Business

Wedgewood Partners Q2 2026 Client Letter (RWGIX)

matejmo/iStock via Getty Images

Are Hyperscalers Still Magnificent?

Chart 1: Momentum Stocks Go Full Tilt

Source: MSCI, Alpine Macro

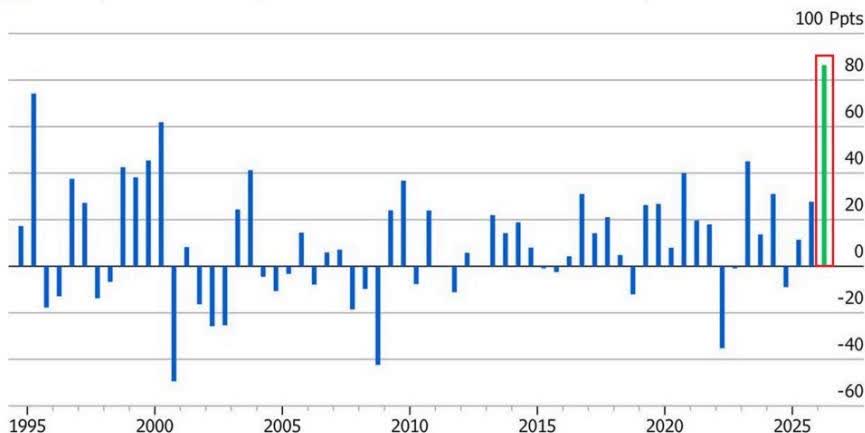

High Quality Stocks’ Underperformance is at 1999 Extremes

Source: Refinitiv, as of 11/10/2025. File #1077

Big Mo’s Low-Quality Rally: High-quality stocks with strong balance sheets continue to be pummeled

Review and Outlook

Top performance contributors for the second quarter include Taiwan Semiconductor Manufacturing, Alphabet, United Rentals, Apple, and Visa.

Top performance detractors in the second quarter include Tractor Supply Company, Copart, CDW, Motorola Solutions, and Hermès (HESAY) ADR. (Note: We no longer have an ADR percentage limit in our portfolio.)

During the quarter, we were unusually busy. We bought Hermès and sold Tractor Supply Company, Zoetis (ZTS), and CDW. We increased positions in Chubb (CB), Progressive (PGR), Meta (META), Amazon (AMZN), Microsoft (MSFT), and Visa. We trimmed United Rentals, Alphabet, and Taiwan Semiconductor Manufacturing.

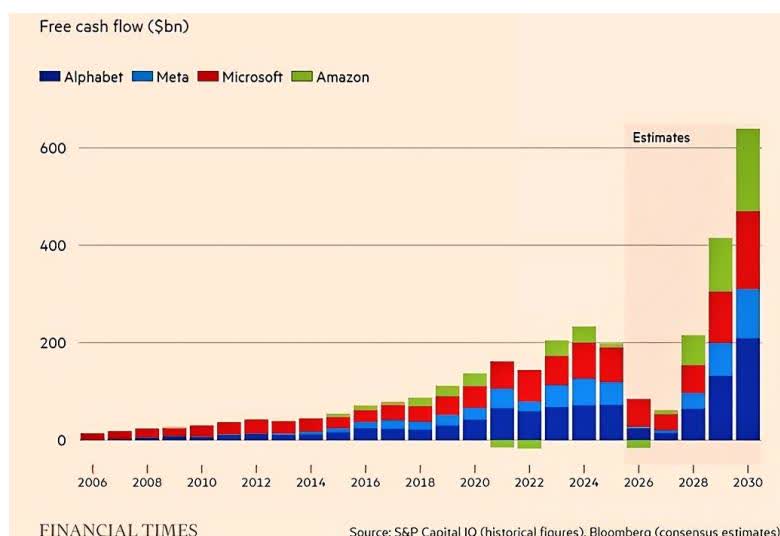

Alphabet was a top contributor to performance during the quarter. Google Search and Cloud continue to accelerate, with Search posting 19% revenue growth and Cloud posting 63% revenue growth, helping drive 30% growth in operating income. That torrid growth in operating income compares to, we estimate, more than 40% growth in Alphabet’s total gross assets. While that means returns on capital were slightly diluted, they remain above 30%. We think Alphabet is an exceedingly rare, if not entirely unique, business, growing a nearly $450 billion gross asset base by 40% while maintaining a 30% return on that massive asset base . These are astonishing compounding figures. Further, we have excluded from operating income large, unrealized gains from the Company’s investment portfolio, which totaled more than $35 billion in the most recent quarter (mostly due to SpaceX (SPACE)) and nearly $50 billion over the past six quarters. The Company also has a 14% stake in the private company Anthropic (ANTHRO). That stake could be worth more than $100 billion based on valuations reported from recent capital raises. We highlight these investments because these investees are drivers of recent inflation in component costs, especially DRAM memory. Although the market typically ignores the “one-time” investment gains that Alphabet has made, we think these extremely large gains have served as a de facto hedge for the rapid, incremental capex spending requirements. In other words, we estimate the $150 billion in investment gains on SpaceX and Anthropic (if realized) could effectively cover incremental DRAM-related capex costs for several years. These one-time gains are not included in our core calculations for returns – but suffice it to say, Alphabet has plenty of excess profitability to continue investing both responsibly and aggressively.

In addition, Alphabet announced it would begin delivering its proprietary Tensor Processing Units (TPU) to external customer data centers, representing a very sizable new addressable market. Alphabet has spent more than a decade developing and iterating on TPU systems for internal workloads, claiming to reduce the cost of serving its AI model (Gemini) by almost 80%. We expect Alphabet to continue delivering excellent returns as it helps proliferate AI use cases for businesses, consumers, and data centers. Despite outperformance during the quarter, we continue to manage portfolio concentration risk by limiting individual position sizes to 10%.

Although Microsoft, Amazon, and Meta have different business models and were not necessarily top drivers of performance during the quarter, we view their investment opportunity set, from both a compounding and returns perspective and a component-cost-hedge perspective, as similar to Alphabet’s.

Microsoft ended the most recent quarter with average gross assets of more than $585 billion (trailing two years), up 22%, yet generated $170 billion in gross cash flow over the prior four quarters, up 27% from a year ago. Again, these are astonishing figures: Microsoft added an average of $100 billion in assets and $27 billion in incremental cash flows. The Company is achieving nearly 30% returns while compounding the assets that generate those returns at more than 20% – extraordinary! On top of that, Microsoft reportedly has an investment in OpenAI (OPENAI) worth over $100 billion, so we think these huge investment gains, if realized, also effectively serve as a hedge against commodity inflation, particularly incremental DRAM-related capex over the coming years.

As we have noted before, Amazon is another member of this elite group generating high returns, and we think it is being quite rational by rapidly compounding its asset base at these returns. During the quarter, Amazon grew revenue by 17% and operating income by 30%. While the bears continue to complain about Amazon’s $200 billion in capex growth and dwindling free cash flow, we estimate this incremental capex will increase the 2025 total asset base by around 28%. With 30% cash flow growth on what we assume is at least 28% asset growth, we conclude Amazon is achieving at least as good, if not better, returns on capital than it has previously – yet the stock is trading near historically depressed multiples. This is another telltale sign to us that the Company’s aggressive free cash flow reinvestment is very rational and that the depressed valuation presents an excellent long-term investment opportunity for us. Moreover, we estimate the Company’s investment in Anthropic is worth at least $100 billion and, if realized, will serve as another effective hedge against commodity memory price inflation, especially in DRAM, over the next few years. That should be long enough to offset inflation until more DRAM capacity comes online to moderate prices.

Last but not least in the capex spending bonanza is Meta Platforms. While they have certainly received its share of criticism for recently increasing its 2026 capex plans by around $10 billion, citing DRAM inflation, we’d like to point out that the warrants Meta holds on Advanced Micro Devices (AMD), related to a strategic sourcing arrangement with AMD struck in late February (~5 months ago), are now worth close to $90 billion, by our estimate (a swift nine times more than the incremental DRAM inflation for 2026). Meta’s sourcing advantage from its massive scale gives it the bargaining power to keep commodity cost inflation in check, which investors are so worried about. Although this investment in AMD does not technically qualify as a GAAP-based accounting hedge, it is certainly an economic hedge that we believe investors have completely overlooked, even though it should serve to blunt the effects of DRAM inflation and bolster returns for years to come.

Another beneficiary of the AI spending boom has been Taiwan Semiconductor Manufacturing. Revenues grew by more than 40% (in USD), on top of 40% growth last year. Its leading-edge fabs and packaging capacity are fully booked, driving margins to all-time highs. Much of this capacity was put in place a few years ago, before generative AI was a household and business-wide term. More recent demand signals from customers – including Nvidia (NVDA), Broadcom (AVGO), and even Micron – indicate AI-related growth of over 50% per annum through 2029. Whereas the Company used to have demand visibility only a few quarters out, it now has visibility a few years out. As with long-held portfolio risk mitigation, we limit all positions to 10% weightings. We believe it is prudent to maintain this risk-management limit on the stock, especially given the massive investor inflows into semiconductor-levered stocks and the large speculative ecosystem (e.g., 2x- and 3x-leveraged single-stock ETFs) that has recently sprung up around them.

United Rentals was a top performer across portfolios. Equipment rental sales growth accelerated to 9%, while adjusted margins stabilized, driving 10% growth in earnings per share. This acceleration was driven by strong nonresidential construction end markets, particularly data centers and power projects, and by continued growth in megaprojects.

Apple was also a top contributor to performance during the quarter. Revenues grew 17%, driven by 22% growth in iPhone and 16% growth in services. The iPhone 17 family has catalyzed a solid upgrade cycle ahead of what we expect to be another strong launch later this year, featuring a new foldable form factor. Because input prices for DRAM have risen at a parabolic rate, the Company recently raised prices on some of its devices to pass these costs through. As one of the largest single purchasers of DRAM, the Company has strong negotiating leverage, but it can also implement hardware and software innovations to reduce its dependence on memory.

