Stay informed with free updates

Simply sign up to the US inflation myFT Digest — delivered directly to your inbox.

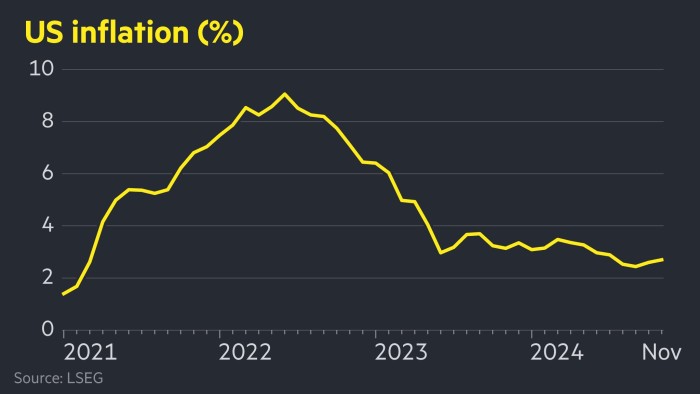

US inflation rose to 2.7 per cent in November, as the Federal Reserve considers how quickly to press ahead with lowering interest rates.

The figure was in line with the expectations of economists polled by Bloomberg but higher than October’s rate of 2.6 per cent.

The data from the Bureau of Labor Statistics on Wednesday underlines concerns about sticky inflation following a previous increase in October.

The Fed is widely expected next week to make its third consecutive quarter-point cut to interest rates, but the trajectory next year is less certain, as the central bank wrestles with its dual mandate to keep inflation close to 2 per cent and maintain a healthy labour market.

On a monthly basis, prices were up 0.3 per cent.

Once food and energy prices were stripped out, core CPI rose 0.3 per cent for the month, or 3.3 per cent on an annual basis.

US stock futures slightly extended their gains after the data was released. Contracts tracking the benchmark S&P 500 gauge were up 0.3 per cent, while those tracking the technology-heavy Nasdaq 100 index rose 0.4 per cent.

Government bonds were muted, with the policy-sensitive two-year Treasury yield steady at 4.15 per cent.

The US central bank’s expected cut next week would take interest rates to a new target range of 4.25-4.5 per cent.

Officials have discussed slowing the pace of cuts as rates reach a more “neutral” setting that is high enough to keep inflation in check but sufficiently low to safeguard the labour market.

They argue that if they move too quickly, inflation may get stuck above their 2 per cent target, but moving too slowly could risk a sharp rise in the unemployment rate.

Jobs growth rebounded sharply in November after being dragged down by hurricanes and strikes the previous month.

However, the unemployment rate rose to 4.2 per cent, suggesting the labour market’s acceleration was not strong enough to risk reigniting inflation.

Economists add that while price pressures remain high in service sectors related to housing, they are expected to level off over time.

Some officials in the outgoing Biden administration have expressed concern that the policies of president-elect Donald Trump will damage the economy after he returns to the White House next month.

US Treasury secretary Janet Yellen said this week that the sweeping tariffs proposed by Trump could “derail” progress on taming inflation.

“[Tariffs] would have an adverse impact on the competitiveness of some sectors of the United States economy, and could significantly raise costs to households,” she said at an event hosted by the Wall Street Journal.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

+ There are no comments

Add yours