Crypto World

British Virgin Islands Emerges as a Major Crypto Hub Amid Growth

More than $1 out of every $10 in the world’s tokenized US Treasuries is issued through entities incorporated in the British Virgin Islands, according to BVI Finance. In its June “Destination Digital” report, the organization estimates that BVI-linked firms accounted for roughly $1.5 billion of a $14.98 billion global tokenized Treasuries market as of June 1—making the small Caribbean territory the second-largest jurisdiction after the United States.

The BVI’s rise appears tied less to headline “tax haven” narratives and more to the legal and regulatory scaffolding that tokenization projects need to operate within institutional-grade workflows. At the same time, industry usage of the territory is nuanced: most companies do not physically relocate to the islands; they often use BVI entities as the legal layer around token issuers, treasury vehicles, holding companies, or special purpose vehicles (SPVs).

Key takeaways

- The BVI is behind about $1.5 billion of $14.98 billion in global tokenized US Treasuries (as of June 1), placing it just behind the US by issuer jurisdiction, per BVI Finance.

- BVI selection is driven primarily by regulatory clarity and legal certainty, not by taxes, according to advisers and executives interviewed in the underlying reporting.

- Regulatory capacity is a differentiator: the BVI’s VASP regime (introduced via the VASP Act in 2023) is overseen by the BVI Financial Services Commission with an application process aimed at faster timelines.

- The territory functions as a corporate home, not a global engineering hub: multiple firms incorporated in the BVI conduct operations elsewhere.

- BVI-linked stablecoin activity and tokenized securities volume are notable, including a high number of tokenized securities tracked in the RWA.xyz dataset, according to Bernstein Research.

Tokenized Treasuries and the “legal home” effect

BVI Finance’s “Destination Digital” report highlights how concentrated the issuance of tokenized US Treasuries has become by jurisdiction. As of June 1, BVI-linked entities represented approximately $1.5 billion out of $14.98 billion in the global market, based on data compiled for the report.

Beyond Treasuries, the same reporting frames the BVI as a broader digital asset jurisdiction. It cites a stablecoin market cap of about $1.2 billion held in BVI-linked addresses and an estimated 28,000 stablecoin asset holders. It also points to regulatory momentum: more than 25 virtual asset service providers (VASPs) have been approved under the BVI’s VASP regime.

In the tokenized securities category, Bernstein Research data referenced by the report suggests the BVI hosts 305 tokenized securities in the RWA.xyz dataset—the highest count of any single jurisdiction. Together, these figures support the view that the BVI has become one of the leading destinations for real-world asset tokenization activity.

Still, the article’s core caveat is important for readers: tokenization is designed to be borderless, and projects can choose where to incorporate without moving their operational footprint. In practice, many digital asset firms treat the BVI as the legal base while teams, infrastructure, and day-to-day operations remain distributed globally.

Regulation and legal certainty outweigh tax assumptions

For years, offshore jurisdictions in the Caribbean have often been described primarily through a tax lens. But advisers and industry executives interviewed in the underlying reporting say that assumption doesn’t match how many tokenization-focused firms decide today.

Andrew Jowett, a partner at Appleby (BVI) Ltd, said clients typically compare multiple jurisdictions—such as the Cayman Islands, the United Arab Emirates, Singapore, and Switzerland—when structuring digital asset businesses. In his account, the “overriding factor” is digital asset regulation rather than tax.

The BVI does have tax advantages: it imposes no corporate income tax or capital gains tax on BVI companies, according to BVI’s financial services commission guidance linked in the reporting (see What tax structure BVI imposes). However, the argument presented is that many competing crypto hubs now offer tax neutrality, making legal and regulatory readiness the differentiator.

Executives echoed that sentiment. Saeed Al-Marri, CEO of Ethra (incorporated in the BVI), described tax neutrality as “table stakes,” adding that institutional adoption depends on legal certainty and clarity. Similarly, Jack Yang, founder and CEO of LTP (which operates regulated entities across the BVI, Hong Kong, Australia, and the UAE), said taxation is “secondary” to whether structures can pass institutional review.

In Yang’s view, a “tax-neutral structure” that banks, custodians, auditors, investment committees, or regulators cannot accept has limited practical value—particularly as tokenization moves deeper into traditional finance processes.

Orest Gavryliak, chief legal officer at 1inch (also incorporated in the BVI), framed the shift as a changing role for jurisdiction itself: it is not becoming irrelevant, but protocols increasingly weigh predictable rules, institutional credibility, and long-term sustainability over the lowest possible tax burden.

What the BVI VASP framework is designed to deliver

One of the central regulatory developments mentioned in the reporting is the BVI’s VASP regime. The BVI introduced the Virtual Assets Service Providers Act (VASP Act) in 2023, overseen by the BVI Financial Services Commission (FSC). BVI Finance and FSC guidance cited in the underlying material describe a targeted review cadence: responses to VASP applications within six weeks, with an aim to complete the review process within six months.

Fast, predictable processing matters in tokenization because projects often need regulatory alignment quickly to meet timelines for custody arrangements, distribution partnerships, and institutional onboarding. The article also argues that “ease of launch” and flexible corporate structuring have been part of the BVI’s appeal beyond tax incentives.

Jowett described the broader corporate-vehicle angle: companies can be set up quickly, the legal framework is flexible, and ongoing reporting is generally lighter than in onshore jurisdictions. The reporting also notes the BVI’s historical preference for corporate confidentiality, adding that BVI companies remain subject to AML and KYC expectations while beneficial ownership information is held by registered agents rather than being publicly disclosed as a register—reducing public-facing disclosure requirements.

Importantly, the accounts provided in the underlying reporting suggest confidentiality and tax neutrality were not the deciding factors for the interviewed companies. Instead, they pointed to legal certainty, regulatory clarity, and the ability to structure corporate arrangements efficiently as tokenization expands.

No “physical HQ rush,” just corporate anchoring

A recurring theme in the reporting is that BVI incorporation does not necessarily mean a company’s people or infrastructure move to the islands. Yang, speaking about LTP, said the entity does not employ full-time staff “on the ground.” Instead, governance is handled by its board while staffing support is drawn from elsewhere in the group.

The same distinction is described through examples across the industry. The article notes that Kraken’s parent company, Payward, is incorporated in the BVI, while the exchange’s primary operations are based in the United States. It also says 1inch’s team and operations are spread across multiple jurisdictions.

The practical implication is that the BVI may be winning a different competition than the one often associated with global tech hubs. It is not primarily attracting large engineering teams or flashy headquarters. Rather, it is becoming a legal anchor for digital asset businesses—particularly tokenization activity—where the corporate structure is a critical input to institutional acceptance.

For readers watching the next wave of real-world asset tokenization, the question is less “which country hosts the most staff” and more “which jurisdictions offer the cleanest path through institutional compliance.” The BVI’s case suggests that if the legal wrapper around a tokenized product can satisfy regulators and counterparties, the incorporation location can become a quiet but decisive advantage.

As more tokenized Treasury issuance, stablecoin usage, and tokenized securities migrate toward regulated frameworks, investors and builders should watch how institutional counterparties (custodians, auditors, banks, and investment committees) respond to BVI structures—and whether similar regulatory programs in other jurisdictions keep tightening timelines and compliance standards.

There is $1.6 trillion in Bitcoin sitting idle, earning nothing, doing nothing. Charles Hoskinson has a plan to put it to work on Cardano, and the plan quietly requires every transaction to burn a little ADA. Whether that saves Cardano or exposes its central problem is the whole question.

Summary

- Cardano founder Charles Hoskinson has laid out a strategy to bring Bitcoin into Cardano’s DeFi ecosystem through a platform called Pogun, targeting the roughly $1.6 trillion in idle Bitcoin.

- Pogun rolls out in three phases across 2026: a non-margin credit market in the second quarter, a yield application in the third, and a BitVM-based trust-minimized bridge in the fourth.

- The mechanism that matters for ADA holders: every transaction in the system requires ADA for fees, paid invisibly by Bitcoin users, creating a demand driver that Cardano’s token has lacked.

- It leans on Midnight, Cardano’s privacy partner chain, for confidential transactions, and on Cardano’s EUTXO architecture, which shares design lineage with Bitcoin’s own UTxO model.

- The sharp objection, raised by Cardano’s own community: if Bitcoin can be lent, earn yield, and settle without users noticing ADA, why hold ADA at all? The plan may build against its own token.