Visa contributed to quarterly performance, reporting accelerating revenue growth of 17%, driven by 11% growth in payment volumes and 21% growth in cross-border volume. Value-added services also grew 25% and now represent almost one-third of the Company’s total revenue. Agentic commerce remains nascent but could represent a new addressable market for Visa as the Company tracks and helps autonomous AI agents perform microtransactions. This contrasts with just a few quarters ago, when the market was fretting about the risks agentic commerce could pose. We think Visa’s global scale, including acceptance at over 130 million merchants, and deep integration with almost 15,000 financial institutions make it a valuable partner for agentic commerce startups.

Company Commentaries

Hermès

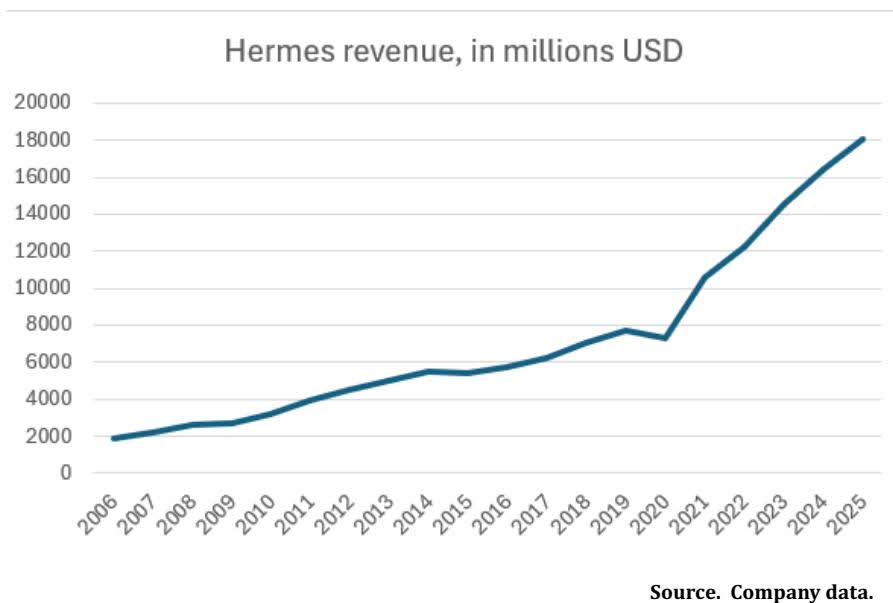

We recently initiated positions in Hermès International, one of the world’s leading designers, manufacturers, and retailers of ultra-luxury leather goods, apparel, and accessories.

Hermès began in 1837 as a harness and saddle maker in a Paris shop, after its founder, Thierry Hermès, trained for eight years as a master craftsman. From the beginning, the company focused on artisanal skill, high-quality materials, and exceptional craftsmanship, earning awards and serving a prestigious upper-class clientele in and beyond Paris, including world leaders and royalty. Over time, the Company expanded into adjacent equestrian-related product categories, including bags, leather gloves, and scarves, intended for riders. In the 20th century, with the advent of the automobile and the fading importance of horses, the Company applied its leather goods expertise to areas such as luggage, leather jackets, and handbags.

Today, the Company still produces equestrian equipment as part of its leather goods segment, which remains its largest at 44% of revenues. The Company has also built important businesses over time in apparel and accessories (28% of revenues), a highly recognizable and unique business in silk scarves and other fabrics (9% of revenues), and businesses in watches, beauty, perfume, and other areas.

The Company has likewise expanded from its single store on Rue Honore in Paris—which still exists—to nearly 300 stores globally. Top geographic markets now are Asia (over 50% of revenues), Europe (roughly 25%), and the Americas (roughly 20%), with sales in the Middle East relatively insignificant. However, Middle Eastern customers make sizable contributions to sales in other markets as tourists.

Over time, Hermès has continued to focus on the factors that led to its success nearly 200 years ago: using highly skilled artisans to hand-produce its products from the highest-quality materials. This has given the Company a lasting brand heritage that has driven demand, commanded deservedly high prices, delivered high, consistent profitability, and insulated the Company to a large degree from competition.

Hermès has repeatedly produced iconic products with decades of staying power, indicating that the brand’s success is not built on the caprices of fashion whims or fads but on its heritage and quality. Some of these products include the Birkin bag, first produced in 1984 after the Company’s CEO shared a plane journey with actress Jane Birkin, who complained that there were no fashionable handbags suitable for a young mother; the Oran sandal, first launched in 1997 and known for its quality, comfort, simplicity, and versatility; and the Company’s iconic silk scarves, produced in very limited runs in a variety of patterns, originally intended to protect the long hair of horse riders and now adapted for a variety of uses.

Many brand names do not mean anything. To demonstrate this, one need only survey the detritus of “brand names” littered all over Amazon, which are clearly made-up noises for cheap, low-quality commodity products. Any company can spend advertising money to tell you that its product is great, preferably through some of our long-time holdings, Meta and Google. Advertising generally seeks to lead consumers to attribute some credit or personal affection to those brand names. Most of those companies are mass-producing products with cheap materials and methods in low-cost manufacturing markets; or perhaps with slightly better materials, methods, or manufacturing; or by trying to convince you that they are doing so with better design sensibilities, which are in fashion and sometimes are not.

Producing luxury goods by the hands of the most skilled artisans in markets such as France or Italy, using the highest-quality materials, which are usually produced in these same markets, is in fact a unique, personal appeal. Doing so with a brand that has developed a decades-long reputation for this (nearly centuries-long, in the case of Hermès), in reality and not only in an advertising pitch, earns you a loyal, often multigenerational following, which should lead to established premium pricing and sustainable high margins.

Selected Apparel, Footwear, and Accessories industry peers

EBIT margins, most recent FY

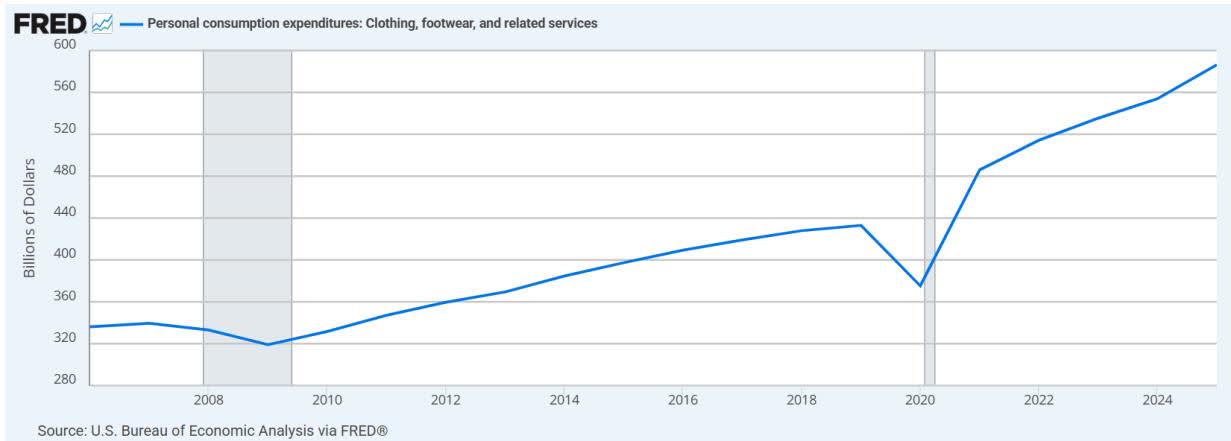

The Company’s long-term focus on the highest quality has led to sustainably strong demand and exceptional profitability. While we have found it difficult to obtain reliable, easily comparable data for the luxury goods industry—and there is an array of definitions of what “luxury” is—we can provide a direct comparison between Hermès and the U.S. Apparel, Footwear, and Accessories industry, which will be most familiar to our readers and comprises the majority of our investment opportunities in this segment.

According to the U.S. Bureau of Economic Analysis, U.S. personal consumption expenditures on clothing, footwear, and related services have grown at a compound annual growth rate of about 2.8% over the past 20 years.

Over the same period, Hermès has seen its revenue growth compound at 11.8%. Given the varying definitions of the global luxury goods market and the lack of particularly good data available to us, our best approximation is that the luxury market itself has roughly tripled over this time, for a CAGR of roughly 5.5%. Although the luxury apparel-footwear-accessories market has outgrown the standard market for those categories, the Company has capitalized on its strategy and heritage to deliver outsized growth relative to its industry. We would note that this period included two of the most traumatic economic periods in recent history: the 2007-2009 global financial crisis and the 2020 pandemic.

Another interesting component of the Hermès story, and of the ultra-luxury world in general, is the supply side of the equation. One could reasonably point out that a business strategy to limit supply is a sound approach in an industry seeking to cultivate an air of exclusivity and sustain high prices. An important point in the luxury goods industry is that supply appears constrained, whether or not that is a company’s strategy. Again, although solid industry data are hard to come by, our readers could search “luxury goods artisans’ shortage” and find more than 10 years of articles lamenting the shortage of skilled artisans in the industry.

The aging of the workforce, as older artisans retire and are not replaced, and the younger generation’s aversion to manual work. We understand that a skeptical person might not take some industry pronouncements at face value, and that a fear of supply shortages may drive both pricing and demand—we have found projections saying the industry is 20,000 artisans short. We have found others saying the industry is 90,000 people short, and there may be some leeway in those numbers. However, we would point out that luxury companies across the industry, as well as the governments of France and Italy in particular, have been investing in training and schools to encourage more people to enter these positions. Hermès itself has opened 24 workshops in its leather goods division, with four more scheduled to open over the next four years. Industry peers LVMH and Bottega Veneta likewise have invested heavily in training and education, and some Italian luxury houses are even making agricultural investments to support Italian silk and wool production.

