As indicated by the Bollinger Bands width indicator, the EUR/USD market remained relatively subdued in February, with the indicator twice retreating towards its lower boundary.

However, price action over the past two sessions suggests renewed activity — the range formed between 11 and 17 February has been broken to the downside by sellers.

From a fundamental perspective, this move reflects a combination of factors, including:

→ Reports that European Central Bank President Christine Lagarde is planning to step down before the end of her term in October next year. This development is viewed as a bearish factor for the euro.

Advertisement

→ Minutes from the FOMC meeting showing that policymakers are in no rush to cut interest rates. Opinions were divided, with some members even open to raising the Fed rate if inflation proves persistent. The prospect of a tighter Federal Reserve stance is supportive for the US dollar.

Technical Analysis of the EUR/USD Chart

The recent bearish pressure has pushed EUR/USD back towards a key support level around 1.1777. Bears attempted to break below this level on 6 February but failed, resulting in a false breakout at point B.

While bulls may attempt a rebound from this support, the broader picture suggests that sellers currently hold a slight advantage in February, reflected in the following:

→ Price action has been forming a descending channel since 11 February (shown in red).

→ High C sits roughly halfway along the A→B bearish impulse. According to Fibonacci proportions, this is consistent with a bearish market structure.

Advertisement

→ Bulls have been unable to secure a foothold above key psychological levels — first above 1.2000 and subsequently above 1.1900.

If selling pressure persists, a decisive break below 1.1777 cannot be ruled out, which could in turn trigger a fresh surge in volatility.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Minutes from the January meeting show rate hikes are not off the table. If inflation stalls, policymakers are ready to tighten again. That is a direct warning to risk markets.

For Bitcoin price, this flips the script. The market was leaning toward cuts. More liquidity. Easier conditions. Now the Fed is signaling the opposite.

Higher rates. Tighter liquidity. And that changes everything for crypto.

Key Takeaways

The Signal: Fed officials discussed “upward adjustments” to rates if inflation stays above target levels.

The Split: The vote was 10-2 to hold rates, but a significant “hawkish” contingent is pushing back against cuts.

The Risk: Higher-for-longer rates typically drain liquidity, creating headwinds for Bitcoin and ETF inflows.

Why Does This Matter for Crypto and Bitcoin Price?

Markets were relaxed. Cuts in 2026 felt almost guaranteed. Now that confidence got shaken again.

Advertisement

The Fed held rates at 3.5% to 3.75%, hitting pause after three straight cuts in late 2025. But the tone was not soft. Inside the discussion, a hawkish group made it clear they are not ready to promise more easing.

Some officials even floated “upward adjustments” if inflation sticks around. That is a big shift. The market had assumed a smooth path lower. The minutes analysis say otherwise.

The Fed wants clear proof that disinflation is real before cutting again. That puts serious weight on the February CPI print. If inflation runs hot, rate hikes move from theory back to reality.

What Happens Next?

Advertisement

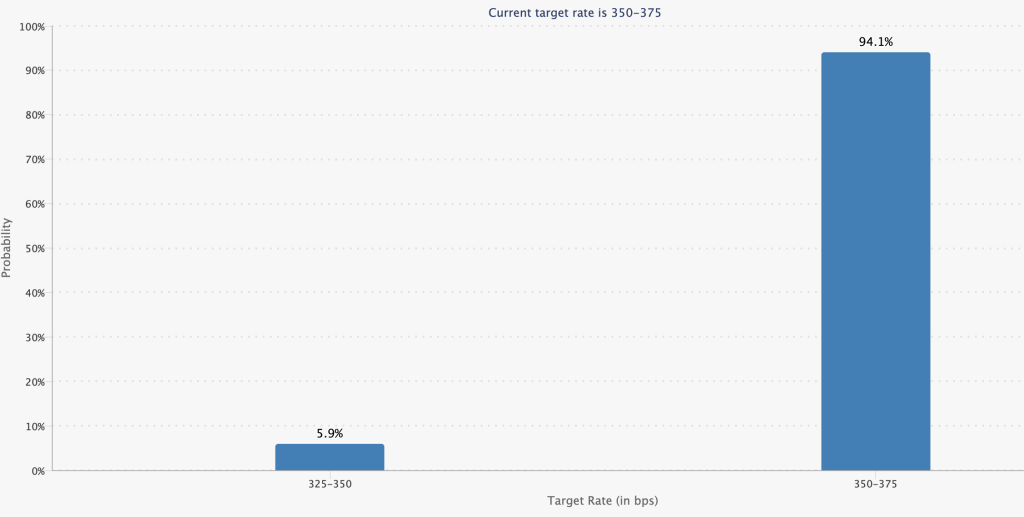

Pricing is getting messy. CME futures still show a 94% chance of a pause in March. But the hike risk is no longer zero.

Source: CMEgroub

Now it all comes down to inflation data. If the next print runs hot, the Fed fears get validated. If not, this scare might fade just as fast as it appeared.

Across the globe, it remains common for crypto users to have their bank accounts frozen and transfers blocked, even as institutional adoption rises.

Panos Mekras, co-founder and CEO of blockchain fintech Anodos Labs, began dealing with crypto in Greece in the late 2010s. Most Greek banks didn’t allow transfers to crypto exchanges back then. Mekras experienced blocked card payments until one bank finally permitted his transfers, but first, he was questioned to ensure he understood he was interacting with a “risky” counterparty.

Mekras told Cointelegraph that those early rejections are symptomatic of how banks treat digital assets as inherently high risk. That label often led to account closures or sudden freezes without explanation, ultimately pushing his business to rely solely on onchain tools and payment rails.

Public perception of crypto has since evolved. Now, crypto is undergoing an image refresh, from a speculative asset class to an infrastructure layer for future financial products. However, Mekras said he still experiences the same banking barriers, as recently as a “few months ago”:

Advertisement

“I tried to send money from an exchange to Revolut, and they froze my account for three weeks. I had no access to my [funds] during that time.”

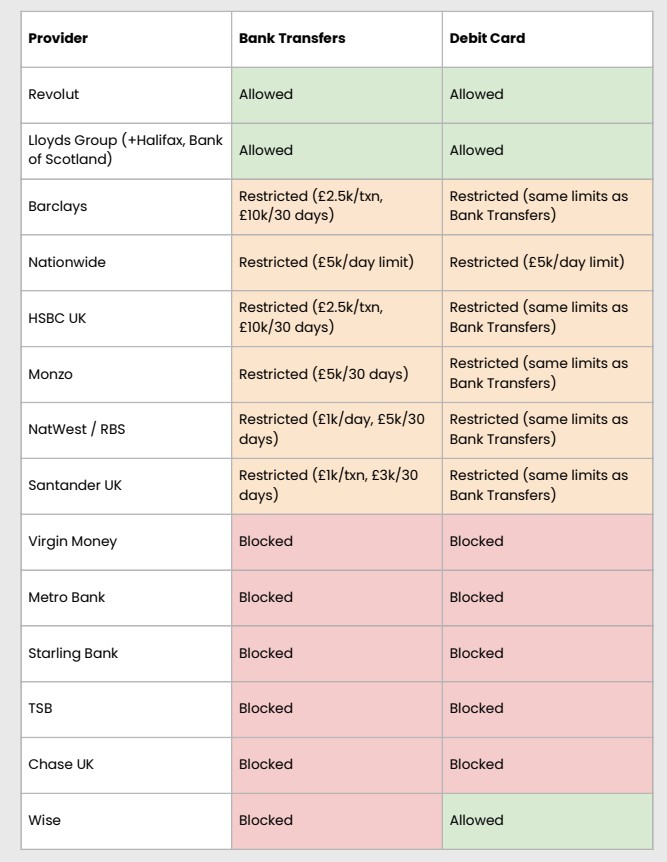

A January report from the UK Cryptoasset Business Council found that bank transfers to exchanges were being blocked or delayed, with roughly 40% of payments encountering restrictions and 80% of exchanges reporting increased friction over the past year.