Cardano has a problem it has had for years, and it is not a technology problem. ADA trades around 94% below its 2021 high, the network’s DeFi activity has long lagged its ambitions, and its founder spends a meaningful share of his time denying rumors that he is quitting. What Cardano has never lacked is engineering and ideas.

What it has lacked is a reason for capital to show up. Charles Hoskinson’s answer, laid out across 2026, is audacious: stop trying to attract crypto capital to Cardano and go get Bitcoin’s instead. There is roughly $1.6 trillion in Bitcoin sitting idle in wallets, earning nothing, and Hoskinson wants to route a slice of it through Cardano’s infrastructure, with every transaction quietly paying fees in ADA. It is the most concrete demand thesis Cardano has produced in years. It also contains a contradiction its own community has already spotted.

The idle-Bitcoin thesis

The premise starts with a real and large number. Something on the order of $1.6 trillion in Bitcoin sits in wallets doing nothing productive. Bitcoin is superb as a store of value and poor as a financial instrument: it does not natively lend, earn yield, or plug into decentralized finance without wrapping, bridging, or handing custody to an intermediary. That gap, enormous dormant capital with no native way to work, is what every “Bitcoin DeFi” project is chasing, and Hoskinson has decided Cardano should chase it hard.

His framing, delivered publicly in May 2026 and reiterated through the year, is that Bitcoin holders would be able to access lending, yield, and privacy tools through Cardano without surrendering control of their assets. A dedicated team, described at various points as around 19 people, is building it. The pitch to Bitcoin holders is straightforward: keep your Bitcoin, but make it productive, through infrastructure that does not require you to trust a centralized custodian.

The pitch to Cardano holders is different and more important to the ADA investment case. Hoskinson has been explicit that the entire system runs on ADA underneath. In his own words, every single transaction requires ADA to happen; the Bitcoin user pays a fee in ADA but does not see it. The idea is to make ADA the invisible fuel of a Bitcoin-DeFi economy, generating persistent, usage-based demand for the token regardless of whether anyone is speculating on ADA itself. For a token whose central weakness has been the absence of a demand driver, that is the whole game.

What Pogun actually is

Pogun is the platform that operationalizes the thesis, and its structure is more concrete than Cardano’s roadmaps usually are.

It rolls out in three phases across 2026. The first, targeted for the second quarter, is a non-margin credit market: lending against Bitcoin without the liquidation-cascade risk that leveraged lending carries. The second, targeted for the third quarter, is a yield-focused application that lets Bitcoin holders earn returns.

The third, targeted for the fourth quarter, is a BitVM-powered bridge, a trust-minimized way to move Bitcoin onto Cardano infrastructure without the custodial risk that has plagued wrapped-Bitcoin products. Input Output Group sought treasury funding for the effort, with figures around 12.3 million ADA cited, as part of a larger proposal slate that also funded the Leios scaling upgrade.

The architecture leans on two Cardano-specific pieces. The first is Midnight, Cardano’s privacy-focused partner chain, which launched its mainnet in early 2026 and serves as the confidential coordination layer, letting Bitcoin holders use DeFi tools without exposing their positions publicly. Hoskinson has framed Midnight as proof of Cardano’s partner-chain model, specialized chains operating alongside the main network while drawing on its security.

The second is Cardano’s EUTXO accounting model, which shares design lineage with Bitcoin’s own UTxO model. That shared lineage is not incidental; it is part of the technical argument that Cardano is a more natural home for Bitcoin DeFi than account-based chains like Ethereum, because the two systems think about transactions in a similar way.

The sequencing is deliberate. The team has described building the credit market and liquidity first, so that by the time the consumer-facing products launch, there is already a functioning market underneath them instead of an empty shell waiting for users.

The bull case

The strongest version of this argument is that Cardano has finally identified the right target and built a credible, differentiated way to reach it.

The demand mechanism is genuinely elegant. Cardano’s problem was never capability; it was that ADA had no structural reason to be in demand beyond speculation and staking. Embedding ADA as the mandatory fee layer of a Bitcoin-DeFi economy creates exactly the kind of usage-based demand that speculation cannot provide, and that does not evaporate when sentiment turns. If Bitcoin DeFi on Cardano generates real volume, ADA demand rises mechanically with it, transaction by transaction, whether or not anyone is bullish on ADA as a trade. That is a far healthier demand base than the memecoin-and-narrative cycles driving other chains.

The target is also the right one. Every serious chain is chasing Bitcoin DeFi because the prize, a fraction of $1.6 trillion in dormant capital, is the largest untapped pool in crypto. Cardano bringing brokerage-grade patience, a privacy layer, and UTxO compatibility to that chase is a real differentiator against the wrapped-Bitcoin approaches that have dominated and repeatedly failed on custody and trust. A BitVM bridge that reduces custodial risk addresses the exact failure mode, hacked or insolvent custodians, that has burned wrapped-Bitcoin users before.

And it fits Cardano’s identity rather than betraying it. Cardano’s whole brand is methodical, research-driven, security-first engineering, often criticized as too slow. Bitcoin holders are, as a group, the most conservative and security-conscious in crypto. A careful, peer-reviewed, custody-minimizing approach to Bitcoin DeFi is arguably better matched to Bitcoin holders than the move-fast culture of other DeFi ecosystems. For once, Cardano’s slowness could be a feature aimed at exactly the audience that values it.

The bear case

The skeptical case starts with a question a Cardano community member asked Hoskinson directly, and it is devastating in its simplicity: what would be the point of holding ADA over Bitcoin? Are we building against our own core token?

The concern is real and structural. If the system is designed so that Bitcoin users pay fees in ADA without seeing it, then the design goal is explicitly to make ADA invisible. A Bitcoin holder using Pogun holds Bitcoin, earns yield in Bitcoin, and never needs to acquire, hold, or think about ADA. The fees are abstracted away. If ADA is successfully hidden from the user, then ADA is a backend utility token that the end user has no reason to hold as an investment, which means the demand is limited to whatever float the protocols need to operate, not the broad holder demand that supports a token’s price.

Making ADA the invisible plumbing is good for usage and potentially bad for ADA as an asset people want to own. Hoskinson’s answer, that transactions require ADA regardless, addresses mechanical demand but not the deeper question of why anyone holds ADA rather than the Bitcoin it is helping to mobilize.

The second problem is execution and timeline. Cardano has a long history of ambitious roadmaps that arrive late or underdeliver relative to the promise. Pogun’s phases are targeted across 2026, and Cardano’s governance has been visibly deadlocked, with treasury votes for exactly this kind of initiative facing friction and Hoskinson warning that rejecting research funding could drive engineers away. A plan that depends on multiple new components, Midnight, the BitVM bridge, the credit and yield layers, all shipping and integrating on schedule, is a plan with substantial execution risk in an ecosystem that has struggled to convert roadmap into adoption before.

The third problem is competition. Cardano is not alone in chasing Bitcoin DeFi; it is late to a crowded race. Bitcoin layer-2s, wrapped-Bitcoin protocols on Ethereum, and Bitcoin-native DeFi efforts are all pursuing the same idle capital, several with more liquidity, more developers, and more existing integrations than Cardano has managed to attract. Cardano’s DeFi TVL has sat around $1.1 billion at times, a fraction of Ethereum’s or Solana’s, which raises the question of why Bitcoin holders would route their capital through the ecosystem that has struggled most to attract capital in the first place. Being a natural technical home for Bitcoin DeFi does not help if the liquidity and developers are elsewhere.

The token question at the center

Everything about this plan comes back to one unresolved tension, and it is worth stating plainly because it is the crux of whether Pogun helps ADA or merely helps Bitcoin.

Cardano is trying to solve its demand problem by making ADA essential but invisible. Those two properties are in tension. Essential means every transaction needs ADA, which creates mechanical demand proportional to usage. Invisible means users never consciously hold or value ADA, which suppresses the discretionary demand that actually drives a token’s price above its pure utility floor. A token that is essential-but-invisible tends to trade at its utility value, the minimum float the system needs to function, rather than at the premium that comes from people wanting to own it. Ethereum resolved this tension by making ETH visible and desirable as an asset in its own right, through staking, through the ultrasound narrative, through being the reserve asset of its own economy. Cardano’s Pogun design points the other way, toward ADA as backend infrastructure.