So, we would say that Hermès and the rest of the industry may have planned for some supply scarcity over time as an effective strategy. Still, there seems to be a genuine scarcity of skilled artisans, with fairly compelling evidence that companies and governments are investing to prevent the supply situation from worsening. Again, we will point out that when you combine strong, consistent demand with limited and arguably declining supply, you get the pricing power and high profitability that we see with Hermès.

Turning to a real-life example, let’s refer back to the iconic Birkin bag. Perhaps you know someone who would like to get their hands on a new one? Here’s how. First of all, walking into a Hermès store isn’t going to do it. The bags are made in very limited quantities, so there will not be any in stock, and the few that trickle into stores are immediately sold by allocation to the store’s most important customers. How do you become one of the most important customers? You develop a long personal relationship with one of the sales associates. The key to this relationship is consistently spending a lot of money on other Hermès products. Sifting through various blogs, it seems you might be expected to spend at least one to two times the price of the Birkin bag before you even have a chance, at which point you might be offered one in a period somewhere between six months and three years later. If you are so lucky, retail prices start around $15,000 for smaller bags made from the company’s “base leather, ” and you can spend multiple times that amount on other designs. If you aren’t able to get an allocation directly from the store, though, don’t worry – you can buy the same bag from someone selling it on the secondary market for roughly double that price. This is very powerful brand equity for a bag introduced 42 years ago. This brand is not a fad. We also highly suspect that this brand equity would no longer exist if Hermès had chosen at some point to skimp on artistry or materials.

On the valuation front, the stock is rarely what many people—especially those outside the U.S. large-cap growth arena—would call “cheap.” Still, we note that significant insider ownership (the family owns 66.7% of the shares) serves as a valuation floor, and a business model of this quality warrants a premium valuation. The stock recently retreated to a more reasonable level after the company’s most recent results showed a modest negative impact from the outbreak of war in the Middle East. This disrupted some travel and particularly weighed on the business of Middle Eastern customers in tourism markets worldwide; we view this impact as temporary.

In summary, we believe Hermès is a true example of a company with significant brand equity, earned through an established, nearly 200-year history of doing things that are not easily replicated: having skilled artisans produce the highest-quality products from the highest-quality materials. The process and the brand work together to create both significant demand for the company’s products and significant profitability, and we expect the company to continue this trajectory of growth and profitability.

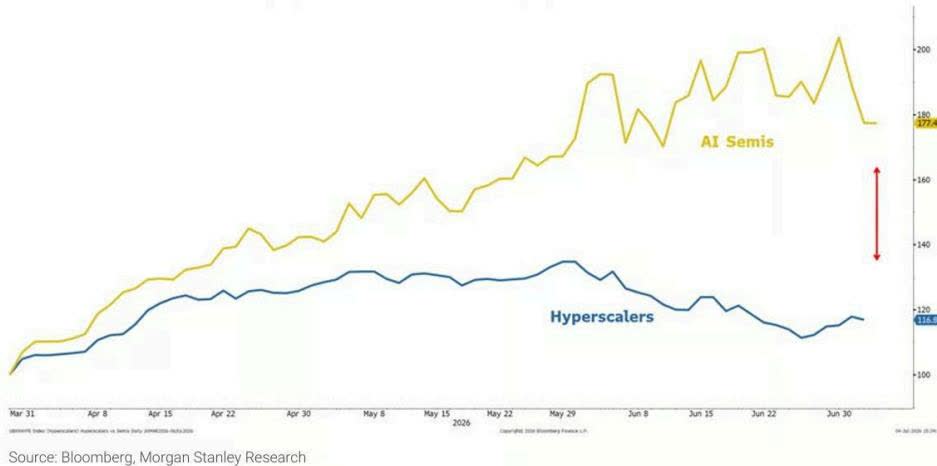

Are Hyperscalers Still Magnificent?

Exhibit 7: Divergence between Hyperscalers and Semis Likely to Close As Capex May No Longer Be Rewarded Unequivocally in the Markets for Now

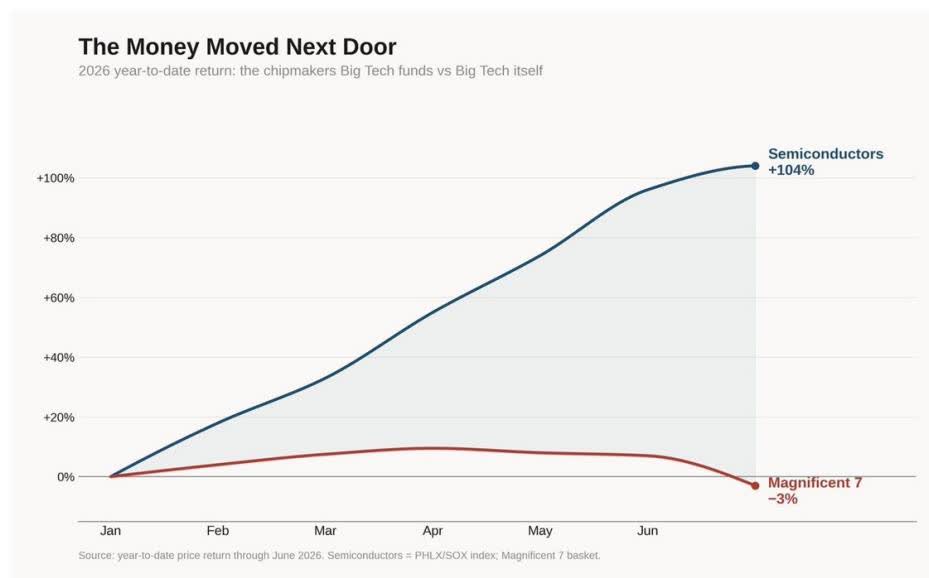

Are the Magnificent 7, particularly the hyperscalers, still magnificent? We certainly think so and have increased our weightings accordingly. Recall the Mag 7: Apple, NVIDIA, Tesla (TSLA); and the four “hyperscalers” – Alphabet, Amazon, Meta Platforms, and Microsoft. For some background, we’ve owned Alphabet and Apple for two decades, Meta Platforms for years, Microsoft for a few years, and, more recently, Amazon.

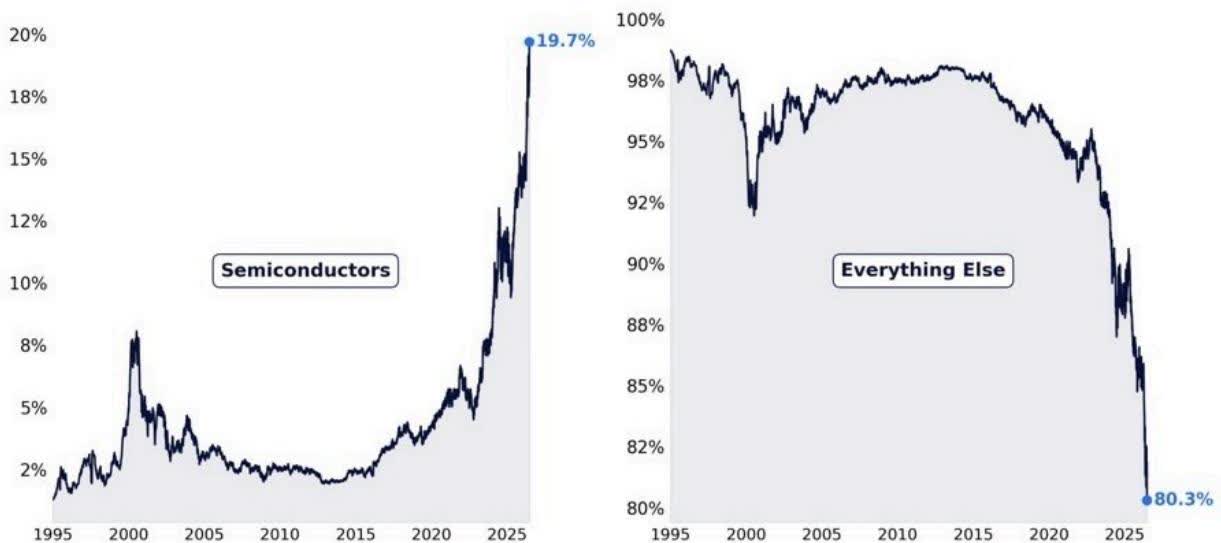

With the exception of Alphabet, which has generated stellar returns over the past one, three, and five years, the other three hyperscalers’ stocks have struggled mightily in 2026. The headwinds for hyperscalers are manifold. First, sentiment has turned quite negative, with the view that spending hundreds of billions to build out AI platforms will certainly benefit technology hardware companies but also materially harm the profitability of the hyperscalers. Second, billions rotating into technology hardware stocks (particularly memory stocks) have been funded relentlessly by selling hyperscaler stocks. On this score, semiconductors currently make up nearly 25% of the S&P 500 Index, up from about 5% just a few years ago. Third, IPO funding for SpaceX and, prospectively, for the IPOs of Anthropic and OpenAI has come at the expense of selling hyperscaler stocks.

Earlier in the Letter, we made our case that the short-term hit to hyperscaler free cash flow, although real, is outweighed by the fact that current hyperscaler profitability is better than most fear. More pertinent to our longer-term bullish view, we expect the hyperscalers’ platforms to be central and critical to managing and providing AI for enterprises of all sizes.

The following graphics illustrate the outsized performance of semiconductor stocks. No doubt, the explosion in capex by hyperscalers has, in turn, boosted earnings for many technology hardware companies, but none more than semiconductors. Please note that our best-performing stock over the past one-, three-, and five-year periods has been Taiwan Semiconductor Manufacturing. The stock has also been among our largest positions. In addition, because the stock is an ADR, it is not part of the benchmark indices. In other words, our position in the stock has been pure active share. That said, our underweight in semiconductors over recent years has been a significant performance headwind.

