Crypto World

What is a token unlock? Vesting and cliffs explained

Every few weeks, a token that has done nothing wrong falls ten percent in a day, and the explanation turns out to have been sitting in public view for years. A tranche of supply, promised to early investors back when the project raised money, hit its scheduled release date.

Insiders who bought at a fraction of the market price suddenly held tokens they could sell, and enough of them did. Traders call these events unlocks, and they are among the most predictable forces in crypto markets, which makes it strange how many investors get blindsided by them.

A token unlock is the moment previously locked supply becomes transferable and enters circulation under rules the project set in advance. The rules themselves are called a vesting schedule, and together they answer a question every serious investor should ask before buying any token: who is going to be allowed to sell, how much, and when. This guide explains what unlocks and vesting are, why projects lock tokens in the first place, the difference between cliffs and linear releases, who actually receives unlocked supply and how differently each group behaves, how unlocks move prices, the low float trap that defined the current market cycle, how to read an unlock calendar like a professional, and the honest limits of unlock analysis.

What a token unlock actually is

When a crypto project creates its token, it almost never releases the full supply into the market on day one. Instead, the total supply is divided into allocations: a slice for the founding team, a slice for the venture investors who funded development, a slice for advisors, a slice for the community, a slice for an ecosystem fund or treasury. Most of these allocations start locked, meaning the tokens exist on paper, and often on chain, but cannot be transferred or sold.

An unlock is the scheduled event that releases some of that locked supply. On the appointed date, or continuously according to a formula, tokens move from the locked state to the liquid state, and their owners can finally do what owners do: hold, stake, or sell. Nothing about an unlock is secret. The schedule is typically published in the project’s tokenomics documentation before the token ever trades, and modern vesting is usually enforced by smart contracts that release tokens automatically, with the whole timetable verifiable on chain.

The distinction between vesting and unlocking trips up newcomers. Vesting is the rulebook, the full timetable governing how allocations are earned and released over months or years. An unlock is a single event within that timetable, the moment a specific batch becomes tradable. A project has one vesting schedule and many unlocks. When traders say a token has an unlock next week, they mean one identifiable batch is crossing from locked to liquid, and the size, recipient, and context of that batch are what analysis is about.

Why projects lock tokens at all

Locking is a credibility device. Imagine a project that raised money by selling thirty percent of its supply to venture funds at an early stage price, then listed the token publicly at twenty times that price. If the investors could sell immediately, the rational move would be to dump everything into the listing hype, crush the price, and move on. Everyone who bought at listing would be exit liquidity. Projects that allowed this quickly found that nobody wanted to buy their tokens at all.

Vesting schedules exist to make the promise of long term alignment enforceable. A team whose tokens unlock over four years has four years of reasons to keep building. An investor with a one year cliff cannot flip the token at listing no matter how tempting the price. The lock converts a verbal commitment into a mechanical one, and because the schedule is public, the market can price the commitment instead of guessing at it.

Locking finally serves a signaling function that has nothing to do with mechanics. When a team accepts a four year schedule and investors accept a one year cliff, they are publishing their own confidence interval. Short schedules whisper that insiders want optionality. Long schedules, especially ones the team imposed on itself beyond what any exchange required, tell the market that the people with the most information expect the token to be worth holding. Markets read these signals imperfectly, but they read them.

Locking also manages the physics of supply. A token’s price is set at the margin, by the balance of buying and selling in liquid markets. Releasing supply gradually gives demand time to grow into it. Releasing it all at once is a flood, and floods move prices the way floods move everything else. The entire discipline of tokenomics, the economic design of a token’s supply, distribution, and incentives, treats the release schedule as one of its central levers.

Cliffs, linear vesting, and the shapes of release

Vesting schedules come in a small number of recognizable shapes, and the shape matters as much as the size. A cliff is a period, commonly six to twelve months after the token generation event, during which nothing unlocks at all. When the cliff ends, a large batch releases at once. Cliffs concentrate sell pressure into a single known date, which is why cliff expiries are the unlock events traders circle on calendars.

Linear vesting releases tokens continuously or in small regular steps, daily, weekly, or monthly, over a defined period. The drip is gentler on price because no single day carries a large release, but it creates persistent background pressure, a steady trickle of new supply that demand must absorb month after month.

Most real schedules are hybrids: a cliff followed by linear release. A typical structure for team tokens might be a one year cliff, then monthly unlocks over the following two or three years. Investor allocations often vest faster than team allocations, and community or ecosystem allocations sometimes have no lock at all, or unlock based on milestones instead of dates. Some projects add non linear schedules, with releases that accelerate or step up at intervals, and a few tie unlocks to performance conditions such as product launches. The token generation event, usually shortened to TGE, marks day zero for most schedules, and many tokens release a small percentage at TGE so that a market can exist at all.

Reading a vesting chart is mostly about learning to see these shapes. A wall of supply at a single future date is a cliff. A smooth ramp is linear release. The steeper the ramp and the taller the walls, the more supply the market will be asked to digest, and the more the token’s future depends on demand showing up on schedule.

Who receives unlocked tokens, and why it matters

The same unlock size can produce completely different market outcomes depending on whose tokens are being released, because different holders face different incentives. Venture investors are the most reliable sellers. Funds have limited lifespans and partners to repay, and a position bought at an early stage price that now trades far higher represents a return that fund managers are professionally obligated to realize. When a large investor tranche unlocks, systematic selling is the base case, not the exception.

Team allocations behave less predictably. Founders and employees have reputational reasons to avoid visible dumping, and many hold for belief or for optics, but personal diversification is a powerful force, and team selling after long cliffs is common enough that markets price it in. Ecosystem and treasury unlocks are different again: those tokens usually flow to grants, market making, or incentives instead of directly to exchanges, though grant recipients frequently sell what they receive, so the pressure arrives second hand and on a lag. Advisors sit somewhere in between, small in size but often quick to exit. Community allocations, including airdrops, scatter supply across thousands of small holders whose behavior varies from instant selling to permanent holding.

Sophisticated unlock analysis therefore never stops at the headline number. The question is not how many tokens unlock, but how many unlock into hands that are likely to sell, at what cost basis, and into how much liquidity.

How unlocks actually move prices

The mechanical story is simple: unlocks increase liquid supply, and if demand does not rise to meet it, price falls. But the mechanism deserves one more sentence of precision. Price is set by transactions, not by existence, so an unlock only moves the market to the degree that unlocked tokens are sold or that traders act on the expectation of selling. Supply that unlocks into wallets and stays there changes the risk picture without changing the order book. The market story is more interesting, because unlocks are public information, and public information gets traded in advance.

