News Videos

Dave Ramsey – 7 Baby Steps to Financial Freedom

#shorts #financialfreedom #debtsnowball

#daveramsey #daveramseybabysteps

source

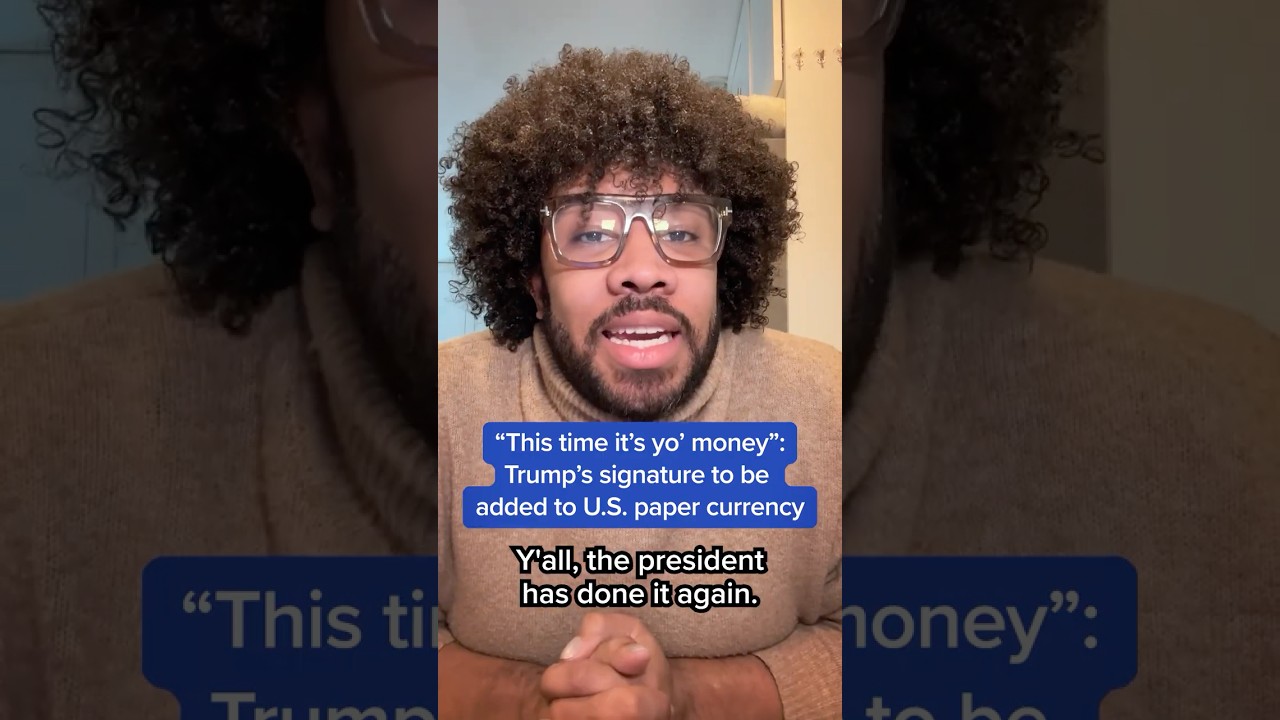

The U.S. Department of the Treasury announced that Trump’s signature will appear on future U.S. paper currency, the latest in a string of items and more bearing his name. MS NOW’s Eugene Daniels breaks down what this pattern may really be signaling.

For more analysis like this, click the link to watch “Clock it with Symone and Eugene” every Thursday on YouTube.

LINK: ms.now/clockit

MS NOW: My Source for News, Opinion, and the World.

» Subscribe to MS NOW: https://www.youtube.com/@msnow

MS NOW is the go-to destination for domestic and international breaking news, and best-in-class opinion journalism. For more context and news coverage of the most important stories of our day click here: https://www.ms.now/

#MSNOW #signature #treasury

source

News Videos

How and WHAT to invest in! #investing #stockmarket #money #finance #recession #inflation #wallstreet

Welcome to Democracy Today! 🇺🇸

The channel dedicated to bringing you the latest U.S. news and politics — fast, clear, and reliable.