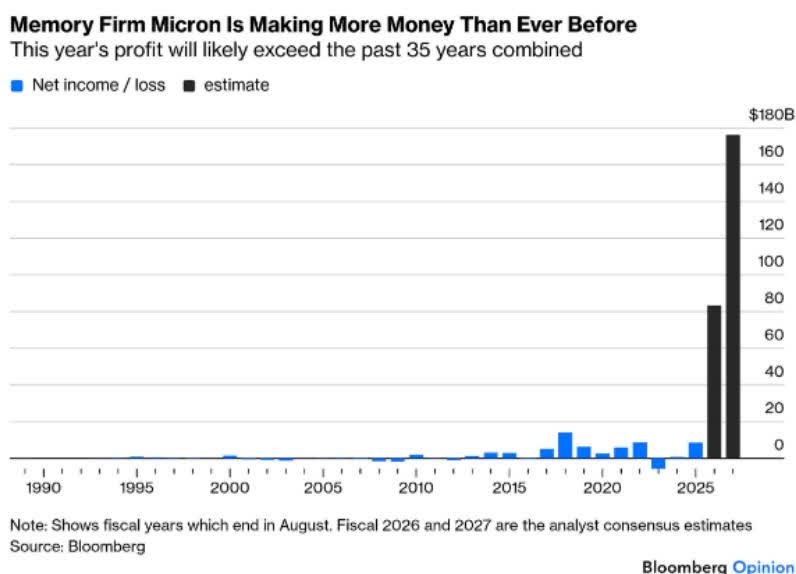

We have a long history of investing in semiconductor stocks. Over the decades, these stocks have included Intel (INTC), Micron Technology (MU), Applied Materials (AMAT), Linear Technology, and Analog Devices (ADI). The key lesson we have learned (we have the scars to prove it) is that the semiconductor sector is notoriously cyclical, both in business cycles and in stock prices. These stocks are the epitome of a “momentum” stock. When business is booming, earnings estimates are typically far too low relative to actual results. Demand, combined with pricing power, drives incredible margin increases. Further, in boom times, earnings soar, and expectations for future earnings do as well. Stocks boom. Said through the lens of fundamentals, peak earnings deserve trough valuations.

The current semiconductor cycle is historic. Consider SK Hynix (SKHY)’s recent results. The South Korean company holds a majority share of high-bandwidth memory, which is essential for the current generation of GPUs. Revenue of $35.5 billion was up 198% year over year, crushing consensus estimates, and the company’s net income surged 398%. Not to be outdone, Micron Technology’s profit surge is one for capitalism’s history books.

(An aside. As this Letter is being finalized – June 13 – Some froth has come out of semiconductor memory stocks – at least the casino-like trading in South Korea stocks. Consider, the 3X levered SK Hynix fund, which was launched just 30 days ago, peaked at $36. Today it is trading at $4. The 2X fund has too crashed, down -70% from recent highs.)

Memory company earnings will surely grow over the next few years, at least until demand cools and/or supply shortages wane. However, and this is key, it only takes a modest cooling in current red-hot demand or a modest easing of the significant supply shortage for these stocks to drop as suddenly as they have risen because expectations reverse; earnings expectations will always be too high once growth-rate deceleration kicks in. It is the second derivative change in the rate of growth that matters. This is how cyclical top traps are set. The market always sniffs out a peak in earnings growth acceleration well before the cycle turns. Again, it matters little if earnings continue to grow; the stocks lead fundamental results, often by years.

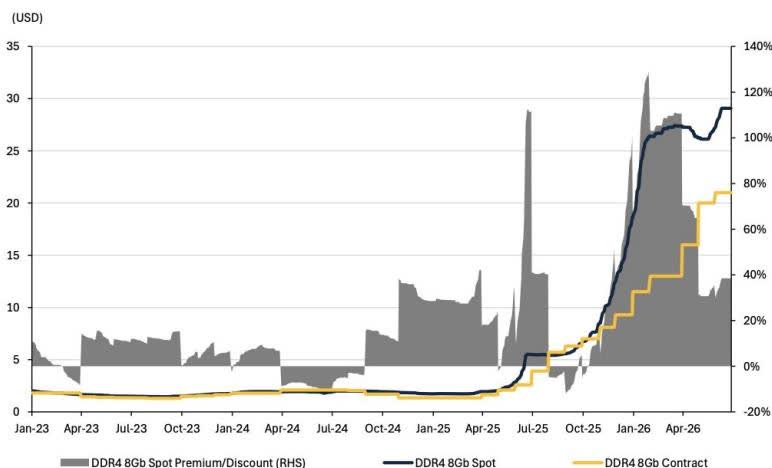

Exhibit 2: DDR4 8Gb spot is trading at 38% premium vs. latest contract price – DDR4 8Gb spot pricing premium/discount vs. contract

Source: Trendforce

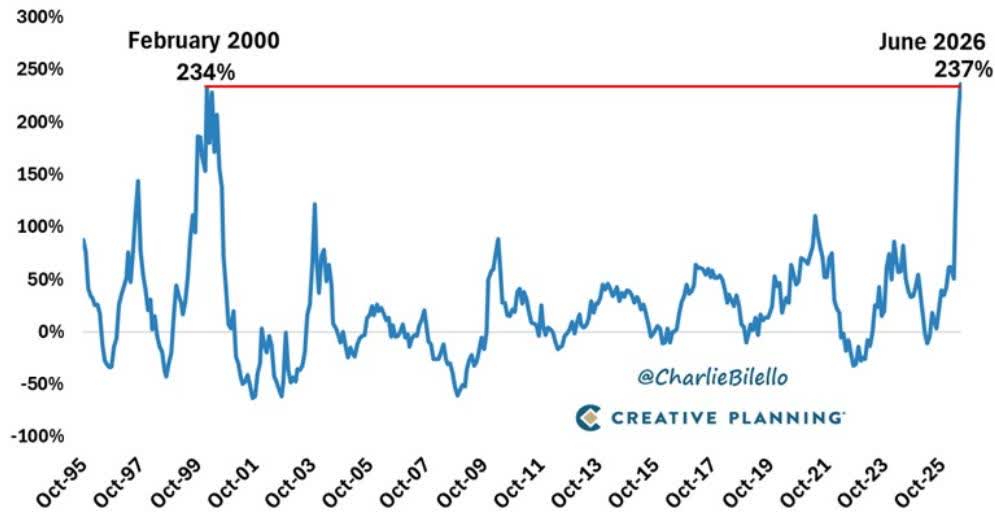

Chip Stocks Head for Best First Half Versus S&P 500 Ever

■ Philadelphia Stock Exchange Semiconductor Index – S&P 500 Index 1H performance

Source: Bloomberg

Semiconductor Index (($SOX)) – Rolling 14-Month Returns

(October 1995 – June 2026 – as of 6/30/26)

Semiconductor Weight in the S&P 500

Since 1995

Source: Bloomberg, S&P Global, as compiled by Citadel Securities, GMI, as of June 2026. Figures are for illustrative purposes only. Past performance figures do not guarantee future results.

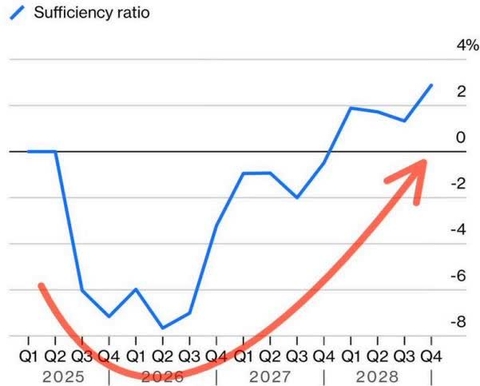

Memory Shortage Won’t Last Forever

The industry might be oversupplied as early as 2028

Source: Bloomberg Intelligence Bloomberg Opinion

We are reposting this graphic from the title page.

Source: Refinitiv, as of 11/10/2025. File #1077

Big Mo’s Low-Quality Rally – High-quality stocks with strong balance sheets continue to be pummeled

Note: Figures show long-short total return starting 04/02/2025 (Liberation Day). Source: Bloomberg Factors To Watch Bloomberg Opinion

As we have written (and discussed with clients) over the past 34-plus years, we usually underperform when momentum strategies are ascendant. That has been true over the past 15 months. Our underperformance has been stark. From mid-April 2025 through June 30, our Composite is up 25%, a relative pittance compared with the 90% gain for the Invesco

S&P 500 Momentum ETF (SPMO). It is little surprise that the SPMO portfolio is composed of 50% technology stocks, mostly semiconductor stocks, plus other AI-related stocks that dominate the largest holdings within the large-cap benchmark indices.

We continue to fish in the high-quality pond. So far, this scarlet-letter pond continues to yield opportunities. In recent months, we’ve added Chubb, Toll Brothers (TOL), United Rentals, Progressive, and, most recently, Hermès. Good fishing.

David A. Rolfe, CFA | Chief Investment Officer

Michael X. Quigley, CFA | Senior Portfolio Manager

Christopher T. Jersan, CFA | Portfolio Manager

Universe: eVestment US Large Cap Growth Equity (Percentile)

References

- 1 Portfolio returns and contribution figures are calculated net of fees. Contribution-to-return calculations are preliminary. The holdings identified do not represent all securities purchased, sold, or recommended. Returns are presented net of fees and include the reinvestment of all income. “Net (actual)” returns are calculated using actual management fees and are reduced by all fees and transaction costs incurred. Past performance does not guarantee future results. Additional calculation information is available upon request.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Business

ETMarkets Smart Talk | India’s retail investing boom is structural, 40 crore demat accounts possible in 10 years: Sandeep Nayak

With India’s young demographic profile, rising incomes and growing awareness of digital investing, Nayak believes the number of Demat accounts could rise from around 20 crore currently to 30 crore over the next five years and potentially touch 40 crore in a decade.