Ahead of a large unlock, traders who expect selling pressure sell first, or open short positions in perpetual futures to profit from the anticipated decline. This front running spreads the price impact across the weeks before the event, and it occasionally produces the counterintuitive pattern traders call sell the rumor, buy the news, where a token falls into an unlock and bounces after it, because the sellers finished selling early. Empirically, the price damage from major unlocks tends to arrive before and during the event, with the days after determined by how much of the released supply actually hits exchanges.

Context decides magnitude. The ratio of the unlock to average daily trading volume matters more than the ratio to market capitalization, because volume measures the market’s absorption capacity. An unlock worth three days of trading volume is a problem; an unlock worth an hour of volume is noise. Market regime matters just as much. Bull markets swallow unlocks that would crater the same token in a bear market, because absorption is a function of demand, and demand is cyclical. And holder cost basis sets the temptation: supply unlocking at a hundred times its purchase price wants to sell far more than supply unlocking underwater.

The clearest evidence that unlocks bind projects came during the 2024 and 2025 cycle, when several teams paused or restructured their own vesting schedules mid stream after watching unlock pressure grind their tokens down. A project that has to renegotiate its own tokenomics to defend its price is admitting that the original schedule asked the market to absorb more than it could.

From ICO free for all to institutional vesting

Vesting was not always standard. During the initial coin offering boom of 2017 and 2018, projects routinely sold tokens with no lockups at all: a whitepaper, a wallet address, and a promise. Teams and early buyers could sell the moment tokens listed, and many did, with predictable results. The wreckage of that era, thousands of tokens that listed, dumped, and died, is the reason vesting became a market requirement instead of a courtesy. Exchanges began expecting lockup disclosures before listing. Venture funds began accepting, and then demanding, multi year schedules as evidence of seriousness. By the early 2020s a token launching without published vesting for insiders read as a warning label.

The professionalization cut both ways. Structured vesting made token launches more credible, but it also standardized the low float playbook, in which a polished schedule defers the supply problem instead of solving it. A four year lockup does not remove twenty five times the float from the future; it just puts the future on a calendar. The modern unlock calendar industry, with dashboards, alerts, and analytics products tracking every scheduled release across the market, exists precisely because vesting became universal. What was once a question of whether insiders were locked at all became a question of exactly when the locks expire, and an entire analytical discipline grew in the gap.

The next stage of that evolution is already visible: on chain vesting contracts that anyone can audit, third party verification services, and standardized disclosure formats. The direction of travel is toward supply schedules as verifiable public infrastructure, which raises the analytical bar. When everyone can see the calendar, seeing it is no longer an edge. Interpreting it is.

The low float, high FDV trap

The defining supply structure of the recent cycle was the low float, high FDV launch. A project lists with a small fraction of total supply circulating, sometimes under ten percent, while the fully diluted valuation, the price of all tokens that will ever exist, implies a number many multiples higher. The small float makes the price easy to support at listing. The enormous locked overhang means years of scheduled unlocks stand between the listing price and the day the token’s market cap honestly reflects its supply.

The arithmetic is unforgiving. If a token trades at a two billion dollar fully diluted valuation with eight percent circulating, then over the coming years roughly twenty five times the current float will be released. For the price simply to stay flat, new demand must absorb all of it. Buyers of such tokens are, whether they realize it or not, betting that demand will grow faster than a supply schedule designed years earlier by people who bought at a fraction of the current price. The bet occasionally pays. The base rate does not favor it.

Markets learned this lesson expensively. Token after token from the low float era spent months in structural decline as unlocks arrived on schedule and demand did not, and by the middle of the cycle, unlock calendars had become one of the most watched datasets in DeFi and beyond. Aggregate unlock volume across the market now runs into billions of dollars in heavy months, and traders treat clusters of large unlocks as a marketwide supply headwind, particularly for assets far down the liquidity curve.

What big unlocks look like in practice

A few well known episodes show the full range of outcomes. Arbitrum’s ARB, one of the largest airdropped tokens of its generation, spent much of its first two years grinding lower as investor and team tranches unlocked month after month into demand that never matched the schedule, becoming the reference example of structural unlock pressure on a fundamentally serious project. The token’s technology kept shipping; the supply kept arriving; the price reflected the arithmetic.

AltLayer provided the reference example of a project blinking. After its first major unlock in mid 2024 hit the price hard, the team announced a six month vesting pause covering investors, team, advisors, and treasury. The pause relieved the calendar but not the market, and the token’s struggles afterward became a case study in why rescheduling supply does not manufacture demand.

Pump.fun’s PUMP token compressed the entire lifecycle into months. The July 2025 sale raised over a billion dollars at a valuation the open market immediately began stress testing, and every subsequent tranche movement from team and treasury wallets was tracked by thousands of traders in real time, a reminder that for high profile tokens, unlock analysis now happens wallet by wallet, not just date by date.

And Pi Network became the retail era’s unlock story: roughly 1.21 billion tokens scheduled to release across 2026 against thin exchange liquidity, an overhang so large relative to volume that the unlock calendar itself became the primary narrative around the asset. Whatever one thinks of the project, the episode taught millions of retail holders the vocabulary of cliffs, floats, and absorption for the first time.

The pattern across all four is consistent. Unlocks did not decide whether these projects mattered. They decided when the market was forced to render a verdict on how much demand actually existed at the prevailing price.

Reading an unlock calendar like a professional

Several platforms track unlock schedules across the market, including Tokenomist, CryptoRank, DropsTab, and CoinGecko, and they present broadly the same data: upcoming unlock dates, sizes in tokens and dollars, percentages of circulating supply, and the allocation buckets involved. The skill is in the interpretation, and it reduces to five questions.

First, how large is the unlock relative to circulating supply? Below one percent is usually noise; above five percent deserves attention. Second, how large is it relative to daily trading volume? This is the absorption test, and it is the single most predictive ratio. A useful rule of thumb: if the unlocked value exceeds three to five days of average volume, absorption will be slow and the price will likely do the absorbing. Third, who receives the tokens? Investor and team tranches carry the highest sell risk; ecosystem and treasury tranches are slower burning. Fourth, what is the recipients’ cost basis? Deeply profitable supply sells harder. Fifth, what happened at this token’s previous unlocks? Past behavior around identical events is the closest thing unlock analysis has to a controlled experiment.

