Business

Top 5 flexicap funds with highest risk-adjusted returns. Check details

Danone BN -0.70%decrease; red down pointing triangle projected steady sales growth for the year ahead, with a muted impact from infant-formula recalls, as the French food maker sought to reassure investors that the hit wouldn’t linger for long.

The company behind Aptamil baby milk has been one of the companies affected by a tainted ingredient in its infant formula. Over the past few months, food companies including Danone and Nestle issued warnings or pulled infant nutrition labels off the shelf in more than 60 countries. Danone’s stock has fallen this year amid the recalls.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

When I first heard about “multi-modal input,” it sounded intimidating. Images, videos, audio, text—all working together in a single video generation? I wasn’t sure how that actually worked in practice, or if I even needed all those features.

But once I started experimenting with Seedance 2.0, I realized the multi-modal capability wasn’t a complicated luxury feature; it was actually the simplest way to create better videos.

Let me walk you through my first real project using multi-modal input, and what I learned along the way.

What I Thought Multi-Modal Input Would Be

Before I actually tried it, I had some misconceptions. I imagined it would require technical skill—like some sort of advanced prompt engineering where I’d need to specify exactly how each file interacted with every other file. I thought I’d need to understand the “rules” of combining images with audio, or know the exact syntax for referencing multiple inputs.

The reality was much simpler.

Multi-modal input just means you can throw different types of files at Seedance 2.0 and tell the model what you want it to do with them. That’s it. You’re not switching between different tools or learning a special command language. You’re just giving the model more information to work with.

My First Project: A Short Brand Story Video

I was approached by a local coffee roastery that wanted a 10-second promotional video. They had given me:

- Three high-quality product photographs of their different bean varieties

- A 5-second video clip of someone pouring coffee into a cup (they’d shot it themselves)

- A 3-second audio clip of coffee brewing sounds

- A brief description of the mood they wanted: “warm, inviting, craft-focused”

Normally, I would have had to choose between using the images OR the video OR the audio in post-production. I’d create one asset and try to make it work, leaving other materials unused.

With Seedance 2.0’s multi-modal capability, I could use everything at once.

How I Actually Set It Up

Step One: Gathering the Assets

The coffee roastery gave me three product photos, a pouring video, and brewing sound effects. I organized these before uploading, though honestly, I could have just uploaded them randomly—the point is that Seedance 2.0 can handle all of it simultaneously.

Step Two: Uploading Everything

Seedance 2.0 lets you upload:

- Up to 9 images

- Up to 3 videos (total duration ≤15 seconds)

- Up to 3 audio files (total duration ≤15 seconds)

- Text descriptions of unlimited length

For my project, I uploaded all three product photos, the pouring video, and the brewing audio. The platform accepted everything without complaint.

Step Three: Writing a Natural Language Description

This was the key part that surprised me. I didn’t need to learn special syntax. I just described what I wanted, referencing the files by number or type.

My prompt looked something like this:

“Create a 10-second promotional video. Start with a close-up of @image1 (the espresso beans), with the coffee brewing sounds from @audio1 playing underneath. Transition smoothly to @video1 (the pouring shot), with the warm, crafted aesthetic of @image2 visible in the background. End with a final shot of @image3 (the roasted beans close-up) with the brewing sounds fading out. The overall mood should be warm and inviting, like a specialty coffee shop experience.”

That was it. Natural language. No special operators or complex syntax.

What Happened When I Generated

I honestly wasn’t sure what to expect. Would it use all the files? Would it ignore some of them? Would it misunderstand my descriptions?

The first generation was surprisingly good. The video opened with the espresso beans from my first image, the audio played throughout, and the pouring shot appeared in the middle. The transition between the still image and the video felt natural, not jarring. The final product felt cohesive in a way that would have been really difficult to achieve with traditional video editing.

Was it perfect? No. There were a few things I’d adjust on the second try. But the point is that all my different media assets—photos, video, and audio—came together into a single coherent video without me having to manually edit them together.

Why This Matters for My Workflow

Before understanding multi-modal input, I was used to this process:

- Choose one primary asset (usually video or images)

- Create supplementary graphics or transitions in editing software

- Add audio in post

- Export the final video

It was time-consuming and resulted in a patchwork feel—pieces assembled together rather than something that felt naturally integrated.

