The familiar sound of the call for changes to Australia’s Capital Gains Tax (CGT) discount is again increasing in volume, with a Senate Select Committee on the Operation of the Capital Gains Discount likely to recommend a reduction in the discount, which translates into higher taxes.

Based on what’s been floated by the government in the press, it feels almost inevitable that a reduction from the current 50 per cent discount is coming. The extent of it we don’t know, but it’s possible it will be restricted to residential property.

The government talks about intergenerational equity and focusing on making housing affordable, especially for the next generation of homeowners.

Those are important aspirations but the illusion that increasing taxes on investors will unlock supply or reduce prices is just misleading.

Advertisement

Data from leading industry analysts like PropTrack and Cotality tells us that investor activity is primarily a response to our tight rental market, not the root cause of unaffordability.

In many places around Australia, rental vacancy rates are at or near historical lows, which is translating into higher rental prices.

What will reduce rents is more supply of rental properties, not less. You don’t solve a supply problem by penalising those who provide homes to rent.

The push for CGT changes is fundamentally based on the premise that a higher tax burden will result in a more affordable housing market, as investors reduce their appetite for property, allowing more homeowners to enter the market.

Advertisement

But even the Grattan Institute, which is hardly a pro-investor lobby, conceded that such a change would reduce house prices by just 1 per cent.

The real drivers of price growth are far more fundamental; the undeniable imbalance between demand and supply.

Homes aren’t suddenly going to become more affordable because investors have to pay a higher rate of tax when they profit on a sale. The outcome is likely to be the opposite of what’s intended.

Advertisement

Property, for a vast majority of investors, isn’t a get-rich-quick scheme; it’s a long-term wealth building strategy.

Treasury research shows property investors are long term holders. WA Treasury commentary shows that residential investment property in WA is predominantly held long term, not traded frequently.

NSW Treasury goes into more detail, with the mean holding period for investors being 13.7 years.

This is a clear indication that most property owners are long-term asset holders. So, what happens when you hit them with a higher CGT? You don’t encourage more sales.

Advertisement

You incentivise investors to hold onto their properties for even longer to avoid paying a higher tax on exiting the asset.

Already some investors have stated to me that they will hold their properties until they retire and sell when they are in a much lower tax bracket.

Australian property owners are already forking out an estimated $67 billion annually through stamp duty, land tax, and capital gains tax alone. This asset class already pays more than its fair share.

We have a clear, pressing target to build 1.2 million homes over five years. If we are genuinely serious about intergenerational equity and getting more people into home ownership, then our focus must be on supply-side solutions.

Advertisement

That means tackling planning bottlenecks, addressing infrastructure shortfalls, and particularly the labour shortages in the construction industry.

Increasing a tax that impacts long-term investors, whose role is often to meet rental demand when supply is scarce, is nothing more than a distraction from the real work that needs doing.

Let’s stop talking about penalising property owners and start talking about how we get more homes built. That’s the only path to genuine housing affordability.

Premier Inn would be on site of Central Plaza Hotel in Victoria Viaduct in Carlisle

Ian Duncan and Local Democracy Reporter

04:00, 20 Feb 2026

A new Premier Inn hotel in Carlisle city centre could be granted planning permission at a meeting in Workington next week(Image: Local Democracy Reporting Service)

A NEW 104-bedroom hotel in Carlisle city centre could be granted planning permission at a meeting in Workington next week.

Advertisement

Members of Cumberland Council’s planning committee are due to meet at Allerdale House on Wednesday (February 25) to consider the proposal.

The proposed hotel would be on land of the former site of the Central Plaza Hotel in Victoria Viaduct and, according to the report, the applicant is Whitbread.

The report states that the proposed hotel would incorporate a restaurant and bar as well as associated back-of-house facilities.

It is being placed before the committee because it is in the public interest and the application is for a large hotel development on a prominent site that is currently owned by the council.