We cover:

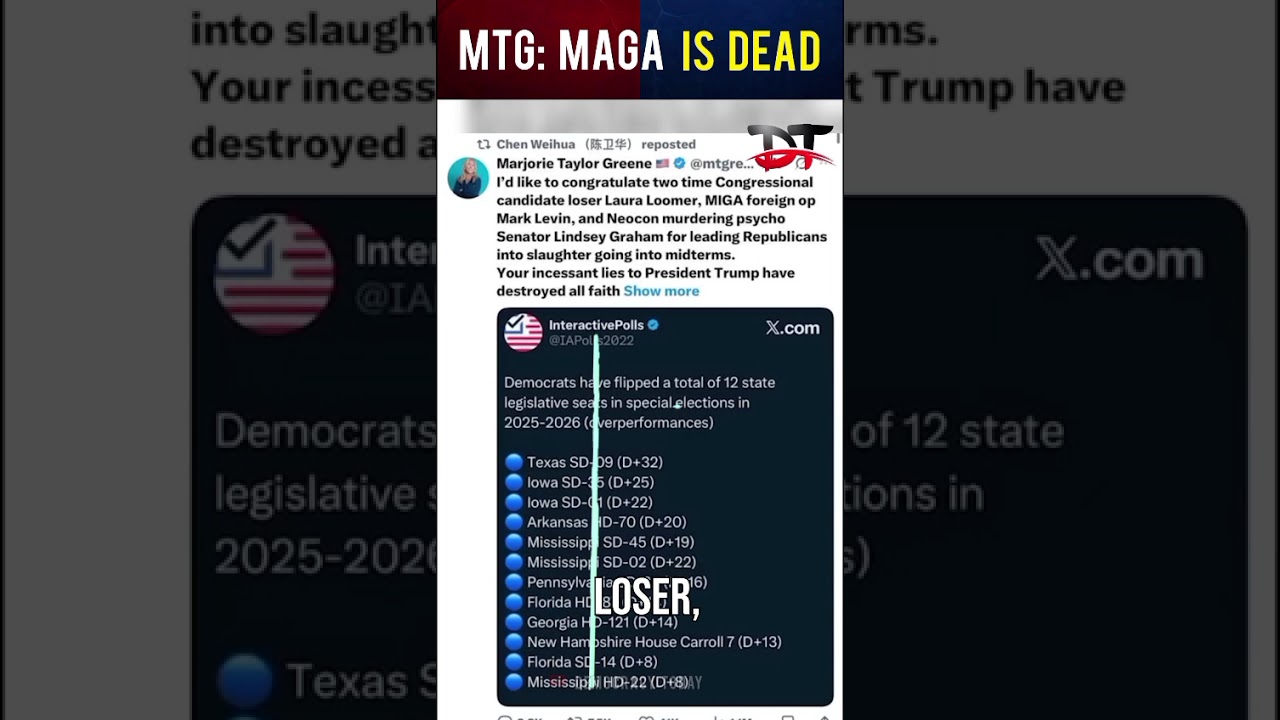

Marjorie Taylor Greene:] I’m #american First, I ain’t MAGA anymore. MAGA is dead… I’d like to congratulate… neocon #murdering psycho Senator Lindsey Graham for leading #Republicans into #slaughter… Trump and the GOP #betrayed their #voters

📰 Breaking news & headlines from across America

🏛️ U.S. politics and leadership battles

💰 Economy, society, and key issues shaping the nation

🔥 Viral & trending stories that everyone’s talking about

🎥 New videos every day to keep you updated and informed.

👉 Stay connected, stay informed, and join our growing community.

Subscribe now for daily updates on U.S. news and politics!

immigration news

Trump breaking news today

US politics latest update

Biden speech live

Zelenskyy latest news

Republicans vs Democrats news

Top US news today

#USANews #60SecAmerica #BreakingNews #DemocracyToday #ShortNews #PoliticsShorts #AmericanUpdates #NewsShorts #DailyHeadlines #AmericanPolitics #WhiteHouse #CongressUpdate #ViralNews #NewsAlert #USUpdates #DemocratsVsRepublicans #DailyNews #news #politics #youtube #shorts #world #us #shortfeed #Latestupdate #Todaynews

CNN

Fox News

MSNBC

ABC News

CBS News

NBC News

PBS NewsHour

Bloomberg TV

CNBC

Newsmax TV

One America News Network

BBC News

AlJazeeraEnglish

ReutersTV

⚠️ Disclaimer

📰 This video is for news, commentary & educational purposes only.

💬 Views & opinions are personal and not official statements.

📽️ Clips & images are used under Fair Use (for reporting, criticism & commentary).

🔎 Always do your own research before forming conclusions.

source

He is a man of less words and more action! Meet China no.1 Wei Yi who is taking part in the FIDE Candidates 2026. In this video, Wei Yi speaks about how he prepared for the Candidates, his team members, who supported him financially and much more. Truly an amazing personality in the world of chess!