With multi-modal input:

- Gather all assets (images, video, audio, description)

- Upload everything to Seedance 2.0

- Describe what I want

- Get a generated video with all elements incorporated

- Make minor tweaks if needed

The second workflow is faster and produces more cohesive results because the model synthesizes everything together from the start, rather than me trying to glue separate pieces together afterward.

Real-World Examples of Multi-Modal Combinations

Since that first project, I’ve experimented with different combinations:

Education Videos

I’ve used reference images of diagrams, a short video clip showing a concept in action, and a voiceover audio track explaining what’s happening. The model generates a video that incorporates the visual information, the dynamic demonstration, and the audio explanation all at once. Students get a more complete learning experience than if I’d just picked one format.

E-Commerce Product Demonstrations

Multiple product photos + a video showing the product in use + background music = a more engaging product video than I could create with any single asset type alone. The images establish what the product looks like, the video shows it functioning, and the audio creates the right emotional tone.

Social Media Clips

For Instagram Reels, I’ve combined a still image of the caption text I want to appear, a short video of motion that fits the content, and upbeat audio. The multi-modal approach ensures all elements appear in the final video without me manually compositing them.

The Learning Curve

Honestly, there wasn’t much of one. The main thing I had to learn was to be more specific about which asset I wanted referenced where. In my first few attempts, I was vague—like, “use the images throughout the video”—and the results were less predictable.

Once I started being explicit—”start with image1, transition to video1, end with image3″—the model understood my intent better. The specificity improved the results significantly.

The other lesson was that quality varies across asset types. My higher-resolution images worked better than low-res ones. My stable video clips worked better than shaky handheld footage. This isn’t surprising, but it’s worth noting: garbage input still produces less impressive output, even with AI.

Limitations I’ve Hit

Multi-modal input is powerful, but it has boundaries. If I upload too many assets and ask the model to incorporate all of them in a short 5-second video, the result feels rushed or cluttered. There’s a reasonable ratio of content to output duration.

Additionally, if the audio I provide has specific timing—like a voiceover with precise pauses—the model doesn’t always match the visual content to those exact timestamps. It’s close, but not frame-perfect. For critical applications like lip-sync, I might need to make adjustments afterward.

Complex interactions between assets can also be unpredictable. If I upload a video where the person is wearing a blue shirt and a photo where they’re wearing red, the model might struggle with consistency. It works better when reference materials are conceptually compatible.

Why I’m Now a Multi-Modal Believer

The practical benefit is this: I can incorporate more creative assets into my videos without doing manual video editing. That means faster turnaround times and more polished final products. It means I can use all the reference material a client gives me, rather than having to choose which piece to prioritize.

For freelancers and small teams, that’s genuinely valuable. It removes a technical bottleneck from the production process.

Moving Forward

I’m still exploring what multi-modal input makes possible. I’ve started experimenting with edge cases—like uploading multiple audio tracks to see how the model combines them, or using reference images and videos that have very different aesthetics to see if the model can synthesize them into something cohesive.

The feature isn’t a magic fix for poor planning or low-quality assets. But if you gather good reference material and think clearly about what you want to create, Seedance 2.0‘s multi-modal capability can genuinely simplify your creative process.

For anyone who’s used to assembling videos from different pieces in post-production, this approach feels like a meaningful step forward. You’re describing your vision once, clearly, and the model generates something that incorporates all your reference materials from the start. That’s the real power of multi-modal input.

Australia’s coastline, stretching more than 25,000 kilometers, boasts some of the world’s most stunning and visited beaches. In 2026, with summer in full swing across the Southern Hemisphere and eco-tourism booming post-pandemic recovery, beaches continue to draw millions of domestic and international visitors. Popularity metrics blend visitor numbers, Tripadvisor reviews, global rankings like the 2026 Travelers’ Choice Awards, and media buzz from outlets including Time Out, Tourism Australia and Nomadasaurus.