The optimistic resolution is that sufficient usage makes even utility-value demand large. If Bitcoin DeFi on Cardano processes enormous volume, the mechanical ADA demand could be substantial even if no one holds ADA for love of it. The pessimistic resolution is that Cardano will have built a successful piece of Bitcoin infrastructure whose value accrues to Bitcoin holders and Pogun’s operators, while ADA captures only the thin utility margin, which is not the outcome ADA holders are hoping for when they cheer a Bitcoin-DeFi announcement.

Which resolution wins depends on numbers that do not exist yet, because the products are still launching. The second-quarter credit market and third-quarter yield app are the first real tests. If they generate meaningful Bitcoin volume and ADA demand rises visibly with it, the thesis has legs. If they launch quietly into the same low-liquidity environment that has characterized Cardano DeFi, then Pogun becomes another well-engineered Cardano initiative that did not move the token, and the community member’s question, why hold ADA over Bitcoin, will have answered itself.

Why Cardano needs this to work

To understand why Hoskinson is betting so heavily on Bitcoin DeFi, you have to understand how much pressure Cardano is under, because Pogun is not an opportunistic add-on. It is a response to an existential question the market keeps asking.

The pressure is visible in the numbers and the noise around them. ADA trades roughly 94% below its 2021 high, deep in the ranks of large-cap tokens that led the previous cycle and never recovered. Cardano’s DeFi total value locked, around $1.1 billion at times, is a fraction of Ethereum’s or Solana’s despite Cardano having been live since 2017 and commanding one of the most committed communities in crypto. Hoskinson has spent 2026 denying rumors that he is leaving the project and calling them fiction, which is not a thing founders of thriving networks typically have to do. And the governance apparatus, the CIP-1694 on-chain system Cardano is genuinely proud of, has been deadlocked over treasury proposals, with Hoskinson warning that rejecting research funding could push engineers out.

Underneath all of it is a criticism Hoskinson himself has accepted in his own framing: Cardano’s problem is not technology. He has said explicitly that it is not a node problem, not a problem of imagination, not a problem of execution capability, but a problem of governance, coordination, and ultimately getting capital and users to show up. That is a striking admission from a founder, and it reframes Pogun. Bitcoin DeFi is not just a product; it is Hoskinson’s answer to the accusation that Cardano builds impressive technology that nobody uses. If he can route Bitcoin’s enormous, idle capital base through Cardano, he solves the adoption problem and the demand problem at once, and he does it without needing to win the crypto-native DeFi users who have consistently chosen other chains.

That is why the stakes are higher than a normal roadmap item. Cardano has tried narratives before: smart contracts, then DeFi, then real-world assets, and none produced the adoption inflection the community keeps waiting for. Bitcoin DeFi is the biggest swing yet, aimed at the biggest target, and it arrives at a moment when patience with the slow-and-steady thesis is visibly thinning. If Pogun works, it vindicates the entire methodical approach. If it lands quietly like its predecessors, it will be much harder to argue that the next initiative will be different. Hoskinson has effectively staked the credibility of Cardano’s whole strategy on reaching an audience that has never been Cardano’s, which is either the boldest possible move or a sign of how few options remain.

What to watch

Three concrete markers will tell you which way this breaks.

The first is whether the Pogun phases actually ship on their 2026 timeline. The credit market was targeted for the second quarter and the yield app for the third; slippage on those dates, in an ecosystem already criticized for slow delivery, would be an early negative signal. Shipping on time, with working products, would be a genuine and somewhat unexpected positive given Cardano’s track record.

The second is Bitcoin volume through the system, not ADA price. The entire thesis rests on attracting idle Bitcoin, so the metric that matters is how much Bitcoin actually flows into Pogun’s credit and yield products once they are live. ADA price will be noisy and driven by the broader market; Bitcoin TVL on Cardano is the clean read on whether the idle-Bitcoin thesis is working.

The third is whether ADA demand becomes visible in the data as usage grows. This is the crux question made measurable. If Bitcoin volume rises and on-chain ADA demand rises with it in a legible way, the essential-and-invisible design is working as a demand driver. If Bitcoin volume rises and ADA does nothing, then the community’s fear was correct, and Cardano will have built valuable infrastructure for someone else’s asset. Hoskinson has made the boldest, most concrete bet of Cardano’s recent history. The next two quarters start to settle whether it was aimed at the right target or against his own token.

Frequently Asked Questions

What is Cardano’s Bitcoin DeFi plan?

It is a strategy, led by founder Charles Hoskinson, to bring Bitcoin into Cardano’s DeFi ecosystem and tap the roughly $1.6 trillion in idle Bitcoin. The centerpiece is Pogun, a platform letting Bitcoin holders lend, borrow, and earn yield through Cardano infrastructure without surrendering custody. Crucially, every transaction in the system requires ADA for fees, creating usage-based demand for Cardano’s token.

What is Pogun?

A three-phase Bitcoin DeFi platform rolling out across 2026: a non-margin credit market in the second quarter, a yield-focused application in the third, and a BitVM-based trust-minimized bridge in the fourth. It integrates Midnight, Cardano’s privacy partner chain, for confidential transactions, and builds on Cardano’s EUTXO architecture, which shares design lineage with Bitcoin’s UTxO model. Input Output Group sought around 12.3 million ADA in treasury funding for it.

How does this benefit ADA holders?

Through embedded demand. Hoskinson has stated that every transaction in the system requires ADA for fees, paid by Bitcoin users who may not even notice. If Bitcoin DeFi on Cardano generates real volume, ADA demand rises mechanically with it, independent of speculation. For a token whose main weakness has been the lack of a structural demand driver, that is the core of the investment argument.

What is the main criticism?

That the design makes ADA essential but invisible, which are properties in tension. If Bitcoin users pay fees in ADA without seeing it, they have no reason to hold ADA as an investment, so demand may stay limited to the minimum the protocols need instead of the broad holder demand that lifts a token’s price. A community member asked Hoskinson directly what the point of holding ADA over Bitcoin would be, capturing the concern that Cardano may be building against its own token.

How is this different from wrapped Bitcoin?

Wrapped Bitcoin typically requires trusting a custodian to hold the underlying Bitcoin, a model that has failed through hacks and insolvencies. Pogun’s fourth phase is a BitVM-based bridge designed to be trust-minimized, reducing reliance on a custodian. Combined with Cardano’s UTxO compatibility with Bitcoin and the Midnight privacy layer, the pitch is a more secure, more private way to make Bitcoin productive than existing wrapped approaches.

Why does Cardano think it can win Bitcoin DeFi?

Three arguments: its EUTXO architecture shares design lineage with Bitcoin’s UTxO model, making it a technically natural fit; its methodical, security-first culture matches Bitcoin holders’ conservatism; and its Midnight privacy chain offers confidentiality that Bitcoin holders value. The counterargument is that Cardano is late to a crowded race with lower liquidity and fewer developers than competitors, which may outweigh any technical fit.

When does Pogun launch?

Its phases are targeted across 2026: the credit market in the second quarter, the yield application in the third, and the BitVM bridge in the fourth. Given Cardano’s history of ambitious roadmaps arriving later than promised, and ongoing governance friction over treasury funding, whether these dates hold is itself a meaningful signal to watch.

Will this fix ADA’s price?

Unknown, and it depends on the essential-versus-invisible tension. If Bitcoin volume through Pogun is large, mechanical ADA demand could be substantial even without holders wanting ADA for its own sake. If volume is modest, or if ADA is so well hidden that demand stays at the minimum float the system needs, the plan could succeed as Bitcoin infrastructure while doing little for ADA as an asset. The next two quarters of launches are the first real test.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. It describes a development roadmap whose components are still launching and whose outcomes are uncertain. Nothing here is a recommendation to buy or sell any asset. Always do your own research. Information is accurate as of July 17, 2026.

The network that moves the world’s money spent 9 months building a blockchain, and the most important decision it made was what not to put on it. No stablecoins. No public tokens. Just bank deposits, wearing a new coat.

Summary

- On July 9, SWIFT launched a blockchain-based shared ledger with 17 major banks, including Citi, HSBC, UBS, and BNP Paribas, for round-the-clock cross-border payments using tokenized deposits.

- The ledger is built on Hyperledger Besu, an EVM-compatible architecture, developed with Consensys in 9 months, and it is positioned openly as the banking industry’s answer to a $315 billion stablecoin sector.