The council warned that blanket bans and transaction limits are often applied without regard to the legal status of the exchange.

How banks are serving crypto users in the UK. Source: UK Cryptoasset Business Council

Revolut is one of two banks that permit both bank transfers and debit cards in the UK council’s study, and it is also the platform where Mekras claims to have experienced his recent account freeze. It operates as an authorized UK bank “with restrictions,” meaning it is currently building up its banking processes before full launch. It also holds a European Union banking license through Lithuania and offers crypto trading services in its app.

A Revolut spokesperson told Cointelegraph it treats account freezes as a “last-resort” customer protection measure in compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations.

Advertisement

“A temporary freeze may occur if our systems detect irregular activity. This could be a combination of a few factors, such as if a customer interacts with a platform frequently exploited by fraudsters, or we believe that the funds in question may be the proceeds of crime or sanctions circumvention,” the spokesperson said.

The representative added that since Oct. 1, just 0.7% of Revolut accounts where customers deposited crypto funds were restricted or frozen after investigation.

In some regions, crypto is blocked and leaves users to more extreme restrictions. Crypto on- and off-ramps are not legally possible in regions like China, so users resort to peer-to-peer (P2P) platforms or black markets to trade crypto.

Similar banking friction patterns also emerged in the US. Lawmakers and the industry have invoked the term “Operation Chokepoint 2.0” to describe the federal regulators’ informal guidance that discouraged banks from maintaining relationships with crypto companies.

Crypto industry claims about “Operation Chokepoint 2.0” were recently echoed in official findings. Source: Alex Thorn

The original “Operation Choke Point” was an initiative in which enforcement agencies were accused of pressuring banks to cut ties with politically contentious industries such as payday lenders and firearms sellers.

In January 2025, Donald Trump took office as the president of the US and has been pushing for crypto-friendly policies to position the world’s largest economy as the “crypto capital” of the world.

Advertisement

Crypto debanking issues have since been officially recognized. In December, the US Office of the Comptroller of the Currency (OCC) released its findings on debanking practices by nine of the country’s largest banks. The OCC also published an interpretive letter to confirm that banks may facilitate crypto transactions in a broker-like capacity.

Crypto is named among nine sectors in OCC’s review of large banks’ debanking activities. Source: OCC

Regardless of the positive momentum, users still complain that the banking sector won’t service accounts exposed to cryptocurrencies.

“This is still the case [and] there are still anti-crypto positions. Some have even said publicly that they are not willing to support crypto activity or engage with the industry,” said Mekras.

Mekras argued that users can consider fully detaching from the traditional banking system and moving finances onchain. It sounds viable in theory, but in reality, most businesses and users still cannot operate purely within crypto without reliable access to fiat rails.

Banking’s turn toward blockchain infrastructure

In recent years, there has been a global shift in how traditional financial institutions engage with crypto.

Advertisement

Major banks and financial infrastructures are increasingly building products and services tied to Web3. In the US, 60% of the top 25 banks are reportedly offering or planning Bitcoin-related services, including custody, trading and advisory solutions.

A large chunk of top banks are exploring Bitcoin-related services. Source: River

Across Europe, regulated services such as crypto custody and settlement are being introduced by legacy exchanges and financial groups under the Markets in Crypto-Assets Regulations (MiCA). In the UK, HSBC’s blockchain platform was selected to support pilot issuances of tokenized government bonds.

In that backdrop of institutional adoption, some companies working to bridge banks and blockchain claim that the challenges that lead to account freezes are linked to tooling gaps and risk frameworks inside banks.

“The problem is that there’s a huge amount of friction because traditional banks don’t really have the internal infrastructure to interpret blockchain data in a way that fits inside their existing risk and compliance frameworks,” Eyal Daskal, CEO of Crymbo — a blockchain infrastructure platform for institutions — told Cointelegraph.

He described the situation as one where banks often default to precautionary measures because they lack the ability to link onchain activity with the identity and compliance signals they rely on:

Advertisement

“If crypto is involved, they block the account and treat it as out of scope. It’s the simplest option for them because they don’t have the tools to assess it properly.”

Crypto is entering the financial mainstream, but for many users, access to basic banking still depends on whether a bank’s risk engine can understand what happens onchain. Until that gap closes, the industry’s institutional embrace and retail friction may continue to coexist.

Cointelegraph Features and Cointelegraph Magazine publish long-form journalism, analysis and narrative reporting produced by Cointelegraph’s in-house editorial team and selected external contributors with subject-matter expertise. All articles are edited and reviewed by Cointelegraph editors in line with our editorial standards. Contributions from external writers are commissioned for their experience, research or perspective and do not reflect the views of Cointelegraph as a company unless explicitly stated. Content published in Features and Magazine does not constitute financial, legal or investment advice. Readers should conduct their own research and consult qualified professionals where appropriate. Cointelegraph maintains full editorial independence. The selection, commissioning and publication of Features and Magazine content are not influenced by advertisers, partners or commercial relationships.

Editor’s note: In this era of digital finance, institutional collaboration between traditional asset managers and crypto exchanges is reshaping markets. The collaboration between Franklin Templeton and Binance demonstrates a practical path to bridge regulated money market products with 24/7 digital markets, using tokenized assets as collateral while preserving custody and risk controls. This editorial snapshot previews how off-exchange collateral programs can improve capital efficiency for institutions without moving assets onto exchanges.

Key points

Off-exchange collateral using Benji tokenized money market fund shares now live on Binance.

Custody by Ceffu minimizes counterparty risk for institutions.

Enables yield-bearing assets to be used for trading without on-exchange parking.

Expands Franklin Templeton and Binance’s networks of off-exchange program partners.

Why this matters

This collaboration signals growing institutional adoption of tokenized real-world assets, improving capital efficiency and risk controls in crypto markets. By tokenizing money market funds and maintaining custody off-exchange, institutions can participate in 24/7 trading with regulated protections, potentially broadening the set of assets available for collateral and fueling more stable liquidity in digital markets.

What to watch next

Broader rollout to additional institutional clients.

Addition of more tokenized Benji funds.

Deeper custody and settlement integrations with Ceffu.

Ongoing collaboration expansion across networks since the 2025 announcement.

Disclosure: The content below is a press release provided by the company/PR representative. It is published for informational purposes.

Franklin Templeton and Binance Advance Strategic Collaboration with Institutional Off-Exchange Collateral Program

Institutions can now use Benji-issued tokenized money market funds as off-exchange collateral to trade on Binance using Ceffu’s custody layer.

SAN MATEO, CA, and ABU DHABI, UAE, February 19, 2026 — Franklin Templeton, a global investment leader, and Binance, the world’s leading cryptocurrency exchange by trading volume and users, today announced a new institutional off-exchange collateral program, making digital markets more secure and capital-efficient. Now live, eligible clients can use tokenized money market fund shares issued through Franklin Templeton’s Benji Technology Platform as off-exchange collateral when trading on Binance.

The program alleviates a long-standing pain point for institutional traders by allowing them to use traditional regulated, yield-bearing money market fund assets in digital markets without parking those assets on an exchange. Instead, the value of Benji-issued fund shares is mirrored within Binance’s trading environment, while the tokenized assets themselves remain securely held off-exchange in regulated custody. This reduces counterparty risk, letting institutional participants earn yield and support their trading activity without hedging on custody, liquidity, or regulatory protections.

Advertisement

“Since partnering in 2025, our work with Binance has focused on making digital finance actually work for institutions,” said Roger Bayston, Head of Digital Assets at Franklin Templeton. “Our off-exchange collateral program is just that: letting clients easily put their assets to work in regulated custody while safely earning yield in new ways. That’s the future Benji was designed for, and working with partners like Binance allows us to deliver it at scale.”