Sydney’s urban icons lead in sheer crowds, while remote paradises top beauty lists. Here’s a look at the 10 most popular beaches in Australia this year:

- Bondi Beach, Sydney, New South Wales The undisputed king of Australian beaches, Bondi remains the most visited urban stretch. Iconic for its golden sand, surf culture and the coastal walk to Bronte, it draws crowds year-round. In 2026, Bondi ranks high on global lists and sees heavy foot traffic from tourists snapping photos at the pavilion or enjoying the Icebergs pool. Its accessibility via public transport and vibrant cafe scene keep it perpetually packed.

- Manly Beach, Sydney, New South Wales Often outranking Bondi in recent awards, Manly topped Australia’s entries in the 2026 Tripadvisor Travelers’ Choice (placing ninth worldwide). The ferry ride from Circular Quay adds charm, while the beach offers excellent surfing, family-friendly vibes and a lively Corso promenade with shops and eateries. Its consistent high ratings reflect strong visitor satisfaction.

- Whitehaven Beach, Whitsunday Islands, Queensland Frequently called the world’s best beach, Whitehaven’s 98% pure silica sand and swirling turquoise waters secure its spot as a must-see. Accessible by boat or seaplane from Airlie Beach or Hamilton Island, it tops many 2026 beauty rankings. Hill Inlet lookout provides postcard views, drawing eco-tourists and cruise passengers.

- Cable Beach, Broome, Western Australia Famous for camel rides at sunset, this 22-kilometer red-dirt-meets-white-sand stretch remains a Kimberley highlight. Its remoteness limits crowds, but popularity surges with adventure seekers. In 2026, it’s praised for clear waters and four-wheel-drive access.

- Hyams Beach, Jervis Bay, New South Wales Boasting some of the world’s whitest sand (verified by Guinness), Hyams draws visitors for its crystal waters and dolphin sightings. Part of Booderee National Park, it offers calm swimming and snorkeling, with growing eco-tourism in 2026.

- Wineglass Bay, Freycinet National Park, Tasmania The curved bay framed by pink granite peaks ranks among Australia’s most photographed. A short hike to the lookout rewards with stunning views. In 2026, it’s a top draw for nature lovers seeking seclusion.

- Bells Beach, Torquay, Victoria Surfing mecca and Rip Curl Pro host, Bells attracts wave riders and spectators. Its dramatic cliffs and consistent swells make it legendary, with strong visitor numbers in summer.

- Lucky Bay, Cape Le Grand National Park, Western Australia Turquoise waters, white sand and kangaroos on the shore make Lucky Bay unforgettable. Esperance-area popularity rises with road-trippers seeking Instagram-worthy moments.

- Surfers Paradise Beach, Gold Coast, Queensland The heart of the Gold Coast, this high-rise-lined beach buzzes with tourists, surfers and nightlife. Its accessibility and facilities keep it among the most visited.

- Palm Cove Beach, Cairns, Queensland A relaxed northern gem with calm waters, palm-fringed shores and Great Barrier Reef proximity. It appeals to families and couples, with strong reviews for tranquility.

These beaches reflect Australia’s diversity — urban energy in Sydney, tropical paradise in Queensland, rugged beauty in the west and south. Visitor numbers spike in summer, with eco-concerns prompting sustainable practices like reef-safe sunscreen and park fees.

Whether chasing waves, solitude or sunsets, these shores capture why Australia’s beaches remain a global draw in 2026.

‘XX-XY Athletics’ founder Jennifer Sey on why major brands are backing away from diversity-branded programs.

The second Trump administration has been marked by blowback to diversity, equity and inclusion (DEI) programs across American companies. It’s a welcome change, according to XX-XY Athletics CEO Jennifer Sey, who calls such programs and hiring practices “excessive.”

“Excessive focus on DEI, whether it’s through hiring practices or public marketing, actually can have an adverse effect on [a] company’s performance,” Sey told Fox News Digital.

“It’s not so fashionable anymore… [Companies] are responding to both Trump and the administration and their push and the executive orders, but they’re also responding to the public and where popular opinion is, and people are rejecting these DEI programs,” she continued.

Gravity Research reported in November that “the term ‘DEI’ fell 98% across Fortune 100 communications.” The report analyzed more than 1,000 corporate documents from January 2023 to May 2025.