Two practical refinements separate careful traders from calendar tourists. Cliff events deserve more respect than equivalent linear amounts, because concentration in time is what overwhelms order books. And exchange flow data, where available, tells you whether unlocked tokens are actually moving toward venues where they can be sold, or sitting in the same wallets that received them. Tokens that unlock and do not move are potential supply; tokens that unlock and flow to exchanges are incoming supply. On chain analytics platforms make this distinction observable in near real time, and the gap between the two is often where the actual trade lives.

What unlock analysis cannot tell you

Unlock data describes supply mechanics, and supply is only half of any price. A token with a brutal unlock schedule and explosive demand growth can rise through every release date, which is exactly what the strongest projects of every cycle have done. A token with a clean, fully vested supply and no demand will still go to zero, just without a schedule announcing it. Unlocks set the height of the wall; they say nothing about whether the buyers on the other side can climb it.

The data also cannot capture private arrangements. Locked tokens are routinely hedged through over the counter deals and derivatives, meaning the economic selling may have happened long before the unlock date, with the on chain release a mere formality. Conversely, some unlocked supply is contractually committed to market makers or custody and cannot hit the market as fast as the calendar implies. On chain vesting contracts have also occasionally diverged from published schedules, in both directions, which is why serious analysts verify the contract instead of trusting the documentation.

Treat unlocks the way professionals treat them: as one high quality, freely available input among several. In a market where edges are scarce and expensive, a public calendar of exactly when supply arrives, from Solana majors to the long tail of meme coins, is a gift. It is not a trading system. It is a schedule of when the questions get asked; demand still writes the answers.

Frequently asked questions

What is a token unlock in crypto?

A token unlock is a scheduled event in which previously locked tokens become transferable and enter circulating supply. Unlocks follow a vesting schedule the project defined in advance, and they typically release tokens to teams, early investors, advisors, or ecosystem funds.

What is the difference between vesting and unlocking?

Vesting is the overall timetable that governs how locked allocations are released over time. An unlock is a single event within that timetable. A project has one vesting schedule but many individual unlock events.

What is a cliff in a vesting schedule?

A cliff is an initial period, often six to twelve months, during which no tokens from an allocation are released. When the cliff ends, a large batch unlocks at once, which concentrates potential sell pressure into a single date.

Are token unlocks always bearish?

No. Unlocks add supply, but the price outcome depends on demand, on how much of the released supply actually gets sold, and on how much was priced in beforehand. Some tokens fall into an unlock and recover afterward once the anticipated selling clears.

How do I check when a token unlocks?

Unlock schedules appear in project tokenomics documentation and on tracking platforms such as Tokenomist, CryptoRank, DropsTab, and CoinGecko. These tools show upcoming dates, sizes, percentages of supply, and which allocation groups receive the tokens.

What is a low float, high FDV token?

It is a token that lists with a small share of total supply circulating while its fully diluted valuation implies a much larger market value. The structure supports the listing price but leaves years of scheduled unlocks that future demand must absorb.

Why do venture capital unlocks cause more selling?

Venture funds have finite lifespans and obligations to return capital to their partners, and their tokens were typically bought at prices far below market. Realizing those gains when tokens unlock is standard practice, so investor tranches carry the highest sell risk.

Can a project change its vesting schedule?

Sometimes, if governance or the token contract allows it. Several projects have paused or extended vesting to relieve price pressure. Any change should be publicly disclosed, and unexplained deviations between the published schedule and on chain behavior are a warning sign.

This article is for educational purposes only and does not constitute financial or investment advice. Vesting structures and unlock data vary by project and change over time. Details are accurate as of July 14, 2026.

The United States has frozen more than $130 million in cryptocurrency held in wallets linked to the Central Bank of Iran, according to Treasury Secretary Scott Bessent.

Summary

- US authorities froze more than $130 million in crypto tied to Iran’s central bank wallets.

- On-chain data showed four Tron wallets holding about $131 million in USDT were frozen Tuesday.

- The action follows April’s $344 million USDT freeze and wider US pressure on Iranian crypto.

The action adds to a broader U.S. campaign targeting Iran’s use of digital assets and other financial channels.In a July 14 post on X, Bessent said the Treasury Department’s Office of Foreign Assets Control sanctioned multiple wallets tied to Iran’s central bank. The sanctions resulted in more than $130 million being frozen.

Four Tron wallets held about $131 million

On-chain investigator Specter identified four wallets on the Tron network holding a combined total of roughly $131 million in USDT. Reports based on the analysis said Tether had frozen the addresses, preventing the stablecoins from being transferred.

Bessent did not identify the individual addresses in his statement. He said Treasury remained “committed to disrupting and degrading Iran’s illicit financial activities, including its abuse of digital assets.” He added that authorities would continue to “follow the money” and restrict access to funds that Washington links to Iranian government revenue networks.

Freeze follows earlier $344 million USDT action

The latest move follows a much larger enforcement action in April.As previously reported, Tether froze about $344 million in USDT across two Tron wallets after U.S. authorities linked the addresses to Iranian networks. One wallet held about $213 million, while another contained roughly $131 million.

Blockchain analysis at the time found transaction patterns associated with wallets linked to Iran’s Islamic Revolutionary Guard Corps and intermediaries connected to the Central Bank of Iran. The funds were blocked through controls built into the USDT token rather than through changes to the Tron blockchain itself.

Treasury expands pressure on Iran’s crypto networks

The United States has increased its focus on Iran’s digital asset infrastructure during 2026. In June, Treasury sanctioned four Iranian crypto exchanges, including Nobitex, which the department said handled more than half of Iranian digital asset inflows during 2025.

As reported, Bessent also said in May that U.S. actions had seized or frozen nearly $1 billion in Iran-linked cryptocurrency. Earlier figures had placed the total near $500 million after the April USDT action.

The Treasury has described the campaign as part of Operation Economic Fury, which targets crypto exchanges, wallets and traditional financial networks that U.S. officials accuse of supporting sanctions evasion and Iranian military financing. Treasury actions have also targeted overseas companies accused of helping move proceeds from Iranian oil sales through cryptocurrency and front companies.

Crypto freeze comes as US-Iran tensions rise

The new wallet action comes during renewed military tensions between Washington and Tehran. U.S. Central Command confirmed fresh strikes against Iranian military targets and the resumption of a blockade of Iranian ports this week after a June pause in hostilities began to break down.

