric upside from here is measured in percentages, not multiples. Traders looking for higher-beta exposure within the Bitcoin ecosystem have been rotating toward infrastructure plays that sit a layer above BTC’s base-layer constraints, specifically, Layer 2 solutions that add programmability without sacrificing Bitcoin’s security model.

Bitcoin Hyper is positioning directly in that gap. The project claims to be the first Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, targeting sub-Solana latency while inheriting Bitcoin’s trust mode. It’s a technically ambitious combination if the architecture delivers.

The presale has raised close to $33 million at a current token price of $0.0136831, with staking live and attracting capital ahead of any exchange listing. Features include a Decentralized Canonical Bridge for native BTC transfers, low-cost execution, and the SVM layer enabling fast smart contract deployment on Bitcoin rails.

Research Bitcoin Hyper’s presale terms before committing capital.

For broader context on where Bitcoin price analysis stands heading into Q3, this breakdown of BTC’s key technical levels is worth the read.

Discover: The Best Token Presales

The post Bitcoin Price Prediction: ETF Bouncing, Bitwise Sees Bottom and Huge Adoption appeared first on Cryptonews.

A 20-year-old man who suffered significant losses after following the advice of a South Korean investment YouTuber has allegedly stabbed the man in an act of revenge. The July 13 attack coincided with a 9% crash in the South Korean stock market — its seventh-largest dip on record.

The Chosun Daily reports that police arrested the man, known only as “Mr A,” on Tuesday on suspicion of attempted murder after he travelled to Busan’s Nam District and stabbed the victim — known as “Mr B” — multiple times in the face.

Mr A reportedly subscribed to a YouTube channel run by 40-year-old Mr B, and structured his investments based on his recommendations.

However, the investments caused Mr A to suffer significant losses.

This all took place as South Korea’s stock market, the KOSPI, was in the midst of a 9% nosedive.

Stocks representing AI giant SK Hynix and Samsung Electronics fell by 15.4% and 10.7%. Indeed, SK Hynix wiped out the gains it had made from its US debut last week.

Read more: These crypto chains raised $500M but generate just $360 in daily fees

As the price fell, Bull Theory reported that the leveraged retail accounts of 1.2 million Koreans triggered margin calls on July 13.

“Between 320,000 and 360,000 of them were fully liquidated by brokers, principal wiped out, and some now owe money to their brokerage,” it said.

It’s unclear what stocks Mr A invested in, and when the investments took place, but police in South Korea are reportedly preparing to probe the investor further to determine his alleged motives before seeking a warrant.

Mr B’s injuries are reported to be no longer life threatening.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

South Korea is preparing a major overhaul of how the government manages “state assets,” including digital assets and intellectual property, as part of efforts to modernize public-sector finance. The Ministry of Economy and Finance (MOEF) says it plans to replace the State Property Act—dating back to 1950—with a new National Asset Basic Act, using a broader definition of what qualifies as state-owned value.

Officials also reiterated plans to test the tokenization of government bonds on a blockchain as early as a 2027 pilot, with an eye toward reducing transaction friction. Beyond securities, the ministry said it will examine tokenizing state-owned real estate to widen retail participation and share a portion of the generated returns with the public.

Key takeaways

- MOEF is moving toward a new National Asset Basic Act to modernize public asset management and expand the legal definition to cover digital assets and intellectual property.

- The government bond tokenization plan is targeted for a 2027 pilot, framed as a way to streamline transactions.

- South Korea is also considering tokenized real-estate models designed to attract retail users and share returns.

- Separately, Seoul’s 2026 growth strategy includes a study period aimed at connecting tokenized government bonds with the Bank of Korea’s CBDC infrastructure.

- Upcoming legal changes to tokenized securities frameworks are scheduled to take full effect in early 2027, with blockchain-ledgers recognized as valid securities registries.

Replacing a decades-old asset framework

MOEF’s proposal centers on updating the legal structure for state asset management. According to the ministry, the National Asset Basic Act is intended to shift policy from a legacy approach—historically focused on tangible, real-estate-heavy state property—toward a framework centered on value creation.