Video: ChessBase India

#Chess #ChessBaseIndia #WeiYi

—————————————————————-

◾Support young talents via HelpChess Foundation: https://helpchess.org/

◾Review us on Google: https://g.page/r/CZ5T1PaLM-7WEBE/review

◾Chess Shop: https://shop.chessbase.in/

◾ChessBase India on amazon: https://amzn.to/2vv0XXy

◾Contact us: http://chessbase.in/contact

Most important links of ChessBase India: https://linktr.ee/chessbaseindia

source

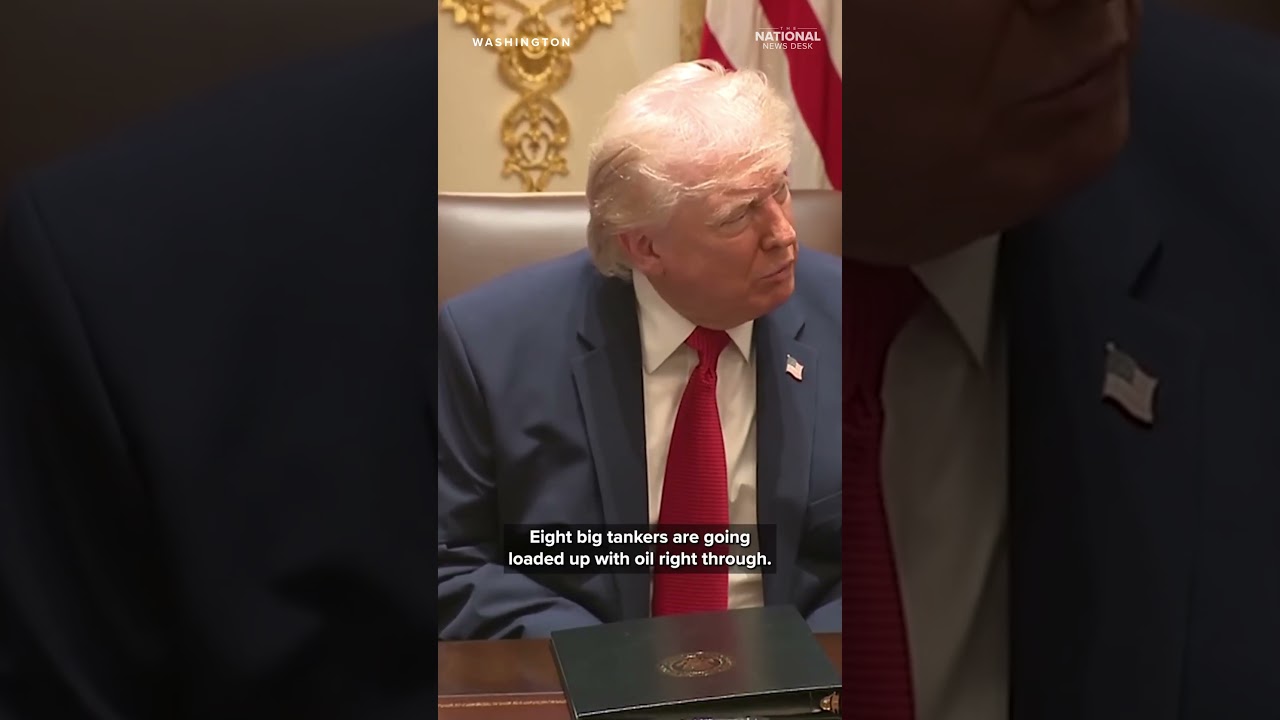

President Donald Trump revealed Thursday that Iran is allowing oil shipments to pass through the Strait of Hormuz as part of what he described as a “big present” amid ongoing backchannel talks between the two countries.

Speaking during a Cabinet meeting, Trump said Iranian officials permitted “eight boats of oil” to move through the critical waterway, calling it an apparent gesture of goodwill as negotiations continue.

READ MORE: https://thenationaldesk.com/news/americas-news-now/president-donald-trump-convenes-cabinet-as-dhs-homeland-security-partial-government-shutdown-democrats-republicans-disrupts-airports-strains-tsa-funding-deadline-immigration-ice-agents-iran-war-save-america-act#

————————————–

The National Desk (TND) brings you award-winning local storytelling from Sinclair Broadcast Group’s local TV newsrooms across the United States and feeds from sources throughout the world.