Advertisement

It is recommended that the application is granted subject to planning conditions and the report states: “The site covers an area of approximately 0.15 hectares and comprises the footprint of the former Grade II listed Central Plaza Hotel. It is located on the western side of Victoria Viaduct, on the edge of Carlisle city centre.

“The site contains a section of the Grade II listed medieval city walls which act as a retaining wall to West Walls and which comprises a mix of traditional stone, bricks and mortar.

“A small remnant staircase and former storage cupboard that served the previous hotel remain in the north-western corner.

“The site is currently accessed from Backhouse Walk to the south of the site, with direct access not currently available from Victoria Viaduct or West Walls given level differences.”

Advertisement

According to the report Victoria Viaduct, to the east, features retail and office buildings linking onto English Street and Devonshire Street at the northern edge of Carlisle’s retail centre.

The planned Premier Inn hotel in Carlisle city centre(Image: Local Democracy Reporting Service)

It states: “Carlisle Railway Station lies further to the east beside the Carlisle Citadel. To the south, between Backhouse Walk and English Damside, are traditional warehouses and former industrial buildings facing the railway.

“Backhouse Walk is a narrow lane set below the level of Victoria Viaduct, whilst West Walls bounds the site to the north, opposite the blank side elevation of the former Tesco supermarket and the service yard of Marks & Spencer.”

According to the report the proposed development comprises the erection of a five-storey, 104-bedroom Premier Inn hotel. It adds: “The bedrooms would be distributed across the lower ground, first, second, and third floors, supported by ancillary areas including linen stores, plant rooms and staff accommodation.”

Thailand needs an economy that delivers better wages, secure jobs, and real competitiveness. But today’s trade and investment rules stand in the way. Without reform, the country risks falling behind in an increasingly cut-throat global economy.

Key Takeaways

Trade and investment rules hinder competitiveness, rewarding low-value industries and protecting inefficiency.

Outdated tax frameworks distort incentives, especially in auto and electric vehicle industries.

Quota systems in agriculture (coffee, wheat, corn) raise costs, block new entrants, and reduce quality improvements.

Service sectors face heavy restrictions (foreign ownership caps, slow permits), limiting competition and innovation.

Weak regulation allows unsafe, ultra-cheap imports, hurting local businesses and consumers.

Instead of driving growth, these rules reward low-value industry, protect inefficiency, and weaken competition. They protect the wrong things, at the wrong time.

If the economy is to move forward, trade and investment rules must change with it.

Obsolete Tax Framework

The first problem lies in an outdated tax system.

Under World Trade Organization rules, Thailand’s official import taxes have fallen sharply over the past 20 years, averaging about 10% today. On paper, this suggests a more open economy. In reality, the tax structure still shields key industries from real competition.

Advertisement

For decades, tariffs were used to support export-oriented manufacturing. Imported raw materials were taxed less than finished products. This lowered cost for local producers and helped Thai factories compete abroad.

The auto industry is a clear example. Imported parts faced low tariffs, while fully built cars—especially from Europe—were taxed heavily. Local assembly became cheaper, helping Thailand grow into a major vehicle manufacturing base.

But that advantage is fading. As free trade agreements expand, the tax gap between parts and finished products has narrowed. The old system no longer protects local assembly. Manufacturers must adapt—or lose ground.

The electric vehicle industry shows the system no longer works.

Under WTO rates, EVs face higher tariffs than EV parts, which should encourage local assembly. But under the Thailand–China free trade agreement, fully built EVs from China enter duty-free, while key components such as batteries still face tariffs. Importing a whole car can be cheaper than importing parts to build one.

Advertisement

Global Pressures

Thailand faces retaliatory tariffs, oversupply from China, and stricter environmental/labour standards in Europe.

Competing on low prices alone is no longer viable.

That discourages local production.

Meanwhile, EVs imported from Japan still face higher taxes, putting a long-standing investor at a disadvantage due to inconsistent taxation.

The same distortion affects Thai producers of patient-care service robots, who pay higher tariffs on imported motors than on fully assembled machines. Local firms lose before they even start.