NIKE’S DIVERSITY INITIATIVES UNDER EEOC SCRUTINY FOR ALLEGED DISCRIMINATION AGAINST WHITE WORKERS

XX-XY Athletics CEO, Jennifer Sey, calls out “excessive” diversity, equity and inclusion (DEI) programs across companies in America that were eliminated under President Trump’s second term. (Christian Alminana/Getty Images / Getty Images)

“Executive teams are happy to abandon these programs. They’re a distraction from the business,” Sey added. “It’s all the training around diversity that people have to go through. It’s the interview process that focuses on anything other than just straight-up merit. It’s a distraction from the business. And at the end of the day, the values that the executive teams and the CEOs do have to make money for the company… That’s their fiduciary responsibility.”

“When they’ve got employees training all day about diversity, they’re not focused on making [a] great product and marketing that product. So, I think [companies are] actually relieved to de-emphasize all of this and walk away from it,” she added.

WENDY’S TO CLOSE HUNDREDS OF RESTAURANTS AS COMPANY LOOKS TO FOCUS ON VALUE TO BOOST SALES

The beginning of the second Trump administration marked the end of diversity, equity and inclusion (DEI) programs across companies in America – a hiring practice that this CEO called out as “excessive.” (Getty Stock Images / Getty Images)

Upon taking office again, President Donald Trump signed executive order 14173, titled “Ending Illegal Discrimination and Restoring Merit-Based Opportunity” – which ordered the heads of all executive departments and agencies to “combat illegal private-sector DEI preferences, mandates, policies, programs, and activities.”

According to Gravity Research, 40 corporations “made public DEI changes” after Trump’s second inauguration, and The Conference Board also found at America’s largest firms, use of the “DEI” acronym dropped by 68% in 2025 compared to 2024 filings.

It was also reported that “33% [of companies] stopped using the term equity altogether,” while “53% of S&P 100 companies” adjusted how DEI efforts were communicated in 2025 annual report filings when compared to 2024.

That didn’t necessarily mean, according to the report, that they were abandoning DEI altogether, but rather “limiting or reframing public disclosures around their diversity initiatives.”

SUPER BOWL ADS GO PATRIOTIC AS BUDWEISER, PEPSI AIM TO WIN BACK AMERICAN CONSUMERS

President Donald Trump pointing at a rally. (Joe Raedle/Getty Images / Getty Images)

The retired gymnast went on to recall the Bud Light marketing failure to use transgender influencer Dylan Mulvaney for an ad campaign in 2023 as an example, citing the company’s attempt to use “wokeness as a marketing strategy.”

“It backfired immensely,” Sey said.

The company has done more traditional, humorous ads in recent years meant to appeal to men, such as its Super Bowl ad this year featuring Peyton Manning, Post Malone and Shane Gillis.

Sey added, “If you want to be woke and that’s who you’re appealing to, that’s fine. Go after it if you think that’s going to satisfy your business goals… If you are going after a much more conservative customer and express that through your marketing and that’s half the country – you can build a successful business on that. But when we’re talking about large brands like Target and Bud Light, I think they do have an obligation to rise to the highest common denominator and focus on the product and unifying values… It shouldn’t just fall prey to cultural whims all the time,” she continued.

TARGET CUTS 500 JOBS, INVESTS MORE MONEY IN STORE STAFFING

A Target employee pulls red shopping carts into a store in New Mexico. (iStock / iStock)

“[People] want optimism, they want unifying, optimistic values expressed in the brands that they’re buying,” the athletic brand builder added.

It’s not complicated, she said, for businesses to simply focus on finding the best employees to “deliver the best results.”

Target and Anheuser-Busch did not respond to Fox News Digital’s request for comment.