Like us on Facebook for live feeds, video: https://facebook.com/TND/

Follow us on Instagram: http://instagram.com/TND

Follow us on TikTok: https://www.tiktok.com/@tndtok

Follow us on X: https://x.com/TND

Read more & watch our videos: http://thenationaldesk.com

TND covers content from Sinclair’s stations in:

Abilene-San Angelo, TX : KTXS

Albany, GA : WFXL

Albany, NY : WRGB

Amarillo, TX : KVII

Asheville, NC : WLOS

Austin , TX : KEYE

Bakersfield, CA : KBAK/KBFX

Baltimore : WBFF

Beaumont, TX : KFDM/KBTV

Birmingham, AL : WBMA

Boise, ID : KBOI/KYUU

Bristol, VA : WCYB

Cedar Rapids, IA : KGAN/KFXA

Champaign, IL : WCCU

Charleston, SC : WCIV

Charleston, WV : WCHS/WVAH

Chattanooga, TN : WTVC

Cincinnati, OH : WKRC/WSTR

Columbia, SC : WACH

Columbus, OH : WSYX/WTTE

Dayton, OH : WKEF/WRGT

El Paso, TX : KFOX/KDBC

Eugene, OR : KVAL/KMTR

Eureka, CA : KAEF

Flint, MI : WEYI/WBSF

Fresno, CA : KMPH

Gainesville, FL : WGFL

Green Bay, WI : WLUK

Greenville-New Bern, NC : WCTI

Harlingen, TX : KGBT

Harrisburg, PA : WHP

Jefferson City, MO : KRCG

Johnstown, PA : WJAC

Kalamazoo-Grand Rapids, MI : WWMT

Kirksville-Ottumwa, IA : KTVO

Las Vegas, NV : KSNV

Lewiston, ID : KLEW

Lincoln, NE : KHGI/KWNB

Little Rock, AR : KATV

Lynchburg, VA : WSET

Macon, GA : WGXA

Medford, OR : KTVL

Mobile, AL : WPMI

Myrtle Beach, SC : WPDE

Nashville, TN : WZTV

Oklahoma City : KOCB/KOKH

Pasco, WA : KEPR

Pensacola, FL : WEAR/WFGX

Portland, ME : WGME/WPFO

Portland, OR : KATU/KUNP

Providence, RI : WJAR

Quincy-Hannibal, IL : KHQA

Redding-Chico, CA : KRCR

Reno, NV : KRNV/KRXI

Rochester, NY : WHAM

Salt Lake City : KUTV

San Antonio, TX : KABB/WOAI

Savannah, GA : WTGS

Seattle, WA : KOMO/KUNS

Sioux City, IA : KMEG/KPTH

South Bend, IN : WSBT

Springfield, IL : WICS

Steubenville, OH : WTOV

Syracuse, NY : WSTM

Toledo, OH : WNWO

Traverse City, MI : WPBN

Tulsa, OK : KTUL

Washington DC : WJLA

West Palm Beach, FL : WPEC

Wilkes-Barre, PA : WOLF

Yakima, WA : KIMA

This video and all Sinclair Broadcast Group content archives of local news and sports coverage are available for your use. For more information contact us at contentsales@sbgtv.com

source

Become a Premium Member: https://www.jimmydore.com/premium-membership

Go to a Live Show: https://www.jimmydore.com/tour

Subscribe to Our Newsletter: https://mailchi.mp/jimmydorecomedy/ytlivestreams

LIVESTREAM & LIVE SHOW ANNOUNCEMENTS:

Email: https://mailchi.mp/jimmydorecomedy/ytlivestreams

Twitter: https://twitter.com/jimmy_dore

Facebook: https://www.facebook.com/JimmyDoreShow

Instagram: https://www.instagram.com/thejimmydoreshow

WATCH / LISTEN FREE:

Videos: https://www.jimmydore.com

Podcasts: https://www.jimmydore.com (Also available on iTunes, Apple Podcasts, Spotify, Google Podcasts, or your favorite podcast player.)

ACCESS TO FULL REPLAYABLE LIVESTREAMS:

Become a Premium Member: https://www.jimmydore.com/premium-membership

SUPPORT THE JIMMY DORE SHOW:

Make a Donation: https://www.jimmydore.com/

Buy Official Merch (Tees, Sweatshirts, Hats, Bags): https://thejimmydoreshow.dashery.com/

The Jimmy Dore Show Store

DOWNLOAD OUR MOBILE APP:

App Store: https://apps.apple.com/us/app/jimmy-dore/id839294547

Google Play: https://play.google.com/store/apps/details?id=com.jimmydore.jimmydore

Jimmy Dore on Twitter: https://twitter.com/Jimmy_Dore

Stef Zamorano on Twitter: https://twitter.com/miserablelib

About The Jimmy Dore Show:

#TheJimmyDoreShow is a hilarious and irreverent take on news, politics and culture featuring Jimmy Dore, a professional stand up comedian, author and podcaster. The show is also broadcast on Pacifica Radio Network stations throughout the country.

source

Can money really buy happiness!?