Quota system

Tariffs are only part of the problem. Other trade barriers often do more harm.

Advertisement

Take coffee. Thailand drinks a lot of it, but coffee roasting remains small. The quota system is a big reason. Imported beans within the quota face a 30% tax; outside it, the rate jumps to 90%. By contrast, instant coffee is taxed at 49%. It is often cheaper to import ready-made coffee than to bring in beans and roast them in Thailand.

Free trade deals within ASEAN do little to help. Even with lower taxes, importers must buy local beans in matching amounts. This clears stock but removes any push to improve quality.

The same pattern appears across agriculture. Import wheat, and you must also buy local corn. These rules raise costs, keep new players out, and favour those already in the system, since quotas are based on past imports.

Unlike tariffs, quotas bring in no revenue. What they create instead is a system where access matters more than efficiency.

Advertisement

When economists translate these barriers into costs, the impact is clear. In farming and meat products, they add costs as high as—or higher than—import taxes, on top of licences, fees, and red tape.

Service businesses face heavy restrictions. Foreign ownership is capped at 49%. Work permits are slow and complicated. New players are discouraged, and competition stays weak.

Telecommunications shows the problem clearly: few operators, little price pressure, and limited innovation.

According to the Service Trade Restrictiveness Index, Thailand ranks among the most restrictive countries for services—4th out of 51—with little change over the past decade.

These rules keep investment low and limit good service jobs. With weak competition, firms have little reason to improve quality. Ownership limits also encourage nominee arrangements, weakening accountability, with sometimes serious consequences.

Advertisement

Unfair trade

At the same time, weak regulation fails to stop the flood of cheap imports, especially from China.

Consumers face real risks. Many ultra-cheap goods do not meet basic safety standards. During online sales, T-shirts sell for 12 baht, and plastic plates for one. At such prices, no one knows how safe the products are.

Local businesses are paying the price. A survey by the Federation of Thai Industries found that 45% of members saw sales fall by more than 20% because of cheap or low-quality imports.

The damage goes further. Lax environmental and health rules have also turned Thailand into a destination for polluting factories relocating from countries with stricter controls.

Advertisement

Global pressures

Thailand’s domestic weaknesses are colliding with a tougher world economy.

The country faces retaliatory tariffs from the Trump era, global oversupply—especially from China—and stricter environmental and labour rules in major markets such as Europe. Competing on low prices alone no longer works.

Businesses must meet higher standards. The government must push a greener economy, open new export markets, and stop the flood of cheap, substandard imports.

Protection is not the answer. Higher tariffs risk breaking trade commitments, inviting retaliation, and pushing up prices at home—hurting consumers most.

Advertisement

What must change

Needed Reforms

Modernize tariffs and remove unnecessary barriers.

Align production and sustainability standards with global norms.

Increase transparency in procurement and adopt open technical standards.

Allow more foreign ownership and skilled professionals in shortage sectors.

Strengthen competition law, enforce product standards, and regulate online platforms.

Expand exports by accelerating trade talks, especially with the EU, and cutting non-tariff costs.

First, Thailand must upgrade how it produces, link factories and services to global value chains, help firms meet international standards, build modern services, and create decent jobs.

That means fixing old rules. Tariffs should be more even across trading partners. Gaps between raw materials and finished goods must narrow. Unnecessary barriers should be replaced with clear rules—or removed. Production and sustainability standards must match global norms. Public procurement must be transparent and accountable.

In areas like smart cities, open technical standards can prevent dependence on a single supplier, bring Thai firms into supply chains, and encourage technology transfer. Companies should also be responsible for equipment at the end of its life.

Pet food shows the path forward. It has strong export potential—but only if producers meet strict hygiene, sustainability, and traceability rules in Europe and the US.

Advertisement

Upgrading also means greater openness. Becoming a health hub, for example, requires fewer barriers and allowing foreign ownership where it brings skills and investment.