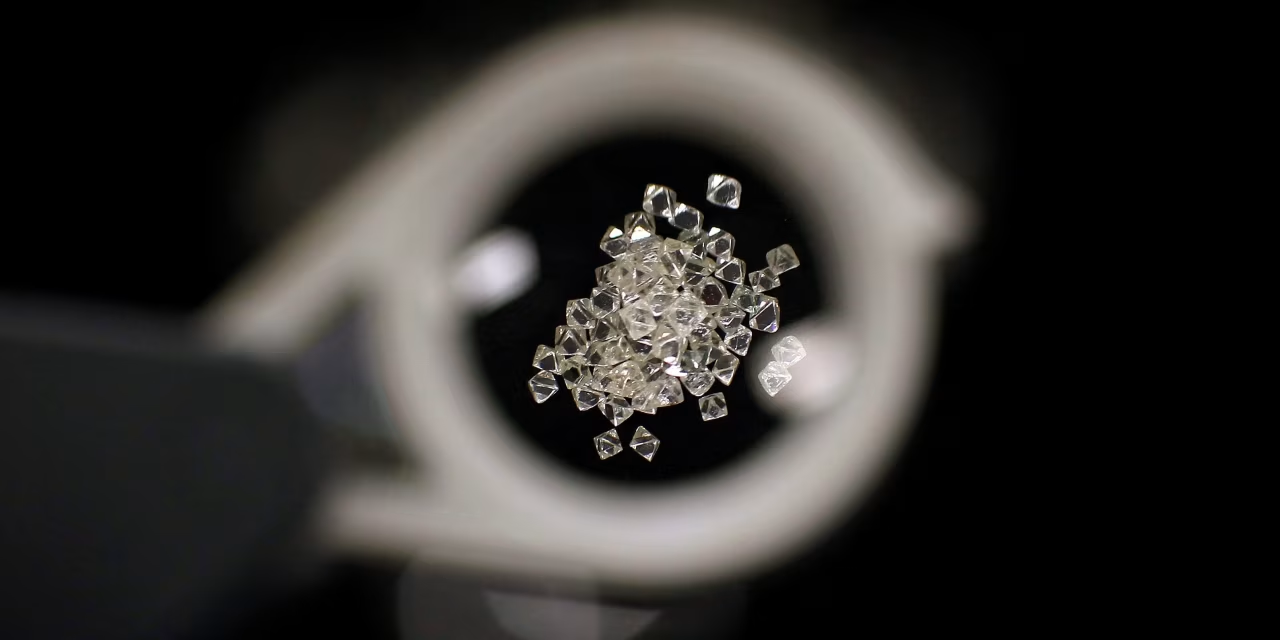

Anglo American AAL 1.09%increase; green up pointing triangle wrote down the value of its De Beers diamond business by $2.3 billion, the third cut in three years, as challenging market conditions complicate plans to dispose of the unit.

The London-listed miner warned earlier this month that it was undertaking a review of the business that could lead to the write-down. For 2025, the unit booked a roughly $500 million underlying earnings loss.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

Australian talent continues to dominate American screens, red carpets and social media feeds in 2026, with actors, musicians and influencers from Down Under ranking among the most recognizable and followed figures in the U.S. entertainment landscape. From blockbuster leads to award contenders and massive online presences, Aussies have solidified their influence in Hollywood and beyond.

Drawing from Instagram follower counts, Golden Globe nominations, AACTA wins, Google search trends and media coverage, here are the 10 most popular Australian celebrities captivating American audiences this year:

1. **Chris Hemsworth**

The Marvel Cinematic Universe star tops lists with his 58.3 million Instagram followers and enduring appeal as Thor. Hemsworth’s fitness brand Centr and family-man image keep him relatable, while recent projects maintain his box-office draw in the U.S.

2. **Margot Robbie**

The Barbie and Wolf of Wall Street alum remains a Hollywood powerhouse, frequently topping “most Googled” and sexiest celebrity rankings. Her production company LuckyChap Entertainment and consistent award buzz cement her as one of the most bankable Australian exports in America.

3. **Nicole Kidman**

With multiple Golden Globe and Oscar nods over the years, Kidman’s work in prestige TV like Big Little Lies and recent films keeps her prominent. Her elegance and longevity make her a staple on U.S. red carpets and in awards conversations.

4. **Hugh Jackman**

The Wolverine icon’s charisma spans Broadway revivals and films like The Greatest Showman. Jackman’s global fanbase and frequent U.S. appearances ensure he ranks high in popularity polls and search interest among Americans.

5. **Troye Sivan**

The singer-songwriter and actor boasts 15.6 million Instagram followers and crossover appeal in music and fashion. His creative direction roles and queer icon status resonate strongly with younger U.S. audiences.

6. **Jacob Elordi**

The Euphoria and Saltburn breakout earned dual Golden Globe nominations in 2026 for supporting and lead roles. His rise from Australian TV to Hollywood heartthrob status has made him a breakout favorite among Gen Z viewers.