In an interview with Kshitij Anand of ETMarkets, Nayak said that while the bull market has accelerated the entry of new investors, the underlying growth is being driven by India’s demographics and increasing financialisation of savings.

However, as younger investors, including Gen Z, embrace equities and derivatives, he cautioned that a get-rich-quick mindset and inadequate focus on risk management remain key challenges.

Nayak also discussed how technology, AI, data-driven research and personalised guidance could shape the next phase of digital broking. He believes that while the past decade was about democratising access to markets, the next 10 years will be about helping investors make more informed decisions, with research, risk management and multi-asset investing playing a crucial role in long-term wealth creation. Edited Excerpts –

Kshitij Anand: So, firstly, let us just understand how Centrum Finverse is taking shape and expanding its digital footprint. I would also want to know how the transformation of GalaxC fits into the overall roadmap.

Sandeep Nayak: When we started Centrum Finverse, we looked at the market landscape and saw that the market had expanded and access to markets had been democratised. But really, we found that traders were making losses. If you see SEBI’s report, which is published annually, retail traders over the last four years have lost close to three-and-a-half lakh crores, and the beneficiaries are players like Jane Street.

There was one background: you had discount brokers who created a platform and expanded the market. We saw that full-service brokers were only catering to the mass affluent and upwards. Really, retail was at God’s mercy. So, we felt that if there was a tech-enabled platform focused on research and guidance, there was a way to be made in this market, and you would get your place in the sun.

I will give you a simple analogy. I mean, if you give a very good cricket bat to everybody, they are not going to become good batsmen. You need coaching, technique, practice, and a lot of effort goes into becoming a good batsman. Or, if you have a high-performance car, digital access is like giving you a high-performance car, but to reach the destination, you still need a GPS.

So, we want to be that player who is bringing research and guidance and hand-holding customers. And if you see our app, which we have launched, GalaxC, which you referred to, is our trading app. We have created a lot of scientific tools to help investors navigate their journey in the markets.

If you look at options trading, or any trading for that matter, we will show the client the risk-reward. Before he enters the trade, he can see his maximum loss and maximum profit, so he knows. And then he knows the risk-reward ratio. So, if you say your loss is Rs 1,000 and there is an option to make Rs 3,000, then your risk-reward is 1:3. But if the trade involves a loss of Rs 1,000 and a profit of Rs 1,000, then the risk-reward is 1:1. Or, if the loss is Rs 1,000 and the profit is only Rs 500, why are you getting into that trade?

So, getting this tool into the hands of retail investors is kind of enabling them to get to that level. Of course, there is a lot more to do, but this will help them in making sure their journey is a lot better in terms of risk management. They know what they are doing. It does not guarantee you profits all the time because you can still incur a loss, but at least before you get into the trade, you know you can digest that loss. So, that is what we have done, and we think that this differentiation will bear out over time.

I mean, I would say the last phase of the last 5-10 years, really, if you count it, was about democratising access. The next 10 years, I think, will be about informed decision-making. It is easy to open a Demat account, (—) a trading account; it can be done in two minutes. But creating wealth is much harder, and that is where we want to help the investor.

We want to bring science to investing through data-driven research, analytics, and decision-support tools so that the investor relies less on emotion and more on evidence. That is what we have focused on. Right now, it is probably my talk; this will bear fruit. I think for this differentiation to be visible in the market, it is a process, and I feel that over the next one to three years, players who have this differentiation are the ones who will be the winners, not just those who have the platforms.

Kshitij Anand: And, in fact, when you were conceptualising GalaxC, what was the kind of need or problem that you were trying to address that was not being addressed earlier, but with GalaxC, it would actually suffice all the needs?

Sandeep Nayak: So, I will tell you that there are two worlds in this industry. One world is of players offering a platform at a low cost, where cheap brokerage is everything. And the other world is where you are offering full-service research, but offering it to the cream, that is, the mass affluent and upwards.

We wanted to bring the best of both worlds to retail investors. So, give them a platform where they can execute efficiently at a low cost, and at the same time, hand-hold them and give them guidance, which is available only to the mass affluent and upwards. And that is how we conceptualised GalaxC—to get the best of both worlds for the retail investor.

Not only give them a platform where they can play around, not just give them a cricket bat, but also coach them, hand-hold them, and show them how to actually play a long innings. That is our motto at Centrum Finverse.

Kshitij Anand: In fact, the digital broking space is also evolving, especially after COVID, you could say. So, let us say we take the past five to six-odd years, and it has really evolved. A lot of players have actually come into the picture. So, what does, let us say, the next decade look like, and who will actually emerge as winners? We are also seeing some consolidation happening, so yes, that is also there.

Sandeep Nayak: See, what I see is that technology has enabled us to offer services to retail customers in a personalised manner. Just like HNIs are getting personalised services from wealth relationship managers, technology can give a retail customer personalised service.

So, today, we are actually able to track a customer who comes to our app. Just like Bigg Boss—you have seen this Bigg Boss show, where there is a Bigg Boss tracking what is happening—you know which section he went to in the app and which section he was spending more time on. So, accordingly, you can tailor-make your offering to him.

So, people who are able to personalise the tech platform and offer personalised services and guidance to retail investors will be the winners. So, when you come in, I know, (—) “Welcome, Kshitij.” I know what your portfolio is, I know what you have been doing, so I am kind of pre-empting and giving you things that you would like to see. So, that is one differentiation.

And the second one is platforms that offer multi-assets. For example, we have also visualised that GalaxC will offer multi-assets. Today, we have equity and derivatives—all these stock brokerage services are the core offering—but we also have mutual funds. We have IPOs. And we are working on bonds and US investing, etc. Right now, we offer these offline, but we will bring the entire thing digitally.

We are going to gradually offer all financial products that a retail investor would want, digitally and with hand-holding—not just a platform, but hand-holding on what he needs to do.

For example, on our mutual fund platform, if you see the mutual funds listed, they are only the whitelisted funds that we are recommending, that our research recommends. And if you want to buy something else, you can still pick it from the drop-down and go buy it. But we are saying these are the ones—if you want to invest in large-cap funds, this; if you want to invest in mid-cap funds, this; if you want to invest in small-cap funds, this.

We have thematic baskets. I mean, portfolio management is available only to HNIs; the minimum threshold is Rs 50 lakh and upwards. Our baskets are available at as low as Rs 30,000. So, you can get a defence basket and know which stocks to buy. There is a power basket, which is thematic. And you are able to participate in the right stock selection without having to go to a top-quality fund manager, so research is doing that.

So, like I said, it is not just a platform, but being a part of the journey and trying to deliver value over the long term. Finally, where does he build trust with me? If I am able to deliver some alpha on his investments, he has to make some profit from using my platform. So, the research team that we have built is focused on that.

I mean, while HNIs get 30-page reports, retail investors do not need a 30-page report. It is probably a one-pager with the rationale that they need to invest in. So, we are focused on creating value for the retail investor because, as a house, we have an institutional brokerage that covers about 200 stocks, where we have a financial model and 30-page detailed reports, which can be given to institutional investors and high-net-worth investors.

Similarly, we run a private wealth outfit where wealth offerings are given to private banking customers. The research we do is about how we package this in a consumable format for the retail investor.

Kshitij Anand: Good that you pointed out the research part of it because most of the discount brokers or brokers that we see are providing the services, but there is no research as such involved in it, and that is where you sort of make that….

Sandeep Nayak: That is where we want to differentiate.

Kshitij Anand: And that will really help the business to carry on. And you rightly pointed out that you will be introducing a lot of other things that are getting into the mainstream, such as US investing, bonds, and other products. Is that something that will fuel the engine for the next five to 10-odd years?

Sandeep Nayak: Yes, over 10 years. But since the segment is retail, they will initially prefer investing domestically, investing in thematic baskets, and investing in mutual funds. I think US investing, etc., is for the mass affluent and upwards because you need to do LRS remittances, etc.

But we are offering certain ETFs. We are highlighting certain ETFs to retail investors, saying that you do not need to remit money abroad to buy US stocks to get exposure. There are certain ETFs through which you can get exposure, where you are getting the benefit of investing in the US. So, that is where….

We do not need to launch a separate US investing product. There are enough products that we need to highlight to investors to help them get into it and take advantage of that exposure.

Kshitij Anand: Now that we are talking about US investing, one theme that has really gained popularity is AI, especially in the last couple of years, or 12 to 18 months, you could say. How are you using AI in the business, technology, or app to make it more convenient for investors?

Sandeep Nayak: Yes, we are working on AI tools to assist customers. Right now, the tools that we have are quant-based, and technology is being used to provide quant-based ideas. We have two things in the works, including an AI-based platform where customers can ask questions and interact. It will first look at our own research that the house generates and answer based on that. If we do not have a report, it will probably look at outside research and give customers what they want. So, there will be an interface that we will provide. We are working on that.

And we also need some regulatory approvals, etc. We need to showcase it to the exchanges and get these things cleared, and we are working on that.

Kshitij Anand: Retail participation has picked up recently, and a lot of new retail participants have come in who are in the age bracket of, let us say, 25-plus. So, a lot of Gen Zs have also come into the picture. Is it because of the recent bull run, you could say, or is there genuinely interest coming in from the younger population? I am sure it is largely about how to make money in a short period of time. Is the focus more on that, or are these guys after long-term investments?

Sandeep Nayak: I think this particular move, the growth that you are seeing, is structural, and it has to do with India’s demographics. If you see, India has 65% of its population in the working-age group, and the median age of the working population is 29. More and more people are getting into the workforce and learning about… they are earning income, saving, and learning about financial planning and investments. So, this trend will continue.

And right now, we have close to 20 crore Demat accounts. Maybe in the next five years, it will be 30 crore, and in 10 years, 40 crore. That is a natural progression because people coming into the workforce will need to invest, and awareness of investing digitally and in equity markets has gone up.