“Partnering with Franklin Templeton to offer tokenized real-world assets for off-exchange collateral settlement is a natural next step in our mission to bring digital assets and traditional finance closer together,” said Catherine Chen, Head of VIP & Institutional at Binance. “Innovating ways to use traditional financial instruments on-chain opens up new opportunities for investors and shows just how blockchain technology can make markets more efficient.”

Assets participating in the program remain held off-exchange in a regulated custody environment, with tokenized money market fund shares pledged as collateral for trading on Binance. Custody and settlement infrastructure is supported by Ceffu, Binance’s institutional crypto-native custody partner.

“Institutions increasingly require trading models that prioritize risk management without sacrificing capital efficiency,” said Ian Loh, CEO of Ceffu. “This program demonstrates how off-exchange collateral can support institutional participation in digital markets while maintaining strong custody and control.”

Launching the institutional off-exchange collateral program expands on both Franklin Templeton’s and Binance’s growing networks of off-exchange program partners and represents another effort since announcing Franklin Templeton and Binance’s strategic collaboration in September 2025.

By using Benji to bridge tokenized money market funds, Franklin Templeton is taking trusted investment products and making them work in modern markets—allowing institutions to trade, manage risk, and move capital more efficiently as digital finance becomes an everyday part of the financial system.

Offering more tokenized real-world assets on Binance meets the increasing institutional demand for stable, yield-bearing collateral that can settle 24/7. This gives investors greater choice and enhances their trading experience on the world’s largest regulated digital asset exchange.

Advertisement

Franklin Templeton is a pioneer in digital asset investing and blockchain innovation, combining tokenomics research, data science, and technical expertise to deliver cutting-edge solutions since 2018. Learn more at http://franklintempleton.com/investments/asset-class/digital-assets.

About Binance

Binance is a leading global blockchain ecosystem behind the world’s largest cryptocurrency exchange by trading volume and registered users. Binance is trusted by more than 300 million people in 100+ countries for its industry-leading security, transparency, trading engine speed, protections for investors, and unmatched portfolio of digital asset products and offerings from trading and finance to education, research, social good, payments, institutional services, and Web3 features. Binance is devoted to building an inclusive crypto ecosystem to increase the freedom of money and financial access for people around the world with crypto as the fundamental means.

Ceffu is a compliant, institutional-grade custody platform offering custody and liquidity solutions that are ISO 27001 & 27701 certified and SOC2 Type 2 attested. Our multi-party computation (MPC) technology, combined with a customizable multi-approval scheme, provides bespoke solutions allowing institutional clients to safely store and manage their virtual assets.

Advertisement

For the purposes of this program, custody services for Benji-issued tokenized money market fund shares are provided by Ceffu Custody FZE, a virtual asset custodian licensed and supervised in Dubai.

About Franklin Templeton

Franklin Templeton is a trusted investment partner, delivering tailored solutions that align with clients’ strategic goals. With deep portfolio management expertise across public and private markets, we combine investment excellence with cutting-edge technology. Since our founding in 1947, we have empowered clients through strategic partnerships, forward-looking insights, and continuous innovations – providing the tools and resources to navigate change and capture opportunity.

With more than $1.7 trillion in assets under management as of January 31, 2026, Franklin Templeton operates globally in more than 35 countries.

All investments, including money funds, involve risk, including loss of principal. There are risks associated with the issuance, redemption, transfer, custody, and record keeping of shares maintained and recorded primarily on a blockchain. For example, shares that are issued using blockchain technology would be subject to risks, including the following: blockchain is a rapidly-evolving regulatory landscape, which might result in security, privacy or other regulatory concerns that could require changes to the way transactions in the shares are recorded.

This is a general announcement. Products and services referred to here may not be available in your region. Terms and conditions apply.

Bitcoin is trading under sustained pressure after losing key higher-timeframe support levels, with the price structure showing a clear transition from distribution to a developing downtrend. Momentum remains weak, and recent rebounds appear corrective rather than impulsive, keeping downside risk elevated in the near term.

Bitcoin Price Analysis: The Daily Chart

On the daily timeframe, the asset continues to respect a descending channel while trading below major moving averages, confirming bearish market structure. The rejection from the mid-range resistance zone and subsequent sharp sell-off toward the low-$60K region reinforces that sellers still control trend direction.

Momentum indicators remain subdued, with RSI holding far below neutral and failing to produce strong bullish divergence. Unless the price can reclaim the $75K–$80K resistance cluster and close above the channel midpoint, the broader bias stays tilted toward continuation lower or prolonged consolidation near the $60K support level.

BTC/USDT 4-Hour Chart

The 4-hour chart shows a steep impulsive drop followed by choppy sideways movement, typical of a bear-flag or accumulation attempt after liquidation. Lower highs continue to form beneath descending dynamic resistance, signaling that buyers have not yet regained short-term control.

Advertisement

Key support sits around the recent wick low near the $60K area, while immediate resistance is clustered between roughly $73K and $76K. A breakout above this range would be the first technical signal of a momentum shift, whereas a breakdown below the mentioned support zone could accelerate another leg downward and lead to another round of massive liquidations.