7. **Rose Byrne**

Nominated for Best Actress in a Musical or Comedy at the 2026 Golden Globes for If I Had Legs I’d Kick You, Byrne’s comedic timing in films like Bridesmaids and TV roles keep her a beloved figure in American comedy circles.

8. **Rebel Wilson**

The Pitch Perfect star’s vibrant personality and diverse projects, including directing and producing, maintain her visibility. Her social media presence and body-positivity advocacy contribute to strong U.S. popularity.

9. **Sarah Snook**

The Succession alum received the AACTA Trailblazer Award in 2026 and remains a critical darling for her nuanced performances. Her work in limited series and films draws consistent praise and attention in the U.S.

10. **Liam Hemsworth**

Chris’s brother stays relevant through high-profile relationships, modeling and acting gigs. His presence at events like the Australian Open 2026 and ongoing Hollywood projects keep him in the public eye.

These celebrities reflect Australia’s outsized impact on American pop culture. Actors dominate due to Hollywood’s global reach, while musicians and influencers leverage social media for massive followings. Recent events like the 2026 Golden Globes (with multiple Aussie nominees) and AACTA Awards highlighted their ongoing success.

Rising stars like Yerin Ha, Lila McGuire and others signal even more Australian talent on the horizon. As U.S. audiences embrace diverse voices, Aussies’ blend of charm, talent and work ethic ensures their popularity endures.

Major League Soccer kicks off its 2026 campaign with a blockbuster matchup as Los Angeles FC welcomes defending MLS Cup champions Inter Miami CF to the iconic Los Angeles Memorial Coliseum on Saturday, February 21, at 6:30 p.m. PT (9:30 p.m. ET).

![]()

The game, billed as the Walmart Saturday Showdown and streamed exclusively on Apple TV, marks LAFC’s ninth MLS regular-season opener and the league’s first match of the year. Instead of their usual home at BMO Stadium (capacity 22,000), LAFC opted for the historic 102-year-old Coliseum, expecting a crowd exceeding 60,000 — potentially setting a new record for the largest attendance in an MLS season opener.

Inter Miami, fresh off lifting the MLS Cup in December 2025, travels west to defend its title against a formidable LAFC side that has amassed more goals, wins and points than any other MLS club over the past eight seasons. The matchup features two of the league’s biggest stars: Lionel Messi for Inter Miami and new LAFC signing Son Heung-min, the South Korean forward who joined from Tottenham Hotspur and has generated massive excitement in Los Angeles’ large Korean community.

Messi, the Inter Miami captain, was confirmed available by coach Javier Mascherano, setting up a highly anticipated clash between the eight-time Ballon d’Or winner and Son, a Premier League Golden Boot winner known for his pace, finishing and leadership. The game represents the first time the two most expensive players in MLS history face off, adding extra intrigue to an already star-studded contest.

LAFC enters the season with momentum after a strong preseason and a dominant 6-1 Concacaf Champions Cup win over Real España in Honduras earlier this week. Coach Steve Cherundolo’s squad boasts attacking depth with Denis Bouanga (26 goals in recent seasons), Olivier Giroud and others, complemented by Son’s arrival to bolster the front line. The Black & Gold hold an unbeaten record in MLS season openers (8W-0L-0D), a league mark they aim to extend.

Inter Miami, under Mascherano, brings championship pedigree and firepower led by Messi, Luis Suárez, Jordi Alba and Sergio Busquets. The Herons’ title defense begins on the road in a hostile environment, testing their ability to handle high expectations and travel early in the campaign.

The venue shift to the Coliseum — site of two Summer Olympics and countless historic events — promises an electric atmosphere. An estimated 60,000+ fans will pack the stands, far surpassing typical MLS crowds and underscoring the growing popularity of the league. The game also highlights MLS’s push for marquee matchups in iconic venues to boost visibility.

Pre-match buzz focused on tactical battles: LAFC’s high-pressing style against Inter Miami’s possession-based play, and individual duels like Messi vs. LAFC’s midfield and Son exploiting spaces. Predictions vary, with some analysts favoring LAFC’s home advantage and depth, while others see Inter Miami’s experience carrying them to a statement win.