The latest freeze also shows the enforcement role centralized stablecoins can play. Unlike Bitcoin, USDT contains issuer-level controls that can prevent sanctioned addresses from moving tokens. Tether has used those controls in several law enforcement actions, including the April Iran-linked freeze and a July action involving wallets sanctioned over alleged ISIS-K financing.

For the latest $131 million action, Treasury has confirmed that the wallets were tied to the Central Bank of Iran and that the funds were frozen. Public statements have not disclosed how the assets were originally obtained or how authorities determined the intended use of the funds.

Binance is looking beyond cryptocurrency trading as it works to build a broader financial “super app” centered on payments, stablecoins and investment products.

Summary

- Binance plans to expand beyond trading by combining payments, stablecoins, stocks and broader financial services.

- Stablecoin adoption is pushing Binance toward payment services aimed especially at users in emerging markets.

- Binance already offers thousands of US stocks and tokenized equities alongside its core crypto products.

Shunyet Jan, the exchange’s head of spot trading and derivatives, outlined the strategy as Binance marked its ninth anniversary.

In an interview with CoinDesk, Jan said trading remains central to Binance but no longer defines the full market available to the company. “We’re trying to not just be a crypto exchange, but be a super app that involves payment,” he said.

Stablecoins push Binance deeper into payments

Jan linked the strategy to growing stablecoin use for payments and transfers. Stablecoins have expanded beyond their original role as trading assets, giving exchanges a way to serve users who need cross-border payments, spending tools and access to dollar-based digital assets.

“If you think of us as a payment provider, then that number becomes much bigger,” Jan said. Binance Research has also identified payments as a major path for crypto super apps. Its April report said Binance Pay had reached more than 21 million merchants and connected with local payment systems such as Brazil’s Pix.

Binance has also expanded its card services. As previously reported, the exchange launched a Mastercard-linked crypto card in selected CIS markets in February, allowing eligible users to spend Bitcoin, Ether, stablecoins and other supported assets through automatic conversion at checkout.

Binance adds stocks to its financial ecosystem

The exchange has spent 2026 adding products outside traditional crypto markets. Binance said in its ninth-anniversary update that it now wants users to move between digital assets, stablecoins, public markets, payments and onchain services from one platform.

However, Binance opened access to more than 7,000 US stocks and ETFs for eligible users outside the United States in June. Users can buy fractional shares using assets including USDT and USDC, connecting stablecoin balances directly with traditional investments.

Binance said direct stock positions reached $1 billion in assets within about 30 days, with close to $3 billion in cumulative trading volume. More than 73% of first-month trading volume came from emerging markets, according to the exchange.

Tokenized equities add an onchain layer

Binance has also launched bStocks, which convert supported US equity exposure into blockchain-based assets. The initial lineup included tokenized versions of Nvidia, Tesla, Circle, Micron and Sandisk.

The products can trade around the clock and move to supported self-custody wallets. Binance says eligible users can also use them in supported decentralized finance applications. The company reported that bStocks passed $100 million in assets within 15 days, while 47% of trading volume occurred outside normal US market hours.

Emerging markets form a key part of the strategy

Jan said demand for Binance’s broader financial services is particularly strong in emerging economies, where access to foreign investments and traditional banking services can remain limited. The company sees its existing crypto infrastructure as a way to connect those users with more payment and investment products.

Binance Research previously estimated that crypto exchanges could bring nearly 300 million new investors and about $2 trillion into global equity markets by 2031. As per report, stablecoin settlement could help exchanges serve investors who face high costs or limited access to overseas markets.

Binance is not alone in pursuing the model. Coinbase has also outlined a financial super app strategy combining trading, lending, payments and other services. Binance’s approach now centers on linking its large trading business with stablecoin payments, traditional assets and onchain products within one platform.