The MOEF briefing held at the President’s Blue House on Wednesday emphasized that the reform would explicitly bring digital assets and intellectual property into the umbrella of state assets. The ministry linked this to a broader modernization goal: aligning the governance of government-held resources with how value is increasingly stored, transferred, and monetized in digital form.

For market participants, the significance is twofold. First, clearer legal coverage can reduce uncertainty around how non-traditional assets may be handled in government programs or public investment strategies. Second, it sets a policy foundation that can support later pilot initiatives—such as bond and real-estate tokenization—without relying on narrow interpretations of older statutes.

Tokenized government bonds and the push toward a “blockchain economy”

Regulatory and infrastructure plans are converging around tokenized government debt. Earlier coverage noted that South Korea’s government unveiled a 2026 Economic Growth Strategy for the second half, which includes a 2027 pilot intended to link tokenized government bonds to central bank digital currency (CBDC) infrastructure. As described in the government strategy, authorities plan to study how to make the Bank of Korea’s (BOK) CBDC system interoperable with other blockchains.

The interoperability concept was first publicly discussed on July 1, when BOK Governor Hyun Song Shin outlined the idea at the European Central Bank Forum on Central Banking. Building on that, the latest strategy positions the research and pilot work as part of a broader effort to develop a “blockchain economy.”

In practice, this matters because interoperability between a CBDC infrastructure layer and public or permissioned blockchain networks can affect how tokenized instruments are issued, transferred, and settled. A pilot that tests that connection in the context of government bonds—an asset class that is typically central to liquidity and price discovery—could serve as a benchmark for future tokenized issuance across other sectors.

From pilots to legal recognition for tokenized securities

South Korea’s push for tokenization is not only about infrastructure; it is also about legal status. The MOEF previously announced a pilot using tokenized deposits to execute government operational spending, with a full rollout planned for the fourth quarter of 2026. That initiative reflects a wider pattern: tokenized rails are being tested in day-to-day state functions before scaling.

Separately, changes to South Korea’s Capital Markets Act and Electronic Securities Act—designed to support the country’s early tokenized securities framework—are scheduled to take full effect on Feb. 4, 2027. The reforms aim to legally recognize blockchain-ledgers as valid securities registries.

Officials say this would bring tokenized assets under the Financial Services Commission’s jurisdiction, moving them out of a purely experimental stage. For investors, that shift is particularly important: securities registration is a core component of custody, ownership tracking, and compliance. Legal recognition of blockchain-ledgers as registries can improve clarity around operational responsibilities and investor protections, although the practical impact will depend on how regulators implement standards and supervision.

Tokenizing state real estate for retail access

Alongside the bond and CBDC-related work, MOEF is exploring tokenization of state-owned real estate. The stated goal is to encourage retail participation and share part of the returns generated from these assets with the public.

While the proposal is framed as an area for further exploration rather than a fully specified rollout, it fits the broader theme of shifting government asset management toward models that can potentially broaden access and reduce barriers to entry. Real estate has historically been difficult for retail investors to access at scale due to high capital requirements and complex transaction processes. Tokenization, at least in theory, could address parts of that problem by enabling smaller ownership units and faster transfer mechanisms.

Still, major details typically determine whether tokenized real estate becomes commercially viable—such as custody arrangements, investor suitability rules, valuation practices, and the regulatory treatment of tokenized property rights. Until those elements are clarified, the move should be viewed as a policy direction that may shape future pilots and rulemaking.

Looking ahead, investors and builders should watch for how MOEF’s National Asset Basic Act language translates into implementation, particularly regarding digital asset classification and governance. The 2026 strategy’s 2027 CBDC interoperability and the Feb. 4, 2027 legal changes to securities registries are likely to be the clearest near-term signals of how quickly tokenization can move from pilots into regulated, scalable markets.