I mean, previous generations were told to be conservative and safe, go into FDs, and go into physical assets. But this generation, Gen Z, which is what we are catering to through Centrum GalaxC, is willing to experiment and take risks. At 25, they are willing to trade options and derivatives, and that is why you are seeing the loss figures as well.

There is a learning process, and when you are learning, obviously, you have to pay. Markets are a place where you have to pay a price to learn. So, this trend will continue. The bull market has certainly helped. I am not saying that it has not helped. It has helped people take cognisance and come to the markets faster, but structurally, India is built in such a way that this has to keep growing. Over the next 10 years, you will probably see phenomenal growth.

Our penetration is still low. I mean, while we have 20 crore Demat accounts, the number of unique investors will be lower because people have multiple Demat accounts; somebody may have two or three. So, we still have less than about 10% of the population investing in the markets. And in advanced markets, we have seen 60-65%. So, even if we get to 20-25%, the opportunity is huge. We (—) do not need to go to 60-65%.

So, structurally, we are built for this. We are in the right place at the right time, and the markets will keep expanding. Bull markets will come and go. The pace may slow down in a bear market, but it will still keep growing. I am not in the camp that believes that it will stop. We will go to 40 crore in 10 years, and how fast we reach 40 crore is the question, not whether we will reach it. We will definitely reach it. So, that is there.

Kshitij Anand: So, we have seen a new lot of investors over the past, let us say, five-odd years. Ten years back, there was a different breed of investors. Now, the new lot has not seen any really big dip, like the 2008 Financial Crisis that we saw, and some of the other big dips that have happened. Are there any mistakes that you think the new lot is now making, or do you think they are more advanced or more upgraded, you could say, in their mindset compared with the older lot?

Sandeep Nayak: No, I think everybody has their fair share of mistakes. It is not that you have to go through… I mean, like the life cycle of a person from birth to death, there are a lot of experiences he goes through. As a child, he goes to school….

Kshitij Anand: We keep on saying that, “Arre, ab toh bahut mature log aa gaye hain,” like now the….

Sandeep Nayak: No, they have more information at hand. They have more information available digitally, but markets are a place where you will tend to make those mistakes that previous generations have made. And some of the things we commonly notice are that youngsters have a get-rich-quick mentality. Even among all the people who come to the markets, this market is like Bollywood—everybody wants to become a star like Shah Rukh Khan. So, when they come here, they feel they can make a killing.

Kshitij Anand: And every stock should be a blockbuster.

Sandeep Nayak: Yes, they feel they can make a killing. This is a place where they think, “My stars are good, I will make a killing,” only to realise that you get killed first. So, you learn. So, that get-rich-quick mentality is there; that is one.

And second, they are not paying sufficient attention to risk management, and that is what we are trying to educate them about. Before a trade, if I am telling you what your risk and reward are, what the loss is and what the potential gain is, at least I am trying to tell you: do not play blind; know what you are doing.

So, it is like that statutory warning on a cigarette pack—it is injurious to health—but at least we are trying to highlight to you what it is and saying that trading is not speculation; it is a science. Please understand.

On our platform, you can execute four trades simultaneously—two sell and two buy—and with a single click, they will get executed. But before that, it shows you, once you… what the margin involved is, what the risk is, what the reward is, and what the risk-reward ratio is.

So, that is where risk management comes in, and new investors fail to focus on that. We are trying to highlight to them: look at the risk first. So, that is how… your trading longevity is preserved. And it is good for me as a business if I train them and get them to become good traders, so that is the objective we have.

It is just like if I open a gym and put 10 trainers there. If there are no trainers, a person will go, stretch himself, get injured, and not come to the gym for six months. But if there is a trainer who is guiding him, he will exercise within his limits and come back the next day. So, that is what we want.

So, these are the two things, and every generation learns them the hard way. They will have to, but we are trying to help them by highlighting the risk….

Kshitij Anand: To bring down the learning curve….

Sandeep Nayak: Yes, and that is what, as a platform, we are trying to help you with—that these are the mistakes people make; look at the risk before you dive in.

Kshitij Anand: So, over the past few years, a lot of products have actually come into the system, and new investors are more open to those products as well. So, how relevant do you feel the multi-asset approach is at this point in time?

Sandeep Nayak: No, the multi-asset approach is highly relevant. I mean, it is one of the better risk management tools as well because when you invest in different asset classes, you are spreading the risk. Markets work in cycles, and cycles do not synchronise with each other.

So, when one asset is in a bull market, the other may be in a bear market, or when one is in a bear market, the other may be in a bull cycle. So, it reduces the impact of market cycles on your portfolio. You are able to better manage volatility, and if you do that, your long-term, consistent, risk-adjusted return is higher. And that is why it is better to have a multi-asset approach.

Because, let us say, you are only in equities. One year, you might get a 25% return if you are lucky; the next year, it could be a loss of 15% as well. But if you have mixed it with fixed income, gold, and silver, probably, if there is a hit in equities, these asset classes are still giving you returns. So, your risk-adjusted return is higher than what it would have been if you were only in a single asset class.

So, both from a risk diversification perspective and for better long-term risk-adjusted returns, a multi-asset strategy is the way to go.

Kshitij Anand: And how is technology shaping the industry at this point in time?

Sandeep Nayak: Technology is one of the big drivers of the financial services space, more so in broking and investments, where differentiation is coming in and where there is more and more excitement because you can offer hyper-personalised services to each customer.

I mean, because of the AI and data analytics tools that are available, we can decide what the risk profile of a customer is and what he should be offered, and technology allows us to do that with a uniform customer experience. If I have people doing it, it depends on how each person is handling the customer, whereas technology, at least, does not have behavioural biases and does not have a mood of its own for the day. There is an objective tool that is telling you what you need to do, so that is one important aspect.

Second, technology also helps you make smarter decisions with risk under control. It reduces behavioural biases. It extracts information easily and analyses it, and early risk detection is also possible. So, those are the things that technology is helping us with, and that is where we want to bring differentiation and add value to our customers—the retail customers who do not have the luxury of having a person advising them or a relationship manager advising them. So, using technology as the guiding factor for the investor has been our focus.

Kshitij Anand: Obviously, when we are using more technology and when we have more personalised data on the web, trust is something that definitely comes into play. How are you balancing that aspect with investors?

Sandeep Nayak: See, trust is always built over a period of time, and Centrum has been in the financial services space for almost 30 years now, across different businesses. So, there is one overarching brand called Centrum, which investors trust.

But more importantly, at Centrum Finverse, being transparent and consistent, highlighting the positives as well as the risks—I mean, that has been the focus for both trading and investments—and that, I believe, will build trust over a period of time.

Ultimately, trust is built if the customer perceives that there is value addition for him from this platform. And that is the value addition that we bring—for trading, the scientific tools to help you compete with the Jane Streets; for investing, the simplified one-pagers giving you the investment rationale; and thematic baskets that give you a basket of stocks if you want to play a particular theme. Because with a single stock, you can go wrong, but when you build a basket, the returns are a little better and you manage the risk better.

So, these things that we are doing for customers will not be visible in one day, but over a period of time, customers will differentiate and give value to this particular approach of ours. It is a question of time, and this is how we want to build trust and continue the journey of Centrum Finverse.

Kshitij Anand: And looking forward, how do you see the industry shaping up, let us say, over the next three to five years?

Sandeep Nayak: Like I already said, technology is enabling you to offer personalised services to each customer, and the next phase is where using technology to hand-hold, guide, and offer personalised services will be the focus and will differentiate the men from the boys.

And second is, like I said, hand-holding and guiding in terms of the tools that you offer. I mean, there is always plenty of information available, but guiding customers in terms of how to interpret that data and what judgement you bring to the table as a research house is what will differentiate.

Over the next 5-10 years, this will be the… Like I said, access has been democratised. Now, it is about making informed decisions, hand-holding customers, and adding value to them. That is the focus, and that is where digital broking is headed, where value addition is the most important thing because cheap brokerage is available everywhere, but advice is not available everywhere, and research is not available everywhere. That is where we hope to bring differentiation. And we feel that over the next 10 years, the market will reward these players.

(Disclaimer: Recommendations, suggestions, views, and opinions given by experts are their own. These do not represent the views of the Economic Times)

Business

What does ‘Las Malvinas Son Argentinas’ mean? All about the Falkland row that followed Messi’s Argentina into the World Cup final

Football and geopolitics rarely mix this dramatically, but Argentina’s dramatic 2-1 win over England in the World Cup 2026 semi-final did exactly that. Within minutes of the final whistle, a banner referencing the Falkland Islands was on the pitch, Lionel Messi and company were mobbed by fans, and social media was flooded with one question in different forms: what exactly is this decades-old dispute, and why does it still spill onto a football pitch?

Also Read: Argentina be banned from FIFA World Cup final against Spain for showing Falkland banner?

Here’s a simple breakdown of everything you need to know.

What does “Las Malvinas son Argentinas” mean?

“Las Malvinas son Argentinas” is Spanish for “The Falklands are Argentine” (or, more literally, “the Malvinas are Argentina’s”). “Las Malvinas” is simply the Spanish name Argentina uses for the Falkland Islands, the name comes from “Îles Malouines,” what French sailors from the port city of Saint-Malo called the islands back in the 1700s.

For Argentines, the phrase isn’t just a geography lesson, it’s a statement of national identity. It reflects the country’s official, constitutionally-backed position that the islands rightfully belong to Argentina, a claim Britain firmly rejects. You’ll see the phrase on murals, license plates, school textbooks, and yes, occasionally, on football banners.

Why did Messi-led Argentina’s team show the Falklands banner?

After Argentina came from behind to beat England 2-1, with Lautaro Martinez heading in a stoppage-time winner off a Messi assist, several players, reportedly including Giovani Lo Celso and Nicolas Otamendi, held up the “Las Malvinas son Argentinas” banner during celebrations before it ended up on the pitch.

