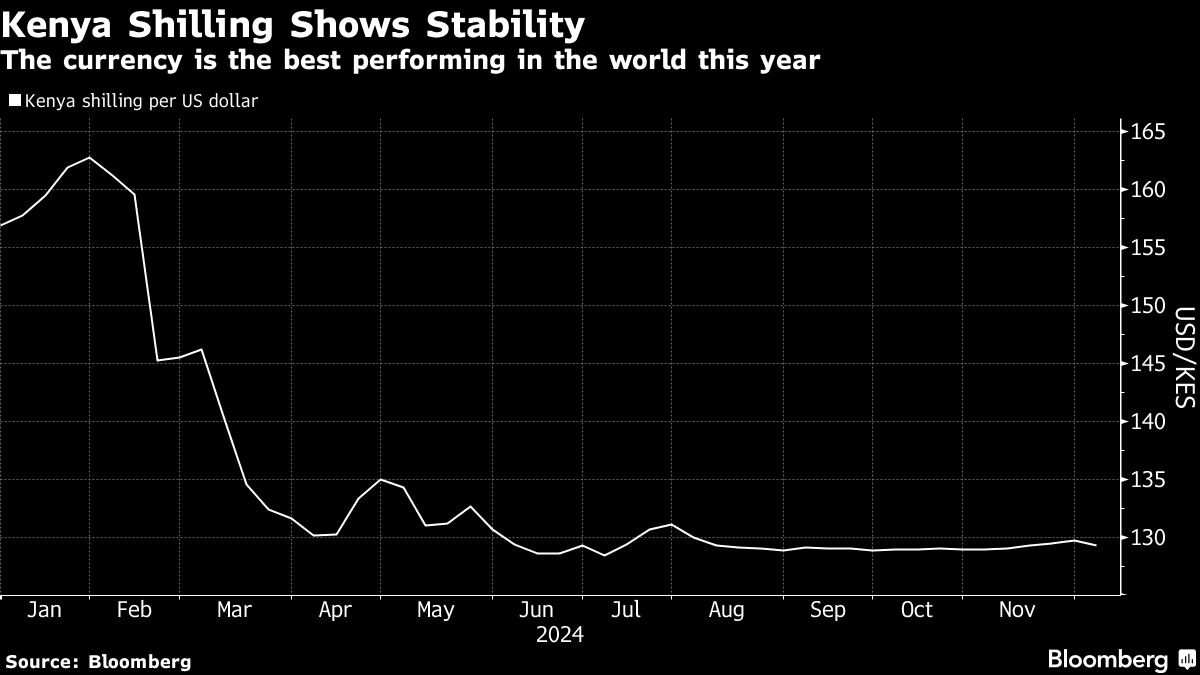

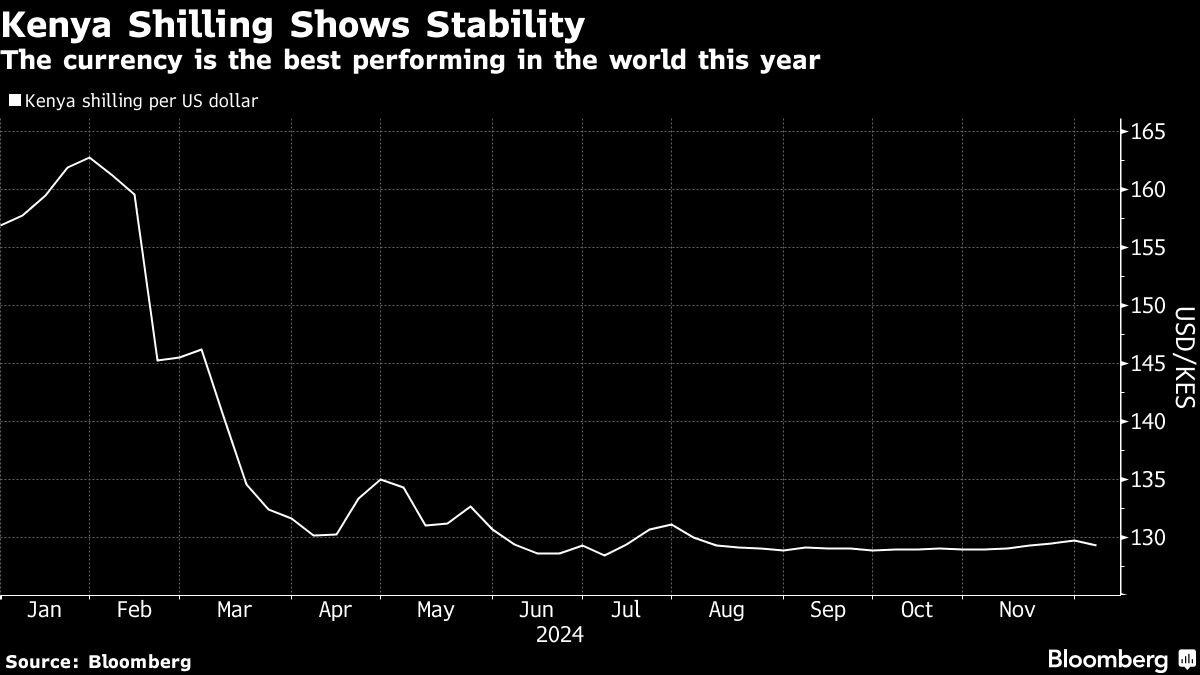

Kenya’s currency, which has weathered the surge in the dollar since Donald Trump won the US election, risks foundering unless the East African nation’s economic growth revives.

Kenya’s currency, which has weathered the surge in the dollar since Donald Trump won the US election, risks foundering unless the East African nation’s economic growth revives.

[matched_con] Source link

Handout Dafydd Bayliss says he has “given up” trying to get the £18,000 he says he’s owed Dafydd Bayliss’s Monday morning blues cleared instantly when [more…]

Sonic SVM, the developer of TikTok App Layer SonicX, has unveiled an ambitious new initiative: an airdrop of $SONIC tokens for all TikTok users onboarded [more…]

A man has been charged over the death of a woman who was set on fire on a New York subway train. Police and federal [more…]

[matched_con] Source link

Quordle was one of the original Wordle alternatives and is still going strong now more than 1,000 games later. It offers a genuine challenge, though, [more…]

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only. TRX, SHIB, and CATZILLA [more…]

In early December 1955, the phone rang at an air base in Colorado Springs. The officers on the watch floor of the Continental Air Defense [more…]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

+ There are no comments

Add yours