- The decisive choice is the instrument. SWIFT built this for tokenized deposits, not stablecoins. That distinction determines who controls the money, whether it is insured, and whether it funds lending.

- Tokenized deposits keep money on bank balance sheets, carry deposit insurance, and preserve credit creation. Stablecoins pull money into reserves, sit outside the banking system, and remove liquidity from it.

- For SWIFT, this is a structural shift: for the first time in 53 years, it is moving from a pure messaging network that never touches funds to an active coordination layer for the movement of value.

For 53 years, SWIFT has done exactly one thing: move messages. When a bank in Singapore pays a bank in Sao Paulo, SWIFT carries the instruction, not the money. It is the postal service of global finance, and it never once opened the envelope.

On July 9, 2026, that changed. SWIFT switched on a blockchain-based shared ledger with 17 of the world’s largest banks, and for the first time in its history it is coordinating the movement of value rather than just the messages about it. The financial press covered the launch as a technology story, which it is.

The more important story is a choice buried inside it: SWIFT built this thing to carry tokenized deposits and pointedly not stablecoins, and that single decision is a statement about who the banking system intends to let issue digital money. This piece is about that choice, why it matters, and who it leaves out.

What SWIFT actually launched

The facts first, because they are concrete and verified across SWIFT’s own release and independent reporting.

On July 9, SWIFT announced its blockchain-based shared ledger was ready for initial use, with 17 banks across 6 continents preparing to pilot live transactions. The roster reads like a directory of global banking: ANZ, BNP Paribas, BNY, Citi, DBS, First Abu Dhabi Bank, FirstRand, HSBC, Itau Unibanco, Lloyds, Mashreq, MUFG, OCBC, Standard Chartered, UBS, UOB, and Wells Fargo. The system was built in 9 months from announcement to production readiness, developed with input from financial institutions globally and, per multiple reports, with Consensys involved in the build.

Technically, the ledger uses an EVM-compatible architecture based on Hyperledger Besu, functioning as a shared orchestration layer that validates inter-bank payment commitments while preserving existing compliance, credit, risk, and control standards. Its purpose is specific and narrow: enable 24/7 cross-border payments, including overnight and on weekends, that current infrastructure cannot support because it depends on overlapping business hours between sender and receiver. Final settlement still occurs through existing payment rails. The ledger does not replace correspondent banking; it coordinates on top of it.

SWIFT’s chief business officer framed the move as extending the trust and stability of incumbent finance into the frontiers of digital money. That sentence is corporate, but it is also precise. The whole design is about carrying something old, bank money, on something new, a shared ledger, without letting go of the controls that make bank money what it is.

The choice that defines it

Here is the decision that matters more than the technology, and that most launch coverage mentioned only in passing: SWIFT built this for tokenized deposits, not stablecoins.

A tokenized deposit is a digital representation of money held in a regulated commercial bank, issued by that bank on a blockchain, maintaining a one-to-one relationship with the deposit on the bank’s balance sheet. It is commercial bank money with a new wrapper. A stablecoin is a token pegged to a currency and issued by a non-bank entity, backed by reserves such as Treasury bills that sit outside the banking system, and it operates on public blockchains accessible to anyone with a wallet.

They look almost identical. A dollar-denominated stablecoin and a tokenized dollar deposit both claim to be worth $1, both move on a blockchain, both settle in seconds. The New York Fed, in a February 2026 staff report, drew the structural line that the surface similarity hides: stablecoins intermediate safe assets into a medium of exchange, while tokenized deposits allow banks to keep funding loans and supporting credit creation, just on digital rails. That is not a technical distinction. It is a distinction about who gets to create money and what happens to the banking system if the answer changes.

SWIFT chose the instrument that keeps banks in the center. Its stated position is that bank-issued tokenized deposits offer a compliance-ready alternative within existing regulatory frameworks, without the risks some institutions associate with non-bank stablecoins. In plainer terms: SWIFT built a blockchain that does what stablecoins do, on rails the banks already control, so that the banks do not have to adopt an instrument that cuts them out.

Why banks care so much about the difference

The reason this choice carries such weight is that stablecoins and tokenized deposits do opposite things to a bank’s balance sheet, and therefore to the banking system’s capacity to lend.

When a customer buys a stablecoin, they move fiat out of their bank account and into the issuer’s reserves. That money leaves the bank. It now sits in Treasury bills or a custodial account backing the token, where it does nothing for credit creation. Multiply that across a $315 billion sector, and you get a measurable drain: deposits leaving banks reduce the money multiplier, the mechanism by which $1 of deposits supports several dollars of lending. Stablecoins, in the language of one industry analysis, remove liquidity from the banking system.

Tokenized deposits do the reverse. The money stays on the bank’s balance sheet, still counted as a deposit, still available to fund loans and investment. The token is just a more mobile representation of it. So a bank that issues tokenized deposits keeps the funding it would lose to a stablecoin, while offering customers the same 24/7 programmable settlement. From the bank’s perspective, that is the entire game: match the stablecoin’s user experience without surrendering the deposit base that the lending business depends on.

There is a safety dimension too, and it is not merely marketing. Tokenized deposits are backed by a bank’s capital and the supervisory framework that governs commercial banks; they carry deposit insurance up to the statutory limit, and the issuing bank can borrow from the Federal Reserve’s lender-of-last-resort window, which reduces run risk. Stablecoins have none of that. Under the GENIUS Act, they must hold full reserves and disclose them, which is real protection, but a stablecoin holder is not an insured depositor, and there is no central bank standing behind the token. The 2008 money-market-fund parallel is apt: instruments that look like deposits and are treated like deposits right up until one breaks the buck and reveals it was never a deposit at all.

The bull case for SWIFT’s approach

The optimistic reading is that SWIFT has done the sober, correct thing, and that its distribution makes it the most credible entrant in the entire tokenized-money contest.

The reach argument is genuinely hard to counter. SWIFT connects more than 11,000 financial institutions across over 200 countries. No stablecoin issuer, no crypto-native payment network, and no single bank consortium can match that footprint. If the pilot works across 17 banks and multiple currency corridors, the marginal cost for the next institution to join is low, because it is already on SWIFT. That is a distribution advantage measured in decades of accumulated network membership, and distribution is what actually decides payment standards.

The problem SWIFT is solving is also real rather than invented. SWIFT already processes 75% of payments to beneficiary banks within 10 minutes on existing rails, often in seconds, so speed of messaging was never the true constraint. The constraint is the dependency on overlapping business hours: a Friday-evening payment from Asia to a counterparty in the Americas waits for Monday. The shared ledger removes exactly that, enabling weekend and overnight settlement inside the regulated perimeter. This is a targeted fix to a specific friction, not a solution in search of a problem to solve.

And the model preserves what regulators and treasurers actually want preserved. Corporate treasurers who have routed weekend wires through batch systems for decades get round-the-clock movement without stepping outside the compliance framework their auditors require. Banks keep their deposits. Regulators keep their oversight. The financial system gets programmable, always-on settlement without a parallel monetary system forming outside it. For institutions whose first question about any innovation is what could go wrong, that is a strong pitch.

The bear case for SWIFT’s approach

The skeptical reading is that SWIFT is defending an incumbency, that a permissioned bank ledger recreates most of the limitations stablecoins were built to escape, and that the market has already voted for the other model.

Start with the scoreboard. Stablecoins are not a proposal; they are in the wild, with supply above $300 billion and tens of trillions in settled transaction volume, having survived multiple crypto winters. Tokenized deposits remain largely in pilots, and SWIFT’s own launch is explicitly an initial pilot, not full deployment. One instrument is battle-tested at scale, and the other is a promising experiment, and the gap is years, not months. BlackRock’s Larry Fink put the competitive framing memorably in his 2025 investor letter: if SWIFT is the postal service, tokenization is email, moving assets directly and instantly, sidestepping intermediaries. SWIFT’s ledger is an attempt to make the postal service deliver like email while keeping the post offices in business.

The permissioning is the deeper limitation. SWIFT’s ledger is a closed, bank-only system. Stablecoins are open: anyone with a wallet can hold and send them, no banking relationship required, which is precisely why they took hold in cross-border corridors that the banking system serves poorly or expensively. A fintech in Lagos pays a supplier in Shenzhen in USDC because the bank wire costs 6% and takes 4 days. SWIFT’s ledger does nothing for that user, because that user is not a bank on SWIFT. The tokenized-deposit model, by design, only serves people already well served by banks, which is not where the disruptive demand is.