In shortage fields, foreign professionals should be allowed to work and pass on skills, alongside faster training for Thai workers. Data protection rules must also meet global standards, especially in Europe.

Second, Thailand must take unfair trade seriously. Competition law is weak, especially in telecoms and digital platforms. Regulators need real power. Product standards must be enforced, anti-dumping rules made workable, and online platforms held responsible for unsafe goods.

Third, Thailand must expand exports. Nearly half of Thai exports go to markets without free trade deals, such as the US and EU, where Thai goods face higher tariffs than rivals, especially Vietnam. Trade talks must move faster, and existing agreements expanded.

Advertisement

Cutting non-tariff costs—often higher than tariffs themselves—matters as much as cutting tariffs. Talks on standards, services, and skills will be crucial. Negotiations with the EU will be a key test, with tough demands on fair competition, data protection, and sustainability.

Who pays

None of this will be painless. Quotas must be phased out, with clear timelines. Support must be real—from compensation and retraining to helping farmers raise productivity and small firms adjust.

Trade reform is not just about trade. It is about who bears the cost of change—and whether the state helps people through it.

Thailand wants stronger industries and a better quality of life. But its trade rules stand in the way. Until they change, those goals will remain out of reach.

Advertisement

Note: Supanutt Sasiwuttiwat is a research fellow, and Newin Sinsiri is an advisor of the Thailand Development Research Institute (TDRI). This article is an edited version of his keynote speech at TDRI’s Annual Conference on Reimagining Thailand’s Development Model, held on November 17. TDRI’s policy analyses appear in the Bangkok Post on alternate Wednesdays.

ET Intelligence Group: MAS Financial Services (MFSL), a mid-tier micro, small and medium enterprises (MSME) financier, has gained 9% over the past month, outperforming the 2% gain in the BSE Financial Services index. The company reported double-digit growth in disbursement and improving margin profile. It plans to touch ₹1,00,000 crore in consolidated assets under management (AUM) by 2036 from ₹14,641 crore at the end of December 2025, driven by loan segments including MSME, vehicles, and housing. Analysts have retained a ‘buy’ rating on the stock and have raised the target price by 7-9% citing attractive valuation amid improving return ratios and double-digit AUM growth.

The company posted double-digit year-on-year growth in AUM, revenue and net profit for the December 2025 quarter as well as for the first nine months of the current fiscal year (FY26). While this was encouraging, what appealed to investors was the management’s intention to approach the demand revival in the loan market cautiously with focus on asset quality. It implies that the company would not indulge in high-risk bets while chasing the targeted loan growth over the next decade, which will require an annual AUM growth of 30-35%. This is critical given the rising trend in the gross non-performing assets (GNPA). The asset quality ratio has increased in each of the 10 quarters to 2.6% in the December quarter from 2.1% in the June 2023 quarter.

Agencies

Big plans Co has reported double-digit growth in assets, revenue and profit in Q3 and hopes to have ₹1L-crore in assets by 2036

MFSL operates across India through 208 branches. The top four states including Gujarat, Rajasthan, Madhya Pradesh and Maharashtra host nearly 88% of the branches. On a standalone basis, the company has five loan segments including micro enterprises, SME, 2-wheelers, commercial vehicles and salaried personal loans. Of this, micro and SME segments form three-fourth of the standalone loan book of ₹13,782.3 crore. The company also has a rural housing finance subsidiary. Its AUM increased by 22.5% year-on-year to ₹859.2 crore or 6% of the consolidated AUM in the December quarter.

Apart from its own branches, MFSL has tied up with 215 business partners. The company considers this partnership as a major catalyst in accelerating the loan book over the next decade. The management has guided for 20-25% AUM growth and return on assets (RoA) of 2.75-3% in the medium-to-long term. In the December quarter, it clocked an RoA of 2.9%.