Sentiment Analysis

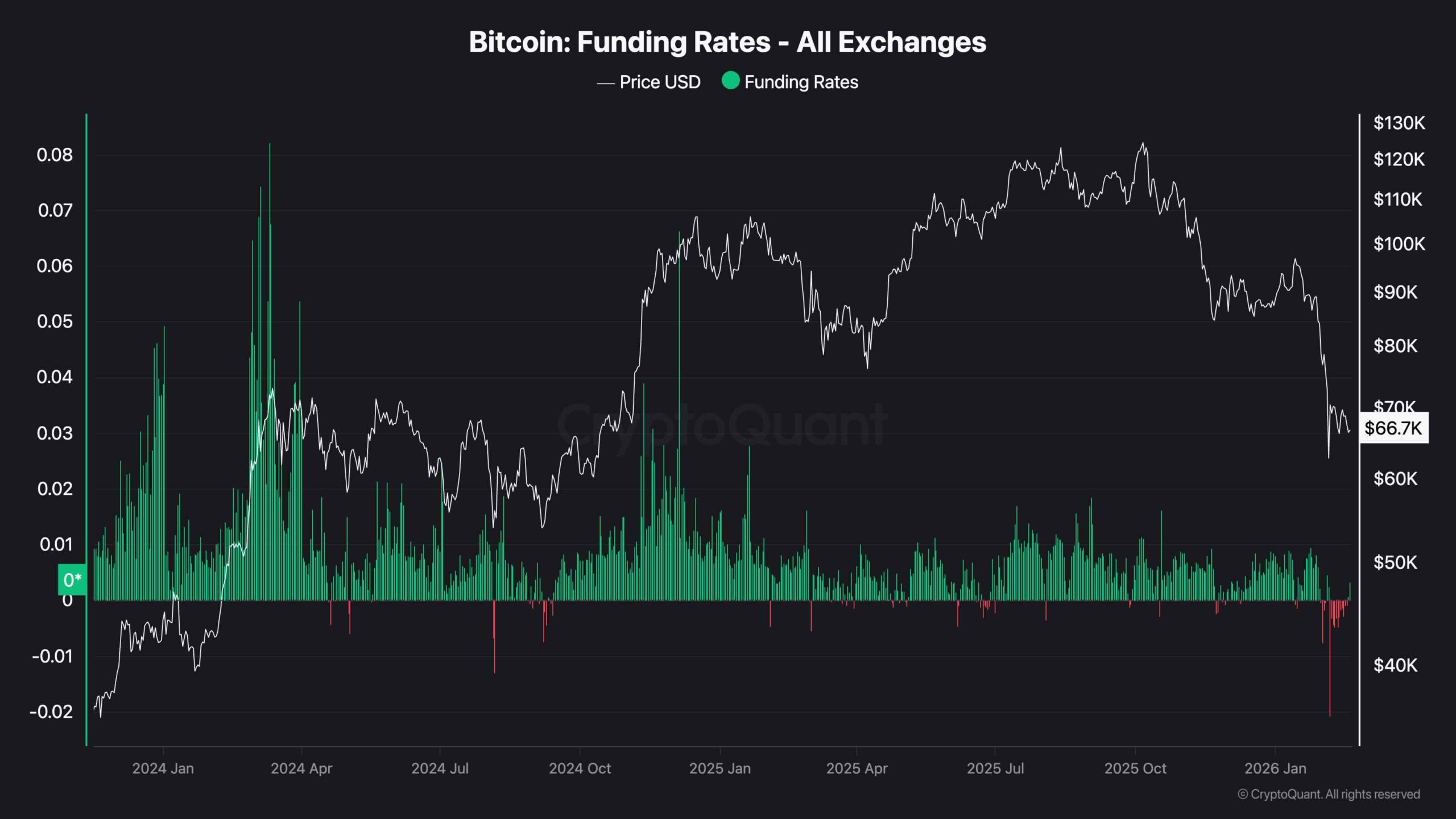

Funding rate data shows sentiment cooling significantly compared to earlier overheated conditions, with the recent deeply negative prints suggesting reduced long-side leverage. This type of reset is constructive over the medium term but does not, by itself, confirm an immediate bullish reversal.

Overall market psychology appears cautious rather than euphoric, which often precedes range formation before the next major move. For sentiment to flip decisively bullish, price strength must return alongside rising but controlled funding and improving momentum across timeframes.

Advertisement

SPECIAL OFFER (Exclusive)

SECRET PARTNERSHIP BONUS for CryptoPotato readers: Use this link to register and unlock $1,500 in exclusive BingX Exchange rewards (limited time offer).

Disclaimer: Information found on CryptoPotato is those of writers quoted. It does not represent the opinions of CryptoPotato on whether to buy, sell, or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk. See Disclaimer for more information.

In Washington, the safest vote is often no vote at all, and the most convenient timeline is “next session.” But when it comes to the future of banking, financial markets and financial services, inaction is unacceptable. The United States needs crypto regulatory clarity to compete and succeed in the digitally networked financial system of the 21st Century.

The Senate is today at a crossroads on market structure legislation—policy designed to bring order to digital asset innovation, an increasingly important component of global finance. Failing to codify the “rules of the road” doesn’t just stall crypto; it invites regulatory chaos that harms banks and consumers alike, saps economic dynamism and forces innovation to drift offshore. Congress must choose whether America leads the next generation of finance or watches from the sidelines.

The current stalemate centers on a perceived conflict between banks and crypto platforms regarding interest yield and rewards on stablecoins—an issue already addressed by the GENIUS Act, signed into law by President Trump last year. The law permits crypto companies to offer rewards and incentives to customers for holding and using stablecoins made available by separate providers. Banks counter that such reward structures closely resemble traditional bank savings and checking products and, if left unchecked, could shift customer balances away from insured deposits without the same prudential requirements.

Framed this way, the disagreement carries more weight than it should. Yield and rewards are questions of design within a payments framework, not questions of systemic safety or financial stability. Treating them as existential risks has delayed an otherwise straightforward resolution, stalling progress on crucial market structure issues.

Advertisement

If one looks past talking points, a workable compromise is already available. Congress can explicitly enable federally regulated banks—including community banks—to offer yield on payment stablecoins. Banks gain a clear, federally sanctioned revenue and customer-acquisition opportunity in the stablecoin market. They obtain a straightforward way to secure customers and funds, especially important for community banks seeking to remain competitive in a world of mega-banks and scaled payment platforms. Crypto platforms, meanwhile, retain the incentive structures their customers expect and that are available under existing law. Congress gets to move market structure legislation forward and create a bill that can pass. And, most importantly, the American consumer benefits from increased competition and the ability to share in the yield potential of their own money.

Framing crypto as an existential threat to the community bank is a rhetorical tactic, not an economic reality. A recent empirical analysis finds no statistically meaningful relationship between stablecoin adoption and deposit outflows, suggesting stablecoins function primarily as transactional instruments rather than savings substitutes. In fact, properly regulated stablecoins may provide local and community banks with a pathway to modernize their payment offerings and reach new customers.

The rewards-yield question is a design issue that can be addressed without upending progress already made. A workable compromise exists that addresses banks’ economic interests, protects crypto innovation and respects the settled law of the GENIUS Act. Advancing on that basis keeps the broader market structure package intact and provides the legal clarity that the American economy deserves.

The Senate has the tools to resolve this impasse and to follow the strong leadership displayed by the White House. Failing to do so would be a choice, not an inevitability.

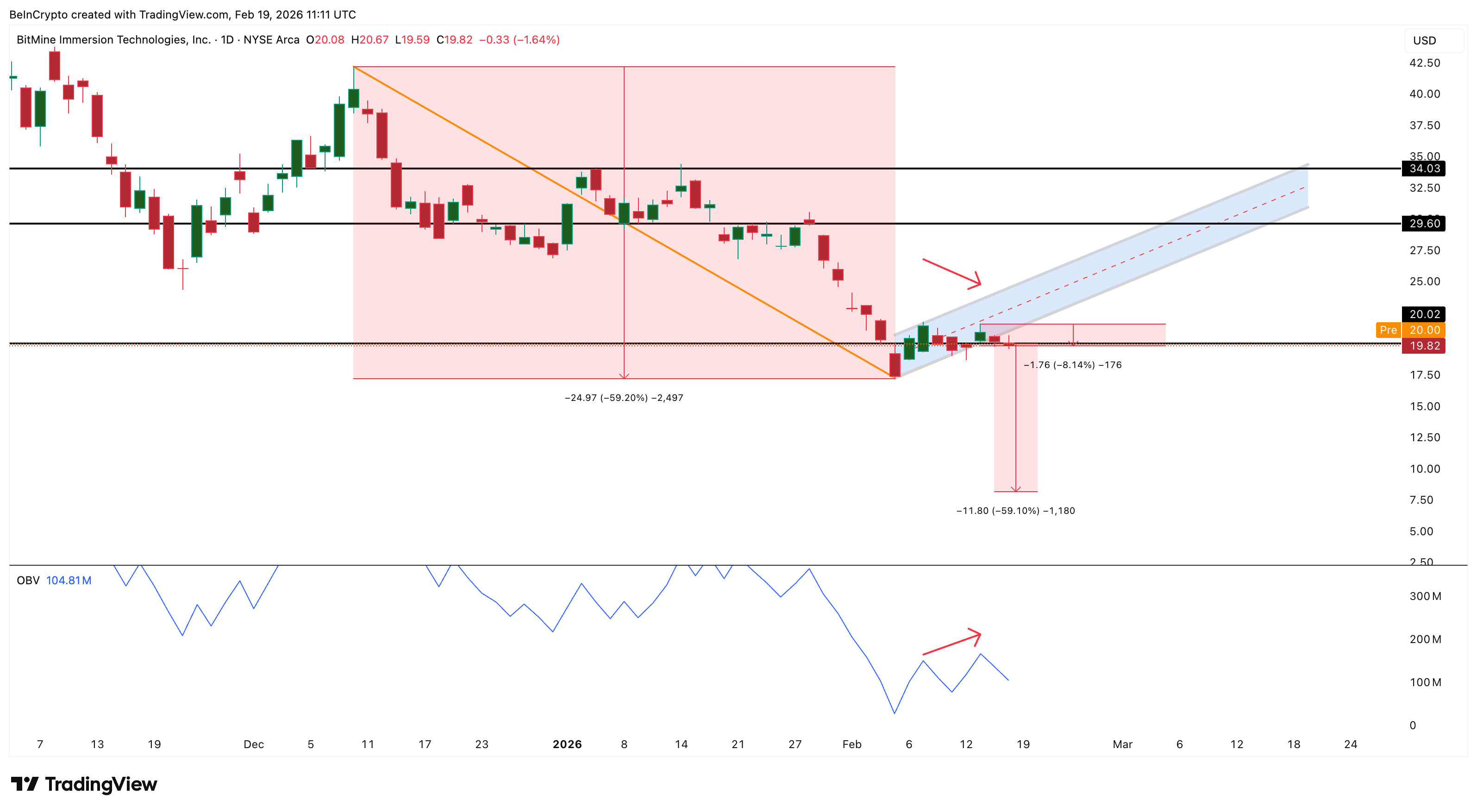

Tom Lee’s BitMine Immersion Technologies just bought another 35,000 ETH, expanding its already massive Ethereum treasury. Normally, such aggressive accumulation would signal confidence and support the stock price. Instead, the BitMine stock price fell nearly 2% in the past 24 hours and is now down more than 8% since February 13.