There is also a crowding problem that undercuts the reach argument. SWIFT is not the only bank consortium building this. A group including JPMorgan, Bank of America, Barclays, and BNY is building a US-focused tokenized-deposit network through The Clearing House, targeting 2027. JPMorgan already runs Kinexys, live on Base and expanded to Canton, settling institutional payments today. If every major bank and consortium builds its own tokenized-deposit rail, the result is not one clean alternative to stablecoins but a fragmented set of walled gardens, which is the exact problem SWIFT’s shared ledger claims to solve, reappearing one level up.

What this means for the stablecoin giants

For Tether and Circle, the two issuers who dominate the $315 billion sector, SWIFT’s move is a signal rather than an immediate threat, and the distinction matters.

It is not an immediate threat because the two instruments serve partly different users. Stablecoins own the open, permissionless, retail-and-crypto corridors: exchange settlement, DeFi collateral, remittances, and the long tail of users without good banking access. SWIFT’s ledger serves regulated institutions moving money between themselves. In the near term, these are different markets, and SWIFT’s pilot takes nothing directly off Tether’s or Circle’s books.

It is a signal because it marks the point where the banking system stopped treating stablecoins as a curiosity and started building the institutional-grade alternative in earnest, with the sector’s most powerful distribution network behind it.

The competitive question for the stablecoin issuers is whether tokenized deposits expand to absorb the use cases stablecoins hoped to grow into, particularly institutional cross-border settlement and corporate treasury, which is exactly the ground stablecoins have been migrating toward as they moved from crypto on-ramps into real commerce. If banks lock down the institutional corridor with insured, compliant tokenized deposits, stablecoins may find their growth capped at the permissionless edge instead of expanding into the regulated core.

The GENIUS Act complicates the picture in both directions. It gave stablecoins a federal framework and legitimacy, which helps them. It also opened the door to bank-issued stablecoin models and, through OCC trust charters granted to Circle, Paxos, Ripple, and others, blurred the line between the two instruments. The likely future is not one model winning but convergence: bank-issued stablecoins, tokenized deposits, and non-bank stablecoins coexisting, with the interesting fights happening at the boundaries. SWIFT just planted a very large flag on the bank side of that boundary.

The three-way race nobody named

The cleanest way to see where SWIFT fits is to stop treating this as stablecoins-versus-banks and start counting the actual competitors, because there are three distinct bets being placed on how institutional money moves next, and they do not all win.

The first is the open stablecoin model: Tether, Circle, and the newer consortium efforts like Open USD. Non-bank issuers, public blockchains, permissionless access, reserves held outside the banking system. This model owns the present. It has the volume, the corridors, and the proven product-market fit in exactly the places banks serve badly. Its weakness is regulatory and structural: it pulls deposits out of banks, it carries no insurance, and it sits in a legal category the GENIUS Act only recently defined.

The second is the single-bank tokenized-deposit model: JPMorgan’s Kinexys is the leading example, live on Base and Canton, settling real institutional payments today. Here, a single large bank builds its own rail, issues its own tokenized deposits, and offers clients programmable settlement inside that bank’s walls. The strength is control and immediacy: JPMorgan did not wait for a consortium. The weakness is reach. A JPMorgan rail moves JPMorgan money well and everyone else’s money not at all, which reintroduces the interoperability problem that correspondent banking exists to solve.

The third is the shared-network model, and this is SWIFT’s bet, alongside the JPMorgan-BofA-Barclays-BNY effort running through The Clearing House for a 2027 launch. Instead of one bank’s walled garden or an open public chain, a coordinated ledger that many banks share. The strength is exactly what the single-bank model lacks: interoperability across institutions. The weakness is governance and speed, because getting 17 banks, let alone 11,000, to agree on anything is slower than one bank acting alone or an issuer minting a token.

Notice that the second and third models are in tension with each other, not just with stablecoins. Every bank that builds its own Kinexys-style rail is a bank that has less reason to join a shared network, because it already has a working system. SWIFT is betting that no single bank’s rail can achieve the reach that its 11,000-member network offers by default, and that banks will therefore converge on a shared layer instead of fragmenting into competing private ones. That is a plausible bet and not a certain one. The history of financial infrastructure is full of both outcomes: shared utilities that became universal, and walled gardens that stayed walled because their owners preferred control to reach.

Where this leaves the honest observer is that the digital-money endgame is not stablecoins-win or banks-win. It is a question of which of three architectures captures which use cases, and the likeliest answer is that all three persist, serving different corridors, with the boundaries between them contested for years. SWIFT’s launch does not settle that. It just guarantees that the shared-bank-network model has the strongest possible distribution behind it, which was not true a month ago.

The honest read

Strip away the framing and SWIFT’s launch is best understood as the incumbent financial system’s most serious attempt yet to answer a question stablecoins forced onto the table: if money is going to move on programmable rails, who issues it and who controls the rails?

Stablecoins answered: non-banks, on open networks, outside the system. SWIFT’s answer is the opposite: banks, on a permissioned ledger, inside the system, with all the existing controls intact. Both answers are coherent, and the choice between them is not really technical. It is a choice about whether the digital-money era strengthens the two-tier banking system or routes around it, and that is a question about power and financial stability, not about block times.

What makes SWIFT’s move consequential is not that it is better technology, because in raw capability a public-blockchain stablecoin is more open and more composable. It is that SWIFT has the one thing the crypto-native challengers cannot manufacture: 11,000 banks already on the network. That distribution is why a 9-month pilot from a 53-year-old messaging cooperative is a bigger deal than a flashier launch from a better-funded startup. The banks are going to move digital money somehow. SWIFT just gave them a way to do it without ever holding a stablecoin, and for an industry whose entire instinct is to preserve itself, that may be exactly the product it wanted.

Whether it works is an open question, and the pilot will answer it slowly, corridor by corridor, over quarters. But the strategic picture is already clear. The stablecoin sector spent years arguing that banks were too slow to compete in digital money. SWIFT just proved they were slow, not absent, and being slow with 11,000 members is a very different position than being fast with none.

Frequently Asked Questions

What did SWIFT launch?

On July 9, 2026, SWIFT launched a blockchain-based shared ledger with 17 major banks across 6 continents, including Citi, HSBC, UBS, and BNP Paribas, for round-the-clock cross-border payments using tokenized deposits. Built on Hyperledger Besu in 9 months, it acts as an orchestration layer coordinating bank-issued tokenized deposits, with final settlement still occurring through existing payment rails. It is an initial pilot, not full deployment.

What is the difference between a tokenized deposit and a stablecoin?

A tokenized deposit is commercial bank money represented on a blockchain, issued by a regulated bank, kept on the bank’s balance sheet, and covered by deposit insurance up to the statutory limit. A stablecoin is a token issued by a non-bank entity, backed by reserves held outside the banking system, operating on open blockchains with no deposit insurance. They look similar but differ in legal status, insurance, and effect on bank lending.

Why did SWIFT choose tokenized deposits over stablecoins?

Because tokenized deposits keep money inside the banking system. When a customer buys a stablecoin, funds leave their bank for the issuer’s reserves, draining deposits banks use to fund lending. Tokenized deposits stay on the bank’s balance sheet, preserving credit creation, while offering the same 24/7 programmable settlement. SWIFT’s position is that they provide a compliance-ready alternative without the risks some institutions associate with non-bank stablecoins.

Is this a threat to Tether and Circle?

Not immediately, but it is a signal. Stablecoins dominate open, permissionless corridors such as exchange settlement, DeFi, and remittances, which SWIFT’s bank-only ledger does not serve. The competitive risk is longer term: if banks lock down institutional cross-border settlement with insured tokenized deposits, stablecoins may find growth capped at the permissionless edge instead of expanding into the regulated institutional core they have been moving toward.

Does SWIFT’s ledger replace the existing system?

No. It is an orchestration layer on top of correspondent banking, not a replacement. Banks issue tokenized deposits on their own ledgers; the shared ledger coordinates the movement, and final settlement still runs through existing payment rails. SWIFT already processes most payments to beneficiary banks within minutes; the ledger’s specific contribution is enabling weekend and overnight settlement that current infrastructure cannot support.

Who else is building tokenized deposit networks?