What’s the Argentina vs England Rivalry?

The opponent. Argentina vs England fixtures always carry historical weight, dating back to the 1982 Falklands War and even earlier flashpoints like Diego Maradona’s “Hand of God” goal in 1986.

Pre-match tension. Argentina’s Vice President had reportedly used provocative language about England in the buildup, and FIFA had already restricted Falklands-related flags from being brought into the stadium as a precaution.

Precedent. This isn’t new territory for Argentina’s football setup, the same banner cost the Argentine Football Association a £20,000 FIFA fine back in 2014, ahead of a friendly against Slovenia.

For many Argentine fans and players, waving the banner after knocking out England was less about football and more about a symbolic, patriotic moment. For FIFA, however, it’s a potential breach of rules that explicitly ban political statements and symbols inside stadiums, meaning Argentina could now face disciplinary action, most likely another fine, even as they prepare for Monday’s final against Spain.

Why are the Falkland Islands important?

The Falklands might be a remote, windswept archipelago with a population smaller than a small Indian town, but their importance goes well beyond size:

Historical and national symbolism: For Argentina, the islands represent an unresolved chapter of national identity and sovereignty, tied closely to the loss of the 1982 war. For Britain, they represent a hard-won territory and a test case for self-determination.

Strategic location: Sitting in the South Atlantic near key shipping routes and close to Antarctica, the islands have long carried military and geopolitical significance.

Natural resources: The surrounding waters are rich fishing grounds, and the Falklands basin has shown potential for oil and gas reserves, adding an economic dimension to the sovereignty question.

A live diplomatic issue: This isn’t just history, 2026 has already seen Argentine President Javier Milei publicly reiterate his country’s claim on the anniversary of the 1982 invasion, while reports of a leaked US government memo questioning British title to the islands briefly reignited global attention on the dispute earlier this year.

Who owns the Falkland Islands now?

As things stand, the Falkland Islands are administered by the United Kingdom as a self-governing British Overseas Territory. Locals handle their own internal affairs through an elected Legislative Assembly, while the UK retains responsibility for defence and foreign policy.

Argentina, however, does not recognise this arrangement and continues to formally claim sovereignty over the islands, referring to them as part of its own national territory.

Key facts on where things stand on Falkland Islands:

- The roughly 3,500 residents of the islands hold full British citizenship.

- In a 2013 referendum, Falkland Islanders voted almost unanimously, around 99.8%, to remain a British Overseas Territory.

- The United Nations lists the Falklands as a “Non-Self-Governing Territory” and has repeatedly urged the UK and Argentina to negotiate, but has never ruled in favour of either side’s sovereignty claim.

- No formal negotiations over sovereignty have taken place since diplomatic relations between the UK and Argentina were restored in 1990.

In short: Britain controls and governs the islands today, but the dispute remains legally and diplomatically unresolved, with Argentina continuing to press its claim through international forums rather than force.

Where is the Falkland Islands?

The Falkland Islands sit in the South Atlantic Ocean, roughly 300 miles (about 480 km) off the southern coast of Argentina, and around 8,000 miles from the United Kingdom. The archipelago consists of two main islands, East Falkland and West Falkland, along with hundreds of smaller islands, adding up to a land area roughly the size of the Indian state of Goa multiplied by nearly ten times over (about 12,000 sq km in total).

The capital, Stanley, is home to most of the population and sits on East Falkland. Despite being geographically closer to South America than to Europe, the islands remain culturally and politically British, right down to red phone booths and driving on the left.

What started as a football celebration has once again put a decades-old territorial dispute in front of a global audience. As Argentina prepares to defend their World Cup title against Spain, the Falklands conversation, much like the sovereignty question itself, shows no signs of settling down anytime soon.

A major logistics centre in Belmont’s Kewdale industrial area has been unanimously approved after planners and the proponent struck a late compromise on lot amalgamation, sustainability requirements and height controls.

United warns of nearly $6 billion fuel hit as oil-price surge weighs on outlook

Business

Palantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

Shares of Palantir Technologies climbed 1.26% on Wednesday, trading at $135.41 as of 11:55 a.m. EDT, up $1.69 on the day, as the AI software company continued building momentum from an expanded partnership with Nvidia and a series of positive analyst actions ahead of its upcoming second-quarter earnings report.

Palantir confirmed this week that it will report its second-quarter results after market close on Monday, August 3, giving investors a clear timeline for the company’s next major fundamental catalyst. Wall Street analysts currently expect Palantir’s second-quarter revenue to grow 80% year over year to approximately $1.8 billion, according to consensus forecasts.

An Expanded Nvidia Partnership Targets Government Deployment

Much of the recent positive momentum for Palantir traces back to an expanded collaboration with Nvidia, combining Nvidia’s AI computing platform with Palantir’s core product suite, including its Artificial Intelligence Platform, Ontology, Foundry and Apollo offerings. The expanded partnership is specifically designed to enable government agencies to deploy AI models within classified and air-gapped environments, while continually refining those models based on mission-specific feedback.

The offering builds on the earlier successful commercial launch of BrokerOS, along with a recent multi-million-dollar contract with Wheels Up to serve as the launch customer for Enterprise BrokerOS, further extending Palantir’s push into commercial applications beyond its traditional government and defense customer base.

Additional Commercial Partnerships

Beyond the Nvidia expansion, Palantir has continued announcing new commercial partnerships in recent weeks. The company recently expanded its existing partnership with Surf Air Mobility, committing additional engineering and go-to-market resources to accelerate development and commercial release of SurfOS, including its OperatorOS, OwnerOS and SurfOS Enterprise Solutions product lines.

Palantir has also announced a strategic partnership with SNP SE at the company’s Transformation World event, along with a new operating model framework developed jointly with Rackspace Technology aimed at supporting AI deployment in production environments.

Analysts Continue Raising Price Targets

Palantir’s stock carries a consensus Buy rating among analysts, with an average price target of $187.42, according to recent tracking data. Several firms have issued bullish updates on the stock in recent weeks. DA Davidson upgraded Palantir to Buy on July 2, raising its price target to $175. Rosenblatt has maintained a Buy rating with a $225 price target as of early June, while Wolfe Research upgraded the stock to Peer Perform in mid-June.

Some analysts have pointed specifically to Palantir’s ability to convert pilot programs into high-value, multi-year contracts as a key driver behind recent upward revisions to price targets, describing a feedback loop in which fundamental business growth continues to justify the stock’s premium valuation and attracts additional momentum-driven investment.

A Shift From Government Contractor to Enterprise Powerhouse

Recent reports have highlighted accelerating adoption of Palantir’s Artificial Intelligence Platform among Fortune 500 companies, a trend some analysts have characterized as shifting the broader narrative around Palantir from a primarily government-dependent contractor toward a more diversified enterprise software company. That shift has been central to the bullish case many analysts have built around the stock in recent months.

A Valuation That Continues to Draw Scrutiny

Despite the positive momentum, Palantir’s valuation remains a persistent point of debate among market participants. The stock currently trades at a price-to-earnings ratio of roughly 146.51 and at approximately 64 times sales, according to recent market data, levels that continue to draw scrutiny from more skeptical investors even as bullish analysts argue the company’s growth trajectory justifies the premium.

CEO Addresses Broader AI Concerns

Beyond the company’s specific business developments, Palantir Chief Executive Alex Karp has continued using public platforms to address broader societal questions tied to artificial intelligence. In a recent appearance on Mathias Döpfner’s “MD Meets” podcast, Karp warned that AI could become one of the biggest drivers of wealth inequality in the United States, describing the issue as “the biggest problem in this country.” Karp elaborated further on the dynamic, framing the AI-driven economic shift as a fundamental transformation with significant societal implications.

A Volatile Trading Pattern

Palantir’s stock has continued to exhibit significant day-to-day volatility even amid its broader upward trajectory this year. Shares gained 2.2% on Monday specifically in response to the earnings date announcement, an unusual reaction given that the news itself did not include any actual financial results. The stock has also experienced sharp single-day moves tied to other catalysts in recent weeks, including a roughly 9% single-day surge on July 1 following the initial announcement of Palantir’s strategic partnership with Nvidia, alongside a financial disclosure revealing that President Donald Trump holds a significant personal stake in the company.

Trading Range Reflects a Turbulent Year

Palantir’s stock has traded within a wide 52-week range between $106.37 and $207.52, according to recent trading data, reflecting substantial volatility throughout the year as investors have weighed the company’s strong revenue growth against persistent valuation concerns and periodic competitive pressure from major cloud computing providers expanding their own AI and data analytics offerings.

What Comes Next

With Palantir’s second-quarter earnings report now scheduled for August 3, investors are likely to focus closely on the company’s free cash flow generation as a key indicator of whether its premium valuation remains justified. Several market analysts have specifically pointed to free cash flow trends as the most important metric to watch when Palantir reports next month, suggesting that strong cash generation could reinforce the bullish case for the stock, while any signs of deceleration could reignite the valuation concerns that have periodically weighed on shares throughout 2026.

AIER educates Americans on the value of personal freedom, free enterprise, property rights, limited government and sound money. Our ongoing scientific research demonstrates the importance of these principles in advancing peace, prosperity and human progress. www.aier.orgFounded in 1933, AIER is a donor-based non-profit economic research organization. We represent no fund, concentration of wealth, or other special interests, and no advertising is accepted in our publications. Financial support is provided by tax-deductible contributions, and by the earnings of our wholly owned investment advisory organization, American Investment Services, Inc. (https://www.americaninvestment.com/)

Business

Argentina-Falklands Banner Row: Messi’s team be banned from FIFA World Cup final against Spain? What FIFA rules and past cases say

Just when the football world thought Argentina vs England couldn’t get any spicier, the aftermath of Wednesday night’s semi-final in Atlanta added a fresh layer of controversy. Argentina came from behind, Anthony Gordon had put England ahead in the second half, before Enzo Fernandez levelled things up and Lautaro Martinez, set up by a inch-perfect Messi assist, struck deep into stoppage time to send the Albiceleste through to a second straight World Cup final.