This creates a strange contradiction. BitMine keeps buying Ethereum, yet its stock keeps falling. At first glance, it looks like two different stories. But underneath, it might all be the same.

Sponsored

Sponsored

Advertisement

BitMine Adds More Ethereum, But the Stock Breaks Down

BitMine’s latest Ethereum purchase reinforces its strategy of becoming one of the largest ETH treasury companies. Buying 35,000 ETH, in two batches, in a single day, shows long-term conviction. The purchase pushed its total holdings to 4.371 million ETH, with combined cash and crypto reserves now worth around $9.6 billion.

Want more insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

Companies usually increase holdings when they expect higher future prices, not lower ones. However, the stock price reaction tells a very different story. Since February 13, BitMine stock has dropped over 8%, and the technical chart now shows a breakdown.

The stock recently fell below the lower boundary of a bear flag pattern. A bear flag forms after a sharp drop, followed by a weak recovery.

Advertisement

BitMine Stock Price And A Bearish Pattern: TradingView

When the lower support breaks, it often signals that the prior recovery structure has weakened and the stock has entered a technically fragile zone. Based on the pattern structure, the ongoing breakdown path could extend by over 50% if the weakness persists. However, this price decline does not automatically confirm active investor selling, which we will see in the next section.

This creates a disconnect between BitMine’s strengthening treasury position and its weakening stock price, suggesting that other external factors may be influencing the move.

Sponsored

Sponsored

Retail Buying Improves, But Big Money Remains Cautious

Despite the falling price, investor behavior beneath the surface shows some early strength. One key indicator is On-Balance Volume, or OBV. This metric tracks cumulative buying and selling pressure. When OBV rises, it means investors, possibly retail, are buying. possibly retail, are accumulating, even if the price has not responded yet.

Between February 9 and February 13, BitMine’s stock price formed a lower high, showing weakening price strength. However, OBV formed a higher high during the same period. It signals that buying activity is increasing quietly. This suggests retail investors were still accumulating BitMine stock despite the falling price.

Another important indicator, the Chaikin Money Flow, or CMF, also shows improving conditions.

CMF measures whether large capital is entering or leaving a stock. The indicator has been rising recently, showing improving inflows and showing divergence similar to OBV.

Sponsored

Sponsored

Advertisement

However, CMF remains below the zero line, which means overall capital flow into BitMine is still negative. This suggests that large institutional investors are not fully supporting the recovery yet. Retail investors are stepping in, but institutional money remains cautious.

Big Money Weak But Improving: TradingView

Together, the rising OBV and improving CMF suggest that underlying participation is stabilizing rather than collapsing. This indicates that the recent breakdown may not be driven by aggressive selling from BitMine investors. Instead, the stock’s weakness appears more closely linked to Ethereum’s own price pressure, reflecting BitMine’s growing role as a high-beta proxy for ETH rather than a stock moving independently.

Ethereum Weakness Is Dragging BitMine Stock Price Lower

The biggest reason behind BitMine’s stock decline becomes clear when comparing it with Ethereum. BitMine’s price is highly correlated with Ethereum’s price. Correlation measures how closely two assets move together. BitMine’s correlation with Ethereum has increased from 0.50 to 0.52. This means the stock is behaving more like a direct proxy for Ethereum.

BMNR-ETH Correlation: Portfolio Slab

Sponsored

Sponsored

At the same time, Ethereum’s futures market shows rising bearish sentiment. The Ethereum long-short ratio has dropped to extremely low levels. This ratio measures how many traders expect prices to rise compared to fall. A low ratio means most traders expect further declines.

Advertisement

This bearish positioning directly impacts BitMine. Because BitMine holds a massive Ethereum treasury, its stock tends to weaken when Ethereum itself faces bearish pressure.

The technical chart now shows key levels ahead. BitMine has already lost support near $19. The next major support sits near $15. If that level breaks, the stock could fall toward $12 and even $9, which would be closer to the projected bear-flag breakdown level.

BMNR Price Analysis: TradingView

On the upside, recovery would first require reclaiming $21. A stronger bullish reversal would need a move above $29.

BitMine buying more Ethereum should have been a bullish signal. Retail investors are slowly accumulating, and capital inflows are improving. However, institutional money remains cautious, and Ethereum itself is facing bearish sentiment. Because BitMine now moves closely with Ethereum, its stock direction depends heavily on Ethereum’s strength. If Ethereum remains weak, BitMine may continue facing pressure regardless of its purchases.

On the surface, BitMine buying Ethereum and BitMine stock falling look like two different events. But in reality, they reflect the same underlying force.

Lemonade (LMND) Q4 revenue hit $228.1 million, up 53.3% year-on-year, beating estimates of $217.6 million

Adjusted EPS loss of -$0.29 beat analyst estimates of -$0.39 by $0.10

Net premiums earned came in at $179.5 million, an 8.3% beat and 77.4% year-on-year growth

Q1 2026 revenue guidance of $246–$251 million tops analyst consensus of $241.6 million

Shares jumped over 17% in pre-market trading following the results

Lemonade (NYSE: LMND) shares surged more than 17% in pre-market trading on Thursday after the company posted Q4 results that beat analyst expectations across the board.

Revenue for the quarter came in at $228.1 million, up 53.3% year-on-year and ahead of the Wall Street consensus of $217.6 million. That’s a solid beat by any measure.

The company reported an adjusted loss of $0.29 per share, compared to analyst estimates of -$0.39. That’s a $0.10 beat, or roughly 26% better than expected.

Net premiums earned — the number analysts tend to watch most closely for insurers — came in at $179.5 million. That beat estimates of $165.8 million by 8.3% and grew 77.4% compared to the same quarter last year.

Pre-tax loss for the quarter was $20.6 million, representing a -9% margin.

Advertisement

Strong Premium Growth Drives the Beat

Net premiums earned have grown at a 47.3% annualized rate over the last five years, well above the broader insurance industry average.

Over the past two years, that growth rate has moderated to around 30% annually — still a healthy clip, and consistent with the company’s overall revenue trajectory.

Lemonade’s revenue has compounded at roughly 50.9% annually over the last five years. The most recent two-year annualized rate of 31% shows some deceleration but still points to strong underlying demand.

Net premiums earned made up about 70.8% of total revenue over the last five years, making it the company’s primary revenue driver.

Advertisement

Q1 2026 Guidance Tops Estimates

Looking ahead, Lemonade guided Q1 2026 revenue to between $246 million and $251 million. The midpoint of that range, $248.5 million, comes in above the analyst consensus of $241.6 million.

That forward guidance gave investors an additional reason to bid the stock higher on Thursday morning.

Lemonade operates across renters, homeowners, pet, car, and life insurance in both the U.S. and EU markets through its AI-powered digital platform.