Several major institutions. A consortium including JPMorgan, Bank of America, Barclays, and BNY is building a US-focused tokenized deposit network through The Clearing House, targeting 2027. JPMorgan’s Kinexys is already live on Base and Canton, settling institutional payments. The proliferation of separate bank networks raises the risk of fragmentation, the same problem SWIFT’s shared ledger claims to solve.

Are tokenized deposits safer than stablecoins?

They carry different protections. Tokenized deposits are backed by bank capital, covered by deposit insurance up to the statutory limit, and issued by banks that can access the Federal Reserve’s lender-of-last-resort window, reducing run risk. Stablecoins under the GENIUS Act must hold full reserves and disclose them, but holders are not insured depositors, and no central bank stands behind the token. The instruments carry structurally different risk profiles.

Why does SWIFT’s reach matter so much?

Because payment standards are decided by distribution, not technology. SWIFT connects more than 11,000 institutions across over 200 countries, a footprint no stablecoin issuer or crypto-native network can match. Once the pilot works, the marginal cost for another member bank to join is low because it is already on SWIFT. That accumulated network membership is why a pilot from a 53-year-old cooperative can matter more than a technically superior launch from a startup.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. It describes payment infrastructure and a pilot program whose outcomes are uncertain, and it is not a recommendation to buy or sell any asset or token. Always do your own research. Information is accurate as of July 17, 2026.

Notional volume on prediction markets climbed sharply in the second quarter of 2026 and reached $113.8 billion, up 48.7% from the previous quarter.

CoinGecko found that the momentum accelerated in June, when monthly notional volume surged to a record $50.7 billion, which represented a 92% increase from the average monthly volume of $27.5 billion posted over the prior five months.

Sports Drive June Surge

In its latest report, CoinGecko attributed the spike to a packed calendar of major sporting events beginning in late May, such as the UEFA Champions League Final, Stanley Cup, NBA Finals, FIFA World Cup, and Wimbledon. The sports-driven activity was particularly evident on Polymarket, where sports-related contracts accounted for 81% of trading volume in June, as opposed to 40% in January.

Despite this increase in sports trading, Polymarket’s market share declined quarter-over-quarter from 35.8% to 30.2%. On the other hand, Kalshi has managed to expand its lead after increasing its share from 42.4% in the first quarter to almost 58.9% in the second.

Meanwhile, Rothera, the Robinhood/Susquehanna International Group joint venture launched in May, quickly climbed to fourth place in June with $2.1 billion in notional volume.

Wall Street and Big Tech Into the Race

Prediction markets gained momentum. Last month, Cboe Global Markets launched Cboe Predicts, its new prediction markets platform featuring securities-based binary option contracts tied to the Mini-S&P 500 Index. The contracts, trading under the symbols XSPBW and XSPBX, are already available through Interactive Brokers, while Charles Schwab is expected to add access in the coming months.

Cboe also said more brokerage firms are likely to support the products over time. The contracts allow traders to take a “yes” or “no” position on whether the Mini-S&P 500 Index will settle at or above a specified level at expiration.

Additionally, the New York Times reported that Meta is developing a standalone prediction markets app called Arena, where users would predict real-world outcomes using points instead of real money. According to the report, the experimental project is a top priority for CEO Mark Zuckerberg and could eventually expand to real-money betting. The initiative follows Meta’s earlier Forecast app, a points-based prediction platform launched in 2020 during the COVID-19 pandemic before being discontinued in 2022.

The post Sports Events Push Prediction Market Trading to Record Highs in June appeared first on CryptoPotato.

Jan said many Binance employees, including himself, already keep most of their assets on the exchange. “I could make payments, I could use my debit card to spend whatever I need wherever I want,” he said.

Lines are blurring

Eneko Knorr, co-founder and CEO of Dubai-based stablecoin company Stabolut, said the line between banks and crypto companies is becoming harder to see.

“Today, you see regular banks offering crypto, and crypto platforms offering real bank accounts and normal banking services,” Knorr told CoinDesk. “Of course, the world still runs on regular money, so we all have to make a standard bank transfer to pay rent or the utility bills.”

Knorr said younger customers may choose an app that combines stablecoins with daily banking services.

Rohan Misra, head of the Gulf Cooperation Council region and CEO of AMINA Bank ADGM, said stablecoins are increasingly used for payments and settlement but still need regulated banking infrastructure.

“The wallet alone isn’t the bank account,” Misra said. “The regulated infrastructure around it is.”

Misra also questioned whether self-custody, where users control their private keys, would become the default.

“Self-custody means if someone accesses your private key, your assets are gone with no recourse, no recovery and no insurance,” he said. “That’s cash under a mattress.”

Ethereum remains trapped below a major higher-timeframe resistance cluster despite recovering strongly from its June lows. The recent rejection near local highs has pushed the asset back into an important support zone, while the price is approaching a technical decision point that should determine whether buyers can extend the recovery toward higher resistance or whether another corrective leg unfolds.

ETH Price Analysis: The Daily Chart

On the daily timeframe, ETH continues to trade below the descending 100-day and 200-day moving averages, confirming that the broader market structure remains bearish despite the recent rebound.

The asset recently failed to sustain a move above the short-term resistance around $1.9K and has now pulled back into the $1.75K-$1.85K demand zone. This region has acted as support throughout the current recovery and now represents the first line of defense for buyers.

As long as Ethereum holds above this area, another push toward the major decision zone between $2K and $2.15K remains possible. This region also aligns with the descending long-term trendline and the declining 100-day moving average, making it the most significant resistance cluster on the daily chart.

A successful breakout above this confluence would mark an important structural improvement, while rejection would likely shift attention back toward the long-term demand zone around $1.45K-$1.55K.

ETH/USDT 4-Hour Chart

The 4-hour chart shows Ethereum pulling back after failing to extend above the recent swing high near $1.95K. The correction has pushed it back to the short-term demand zone around $1.76K-$1.84K, which has repeatedly attracted buyers over the past week.

This area now serves as the immediate support needed to preserve the sequence of higher lows established since early July. Holding above it could allow another attempt toward the upper boundary of the current recovery structure and eventually the daily resistance around $2K.

However, losing this demand zone would likely expose the lower support levels around $1.7K before buyers attempt another recovery.

Sentiment Analysis

The liquidation heatmap highlights a large concentration of short liquidations positioned above the current market, with the most notable liquidity cluster sitting around the $1.95K-$2K region.

Importantly, this liquidity pool aligns closely with the key technical resistance visible on both the daily and 4-hour charts. The cluster sits directly beneath the higher-timeframe supply zone around $2K-$2.15K and near the descending trendline, creating a strong confluence between derivatives positioning and technical resistance.

This alignment increases the probability that Ethereum could first stage an upside liquidity grab into the $1.95K-$2K area to sweep leveraged short positions before facing renewed selling pressure from the overhead supply zone. A decisive breakout through both the liquidity cluster and the daily resistance would invalidate this scenario and instead strengthen the case for a broader bullish reversal.

The post Ethereum Price Analysis: $2K Dream Remains on the Table as ETH Defends Key Levels appeared first on CryptoPotato.

Supporters of BIP-110 view Bitcoin as a public utility whose scarce block space should be reserved primarily for monetary settlement. Inscriptions and other data-heavy applications represent consumption of a limited resource that should be protected for financial transactions, even if doing so requires introducing new consensus rules.

DOG Mode starts from the opposite premise.

Leonidas argued Bitcoin should remain a neutral marketplace for block space, where any valid transaction is equally legitimate provided the sender pays the prevailing fee. From that perspective, there is no objective distinction between a bitcoin payment and an Ordinals inscription.

Rather than seeking permission through a protocol upgrade, the intention for DOG Mode is to remove policy restrictions that its supporters argue Bitcoin itself never required.

The proposal also raises a more subtle question about Bitcoin’s infrastructure.

If enough nodes begin running different policy software, the network’s mempool — the collection of unconfirmed transactions waiting to be mined — could become increasingly fragmented. Consensus would remain intact, but different parts of the network could relay different transactions, affecting fee estimation and how quickly some transactions reach miners.

That fragmentation already exists to a degree, but DOG Mode could widen those differences by encouraging broader acceptance of transactions that many default nodes currently refuse to relay.

Crypto World

Trump targets Brazil’s payments system while dollar stablecoins are quietly overtaking country’s payments

Dollar-linked stablecoins already account for roughly 90% of crypto transaction volume in Brazil, most of it used for payments and settlement, according to tax authority data.