The contest airs globally on Apple TV, with additional broadcasts in Korea via Coupang Play and SpoTV. Tickets sold briskly since going on sale in December 2025, with priority for season members and groups.

As MLS enters its 31st season, this opener sets the tone for a year of expansion, star power and competitive balance. LAFC seeks to reclaim supremacy in the West, while Inter Miami aims to prove its championship was no fluke.

Kickoff at the Coliseum promises drama, goals and a fitting start to what could be one of MLS’s most exciting campaigns yet. Fans worldwide tune in for what could be a classic from the opening whistle.

MILAN, Italy — The stage is set for one of the most anticipated matchups in international hockey history: the United States faces Canada in the men’s ice hockey gold medal game at the Milano Cortina 2026 Winter Olympics on Sunday, February 22, at Milano Santagiulia Ice Hockey Arena.

Puck drop is scheduled for 2:10 p.m. CET (8:10 a.m. ET / 5:10 a.m. PT), with broadcast coverage on NBC in the United States, Peacock streaming, CBC and Sportsnet in Canada, and international feeds via Olympic channels. The game caps a tournament that marked the return of NHL players to the Olympics for the first time since Sochi 2014, delivering star-studded rosters and high-stakes drama.

Both teams enter undefeated, with Canada (5-0) and the United States (5-0) cruising through their paths to the final. The Americans advanced with a commanding 6-2 semifinal victory over Slovakia on Friday, powered by two goals from Jack Hughes (New Jersey Devils) and three assists from Zach Werenski (Columbus Blue Jackets). Goaltender Connor Hellebuyck (Winnipeg Jets) was solid, allowing just two goals in a dominant performance that showcased U.S. depth and speed.

Canada secured its spot earlier Friday with a thrilling 3-2 comeback win over Finland, overcoming a two-goal deficit in a tense semifinal. Nathan MacKinnon’s late heroics and strong goaltending sealed the victory, highlighting the Canadians’ resilience and firepower.

This gold medal showdown revives one of sport’s fiercest rivalries. Canada has dominated the all-time Olympic series against the U.S., winning 15 of 19 meetings, including gold medal victories in 2002 (5-2 in Salt Lake City) and 2010 (3-2 in overtime in Vancouver on Sidney Crosby’s iconic “golden goal”). The U.S. seeks its first men’s hockey gold since the “Miracle on Ice” triumph in 1980 at Lake Placid and its first against Canada in a gold medal game.

The buildup intensified last year during the 2025 4 Nations Face-Off, the first best-on-best international tournament since 2016. The teams split their meetings: the U.S. won a 3-1 round-robin game in Montreal amid a politically charged atmosphere, but Canada claimed the championship with a 3-2 overtime victory in Boston on Connor McDavid’s heroics. That final drew massive viewership and set the tone for this rematch.

Rosters feature NHL superstars on both sides. Canada boasts McDavid (Edmonton Oilers), MacKinnon (Colorado Avalanche), Cale Makar (Avalanche), Auston Matthews (Toronto Maple Leafs), and emerging talent Macklin Celebrini. The lineup emphasizes speed, skill and depth, with strong defensive play and goaltending.

The United States counters with Jack Hughes, Quinn Hughes (Vancouver Canucks), Jack Eichel (Vegas Golden Knights), Dylan Larkin (Detroit Red Wings) and Hellebuyck. The Americans have leaned on offensive explosiveness and transition play, overwhelming opponents in key moments.

Betting odds reflect a near pick’em: Canada is a slight favorite at -111 to -118 on the moneyline, with the U.S. at -102 to -108. The puck line sits at Canada -1.5 (+205) and U.S. +1.5 (-265), while the over/under is 5.5 goals (over +134, under -164). Analysts predict a physical, low-scoring affair early, with potential for late drama given both teams’ come-from-behind abilities.

Key storylines abound: Can the U.S. end Canada’s Olympic dominance and claim its first gold in 46 years? Will McDavid add another signature moment? How will political undertones from recent years influence the atmosphere?

The game holds massive stakes beyond medals. A U.S. win would mark a breakthrough in a rivalry where Canada has long held bragging rights as hockey’s birthplace. For Canada, victory would extend its record to 10 Olympic golds in men’s hockey.