Why Argentina’s Falkland banner is such a big deal

For anyone unfamiliar, the Falkland Islands, called “Las Malvinas” in Argentina, are a British Overseas Territory sitting roughly 300 miles off Argentina’s coast, thousands of miles from Britain itself. Argentina has claimed sovereignty over the islands going back to the 19th century, a dispute that escalated dramatically in 1982 when Argentina’s military government invaded the territory, triggering a 74-day war. That conflict claimed the lives of over 900 people, including 255 British servicemen and roughly 650 Argentine troops, before Britain regained control.

The wound has never fully closed, and it resurfaces almost every time the two nations meet on a football pitch — memories of Diego Maradona’s “Hand of God” goal in 1986 haven’t helped either. This year, tensions were already running hot before kickoff after Argentina’s Vice President reportedly used inflammatory language describing the English in the build-up to the match.

Argentina-Falkland Controversy: What FIFA’s rulebook actually says

This is where things get serious for Argentina. Both FIFA and the International Football Association Board (IFAB), which frames the laws of the game, are unambiguous on this front. Their stadium code of conduct explicitly prohibits banners, flags, or any paraphernalia carrying political, offensive, or discriminatory messaging inside venues.

The IFAB rulebook goes further, stating that team equipment cannot carry political, religious, or personal statements, and that any breach leaves the player or team open to sanction, whether from the competition organiser, the relevant football association, or FIFA itself.

In simple terms: if match officials or FIFA’s disciplinary body determine the banner counts as a political statement (and given its content, that’s fairly likely), some form of punishment could follow.

Has this happened before?

Yes, and this isn’t even the first time this exact banner has landed Argentina in hot water. Back in 2014, the Argentine Football Association was fined £20,000 by FIFA after players held up an identical “Las Malvinas son Argentinas” banner ahead of a friendly against Slovenia.

Based on that precedent, and how FIFA has typically handled similar political-symbol breaches at major tournaments since, most reports suggest the punishment this time is likely to be a financial one too, potentially in the region of £30,000, rather than anything affecting Argentina’s participation in the tournament.

So, will Argentina actually be banned from the final?

No, at least not based on anything reported so far. Despite some sensational headlines doing the rounds, there is no confirmed FIFA ruling barring Argentina from Monday’s final. The tie against Spain, who beat France 2-0 in the other semi-final, is very much still on. What Argentina realistically face is a fine and possibly a formal warning, in line with how FIFA has dealt with this exact banner controversy before.

FIFA is yet to issue an official statement on the matter, and until a formal disciplinary decision is announced, this remains a developing story rather than a settled one.

But it’s what happened after the final whistle that’s now dominating headlines.

What actually happened

As players celebrated on the pitch, a banner reading “Las Malvinas son Argentinas”, translating to “The Falklands are Argentine”, was unfurled by members of the Argentina squad, reportedly including Giovani Lo Celso and Nicolas Otamendi, before it was placed down on the turf. Reports suggest the banner had originally come from the stands, was briefly tucked away, and then brought back out during celebrations.

The timing made it more pointed than usual. FIFA had specifically restricted Falklands-related flags from being brought into the stadium ahead of the match, wary of exactly this kind of flashpoint given the fixture’s history.

Head coach Lionel Scaloni had, before kickoff, tried to keep the narrative purely sporting, hoping the game wouldn’t be overshadowed by politics. That request didn’t quite hold up once the final whistle blew.

The battle for Number 10 is over.

An overwhelming number of Labour MPs have nominated Andy Burnham. Under Labour’s rules he needs trade union support too.

He crossed that threshold today. He is moving into Number 10 on Monday.

But the beneath-the-radar battle for Number 11 Downing St is continuing. Whoever Burnham appoints as chancellor – and next-door neighbour in Downing Street – will send a signal of his intent both to politicians and to the bond markets.

The official line from team Burnham is that no decision has been taken.

Announcements on cabinet posts are not expected to be made until Monday, when Burnham moves to Number 10.

Discussions have been taking place amongst a tight group of people – the next Number 10 chief of staff James Purnell, Louise Haigh and the former MP who stood aside for Burnham, Josh Simons.

When Burnham won the subsequent Makerfield by-election the widespread assumption was that the Energy Secretary Ed Miliband would move to the Treasury.

But there has been both noisy and more subtle attempts to influence Burnham’s choice of chancellor – ranging from unions with workers in the oil and gas industry and who distrust Miliband’s instincts, to Sir Keir Starmer’s unpaid ‘cost of living’ tsar Lord Walker, the boss of Iceland.

He runs supermarkets but argues that it’s the bond markets that would “freak out” if an “ideological” chancellor was installed in the Treasury.

In recent days, a number of MPs close to Burnham – who have no animus to the energy secretary – believe the likelihood of appointing Miliband has lessened significantly.

The caveat is that they are not making the decisions, but are discerning the mood.

Those close to Miliband believe that it’s not only highly possible that he will still be appointed but highly desirable too.

They point to his credentials. He has an economics background, was an adviser in the Treasury under Gordon Brown and chaired the Council of Economic Advisers.

He has ministerial experience in the last Labour government and this one. He knows his way around. A colleague put it like this: “He can make the Treasury do what it doesn’t want to do.”

Miliband has offered advice to Burnham regularly and recently and would be in lock-step with Burnham in the task of spreading growth, in Burnham’s words, “to every postcode”.

As for the bond markets, one supporter has stressed his adherence to the fiscal rules on debt and borrowing, and another put it more colourfully: “He isn’t Che Guevara.”

Many in the parliamentary party would expect him to move to Number 11. If he isn’t, some on the party’s soft left will think that Burnham has refused the first fence in the race to change Britain.

Billionaire investor Warren Buffett has described Bill Gates’ relationship with late sex offender Jeffery Epstein as “distasteful”, but said he himself had made mistakes in life by being friends with people “who weren’t great”.

On Tuesday, Buffett’s firm Berkshire Hathaway stopped giving donations to the Microsoft co-founder’s charity for the first time in 20 years and instead handed his remaining stock to foundations linked to his family.

Buffett told CNBC he and Gates have had a “wonderful friendship” but confirmed his pivot over donations followed Gates’ testimony to US Congress about Epstein.

Gates called Buffett “a dear friend”, adding: “My gratitude to Warren is immeasurable.”

Gates appeared before the US House Oversight Committee in June to answer questions about his relationship with Epstein, who died in a New York prison in 2019 while awaiting trial on sex trafficking charges.

In a transcript of his testimony, Gates said that he had been introduced to Epstein in 2011 as someone who could help raise billions of dollars for global health, which is a key focus of the Gates Foundation.

He said: “I recall being aware that Epstein had faced prior legal issues, but I did not fully understand the extent of the crimes he committed.”

In 2008, Epstein had pleaded guilty to soliciting a minor for prostitution and procuring a person under age 18 for prostitution.

Gates told the committee: “I should never have met with Epstein in the first place. Based on what I know now, I understand that even if he had delivered the donors he promised, it would not have justified associating with him.”

Buffett said on Wednesday he had read Gates’ testimony.

He said: “While it’s distasteful, while he made mistakes, I’ve made mistakes in hiring all kinds of people, choosing friends and finding out later that one way or another they weren’t what I thought they were.

“So, I found nothing in there that was beyond what I could picture myself doing.”

Buffett said the decision to stop donations to the foundation did not come as a surprise to Gates. The two met around three weeks ago for three hours.

The 95-year-old said: “At some point I had read what Congress had come up with, I’d read everything and all I can say is I don’t know whether I’ve done dumber things but I’ve done many dumb things in life.”

Buffett added that he and Gates have had an “enormous number of good times together” since they met in 1991. “It has been a wonderful friendship,” he said.

Gates said: “I cherish the time we spend together. I hope we have much more of it ahead.”

SInce 2006, when Buffett pledged to make annual donations to the Bill and Melinda Gates Foundation, as it was then known, “throughout my lifetime”, he has given $47bn (£34.7bn) to the charity.

But even without his backing, the foundation still holds “very substantial resources”, said Buffett.

In 2025 alone, the Gates Foundation gave away $8.5bn in charitable support.

While Buffett originally pledged a lifetime commitment two decades ago, he explained that his thinking has evolved over time.

When he first made the pledge, Buffett noted that he did not feel his three children were ready to manage such vast sums, but he now believes they are fully capable and deeply aligned with his goals.

- Global AI adoption reached 17.8% of the working-age population in Q1 2026, up 1.5 percentage points from the prior quarter, according to Microsoft’s Global AI Diffusion Report. The UAE led all nations at 70.1%, while 26 economies now exceed 30% usage. The United States ranked 21st with a 31.3% usage rate.

- Asia saw notable acceleration, driven by improved multilingual AI capabilities, with South Korea, Thailand, and Japan recording the largest regional gains. Despite this progress, the gap between the Global North and Global South widened to 27.5% versus 15.4%. In software development, AI coding tools contributed to a 78% year-over-year rise in git pushes, while U.S. developer employment reached a record 2.2 million.

Global AI adoption climbed to nearly 18% of the world’s working-age population in the first quarter of 2026, according to Microsoft’s latest Global AI Diffusion Report, even as the gap between wealthy and developing nations continued to widen and Asia emerged as a surprising bright spot.

Key takeaways

- Global AI adoption reached 17.8% of the world’s working-age population in Q1 2026, with the UAE leading at 70.1% and 26 economies now surpassing 30% usage.

- Asia is the quarter’s biggest mover thanks to better multilingual AI, but the Global North–South gap widened to 27.5% versus 15.4%.