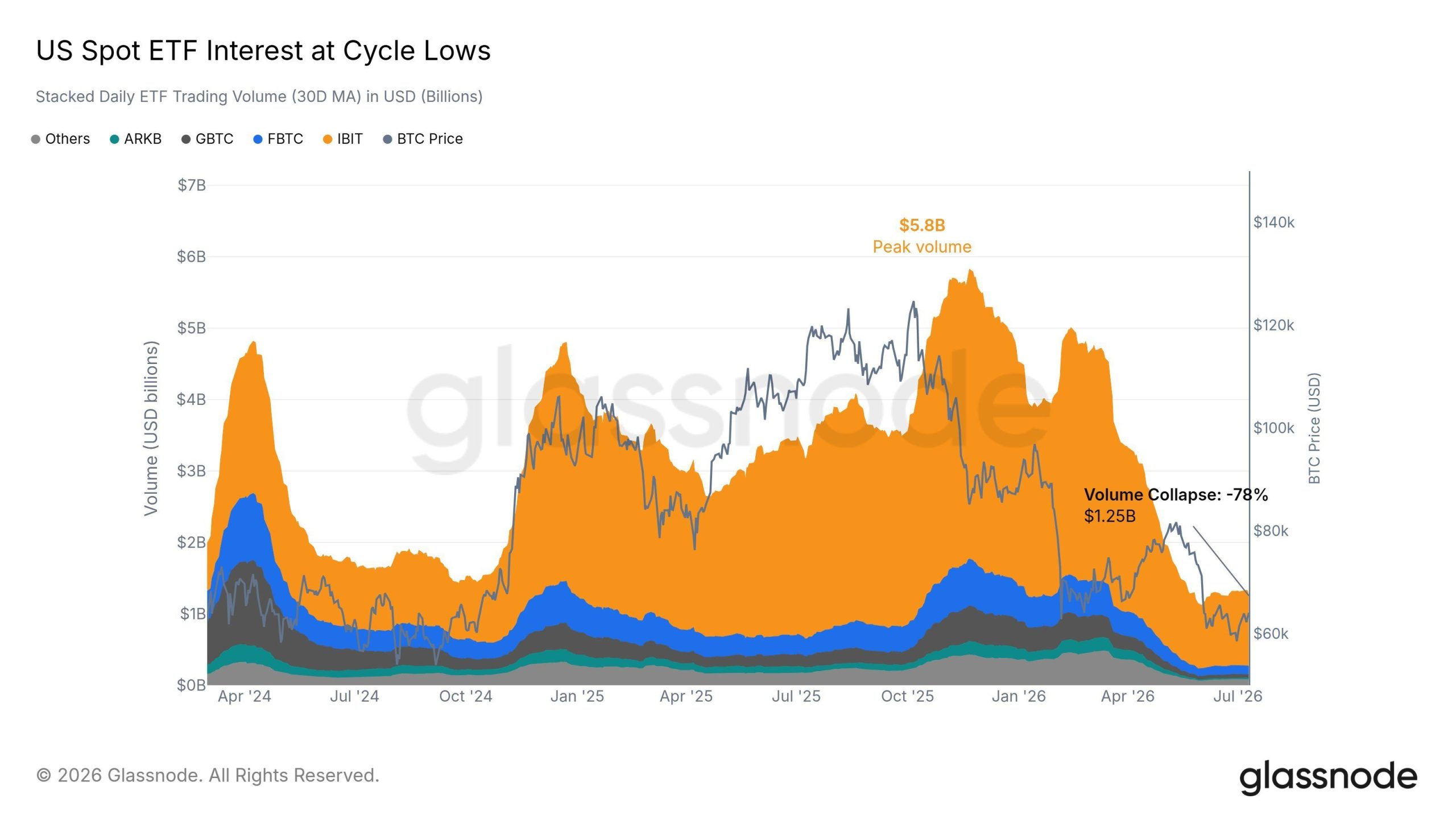

US spot Bitcoin (BTC) ETF outflows reached roughly $430 million on July 13. Fidelity’s FBTC lost $246.3 million and BlackRock’s IBIT shed $186.1 million, according to Glassnode data.

The redemptions hit a market already trading at its quietest levels this cycle. ETF volumes have collapsed 78% from their peak, and analysts warn that attention has rotated to other asset classes.

ETF Trading Volumes Collapse 78% From Peak

Glassnode’s 30-day moving average of daily trading volume across US spot Bitcoin ETFs now sits at $1.25 billion. That marks a 78% collapse from the $5.8 billion peak recorded in late 2025.

Activity has also slipped below 2024 levels. BlackRock’s IBIT still accounts for most of the remaining turnover. However, even its share has thinned in recent months.

The on-chain analytics firm framed the slowdown as a loss of attention rather than a temporary lull. Glassnode shared the observation in a post on X:

“Trading activity in US spot ETFs sits in a quiet regime. Volumes are down 78% from the peak and below 2024 levels. A sustained recovery in $BTC price momentum would likely require attention and market participation to return from other asset classes.”

Bitcoin ETF Outflows Top $430 Million in One Day

Monday’s session showed how one-sided flows have become. Fidelity’s FBTC led the exit with $246.3 million in redemptions. IBIT followed with $186.1 million, while VanEck’s HODL bucked the trend with a $3.5 million inflow.

Grayscale’s GBTC and Franklin Templeton’s EZBC posted smaller losses. Combined, the funds bled roughly $430 million in a single day.

The IBIT figure drew loud reactions. Evan Luthra, entrepreneur and BeInCrypto Experts Council member, reacted to the data in a post on X.

The framing deserves nuance, however. ETF outflows reflect investors redeeming shares, which forces issuers to sell bitcoin held in trust. BlackRock did not liquidate a proprietary position, and Fidelity’s outflow was the larger of the two.

The reversal also stings because of its timing. Bitcoin funds had just attracted $197.4 million in net inflows during the week ending July 10, snapping eight straight losing weeks. June, in contrast, produced record monthly outflows of $4.5 billion.

BTC Price Prediction Hinges on the $58,000 Support

BTC trades near $64,681, up 4.4% over the past 24 hours, per BeInCrypto market data. Glassnode’s flows chart tracks the token’s slide from roughly $78,000 in mid-May to a June 30 low near $58,000.

That $58,000 area remains the level to defend. A daily close below it would put the cycle floor near $57,500 in play, roughly an 11% drop from current prices.

On the upside, bulls must reclaim $68,000, the zone where the early June breakdown began. A recovery above that level would suggest institutional demand is returning after a two-month drought.

There are early signs of absorption elsewhere. Long-term holders flipped back to accumulation on July 11 and 12, adding a net 5,912 BTC.

Sustained positive flows and a volume recovery would confirm renewed participation. Until then, BTC either rebuilds momentum above $68,000 or retests $58,000 with little institutional cushion beneath it.

The post ‘BlackRock Dumped $185M in Bitcoin’ Claim Fuels ETF Panic as Trading Hits Cycle Lows appeared first on BeInCrypto.

Three Democratic senators have opposed the Digital Asset Market Clarity Act unless lawmakers add stronger ethics rules covering senior officials and their families.

Summary

- Murphy, Merkley and Van Hollen oppose the CLARITY Act unless lawmakers add strict ethics safeguards.

- John Thune pledged a Senate vote before recess, but timing and Democratic support remain uncertain.

- The bill needs 60 votes, making bipartisan support essential amid disputes over ethics and DeFi.

Senators Chris Murphy, Jeff Merkley and Chris Van Hollen raised their objections during a July 14 press conference organized with Americans for Financial Reform and Indivisible.

The lawmakers tied their opposition to President Donald Trump’s crypto businesses, including his memecoin and the World Liberty Financial project. Murphy claimed Trump earned $1.4 billion from crypto in 2025. Trump has rejected claims of wrongdoing involving his digital asset interests.

Senators demand conflict-of-interest protections

Murphy said Congress should not create a new crypto framework without rules that prevent officials from profiting from the industry they regulate. He said, “There is no reason to pass a new regulatory system for crypto if this system does not stop Trump’s corruption.”

Merkley called for restrictions covering the president, vice president, Cabinet officials, members of Congress and their families. Van Hollen also argued that the bill needs stronger consumer, anti-crime and conflict-of-interest provisions before he can support it.

The lawmakers did not reject digital asset regulation as a general goal. Their position centers on whether the final Senate text includes enforceable ethics language. Senator Elizabeth Warren has made a similar demand, calling for restrictions on crypto profits involving senior government officials.

Thune commits to vote before August recess

Senate Majority Leader John Thune told Bloomberg Government that the chamber will vote on the CLARITY Act during the current work period. He said leaders had not fixed the exact date and added that Democratic support remains the main question.

The press conference organizers listed July 20 as the expected vote date. However, Thune only committed to action before the recess and said the exact timing remained undecided.