Fans worldwide anticipate a battle of skill, speed and grit. The Santagiulia Arena promises an electric crowd, with global viewership expected to soar.

As the final event of the Milano Cortina Games, this USA-Canada clash delivers the pinnacle of Olympic hockey — a rematch fans have craved since the 4 Nations Face-Off and a fitting conclusion to a star-powered tournament.

New home sales dropped 1.7% to a seasonally adjusted annualized rate of 745,000 units, the Commerce Department’s Census Bureau said on Friday. Sales increased to a rate of 758,000 units in November from 656,000 in October. The data was delayed by last year’s shutdown of the government.

New home sales account for a small share of U.S. home sales and tend to be volatile on a month-to-month basis. They are counted at the signing of a contract. New home sales advanced 3.8% on a year-over-year basis in December.

New housing inventory fell to 472,000 units in December from 485,000 units in November. The inventory of homes under construction was the lowest in nearly 4-1/2 years. At December’s sales pace, it would take 7.6 months to clear the supply of new houses on the market, down from 7.7 months in November.

The median new house price increased 4.2% to $414,400 in December from a year earlier.

The housing market could get a lift from mortgage rates. The average rate on the popular 30-year fixed-rate mortgage declined to 6.01% this week, the lowest level since September 2022, from 6.09% last week, data from mortgage finance agency Freddie Mac showed.

The stud continues but a visitor centre and cafe closes as the rare-breed centre takes stock.

Top 25 roundup: No. 18 Saint Louis bounces back with win over VCU

Winter Olympics 2026: When is USA and Canada men’s ice hockey final?

Danone Forecasts Steady Sales Growth, Limited Hit From Infant-Formula Recalls

-

Video5 days ago

Video5 days agoBitcoin: We’re Entering The Most Dangerous Phase

-

Tech6 days ago

Tech6 days agoLuxman Enters Its Second Century with the D-100 SACD Player and L-100 Integrated Amplifier

-

Crypto World4 days ago

Crypto World4 days agoCan XRP Price Successfully Register a 33% Breakout Past $2?

-

Sports4 days ago

Sports4 days agoGB's semi-final hopes hang by thread after loss to Switzerland

-

Fashion17 hours ago

Fashion17 hours agoWeekend Open Thread: Boden – Corporette.com

-

Video1 day ago

Video1 day agoXRP News: XRP Just Entered a New Phase (Almost Nobody Noticed)

-

Tech4 days ago

Tech4 days agoThe Music Industry Enters Its Less-Is-More Era

-

Business3 days ago

Business3 days agoInfosys Limited (INFY) Discusses Tech Transitions and the Unique Aspects of the AI Era Transcript

-

Entertainment3 days ago

Entertainment3 days agoKunal Nayyar’s Secret Acts Of Kindness Sparks Online Discussion

-

Video4 days ago

Video4 days agoFinancial Statement Analysis | Complete Chapter Revision in 10 Minutes | Class 12 Board exam 2026

-

Tech3 days ago

Tech3 days agoRetro Rover: LT6502 Laptop Packs 8-Bit Power On The Go

-

Sports2 days ago

Sports2 days agoClearing the boundary, crossing into history: J&K end 67-year wait, enter maiden Ranji Trophy final | Cricket News

-

Entertainment3 days ago

Entertainment3 days agoDolores Catania Blasts Rob Rausch For Turning On ‘Housewives’ On ‘Traitors’

-

Business3 days ago

Business3 days agoTesla avoids California suspension after ending ‘autopilot’ marketing

-

NewsBeat6 days ago

NewsBeat6 days agoThe strange Cambridgeshire cemetery that forbade church rectors from entering

-

Crypto World3 days ago

Crypto World3 days agoWLFI Crypto Surges Toward $0.12 as Whale Buys $2.75M Before Trump-Linked Forum

-

Politics4 days ago

Politics4 days agoEurovision Announces UK Act For 2026 Song Contest

-

NewsBeat6 days ago

NewsBeat6 days agoMan dies after entering floodwater during police pursuit

-

Crypto World2 days ago

Crypto World2 days ago83% of Altcoins Enter Bear Trend as Liquidity Crunch Tightens Grip on Crypto Market

-

NewsBeat7 days ago

NewsBeat7 days agoUK construction company enters administration, records show