I always hated this question because it always came from people who already had money!

So we decided to look at data and see if we can get our answers there

We came across these all of these research papers

High income improves evaluation of life but not emotional well-being:https://www.princeton.edu/~deaton/downloads/deaton_kahneman_high_income_improves_evaluation_August2010.pdf

Lottery Winners and Accident Victims: Is Happiness Relative?: https://gwern.net/doc/psychology/1978-brickman.pdf

To do or to have? That is the question:https://pubmed.ncbi.nlm.nih.gov/14674824/

But all of them gave different results!, so I figured out the solution in a ECV framework!

Check out the framework in our video and let us know in the comments what do you think,

Can money buy happiness? 🤔

source

Global Financial Insights for Long-Term Success

Unlock the mysteries of global financial success and discover the secret to achieving your long-term financial goals. In this video, we’ll delve into the world of high finance and explore the strategies and techniques used by the world’s most successful investors and entrepreneurs. From managing risk to maximizing returns, we’ll examine the key principles that underpin global financial success and provide you with the knowledge and insights you need to take your finances to the next level. Whether you’re a seasoned investor or just starting out, this video is packed with valuable information and expert advice to help you achieve your financial objectives and secure a brighter financial future.

Time Code

0:00 Intro

0:10 Myanmar News

1:00 Myanmar News

2:30 News

3:00 News

4:00 Myanmar News

Facebook တွင်လည်းကြည့်ရှုနိုင်ပါသည်။ Like and Share လုပ်ပေးဖို့မမေ့နဲ့နော်

https://www.facebook.com/profile.php?id=100064732721170

Youtube Channel ကို Subscribe and Share လုပ်ပေးခြင်းဖြင့်ကူညီပါ

https://www.youtube.com/@mytv8362

Youtube Play List

https://www.youtube.com/@mytv8362/playlists

#GlobalFinance #LongTermSuccess #FinancialInsights #SmartInvesting #WealthBuilding

source

Darlington Council vows to build more council homes

Solana (SOL) vs XRP: A Deep Dive Into Long-Term Investment Potential

JD Vance Believes UFOs Are 1 Of The ‘Devil’s Great Tricks’

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

How Much Money Does He Make Flipping This Mercedes? #shorts #reselling #flipping #money

“This time it’s yo’ money”: Trump’s signature to be added to U.S. paper currency

How and WHAT to invest in! #investing #stockmarket #money #finance #recession #inflation #wallstreet

-

NewsBeat5 days ago

NewsBeat5 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

News Videos4 days ago

News Videos4 days agoParliament publishes latest register of MPs’ financial interests

-

Sports7 days ago

Sports7 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Sports7 days ago

Sports7 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

NewsBeat2 days ago

NewsBeat2 days agoThe Story hosts event on Durham’s historic registers

-

Business3 days ago

Business3 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

News Videos7 days ago

News Videos7 days agoCh 9 Financial Management Part 1 | Detailed One Shot | Class 12 Business Studies Boards 2026

-

NewsBeat5 days ago

NewsBeat5 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Entertainment7 days ago

Entertainment7 days agoCynthia Bailey Dishes on ‘RHOA’ Season 17, Discusses Kandi

-

Tech6 days ago

Tech6 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

Entertainment1 day ago

Entertainment1 day agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

NewsBeat7 days ago

NewsBeat7 days agoColombian military plane with 110 soldiers onboard crashes following takeoff

-

Business6 days ago

Business6 days agoMore women enter wealth management, but few in advisory roles: study

-

Fashion6 days ago

Fashion6 days agoDoes It Matter What You Wear When You’re Laid Off and Looking?

-

Fashion7 days ago

Fashion7 days agoFringe Bags for the Season

-

NewsBeat5 days ago

NewsBeat5 days agoEntrepreneurs Forum survey reveals optimism in North East

-

Business6 days ago

Business6 days agoLate-paying firms face multimillion-pound fines under new crackdown

-

Politics6 days ago

Politics6 days agoHow Media Platforms Balance Performance and Accessibility in Image Delivery

-

Sports5 days ago

Sports5 days agoFantasy Baseball Week 1 Preview: Top sleeper hitters for both five- and 12-day period led by Munetaka Murakami

-

NewsBeat6 days ago

NewsBeat6 days agoNASA Artemis II Astronauts enter 14-Day quarantine as moon rocket reaches launchpad

You must be logged in to post a comment Login