The Senate’s official calendar starts its state work period on Aug. 10, leaving Aug. 7 as the final scheduled session day before the break. As of July 15, the public Senate floor schedule did not list a CLARITY Act vote, leaving the reported timing still subject to change.

The bill needs 60 votes, so Republicans cannot pass it without Democratic support. The House approved the CLARITY Act in July 2025 by a 294-134 vote. The measure would divide digital asset oversight between the SEC and CFTC while setting registration and custody rules for crypto firms.

Ethics dispute adds to unresolved policy fights

As previously reported, ethics rules are one of three disputes shaping the Senate negotiations. Lawmakers also remain divided over protections for non-custodial developers and whether crypto platforms may offer rewards tied to stablecoin balances.

The ethics debate has gained urgency as senators prepare a combined draft from the Banking and Agriculture committees. Supporters want a durable federal framework, while opponents say the bill should not move without clear limits on financial conflicts involving public officials.

Bill also gains law enforcement support

The National Organization of Black Law Enforcement Executives and Federal Law Enforcement Officers Association have backed the bill. FLEOA also requested tighter DeFi accountability rules and language preserving federal investigative powers.

As reported by crypto.news, the two endorsements give supporters added backing before the Senate vote. However, the ethics opposition shows that the bill still lacks the bipartisan coalition needed for passage. The final wording and vote date remain unsettled.

The European Central Bank is moving the digital euro from planning into testing, with dozens of payment companies joining the next stage of the project.

The ECB selected 36 payment service providers (PSPs) to participate in a digital euro pilot, according to an official announcement published Tuesday.

The list of selected PSPs includes fintechs Stripe and Revolut alongside traditional banks including Deutsche Bank, UniCredit and BPCE. Revolut has recently adjusted some cryptocurrency services for EU users by phasing out support for Tether USDt.

The pilot comes as governments take different approaches to digital currencies. While Europe is expanding testing of its proposed central bank digital currency (CBDC), the US has moved to block the Federal Reserve from issuing a CBDC.

Italy tops list of digital euro pilot providers

The ECB began selecting providers from across the euro area for its digital euro pilot earlier this year, with the 12-month trial set to begin in the second half of 2027.

The central bank said it received more than 50 applications from payment companies after opening a call for interest in March 2026. The selected participants include traditional banks, payment processors and non-bank service providers.

Source: ECB

Italy has the largest number of selected participants, with seven companies joining the pilot, including UniCredit, Poste Italiane, Nexi Payments, Banca Sella, Banca Monte dei Paschi di Siena, Isybank and Numia.

Germany follows with five selected providers, while Portugal and Greece each have three. The ECB said the mix of countries is designed to create a broad testing environment, with selected providers able to offer pilot services outside their home markets.

Strong interest in digital euro pilot

ECB Executive Board member Piero Cipollone, who chairs the high-level task force on a digital euro, said the level of participation shows private-sector interest in helping develop it, adding that the Central Bank expects deeper cooperation with payment providers during the pilot.

“We look forward to deeper engagement as we work with and learn alongside European payment service providers in developing a secure, efficient and inclusive digital euro,” Cipollone said.

Related: South Korea to test tokenized government bonds with CBDC in 2027

The pilot will involve the ECB and the central banks of 19 bloc-members, including Belgium, Germany, France, Italy, Spain and the Netherlands, alongside payment companies and merchants testing the system before any potential token issuance.

Selected providers will have different responsibilities during the trial, with some focused on supporting user access to beta digital euro services and others helping merchants accept payments. Several companies will take on both roles, the ECB said.

Magazine: The 5 types of real world assets being tokenized fastest onchain

Chinese AI startup DeepSeek has begun preparing for an initial public offering (IPO) and has also opened early talks with new investors for another funding round.

The moves come only weeks after DeepSeek closed its first external round, signaling that investors are aggressively chasing top Chinese artificial intelligence (AI) plays.

DeepSeek Eyes IPO Filing This Year as It Sounds Out New Investors

According to Bloomberg, DeepSeek could file its IPO paperwork late this year or in early 2027. That timeline would clear the way for a debut next year.

The company is working with accounting and banking advisers. It wants to finish its financial report by the end of December.

The Hangzhou firm has also opened preliminary talks with new investors this week. The Financial Times reported that DeepSeek is seeking fresh funds in another round, targeting a pre-money valuation of about $71 billion.

Follow us on X to get the latest news as it happens

That tops the roughly $50 billion figure from its first external round. That raise closed nearly a month ago and drew Tencent and battery maker CATL. Founder Liang Wenfeng put about $3 billion of his own money into it.

The rapid return to fundraising reflects DeepSeek’s expectation of higher spending ahead. The company plans to build its own data center and buy more AI chips. DeepSeek is also developing its own AI chip, which could cut reliance on Nvidia and Huawei, Reuters reported earlier this month.

Plans remain fluid, and both the IPO timing and the funding could shift. Much depends on market conditions and the company’s performance.

DeepSeek’s IPO push comes as US rivals move in the same direction. Anthropic and OpenAI both filed confidential IPO prospectuses in June. Anthropic said any offering would depend on market conditions and other factors, keeping the timing open.

OpenAI’s timeline looks less settled. CFO Sarah Friar floated the idea of waiting until 2027 to go public. She cited heavy cash burn, large compute commitments, and the burden of public reporting.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post DeepSeek May File for IPO This Year as It Weighs Fresh Fundraising appeared first on BeInCrypto.

Corporate treasury demand remains one of Bitcoin’s most important structural sources of support, but experts suggest that the market is no longer treating it as a permanent, price-insensitive floor.

Instead of focusing solely on how much BTC companies hold, QCP Capital stated that investors are increasingly evaluating whether the funding conditions behind those holdings can continue to support accumulation.

Funding Model Matters More

In its latest report, QCP said that the trend became clear in Q2 after Strategy’s late-May sale of 32 BTC. Although the sale was “immaterial” relative to its 846,842 BTC holdings, it challenged the long-held belief that corporate Bitcoin treasuries would only keep buying, never sell.

It also prompted the market to reassess whether treasury holdings were truly untouchable. Even as Strategy resumed buying within weeks, there has been no meaningful positive reach for Bitcoin, which essentially suggests that the market had become more focused on funding capacity, balance-sheet liquidity, and confidence in the treasury model than on accumulation alone.