The company’s Giveback program, which donates unused premiums to policyholder-selected charities, remains a differentiator in its positioning — though it’s the underlying growth numbers doing the heavy lifting right now.

Advertisement

Lemonade held a market capitalization of $4.91 billion at the time of reporting.

The company hosted a conference call Thursday at 8:00 am Eastern to discuss results.

Shares traded up 11.1% to $73.05 immediately after the report, with pre-market gains extending above 17% as the session progressed.

Choosing the right scaling architecture is one of the most critical decisions in modern crypto development. The wrong choice can lead to high fees, slow performance, security risks, and stalled adoption. The right choice can unlock growth, institutional trust, and long-term sustainability. This choice impacts system resilience and future upgrade flexibility with the support of a crypto development company.

In this guide, we break down Layer-2, Sharding, and Hybrid models to help you select the most scalable, secure, and future-ready approach for your product.

Why Scalability Is the Biggest Challenge in Crypto Development

As blockchain adoption grows, platforms face increasing pressure to handle:

Higher transaction volumes

Lower latency expectations

Rising compliance standards

Complex integrations

Institutional security requirements

Many crypto coin development projects fail not because of weak ideas, but because their infrastructure cannot scale sustainably.

Common challenges include:

Advertisement

Network congestion

Unpredictable transaction fees

Poor user experience

Limited throughput

Regulatory constraints

These issues directly affect retention, revenue, and valuation.

Discover the Best Architecture for Your Platform.

Understanding the Three Main Scaling Approaches

Selecting the right scaling model is a foundational decision in crypto development. Your choice determines performance, cost structure, compliance readiness, and long-term growth. This decision becomes a powerful growth advantage with the right strategy and expert guidance.

1. Layer-2

Layer-2 solutions process transactions outside the main blockchain while inheriting its security. Only final transaction proofs are submitted to Layer-1. This model has become the backbone of many successful crypto development platforms because it delivers scalability without sacrificing reliability.

Layer-2 Overview

Category

Details

Processing Method

Off-chain batching with on-chain settlement

Security

Inherits Layer-1 security

Transaction Cost

Very low

Tooling Ecosystem

Mature

Wallet Support

Strong

Ideal Users

Startups, DeFi, Payments, Gaming

Main Risks

Bridge security, L1 dependency

For most crypto coin development services, Layer-2 offers the best balance between speed, affordability, and long-term stability. With proper implementation, Layer-2 becomes a strong foundation for sustainable growth and rapid market adoption.

2. Sharding

Sharding is designed for teams building new blockchain protocols and foundational infrastructure. It focuses on scaling at the network level rather than at the application layer.

Advertisement

Sharding Overview

Category

Details

Processing Method

Parallel shard execution

Security

Shared validator security

Scalability

Very high (theoretical)

Deployment Speed

Slow

Development Complexity

High

Ecosystem Maturity

Limited

Ideal Users

Layer-1 builders, infrastructure teams

Main Risks

Cross-shard communication, security coordination

For crypto development company teams working on next-generation blockchain networks, sharding enables deep technical control and long-term ownership. Sharding can position teams as leaders in protocol innovation, with strong expertise and planning.

3. Hybrid Architecture

Hybrid architecture is designed for organizations that require scalability, privacy, and regulatory alignment. It combines multiple systems to balance decentralization with operational control.

Hybrid Architecture Overview

Category

Details

Processing Method

Private networks + L2 + public settlement

Security

Controlled with public anchoring

Privacy Level

High

Regulatory Support

Strong

Deployment Speed

Medium

Operational Cost

High

Ideal Users

Banks, RWA platforms, enterprises

Main Risks

Governance complexity, infrastructure cost

Hybrid systems are widely used in institutional crypto coin development because they support compliance, governance, and enterprise integration. With the right technical partner, hybrid architecture becomes a future-ready platform for large-scale adoption.

Which Scaling Model Should You Choose?

Business Priority

Best-Fit Model

Fast Market Entry

Layer-2

Low Operational Cost

Layer-2

New Blockchain Development

Sharding

Regulatory Compliance

Hybrid

Enterprise Privacy

Hybrid

Most successful crypto projects begin with a clear architecture roadmap and evolve as their user base, revenue, and regulatory exposure grow. When supported by an experienced crypto development company, scalability becomes a competitive advantage that drives long-term success.

Advertisement

Get Personalized Guidance for Your Crypto Growth Strategy

Common Mistakes in Scalable Crypto Development

Many projects struggle not because of weak ideas, but because of avoidable strategic and technical errors. In scalable crypto development, early decisions have long-term consequences on performance, cost, security, and investor confidence. Working with an experienced partner helps reduce these risks, but founders and technical leaders must also understand the most common pitfalls.

Avoid these costly mistakes:

1. Choosing technology before defining the business model

Selecting Layer-2, sharding, or hybrid systems without understanding user needs, revenue flows, and compliance requirements often leads to misaligned infrastructure.

2. Ignoring compliance and regulatory planning early

Advertisement

Delaying legal and KYC considerations can block partnerships, exchange listings, and institutional funding.

3. Underestimating long-term infrastructure and maintenance costs

Many crypto coin development projects budget only for launch, not for ongoing node operations, indexing, monitoring, and upgrades.

4. Skipping independent security audits and testing

Advertisement

Unreviewed smart contracts expose platforms to exploits, fund loss, and reputation damage.

5. Delaying scalability planning until growth occurs

Retrofitting scalability after user adoption is expensive, risky, and disruptive.

Many failed crypto coin development projects made these mistakes, resulting in stalled growth, lost trust, and wasted capital. Planning scalability from the beginning is essential for long-term success.

Advertisement

Final Words

Choosing between Layer-2, sharding, and hybrid architecture is a strategic decision that directly impacts performance, compliance, and long-term growth. While Layer-2 suits most high-growth platforms, hybrid models serve regulated enterprises, and sharding supports core protocol builders. The key to success is aligning your technology with your business goals and working with a trusted cryptocurrency development company that understands both engineering and market realities.

Antier, a leading crypto development company, delivers end-to-end solutions, from architecture design and security audits to compliance integration and infrastructure optimization. We help businesses launch faster, scale smarter, and operate with confidence. Ready to build with confidence? Book your free consultation with Antier today and get a personalized scalability roadmap for your project.

Frequently Asked Questions

01. What is the importance of choosing the right scaling architecture in crypto development?

Choosing the right scaling architecture is crucial as it affects transaction fees, performance, security, and overall adoption. The right choice can lead to growth, institutional trust, and long-term sustainability.

02. What are the common challenges faced in crypto development related to scalability?

Common challenges include network congestion, unpredictable transaction fees, poor user experience, limited throughput, and regulatory constraints, all of which can impact retention, revenue, and valuation.

Advertisement

03. What are the three main scaling approaches discussed in the guide?

The three main scaling approaches are Layer-2, Sharding, and Hybrid models, each offering different benefits in terms of scalability, security, and future readiness for crypto platforms.