Advertisement

“The company is expected to benefit from continued downward repricing of borrowings with incremental cost of funds (CoF) ranging between 9-9.25% versus 9.5% for the December quarter,” noted Axis Securities in a report highlighting that the management expects another 10 basis point reduction in CoF for the March quarter. The broking firm believes that current valuation offers scope for meaningful re-rating on the back of steady performance. It has raised the stock price target by nearly 7% to ₹405.

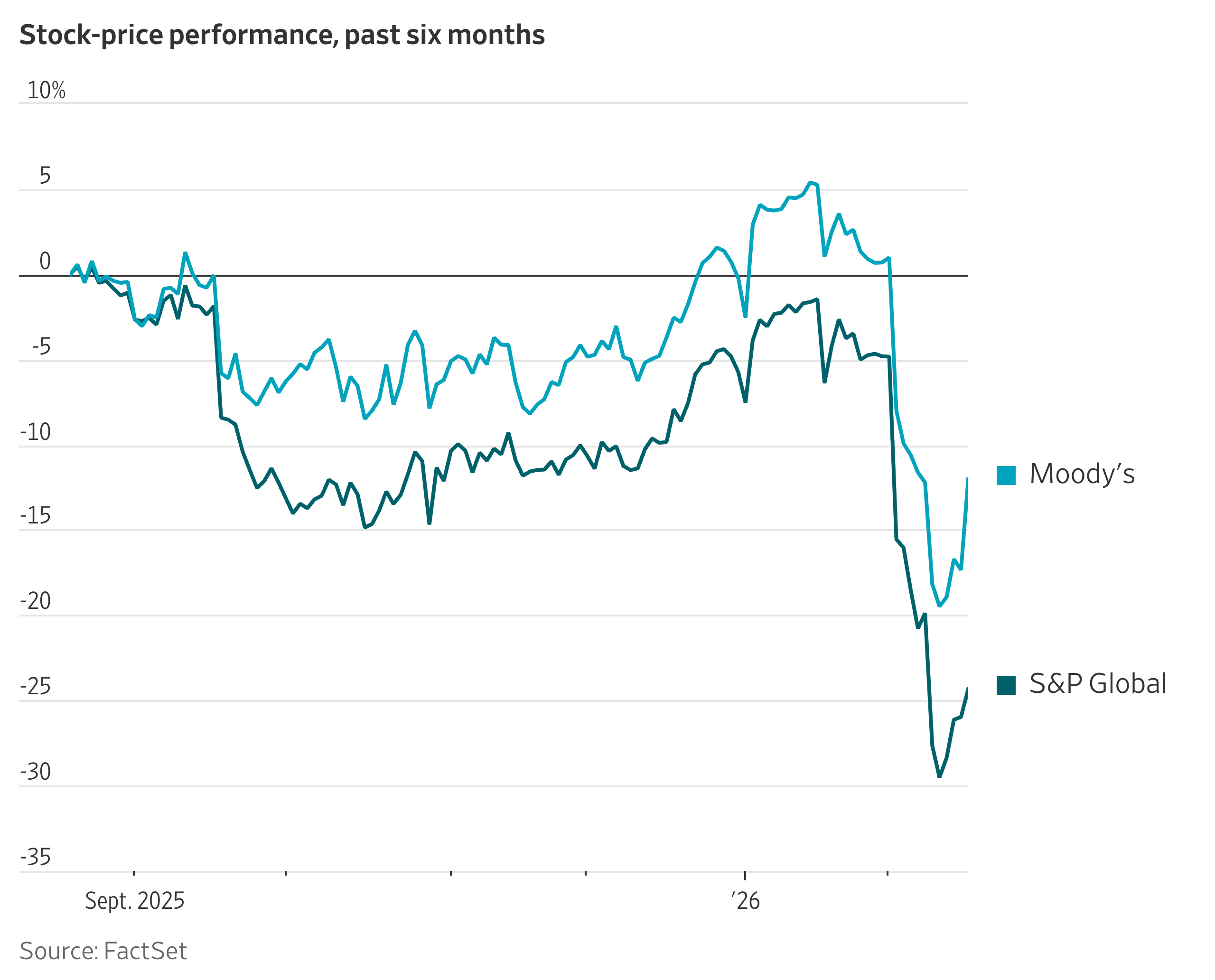

“Our data can’t be synthesized from public sources,” Moody’s Chief Executive Rob Fauber said on an investor call Wednesday.