Brazil processes between $6 billion and $8 billion in crypto each month, much of it using dollar-denominated stablecoins instead of the country’s own currency.

However, even as dollar stablecoins have proliferated, Brazil’s central bank has moved to limit their role in regulated cross-border payments. Resolution 561, effective October 1, is set to bar payment firms from settling cross-border payments in stablecoins or other crypto, closing a back-end channel that had routed reais through dollar tokens. The central bank has cast stablecoins as a threat to monetary sovereignty, tax enforcement and anti-money laundering controls.

Pix now faces pressure from both sides after Washington named it a trade barrier, while Brazilian regulators shield it from growing competition from dollar-backed stablecoins.

Pix, however, may not be competing with stablecoins.

“In practice, they are complementary,” Rodrigo Caggiano, founder of Brazilian real-world asset monitoring platform RWA Monitor, told CoinDesk. “Pix has addressed domestic instant payments well, while stablecoins expand what is possible by operating on blockchain networks.”

U.S. pressure is likely to accelerate Brazil’s regulatory debate on stablecoins and digital financial infrastructure, Caggiano said, as the central bank builds its own tokenized-settlement system, Drex, on similar programmable rails.

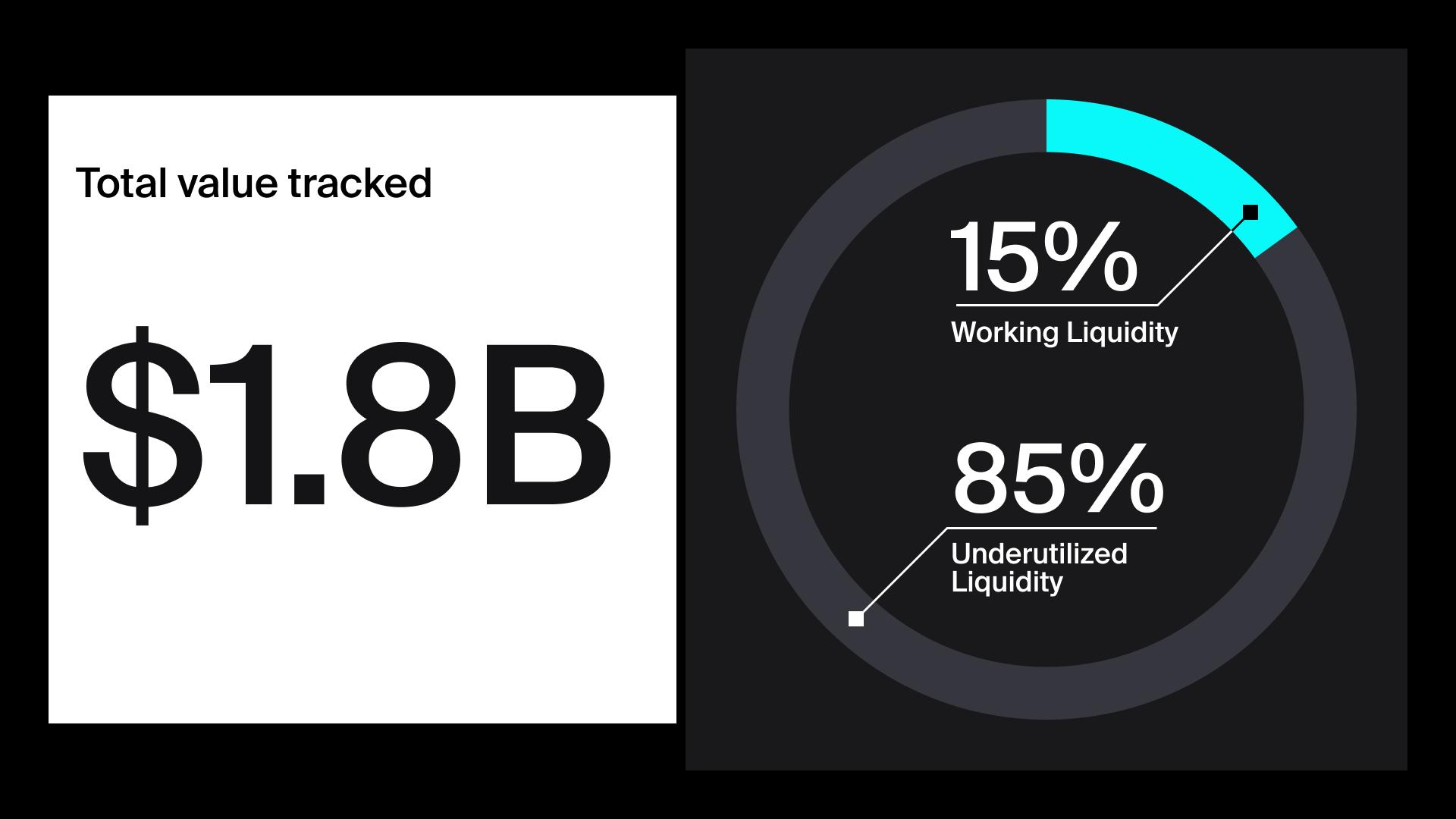

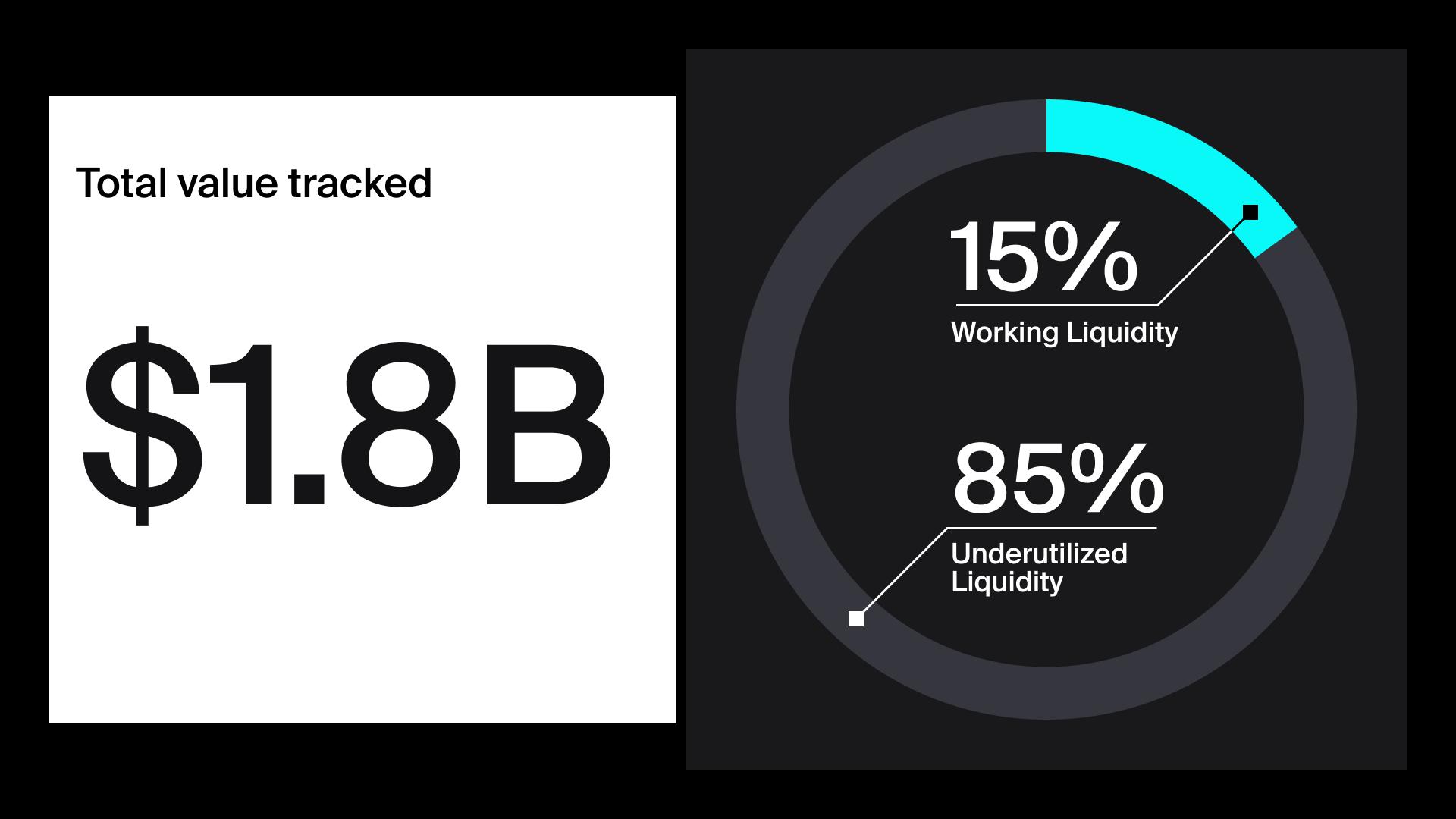

Around 54% of liquidity in positions below $1,000 was out of range, compared with 26% for positions above $1 million. Yet positions worth more than $1 million accounted for 47% of all idle capital, or roughly $260 million.