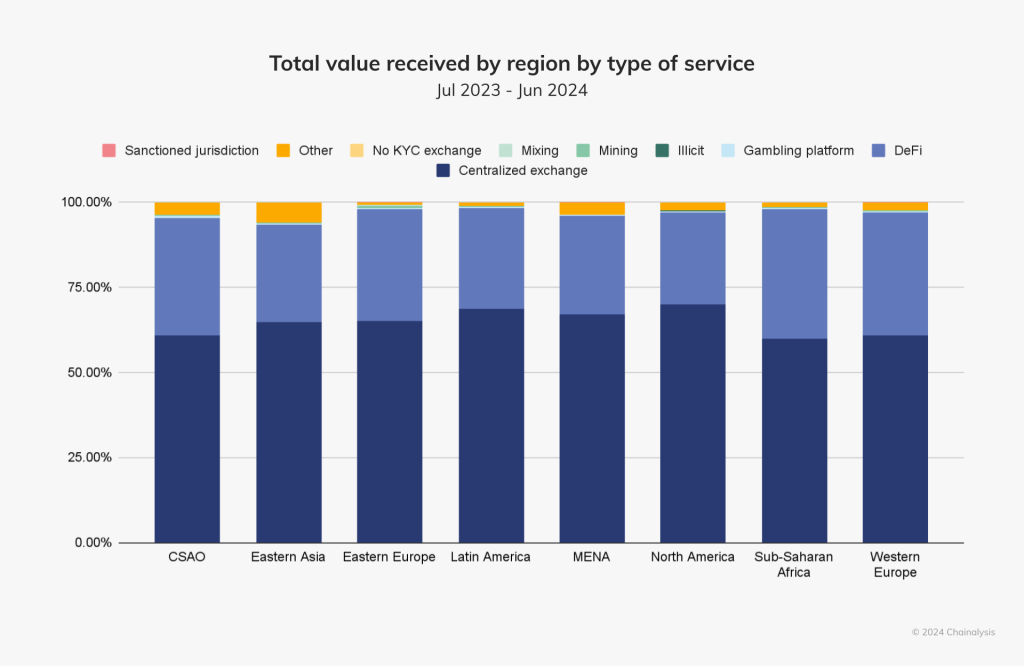

Cryptocurrency trading volumes in Latin America grew 63% and crossed $1.5 trillion between July 2024 and June 2025, establishing the region as one of the most crypto-progressive regions. In February 2026, Argentina, Brazil, and El Salvador dominated the headlines with noteworthy cryptocurrency developments. El Salvador plans a $100M tokenized investment program for localized SMEs, where Brazil considers eliminating crypto taxes and establishing a strategic Bitcoin reserve, and Argentina revokes the right to receive salaries in digital wallets. These signals demonstrate how LATAM governments and businesses are actively experimenting with new financial models.

Crypto finance group, a part of Deutsche Börse Group, entered LATAM after it sensed a “strong, concrete demand from institutions for well-structured, compliant crypto offerings”, in the words of Vander Straeten, the CEO.

If institutional capital and policy momentum are converging this fast, it is clear that LATAM crypto exchange development is commercially compelling in 2026 and beyond. However, this opportunity materializes only for platforms designed around the region’s real adoption mechanics.

What Actually Drives LATAM Digital Asset Adoption?

Crypto exchange software businesses can’t reach 200K users in LATAM by listing region-popular pairs or tokens or by increasing the leverage. The region’s digital asset adoption curve is driven by currency stability, cross-border transfer dependency, and mobile-first fintech habits.

Advertisement

By the end of 2025, LATAM had approximately 70 million unique crypto users, up from 73.7 million in Q3 2025 and 57.7 million earlier in the year. But the growth didn’t come from speculation but utility.

1. Inflation Hedging Via Stablecoins

Currency volatility remains the primary entry trigger in markets like Argentina, where inflation has stayed structurally high. In such markets, stablecoins function as everyday digital dollars rather than trading assets.

Stablecoins dominated more than 90% of exchange flows in Brazil, 62% in Argentina, and 48-60% region-wide. This proves that most users in the Latin American region hold balances for savings and payments, not trading.

LATAM received an estimated $165.1 billion in remittances in 2024, and another research predicted it would reach $174.4 billion by the end of 2025. Crypto has been increasingly used to bypass high-fee corridors.

Advertisement

Mexico, which is the second-largest corridor from the US, alone totaled $63.3 billion in remittances in 2024-25. Bitso, a leading crypto exchange software, handled over $6.5 billion in US-Mexico remittances, which totaled in 2024, representing more than 10% of the total corridor volume.

Stablecoin-based remittances cut costs by 50-80%, dropping from traditional 6-7% averages to 1-3%. High-fee LATAM corridors even benefit from 76% savings with stablecoins.

3. P2P and Social Money Behavior

Money movement in Latin America is socially mediated between families, communities, and informal networks, rather than institutionally intermediated. Crypto leads the peer-to-peer money movement in the region due to the popularity of social tipping and community payments. Many users from the region adopt wallets through contacts and not financial products.

Tron has sustained as a high-volume blockchain infrastructure supporting 78% of P2P transfers, which is an essential crypto exchange development feature for LATAM.

4. Mobile-Native Onboarding Expectations

LATAM fintech usage is mobile-centric, with 70% regional mobile penetration, and strong familiarity with chat-based payments. More users are expecting WhatsApp-style transfers and low-literacy onboarding flows with instant notifications and real-time balances in the application. So, crypto exchange software businesses in the region are competing with neobanks, not global trading apps.

Advertisement

In short, LATAM cryptocurrency exchange software scales when they behave like payment rails, not a trading terminal.

Essential Crypto Exchange Development Features Required to Reach 200K Users in Latin America

The primary crypto exchange software development feature in LATAM isn’t order books but stablecoin wallets. Exchanges that nurture their in-built centralized or decentralized wallets can capture the audience that approaches crypto exchange apps as a dollar account. Here are essential crypto wallet components for LATAM exchanges:

As deduced from the statistics above, remittances create the strongest viral loop in the region. Peer-to-peer transfer engine forms another essential component for LATAM crypto exchange development. These features fetch revenues and act as customer magnets at the same time as each remittance/payment sender typically onboards 1-3 new users. So, for businesses planning to launch their digital asset exchange, the following capabilities are indispensable:

Cross-border stablecoin transfers

QR / phone-number payments

P2P marketplace matching

Chat-based or whatsapp style P2P transfers

Local cash-out counterparties

Corridor-specific liquidity routing

3. Local Fiat Rails

Instant and cost-efficient fiat access determines retention for crypto exchanges in LATAM. Users quickly abandon platforms that delay deposits and withdrawals beyond minutes or fail to support end-to-end money movement. For this reason, any cryptocurrency exchange software development targeting this region must implement Pix-style crypto-fiat rails as a foundational layer. These are the basic requirements:

In countries like Latin America, where money flows socially before it flows financially, community finance features accelerate onboarding and adoption. Money movement mostly occurs within creator communities, family groups, and informal networks rather than purely financial contexts. As a result, cryptocurrency exchange software in the LATAM region increasingly functions as a social finance platform where users interact, tip, and transact around personalities and communities. Implementing creator monetization and community finance tools, along with the following features inside the exchange helps exchanges engage a wider audience.

In the LATAM region, speculative behavior is culturally linked to sports outcomes and macroeconomic events rather than traditional financial instruments. Prediction markets embedded inside crypto exchange software, therefore, attract users who may not engage with spot or derivatives trading but are comfortable with simple outcome-based participation. Cryptocurrency exchanges can create familiar entry points into digital asset usage and still generate liquidity, engagement, and revenue with the following:

Stablecoin savings represent one of the strongest retention drivers in inflation-prone Latin American economies, where users seek protection from local currency devaluation. Many users adopt crypto exchange wallets primarily to store digital dollars rather than to trade or transact. Crypto exchange software solutions that integrate accessible yield or savings interfaces can therefore retain liquidity and transition utility users into broader financial activity with gamification and rewards.

One-tap stablecoin savings or vault accounts

Transparent APY display in USD

Recurring local-to-USD conversion

Flexible withdrawals or redemption options

Risk tier or yield source labeling

A LATAM exchange that reaches 200K users behaves as a dollar wallet, remittance network, social finance app with trading infrastructure and engagement layers operating in the background rather than the foreground.

What are the UX Principles that Support Sustainable and Fast LATAM Crypto Exchange Software Growth?