QCP explained that while public companies collectively hold about 1.26 million BTC, roughly two-thirds belong to Strategy. This leaves the corporate treasury narrative heavily concentrated around a single company. As a result, its purchases, issuance conditions, and reserve policy continue to influence Bitcoin sentiment well beyond their direct impact on the spot market.

The financial structure supporting corporate accumulation has come to attention in Q2. Rather than judging treasury demand through purchase announcements, investors are now watching factors such as mNAV, equity issuance, preferred demand, convertible capacity, and cash reserves.

When funding conditions remain favorable, companies can raise capital, expand their Bitcoin reserves, and reinforce confidence in the treasury model. On the other hand, when conditions tighten, recurring preferred-stock obligations create cash needs, as seen with the Strategy’s May sale.

QCP went on to add that the company’s equity still trades above the combined value of its Bitcoin net asset value and US dollar reserves, which indicates a premium on its ability to continue raising capital, even as around $22.2 billion in preferred securities and convertible instruments rank ahead of common equity.

Looking ahead to Q3, continued net accumulation by Strategy and other public companies, particularly alongside stabilizing ETF inflows, would strengthen Bitcoin’s absorption channel and help repair the confidence damage from Q2. However, QCP warned that slower purchases, weaker preferred pricing, a compressed mNAV premium, or declining cash reserves would point to growing stress, which would end up making the corporate treasury bid more selective and increasing sentiment risk.

Besides, Bitwise CIO Matt Hougan recently said that Strategy is unlikely to have the same influence on Bitcoin demand in the next market cycle as it did previously. Hougan does not expect the company to become a major seller and still sees it remaining a net buyer if the crypto asset’s prices recover.

Scenarios For BTC

QCP outlined three possible paths for Bitcoin in Q3. Its base case calls for the crypto asset to remain between $60,000 and $75,000 as ETF flows stabilize and corporate treasury demand supports the market.

A steady reclaim of $75,000 could drive prices toward $80,000-$82,000, while renewed ETF outflows, a stronger dollar, or rising real yields could trigger a break below $58,000-$60,000 and confirm a more bearish outlook.

The post Why Strategy’s Tiny 32 BTC Sale Changed How Investors View Corporate Bitcoin Buying appeared first on CryptoPotato.

![]()

Reed Smith has launched an automated MiCA compliance platform as crypto firms across the European Union have entered full regulatory supervision following the end of the bloc’s transition period.

Summary

- Reed Smith has launched an automated platform to help crypto companies comply with the European Union’s MiCA regulation.

- The platform automates crypto asset classification, regulatory filings, due diligence and ESG disclosures for firms entering the EU market.

- The launch comes as European regulators move from MiCA licensing to operational supervision and consider future changes to the framework.

According to global law firm Reed Smith, the new platform, called Aquarius, automates key compliance tasks under the European Union’s Markets in Crypto-Assets (MiCA) regulation, including crypto-asset classification, regulatory white paper generation, due diligence and environmental, social and governance (ESG) disclosures.

Designed for companies entering the European market or expanding existing crypto services, the platform combines automated compliance workflows with legal support to simplify MiCA requirements. Reed Smith said future versions will also support crypto compliance regimes in the United Kingdom, the United Arab Emirates, Hong Kong, and Singapore.

The launch comes shortly after the European Union’s MiCA transition period ended on July 1, when crypto companies could no longer rely on temporary national exemptions in member states that adopted the full grandfathering period. The framework now requires crypto-asset service providers to meet common licensing, consumer protection, and operational standards across all 27 EU member states.

Reed Smith has continued expanding its digital asset practice through its “On Chain” initiative. The firm acted as legal counsel to the placement agents in Trump Media’s $2.5 billion Bitcoin treasury financing and also advised Nakamoto Holdings on its merger with KindlyMD to establish a Bitcoin treasury company.

Focus moves from licensing to supervision

Recent regulatory activity indicates that European authorities are now concentrating on how licensed firms operate after receiving approval.

Last week, the European Securities and Markets Authority (ESMA) began a Common Supervisory Action covering selected MiCA-authorized crypto-asset service providers. According to ESMA, the review examines custody operations, including private key management, transaction controls, incident response procedures and reliance on third-party technology providers.

Sebastien Dessimoz, co-founder and managing partner of digital asset infrastructure provider Taurus, previously said obtaining a MiCA licence is only the starting point for custodians because regulators now expect firms to demonstrate that their operational controls can withstand real-world risks. He added that supervision increasingly focuses on cybersecurity, governance and protection of client assets rather than licensing alone.

Institutional expectations have also increased. Jody Mettler, chief operating officer of BitGo and president of BitGo Trust, previously said clients are paying closer attention to how custodians segregate customer assets, control access, respond to security incidents and maintain business continuity during periods of market stress.

Meanwhile, European policymakers continue discussing possible changes to MiCA after its rollout. According to a Euronews report, officials are considering future revisions to stablecoin rules, including the treatment of non-euro-denominated stablecoins, following the passage of the United States’ GENIUS Act.

The European Parliament has also asked the European Commission to examine whether decentralized finance, staking, crypto lending and borrowing, non-fungible tokens and tokenized financial assets should receive more specific treatment under the EU’s crypto framework. Parliament’s position does not change the law but provides political support for further reviews, while any expansion of MiCA would still require separate legislative proposals.

US Treasury Secretary Scott Bessent confirmed the US government ordered the freezing of more than $130 million in cryptocurrency held in wallets linked to Iran on Tuesday, as hostilities ramped up in the Middle East.

Earlier on Tuesday, blockchain investigator Specter pointed to onchain data showing Tether froze four Tron wallets holding $131 million worth of USDt (USDT). Bessent confirmed on X that the wallets were tied to the Central Bank of Iran.

“US Treasury is committed to disrupting and degrading Iran’s illicit financial activities, including its abuse of digital assets,” Bessent said Tuesday. “We will continue to aggressively follow the money and deny the Iranian regime access to the proceeds of its illicit revenue schemes.”

The asset freeze comes amid a collapse in the ceasefire between the US and Iran. The US said it has renewed its blockade of Iranian ports, while the US military’s Central Command announced a new wave of strikes on Iran. Meanwhile, Iran’s military claimed on Tuesday that it carried out drone strikes against US military facilities at Jordan’s Al Azraq Air Base.

Source: Scott Bessent

The move follows a similar freeze in April, when stablecoin issuer Tether confirmed it had frozen more than $344 million in USDT at the request of US authorities.