Fauber fielded questions from analysts about the moats protecting Moody’s businesses. He said the data Moody’s had collected over many years was “both AI-enabling and AI resilient.”

Apurva Sheth, Head of Market Perspectives and Research at Samco Securities, the brokerage that forecast the sharp rally in gold and silver, believes the precious metals bull market is far from over. Despite recent volatility, Sheth expects both metals to hit fresh record highs, backed by structural deficits, strong investment demand and supportive macroeconomic tailwinds.

Samco’s 3-year target for gold is $7,040 while silver can trade anywhere between $140-210.

Edited excerpts from a chat with the market expert on why the gold and silver bull run isn’t over yet:

Samco was among the first to have given bullish calls on silver which has played out very well. Do you think the white metal has topped out and won’t go back above the $100-mark anytime soon?

Advertisement

We were the first ones to call out a bull market in silver back when it was trading around $23/troy ounce. Silver still remains a high conviction idea with a bullish outlook for the long term. The fundamentals of the silver market which drove the prices from $23 to $121 haven’t changed much. Silver is entering its sixth consecutive year of structural deficit due to inelastic by-product supply and surging demand from solar energy and electric vehicles.

Live Events

Despite the sharp correction, silver is still outperforming gold. China has classified silver as a strategic asset, restricting exports and driving Shanghai physical premiums to record highs. Silver prices in Shanghai are still quoting at a premium of around $91 compared to $75 in the US. We believe that recent price dips are strategic buying opportunities for a secular bull market that has not yet peaked. One view in the market is that gold will outperform silver in 2026 and that appears to be playing out as well. What do you think? The gold to silver ratio had dipped to a low of 43 in January 2026. Over the last 12 years the level of 65 has acted as strong support for the ratio. A falling ratio means gold is underperforming silver and vice versa. Over the last 6 months silver was playing catch up with gold as it was massively undervalued compared to gold which was also one of the reasons for being bullish on silver. Now that silver has caught up and probably even went slightly ahead in terms of outperformance, we are seeing a role reversal and gold will take leadership while silver consolidates.Any targets that you have for both gold and silver? Ever since gold broke out above the sideways consolidation in December 2023 we have been talking of these three levels – 2,608, 3335, 4750. These are Fibonacci projections drawn from September 2011 peak to December 2015 bottom in gold. The next extension level that comes after this is $7,040. This is a 3-year target that we are holding for gold. Silver normally trades at 2-3% the price of gold in precious metals bull run. So if gold trades at $7,040 then silver could trade anywhere between $140-210 in the same period.

For many investors, asset allocation is going for a toss as equity is struggling and bullion is leading to FOMO. Would you go on the extent of recommending a 50:50 allocation to precious metals and equity for someone who is moderately aggressive but has a 4-5 year horizon?

It cannot happen that you give a 50:50 allocation to equities and gold once and forget about it for the next 4-5 years. Asset allocation will have to be much more dynamic and tactical depending on the macro developments and the investor’s own risk profile. So for someone with an appetite for risk the allocation goes as high as 50% but it may not be suitable for everyone.

If the de-dollarisation theory, linked to rising US debt level, plays out, then we could be seeing a multi-year bull run in gold. What are the odds of that happening from a macro perspective? US debt currently stands at $39 trillion. According to certain projections, the US is going to add $2.4 trillion in debt each year for the next 10 years. This will push the US debt to $64 trillion by 2036. The US currently spends more than a trillion dollars per year to service this debt. US interest expense and gold price are positively correlated. If the US pays more interest on its debt then naturally it will flood the monetary system with dollars which has been losing its purchasing power over the years.