Ethereum price is heating up as it pounces higher above $1,850, gaining more than 5% over the past day. The $2,000 level is finally back in view, although that ceiling has humbled plenty of eager bulls before. The setup looks encouraging, but resistance is still looming.

The Ethereum Foundation has spun out a new entity called EthSystems. Its mission is to build technology and consulting services that help institutions operate on Ethereum while keeping transactions confidential. That targets one of the biggest hurdles for traditional finance, where privacy expectations often clash with public blockchain transparency.

Moving the project outside the Foundation also changes the narrative. Instead of treating privacy tools as research, Ethereum is packaging them as enterprise-ready infrastructure. If institutions gain confidence in deploying on-chain, that could support long-term network activity and, eventually, ETH demand.

Meanwhile, the market has offered a helping hand. Capital has rotated back into major smart contract platforms, giving Ethereum price room to recover after weeks of hesitation. Still, the real test sits near $2,000.

Discover: The Best Token Presales

Can Ethereum Price Hit $2,000 This Week?

Ethereum price is technically constructive as it has broken above the $1,845 to $1,865 resistance zone. The next key hurdle sits around $1,975 to $2,000, where sellers may finally wake up. Trading activity also backs the move, with 24-hour volume approaching $14 billion instead of a quiet climb.

The bullish path stays intact if ETH holds above the former $1,845 to $1,865 resistance zone, now acting as support. A brief pause would not hurt the trend. Instead, it could give buyers enough fuel for another run at the $2,000 mark. The EthSystems and Dashlink announcement also gives investors another reason to stay interested.

Meanwhile, the base case is a rejection near $1,975 to $2,000, followed by profit taking and a pullback toward support. That would not be unusual after a strong rally. Markets rarely climb in a straight line, no matter how much the bulls wish they did.

The bullish outlook weakens if ETH closes below the $1,750 to $1,770 support area. A break there shifts attention toward $1,620, with $1,530 as the next meaningful floor. In that case, traders could view the recent EthSystems catalyst as positive news, but not enough to keep momentum alive.

Even so, ETH still trades about 62% below its all-time high above $4,950. That leaves room for upside over time, although $2,000 remains a realistic ceiling in the near term. If buyers clear that level with convincing volume, the next chapter could get much more interesting.

Trade Ethereum Before It Breaches $2,000 on Bybit and Get Our $1,000 USDT Airdrop

LiquidChain Targets Early-Mover Upside as Ethereum Tests Key Levels

ETH at $1,870 is a meaningful recovery, but a 6% daily move on a $226 billion asset carries proportionally modest return potential for new capital entering here. Traders chasing the $2,000 breakout are essentially pricing in a move already in progress. That’s where early-stage infrastructure plays draw attention, particularly those positioned at the intersection of the ecosystems driving current market momentum.

LiquidChain ($LIQUID) is a Layer 3 infrastructure project building what it describes as a unified cross-chain liquidity layer. It is fusing Bitcoin, Ethereum, and Solana liquidity into a single execution environment.

LiquidChain is cooking.

The Order doesn't sleep. ⟁pic.twitter.com/CXY4ya0MC5

— LiquidChain (@getliquidchain) June 3, 2026

The architecture centers on four components: a Unified Liquidity Layer, Single-Step Execution, Verifiable Settlement, and a Deploy-Once Architecture that lets developers ship to all three ecosystems simultaneously.

As of now, the presale is currently priced at $0.0148, with $900K raised. For traders who want exposure to cross-chain infrastructure before it’s priced in, research LiquidChain before the next pricing tier moves.

Discover: The Best Crypto to Diversify Your Portfolio

The post Ethereum Price Approaches $2,000 as Foundation Team Spins Out EthSystems appeared first on Cryptonews.

Revolut has secured in-principle approval from Dubai’s Virtual Assets Regulatory Authority to expand its regulated crypto business in the United Arab Emirates, adding another regulatory milestone to its global digital asset strategy.

Summary

- Revolut has received in principle approval from Dubai’s VARA to offer regulated virtual asset services in the UAE.