While contract-managed positions stayed within a more consistent range, individual wallets accounted for between 82% and 94% of the attributed idle capital on Uniswap v3, depending on the chain. That suggests liquidity deposited directly by users and requiring manual adjustments is more likely to go unattended and fall out of range.

Dune estimated that these out-of-range providers, that are sitting idle, could be missing roughly $150 million in fees each year, based on a blended in-range fee APR of about 35%.

Liquidity providers deposit token pairs that decentralized exchanges use to complete swaps. They earn a share of the fees paid for trades using that liquidity pool while their positions remain in the range they set.

However, the research said that the figure is not guaranteed recoverable income. Keeping positions active can add transaction costs, execution risk and exposure to unfavorable price movements.

1inch commissioned the research ahead of the planned launch of Aqua, a new liquidity protocol. Dune said it developed the methodology and reached its conclusions independently.

Meta is reportedly in talks to lease computing power to Anthropic in a deal worth as much as $10 billion over two years, according to the New York Times.

The arrangement would open a new business line for Meta while easing Anthropic’s desperate hunt for compute.

Inside the Reported Meta and Anthropic Compute Deal

Computing power, or compute, refers to the data center capacity used to train and run artificial intelligence models. The Anthropic proposal, first announced in June, would let the startup rent Meta’s excess infrastructure rather than build its own facilities.

According to the NTY, Anthropic would pay Meta in monthly installments over the two-year period, with an early-exit clause available to either party.

The scale still looks modest by industry standards. The proposal runs about a third of the deal Anthropic signed with Elon Musk’s SpaceX in May.

Follow us on X to get the latest news as it happens.

Under that agreement, the AI firm pays roughly $1.25 billion monthly, or $45 billion over three years, for computing power. Similar early-exit provisions reportedly applied to that larger contract as well.

The talks remain in early stages and may still collapse before closing. Both Anthropic and Meta declined to comment on the reported negotiations.

The context explains the urgency. Leading AI companies are racing to secure compute, while Meta, Google, and Microsoft pour hundreds of billions into new data centers worldwide.

That construction boom has unsettled Wall Street. Investors increasingly question whether such extraordinary levels of spending can ever be justified by real returns.

“Anthropic needs a lot of compute, and Meta has a lot of compute. Anthropic has really good models. Meta, until very recently, didn’t have very good models, and now they have, you know, I would say an A-minus to B-tier frontier model,” MTS’s Theo Jaffee said.

Why Would Meta Rent Compute to a Direct Rival

For Meta, a potential deal would carry unusual weight. It could create fresh revenue and ease pressure from shareholders skeptical of the company’s aggressive infrastructure budget.

Mark Zuckerberg has said Meta will spend as much as $145 billion this year, most of it on AI. That figure more than doubles the $72 billion spent the previous year.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

Doubts about Meta’s own models add another layer. The company has admitted it might build more data centers than its AI products currently require.

Selling that surplus offers an obvious fix. Zuckerberg hinted on a May investor call that outside firms regularly ask to buy compute at a premium.

He said Meta had resisted so far because it still expected to use the capacity internally. Overbuilding, however, would make leasing the surplus a far more logical option.

The growing scarcity of compute has pushed direct rivals toward cooperation. Anthropic, valued near $1.2 trillion and preparing to go public, has seen demand surge since launching Claude Code.

Meta itself already rents capacity elsewhere, including a $21 billion CoreWeave deal and a $27 billion agreement with Nebius. Rising compute prices now let the company consider renting its own centers out to others.

The post Meta Reportedly In Talks With Anthropic Over a $10 Billion AI Deal appeared first on BeInCrypto.

France’s gambling regulator has ordered internet providers to block access to Polymarket. The order comes days before Les Bleus face England in the FIFA World Cup 2026 bronze medal match.

The National Gambling Authority, known as the ANJ, has labeled the platform an illegal betting operation. It also flagged manipulation risks just as the prediction interest around the fixture builds.

France’s Regulator Moves to Cut Off Access

The ANJ’s president instructed French internet providers to block Polymarket entirely, calling the platform’s offering illegal. The regulator said Polymarket attracts a particularly large audience while promoting an illegal gambling and betting offering.

The agency also flagged manipulation risks tied to some Polymarket wagers. That adds pressure on a platform facing scrutiny across Europe’s Polymarket bans. The Netherlands already threatened steep fines earlier this year.

A Pattern Stretching Well Beyond France

France now joins a lengthening list of regulators pushing back. Kentucky’s attorney general filed a prediction market lawsuit against Polymarket and Kalshi this year. Australia tightened gambling ad restrictions around live sports broadcasts.

Polymarket, meanwhile, has kept courting friendlier jurisdictions. The company is reportedly pursuing a Japan approval push, targeting Tokyo by 2030.

The split shows a clash between wary regulators and Polymarket. Regulators worry about consumer harm. Polymarket insists its contracts serve legitimate price discovery, not gambling.

Bettors Still Favor Les Bleus

None of that scrutiny has cooled interest in today’s third-place playoff. That mirrors a broader surge in World Cup prediction markets throughout the tournament. Polymarket’s live market prices France at 67 cents to beat England. That implies roughly a 67% chance for Les Bleus.

The French ban does not reach bettors abroad. But it signals regulators are no longer willing to wait for prediction markets to police themselves. Whether Polymarket adapts its French offering or simply walks away remains an open question heading into kickoff.

The post France Blocks Polymarket Ahead of World Cup 3rd Place Match appeared first on BeInCrypto.

Apple TV’s New Anya Taylor-Joy Thriller Has a Dark Real-Life Origin

The White House is now deciding who gets access to frontier AI models, not the labs

Thomas Tuchel called out for ‘talking nonsense’ before England vs France World Cup clash

-

NewsBeat2 days ago

NewsBeat2 days agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Fashion1 day ago

Fashion1 day agoWeekend Open Thread – Corporette.com

-

Politics10 hours ago

Politics10 hours agoThe House | The City of London can help the new chancellor deliver growth in every postcode

-

Crypto World3 days ago

Crypto World3 days agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Politics3 days ago

Politics3 days agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Business3 days ago

Business3 days agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Crypto World9 hours ago

Crypto World9 hours agoRipple Payments Joins MiCA With 14 Firms, Does It Mean Anything For XRP?

-

Entertainment3 days ago

Entertainment3 days agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

Crypto World22 hours ago

Crypto World22 hours agoRipple wins EU-wide access as ESMA adds it to MiCA register

-

Business3 days ago

Business3 days agoPalantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

-

Tech5 days ago

Tech5 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

News Videos4 days ago

News Videos4 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Crypto World2 days ago

Crypto World2 days agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

Tech4 days ago

Tech4 days agoDark Secrets Emerge When Jailbreaking LLMs

-

NewsBeat1 day ago

NewsBeat1 day agoRegistration is now open for March for Men with Kev 2026

-

Sports3 days ago

Sports3 days agoNew Cornerback Enters Vikings Trade Rumor Mill

-

News Videos2 days ago

News Videos2 days agoMoney | Class 12 Economics | CBSE Board Exam 2026-27

-

Business2 days ago

Business2 days agoBanco Bilbao Vizcaya Argentaria, S.A. (BBVA) Discusses Global Macro Environment and Economic Outlook for Core Markets Transcript

-

Tech5 days ago

Tech5 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

NewsBeat15 hours ago

NewsBeat15 hours agoDurham County Council to send out electoral registration emails

You must be logged in to post a comment Login