Advertisement

Richard Nixon took the US dollar off the gold standard on 15 August 1971. Gold prices have grown with a CAGR of 9% since then. If this rate of growth were to continue then gold will trade above $10,000 by 2036.

WGC data shows that central banking buying of gold slowed down in 2025 in volume terms. Is the central bank to gold what FIIs are to Indian largecap stocks? Central banks bought gold to the tune of 1080 tonnes in 2022, 1050 tonnes in 2023, 1092 tonnes in 2024 and 863 tonnes in 2025. There is a drop of 20% in 2025 compared to 2024. Now compare this with investment demand in gold during the same period: 1125 tonnes in 2022, 951 tonnes in 2023, 1185 tonnes in 2024 and 2175 tonnes in 2025. The demand from investment has nearly doubled. So, although buying has slowed down I don’t think this is going to be a major hurdle for gold prices.

What makes you believe that the entire commodity basket, and not just precious metals, will see a supercycle? Help us understand how the rally in gold, silver and even copper for that matter can spill over to impact oil and gas? Gold is the leader of all commodities because it responds first to monetary debasement and inflation expectations. Historically, oil lags gold. In the past reflationary cycles of 1971-80 and 2000-2008 too gold led the rally and oil participated later. The current degree of oil’s underperformance relative to gold is unprecedented, suggesting oil is poised for a massive catch-up phase. We believe that we are in a commodity supercycle which is driven by a shift towards hard assets from soft assets. This cycle transcends precious metals because systematic underinvestment has created structural deficits across the entire commodity basket.

For someone who wants to play the commodity or precious metals boom via the equity route, do you think commodity exchange, gold financers, oil producers and miners can also see significant upside? All of the above are leveraged plays to benefit from the commodity basket. Take gold miners for example. Vaneck Gold Miners ETF tracks the world’s largest gold mining companies. Gold has moved up by 146% since 1st January 2024 but the ETF has moved up by 234% in the same period. So one can definitely ride the commodity supercycle indirectly through the routes you listed above.

Advertisement

Can proxy investing via the equity route beat the returns of owning the commodity itself as operating leverage would be on the side of existing players? Proxy investing through equities can outperform the underlying commodity because miners and producers have operating leverage. A 10% rise in the commodity price can translate into a much larger increase in earnings due to fixed costs. However, equity returns also embed management risk, capital allocation discipline, debt levels, and valuation multiples, which can dilute that advantage.