- The company plans to launch crypto trading, exchange, and investment services through its app and Revolut X after final regulatory approval.

- The approval follows recent regulatory moves in Europe and the United States as Revolut expands its crypto business across regulated markets.

According to a company announcement on Tuesday, the approval allows Revolut to move toward offering virtual asset broker-dealer, management, investment, and exchange services in the UAE, subject to receiving final authorization from Dubai’s Virtual Assets Regulatory Authority (VARA).

Once fully licensed, Revolut said eligible customers in the UAE will be able to buy, sell, and hold digital assets through its main retail app and its dedicated trading platform, Revolut X.

The latest approval follows an earlier authorization from the Central Bank of the UAE for Revolut’s payments business, as the fintech continues building a locally regulated financial platform in the country.

Joseph Khair, head of Revolut Digital Assets FZE, UAE, said the UAE has established “a robust and transparent framework for virtual assets” and added that the approval creates the foundation for the company to launch regulated crypto services while supporting VARA’s efforts to develop a safe and innovation-focused digital asset ecosystem.

UAE becomes the latest step in Revolut’s regulated crypto expansion

Outside the UAE, Revolut has continued to adapt its crypto business to local regulatory requirements across several markets.

Earlier this month, the company confirmed it would remove Tether’s USDT from eligible European accounts after the European Union’s Markets in Crypto-Assets (MiCA) framework entered full enforcement. Revolut said affected users can continue selling or transferring their USDT until Aug. 31 before the stablecoin is removed from supported accounts.

The company said the restriction applies only to notified customers in eligible European jurisdictions and does not affect markets where USDT remains supported.

MiCA requires crypto service providers and stablecoin issuers operating in the European Union to comply with licensing, reserve, disclosure, and supervisory requirements. Tether has not received MiCA authorization, and Chief Executive Officer Paolo Ardoino has previously argued that some of the framework’s reserve rules were not suitable for the issuer.

The UAE approval also comes as Revolut continues preparing for its U.S. expansion. Reuters reported in June that the fintech plans to launch a U.S. bank next year after filing for a national bank charter with the Office of the Comptroller of the Currency. According to Reuters, the planned platform will combine FDIC-insured banking products with crypto trading, stablecoins, and multi-currency services.

3 vehicles crash on A1 in Yorkshire – resulting in delays

Aker BP ASA (AKRBY) Q2 2026 Earnings Call Transcript

Crypto Firms Warned of AML Compliance Risks After MiCA Migration, AMLA Chair Says

-

Fashion6 days ago

Fashion6 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports6 days ago

Sports6 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports5 days ago

Sports5 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech6 days ago

Tech6 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

News Videos19 hours ago

News Videos19 hours agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Politics2 hours ago

Politics2 hours agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Tech1 day ago

Tech1 day agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech18 hours ago

Tech18 hours agoDark Secrets Emerge When Jailbreaking LLMs

-

News Videos7 days ago

News Videos7 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

NewsBeat6 days ago

NewsBeat6 days agoMajor update after Huntingdon train attack as man enters plea

-

Tech6 days ago

Tech6 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Sports7 days ago

Sports7 days ago39-year-old Djokovic wins five-hour thriller to enter Wimbledon semis | Other Sports News

-

Tech2 days ago

Tech2 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Tech7 days ago

Tech7 days agoEntra passkey enrollment vishing targets Microsoft 365 users

-

Crypto World6 days ago

Crypto World6 days agoDeFi Dashboard Zapper to Shut Down After 7 Years

-

Crypto World6 days ago

Crypto World6 days agoMark Cuban-Backed DeFi Dashboard Zapper Shuts Down After 7 Years

-

Tech6 days ago

Tech6 days agoClaude’s New Reflect Dashboard Wants To Help You Log Off Of Claude

-

Crypto World7 days ago

Crypto World7 days agoFed minutes June 2026: officials split on rates

You must be logged in to post a comment Login