In May, Bessent said the US has seized around $1 billion in Iranian crypto assets as part of the US financial pressure campaign against Iran known as Operation Economic Fury, which launched in March 2025.

Related: Iran-linked entities moved $3.8B through CoinEx, TRM says

“Through Economic Fury, the Treasury Department is disrupting the foreign procurement networks that support the Iranian military’s efforts to acquire weapons,” Bessent said in a statement in June.

“Treasury has frozen the Iranian regime’s assets, severely disrupted its economy, and dismantled the Iranian war machine. Treasury will not tolerate any support of the Iranian military.”

Magazine: Thai scammer’s $122M wallet, Japan embraces crypto credit: Asia Express

Confirmo has launched a stablecoin subscription payment service that supports automated recurring billing across more than 700 self-custody wallets and exchange accounts.

Summary

- Confirmo has launched Subscribe to let businesses automate recurring stablecoin payments through wallets and exchange accounts.

- The service supports USDC and USDG on Solana and Polygon, with more than 700 WalletConnect compatible wallets available.

- The launch comes as stablecoin payments continue expanding across business subscriptions, cross border settlements and enterprise payment services.

According to a July 14 press release shared with crypto.news, Subscribe allows enterprise businesses such as SaaS providers, trading platforms, and subscription services to add recurring stablecoin payments to their existing payment systems without developing the infrastructure internally.

The product has arrived as the global subscription economy is projected to reach $1.2 trillion by 2030, while Confirmo said more than 700 million people, or about 8.5% of the global population, now hold digital assets.

Built on Solana and Polygon, Subscribe initially supports Circle-issued USDC and Paxos-issued USDG. Paxos also serves as Confirmo’s US infrastructure partner, with the companies working together on stablecoin infrastructure and market access.

Subscribe supports wallets and exchange accounts

Unlike services limited to self-custody wallets, Subscribe accepts payments from both wallets and exchange accounts. WalletConnect integration gives customers access through more than 700 supported wallets, according to Confirmo.

Once a customer approves a subscription, the system automatically pulls stablecoins from the selected wallet or account on each billing date. Every payment is recorded from the outset, allowing merchants to monitor completed and scheduled transactions.

Existing Confirmo clients can view subscription activity through the same dashboard used for their other stablecoin payment products. The combined view removes the need to manage recurring transactions through a separate system.

Subscription plans are priced in US dollars to limit exposure to digital asset price changes. Confirmo said stablecoin settlement can also lower cross-border costs and reduce unexpected charges for customers.

Card declines and failed billing attempts can cause subscribers to lose access to a service without choosing to cancel. The company said wallet-based pull payments remove some of those failure points by collecting funds automatically after the customer grants approval.

Anna Kratky Strebl, Group CEO at Confirmo, said the service was developed around the payment needs of the company’s business customers.

“Built in collaboration with our long-term customers, it gives merchants a more transparent, cost-effective way to manage subscription and recurring revenue models, while making it easier for consumers worldwide to pay with the wallets and accounts they already use,” Strebl said.

She added that Confirmo would continue adapting its services as stablecoins become part of mainstream financial infrastructure and businesses seek new digital payment models.

FTMO helped design the payment system

Confirmo developed Subscribe with proprietary trading firm FTMO, which served as the product’s design partner. The collaboration allowed the infrastructure provider to test the system against the operational requirements of an existing merchant before launch.

Milan Flosman, Head of Finance Operations at FTMO, said the service would allow the company to introduce automated stablecoin billing without building its own payment system.

“Subscribe will give us something that didn’t exist before, a way to run automated, recurring stablecoin billing without building it ourselves,” Flosman said.

He added that Confirmo understood FTMO’s setup through the companies’ existing relationship and built the service to integrate with its operations.

“We’re not just looking to accept a new payment method; we’re preparing to launch a new payment model entirely,” Flosman said.

Stablecoin payments continue expanding beyond trading

The launch comes as businesses continue adopting stablecoins for commercial payments instead of limiting their use to crypto trading.

As previously reported by crypto.news, stablecoin cross-border payments were priced below interbank foreign exchange rates throughout the second quarter of 2026, Borderless.xyz highlighted in its Q2 2026 benchmark.

The firm tracked 260 payment corridors across 108 countries using nearly three million exchange rate observations and found stablecoin transfers maintained predictable pricing while provider selection became the largest factor affecting payment costs.

Borderless.xyz also reported that real-world stablecoin payment volume doubled to about $400 billion in 2025 as business-to-business payments, payroll and cross-border settlement gained traction.

The report said payment providers have continued expanding stablecoin services across new markets, with companies including dLocal and SBI Remit increasing support for international payment corridors.

Lionel Messi gets his favourite referee for England vs Argentina World Cup semi-final despite conspiracy theories that tournament is ‘rigged’

Texas launches investigates LinkedIn over claims of ‘ghost jobs’

US freezes $131M in Iran-linked crypto tied to central bank

-

Fashion6 days ago

Fashion6 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports6 days ago

Sports6 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports5 days ago

Sports5 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech6 days ago

Tech6 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

News Videos9 hours ago

News Videos9 hours agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech1 day ago

Tech1 day agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech9 hours ago

Tech9 hours agoDark Secrets Emerge When Jailbreaking LLMs

-

News Videos6 days ago

News Videos6 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

NewsBeat6 days ago

NewsBeat6 days agoMajor update after Huntingdon train attack as man enters plea

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Sports7 days ago

Sports7 days ago39-year-old Djokovic wins five-hour thriller to enter Wimbledon semis | Other Sports News

-

Tech6 days ago

Tech6 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

Tech1 day ago

Tech1 day agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Tech6 days ago

Tech6 days agoEntra passkey enrollment vishing targets Microsoft 365 users

-

Crypto World6 days ago

Crypto World6 days agoDeFi Dashboard Zapper to Shut Down After 7 Years

-

Crypto World6 days ago

Crypto World6 days agoMark Cuban-Backed DeFi Dashboard Zapper Shuts Down After 7 Years

-

Tech6 days ago

Tech6 days agoClaude’s New Reflect Dashboard Wants To Help You Log Off Of Claude

-

Crypto World7 days ago

Crypto World7 days agoMicrosoft Cuts AI Bill by Replacing OpenAI and Anthropic in Software Products

-

Crypto World6 days ago

Crypto World6 days agoFed minutes June 2026: officials split on rates

You must be logged in to post a comment Login