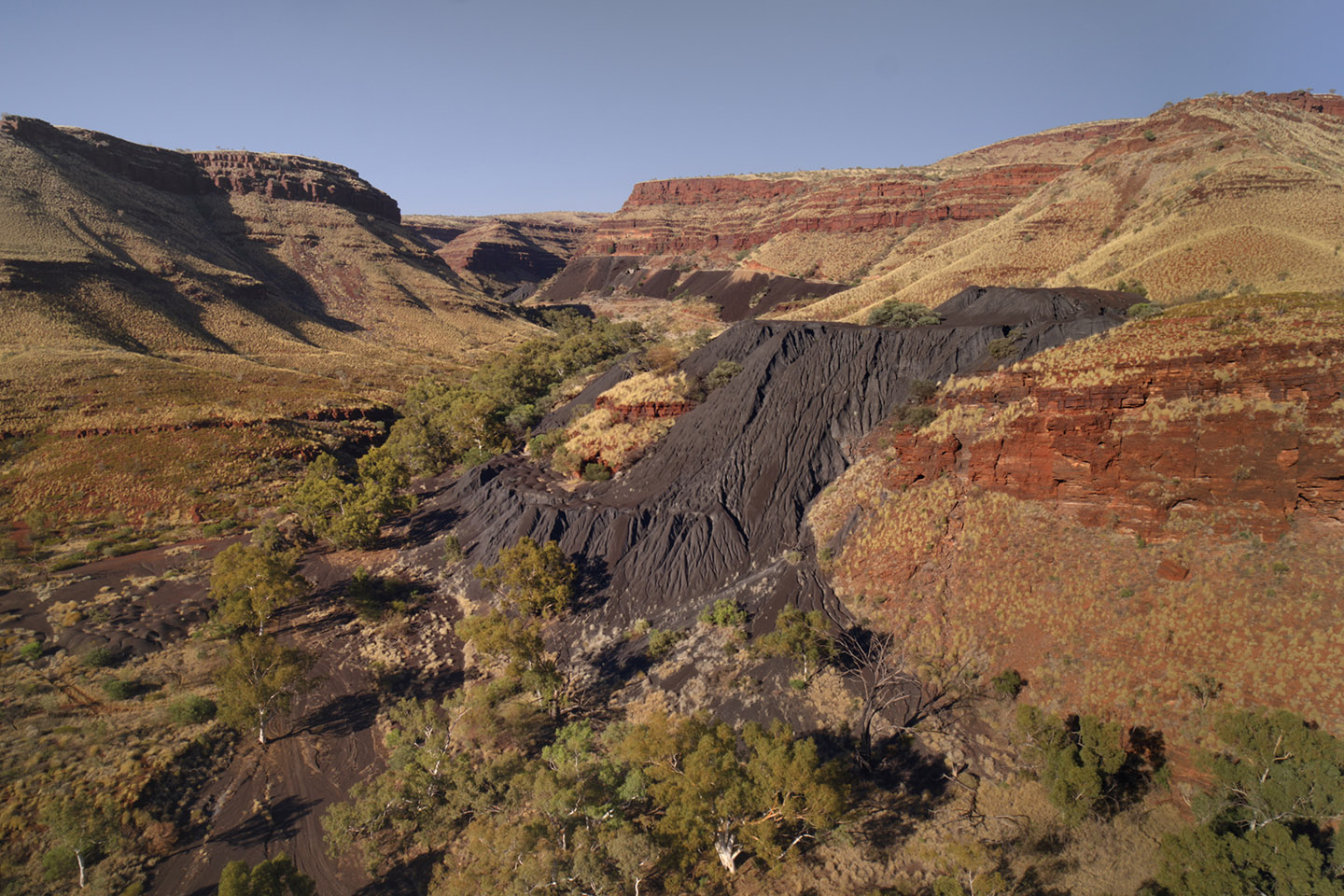

Traditional owners will raise alleged human rights breaches with the United Nations next month as they ramp up a campaign to clean Australia’s most contaminated site.

Formerly known as Prince Andrew, King Charles III’s younger brother was arrested Thursday, which happened to be his 66th birthday.

Trump Reacts to Andrew Mountbatten-Windsor’s Arrest

According to a report by 9News, Trump spoke to reporters about what he thinks about Mountbatten-Windsor’s arrest.

“I think it’s a shame. I think it’s very sad,” Trump told reporters. “I think it’s so bad for the royal family.”

Advertisement

“It’s very, very sad to me,” he added. “It’s a very sad thing when I see that.”

Trump also spoke about King Charles, saying that “It’s a very sad thing to see it and to see what’s going on with his brother, who’s obviously coming to our country very soon, and he’s a fantastic man, the king.”

US Lawmakers Ask ‘Who’s Next?’

When asked if any high-level arrests will be made in America, Trump said that “It’s really interesting, because nobody used to speak about Epstein when he was alive, but now they speak.”

“But I’m the one that can talk about it, because I’ve been totally exonerated,” the US President noted.

Advertisement

However, for some members of the US Congress, it is time to take action against those who have been associated with disgraced pedophile Jeffrey Epstein.

According to a report by the BBC, Republican congressman Thomas Massie declared “Now we need JUSTICE in the United States” in a tweet posted on his X account.

In reaction to the former prince’s arrest, Republican congresswoman Nancy Mace asked, “Who’s next?”

“We will not stop until every co-conspirator, every enabler, and every powerful figure who hid behind wealth and connections is held fully accountable,” she emphasized. “No one is above the law.”