As stated earlier, most LATAM cryptocurrency exchange software users are leveraging trading platforms for their financial needs. Exchanges that aim to scale quickly in the region must mirror familiar mobile money patterns and minimize cognitive and compliance friction at entry. Let’s again highlight the UX essentials for LATAM cryptocurrency exchange development:

1. USD-first balances as users in inflationary markets think in dollars even when transacting locally. Displaying portfolios and transaction values in USD by default aligns the app with real financial perception.

Advertisement

2. Simplified KYC entry and verification allow low-limit onboarding and accelerate first transactions while deferring heavier compliance steps to later stages of engagement.

3. WhatsApp-like transfers, chat-style sending, contact-based payments, and conversational confirmations reduce learning effort. Such financial experience matches how users already communicate over messaging apps.

4. Low-literacy-friendly flows can be created with icon-led actions, guided steps, and clear visual confirmations. This enables users across varied education levels to complete transfers and deposits without confusion.

5. Offline-friendly lightweight alerts, queued transaction updates, and low-bandwidth operation ensure efficient operation in environments with inconsistent connectivity.

Advertisement

Launch a LATAM-ready crypto exchange with Antier’s production-grade infrastructure

Closing: Why Most LATAM-Based Crypto Exchange Software Fail & How They Can Reach 200K Users in 6 Months

Many cryptocurrency exchange software launches in Latin America underperform, not because the markets lack demand, but because platforms are built around trading assumptions instead of regional money behavior. So, this is what businesses must avoid during crypto exchange development and launch;

Launching trading before payments

Providing USD as a secondary balance

Slow fiat rails

Heavy KYC at entry

No cash-out liquidity

To make a crypto exchange software development project scale to hundreds of users in the first 180 days, crypto exchanges must primarily launch stablecoin wallets, local fiat rails, remittance loops, and social finance features.

This is why the fastest-growing LATAM cryptocurrency exchanges function less like trading terminals and more like payment networks layered with savings and social money features. Trading remains present, but it operates as a monetization layer that activates after users already rely on the app for everyday financial activity.

Antier offers LATAM-ready white label cryptocurrency exchanges and custom development solutions with the exact stack required to reach 200K users in 6 months. We support the full lifecycle from development and launch to growth and compliance. Connect today!

Frequently Asked Questions

01. What was the growth percentage of cryptocurrency trading volumes in Latin America between July 2024 and June 2025?

Cryptocurrency trading volumes in Latin America grew by 63% and crossed $1.5 trillion during that period.

Advertisement

02. What are some notable cryptocurrency developments in Argentina, Brazil, and El Salvador as of February 2026?

El Salvador plans a $100M tokenized investment program for SMEs, Brazil is considering eliminating crypto taxes and establishing a Bitcoin reserve, and Argentina has revoked the right to receive salaries in digital wallets.

03. What factors drive digital asset adoption in Latin America?

Digital asset adoption in LATAM is driven by currency stability, dependency on cross-border transfers, and mobile-first fintech habits, rather than speculation.

Editor’s note: Gold has surged on geopolitical uncertainty and sticky inflation, creating a broad bullish backdrop that has carried prices to fresh highs. A pause in the rally, like this week’s dip below US$5,000, can be a healthy consolidation rather than a sign of weakness. This editorial note frames the accompanying press release as a measured read on near-term dynamics, while acknowledging the longer-term drivers — such as central bank activity, ETF demand, and policy expectations — that keep gold well bid. For UAE investors and global traders, the current pullback may offer a cautious entry point into the next leg higher.

Key points

Gold dips below US$5,000 after a 14% year-to-date rally, seen as consolidation by eToro.

The move followed hawkish signals from Trump nominee Warsh; trading volumes thinner during Lunar New Year.

Longer-term drivers remain intact: geopolitical risk, sticky inflation, and a shifting US rate outlook.

Potential for another leg higher as Fed rate trajectory and cut expectations evolve; UAE investors see entry points in volatility.

Why this matters

This release underlines that near-term volatility does not erase gold’s fundamental support, with central bank demand and ETF inflows suggesting further upside as policy expectations evolve.

What to watch next

Monitor US inflation data for potential shifts in rate expectations.

Watch for new geopolitical developments that could reignite momentum.

Track ETF inflows and central bank activity that could sustain the rally.

Disclosure: The content below is a press release provided by the company/PR representative. It is published for informational purposes.

Press release: Gold Dips Below US$5,000 After 14% Rally

Abu Dhabi, UAE – February 19, 2026: Gold’s pullback below the US$5,000 level this week should not unsettle investors, according to eToro, which views the move as a natural consolidation within one of the strongest bull runs in recent years.

Zavier Wong, Market Analyst at eToro

Gold’s dip below US$5,000 this week shouldn’t rattle investors. If anything, it’s a healthy pause in what remains one of the strongest bull runs in recent memory. — Zavier Wong, Market Analyst at eToro

The precious metal touched fresh record highs above US$5,000 earlier this month before retreating, following market reaction to former US President Donald Trump’s nomination of Kevin Warsh as Federal Reserve Chair. Investors interpreted the pick as hawkish, weighing on gold prices in the short term.

The move was further amplified by thinner trading volumes during the Lunar New Year period and US market holidays. However, Wong noted that much of the initial reaction has already been priced in, and the broader drivers behind gold’s rally remain firmly intact.

Advertisement

“Gold has gained more than 14% since the start of the year, and the conditions that have driven that rally — including geopolitical uncertainty, sticky inflation concerns, and a shifting US rate outlook — haven’t gone anywhere.” — Wong added

For UAE investors, the fundamentals supporting gold remain unchanged. Central bank buying continues at a steady pace, ETF inflows are building, and institutional conviction behind the rally appears far from exhausted.

“When you layer in growing expectations that the US Federal Reserve could cut rates later this year, the case for holding gold only strengthens. That means another leg higher from here is not off the cards, and further record highs aren’t out of the question.” — Zavier Wong, Market Analyst at eToro

Wong emphasised that the current price action should be viewed as the market “catching its breath” rather than losing conviction, with gold continuing to trade near key technical support levels.

“The best way to look at this current consolidation is that the market is essentially catching its breath rather than losing conviction. Any fresh catalyst – whether a softer US inflation print or an escalation in geopolitical tensions – could quickly reignite momentum.” — he said.

For investors in the UAE already holding gold, this week’s volatility is likely to be short-term noise. For those still on the sidelines, Wong suggested it may offer a more attractive entry point than seen in recent weeks.

About eToro

eToro is the trading and investing platform that empowers you to invest, share and learn. We were founded in 2007 with the vision of a world where everyone can trade and invest in a simple and transparent way. Today we have 40 million registered users from 75 countries. We believe there is power in shared knowledge and that we can become more successful by investing together. So we’ve created a collaborative investment community designed to provide you with the tools you need to grow your knowledge and wealth. On eToro, you can hold a range of traditional and innovative assets and choose how you invest: trade directly, invest in a portfolio, or copy other investors. You can visit our media centre here for our latest news.

Advertisement

Risk & affiliate notice: Crypto assets are volatile and capital is at risk. This article may contain affiliate links. Read full disclosure

(@Binansmartkid) February 18, 2026

(@Binansmartkid) February 18, 2026

Video3 days ago

Video3 days ago

Tech4 days ago

Tech4 days ago

Crypto World2 days ago

Crypto World2 days ago

Sports2 days ago

Sports2 days ago

Video6 days ago

Video6 days ago

Business2 days ago

Business2 days ago

Video2 days ago

Video2 days ago

Entertainment1 day ago

Entertainment1 day ago

Crypto World6 days ago

Crypto World6 days ago

Tech1 day ago

Tech1 day ago

Entertainment17 hours ago

Entertainment17 hours ago

Business1 day ago

Business1 day ago

Crypto World6 days ago

Crypto World6 days ago

Crypto World20 hours ago

Crypto World20 hours ago

Crypto World7 days ago

Crypto World7 days ago

NewsBeat5 days ago

NewsBeat5 days ago